North America Pumps Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2020 - 2023 |

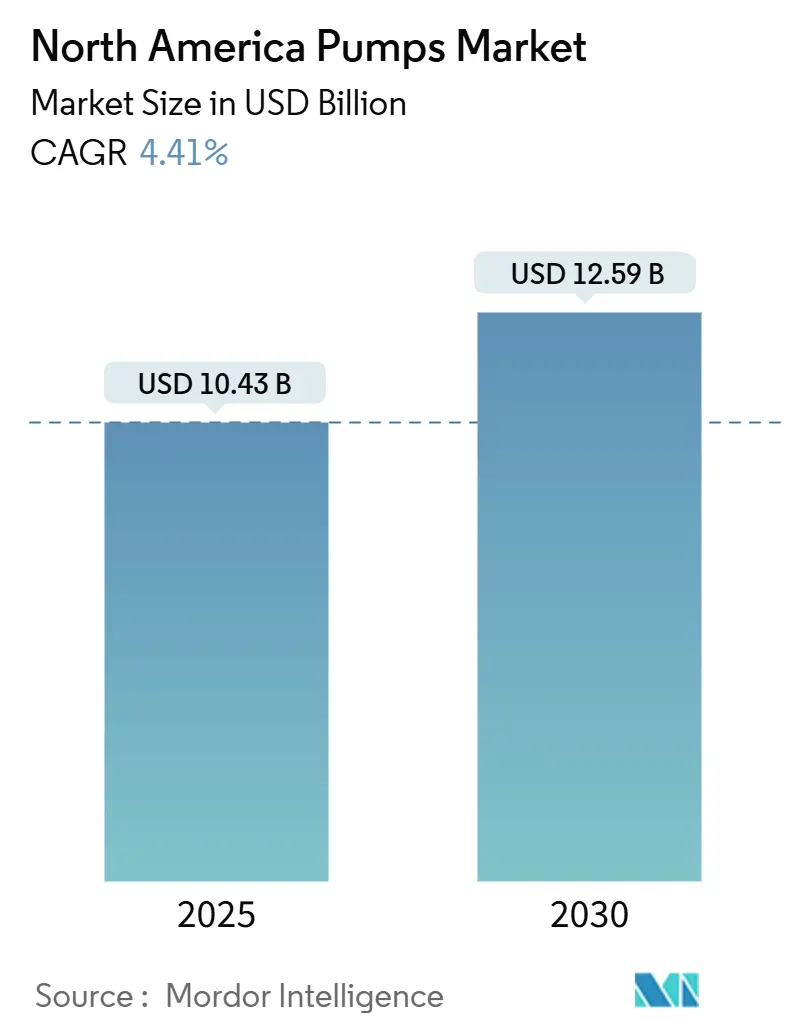

| Market Size (2025) | USD 10.43 Billion |

| Market Size (2030) | USD 12.59 Billion |

| Growth Rate (2025 - 2030) | 4.41% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Pumps Market Analysis by Mordor Intelligence

The North America Pumps Market size is estimated at USD 10.43 billion in 2025, and is expected to reach USD 12.59 billion by 2030, at a CAGR of 4.41% during the forecast period (2025-2030).

This expansion of the North America pumps market is fueled by federal water-quality mandates, the rebound of shale production, and investment in hydrogen corridors that call for specialized high-pressure equipment. Municipal utilities speeding up PFAS compliance, agricultural users shifting to solar irrigation, and miners demanding deeper dewatering solutions are reshaping tender specifications across the North America pumps market. Simultaneously, OEMs are integrating Industrial Internet of Things (IIoT) sensors that trim downtime, while volatile nickel pricing and a tightening labor pool temper near-term margins. Competitive dynamics in the North America pumps market remain moderate as the top five suppliers hold roughly 40% revenue and increasingly lean on predictive-maintenance contracts to lock in service income.

Key Report Takeaways

- By pump type, centrifugal designs captured 53.1% of North America's pump market share in 2024; positive-displacement alternatives will post the swiftest 5.2% CAGR through 2030.

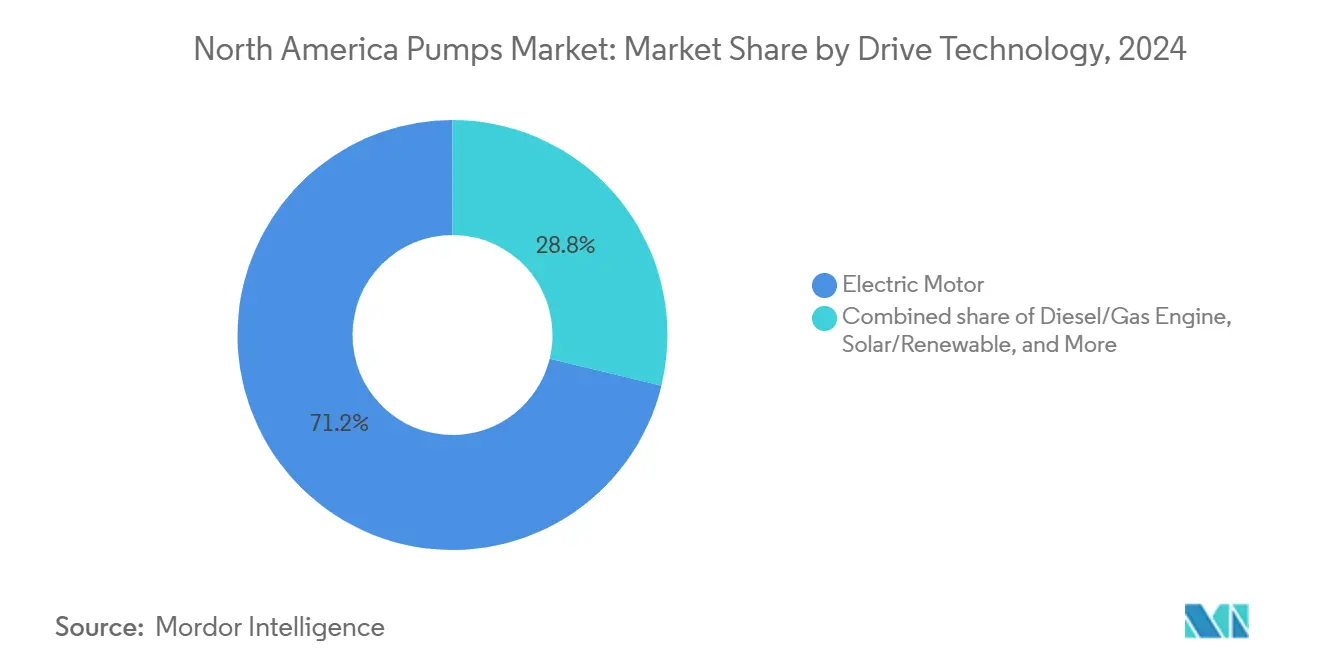

- By drive technology, electric-motor pumps commanded 71.2% of the North America pumps market size in 2024, whereas solar and other renewables will expand at a 5.7% CAGR to 2030.

- By position, surface-mounted units held 59.6% revenue in 2024, yet submersible models are on course for a 6.2% CAGR, the highest within this segmentation.

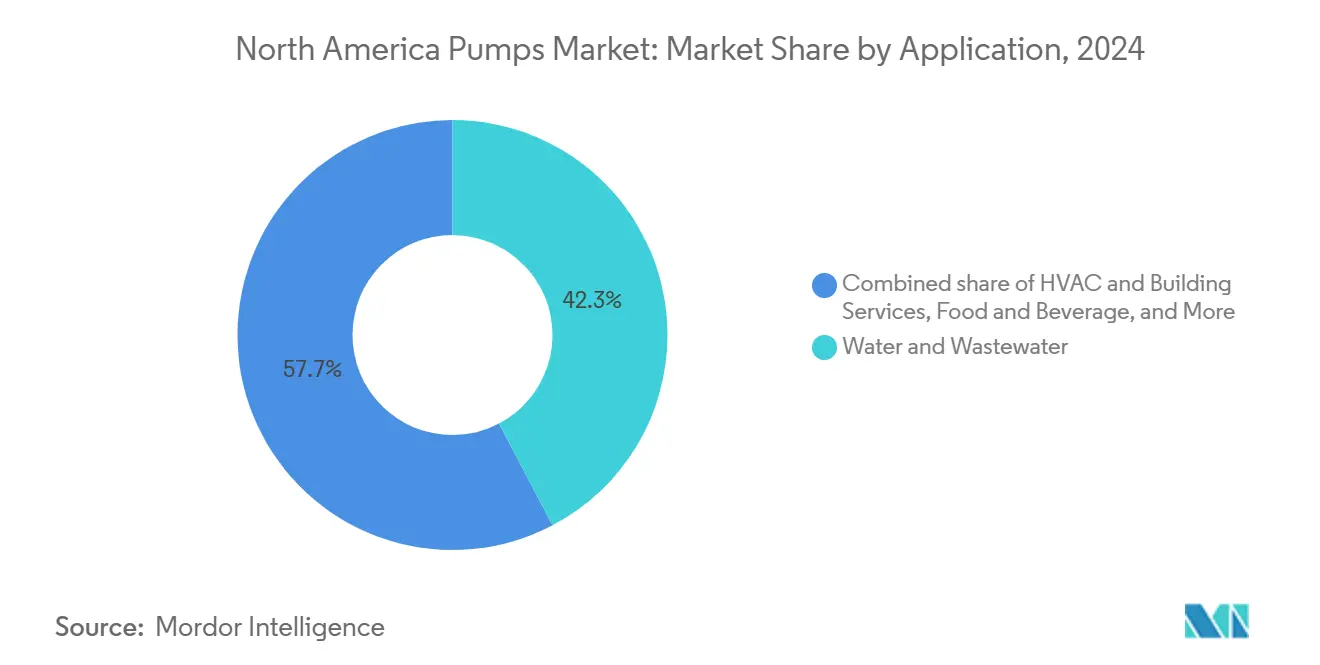

- By application, water and wastewater accounted for 42.3% of North America's pump market size in 2024 and are advancing at a 5% CAGR on the back of stricter federal standards.

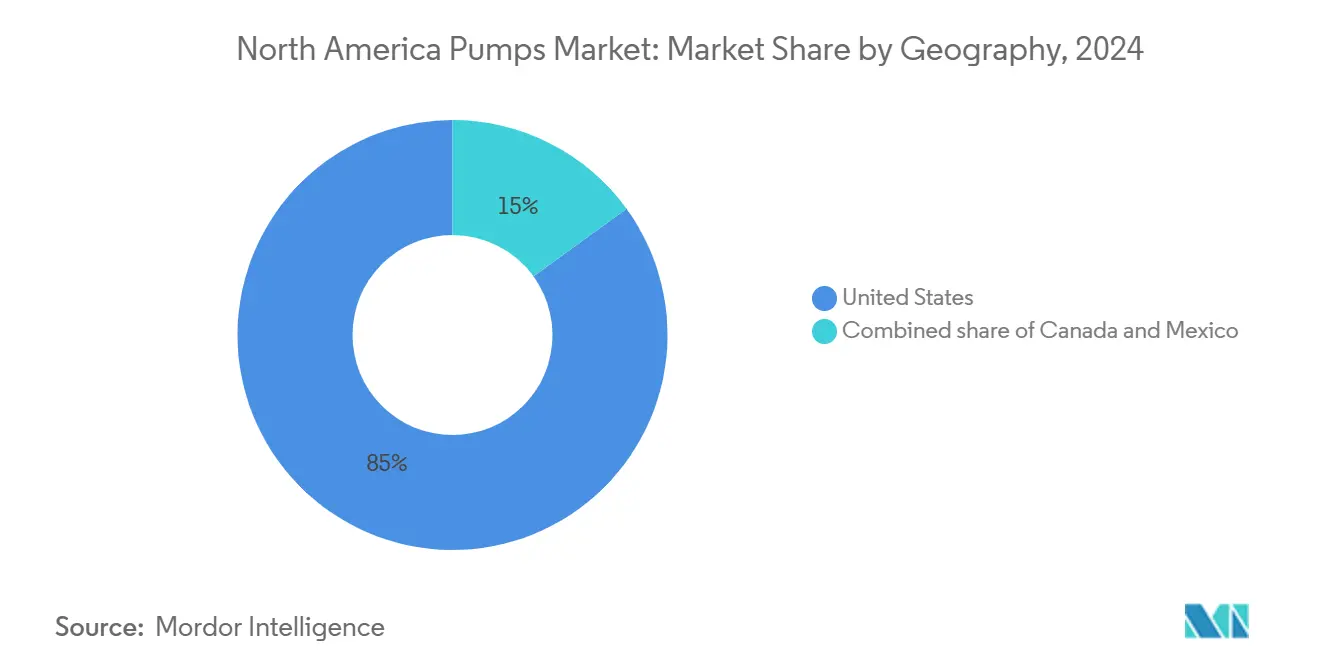

- By geography, the United States led with 85% revenue and is growing at 4.7%, outpacing Canada and Mexico thanks to sustained infrastructure appropriations.

North America Pumps Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Industrial automation & IIoT adoption | +0.8% | United States Midwest, Gulf Coast; Southern Ontario | Medium term (2-4 years) |

| Shale-oil recovery resurgence | +0.6% | Permian, Bakken, Eagle Ford | Short term (≤ 2 years) |

| Federal PFAS water-treatment mandates | +1.2% | Nationwide, highest in Northeast and Great Lakes | Long term (≥ 4 years) |

| AI-enabled predictive maintenance platforms | +0.7% | United States and Canada industrial corridors | Medium term (2-4 years) |

| Hydrogen pipeline build-out | +0.4% | Gulf Coast hubs, California | Long term (≥ 4 years) |

| On-site modular desalination pilots | +0.3% | California, Florida, Texas coasts | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Industrial Automation & IIoT Adoption

Manufacturers are embedding edge-computing chips and wireless vibration sensors into centrifugal and positive-displacement pumps, cutting mean time to repair by 25% and extending seal life by 30% in 2024 field pilots. Sixty-two percent of North American plant managers intend to retrofit legacy assets with IIoT gateways by 2026, driven by insurance incentives and corporate sustainability reporting. The converging operational-technology and IT stacks expose assets to cyber threats, prompting IEC 62443 certification and partnerships with specialist security vendors.[1]International Electrotechnical Commission, “IEC 62443 Cyber Security Standards,” iec.ch Pumps fitted with anomaly-detection firmware now command premiums because ransomware strikes on water utilities jumped 40% in 2024. Subscription analytics are reshaping revenue models; over the life cycle, data services can out-earn the original hardware within three years.

Shale-Oil Recovery Resurgence

United States crude output averaged 13.2 million barrels per day in December 2024, lifting demand for electric submersible and progressive-cavity pumps that tolerate high gas-to-oil ratios.[2]U.S. Energy Information Administration, “Petroleum Production Data,” eia.gov Operators are specifying tungsten-carbide wear parts and elastomer stators rated for 180 °C, doubling run life and trimming workover costs by USD 1.5 million per well. Eight hundred kilometers of new gathering pipelines commissioned in 2024 require multistage boosters delivering 60 bar discharge. Because Permian break-even prices slipped below USD 40 per barrel, producers now optimize artificial-lift systems with variable-frequency drives and down-hole sensors that tie directly into cloud platforms.

Federal PFAS Water-Treatment Mandates

The April 2024 EPA rule compels 6,000 U.S. water systems to add granular activated-carbon or ion-exchange trains by 2029, triggering a surge in high-flow transfer pumps, backwash pumps, and chemical metering units.[3]U.S. Environmental Protection Agency, “PFAS National Primary Drinking Water Regulation,” epa.gov New Jersey alone earmarked USD 400 million in 2024 for remediation, specifying stations that process 50 million liters per day. OEMs now market ANSI/NSF 61-certified wetted parts, such as 316L stainless steel casings, to avoid secondary contamination. Required contact-time extensions push utilities to uprate pump capacities 30%, fostering demand for larger frames and inverter duty motors.

AI-Enabled Predictive Maintenance Platforms

Machine-learning models parsing vibration and power data are forecasting bearing failures up to two weeks ahead, cutting emergency shutdowns by 35% in pilot programs at Dow and BASF plants. Algorithms ingest accelerometer feeds at 25 kHz and separate normal wear from cavitation signatures with convolutional neural networks. Because unplanned outages cost USD 250,000 per hour, even USD 50,000 sensor retrofits deliver rapid payback. Data-model interoperability improved after the 2024 Open Process Automation Forum released a unified schema, easing analytics across mixed fleets. Distributors now partner with community colleges to train technicians in data science, helping close skill gaps flagged by the Bureau of Labor Statistics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile nickel-based alloy pricing | -0.5% | United States and Canada chemical, offshore | Short term (≤ 2 years) |

| Skilled-labor shortages for pump retrofits | -0.7% | United States nationwide, acute in Rust Belt and Gulf Coast | Medium term (2-4 years) |

| Mexico energy-policy uncertainty | -0.3% | Countrywide midstream projects | Medium term (2-4 years) |

| Cyber-security risks in connected pumps | -0.2% | United States and Canada critical infrastructure | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Nickel-Based Alloy Pricing

Nickel averaged between USD 16,800 and USD 22,400 per metric ton in 2024, a 33% swing that inflated costs for super-duplex and Hastelloy pumps.[4]London Metal Exchange, “Nickel Prices and Data,” lme.com A 10% nickel uptick lifts material spend on a 500 hp chemical pump by USD 12,000, compressing gross margin from 28% to 22% unless price-escalator clauses kick in. Some OEMs pivot to nickel-aluminum bronze or ceramic-lined steel for non-critical duties, but these alloys cannot survive high-chloride offshore environments. Hedging on futures exchanges adds 2-3% to bid prices, and Gulf Coast EPC contractors increasingly demand fixed-price contracts with 18-month delivery windows, heightening exposure to metal volatility.

Skilled-Labor Shortages for Pump Retrofits

The United States recorded 87,000 unfilled industrial-machinery mechanic posts in 2024, a 15% vacancy that prolonged pump commissioning by up to six weeks.[5]U.S. Bureau of Labor Statistics, “Industrial Machinery Mechanics,” bls.gov High-precision tasks, such as laser alignment within 0.05 mm and dynamic balancing of large impellers, face acute scarcity as 40% of experienced technicians retire by 2027. Turnkey installation bundles from distributors now carry 8-10% cost premiums but guarantee schedule adherence. Modular pump skids delivered factory-tested and pre-aligned reduce on-site labor hours by 60%, increasingly appealing where artisans are unavailable.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Pump Type: Centrifugal Dominance Anchored by Municipal Upgrades

Centrifugal units captured 53.1% of the North America pumps market share in 2024 and are slated to grow at a 5.2% CAGR to 2030. This slice of the North American pumps market benefits from utilities choosing ANSI B73.1 end-suction designs with 316 stainless impellers that tolerate chlorine and ozone in advanced-oxidation processes. Positive-displacement pumps, while holding the balance of revenue, retain niches in polymer injection, viscous food handling, and biopharma single-use systems that eliminate cross-contamination despite higher consumable costs.

Flowserve’s RedRaven platform embeds wireless sensors that predict seal failure 14 days in advance, raising centrifugal reliability and winning municipal bids where lifecycle cost trumps capex. Energy-efficiency codes hinder positive-displacement adoption in certain states because inherent slip drives 10-15% lower wire-to-water efficiency than centrifugal baselines. Yet progressive-cavity and peristaltic models remain indispensable in bioreactors and chocolate transfer, safeguarding shear-sensitive fluids.

By Drive Technology: Solar Gains Traction in Off-Grid Agriculture

Electric motors commanded 71.2% of the North America pumps market size in 2024, thanks to mature variable-frequency drives that trim energy across fluctuating loads. Solar-powered units, though a smaller slice, are expanding 5.7% annually as U.S. Department of Agriculture grants offset half the photovoltaic cost for irrigation in desert states.[6]U.S. Department of Agriculture, “Renewable Energy Programs,” usda.gov Franklin Electric’s solar shipments jumped 35% in 2024 to Arizona, New Mexico, and California ranches, where growers sidestep diesel volatility and emissions.

Diesel and gas engines still serve remote oil fields but face rising fuel logistics costs and tighter emissions standards. A sealless subset, magnetically driven pumps, meets zero-emission mandates in semiconductor and chemical services, cutting VOC leakage by 98% and complying with California’s South Coast Air Quality rulebook, although premiums of up to 80% restrain wider uptake.

By Position: Submersible Surge Tied to Mining Dewatering

Surface-mounted equipment held 59.6% revenue in 2024, but submersible models will outpace the segment at a 6.2% CAGR, reflecting deeper copper-lithium pits in Nevada and Arizona. Removing suction-lift constraints, submersibles operate below the waterline, avoiding cavitation at depths beyond 300 m and cutting site noise.

Miners now specify hard-metal impellers and abrasion coatings that stretch overhaul intervals to 12,000 hours while coastal desalination pilots pick super-duplex casings to fend off chloride corrosion, trading 25% higher capex for lifetime savings by eliminating sacrificial anodes. Vertical in-line pumps service high-rise HVAC loops where footprint limits preclude horizontal frames and Leadership in Energy and Environmental Design compliance demands low noise performance.

By Application: Water and Wastewater Lead on Regulatory Tailwinds

Water and wastewater projects generated 42.3% of the North America pumps market size in 2024 and will lead growth at 5% through 2030 as plants address PFAS and revised Lead and Copper Rule thresholds. Chemical and petrochemical operators, roughly 18% of demand, specify API 610 pumps with Plan 53B seals for fugitive-emission compliance.

Building services are swapping legacy circulators for electronically commutated motor pumps that cut energy 70%, aligning with the U.S. Department of Energy’s 2024 efficiency mandate. Oil and gas cover 15% of revenue, driven by shale plays and LNG terminals, while food processors rely on 3-A-certified hygienic designs for dairy and beverage lines. Mining applications require 100-bar multistage pumps for tailings pipelines, and power plants demand ASME-qualified units with seismic bases in West Coast nuclear stations. Pharmaceutical producers prefer single-use and magnetically driven pumps after the 2024 FDA biologics guidance accelerated continuous manufacturing adoption.

Geography Analysis

The United States dominated the North America pumps market with 85% revenue in 2024 and is tracking a 4.7% CAGR through 2030 as the Bipartisan Infrastructure Law funnels USD 50 billion into drinking-water projects. Western drought intensifies desalination investment, while the Rust Belt channels funds toward stormwater overflow containment, both adding bespoke pump demand. Shale states account for 60% of upstream orders, tying volume to oil-price volatility. Hydrogen hubs backed by USD 7 billion in Department of Energy grants will require cryogenic pumps, potentially injecting USD 200 million in incremental demand by 2028.

Canada represents about 10% of regional turnover. Ottawa’s 2024 budget set aside CAD 6 billion (USD 4.4 billion) for water infrastructure, prioritizing First Nations systems in Ontario and Quebec.[7]Infrastructure Canada, “Investing in Canada Plan,” infrastructure.gc.ca Alberta oil-sands require 200 °C-rated pumps for bitumen froth, concentrating orders with a handful of OEMs, while British Columbia LNG export build-outs demand cryogenic centrifugal units for Kitimat’s new terminal.

Mexico delivers the remaining 5%, restrained by energy policies that favor state utility Comisión Federal de Electricidad over private generation, slowing pump procurement for combined-cycle plants. Nevertheless, nearshoring of electronics and auto plants to Nuevo León and Guanajuato drives HVAC and process-cooling pump installs certified to NOM-006-ENER efficiency rules.[8]Government of Mexico, “Energy Efficiency Standards – NOM-006-ENER,” gob.mx Northern states facing water scarcity invest in groundwater pumping and reuse schemes, although funding gaps limit scale compared with U.S. programs.

Competitive Landscape

The North America pumps market shows moderate concentration: Flowserve, Xylem, ITT, Pentair, and Grundfos command roughly 40% of revenue, leaving room for specialists in slurry, solar, and sanitary niches. Xylem’s USD 7.5 billion Evoqua acquisition in October 2024 created a vertically integrated water-solutions supplier with bundled digital analytics. Flowserve’s RedRaven IoT augments its ANSI portfolio with vibration-based seal-life prediction that slashes downtime 20-30%.

Patent filings signal a pivot toward magnetic bearings and ceramic-composite impellers; Sulzer logged 12 U.S. patents in 2024 on non-contact bearing systems rated for 100,000 hours between failures, targeting nuclear and sterile pharma lines.[9]U.S. Patent and Trademark Office, “Patent Database,” uspto.gov Hydrogen infrastructure represents white-space growth: cryogenic pumps able to manage liquid hydrogen at -253 °C are currently supplied at scale only by Ebara and Nikkiso, giving early movers a pricing umbrella. Modular desalination needs skid-mounted, super-duplex submersibles that cut field labor 60%, a sweet spot for mid-size fabricators versed in coastal corrosion.

Cybersecurity compliance under IEC 62443 is emerging as a tender differentiator, commanding 8-10% premiums in chemical and power bids where ransomware exposure is material. Disruptors such as EDDY Pump leverage non-clog geometries to handle mining slurries with 70% solids by weight, chopping wear-ring replacements, and courting copper-belt miners.

North America Pumps Industry Leaders

Flowserve Corporation

Xylem Inc.

Grundfos Holding A/S

ITT Inc.

KSB SE & Co. KGaA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Pierce Manufacturing Inc., a subsidiary of Oshkosh Corporation, announced the delivery of its 4,000th Pierce Ultimate Configuration (PUC) Pump. This milestone order, facilitated by Pierce dealer Hughes Fire Equipment, is now serving the Clark County Fire Department (CCFD) in Nevada.

- November 2025: Unibloc Hygienic Technologies launched its latest offering: the Unibloc CleanPlus line. These pumps cater to the cosmetic, pharmaceutical, and tanker truck sectors, emphasizing durability and sanitary operations.

- August 2025: Pioneer Pump unveiled a new line of industrial pumps, now certified to meet the NSF/ANSI 61 standard, specifically designed for municipal and potable water applications.

- March 2025: Eaton began distributing Bezares variable-flow hydraulic pumps (95-130 cc/rev) across North America, targeting waste-collection trucks and farm equipment with energy-saving load-sensing control.

North America Pumps Market Report Scope

Pumps, mechanical devices, convert energy to elevate, transport, or compress fluids, be it liquids or gases. By transforming mechanical energy into hydraulic or pneumatic energy, pumps generate a pressure difference, propelling fluids from lower to higher pressure zones.

The North America pumps market is segmented by pump type, drive technology, position, application, and geography. By pump type, the market is segmented into centrifugal and positive-displacement. By drive technology, the market is segmented into electric motor, diesel/gas engine, solar/renewable, and magnetically-driven/sealless. By position, the market is segmented into surface, submersible, and vertical in-line. By application, the market is segmented into water and wastewater, chemical and petrochemical, HVAC and building services, oil and gas, food and beverage, mining and metals, power generation, pharmaceuticals and biotech, and others. The report also covers the market sizes and forecasts for the North America pumps market across major countries. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Centrifugal |

| Positive-Displacement |

| Electric Motor |

| Diesel/Gas Engine |

| Solar/Renewable |

| Magnetically-Driven/Sealless |

| Surface |

| Submersible |

| Vertical In-Line |

| Water and Wastewater |

| Chemical and Petrochemical |

| HVAC and Building Services |

| Oil and Gas (Upstream, Midstream, Downstream) |

| Food and Beverage |

| Mining and Metals |

| Power Generation (Thermal, Nuclear, Renewables) |

| Pharmaceuticals and Biotech |

| Others |

| United States |

| Canada |

| Mexico |

| By Pump Type | Centrifugal |

| Positive-Displacement | |

| By Drive Technology | Electric Motor |

| Diesel/Gas Engine | |

| Solar/Renewable | |

| Magnetically-Driven/Sealless | |

| By Position | Surface |

| Submersible | |

| Vertical In-Line | |

| By Application | Water and Wastewater |

| Chemical and Petrochemical | |

| HVAC and Building Services | |

| Oil and Gas (Upstream, Midstream, Downstream) | |

| Food and Beverage | |

| Mining and Metals | |

| Power Generation (Thermal, Nuclear, Renewables) | |

| Pharmaceuticals and Biotech | |

| Others | |

| By Geography | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

How large is the North America pumps market in 2025?

The North America pumps market size stands at USD 10.43 billion in 2025 and is set to grow to USD 12.59 billion by 2030.

Which pump type leads demand across the region?

Centrifugal designs dominate with 53.1% revenue in 2024 and remain the preferred choice for municipal and industrial users.

What regulatory factor is driving new municipal pump purchases?

The EPA’s 2024 PFAS rule compels thousands of U.S. water systems to upgrade treatment trains, boosting high-flow pump demand.

Where is solar-powered pumping seeing the fastest uptake?

Off-grid agricultural irrigation in Arizona, New Mexico, and California is adopting solar submersibles at a 5.7% CAGR.

Which country outside the United States is growing fastest?

Canada is benefiting from CAD 6 billion in federal water-infrastructure funding, lifting pump demand in Ontario and Quebec.

What technology trend is reshaping aftermarket service?

AI-enabled predictive maintenance platforms now forecast bearing failures two weeks ahead, cutting unplanned outages by one-third.

Page last updated on: