North America Global Capability Centers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

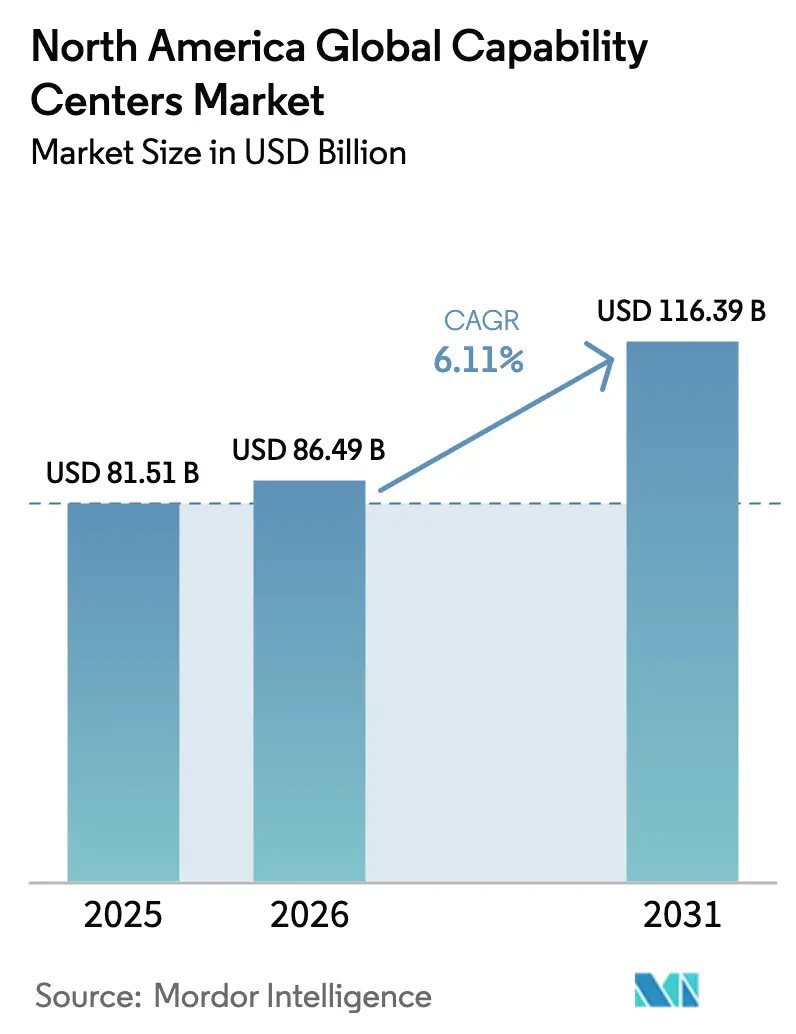

| Base Year Market Size (2025) | USD 81.51 Billion |

| Market Size (2026) | USD 86.49 Billion |

| Market Size (2031) | USD 116.39 Billion |

| Growth Rate (2026 - 2031) | 6.11% CAGR |

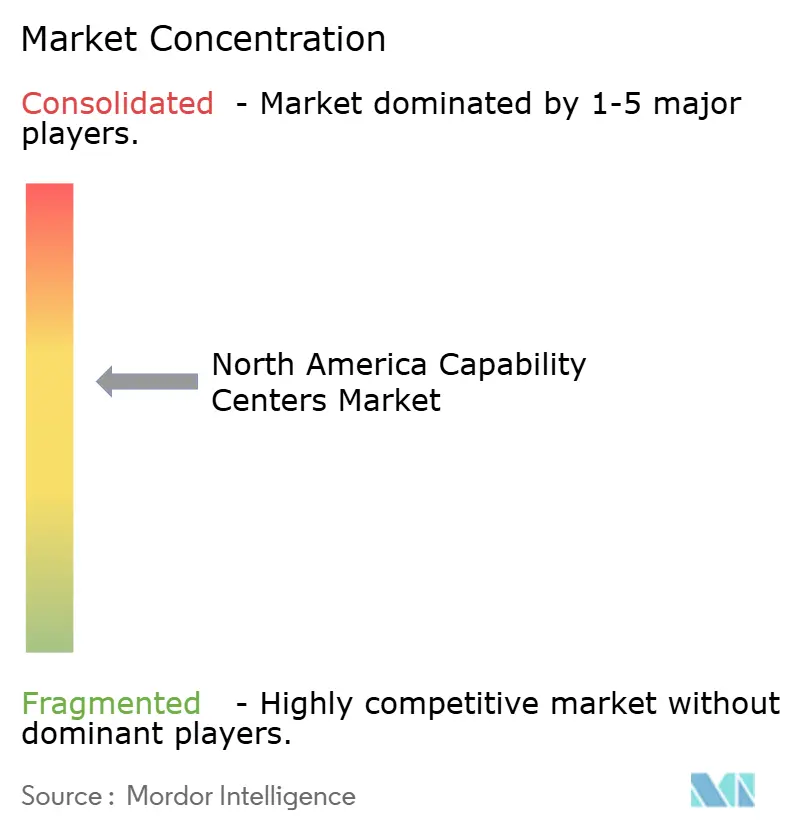

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America Global Capability Centers Market Analysis by Mordor Intelligence

The North America Global Capability Centers market size in 2026 is estimated at USD 86.49 billion, growing from 2025 value of USD 81.51 billion with 2031 projections showing USD 116.39 billion, growing at 6.11% CAGR over 2026-2031. Demand is shifting from offshore cost arbitrage toward nearshore innovation, as enterprises require same-day collaboration, cultural alignment, and stricter data-residency compliance. Heightened investment incentives in the United States and Canada, combined with Mexico’s bilingual talent advantage, keep the growth trajectory resilient despite inflationary real estate costs and ongoing digital talent shortages. New Build-Operate-Transfer (BOT) variants, rising knowledge process adoption, and industry-specific compliance needs have repositioned Global Capability Centers as strategic infrastructure rather than back-office extensions. Competitive intensity remains moderate, with global consultancies, Indian technology majors, and emerging nearshore specialists all targeting value-added functions over commoditized services.

Key Report Takeaways

- By function, Information Technology and Digital Services led the North America Global Capability Centers market with a 53.22% share in 2025, while Knowledge Process Outsourcing is expected to advance at a 6.57% CAGR through 2031.

- By engagement model, captive centers commanded 59.10% of the North American Global Capability Centers market size in 2025, while the Hybrid Build-Operate-Transfer model is projected to grow at a 7.22% CAGR through 2031.

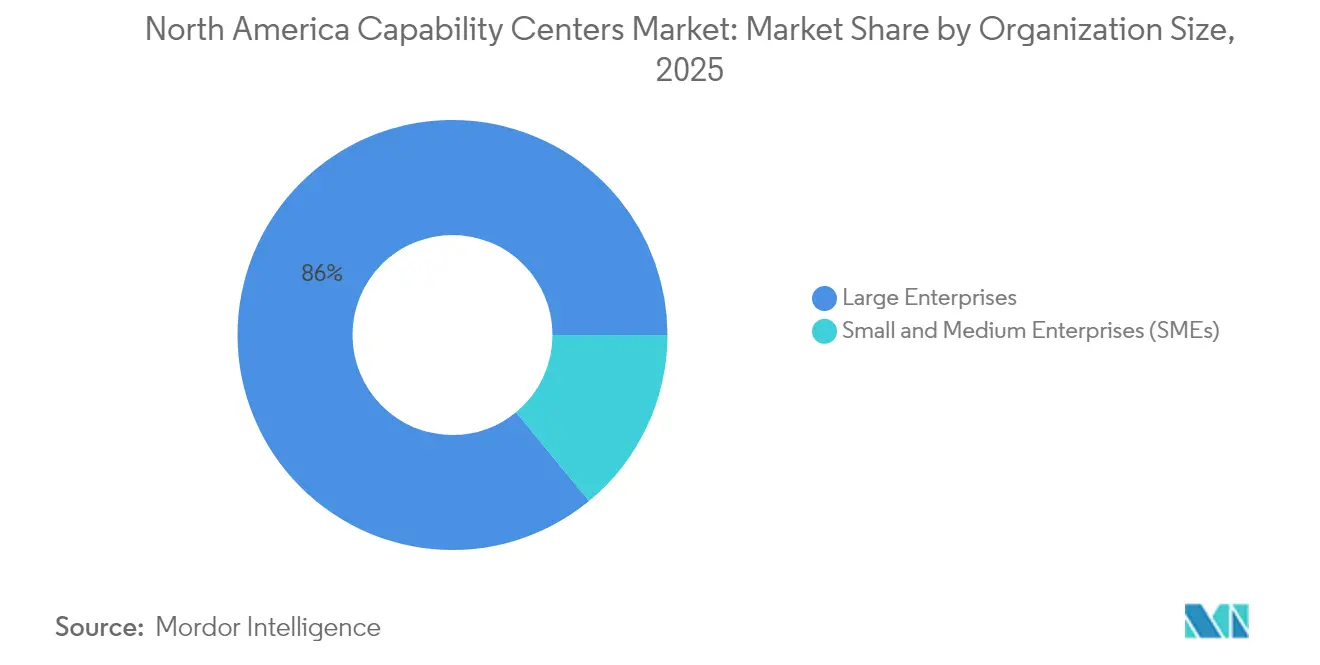

- By organization size, Large Enterprises held an 85.95% revenue share in 2025, while Small and Medium Enterprises are forecast to post an 8.31% CAGR by 2031.

- By industry vertical, Banking, Financial Services, and Insurance captured 35.88% of the North American market, projected to record a 6.92% CAGR through 2031.

- By country, the United States accounted for an 84.10% share of the North America Global Capability Centers market in 2025, while Mexico is expected to expand at a 6.98% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Global Capability Centers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated Nearshore Digital Transformation Demand Post-Pandemic | +1.2% | North America and LATAM | Short term (≤ 2 years) |

| Rising Talent Scarcity in Traditional Offshore Hubs | +1.0% | North America and India | Medium term (2-4 years) |

| Favorable Government Incentives and Tax Credits | +0.8% | United States and Canada | Long term (≥ 4 years) |

| Need for Real-Time Collaboration Across Time Zones | +0.9% | United States-Mexico corridor | Medium term (2-4 years) |

| Increasing Cybersecurity and Data-Residency Regulations | +0.7% | North America and Europe | Long term (≥ 4 years) |

| Availability of a Highly Skilled Bilingual Workforce in Mexico | +0.6% | Mexico and LATAM | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerated Nearshore Digital Transformation Demand Post-Pandemic

Uninterrupted remote operations during the pandemic forced enterprises to reassess latency in offshore collaboration, elevating nearshore Global Capability Centers that allow real-time iteration and faster product cycles.[1]Leandro Antunes Rodrigues, "GFT Right Shore: Understanding nearshore outsourcing," gft.com Companies reported improved stakeholder alignment because design, engineering, and compliance teams can work within a single business day. Same-day travel options shortened feedback loops and reduced project overruns. Technology and financial services firms were early adopters, but consumer brands and manufacturers are now replicating the model to accelerate omnichannel rollouts. The North America Global Capability Centers market benefits as nearshoring turns from a contingency into a core strategy.

Rising Talent Scarcity in Traditional Offshore Hubs

Salary premiums for niche AI and cybersecurity roles in India have risen to 30-40%, eroding historical cost gaps and prompting firms to tap into North American talent pools. New Global Capability Centers in Austin, Toronto, and Guadalajara emphasize market career advancement and proximity to headquarters as key differentiators. Domestic centers also mitigate geopolitical risk and currency volatility that complicate offshore workforce planning. Specialized universities and community college pipelines in the region are aligning curricula with emerging skills, further improving the supply. Consequently, North American Global Capability Centers are no longer viewed as cost outliers but as talent magnets that drive innovation, sustaining North America's growth in the Global Capability Centers market.

Favorable Government Incentives and Tax Credits

United States CHIPS and Science Act grants, NSF regional-innovation funding, and Canada’s Start-up Visa Program lower entry barriers for advanced Global Capability Center functions.[2]National Science Foundation, "Regional Innovation Engines," nsf.gov Incentives range from payroll rebates to fast-track permits for R&D-intensive operations. Canadian provinces actively recruit technical talent displaced by immigration uncertainty elsewhere. These programs emphasize innovation over routine operations, aligning with the evolution of the North America Global Capability Centers market toward high-value centers. Local economic-development agencies also broker university partnerships that give Global Capability Centers first access to specialized graduates. The incentive landscape has shifted from generic job creation to building sustainable innovation ecosystems.

Need for Real-Time Collaboration Across Time Zones

Agile development, continuous integration, and design thinking methodologies require synchronous communication that offshore models cannot deliver. Even minor time-zone advantages, such as the 2-3 hour gap between the East Coast and Mexico, yield measurable productivity gains compared to 12-hour separations with Asia. Crisis-response capabilities improve when teams can mobilize without waiting for offshore counterparts to start their day. Stakeholder satisfaction increases when meetings occur during standard business hours, rather than early mornings or late evenings. The North America Global Capability Centers market benefits as organizations prioritize collaboration quality over pure cost metrics, making proximity a competitive advantage rather than a luxury.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Commercial Real Estate and Labor Costs in Tier-1 North American Cities | -0.9% | Major metropolitan areas | Short term (≤ 2 years) |

| Immigration Policy Uncertainty Impacting Specialist Talent Mobility | -0.7% | The United States primarily | Medium term (2-4 years) |

| Competition for Digital Talent from Tech Giants and Start-Ups | -0.6% | Technology hubs | Long term (≥ 4 years) |

| Cultural Integration Challenges in Hybrid Engagement Models | -0.4% | Cross-border operations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Commercial Real Estate and Labor Costs in Tier-1 North American Cities

Office fit-out costs, ranging from USD 150 to USD 300 per square foot in major metropolitan areas, consume 25-30% of Global Capability Center operational budgets.[3]Savills, "Global Office Market Research," savills.com Specialized technology roles in San Francisco, New York, and Toronto command salaries that eliminate traditional offshore savings. This economic pressure drives organizations toward secondary markets, such as Austin, Nashville, and Montreal, where talent availability balances with sustainable cost structures. The North America Global Capability Centers market adapts through hybrid footprint strategies, placing high-value functions in premium locations while scaling routine operations in cost-effective areas. Real estate inflation particularly impacts large-scale operations requiring extensive floor space for collaboration zones and specialized labs.

Immigration Policy Uncertainty Impacting Specialist Talent Mobility

The unpredictable H-1B visa program changes force organizations to develop contingency plans for talent displacement, often requiring the establishment of alternative Global Capability Center locations to ensure operational continuity. This uncertainty particularly affects organizations dependent on international talent for specialized roles in AI, cybersecurity, and advanced analytics, where domestic talent pools remain insufficient. The North America Global Capability Centers market faces challenges as organizations must consider immigration risk in their location decisions and operational models. Policy volatility also undermines client confidence in Global Capability Center stability, particularly for mission-critical functions that require assured talent continuity and operational resilience.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Function / Capability: IT Services Dominance Amid KPO Acceleration

Information Technology and Digital Services maintains commanding market leadership with a 53.22% share in 2025, reflecting the foundational role of technology infrastructure in modern Global Capability Center operations. The North America Global Capability Centers market size for this segment continues to expand as organizations establish technology hubs that support cloud migration, application modernization, and cybersecurity operations. These functions benefit from proximity to corporate headquarters, enabling real-time collaboration on strategic technology initiatives and facilitating faster decision-making cycles for critical infrastructure projects. The segment's resilience stems from continuous technology refresh cycles that require specialized expertise in emerging areas, such as containerization, microservices architecture, and zero-trust security frameworks.

Knowledge Process Outsourcing (KPO) emerges as the fastest-growing segment, with a 6.57% CAGR through 2031, signaling a strategic evolution toward high-value analytical and research capabilities. Organizations are increasingly viewing Global Capability Centers as strategic assets for knowledge creation, rather than as a means of operational cost reduction. This shift aligns with broader market evolution toward AI-driven automation, where Global Capability Centers serve as testing grounds for hyperautomation initiatives that combine artificial intelligence, robotic process automation, and machine learning. The North America Global Capability Centers market share for KPO functions expands as organizations recognize that specialized knowledge processes provide sustainable competitive advantages that are difficult to replicate, unlike traditional BPO functions that face commoditization pressure. The acceleration also reflects regulatory compliance requirements, particularly in healthcare and financial services, where specialized knowledge processes require domain expertise and familiarity with relevant regulations.

By Engagement Model: Hybrid BOT Models Reshape Traditional Outsourcing

Captive/In-house models dominate the market, accounting for a 59.10% share in 2025, reflecting organizational preferences for direct control over strategic operations and intellectual property protection. The North America Global Capability Centers market size for captive operations continues to expand as organizations seek greater control over mission-critical functions and intellectual property development. These models provide maximum flexibility for strategic pivots, talent management, and operational integration with corporate functions. The captive dominance reflects market maturity where organizations understand the long-term strategic value of direct operational control, particularly for functions that drive competitive differentiation and innovation capacity.

Hybrid Build-Operate-Transfer models are projected to grow at a 7.22% CAGR through 2031, representing a fundamental shift in how organizations approach establishing Global Capability Centers and risk management. Modern BOT models, now evolving into Build-Operate-Transform-Transfer (BOTT), focus on capability building rather than infrastructure development, with providers designing operating models upfront and executing digital transformations during the operate phase. The North America Global Capability Centers market share for hybrid models expands as organizations seek balanced approaches that provide immediate operational capabilities while preserving long-term strategic control options. These models are particularly beneficial for organizations new to Global Capability Center operations, as they provide structured pathways to build capabilities while mitigating establishment risks and accelerating the time-to-value for strategic initiatives.

By Organization Size: SME Adoption Democratizes Global Capability Center Access

Large Enterprises maintain an overwhelming market dominance, with an 85.95% share in 2025, reflecting the capital requirements and operational complexity traditionally associated with establishing a Global Capability Center. The North America Global Capability Centers market size for large enterprise operations continues to expand as Fortune 500 companies establish multiple centers with specialized functions and geographic distribution strategies. These organizations leverage Global Capability Centers as strategic assets for digital transformation, innovation acceleration, and talent acquisition in competitive technology markets. The large enterprise dominance reflects historical patterns in which the establishment of a Global Capability Center required significant capital investment, specialized expertise, and operational scale that smaller organizations struggled to achieve.

Small and Medium Enterprises represent the fastest-growing segment, with an 8.31% CAGR through 2031, indicating the democratization of Global Capability Center access through innovative service models and technology platforms. This growth trajectory suggests fundamental changes in Global Capability Center economies, where cloud-native architectures, automation platforms, and BOT models enable smaller organizations to access captive capabilities previously reserved for larger companies. The North America Global Capability Centers market share for SME operations expands through "Global Capability Center-as-a-Service" models, which provide turnkey solutions without the traditional complexities of establishing a global capability center. These platforms leverage shared infrastructure, standardized processes, and automation technologies to deliver Global Capability Center capabilities at scales economically viable for smaller organizations. The democratization trend also reflects talent dynamics, where SMEs compete for specialized skills by offering career development opportunities based on Global Capability Centers.

By Industry Vertical: Healthcare Acceleration Amid BFSI Dominance

The Banking, Financial Services, and Insurance sector maintains the largest industry share at 35.88% in 2025, reflecting the sector's early adoption of Global Capability Center models for regulatory compliance, risk management, and customer service operations. The North America Global Capability Centers market size for BFSI operations continues to expand as financial institutions establish specialized centers for anti-money laundering, fraud detection, and digital banking capabilities. These functions benefit from proximity to regulatory bodies and financial markets, allowing real-time compliance monitoring and faster adaptation to regulatory changes. The sector's dominance reflects the strategic importance of technology operations in the financial services industry, where digital capabilities are increasingly driving competitive differentiation and enhancing customer experience.

Healthcare and Life Sciences emerge as the fastest-growing vertical, with a 7.06% CAGR through 2031, driven by regulatory complexity, data residency requirements, and specialized domain expertise needs. The North America Global Capability Centers market share for healthcare operations expands as organizations establish specialized centers for clinical data management, regulatory technology, and digital health solutions. The sector's growth is driven by AI and machine learning applications in drug discovery, medical imaging, and personalized medicine, which necessitate close collaboration between clinical experts and technology teams. Healthcare Global Capability Centers are increasingly serving as innovation centers for telemedicine platforms and regulatory technology, enabling organizations to navigate complex compliance requirements while accelerating product development cycles. The vertical's growth trajectory suggests that specialized industry expertise becomes a key differentiator in Global Capability Center value propositions.

Geography Analysis

The United States commands overwhelming market dominance with an 84.10% share in 2025, reflecting its role as the primary demand center for Global Capability Center services and the preferred location for innovation-focused captive operations. The North America Global Capability Centers market size in the US continues to expand as organizations establish specialized centers for artificial intelligence, cybersecurity, and advanced analytics functions that require proximity to corporate decision-makers and technology ecosystems. Major Global Capability Center hubs, including Austin, Chicago, and the Bay Area, benefit from university partnerships and established technology communities that facilitate the acquisition of talent. The US market also benefits from intellectual property protection frameworks that provide confidence for organizations establishing strategic operations. However, cost pressures in Tier-1 cities drive geographic dispersion, with secondary markets like Nashville, Denver, and Phoenix emerging as alternatives that balance talent availability with operational economics.

Canada represents a strategic growth opportunity, leveraging immigration policy advantages and government incentives to attract international talent and investment in the Global Capability Center. The country's strategy to attract H-1B visa holders displaced by US immigration uncertainty has created talent pools in Toronto, Vancouver, and Montreal that rival traditional offshore destinations in terms of skills availability and cost competitiveness. The North America Global Capability Centers market share for Canadian operations expands as organizations establish specialized centers for artificial intelligence, data science, and cybersecurity functions that benefit from the country's research institutions and government support programs. Canadian Global Capability Centers benefit from cultural alignment with US business practices, favorable exchange rates, and government programs that support the establishment of innovation centers. The regulatory environment, including data privacy frameworks and cybersecurity standards, aligns with US requirements while providing operational flexibility that offshore locations cannot match.

Mexico emerges as the fastest-growing geography, with a 6.98% CAGR through 2031, driven by nearshoring trends, competitive labor costs, and strategic investments in technology infrastructure. The North America Global Capability Centers market size in Mexico continues to expand as organizations establish specialized centers for software development, digital services, and customer experience operations that benefit from the country's bilingual workforce and time zone alignment. Micron Technology's establishment of an Engineering and Operations Center in Guadalajara exemplifies this evolution, with a focus on DRAM product development and IT operations. [4]Autores AméricaEconomía.com, "Micron Technology will open a new engineering and operations center in Mexico," americaeconomia.com. AWS's USD 5 billion investment in Mexican infrastructure further validates the country's potential as a strategic technology hub that can support advanced Global Capability Center operations. Mexico's cultural affinity with US business practices creates compelling value propositions for organizations seeking nearshore alternatives to traditional offshore models. The country's growth trajectory suggests it will play an increasingly important role in North American Global Capability Center strategies as organizations balance cost optimization with operational proximity.

Competitive Landscape

The North American Global Capability Center market exhibits moderate fragmentation with established Indian service providers competing against global consulting firms and emerging regional specialists. Traditional offshore leaders, including TCS, Infosys, Cognizant, and Wipro, leverage their global delivery capabilities and established client relationships to expand their operations in North America, while consulting giants like Accenture, Deloitte, and Capgemini position themselves as strategic transformation partners. The North America Global Capability Centers market competition reflects evolution from cost-focused outsourcing to strategic capability building, where success depends on domain expertise, innovation capacity, and cultural alignment rather than labor arbitrage alone. Accenture's USD 250 million investment in Global Capability Center capabilities and partnerships with specialized providers demonstrates how market leaders combine organic growth with strategic acquisitions to build comprehensive service portfolios.

White-space opportunities emerge in specialized verticals like healthcare, advanced manufacturing, and cybersecurity, where domain expertise creates sustainable competitive advantages. The rise of Build-Operate-Transfer specialists and regional providers that focus exclusively on North American markets creates new competitive dynamics, as these organizations offer cultural alignment and geographic proximity that global providers struggle to match. The North America Global Capability Centers market share distribution increasingly rewards providers that demonstrate measurable business outcomes rather than operational metrics, reflecting client sophistication and the strategic importance of Global Capability Center operations in enterprise digital transformation initiatives. Technology adoption becomes a key differentiator, with leading providers investing in AI-driven automation, hyperautomation platforms, and cloud-native architectures that enable superior service delivery and operational efficiency.

The competitive landscape continues to evolve as traditional boundaries between service providers, consulting firms, and technology companies become increasingly blurred. Global systems integrators expand their North American delivery capabilities through strategic acquisitions and talent investments, while specialized boutique firms carve out niches in emerging technology areas and industry-specific solutions. The North America Global Capability Centers market is experiencing intensified competition as organizations seek partners that combine technology expertise with industry knowledge and cultural alignment. Strategic alliances between global and regional providers create new service models that balance the advantages of scale with local market knowledge and client proximity. The market rewards providers that demonstrate innovation capacity, talent development capabilities, and strategic alignment with client business objectives, rather than focusing solely on pure cost optimization.

North America Global Capability Centers Industry Leaders

-

Accenture plc

-

Cognizant Technology Solutions Corporation

-

Tata Consultancy Services Limited

-

Capgemini SE

-

IBM Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Dark Matter Technologies launched a 140,000-square-foot Global Capability Center in Hyderabad to serve over 900 companies across the US, Canada, Africa, and Australia, with a focus on artificial intelligence, machine learning, cloud computing, and cybersecurity capabilities. The company plans 2-3x growth in the India workforce and is committed to a five-year lease for an additional site in Bhubaneswar to accommodate 700-800 employees.

- December 2024: Inductus Global Capability Center reported that India hosts approximately 1,800 Global Capability Centers, representing 50% of the global total, with a total headcount of 1.9 million and FY2024 revenues of USD 64.6 billion, representing 40% year-over-year growth. The report highlighted that 66% of these Global Capability Centers serve American-based companies, with the USA accounting for 1,250 centers and Canada for 30 centers.

- August 2024: Charles Schwab selected Hyderabad as its first Technology Development Center in India, following discussions between Telangana government officials and Schwab executives at the company's Dallas headquarters. The center will focus on technology development and operations to support Schwab's North American business operations. Hiring is expected to accelerate in the fall of 2024, with the goal of reaching over 100 team members by year-end.

North America Global Capability Centers Market Report Scope

The scope of the global capability center study for the market segmentation by the Function/Capability for (i) Information Technology (IT) and Digital Services segment is limited to Software Development, Cloud and Infrastructure Management, Cybersecurity, Data Analytics and AI/ML; (ii) Engineering / ER&D segment is limited to Product Design and Testing, Embedded Systems, Digital Twin / Simulation; (iii) Business Process Management (BPM) segment is limited to Finance and Accounting, HR, Payroll and Talent Management, Procurement, Customer Service; and (iv)Knowledge Process Outsourcing (KPO) segment is limited to Market Research and Insights, Risk and Compliance, Legal and Regulatory Support, Strategy and Consulting Support. Similarly, for segmentation by the Engagement Model, scope for (i) Hybrid Build-Operate-Transfer (BOT) is limited to Joint Venture / Strategic Partnership and Virtual Captive Model. The rest of the segment scope is as specified for the listed segment.

| Information Technology (IT) and Digital Services |

| Engineering / ER&D |

| Business Process Management (BPM) |

| Knowledge Process Outsourcing (KPO) |

| Captive (Self-Build)/ In-house |

| Build-Operate-Transfer (BOT) |

| Hybrid Build-Operate-Transfer (BOT) |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| Banking, Financial Services, and Insurance (BFSI) |

| Telecom and IT |

| Healthcare and Life Sciences |

| Manufacturing, Automotive and Industrial |

| Retail and Consumer Goods |

| Other Industry Verticals |

| United States |

| Canada |

| Mexico |

| By Function / Capability | Information Technology (IT) and Digital Services |

| Engineering / ER&D | |

| Business Process Management (BPM) | |

| Knowledge Process Outsourcing (KPO) | |

| By Engagement Model | Captive (Self-Build)/ In-house |

| Build-Operate-Transfer (BOT) | |

| Hybrid Build-Operate-Transfer (BOT) | |

| By Organization Size | Large Enterprises |

| Small and Medium Enterprises (SMEs) | |

| By Industry Vertical | Banking, Financial Services, and Insurance (BFSI) |

| Telecom and IT | |

| Healthcare and Life Sciences | |

| Manufacturing, Automotive and Industrial | |

| Retail and Consumer Goods | |

| Other Industry Verticals | |

| By Country | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

What are the main advantages of nearshore Global Capability Centers over traditional offshore models?

Nearshore Global Capability Centers offer real-time collaboration within similar time zones, cultural alignment, easier travel for in-person meetings, and stronger data residency compliance. Mexico's Global Capability Centers are projected to grow at a 6.98% CAGR through 2031, driven by these advantages, along with bilingual talent at competitive costs.

How are Build-Operate-Transfer models evolving in the Global Capability Center landscape?

Traditional BOT models are evolving into Build-Operate-Transform-Transfer (BOTT) approaches that focus on capability building rather than just infrastructure. These hybrid models are projected to grow at a 7.22% CAGR through 2031, as they offer immediate operational capabilities while preserving long-term strategic control options.

Which industries are driving Global Capability Center growth in North America?

Banking, Financial Services, and Insurance leads with a 35.88% market share, while Healthcare and Life Sciences are the fastest-growing verticals, with a 7.06% CAGR through 2031. Healthcare growth is driven by regulatory complexity, data residency requirements, and specialized domain expertise needs in areas like clinical data management and digital health solutions.

How are SMEs participating in the North America Global Capability Center market?

SMEs represent the fastest-growing segment, with an 8.31% CAGR through 2031, driven by "Global Capability Center-as-a-Service" models that provide turnkey solutions without the complexities of traditional establishment. Cloud-native architectures, automation platforms, and BOT models enable smaller organizations to access captive capabilities previously reserved for Fortune 500 companies.

What impact do government incentives have on Global Capability Center location decisions?

Government programs, such as the US CHIPS and Science Act, NSF regional innovation funding, and Canada's Start-up Visa Program, provide grants, payroll rebates, and fast-track permits that lower entry barriers for advanced Global Capability Center functions. These incentives are shifting from generic job creation to building sustainable innovation ecosystems that attract high-value Global Capability Center operations.

What challenges do North American Global Capability Centers face compared to offshore locations?

North American Global Capability Centers face commercial real estate costs of USD 150-300 per square foot in major cities, immigration policy uncertainty affecting talent mobility, intense competition for digital talent from tech giants, and challenges in cultural integration within hybrid models. These factors drive organizations toward secondary markets, such as Austin, Nashville, and Montreal, that balance talent availability with sustainable cost structures.

Page last updated on: