North America Monk Fruit Sweeteners Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

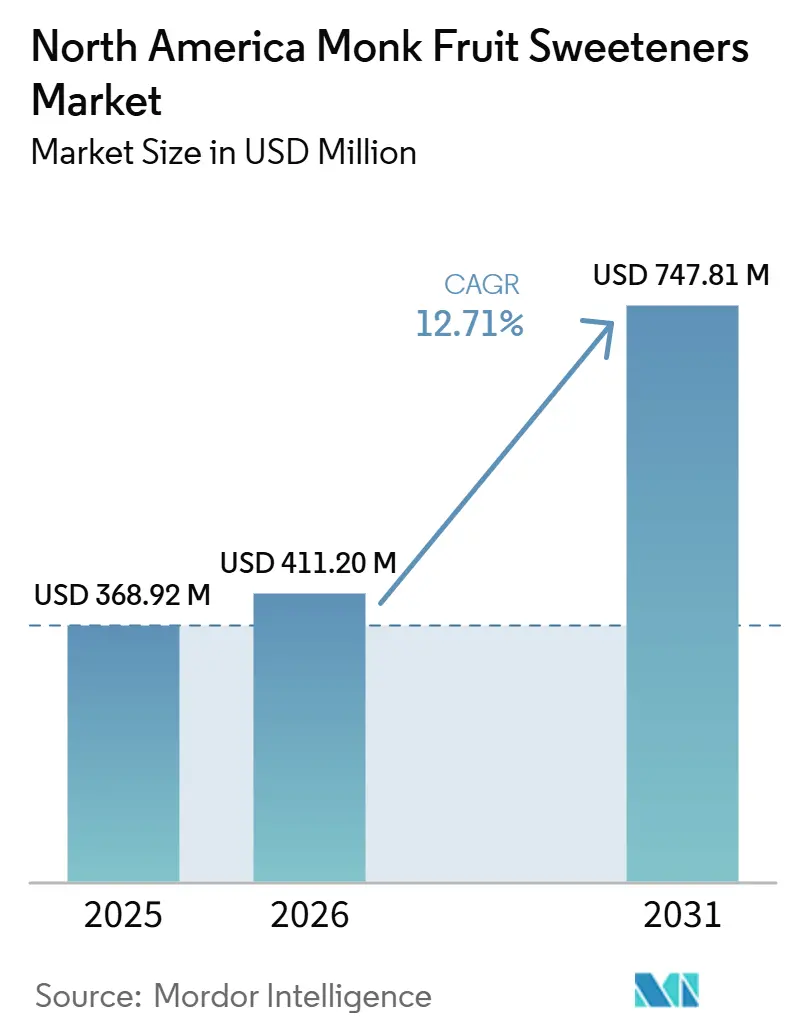

| Base Year Market Size (2025) | USD 368.92 Million |

| Market Size (2026) | USD 411.20 Million |

| Market Size (2031) | USD 747.81 Million |

| Growth Rate (2026 - 2031) | 12.71% CAGR |

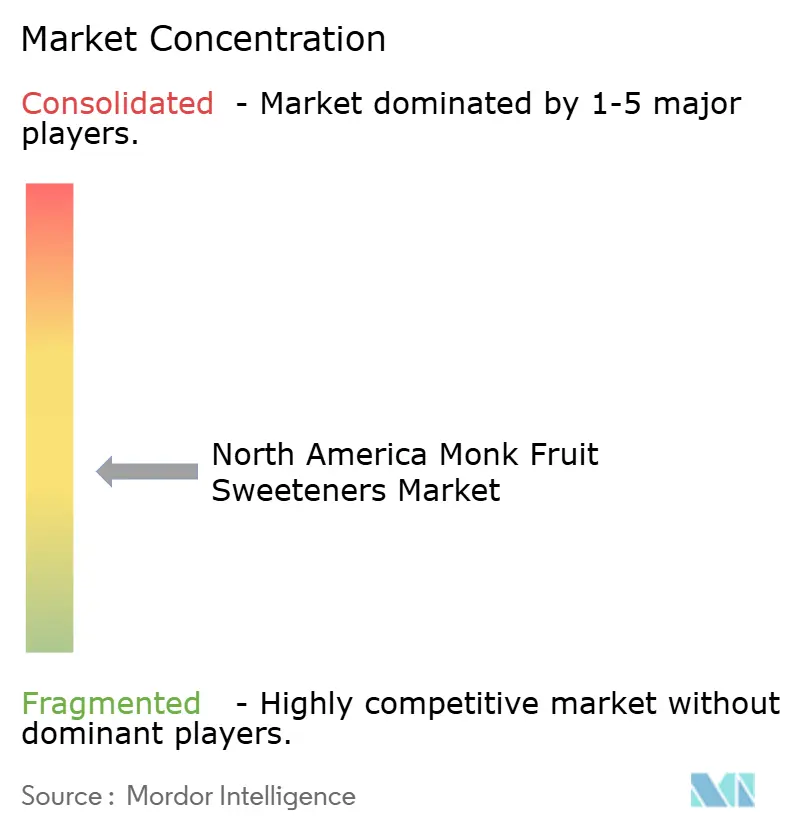

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Monk Fruit Sweeteners Market Analysis by Mordor Intelligence

The North America monk fruit sweeteners market size is projected to grow from USD 368.92 million in 2025 and USD 411.20 million in 2026 to USD 747.81 million by 2031, registering a CAGR of 12.71% during 2026-2031. The market is expanding as food and beverage companies shift from artificial sweeteners to naturally derived, zero-calorie alternatives that support product reformulation while maintaining clean-label positioning. A favorable regulatory environment also supports the market, as the FDA’s long-standing GRAS classification removes a key approval barrier that continues to affect some newer ingredients[1]Source: U.S. Food and Drug Administration, “High-Intensity Sweeteners,” U.S. Food and Drug Administration, fda.gov. Demand growth is outpacing the supply flexibility of mogroside raw materials, keeping prices elevated and preserving monk fruit extract’s premium position compared to stevia and allulose. Beverage manufacturers continue to view monk fruit sweeteners as a practical reformulation option because they support calorie reduction and align with natural positioning across mainstream packaged products. At the same time, the market is evolving around two key competitive priorities: supply security and application support, as both factors now influence buyer confidence as much as ingredient performance.

Key Report Takeaways

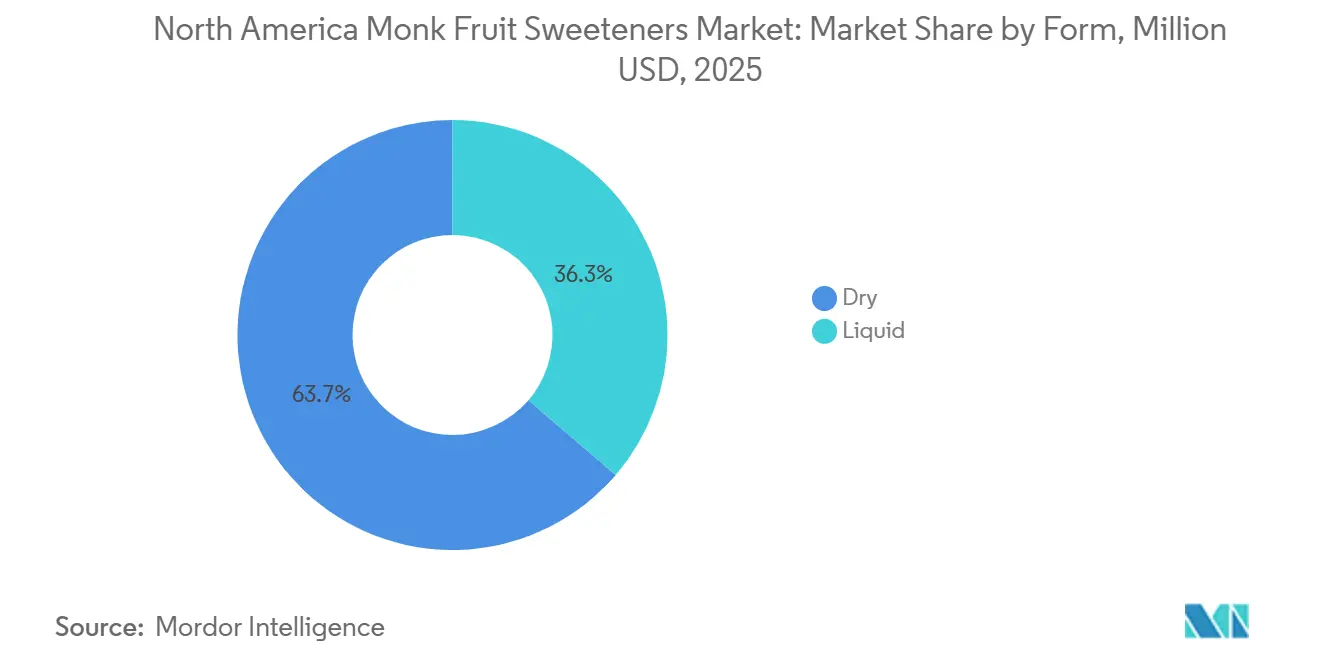

- By form, dry monk fruit sweeteners led with 63.71% share in 2025, while liquid monk fruit sweeteners are forecast to grow at a 13.96% CAGR through 2031.

- By category, conventional monk fruit sweeteners held 81.79% share in 2025, while organic monk fruit sweeteners are projected to expand at a 14.81% CAGR through 2031.

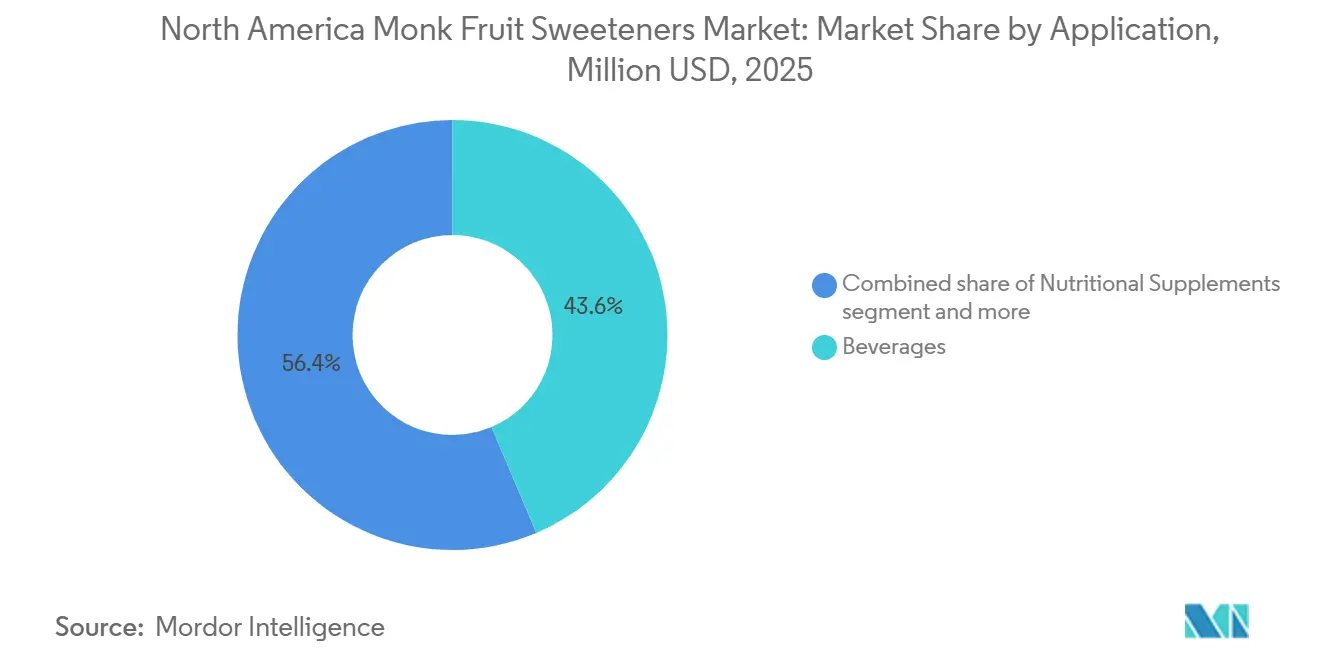

- By application, beverages accounted for 43.62% of the monk fruit sweeteners market size in 2025, while nutritional supplements are advancing at a 13.42% CAGR through 2031.

- By geography, the United States held 79.13% of the monk fruit sweeteners market share in 2025, while Mexico recorded the highest projected CAGR at 13.93% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Monk Fruit Sweeteners Market Trends and Insights

Drivers Impact Analysis*

| Driver | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Clean-label sugar reduction in food and beverage reformulation | +3.2% | Led by the United States and Canada | Medium term (2-4 years) |

| Premium natural zero-calorie sweeteners in North American retail and b2b formulations | +2.4% | United States and Canada | Short to medium term (≤ 4 years) |

| High-performance blends with allulose, stevia, and soluble fiber | +1.5% | United States (core), Canada (secondary) | Medium term (2-4 years) |

| Adoption in keto, low-carb, and diabetic-friendly products | +1.9% | United States | Short term (≤ 2 years) |

| Monk fruit use in beverages, dairy, and nutritional supplements | +2.0% | United States and Canada | Short term (≤ 2 years) |

| Technical service, application support, and custom sweetening systems | +0.7% | North America-wide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Clean-label sugar reduction in food and beverage reformulation

Regulatory pressure on added sugars, including the FDA's updated Nutrition Facts labeling requirements and increasing state-level discussions on sugar taxes, has created a structural shift in ingredient procurement priorities for large food and beverage companies. Mogroside V contains no carbohydrates associated with traditional sugars, allowing formulators to make zero-calorie claims without using artificial additives. Stevia offers a similar positioning advantage, but monk fruit often benefits from a more favorable consumer taste perception. Cargill's October 2025 consumer research found that buyers are willing to pay 10% more for beverages labeled “naturally sweetened,” signaling a premium opportunity that is encouraging brands to reformulate with monk fruit and stevia combinations. This regulatory driver affects both the FDA and the Canadian Food Inspection Agency, as Canada's Food Labeling Modernization Regulations are increasing scrutiny of added sugar declarations and creating parallel compliance pressure across the two primary North American markets.

Adoption in keto, low-carb, and diabetic-friendly products

The keto and low-carb dietary segment maintains a demand floor for monk fruit sweeteners that differs qualitatively from broader health-and-wellness trends. It drives repeat purchases among a loyal, higher-spending consumer cohort that makes dietary choices with near-clinical precision around glycemic impact. Monk fruit’s zero glycemic index, validated under the FDA GRAS framework and supported by its non-glycemic mogroside V profile, makes it well-suited for diabetic-friendly and keto formulations, as it does not trigger an insulin response. Lakanto is expected to launch a proprietary golden monk fruit sweetener with allulose in 2025, specifically engineered for browning and caramelization in commercial bakery and home cooking applications[2]Source: Lakanto, “Lakanto Product Disclosures,” Lakanto, lakanto.com. A peer-reviewed study scheduled for publication in the Journal of Drug Delivery and Therapeutics in February 2026 is expected to demonstrate the successful formulation of a monk fruit extract-based zero-calorie electrolyte replenisher powder for diabetic, keto, and athletic users, highlighting the expanding application range beyond tabletop sweeteners.

Monk fruit use in beverages, dairy, and nutritional supplements

Beverages are expected to be the largest demand generator, accounting for 43.62% of the North American market in 2025. A less-examined factor is the growing preference for liquid monk fruit concentrate over dry powder in beverage manufacturing lines. Liquid formats enable sweetness adjustment through in-line dosing systems, reducing batch variability during continuous production. This operational advantage is reshaping how ingredient buyers negotiate procurement specifications, as liquid-format suppliers secure more stable, long-term supply relationships once dosing equipment is calibrated to a specific extract grade. Layn Natural Ingredients is expected to expand its monk fruit portfolio in 2026 with monk fruit decoction in powder and liquid formats, responding to demand from global brands for clean-label, fruit-derived sweetening solutions that offer broader formulation flexibility alongside high-purity extracts. The beverage market also serves as a consumer education channel, as front-of-pack monk fruit claims on mainstream ready-to-drink products build ingredient familiarity and subsequently drive retail tabletop sweetener sales in the same geography.

High-performance blends with allulose, stevia, and soluble fiber

The most commercially significant trend in North America's monk fruit market is the use of synergistic blends of mogroside V with stevia Reb M, allulose, or erythritol, rather than standalone monk fruit. These combinations improve the sweetness curve and reduce the aftertaste limitations of individual high-intensity sweeteners while maintaining a clean-label status. The blends are commoditizing plain mogroside extract and creating proprietary differentiation at the formulation layer. This structural shift favors integrated suppliers with application laboratory infrastructure over pure-play raw material distributors. In March 2026, Tate & Lyle and Manus Bio are expected to jointly launch the Yume sweetener brand, with initial products targeting beverage and dairy applications through precisely engineered monk fruit and stevia synergies. In March 2024, ADM launched a monk fruit-stevia blend line specifically formulated for beverage applications, indicating that major ingredient companies have moved from exploratory positioning to committed product lines in this category[3]Source: Archer Daniels Midland, “ADM Press Release, March 2024,” ADM, adm.com.

Restraints Impact Analysis*

| Restraint | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Concentrated raw material supply chain tied to southern China cultivation | -1.8% | Global, particularly North American importers | Long term (≥ 4 years) |

| High ingredient cost versus mainstream sugar and some alternative sweeteners | -1.3% | North America-wide | Medium term (2-4 years) |

| Batch-to-batch taste and Mogroside profile variability | -0.9% | United States (B2B manufacturing channel) | Short to medium term (≤ 4 years) |

| Limited consumer familiarity compared with better-known sweetener alternatives | -1.2% | United States (mass-market) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Concentrated raw material supply chain tied to southern China cultivation

Monk fruit cultivation remains structurally limited to a narrow geographic belt centered in the Guangxi Zhuang Autonomous Region of southern China, which accounts for over 90% of global raw fruit production. The crop requires a 3–5-year maturation cycle, preventing growers from rapidly expanding cultivation acreage in response to demand spikes and creating supply-side inelasticity that contractual hedging cannot fully offset. A peer-reviewed analysis in Foods (MDPI, 2025) notes that this geographic concentration exposes North American buyers to phytosanitary disruptions and geopolitical trade interventions at a severity level not seen in any other major high-intensity sweetener. Guilin-based extractors reported in 2025 that they had independently developed advanced extraction technologies and held over 130 global patents to maintain export competitiveness despite trade uncertainties between China and the United States. The USDA organic and NSF International supply-chain certification frameworks further increase audit costs and lead times for importers sourcing from this geographically concentrated supply base.

High ingredient cost versus mainstream sugar and some alternative sweeteners

Monk fruit extract remains significantly more expensive per unit of sweetness than stevia or sucralose, creating a cost barrier in segments where price-sensitive reformulation decisions drive procurement. Extracting high-purity mogroside V requires capital-intensive chromatographic separation and spray-drying processes, which remain concentrated among a few large Chinese processors. This oligopolistic upstream structure limits price negotiation leverage for North American buyers. For mid-sized food manufacturers, this cost barrier often results in blended formulations, with mogroside V used at minimal inclusion rates alongside lower-cost bulking sweeteners such as erythritol. This approach can weaken the clean-label positioning that initially justified the sourcing decision. The tariff environment between the United States and China during 2025-2026 may further increase import costs for monk fruit ingredients, compounding the existing cost disadvantage relative to sweeteners with more geographically diversified supply chains. It may also create a secondary competitive disadvantage that the industry is beginning to address through domestic fermentation-based production.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Liquid Formats Gain Ground in Precision Beverage Manufacturing

The dry form is expected to account for 63.71% of the North America monk fruit sweeteners market in 2025, reflecting its dominance across tabletop sweeteners, dry-mix protein supplements, baked goods, and bakery formats, where flowability and shelf stability are critical. Dry monk fruit, typically spray-dried mogroside V powder blended with a carrier such as erythritol or inulin, supports easy handling and precise dosimetry in high-throughput manufacturing. Although liquid monk fruit is expected to hold a smaller share, it is projected to register a CAGR of 13.96% from 2026 to 2031. Beverage manufacturers are driving this growth due to their preference for aqueous concentrates in RTD teas, flavored waters, and carbonated soft drinks, where dissolution uniformity and real-time sweetness adjustment are essential production requirements. Layn Natural Ingredients’ planned 2026 expansion into monk fruit decoction in liquid format, standardized to 1%–3% mogroside V, directly addresses global brand demand for fruit-derived sweetening solutions that offer formulation flexibility beyond high-purity extraction premiums. As the beverage industry moves toward personalized sugar-reduction targets and continuous dosing technology, the liquid form is likely to progressively reduce the dry segment’s share through 2031.

A less-examined dynamic within form segmentation is that liquid monk fruit formats generate higher margins for ingredient suppliers despite representing lower-purity grades than concentrated dry extracts. Beverage co-manufacturers that standardize liquid dosing systems create equipment-calibrated switching costs within their procurement structures, resulting in long-term supplier relationships that bulk dry-powder distributors struggle to replicate. The FDA’s GRAS classification applies equally to aqueous and powdered monk fruit extracts, providing the regulatory certainty manufacturers need to transition between forms without triggering new compliance reviews. This distinction is practically important as supply chain optimization drives format switching.

By Category: Organic Premiumization Reshapes Competitive Positioning

Conventional monk fruit sweeteners are expected to maintain an 81.79% market share in 2025, supported by their cost advantage and wider availability across mass-market retail and B2B ingredient distribution. The conventional category’s dominance reflects the added cost burden of USDA organic-certified raw fruit processing, which significantly increases upstream cost structures. As a result, organic monk fruit remains concentrated in premium retail formats, nutraceutical applications, and brands that require certified-natural positioning. However, the organic segment is projected to register a 14.81% CAGR from 2026 to 2031, the highest across all segmentation categories in this market. This growth signals a systematic shift in brand-owner procurement toward organic monk fruit as clean-label certification requirements move into major retailers’ private-label specifications. Guilin Layn Natural Ingredients’ SAI Gold certification from the Sustainable Agriculture Initiative for its monk fruit products reflects the supply-side response to organic premiumization. The certification provides documented farm-level sustainability credentials, supports upstream regulatory compliance, and strengthens traceability claims for North American buyers.

The organic segment’s rapid growth carries a second-order implication. As organic specifications become a default requirement for premium retail shelf access, conventional monk fruit suppliers without organic certification face a rising risk of channel exclusion in the natural and specialty grocery segment. Pyure Brands’ organic monk fruit sweetener line and Lakanto’s organic product offerings are early examples of retail-facing brands that have built category positioning around organic certification. These brands are shaping consumer expectations that conventional-only suppliers may struggle to address in premium channels. This bifurcation is likely to accelerate during the forecast period as private-label product specifications at major natural grocery retailers increasingly require certified organic sourcing from monk fruit ingredient suppliers.

By Application: Nutritional Supplements Emerge as the High-Growth Adjacency

Beverages are expected to command a 43.62% share of the North America monk fruit sweeteners market in 2025. This dominance is supported by mogroside V's clean taste profile at low inclusion rates, broad solubility across cold and hot liquid formats, and lack of the persistent aftertaste that limits stevia's use in complex flavor systems, such as carbonated beverages. Dairy products, bakery products, confectionery, and sauces and dressings form a secondary demand base, supported by monk fruit's strong heat stability. Mogroside V does not degrade or lose sweetness potency during pasteurization or baking, which enables its use in processed formats that restrict many other high-intensity sweeteners. Other applications, including confectionery and bakery, are increasingly adopting monk fruit-allulose blends that replicate sucrose's browning behavior in Maillard reactions, addressing a functional gap that previously limited monk fruit to beverages and cold formats.

Nutritional supplements are projected to be the fastest-growing application, registering a CAGR of 13.42% from 2026 to 2031. This growth reflects a deeper shift in consumer behavior, as supplement buyers accept substantially higher ingredient premiums for zero-calorie, zero-glycemic sweeteners than food and beverage buyers. This creates a margin-expansion opportunity that differs from the commodity dynamics of beverage reformulation. Functional powder formats, electrolyte replenishers, protein blends, and adaptogen mixes are systematically replacing sucrose- and maltodextrin-based carriers with monk fruit and stevia combinations to maintain clean-label positioning in a product category where ingredient scrutiny remains unusually high. The FDA GRAS classification for monk fruit mogrosides provides regulatory confidence, allowing supplement-grade monk fruit to support on-pack claims without pre-approval delays and giving it a competitive advantage over novel food ingredients that are still navigating GRAS notification timelines.

Geography Analysis

The United States is projected to hold 79.1% of the monk fruit sweeteners market share in 2025, keeping it well ahead of every other geography in the region. This leadership is supported by clear regulatory treatment, strong retail infrastructure, and a long product launch runway following the FDA’s GRAS position on monk fruit mogrosides. In the monk fruit sweeteners market, regulatory clarity has supported more than a decade of growth across beverages, supplements, and tabletop products, improving consumer familiarity and retailer acceptance. The US market now shows a split growth pattern, with branded retail channels expanding steadily while the industrial ingredient channel grows faster through large-scale reformulation by food manufacturers. This industrial momentum is important because it shifts revenue toward B2B supply agreements, technical support, and application-specific sweetening systems, rather than only finished retail packs.

Canada and Mexico represent two distinct secondary demand profiles within the monk fruit sweeteners market. Canada benefits from a policy direction that favors healthier eating patterns and sugar reduction, creating a regulatory backdrop aligned with the broader clean-label movement across North America. Mexico is the fastest-growing geography, with a projected CAGR of 13.9% from 2026 to 2031. This momentum is directly tied to front-of-pack warning labels, which increase reformulation pressure on beverage and confectionery makers. In practice, the monk fruit sweeteners market in Mexico benefits from a more urgent need to avoid warning-label outcomes that can weaken shelf appeal and brand competitiveness. A younger urban consumer base and continued growth in modern retail further support this trend, helping explain why Mexico is expanding faster than the rest of the region.

The remaining regional demand base follows a different pattern, as smaller markets access monk fruit products mainly through broader natural sweetener distribution systems rather than direct extraction-stage sourcing. This gives them exposure to the monk fruit sweeteners market, but usually with a lag behind the US retail cycle and without the same industrial scale. Certification continues to shape shelf placement across the region, as products with credible sourcing documentation are more likely to secure mainstream retail acceptance. Academic and educational communication around monk fruit’s metabolic profile is also gradually widening awareness, supporting broader consumer pull over time. Even so, the regional picture remains uneven, and the monk fruit sweeteners market continues to depend most heavily on the United States for scale and on Mexico for the fastest incremental growth.

Competitive Landscape

The North America monk fruit sweeteners market has a moderately consolidated structure at the ingredient supply level. Archer Daniels Midland, Cargill, Ingredion, and Tate & Lyle exert a strong influence by combining broad distribution reach, established customer relationships, and formulation support that smaller suppliers often struggle to match. In the monk fruit sweeteners market, these companies compete less on basic extract pricing and more on supply assurance, regulatory documentation, and the ability to address specific formulation challenges for B2B buyers. This positioning gives large integrated suppliers an advantage when food and beverage manufacturers seek to reduce risk during sweetener transitions. Specialist players and retail-facing brands remain relevant, although they typically have stronger differentiation opportunities in premium niches than in large-scale ingredient supply.

A major structural shift is expected as domestic fermentation-based production enters a category that has historically depended on agricultural supply from southern China. Manus Bio’s planned June 2026 commercial launch of a United States-produced, fermentation-based monk fruit sweetener at its Augusta, Georgia, facility is expected to introduce a domestic supply option for North American manufacturers. This development matters because it may reduce exposure to tariffs, harvest disruptions, and concentrated farm supply, all of which have influenced purchasing risk in the monk fruit sweeteners market. It also shifts the competitive discussion from simple sourcing access to production model choice, as agricultural extraction and bio-based manufacturing compete within the same value chain. Tate & Lyle’s planned March 2026 partnership with Manus to launch the Yume sweetener brand indicates that established suppliers are aligning with this shift rather than waiting for it to challenge them externally.

Competitive strategy is also becoming more application-led across the monk fruit sweeteners market. ADM’s 2024 launch of a beverage-focused monk fruit and stevia blend demonstrates how large suppliers are building product lines around use-case performance instead of selling monk fruit only as a standalone ingredient. Lakanto’s planned 2025 golden monk fruit sweetener with allulose reflects the same approach at the product level by targeting browning and caramelization outcomes that matter in baking and cooking. These moves suggest that the monk fruit sweeteners market rewards suppliers and brands that connect sweetness delivery to practical formulation challenges. Overall, competition is not fragmented enough to resemble a commodity market, but it is also not concentrated enough for a few players to control demand without continued innovation and supply investment.

North America Monk Fruit Sweeteners Industry Leaders

Archer Daniels Midland Company

Cargill, Incorporated

Ingredion Incorporated

Tate & Lyle PLC

GLG Life Tech Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2026: Layn Natural Ingredients expanded its monk fruit decoction portfolio at IFT FIRST 2026 in Chicago, with powder and liquid formats standardized to 1%–3% Mogroside V. The launch highlighted the company’s strategy to broaden monk fruit’s formulation applicability beyond high-purity extract formats for global food, beverage, and nutraceutical brands.

- June 2026: Manus Bio unveiled the first monk fruit sweetener produced at a commercial scale in the United States through industrial fermentation at its biofacility in Augusta, Georgia. The ingredient used more than 30 enzymatic steps to produce mogroside V domestically, reducing dependence on China’s single-region agricultural supply. The product completed the FEMA GRAS review (FEMA No. 5108), and an FDA GRAS Notification was in progress.

- March 2026: Tate & Lyle and Manus Bio jointly launched the Yume sweetener brand, targeting beverage and dairy applications by combining engineered monk fruit and stevia. Manus Bio produced the first Yume product, Yume M, at its Augusta biofacility using fermentation-based stevia Reb M technology.

North America Monk Fruit Sweeteners Market Report Scope

Monk fruit sweeteners are natural, zero-calorie sugar substitutes extracted from the Southeast Asian Siraitia grosvenorii fruit, also known as luo han guo. The North America monk fruit sweeteners market report is segmented by form, category, application, and geography. By form, the market is segmented into liquid and dry. By Category, the market is segmented into conventional and organic. By application, the market is segmented into beverages, dairy products, nutritional supplements, bakery products, confectionery, sauces and dressings, and other applications. By geography, the market is segmented into the United States, Canada, Mexico, and the Rest of North America. The market forecasts are provided in terms of value (USD).

| Liquid |

| Dry |

| Conventional |

| Organic |

| Beverages |

| Dairy Products |

| Nutritional Supplements |

| Bakery Products |

| Confectionery |

| Sauces and Dressings |

| Other Applications |

| United States |

| Canada |

| Mexico |

| Rest of North America |

| Form | Liquid |

| Dry | |

| Category | Conventional |

| Organic | |

| Application | Beverages |

| Dairy Products | |

| Nutritional Supplements | |

| Bakery Products | |

| Confectionery | |

| Sauces and Dressings | |

| Other Applications | |

| Geography | United States |

| Canada | |

| Mexico | |

| Rest of North America |

Key Questions Answered in the Report

What is the 2031 outlook for North America monk fruit sweeteners?

The North America monk fruit sweeteners market is forecast to reach USD 747.81 million by 2031 from USD 411.2 million in 2026, growing at a 12.71% CAGR from 2026 to 2031.

Which application drives the most revenue for monk fruit sweeteners in North America?

Beverages are the largest application, accounting for 43.62% of revenue in 2025 because manufacturers are using monk fruit in reformulated zero-calorie and reduced-sugar drinks.

Why is Mexico growing faster than other countries in the region?

Mexico is projected to grow at a 13.93% CAGR through 2031 because front-of-pack warning label rules are pushing faster reformulation in beverage and confectionery products.

Which form is growing fastest in monk fruit sweeteners?

Liquid monk fruit sweeteners are the fastest-growing form, with a projected 13.96% CAGR through 2031, supported by beverage producers that use in-line dosing systems.

Page last updated on: