North America Printed Circuit Board Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

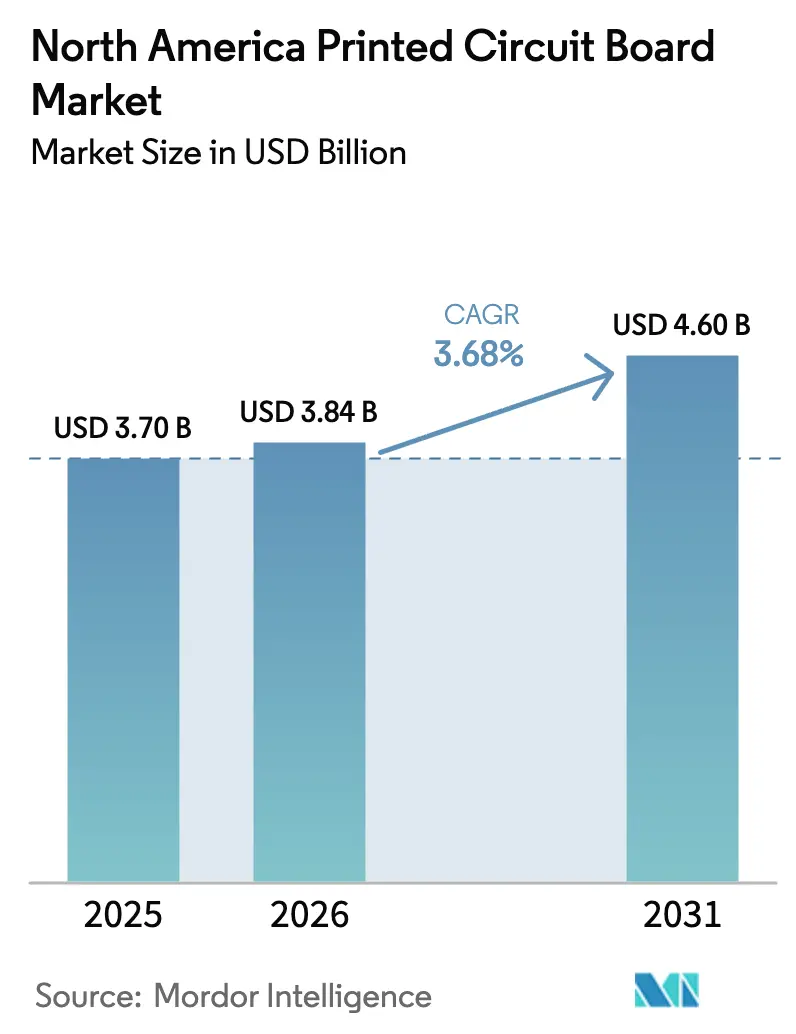

| Base Year Market Size (2025) | USD 3.70 Billion |

| Market Size (2026) | USD 3.84 Billion |

| Market Size (2031) | USD 4.60 Billion |

| Growth Rate (2026 - 2031) | 3.68% CAGR |

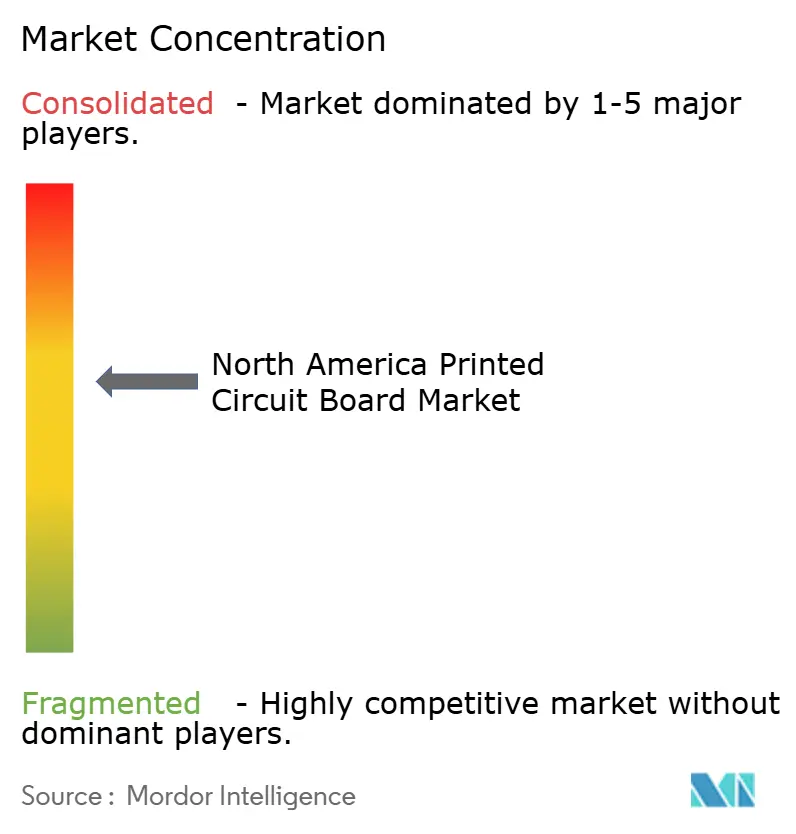

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Printed Circuit Board Market Analysis by Mordor Intelligence

The North America Printed Circuit Board Market size in 2026 is estimated at USD 3.84 billion, growing from 2025 value of USD 3.70 billion with projections showing USD 4.60 billion, growing at 3.68% CAGR over 2026-2031. Stable headline growth conceals a rapid pivot toward sovereign defense supply chains, hyperscale data-center expansion for generative AI, and speed upgrades from 400 G to 800 G optical modules. Book-to-bill ratios for rigid boards climbed to 1.06 in September 2025, signalling that design activity now exceeds shipments and that capacity is tightening for advanced-layer-count and HDI production. The United States held 85.75% of regional revenue in 2025, yet Canada is expanding faster, with a 4.87% CAGR, as federal incentives promote semiconductor packaging and cross-border automotive clusters drive demand for quick-turn flexible circuits. Automotive battery-management systems, 5G base-station rollouts, and liquid-cooled AI servers continue to lift average layer counts, driving sustained investment in ultra-HDI processes and high-speed, low-loss laminate lines.

Key Report Takeaways

- By PCB type, standard multilayer boards held 25.53% of the North America printed circuit board market share in 2025, while flexible circuits are forecast to grow at a 4.23% CAGR through 2031.

- By substrate material, glass epoxy FR-4 accounted for 40.85% of the North America PCB market share in 2025, whereas high-speed low-loss laminates are expected to expand at a 4.67% CAGR between 2026 and 2031.

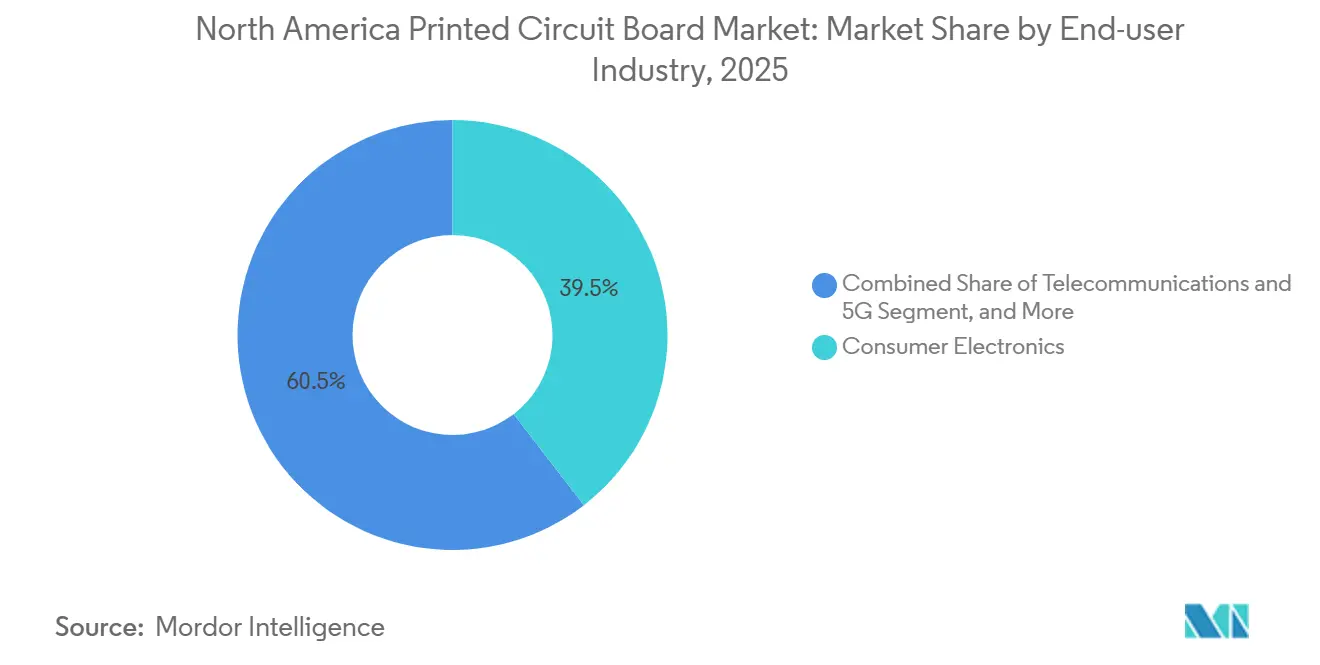

- By end-user industry, consumer electronics captured 39.53% revenue in 2025, and telecommunications and 5G infrastructure are projected to record the fastest 4.51% CAGR to 2031.

- By country, the United States dominated with an 85.75% revenue share in 2025, and Canada showed the highest 4.87% CAGR outlook to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Printed Circuit Board Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-Center AI Chips Spurring IC Substrates | +0.9% | United States hyperscale hubs | Medium term (2-4 years) |

| 5G Rollout Accelerating HDI PCB Demand | +0.8% | North America, spill-over to Europe and Asia-Pacific | Short term (≤ 2 years) |

| EV and ADAS Growth Driving High-Power Boards | +0.7% | United States and Canada automotive corridors, Mexico assembly | Medium term (2-4 years) |

| Ultra-Low-Loss Materials for 112 G PAM4 | +0.6% | United States data-center supply chains, Taiwan technology nodes | Long term (≥ 4 years) |

| Defense Secure-Supply Mandates | +0.5% | United States ITAR-compliant sites | Long term (≥ 4 years) |

| Additive Manufacturing for Quick-Turn PCBs | +0.3% | California, Massachusetts, Texas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Data-Center AI Chips Spurring IC Substrates

Graphics and tensor processors used for generative AI now rely on flip-chip ball-grid-array packages with finer pitch and higher I/O density, elevating substrate value per server. Capital spending on 300-millimeter advanced-packaging lines surpassed USD 100 billion in 2025, and a growing share is earmarked for North American capacity. [1]SEMI Analysts, “300 mm Fab Equipment Spending Outlook,” SEMI, semi.org Liquid-cooled racks exceeding 50 kilowatts per rack require substrates with embedded thermal vias and copper coin heat spreaders, prompting fabricators to adopt Ajinomoto Build-up Film and other high-performance resins. Sanmina’s 2025 purchase of ZT Systems transferred proprietary know-how for designing backplanes that integrate power delivery and high-speed SerDes on a single substrate, cutting latency and board count. Export controls on leading-edge semiconductor equipment indirectly tighten substrate supply, increasing the strategic importance of regional production.

5G Rollout Accelerating HDI PCB Demand

North American carriers are densifying networks with Open RAN base stations and millimeter-wave small cells, each requiring PCBs that stack multiple signal layers into thinner formats. IPC data for February 2025 showed rigid-board shipments rising 8.4% year over year, with HDI units fueling most of the increase. Laser-drilled microvias as small as 75 micrometers are now standard for routing ball-grid-array packages that host field-programmable gate arrays and radio chips.[2]Aviat Networks Engineering, “Open RAN Radio Platforms,” Aviat Networks, aviatnetworks.comCompliance with IPC-6012 Class 3, which mandates thermal cycling from -40 °C to +85 °C and enhanced moisture resistance, raises fabrication complexity but ensures field reliability. Spectrum auctions concluded in 2025 advanced deployment schedules, creating a near-term spike that should stabilize by 2027.

EV and ADAS Growth Driving High-Power Boards

Electric vehicle platforms use thick-copper PCBs, often six to ten ounces per square foot, to manage currents above 400 amperes and voltages up to 800 volts. On-board chargers and traction inverters combine power-plane layers with controlled-impedance signaling, bringing high-frequency design rules into power electronics. Radar modules at 77 GHz and lidar controllers rely on HDI stack-ups with blind and buried vias to fit dense sensor arrays. Infineon’s CoolSiC MOSFET lineup demands boards with embedded heat sinks and thermal-interface materials to dissipate switching losses. Automotive Electronics Council AEC-Q200 and ISO 26262 safety rules extend qualification cycles and elevate material traceability requirements.

Ultra-Low-Loss Materials for 112 G PAM4

Hyperscale data centers are moving from 100 G NRZ to 112 G PAM4 signaling, exposing insertion-loss limits in standard FR-4. Panasonic MEGTRON 8, which posts a 0.0015 dissipation factor at 28 GHz, has entered volume production and anchors many 800 G optical module designs. Rogers RO1200 bondply enables hybrid stack-ups, pairing low-loss signal layers with FR-4 power layers to cut laminate cost by nearly 30%. Isola’s halogen-free TerraGreen 400G2 satisfies European environmental directives while supporting 56 GHz Nyquist operation. [3]Isola Group Product Management, “TerraGreen 400G2 Launch,” Isola Group, isola-group.comCadence and Texas Instruments design guides specify via-stub resonances and maximum trace lengths that only select North American fabricators can meet.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply-Chain Raw-Material Volatility | -0.4% | North America, limited domestic laminate and foil production | Short term (≤ 2 years) |

| CAPEX Intensity and Long ROI Cycles | -0.3% | United States and Canada advanced HDI and IC substrate investments | Medium term (2-4 years) |

| Skilled-Labor Shortages in North America | -0.3% | United States and Canada Class 3 aerospace and medical segments | Long term (≥ 4 years) |

| Environmental Compliance Costs | -0.2% | United States PFAS and state discharge limits | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Supply-Chain Raw-Material Volatility

Ultra-thin copper foil and specialty laminates continue to face 8- to 16-week lead-time swings as most capacity is located in Asia. Rogers and Isola operate limited North American laminate plants, leaving fabricators vulnerable to freight surcharges and changes in duties. Copper prices on the London Metal Exchange fluctuated by 25% in 2024, yet contractual obligations with original equipment makers restricted pass-through, compressing margins by up to 300 basis points. Geopolitical events, such as sanctions disrupting palladium supplies used in electroless plating, trigger requalification expenses and schedule slips. Working-capital needs have climbed as firms now hold 60-90 days of inventory, up from 30-45 days pre-pandemic.

CAPEX Intensity and Long ROI Cycles

Installing a next-generation IC substrate line or ultra-HDI laser drill cell can exceed USD 40 million, with payback periods stretching beyond five years in moderate-growth segments. Federal incentives under the CHIPS and Science Act offset part of the burden, yet qualifying for disbursements requires extensive reporting and local-content commitments. Smaller regional shops struggle to finance direct-imaging lithography, x-ray drilling, and automated optical inspection, widening the technology gap versus tier-one players. Extended qualification loops with aerospace and medical customers further defer revenue currency conversions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By PCB Type: Flexible Circuits Expand in Automotive and Wearables

Standard Multilayer constructions accounted for 25.53% of revenue in 2025, reflecting their entrenched role in industrial controls and legacy computing. Flexible Circuits, though smaller in absolute volume, are predicted to grow at a 4.23% CAGR as battery-management harnesses, foldable phones, and wearable monitors require bendable interconnects. The North America printed circuit board market size for High-Density Interconnect boards is advancing in step with 5G radios and automotive lidar, although smartphone saturation keeps unit growth modest. IC Substrates remain a high-value niche tied to AI accelerators and chiplet packages, while Rigid-Flex combinations gain share in avionics where vibration tolerance is critical. Over the forecast period, liquid-crystal polymer antennas and additively printed multilayer prototypes should further diversify the North America printed circuit board market.

Historical averages show the PCB-type mix grew by 2.8% between 2020 and 2025, but momentum now favors Flexible Circuits and IC Substrates due to electric-vehicle and AI buildouts. Nano Dimension additive platforms enable same-day iterations for defense customers, cutting prototype cycle times from weeks to days. Rigid 1-2-Sided boards remain cost leaders for simple LED lighting and appliance controls, though volume pressure from integrated modules persists. Emerging embedded-passive designs promise incremental BOM savings and layout area reductions, sustaining HDI competitiveness in mobile and automotive devices.

By Substrate Material: Low-Loss Laminates Capture High-Speed Demand

Glass Epoxy FR-4 maintained 40.85% revenue in 2025, favored for cost and UL 94 V-0 compliance. High-Speed Low-Loss materials are projected to rise at a 4.67% CAGR as 112 G PAM4 and 800 G optical modules proliferate; this outlook positions the segment to outpace overall North America PCB market share gains. Polyimide films hold steady in automotive flex and space avionics because of 200 °C thermal ratings, while packaging resins such as bismaleimide-triazine underpin IC Substrates with sub-15 micrometer lines.

Between 2020 and 2025, substrate revenue expanded 3.1%, constrained by smartphone softness, yet the pathway to 224 G SerDes and 1.6 T switches is lifting demand for MEGTRON 8, RO1200, and TerraGreen grades. AGC Multi Material’s low-loss glass cloth announced in 2025 underscores continuing innovation aimed at future 224 G and terahertz applications. Regulatory anchors remain IPC-4101 slash sheets and UL certification, but customers increasingly impose halogen-free and PFAS-free requirements that accelerate material churn.

By End-User Industry: 5G Infrastructure Leads Growth

Consumer Electronics held 39.53% revenue in 2025, yet volume is plateauing as handset replacement cycles lengthen. Telecommunications and 5G infrastructure, however, is slated to grow 4.51% annually, driven by Open RAN radios and optical access terminals that demand HDI reliability. Computing and Data Centers retain robust pull for backplanes and accelerator substrates as generative AI scales. Automotive and EV systems double board content per vehicle versus combustion engines, lifting the North America printed circuit board market size for high-power and radar assemblies.

Industrial drives, solar inverters, and UPS units keep thick-copper demand healthy, whereas medical and aerospace segments maintain smaller but high-margin volumes due to FDA and ITAR qualifications. Emerging embedded-die radar modules in vehicles and printed antennas for 5G small cells illustrate the convergence of packaging and board design. Historical end-user growth averaged 2.9% over 2020-2025, but accelerating electrification and AI workloads underpin a stronger 2026-2031 trajectory.

Geography Analysis

The United States generated 85.75% of North America printed circuit board market revenue in 2025 and is home to most ITAR-cleared sites, ensuring captive defense demand. TTM Technologies expanded its Syracuse plant in 2025, adding sequential lamination for ultra-HDI avionics, while its early-2025 Wisconsin acquisition improved 24-hour prototype support in the automotive Midwest. IPC data for September 2025 showed a 6.0% year-over-year booking increase, resulting in a 1.06 book-to-bill ratio, reflecting tightening regional capacity. Smaller shops such as Sierra Circuits compete by offering rapid engineering feedback and 48-hour turns for medical prototypes.

Canada, supported by CAD 240 million (USD 176 million) in federal incentives under the Strategic Innovation Fund, is projected to grow 4.87% per year through 2031. Ontario and Quebec benefit from proximity to U.S. automotive OEMs and tariff-free access under the United States-Mexico-Canada Agreement, spurring investments in flexible-circuit and HDI lines. Regional universities funnel engineering talent into fabrication plants, helping mitigate skilled-labor shortages.

Mexico remains smaller, but near-shoring shifts are enlarging demand for domestically sourced boards. Jabil expanded Guadalajara and Monterrey campuses in 2025 to support high-mix assembly for cloud infrastructure. Limited indigenous PCB capacity means most rigid-board volume still crosses the border from U.S. suppliers, yet the USMCA rule-of-origin thresholds encourage incremental Mexican investments. Environmental compliance remains less stringent than in the United States, offering cost relief but limiting penetration into Class 3 aerospace programs.Collectively, regional growth averaged 2.7% between 2020 and 2025. The forecast uptick to 3.68% reflects reshoring incentives under the CHIPS and Science Act, defense modernization, and proximity advantages that offset higher labor and compliance costs. PFAS wastewater rules introduced in 2024 raise capital needs for filtration but also strengthen the competitive moat for certified facilities.

Competitive Landscape

The market concentration is moderate, with players such as TTM Technologies, Sanmina, and Jabil anchoring scale, each operating multi-site networks spanning prototyping, medium-volume builds, and Class 3 defense programs. Sanmina’s 2025 integration of ZT Systems provided liquid-cooled server backplane capability aligned with AI cluster demand. TTM’s Syracuse upgrade brought stacked microvias and sequential lamination to military avionics.

White-space persists in IC substrates, as Asia still controls most flip-chip BGA capacity. Nano Dimension additive printers, already installed at defense contractors, enable embedded-component prototypes in hours, a unique differentiator in classified development. Flexible-circuit specialists leverage polyimide and liquid-crystal polymer know-how to serve battery-management and wearable niches, outmaneuvering commodity rigid-board suppliers on agility.

Large fabricators continue to deploy automated optical inspection, direct-imaging lithography, and laser drilling to improve yields and reduce touch labor, widening the technology gap. Smaller shops differentiate on engineering support, offering design-for-manufacturing feedback and rapid iterations. ISO 13485, AS9100, and IPC-6012 Class 3 certifications remain critical entry barriers, protecting incumbents that have established audit histories and validated processes.

North America Printed Circuit Board Industry Leaders

TTM Technologies Inc.

Sanmina Corporation

Jabil Inc.

Summit Interconnect Inc.

AdvancedPCB (APCT, Inc.)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: TTM Technologies completed its ultra-HDI expansion in Syracuse, New York, adding stacked microvia capacity for space-qualified PCBs.

- December 2025: Sanmina reported USD 1.89 billion fiscal Q4 revenue following ZT Systems integration, boosting data-center backplane capability.

- September 2025: IPC noted rigid PCB bookings up 6.0% year over year with a 1.06 book-to-bill ratio, the highest since early 2022.

- August 2025: Jabil recorded USD 6.8 billion fiscal Q3 revenue as cloud and 5G equipment lifted electronics manufacturing demand.

North America Printed Circuit Board Market Report Scope

Printed Circuit Boards (PCBs) are essential components that mechanically support and electrically connect electronic components via conductive pathways, tracks, or signal traces. They are widely utilized across various industries, including consumer electronics, automotive, telecommunications, and healthcare, among others.

The North America Printed Circuit Board (PCB) Market Report is Segmented by PCB Type (Standard Multilayer, Rigid 1-2 Sided, High-Density Interconnect, Flexible Circuits, IC Substrates, Rigid-Flex, and Other PCB Types), Substrate Material (Glass Epoxy, High-Speed Low-Loss, Polyimide, Packaging Resins, and Other Substrate Materials), End-user Industry (Consumer Electronics, Computing and Data Centers, Telecommunications and 5G, Automotive and EV, Industrial and Power, Healthcare and Medical, Aerospace and Defense, and Other End-user Industries), and Country (United States, Canada, and Mexico). The Market Forecasts are Provided in Terms of Value (USD).

| Standard Multilayer (non-HDI) |

| Rigid 1-2 Sided |

| High-Density Interconnect (HDI) |

| Flexible Circuits (FPC) |

| IC Substrates (Package Substrates) |

| Rigid-Flex |

| Other PCB Types |

| Glass Epoxy (FR-4) |

| High-Speed / Low-Loss |

| Polyimide (PI) |

| Packaging Resins (BT / ABF) |

| Other Substrate Materials |

| Consumer Electronics |

| Computing and Data Centers |

| Telecommunications and 5G |

| Automotive and EV |

| Industrial and Power |

| Healthcare / Medical |

| Aerospace and Defense |

| Other End-user Industries |

| United States |

| Canada |

| Mexico |

| By PCB Type | Standard Multilayer (non-HDI) |

| Rigid 1-2 Sided | |

| High-Density Interconnect (HDI) | |

| Flexible Circuits (FPC) | |

| IC Substrates (Package Substrates) | |

| Rigid-Flex | |

| Other PCB Types | |

| By Substrate Material | Glass Epoxy (FR-4) |

| High-Speed / Low-Loss | |

| Polyimide (PI) | |

| Packaging Resins (BT / ABF) | |

| Other Substrate Materials | |

| By End-user Industry | Consumer Electronics |

| Computing and Data Centers | |

| Telecommunications and 5G | |

| Automotive and EV | |

| Industrial and Power | |

| Healthcare / Medical | |

| Aerospace and Defense | |

| Other End-user Industries | |

| By Country | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

How large is the North America printed circuit board market today?

The market reached USD 3.84 billion in 2026 and is forecast to climb to USD 4.60 billion by 2031 on a 3.68% CAGR.

Which PCB type is growing fastest in North America?

Flexible Circuits lead growth with a 4.23% CAGR, fueled by electric-vehicle battery packs, foldable devices, and wearable medical sensors.

What drives demand for high-speed, low-loss laminates?

Migration to 112 G PAM4 and 800 G optical modules in hyperscale data centers requires materials with dissipation factors below 0.002.

Why is Canada’s PCB sector expanding faster than the U.S. segment?

Federal incentives under the Strategic Innovation Fund and proximity to cross-border automotive clusters support a 4.87% CAGR outlook for Canadian fabricators.

Which end-user segment will contribute the most new revenue?

Telecommunications and 5G infrastructure should post the highest incremental gains, advancing at a 4.51% CAGR as Open RAN and small-cell deployments scale.

Page last updated on: