North America Sodium Bicarbonate Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

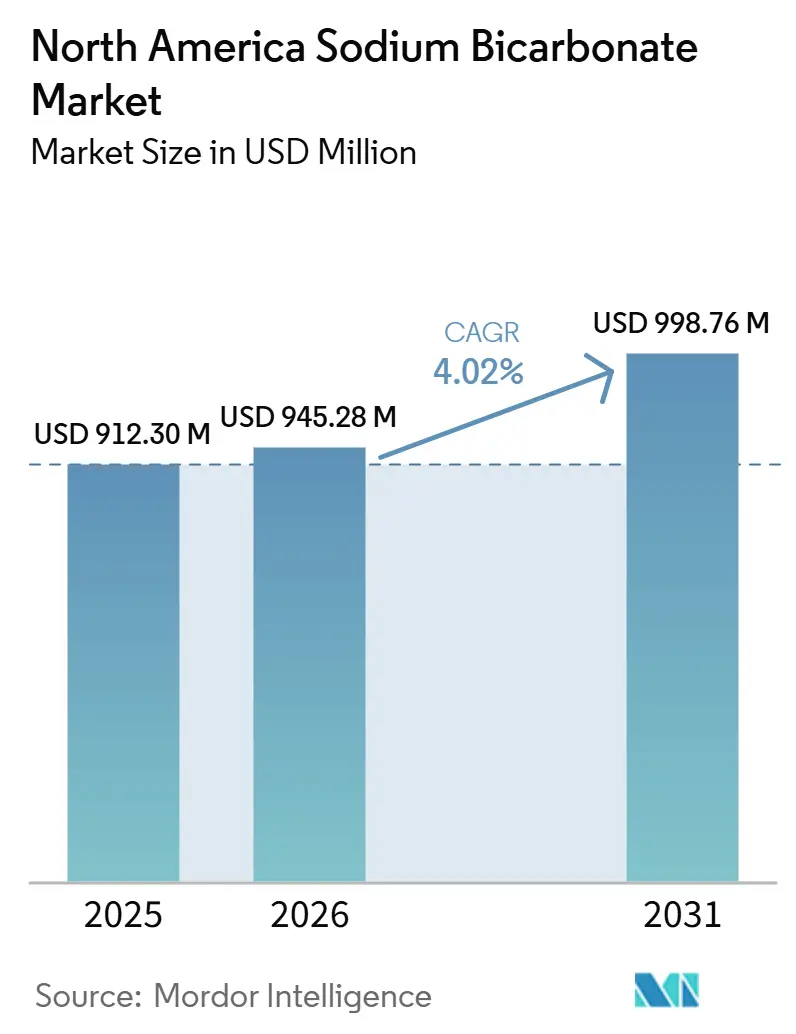

| Base Year Market Size (2025) | USD 912.30 Million |

| Market Size (2026) | USD 945.28 Million |

| Market Size (2031) | USD 998.76 Million |

| Growth Rate (2026 - 2031) | 4.02% CAGR |

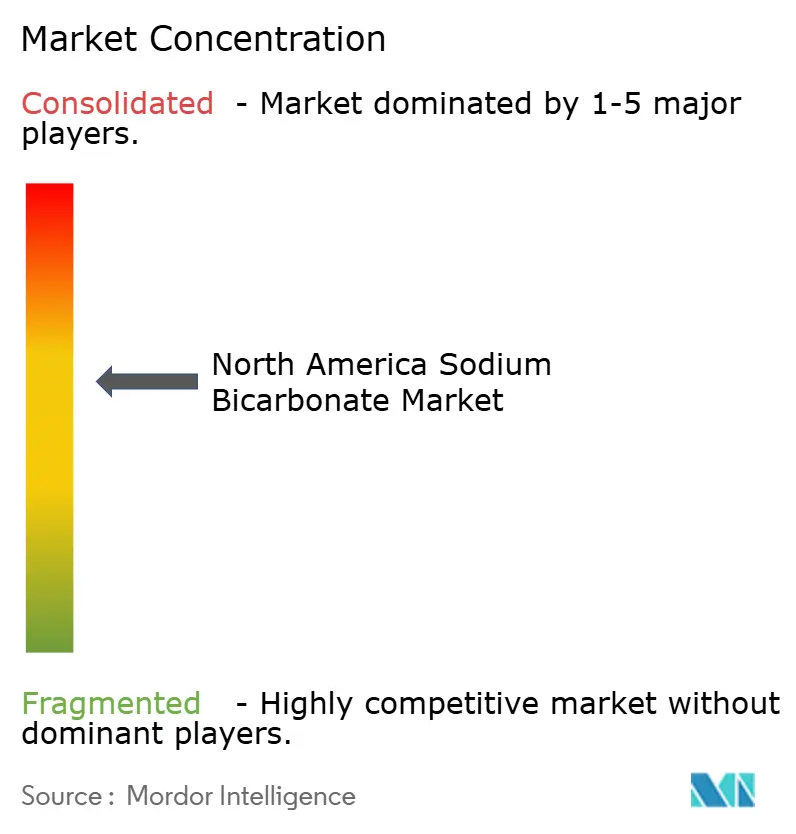

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Sodium Bicarbonate Market Analysis by Mordor Intelligence

The North America sodium bicarbonate market size is projected to expand from USD 912.30 million in 2025 and USD 945.28 million in 2026 to USD 1.15 billion by 2031, registering a CAGR of 4.02% from 2026 to 2031. The North America sodium bicarbonate market continues to benefit from demand that is spread across food manufacturing, pharmaceutical use, animal nutrition, cleaning products, and industrial emissions control, which keeps the business base relatively stable even when one end use slows. A large part of that resilience comes from the United States resource base, where Wyoming trona deposits support a cost position that strengthens the North America sodium bicarbonate market against producers that depend on more energy-intensive synthetic routes. Clean label reformulation in food, steady dialysis-related demand in healthcare, and wider use in flue gas treatment are also keeping the North America sodium bicarbonate market tied to applications where performance and regulatory acceptance matter as much as price[1]Source: National Institute of Diabetes and Digestive and Kidney Diseases, “Kidney Disease Statistics for the United States,” niddk.nih.gov. The competitive picture in the North America sodium bicarbonate market is becoming tighter as scale, purification capability, and compliance documentation increasingly shape who can supply higher value grades, while acquisitions and capacity investments continue to strengthen the position of large integrated producers. That combination leaves the North America sodium bicarbonate market with room for growth in high purity, liquid, and compliance driven uses, even as cost pressure and utility exposure continue to shape investment choices at the producer level.

Key Report Takeaways

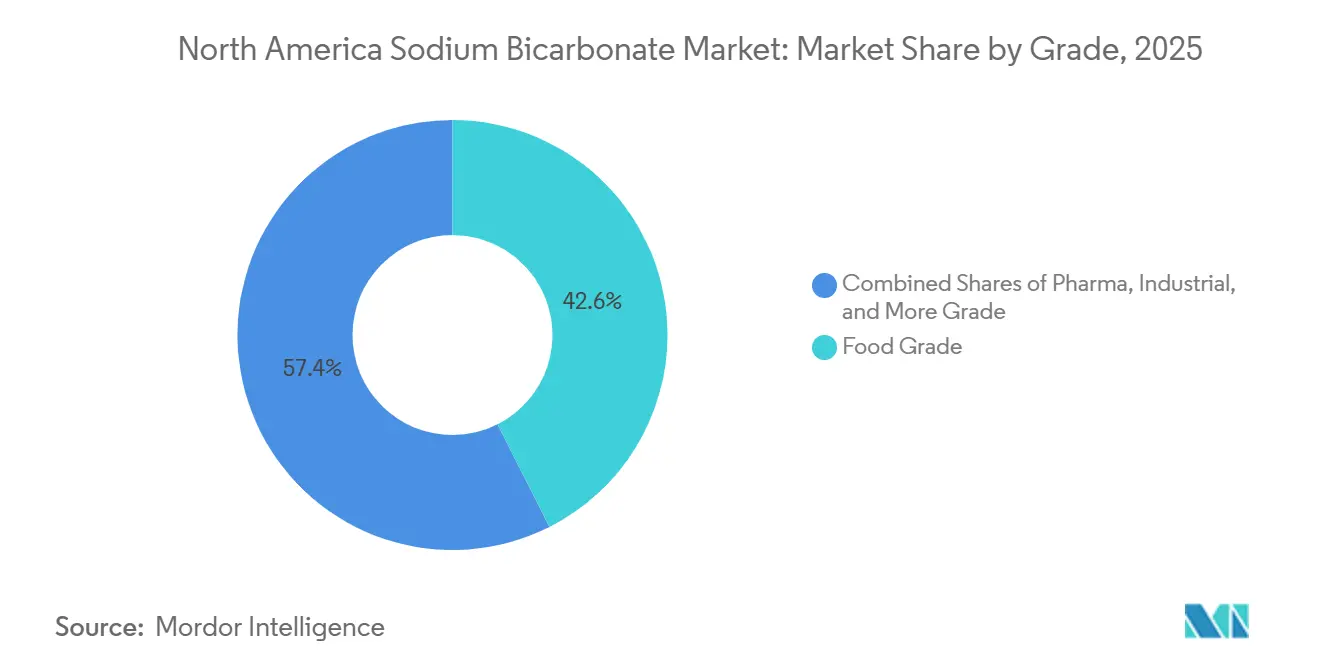

- By grade, food grade led with a 42.56% share in 2025, while pharma grade is forecast to expand at a 5.02% CAGR through 2031.

- By form, powder held a 65.48% share in 2025, while liquid recorded the highest projected CAGR at 5.11% through 2031.

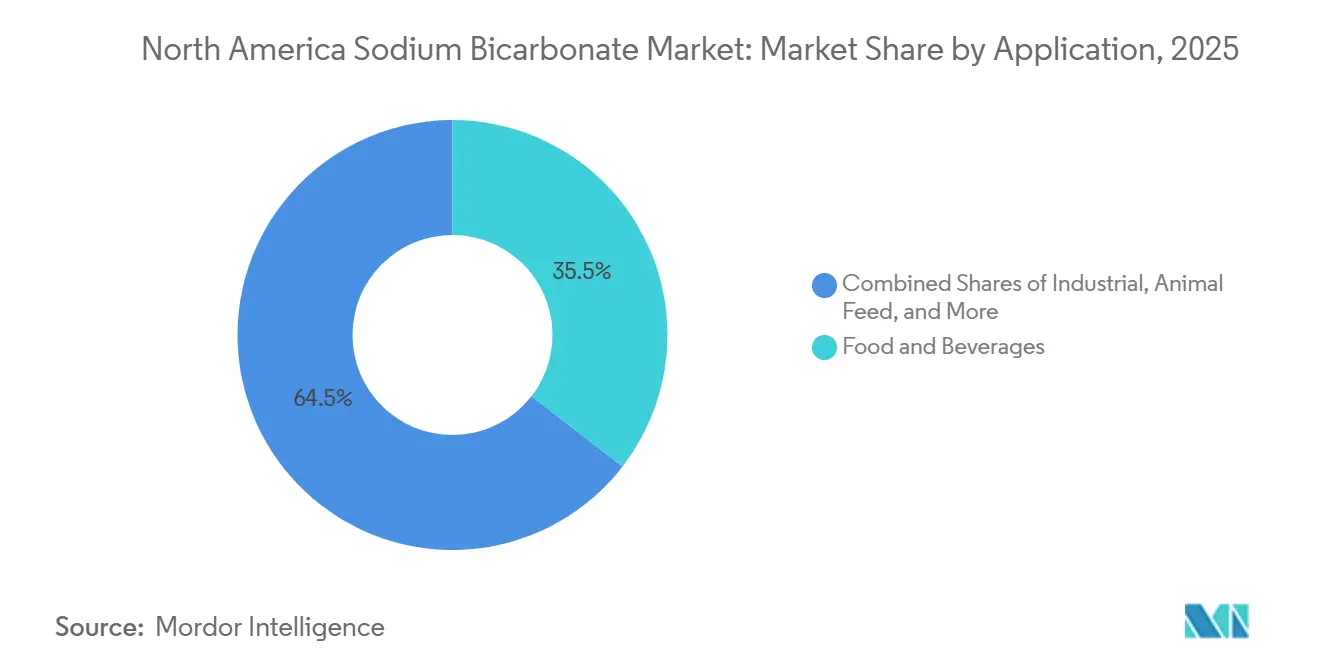

- By application, food and beverages accounted for a 35.48% share in 2025, while industrial is advancing at a 5.34% CAGR through 2031.

- By geography, the United States held a 40.23% share in 2025, while Canada is forecast to grow at a 5.74% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Sodium Bicarbonate Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strong Demand from the Food and Beverage Industry | +1.2% | United States & Canada | Medium term (2–4 years) |

| Expanding Flue Gas Treatment Adoption in Industrial Emissions Control | +0.8% | United States (primary), Canada | Medium term (2–4 years) |

| Higher Consumption in Hemodialysis and Antacid Formulations | +0.6% | United States (primary) | Long term (≥ 4 years) |

| Abundant Natural Soda Ash Resources in the United States | +0.5% | United States | Long term (≥ 4 years) |

| Growing Demand for Eco-Friendly Cleaning Products | +0.3% | United States & Canada | Short term (≤ 2 years) |

| Increasing Industrial Research and Development and Product Innovation | +0.2% | United States | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Strong Demand From The Food And Beverage Industry

The food and beverage sector remains the largest base of demand for the North America sodium bicarbonate market, but the composition of that demand is shifting toward higher purity and more tightly specified supply. Food manufacturers continue to use sodium bicarbonate across bakery, dairy, and packaged food formulations, and the material keeps a strong position because formulators already know its functionality and handling profile. The North America sodium bicarbonate market is also benefiting from adjacent consumer product demand, as Church and Dwight announced the 2026 launch of ARM and HAMMER Fresh Laundry Detergent with 10x more baking soda, which shows how product development continues to widen commercial use around established baking soda familiarity. Church and Dwight also reported that sodium bicarbonate and animal nutrition businesses were key contributors to its 2025 performance, which supports the view that demand is not limited to one narrow food subsegment. FDA acceptance and established food use continue to support the North America sodium bicarbonate market, where manufacturers want familiar ingredients that fit clean label reformulation paths. That keeps value creation centered less on tonnage growth alone and more on reliable delivery of food compliant grades.

Expanding Flue Gas Treatment Adoption In Industrial Emissions Control

Industrial emissions control is adding a durable demand layer to the North America sodium bicarbonate market because many installations buy on compliance need rather than discretionary preference. The US Environmental Protection Agency continued to shape this application through combustion and incineration rules that govern acid gas and related emissions across multiple industrial sources[2]Source: U.S. Environmental Protection Agency, “Air Emissions from Combustion and Incineration Processes,” govinfo.gov. That regulatory framework supports dry sorbent injection demand, especially where operators need strong acid gas removal with manageable residue volumes and dependable material handling. The North America sodium bicarbonate market also gains from the fact that industrial-grade supply can be supported by the same regional production base that serves other end uses, which helps reduce procurement friction when compliance schedules tighten. This matters because emissions control buying patterns often move in waves as plants retrofit or upgrade, and the presence of nearby supply improves readiness. As a result, industrial applications give the North America sodium bicarbonate market a more balanced demand mix that does not depend only on food or healthcare volumes.

Higher Consumption In Hemodialysis And Antacid Formulations

Pharmaceutical demand remains one of the clearest higher-value growth pockets in the North America sodium bicarbonate market because it is tied to healthcare needs and strict product quality expectations. The United States continues to have a large chronic kidney disease burden, with 35.5 million Americans living with chronic kidney disease and 131,000 new patients beginning dialysis annually, which sustains the need for bicarbonate-based renal care inputs. CMS also projected a 2.2% increase in total ESRD facility payments for calendar year 2026, which points to continued activity across dialysis services that depend on stable supply chains[3]Source: Centers for Medicare & Medicaid Services, “Calendar Year 2026 End-Stage Renal Disease Prospective Payment System Final Rule,” cms.gov. In the North America sodium bicarbonate market, this creates a demand stream that is less cyclical than many industrial categories because patient treatment volumes continue regardless of broader economic conditions. Antacid formulations add another steady outlet, and together these uses support the premium for suppliers that can meet pharmaceutical documentation and purity expectations. The result is that healthcare demand lifts both the value mix and the entry barrier profile of the North America sodium bicarbonate market.

Abundant Natural Soda Ash Resources In The United States

Resource availability remains one of the strongest structural supports for the North America sodium bicarbonate market because regional production is tied to a deep and established trona base. Wyoming Energy Authority states that Wyoming trona deposits are estimated at 127 billion tons, which gives producers in the region a long runway for feedstock availability. That resource advantage matters because it supports vertically integrated production chains and helps the North America sodium bicarbonate market maintain stronger supply security than regions that depend more heavily on synthetic routes or imported feedstock. It also supports investment confidence across logistics, terminals, and mine linked infrastructure. The North America sodium bicarbonate market benefits further when new resource projects and ownership consolidation improve the ability of large operators to align mine output, export capability, and derivative chemical supply. Over time, that supply structure strengthens cost visibility and helps the region serve both domestic users and export linked production networks.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Soda Ash Price Volatility And Conversion Economics | -0.50% | United States and Canada | Short term (≤ 2 years) |

| Rising Energy Water And Utility Expenses | -0.40% | United States | Medium term (2-4 years) |

| Competition From Alternative Neutralizing And Sorbent Inputs | -0.30% | United States | Medium term (2-4 years) |

| Stringent Quality And Traceability Requirements | -0.20% | United States and Canada | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Soda Ash Price Volatility And Energy Intensive Conversion Economics

Even with strong trona access, the North America sodium bicarbonate market still faces exposure to feedstock and conversion economics because sodium bicarbonate production remains tied to soda ash availability and processing cost. Producers that are fully integrated have a clearer buffer, but participants that rely more on purchased input remain more exposed to shifts in procurement conditions. In the North America sodium bicarbonate market, this difference can widen the performance gap between large upstream linked suppliers and smaller conversion focused operators. Cost swings also complicate downstream pricing because food, pharma, and industrial buyers do not always absorb increases at the same pace. That pressure becomes more pronounced in applications where sodium bicarbonate competes with lower complexity alternatives. As a result, conversion economics remain a practical restraint on how quickly less integrated participants can scale.

Increasing Energy, Water, And Utility Expenses In Sodium Bicarbonate Manufacturing

Utility cost pressure remains a real operating issue for the North American sodium bicarbonate market because mining, processing, purification, and handling all carry meaningful energy and water needs. Wyoming Public Media reported that Tata Chemicals’ Green River facility draws 32 megawatts of continuous power and is deploying 8 nuclear microreactors to replace fossil fuel-based power generation, which shows how significant long-run utility management has become for major producers. Water constraints in the Green River Basin also keep resource use under scrutiny, which matters because the North American sodium bicarbonate market depends heavily on this production corridor. These cost factors are especially important in high purity production, where purification and wastewater management add another layer of operating expense. Participants with scale and capital can respond through technology and infrastructure upgrades, but smaller operators have less room to absorb those investments. That makes utilities a restraint that tends to reinforce concentration over time.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Grade: Pharma Grade Outpacing The Market’s Dominant Food Segment

Food grade held 42.56% of the North America sodium bicarbonate market share in 2025, which kept it as the largest grade in the region. That leadership reflects broad use across bakery, dairy, and packaged food manufacturing, where sodium bicarbonate remains a standard and familiar functional ingredient. The North America sodium bicarbonate market also continues to draw stable support from industrial and feed grades, with industrial grade tied to emissions control and water treatment and feed grade tied to dairy and beef nutrition. This mix reduces dependence on any one end market and helps the grade structure of the North America sodium bicarbonate market stay balanced. It also means that food grade leadership rests on both volume depth and wide customer reach.

Pharma grade is projected to grow at a 5.02% CAGR through 2031, which makes it the fastest expanding grade in the North America sodium bicarbonate market. Growth is tied to hemodialysis concentrate demand and antacid-related use, both of which benefit from the scale of the United States renal care base. The North America sodium bicarbonate industry therefore shows a clear split between its largest grade by volume and its fastest grade by value-linked growth. That distinction matters because pharma supply depends more on documentation, purity assurance, and validated systems than on bulk scale alone. In the North America sodium bicarbonate market, suppliers that already meet these standards hold an advantage that is difficult to narrow quickly.

By Form: Powder Dominates, But Liquid Is Gaining Relevance In Precision Uses

Powder accounted for 65.48% of the North America sodium bicarbonate market size in 2025, which made it the dominant form across the region. That position is supported by straightforward storage, bulk handling efficiency, and compatibility with food production, animal feed, and large industrial systems. Powder also fits the logistics patterns of the North America sodium bicarbonate market because many large volume buyers already use handling systems built around dry material movement. Crystal and pallet forms remain more specialized, serving industrial cleaning and related uses where particle profile and application method matter. This keeps form demand broad, but clearly led by powder.

Liquid is forecast to grow at a 5.11% CAGR through 2031, which makes it the fastest-expanding form in the North America sodium bicarbonate market. The main drivers are pharmaceutical compounding and water treatment, where pre-dissolved material can simplify dosing and reduce transfer-related contamination risk. The North America sodium bicarbonate market is also seeing liquid gain relevance in dialysis-related settings because precision and preparation control matter more in those applications than simple bulk transport. This means liquid growth is linked less to mass volume and more to tighter use conditions and higher service expectations. That pattern mirrors the wider shift in the North America sodium bicarbonate market toward more credential based and application specific value pools.

By Application: Industrial Is The Fastest Growing Pocket While Food And Beverages Stays Largest

Food and beverages represented 35.48% of the North America sodium bicarbonate market size in 2025, keeping this as the largest application segment. Demand remains broad across bakery, carbonated beverages, and dairy processing, where sodium bicarbonate holds an established role and benefits from consistent purchasing patterns. Pharmaceuticals and animal feed form the next important application clusters in the North America sodium bicarbonate market, with healthcare tied to dialysis and antacid use and feed tied to ruminal buffering in dairy and beef systems. Water treatment adds a smaller but growing outlet through pH correction and alkalinity control in municipal and industrial systems. Together, these applications give the North America sodium bicarbonate market a diverse end-use base.

Industrial is projected to expand at a 5.34% CAGR through 2031, which places it as the fastest-growing application in the North America sodium bicarbonate market. Growth is linked mainly to dry sorbent injection in utilities, waste-to-energy plants, and other combustion-linked operations under tightening emissions rules. The segment also includes specialty cleaning and process uses where bicarbonate is valued for being non toxic and biodegradable in comparison with harsher alternatives. Church and Dwight’s efforts to broaden ARM and HAMMER across laundry, cleaning, and oral care further show that commercial applications continue to stretch beyond the most traditional use categories. This leaves the North America sodium bicarbonate industry with one application segment that anchors current share and another that is setting the pace for future expansion.

Geography Analysis

The United States held 40.23% of the North America sodium bicarbonate market share in 2025, which kept it as the clear regional leader. That position comes from resource depth, integrated production, and broad demand across food, healthcare, animal feed, and industrial emissions control. Wyoming remains central to the North America sodium bicarbonate market because its trona base underpins feedstock security and supports large-scale processing. The United States also continues to attract logistics and infrastructure investment that supports the North America sodium bicarbonate market well beyond basic mine output. OmniTRAX was appointed exclusive switching partner for Tata Chemical Soda Ash Partners’ Wyoming mine in August 2025 with projected annual rail movement of 2.7 million tons, which highlights the scale of supporting transport activity.

The United States' position is reinforced by investments that improve both export access and downstream supply flexibility. Solvay and the Port of Vancouver USA broke ground in May 2025 on a soda ash export terminal in Washington State, which supports broader soda ash logistics linked to the North American sodium bicarbonate market. Tata Chemicals’ move toward nuclear microreactors at Green River also shows that major operators are treating power strategy as part of long term competitiveness rather than as a routine utility issue. Canada is forecast to grow at a 5.74% CAGR through 2031, which makes it the fastest growing geography in the North America sodium bicarbonate market. That growth is supported by food processing expansion, dairy demand, and water infrastructure needs, while the country continues to benefit from access to U.S. supply without carrying the same level of domestic production capital burden. The gap between Canada’s growth rate and the regional average shows that demand side expansion is the main driver there.

Mexico contributes steady demand to the North America sodium bicarbonate market through bakery, carbonated beverage, household cleaning, and industrial cleaning uses. Its role is smaller than that of the United States and Canada, but it adds stability because these uses are spread across both consumer and industrial channels. Rest of North America remains a residual geography, yet it still reflects how proximity to U.S. supply keeps incremental logistics barriers relatively contained. Overall, the geography structure of the North America sodium bicarbonate market remains anchored in U.S. production strength while growth momentum broadens through Canada and steady consumption persists in Mexico.

Competitive Landscape

The North America sodium bicarbonate market is consolidated, with a limited group of large producers shaping supply through feedstock access, purification capability, and compliance readiness. This structure gives established suppliers an advantage because mining, processing, documentation, and customer qualification all require time and capital. Solvay remains one of the central companies in the North America sodium bicarbonate market through its dry sorbent platform and pharmaceutical-grade capabilities. In its 2025 Q4 earnings roadshow, the company identified sodium bicarbonate as one of the categories targeted for discretionary capital investment and described bicarbonate sales as resilient even when broader soda ash conditions were weaker. That move shows a clear preference for higher-value derivative products within the North America sodium bicarbonate market. It also signals that leading players are directing capital toward segments where product quality and application support can protect margins better than basic commodity exposure.

Church and Dwight holds an important position in the North America sodium bicarbonate market through the ARM and HAMMER franchise and its broad presence across consumer and ingredient-linked channels. The company reported 2025 net sales of USD 6,203.20 million and pointed to sodium bicarbonate and animal nutrition as key contributors, which indicates continued commercial strength around the category. Its 2026 launch of ARM and HAMMER Fresh Laundry Detergent with 10x more baking soda is a clear example of a strategy that extends demand through branded product development rather than through bulk supply competition alone. Another major move came in March 2025, when WE Soda completed the acquisition of Genesis Alkali, creating the world’s largest natural soda ash producer with 10.50 million metric tons per year of combined capacity. That transaction matters for the North America sodium bicarbonate market because upstream scale can influence feedstock leverage and supply alignment for downstream bicarbonate operations.

Specialty participants also shape the North America sodium bicarbonate market where purity, customization, and end use documentation matter more than broad tonnage. J.M. Huber strengthened that position when Huber Engineered Materials acquired the Natrium Products business assets in April 2024, bringing specialty sodium bicarbonate capability more directly under Huber Specialty Minerals. This move supports the part of the North America sodium bicarbonate market that serves pharmaceutical, water treatment, and industrial niches with tighter specification needs. The competitive direction is therefore not only about who can produce the most, but also about who can qualify faster, document better, and support higher purity applications more consistently. That is why the North America sodium bicarbonate market continues to look concentrated in core supply while still leaving selective room for specialized players.

North America Sodium Bicarbonate Industry Leaders

Church and Dwight Co., Inc.

Solvay Inc.

Tosoh Corporation

Natural Soda LLC

FMC Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Solvay announced an optimization of soda ash production capacity at its Torrelavega plant in Spain, reducing output from 600 kt to 420 kt effective Q3 2026, with an explicit statement that sodium bicarbonate operations at the site remain unaffected. The measure is part of Solvay's broader strategy to strengthen global asset competitiveness while continuing to invest selectively in bicarbonate as a priority growth category.

- November 2025: Glenmark Pharmaceuticals Inc., USA announced the launch of its 8.4% Sodium Bicarbonate Injection USP (50 mEq/50 mL Single-Dose Vial), a bioequivalent and therapeutically equivalent alternative to Abbott Laboratories' reference product. The injectable is indicated for the treatment of severe metabolic acidosis and expands Glenmark's institutional injectable portfolio.

North America Sodium Bicarbonate Market Report Scope

| Pharma Grade |

| Food Grade |

| Industrial Grade |

| Feed Grade |

| Powder |

| Liquid |

| Crystal |

| Pallets |

| Food and Beverages |

| Pharmaceuticals |

| Animal Feed |

| Water Treatment |

| Industrial |

| Others |

| United States |

| Canada |

| Mexico |

| Rest of North America |

| By Grade | Pharma Grade |

| Food Grade | |

| Industrial Grade | |

| Feed Grade | |

| By Form | Powder |

| Liquid | |

| Crystal | |

| Pallets | |

| By Applications | Food and Beverages |

| Pharmaceuticals | |

| Animal Feed | |

| Water Treatment | |

| Industrial | |

| Others | |

| By Geography | United States |

| Canada | |

| Mexico | |

| Rest of North America |

Key Questions Answered in the Report

What is the 2031 outlook for sodium bicarbonate demand in North America?

The North America sodium bicarbonate market is projected to reach USD 1.15 billion by 2031 from USD 945.28 million in 2026, growing at a 4.02% CAGR over 2026 to 2031.

Which grade leads regional sales and which grade is growing fastest?

Food grade led with 42.56% share in 2025, while pharma grade is forecast to grow fastest at a 5.02% CAGR through 2031.

Why is the United States so important to regional supply?

The United States held 40.23% share in 2025 and benefits from Wyoming trona resources, integrated production, rail infrastructure, and export linked logistics that support regional supply.

What is driving growth in the liquid form segment?

Liquid is projected to grow at a 5.11% CAGR because pharmaceutical compounding, water treatment, and dialysis related handling needs favor controlled dosing and easier preparation.

Page last updated on: