North America Manufacturing Automation Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

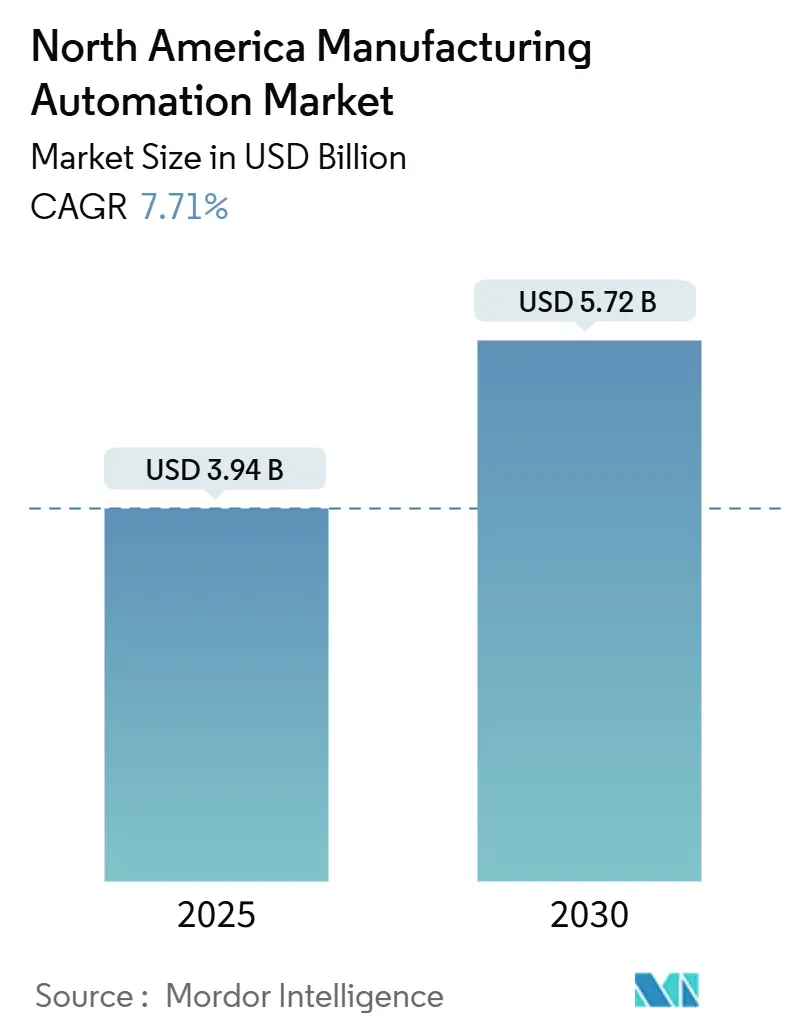

| Market Size (2025) | USD 3.94 Billion |

| Market Size (2030) | USD 5.72 Billion |

| Growth Rate (2025 - 2030) | 7.71% CAGR |

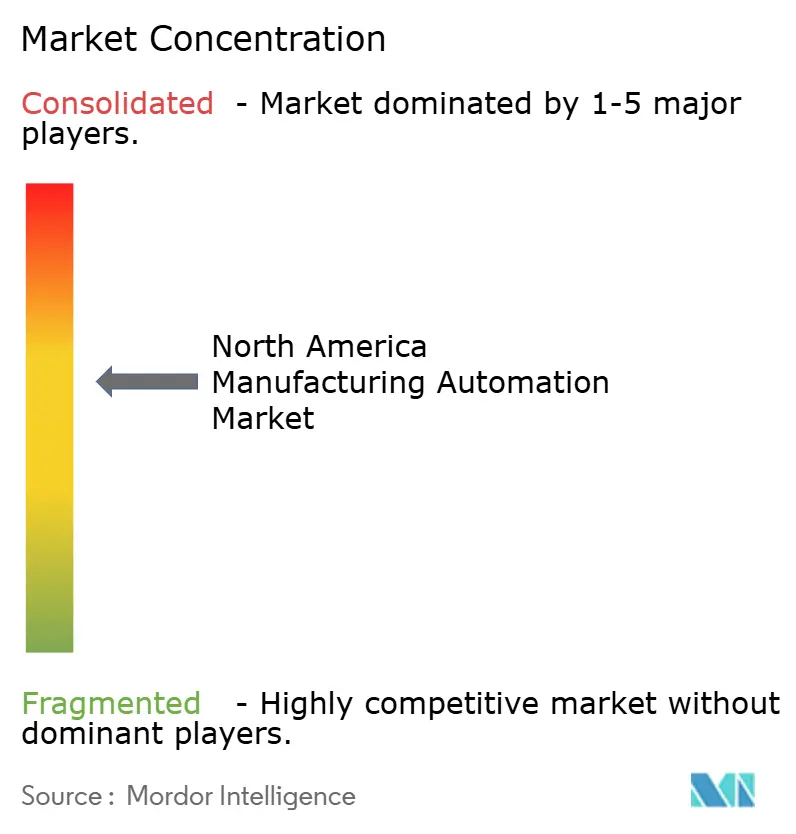

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Manufacturing Automation Market Analysis by Mordor Intelligence

The North America manufacturing automation market size is valued at USD 3.94 billion in 2025 and is projected to reach USD 5.72 billion by 2030, reflecting a 7.71% CAGR. Makers across the automotive, electronics, and process industries increasingly view automation as a strategic hedge against skilled labor scarcity and a prerequisite for reshoring. Hardware remains the principal expenditure because production lines often require complete retrofits rather than piecemeal upgrades; yet, cloud-native software platforms are experiencing the most rapid uptake as firms demand real-time analytics and predictive maintenance. Federal incentives under the CHIPS and Science Act and the Inflation Reduction Act lower effective ownership costs for capital equipment, reinforcing the economic case for advanced robotics and sensor networks. Mexico’s nearshoring boom and Canada’s SME-focused excellence centers demonstrate that automation is no longer a U.S.-only story, even though domestic manufacturers still account for the majority of spending. Vendor strategies now prioritize secure, unified platforms capable of managing legacy controllers alongside IoT endpoints, because cyber risk is rising in tandem with connectivity.

Key Report Takeaways

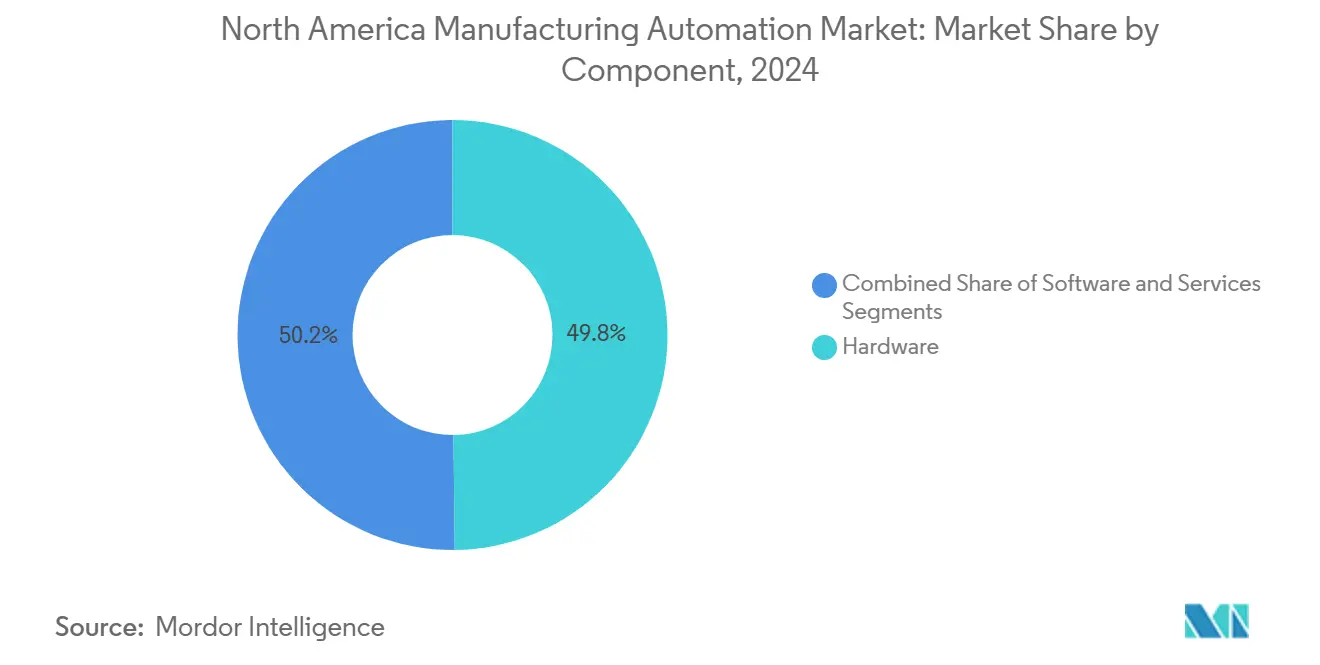

- By component, hardware accounted for 49.84% of the North America manufacturing automation market share in 2024; software solutions are expected to expand at a 7.91% CAGR through 2030.

- By automation type, fixed (discrete) automation systems accounted for 42.77% of the North America manufacturing automation market share in 2024, while flexible and soft automation is forecast to advance at an 8.11% CAGR through 2030.

- By end user, the automotive sector led with a 42.79% share of the North America manufacturing automation market size in 2024, whereas electronics and semiconductor manufacturing is expected to post an 8.79% CAGR through 2030.

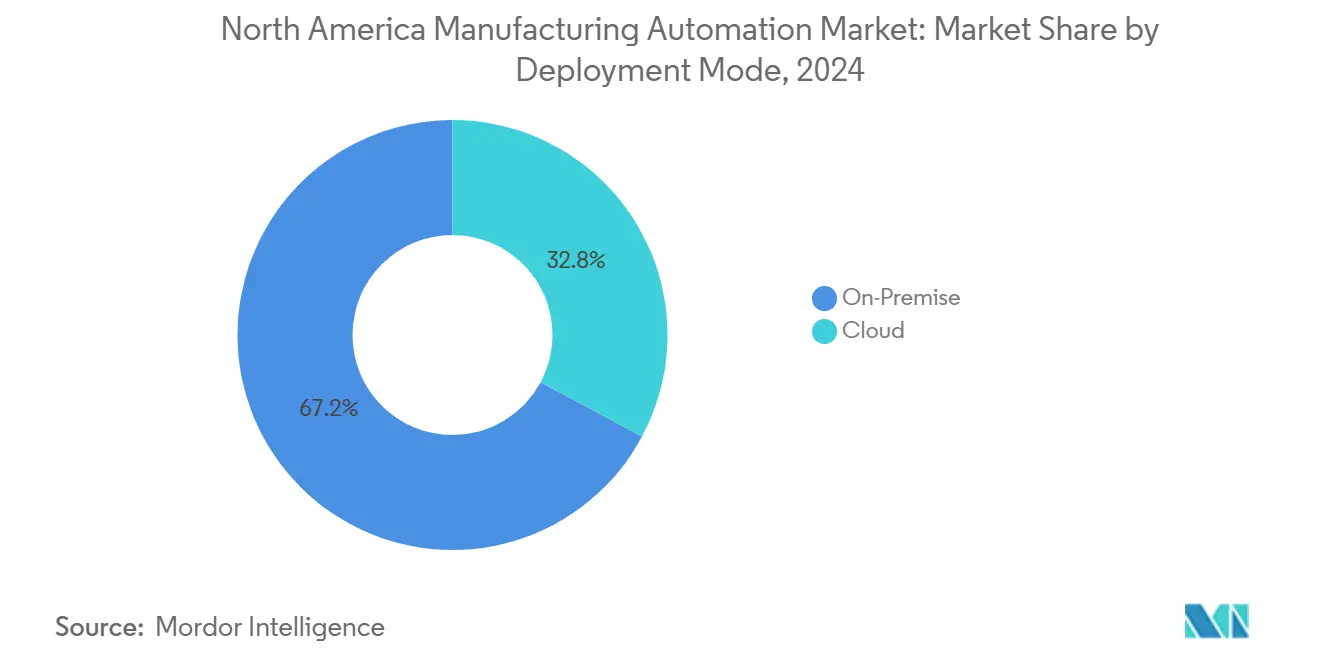

- By deployment mode, on-premise installations accounted for 67.18% share of the North America manufacturing automation market size in 2024, while cloud deployment is expected to grow at an 8.09% CAGR over the forecast horizon.

- By geography, the United States accounted for 78.19% share of the North America manufacturing automation market size in 2024; Mexico is poised for the fastest growth, with an 8.67% CAGR to 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Manufacturing Automation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated Adoption of Industrial IoT and Smart Sensor Networks | +1.8% | United States and Canada, spillover to Mexico | Medium term (2-4 years) |

| Government Incentives for Reshoring and Advanced Manufacturing | +2.1% | United States, selective programs in Canada | Short term (≤ 2 years) |

| Rising Labor Cost and Skilled Worker Shortages in North America | +1.6% | All North American markets, most acute in United States | Long term (≥ 4 years) |

| Demand for Mass Customization and Flexible Production Lines | +1.4% | United States and Mexican corridors | Medium term (2-4 years) |

| Integration of Edge AI for Real-Time Quality Control | +1.2% | United States and Canada advanced hubs | Long term (≥ 4 years) |

| Tax Incentives for Energy-Efficient Automation Equipment | +0.9% | United States federal and state, Canada provincial | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerated Adoption of Industrial IoT and Smart Sensor Networks

North American factories deploy dense sensor arrays to capture temperature, vibration, and throughput data, enabling predictive maintenance that cuts unplanned downtime by as much as 35%.[1]Rockwell Automation, “Rockwell Automation Announces New Industrial IoT Platform,” rockwellautomation.com Edge-processing modules route critical insights directly to programmable logic controllers, which maintain millisecond response times needed in automotive paint lines and semiconductor lithography. Interoperability standards such as OPC-UA now bridge newer sensor suites with installed SCADA assets, resolving integration obstacles that once deterred mid-tier plants. Falling silicon costs reduce payback periods for smart-sensor retrofits to under two years, a threshold that CFOs are increasingly accepting. Smaller firms move from pilot projects to plant-wide rollouts after seeing tangible energy savings and scrap reduction. Vendors that bundle hardware, analytics, and cybersecurity monitoring position themselves as single-invoice partners, an attractive model for resource-constrained operations teams.

Government Incentives for Reshoring and Advanced Manufacturing

The CHIPS and Science Act allocates USD 52.7 billion to semiconductor capacity, with funds explicitly tied to the purchase of advanced automation tools. States such as Texas and Ohio offer additional tax credits for energy-efficient robots, reducing the after-tax cost of a six-axis unit by up to 30%. Accelerated depreciation on qualifying machinery further improves internal-rate-of-return metrics, motivating manufacturers to pull forward capital projects scheduled for later years. Similar but smaller initiatives in Ontario and Quebec leverage shared robotics cells at excellence centers, enabling SMEs to access world-class tools without full ownership. Because certain U.S. credits begin phasing out after 2027, integrators are reporting an order surge as customers rush to secure delivery slots. The temporary nature of the incentives concentrates demand in the near term, propelling double-digit growth in orders for motion-control vendors.

Rising Labor Cost and Skilled Worker Shortages in North America

Open manufacturing positions exceeded 2.1 million in 2024, while the average hourly wage for skilled technicians increased by 6.2% year over year.[2]U.S. Bureau of Labor Statistics, “Job Openings and Labor Turnover Summary,” bls.gov Retirement-driven attrition outpaces new entrants, forcing managers to reconfigure lines around automated stations that need fewer operators. Community colleges are expanding their robotics curricula, yet certification programs can take up to two years, which is longer than most automation system commissioning cycles. Consequently, boardrooms increasingly view capital outlays as the only scalable response to workforce tightness. Automated guided vehicles now backfill logistics tasks once performed by forklift drivers, freeing scarce labor for quality roles. Payroll stability also aids long-term cost planning, which appeals to publicly listed manufacturers under pressure to defend margins.

Demand for Mass Customization and Flexible Production Lines

Consumer expectations for personalized vehicles, appliances, and electronics are compressing product lifecycles, compelling factories to handle frequent model changes without extended downtime. Flexible automation platforms reconfigure tooling via software, supporting economically viable batch sizes as low as 50 units. Automotive seat plants, for example, now sequence frames in real time based on dealership orders delivered minutes earlier, a workflow made feasible through adaptive robots and quick-release end-effectors. Machine learning schedulers balance part-mix complexity with takt-time constraints, trimming work-in-progress inventory. Electronics assemblers similarly adopt reconfigurable feeder carts that adapt to short-run PCB revisions. The resulting operational agility opens premium-pricing niches, offsetting the higher capital cost of flexible cells.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Capital Expenditure for SMEs | -1.4% | United States and Canada SME sectors, limited Mexico impact | Medium term (2-4 years) |

| Cybersecurity Vulnerabilities in Connected Production Systems | -1.1% | All North American markets, most critical in United States | Short term (≤ 2 years) |

| Interoperability Challenges Among Legacy and Modern Equipment | -0.8% | United States and Canada mature regions | Long term (≥ 4 years) |

| Supply Chain Disruptions for Semiconductor Components | -0.9% | All North American markets, acute in electronics plants | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront Capital Expenditure for SMEs

Comprehensive robot-based line upgrades cost between USD 2.5 million and USD 5.0 million, equating to as much as 25% of annual revenue for many mid-sized firms.[3]U.S. Small Business Administration, “SBA Announces New Funding Opportunities for Small Manufacturers,” sba.gov Conventional loan products rarely align with the depreciation profile of automation hardware, forcing owners to pledge real estate or provide personal guarantees. While leasing programs exist, they often exclude installation and integration costs, leaving firms to fund essential engineering services out of pocket. Fragmented federal and provincial grants provide partial relief, yet they typically require lengthy applications that discourage first-time adopters. Vendors offering outcome-based financing, where payments align with realized productivity gains, are gaining traction but remain a niche market. Without broader financial innovation, SME adoption curves risk lagging large-enterprise trends.

Cybersecurity Vulnerabilities in Connected Production Systems

Manufacturing ransomware events increased by 87% in 2024, with the average recovery expense reaching USD 3.2 million per incident. Expanded connectivity introduces previously isolated programmable controllers to external networks, enabling threat actors to halt conveyors, tamper with batch recipes, or exfiltrate proprietary CAD files. Insurance exclusions for operational-technology downtime leave many plants bearing the full impact of an outage. Security patching cycles struggle to keep pace with production schedules, since firmware updates often necessitate planned line shutdowns. Integrators now pitch zero-trust architectures and segmented networks as core requirements, yet incremental cybersecurity spending competes with visible ROI from new robots. Until risk frameworks become standard, board-level apprehension will continue to temper deployment velocity in highly regulated sectors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Hardware Spending Anchors Conversion Projects

Hardware captured 49.84% of the North America manufacturing automation market share in 2024, reflecting the need to replace aging conveyance, vision, and motion-control gear rather than merely layering software onto outdated assets. The North America manufacturing automation market size allocated to hardware reached USD 1.96 billion in 2024 and continues to rise as electric-vehicle plants specify high-payload robots for battery assembly lines. Edge controllers embedded in new drives handle deterministic control locally, reducing reliance on plant servers and minimizing latency during toolpath adjustments. Growth in software, however, outpaces hardware because subscription-based analytics platforms offer lower entry points and immediate diagnostics, encouraging even capital-constrained facilities to experiment with data-driven workflows.

Service providers benefit from the complexity of multi-vendor environments; integration services now bundle mechanical installation, network design, and cybersecurity hardening. Outcome-based contracts tie monthly fees to throughput or yield targets, shifting risk from the manufacturer to the service partner. Hardware manufacturers are increasingly preloading digital twins of their equipment, enabling rapid commissioning and remote troubleshooting. These twins, coupled with augmented-reality guidance, shrink maintenance windows and free up limited technical staff for higher-value tasks. As a result, many plants opt for vendor-managed maintenance, ensuring uptime without expanding internal headcount.

By Automation Type: Shift Toward Flexible and Soft Systems

Fixed automation retained 42.77% of the revenue in 2024 and remains entrenched in high-volume paint shops and bottling lines, where product variety is minimal. Still, flexible and soft automation posts an 8.11% CAGR, signaling a structural pivot in the North America manufacturing automation market. Programmable automation sits between the two extremes, letting firms amortize tooling over multiple part numbers while avoiding the engineering intensity of full flexibility.

Flexible systems integrate vision-guided robots that adjust grip points on the fly, making them ideal for electronics plants that deal with rapid SKU churn. Cloud-based scheduling engines model thousands of potential sequences, selecting an optimal path that maximizes spindle utilization while ensuring job due dates are not violated. This adaptability underpins mass-customization strategies highlighted in direct-to-consumer auto trim packages and bespoke kitchen appliances. Meanwhile, soft automation, exemplified by collaborative robots, penetrates manual assembly cells because it requires minimal guarding and is redeployable. Manufacturers thus move closer to one-piece flow without sacrificing floor space efficiency.

By End User Industry: Electronics Leads Growth Trajectory

Automotive lines still account for 42.79% of spending, buoyed by electric-vehicle drivetrain programs that require specialized torque and dispensing applications. The North America manufacturing automation market size tied to electronics and semiconductor plants, though smaller today, is on track to expand at an 8.79% CAGR as reshoring subsidies mature. Cleanroom-rated robots that minimize particle shedding are dominating new wafer-fab procurement lists, while high-speed surface-mount machines incorporate AI vision to detect solder defects during paste inspection.

Food and beverage processors automate end-of-line packaging to satisfy retailer traceability mandates, and stainless-steel hygienic designs cut sanitization downtime. Metals and machinery shops utilize large-format cobots for grinding and deburring, replacing repetitive manual tasks that often lead to ergonomic injuries. Pharmaceutical plants integrate serial-number printing and in-line inspection to comply with federal drug supply chain security regulations, pushing automation into upstream formulation suites as well.

By Deployment Mode: Cloud Momentum Builds Despite Control-Room Skepticism

On-premise installations accounted for 67.18% of 2024 turnover because critical motion loops and intellectual property reside within factory firewalls. Yet, cloud instances grow at an annual rate of 8.09%, thanks to the maturation of industrial-edge gateways that isolate deterministic control from analytics traffic. Software-as-a-service licenses eliminate large perpetual fees, an attractive shift for cash-conscious finance departments.

Hybrid approaches dominate greenfield builds: controllers and safety I/O remain in-plant, while historian data flows to cloud warehouses for KPI dashboards. Latency-sensitive tasks such as vision-guided pick-and-place stay local, while scheduling algorithms run in regional data centers overnight. Sectors governed by ITAR or GMP standards deploy private cloud nodes in colocation facilities to satisfy data sovereignty rules. Vendors differentiate on encryption strength and role-based access, positioning secure connectivity as a core selling point rather than an add-on.

By Enterprise Size: SMEs Close the Adoption Gap

Large enterprises controlled 58.32% of 2024 revenue, yet SMEs post a 7.97% CAGR, signaling democratization of advanced automation. Subscription robotics, pay-per-pick financing, and modular pallets enable small plants to deploy in stages, converting one work cell per quarter. Provincial grants in Canada cover up to 30% of qualifying hardware costs, while U.S. Manufacturing Extension Partnerships fund feasibility studies that derisk initial investments.

Ease-of-use gains also drive uptake: graphical drag-and-drop programming enables electricians, not only controls engineers, to reconfigure palletizing tasks after a product changeover. Vendors targeting SMEs provide all-inclusive kits that include a robot, gripper, vision system, and application templates, all delivered on a single skid. Remote support portals further reduce the total cost of ownership by resolving logic errors without dispatching a field technician. As SMEs embrace these models, overall unit volumes rise, lowering per-robot pricing and fueling a virtuous adoption cycle in the North America manufacturing automation market.

Geography Analysis

The United States generated 78.19% of 2024 automation revenue, reflecting both its large manufacturing base and the strength of federal funding vehicles aimed at domestic capacity expansion. Automakers in Michigan, battery plants in Ohio, and semiconductor fabs in Arizona spearhead high-ticket projects, often bundling robotics, automated material handling, and AI-enabled inspection. The North America manufacturing automation market size attributable to U.S. facilities is set to grow steadily as tier-one suppliers align with OEM localization mandates.

Canada follows a targeted model that concentrates resources in Ontario and Quebec, where manufacturing excellence centers lend robots and metrology equipment to consortium members. These centers accelerate prototype iteration and provide cybersecurity sandboxes that let SMEs validate cloud connectivity without jeopardizing production systems. Collaborative robotics gains particular momentum because Canadian safety regulations emphasize worker interaction, making cobots a natural fit for mixed-model assembly. Provincial tax credits, although smaller than U.S. stimulus, have narrow payback periods that are sufficient for many mid-market firms to proceed with phased rollouts.

Mexico records the fastest regional CAGR at 8.67%, catalyzed by nearshoring from electronics and appliance brands seeking to reduce trans-Pacific freight risks. Foreign direct investment approvals increasingly stipulate automation milestones to ensure export-grade quality and consistent takt times. Border states leverage their logistics proximity to U.S. distribution hubs, adopting high-speed sorters and vision systems that meet just-in-sequence delivery windows. Automation also helps offset rising wage floors by boosting labor productivity, enabling companies to maintain cost competitiveness while adhering to new labor-rights provisions in the USMCA trade pact.

Competitive Landscape

Incumbents such as ABB, Siemens, and Rockwell Automation leverage decades-old installed bases, extensive channel partners, and unified engineering suites to anchor their market positions. Each firm promotes integrated stacks that combine PLCs, drives, SCADA, and cybersecurity appliances, reducing vendor-management overhead for plant managers. Mid-cycle software updates now introduce AI modules that optimize axis paths and predict component wear, locking customers into multi-year support agreements.

Emergent challengers focus on cloud-first architectures and collaborative robotics, offering lower entry barriers and faster iteration cycles. Universal Robots popularized lightweight cobot arms that deploy without complex guarding, and numerous start-ups now supply plug-and-play grippers, expanding the application envelope. Edge AI start-ups are filing patents for inline defect detection, a category where USPTO data shows a 156% increase in 2024 filings for machine-vision inference models.

Strategic alliances shape the market: Rockwell’s acquisition of Clearpath Robotics folds autonomous mobile robots into its MES ecosystem, while Siemens bundles Digital Industries Software with its motion hardware to create closed-loop digital twins. Cybersecurity partnerships also proliferate, as OT-focused vendors integrate with IT security platforms to offer unified threat detection. Consolidation is likely because buyers prefer fewer interfaces across robotics, analytics, and security, amplifying the appeal of end-to-end suites.

North America Manufacturing Automation Industry Leaders

ABB Ltd.

Rockwell Automation Inc.

Siemens AG

Emerson Electric Co.

Schneider Electric SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Universal Robots and NVIDIA announced a partnership to embed GPU-accelerated vision processing in next-generation cobots, shortening pick-and-place cycle times in high-mix electronics production.

- May 2025: ABB launched its GoFa 20 collaborative robot model, featuring a 20 kg payload and built-in vision guidance designed for flexible assembly lines in small and medium enterprises.

- March 2025: Siemens opened an Edge Innovation Center in Austin, Texas, dedicated to co-developing AI-enabled quality-inspection applications with automotive and electronics manufacturers.

- January 2025: Rockwell Automation released its FactoryTalk Guardian cybersecurity suite, integrating real-time anomaly detection with automated incident response for industrial control systems across North American plants.

North America Manufacturing Automation Market Report Scope

| Hardware |

| Software |

| Services |

| Fixed (Discrete) Automation |

| Programmable Automation |

| Flexible and Soft Automation |

| Automotive |

| Electronics and Semiconductor |

| Food and Beverage |

| Metals and Machinery |

| Pharmaceuticals |

| On-Premise |

| Cloud |

| Large Enterprises |

| Small and Medium Enterprises |

| United States |

| Canada |

| Mexico |

| By Component | Hardware |

| Software | |

| Services | |

| By Automation Type | Fixed (Discrete) Automation |

| Programmable Automation | |

| Flexible and Soft Automation | |

| By End User Industry | Automotive |

| Electronics and Semiconductor | |

| Food and Beverage | |

| Metals and Machinery | |

| Pharmaceuticals | |

| By Deployment Mode | On-Premise |

| Cloud | |

| By Enterprise Size | Large Enterprises |

| Small and Medium Enterprises | |

| By Country | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

What is the current value of the North America manufacturing automation market?

The market stands at USD 3.94 billion in 2025 and is forecast to reach USD 5.72 billion by 2030.

Which component segment is expanding the fastest?

Software solutions, especially cloud-native platforms, are growing at a 7.91% CAGR through 2030.

Why is Mexico experiencing the highest growth rate?

Nearshoring investments and just-in-time export requirements drive an 8.67% CAGR for Mexican automation spending.

How do government incentives influence automation adoption?

U.S. federal and state tax credits reduce capital costs, accelerating investment timelines, especially in semiconductor and EV manufacturing.

What is the main barrier for small and medium manufacturers?

Upfront capital expenditures, ranging from USD 2.5 million to USD 5.0 million per line, challenge SMEs despite emerging financing options.

Which industry vertical is projected to record the fastest automation growth?

Electronics and semiconductor manufacturing is expected to expand at an 8.79% CAGR due to reshoring and cleanroom automation needs.

Page last updated on: