North America Irrigation Pumps Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

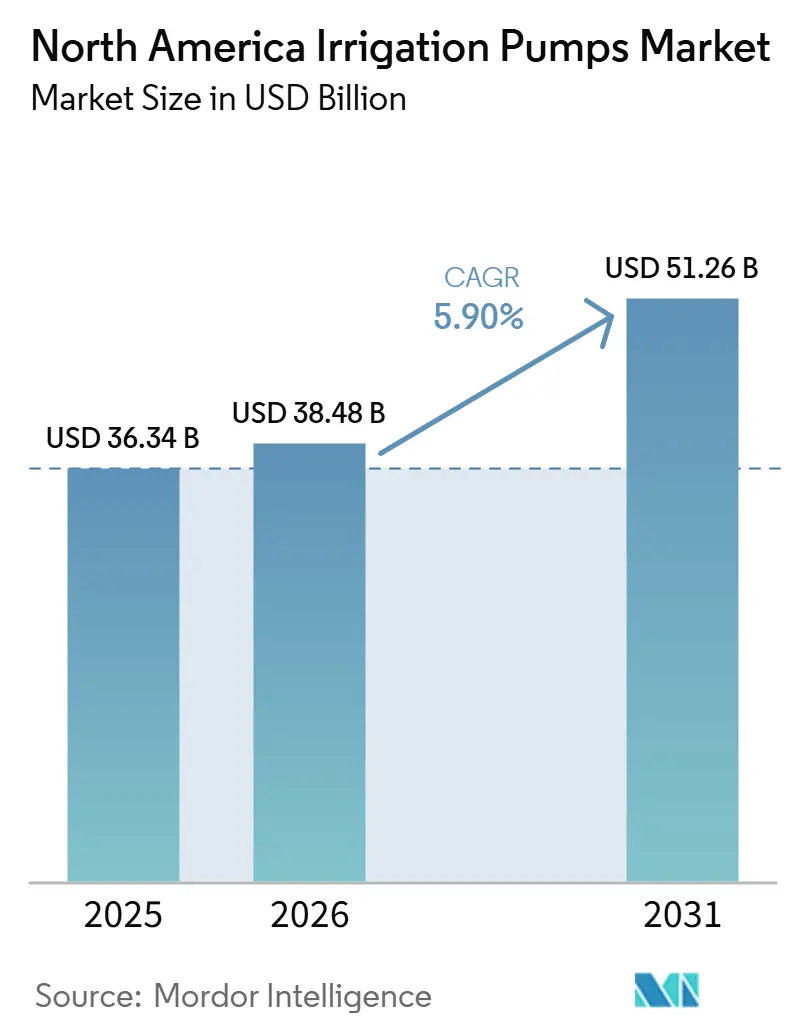

| Base Year Market Size (2025) | USD 36.34 Billion |

| Market Size (2026) | USD 38.48 Billion |

| Market Size (2031) | USD 51.26 Billion |

| Growth Rate (2026 - 2031) | 5.90% CAGR |

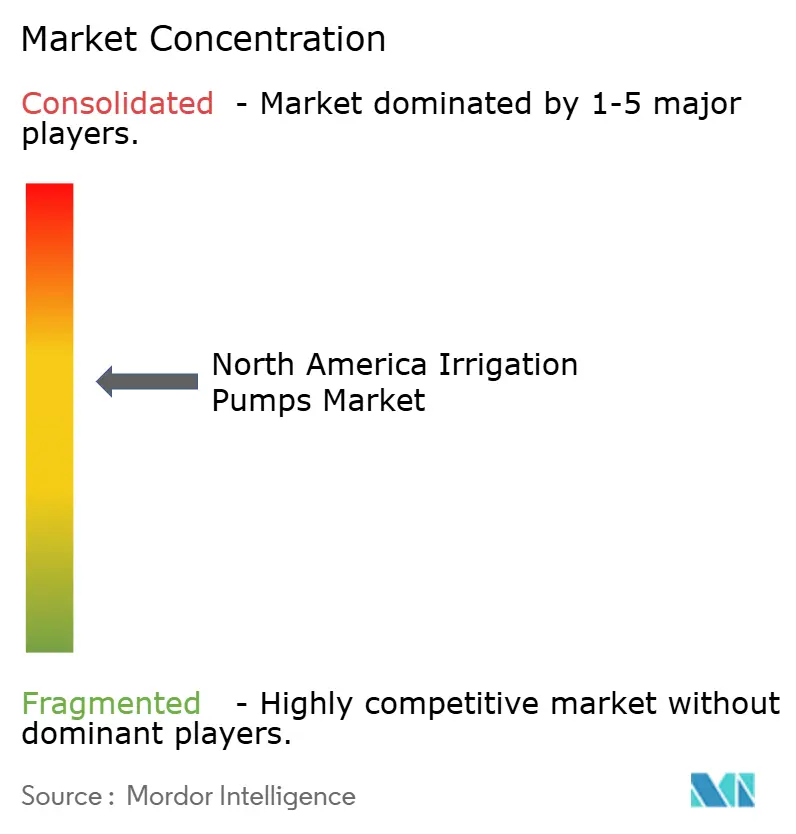

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America Irrigation Pumps Market Analysis by Mordor Intelligence

The North America irrigation pumps market size is projected to grow from USD 36.34 billion in 2025 and USD 38.48 billion in 2026 to USD 51.26 billion by 2031, registering a CAGR of 5.9% between 2026 and 2031. Increasing groundwater stress is driving higher investments in pumps, as irrigation accounts for 70% of groundwater withdrawals in the United States, making efficient pumping essential for farm output planning. Replacement demand is also rising due to public irrigation systems in the western United States entering a significant rehabilitation phase, supported by federal funding for pump plant and control system upgrades. Additionally, the market is benefiting from United States Department of Agriculture (USDA) grant and loan programs, which lower the installed cost of efficient equipment and enhance financing options for growers. In the North America irrigation pumps market, suppliers are increasingly focusing on variable-speed drives, monitoring systems, and service capabilities, elevating the standard product requirements in premium categories. The market also offers opportunities for suppliers that can integrate hardware with financing, software, and project support, particularly in alignment with regional modernization initiatives.

Key Report Takeaways

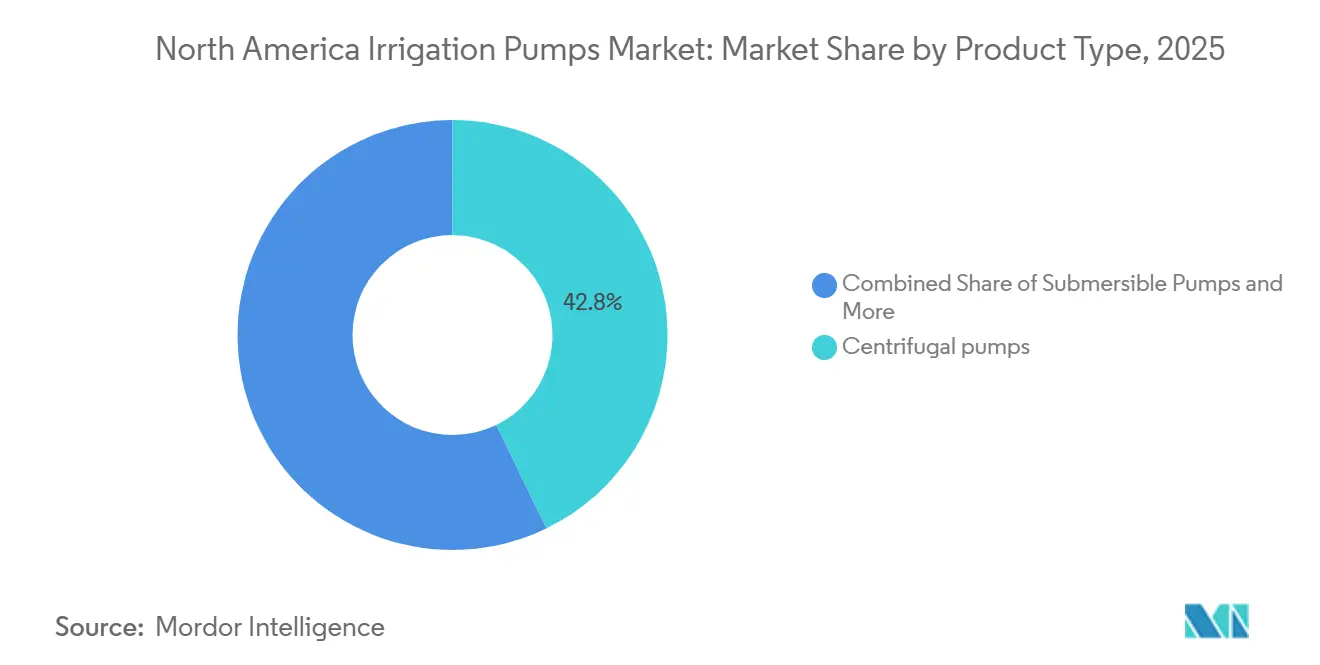

- By product type, centrifugal pumps accounted for 42.8% of the North America irrigation pumps market share in 2025, while submersible pumps are projected to grow at a CAGR of 7.6% between 2026 and 2031.

- By geography, the United States represented 71.4% of the North America irrigation pumps market size in 2025, while Mexico is anticipated to achieve the highest CAGR of 6.9% between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Irrigation Pumps Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Precision irrigation retrofits in water-stressed row crop operations | +1.4% | United States Great Plains and western states, with spillover to Mexico | Long term (≥ 4 years) |

| Solar-ready and hybrid pumping systems in off-grid farms | +0.9% | Off-grid agricultural areas in the United States and Mexico, and the Canadian prairie provinces | Medium term (2-4 years) |

| Replacement cycles from aging pump fleets in mature agricultural corridors | +1.1% | United States Midwest, Pacific Northwest, and Canadian prairies | Medium term (2-4 years) |

| Utility and state incentive programs for high-efficiency pumps | +0.8% | United States, especially California, Oregon, the Pacific Northwest, and the Midwest, with some relevance in Canada | Short term (≤ 2 years) |

| Climate volatility and flexible irrigation pressure management | +0.9% | North America, with stronger concentration in the United States Southwest and Great Plains | Long term (≥ 4 years) |

| Digital controls, remote monitoring, and variable-speed optimization | +0.7% | North America, with faster adoption in the United States and Canada | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expanding Precision Irrigation Retrofits in Water-Stressed Row Crop Operations

The demand for precision retrofit solutions is increasing rapidly in water-stressed row crop systems across the North America irrigation pumps market. This trend is driven by declining water tables, which are adding complexity to pumping operations. According to United States Geological Survey (USGS) monitoring, groundwater levels in certain areas of the High Plains Aquifer have dropped by over 100 feet, compelling growers in key irrigated states to upgrade their pumping systems to ensure stable water delivery at lower static water levels[1]Source: United States Geological Survey, "Groundwater Decline and Depletion,"usgs.gov. The USDA has reported that its Water-Saving Commodities partnerships aim to conserve up to 50,000 acre-feet of water across 250,000 irrigated acres. This initiative connects infrastructure modernization with program participation. Additionally, a 2024 GAO report indicates that 68% of large-scale United States crop-producing farms are utilizing precision technologies, driving retrofit demand toward advanced commercial pump packages[2]Source: United States Government Accountability Office, "Precision Agriculture Benefits and Challenges for Technology Adoption and Use,"gao.gov. Support programs such as EQIP WaterSMART, which facilitate variable-speed pump upgrades and canal automation, help reduce capital barriers. These programs provide a funding channel for the North America irrigation pumps market that operates independently of commodity cycles.

Replacement Cycle Acceleration from Aging Pump Fleets in Mature Agricultural Corridors

Replacement demand is emerging as a significant growth driver in the North America irrigation pumps market, particularly as mature irrigation districts transition beyond routine repairs. In December 2025, the Byron-Bethany Irrigation District announced plans to replace the century-old Wicklund Cut Pump Station following repeated breakdowns during the 2024-2025 irrigation season. Additionally, the United States Bureau of Reclamation allocated funding in 2025 for aging infrastructure projects, including the USD 4.77 million rehabilitation of the Helena Valley Irrigation District pumping plant in Montana. Many pump fleets installed in western agricultural corridors are now reaching a similar replacement phase, leading to concentrated procurement within a shorter timeframe. In this market, companies with local service teams and expertise in high-horsepower installations are well-positioned to meet this growing demand.

Utility and State Incentive Programs for High-Efficiency Pumps

Utility and public program support is reducing the effective purchase cost of efficient equipment in the North America irrigation pumps market. According to the Energy Trust of Oregon, adding a variable frequency drive to irrigation pumps can lower energy costs by 35% or more, with project incentives reaching up to USD 9,200 per installation. The USDA Rural Energy for America Program (REAP) program identifies electric, solar, and gravity pumps for sprinkler pivots as eligible improvements, with loans approved in fiscal year 2025 carrying an 80% government guarantee[3]Source: United States Department of Agriculture, "Rural Energy for America Program Renewable Energy Systems & Energy Efficiency Improvement Guaranteed Loans,"rd.usda.gov. Additionally, the EQIP WaterSMART program provides a second cost-sharing layer for efficiency upgrades, enabling stacked incentives to make premium pump systems more financially viable. Dealers who assist farmers in navigating these programs are gaining a competitive edge, as the North America irrigation pumps market increasingly values project support alongside product supply.

Climate Volatility Increasing Demand for Flexible Irrigation Pressure Management

Climate variability is driving increased demand for pump systems capable of adjusting pressure and flow to accommodate changing field conditions in the North America irrigation pumps market. A study published in Geophysical Research Letters in 2025 estimated that the Colorado River Basin lost 52.2 km3 of terrestrial water storage over 22 years through October 2024, with groundwater accounting for 65% of that loss. This water deficit has heightened the importance of delivery efficiency, as growers require improved control over the volume of water extracted and the pressure applied throughout the season. Fixed-speed systems are less effective under such conditions, prompting a shift toward multi-stage centrifugal units and variable-speed submersible systems with broader operating ranges. Consequently, the North America irrigation pumps market is transitioning toward equipment capable of managing both routine irrigation needs and short-notice supplemental demand within the same season.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront capital cost for efficient and smart pumping systems | -0.8% | North America, with the strongest effect on small and mid-size growers | Short term (≤ 2 years) |

| Water rights and groundwater permit uncertainty | -0.5% | United States western states, especially Idaho, California, Oregon, Texas, and Kansas | Long term (≥ 4 years) |

| Service technician shortages in rural areas | -0.3% | Rural United States and Canada, especially sparsely populated farm regions | Medium term (2-4 years) |

| Volatile input costs for motors, castings, and power electronics | -0.3% | Global supply chains with direct effect on North America manufacturing | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront Capital Cost for Efficient and Smart Pumping Systems

The high upfront capital cost continues to restrict the widespread adoption of efficient equipment in the North America irrigation pumps market. According to a 2024 GAO report, precision agriculture adoption remains lowest among the United States farms with gross cash farm income below USD 350,000, highlighting a financing gap that similarly impacts the purchase of advanced pump systems. This challenge is significant as many smaller and mid-sized growers focus on the initial list price of smart pump systems without fully considering available grants, rebates, or guaranteed lending options. As a result, there is underinvestment in premium configurations, even when the net installed cost could be more affordable after applying incentives. The North America irrigation pumps market is anticipated to experience faster adoption in scenarios where dealers integrate financing options, program guidance, and after-sales support into a streamlined purchasing process.

Volatile Input Costs for Motors, Castings, and Power Electronics

Input cost volatility continues to challenge manufacturers in the North America irrigation pumps market. The production of pumps relies on components such as motors, castings, and power electronics, and fluctuations in the prices of these inputs can disrupt standard annual pricing strategies. Mid-tier manufacturers are particularly vulnerable, as they often lack the purchasing scale required to secure longer-term supply contracts. This vulnerability can lead to extended lead times or reduced pricing stability during critical installation periods. In contrast, larger suppliers with extensive sourcing networks or in-house component production capabilities are better equipped to manage short-term cost fluctuations in the North America irrigation pumps market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Submersible Pumps Lead Technological Momentum

Centrifugal pumps accounted for 42.8% of the North America irrigation pumps market share in 2025, maintaining their leading position within the product mix. Their dominance is attributed to their extensive use in surface irrigation networks, main distribution pipelines, and flood-to-drip conversion projects across large commercial farms. Vortex pumps, on the other hand, serve a more specialized role in scenarios where water sources contain sediment, suspended solids, or field residue, particularly in canal-fed systems. Other product types, such as vertical turbine and positive-displacement pumps, remain significant in high-head well applications where standard centrifugal designs are less effective.

The North America irrigation pumps market size for submersible pumps is projected to grow at a 7.6% CAGR from 2026 to 2031, making them the fastest-growing product category. According to the December 2024 PCAST groundwater report, 70% of the United States groundwater withdrawals are used for irrigation, driving sustained demand for pump systems designed for deeper extraction conditions. The September 2025 launch of Franklin Electric’s Cerus X-Drive highlights advancements in submersible systems, including higher horsepower capabilities and grid-compliant drive integration. Within the North America irrigation pumps market, the submersible segment is diverging into solar DC solutions for remote fields and variable-speed grid-tied systems for large commercial farms. This differentiation enables manufacturers to address varying field conditions while maintaining the core focus on efficient water delivery.

Geography Analysis

In 2025, the United States accounted for 71.4% of the North America irrigation pumps market share, establishing itself as the primary driver of regional demand. Federal support for irrigation infrastructure remains active, with pump plant rehabilitation included in funded project pipelines across western districts. Additionally, EQIP WaterSMART grant criteria promote the adoption of variable-speed pump installations and canal automation, ensuring a high level of technology integration in new procurements. Aging infrastructure in states such as California, Arizona, and the Pacific Northwest is driving replacement demand, moving beyond routine maintenance cycles. Consequently, the United States remains the largest revenue contributor in the North America irrigation pumps market, encompassing both standard equipment and advanced control systems.

Canada holds a smaller share of the North America irrigation pumps market. However, demand is supported by established irrigation systems in provinces like Alberta, Saskatchewan, and British Columbia. Buyers in these regions are increasingly prioritizing water-use efficiency and data logging capabilities when considering pump upgrades. Meanwhile, Mexico is the fastest-growing market in the region, with a projected CAGR of 6.9% through 2031. Its demand is primarily project-driven rather than replacement-focused, creating opportunities for suppliers capable of supporting modernization efforts across wells, canals, and distributed pumping points. This dynamic positions Mexico as a significant growth area within the North America irrigation pumps market, despite the United States maintaining dominance in absolute revenue terms.

The rest of North America represents the smallest geography in the North America irrigation pumps market. Demand in this area is distributed across island agriculture and export-oriented farming systems, which typically procure through regional distributors. Product preferences in these markets lean toward flexible submersible and centrifugal configurations that can adapt to varying water-source conditions and smaller field layouts. While procurement remains steady, this geography does not significantly influence the overall growth trajectory or market concentration within the North America irrigation pumps market.

Competitive Landscape

The North America irrigation pumps market exhibited moderate concentration in 2025, with the top five companies accounting for a major share. The remaining share of the market was distributed among regional manufacturers and specialized pump suppliers, maintaining competition below the top tier. In this market, while price remains a factor, differentiation is increasingly focused on features such as variable-speed operation, remote visibility, and service responsiveness. These evolving standards for premium products pose challenges for mid-sized brands lacking advanced control software or robust dealer networks.

Valmont reported a 1.5% increase in North America irrigation sales in Q1 2026, despite lower volumes, indicating sustained pricing discipline within its regional operations. In September 2025, Franklin Electric introduced the Cerus X-Drive Low Harmonic Pump Panel, designed for high-horsepower centrifugal and submersible applications. These developments highlight how leading brands are focusing on technological advancements and portfolio diversification to maintain their competitive positions, rather than solely relying on unit sales growth.

In September 2025, Pentair announced the acquisition of Hydra-Stop LLC for USD 290 million, enhancing its capabilities in specialty water infrastructure components. While this acquisition does not position Pentair as a top-tier leader in the irrigation pump market, it strengthens its presence in adjacent water network solutions. Smaller companies continue to hold significance in local markets, where factors such as dealer relationships, inventory availability, and service speed influence purchasing decisions. However, penetrating the premium segment of the North America irrigation pumps market remains challenging without access to financing options, extensive installation networks, and advanced digital control capabilities.

North America Irrigation Pumps Industry Leaders

-

Franklin Electric Co., Inc.

-

Xylem Inc.

-

Grundfos Holding A/S

-

Valmont Industries, Inc.

-

Lindsay Corporation.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: DSI, a member of Headwater Companies, acquired Benson Pump Corporation, a groundwater distributor founded in 1985 and operating in Conway, Arkansas. This acquisition marks Headwater's first expansion into Arkansas. This development is relevant to irrigation pump distribution in the United States South/Southeast agricultural belt.

- February 2026: Franklin Electric Europe introduced the MHp Series self-priming horizontal multistage pumps and the NCV Series vertical multistage pumps, with the NCV supporting maximum flow rates up to 18 m3/h and heads up to 180 m. Both series are designed for irrigation, sprinkler, and water treatment applications.

- September 2025: Workhorse Pumps released its 2025–2026 Solar Pump Catalog, featuring the W6C-125-80 ultra-high volume centrifugal solar pump (up to 3HP) for irrigation and pond applications across rural North America.

North America Irrigation Pumps Market Report Scope

Irrigation pumps are devices designed to extract and transfer water from natural or artificial sources, such as rivers, lakes, wells, and reservoirs, to agricultural fields. The North America irrigation pumps market is segmented by product type (Submersible Pump, Vortex Pump, Centrifugal Pump, Other Product Types) and by geography (United States, Canada, Mexico, and Rest of North America). The market forecasts are provided in terms of value (USD).

| Submersible Pump |

| Vortex Pump |

| Centrifugal Pump |

| Other Product Types |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America |

| By Product Type | Submersible Pump | |

| Vortex Pump | ||

| Centrifugal Pump | ||

| Other Product Types | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

Key Questions Answered in the Report

What is the current outlook for irrigation pump demand across North America?

The North America irrigation pumps market is projected to grow from USD 38.48 billion in 2026 to USD 51.26 billion by 2031 at a 5.9% CAGR, supported by groundwater stress, replacement demand, and efficiency programs.

Which product type is growing the fastest through 2031?

Submersible pumps are the fastest-growing category, with a projected 7.6% CAGR through 2031, supported by deeper groundwater extraction needs and higher-specification control integration.

Why does the United States dominate regional sales?

The United States held 71.4% of regional revenue in 2025 because it has the largest irrigated agricultural base, active public rehabilitation programs, and stronger demand for advanced pump controls.

What is holding back faster adoption of smart pumping systems?

The main limits are upfront capital cost, water rights uncertainty, technician shortages in rural areas, and volatile input costs for motors, castings, and power electronics.

Page last updated on: