North America Frontline Worker Technology Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

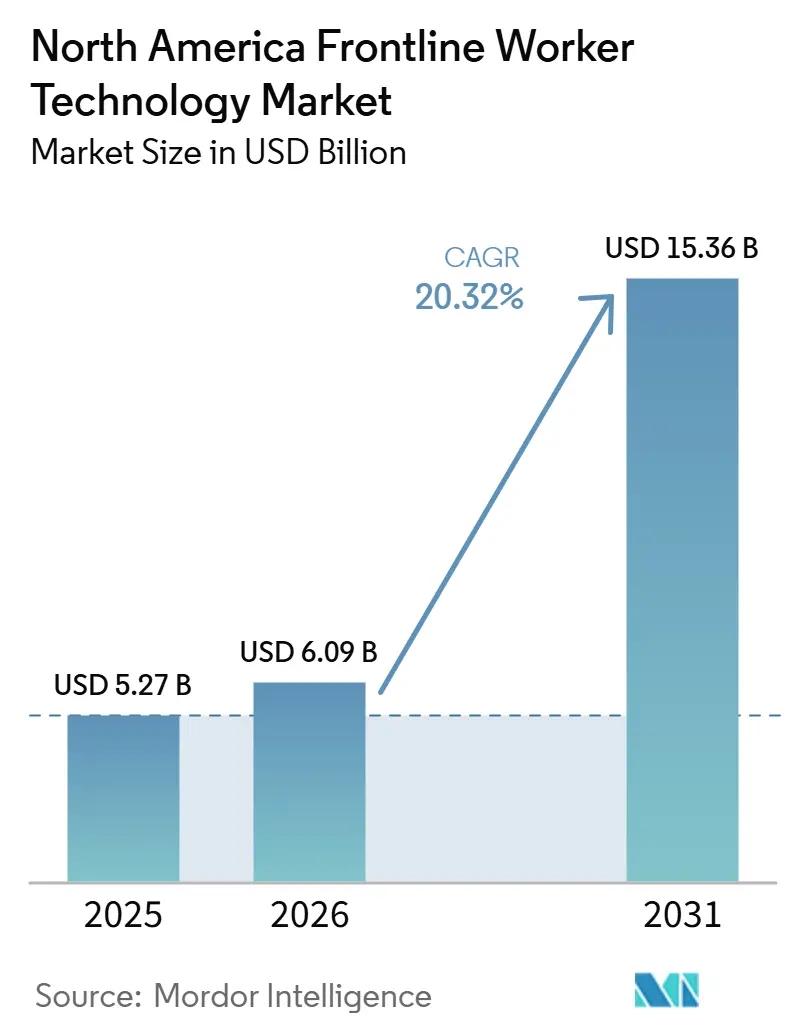

| Base Year Market Size (2025) | USD 5.27 Billion |

| Market Size (2026) | USD 6.09 Billion |

| Market Size (2031) | USD 15.36 Billion |

| Growth Rate (2026 - 2031) | 20.32% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Frontline Worker Technology Market Analysis by Mordor Intelligence

The North America frontline worker technology market size is projected to expand from USD 5.27 billion in 2025 and USD 6.09 billion in 2026 to USD 15.36 billion by 2031, registering a CAGR of 20.32% between 2026 and 2031. The North America frontline worker technology market is advancing as compliance-related digitization becomes part of daily operations across regulated workplaces. Labor shortages across shift-based roles are also pushing employers to improve output with digital tools rather than relying solely on additional hiring. AI-guided work support is becoming increasingly relevant as companies seek to have workers complete tasks faster and with fewer errors. Buyers are also placing greater weight on deployment support, integration depth, and measurable productivity outcomes when comparing vendors. This is creating room for platforms that combine software, services, and workflow governance in a single offering across the North America frontline worker technology market.

Key Report Takeaways

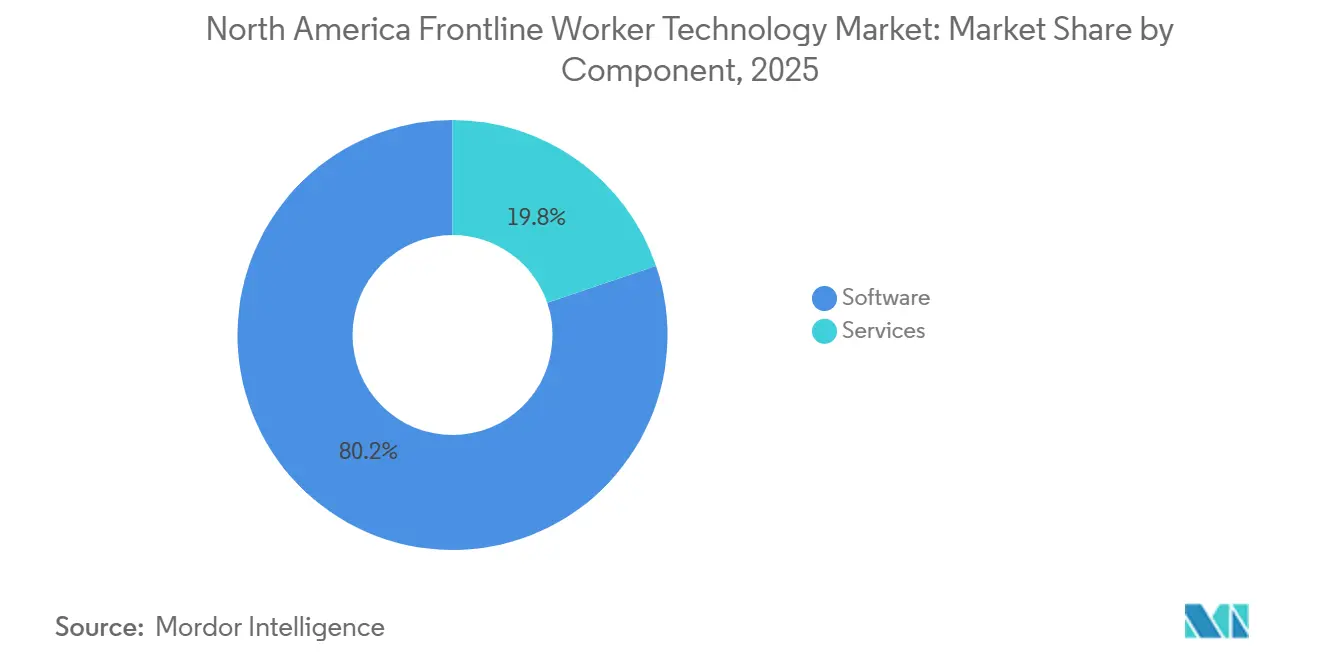

- By component, software led with 80.21% of the North America frontline worker technology market revenue share in 2025, while services are projected to expand at a 26.72% CAGR through 2031.

- By deployment, cloud-based held 78.05% share of the North America frontline worker technology market in 2025, while cloud-based is also expected to record the highest CAGR at 25.58% through 2031.

- By organization size, large enterprises held 74.39% of the North America frontline worker technology market revenue share in 2025, while SMEs are projected to expand at a 26.44% CAGR through 2031.

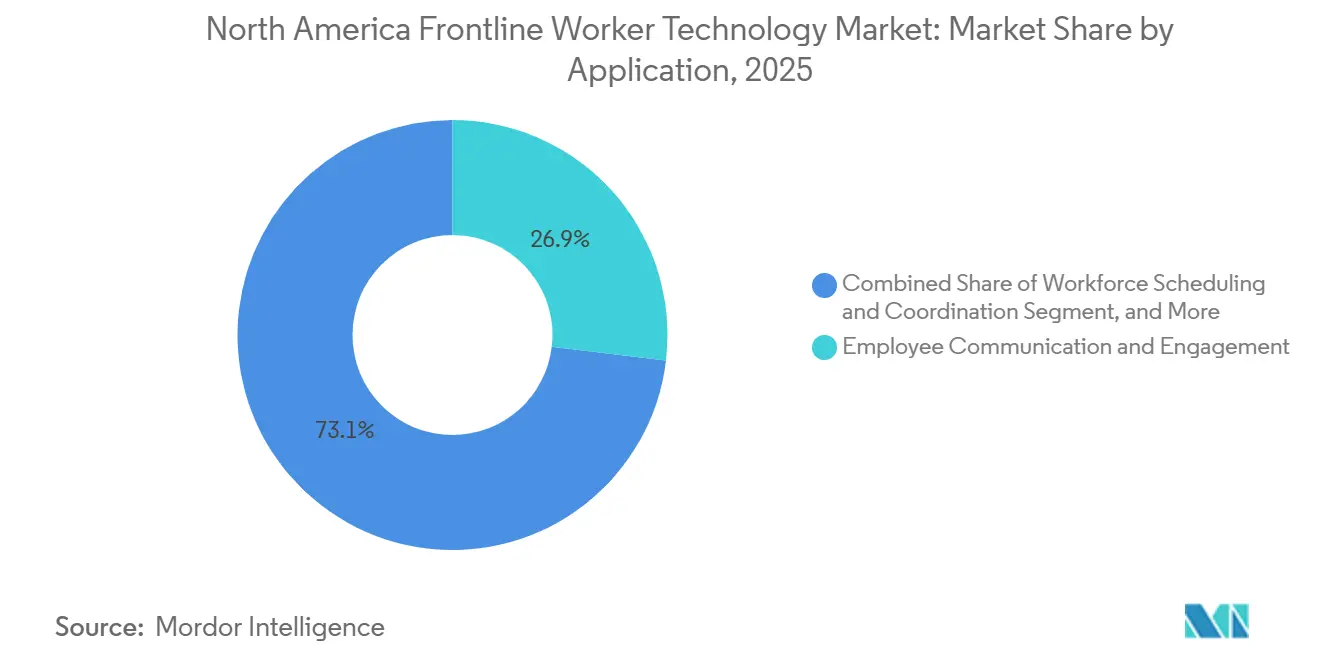

- By application, employee communication and engagement accounted for 26.89% of the North America frontline worker technology market share in 2025, while workforce analytics and performance management are expected to advance at a 25.12% CAGR through 2031.

- By end-user industry, retail and e-commerce accounted for 25.45% of the North America frontline worker technology market share in 2025, while transportation and logistics is projected to grow at a 24.87% CAGR through 2031.

- By geography, the United States held 83.44% of the North America frontline worker technology market share in 2025, while Mexico is expected to expand at a 25.91% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Frontline Worker Technology Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Compliance-Linked Digital Workflows in Regulated Operations | +3.8% | US, Canada | Short term (≤ 2 years) |

| Labor Scarcity across Shift-Based and Field Operations | +3.5% | US, Canada, northern Mexico | Short term (≤ 2 years) |

| ROI Pressure on Reduced Downtime and Faster Task Completion | +3.2% | US-led regional relevance | Medium term (2-4 years) |

| Expansion of AI-Guided Work Instructions at the Point of Use | +3.0% | US, Canada, Mexico export zones | Medium term (2-4 years) |

| Proliferation of Ruggedized Wearables and Mobile-First Enterprise Apps | +2.4% | US, Canada | Medium term (2-4 years) |

| Growing Demand for Real-Time Knowledge Capture From Senior Workers | +2.0% | US, Canada | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Compliance-Linked Digital Workflows in Regulated Operations

Compliance requirements have moved from a background condition to a direct purchase trigger in the North America frontline worker technology market. Electronic recordkeeping needs are pushing employers to capture safety and workflow data at the point of work rather than rely on delayed manual reporting. The NLRB guidance on electronic surveillance has also raised the standard for how organizations document and justify worker monitoring, encouraging the use of auditable workflow platforms rather than informal tracking tools.[1]National Labor Relations Board, “NLRB General Counsel Issues Memo on Unlawful Electronic Surveillance and Automated Management Practices,” National Labor Relations Board, nlrb.gov This is changing vendor selection because built-in governance controls now matter as much as frontline usability. In pharmaceutical manufacturing and healthcare, pre-configured audit trails are becoming more important. Buyers want systems that are easier to validate and defend during compliance reviews. Documenting and justifying faster compliance-led buying cycles are also helping the North America frontline worker technology market, as these projects are less likely to be delayed than discretionary software spending.

Labor Scarcity Across Shift-Based and Field Operations

Labor scarcity remains a core growth driver for the North America frontline worker technology market, as many shift-based employers still struggle to fill operational roles. Trucking wages rose 16%, and warehousing pay increased 15% year over year in Q1 2025, underscoring how intense the competition for frontline labor had become. In transportation, logistics, and automotive, 74% of US employers reported difficulty filling roles in 2025, reinforcing the pressure to improve output with digital tools rather than incremental hiring. Manufacturing sites faced the same issue, with nearly 75% reporting difficulty hiring due to a shortage of skilled candidates. As a result, companies are buying digital work instructions, task routing, and analytics tools as direct labor productivity solutions in the North America frontline worker technology market. That same pressure is also shortening onboarding expectations because employers need new hires to become effective faster.

ROI Pressure on Reduced Downtime and Faster Task Completion

The North America frontline worker technology market is also benefiting from tighter return-on-investment screening by enterprise buyers. Research cited in July 2025 showed that companies investing in frontline-focused digital tools achieved a 22% increase in productivity, doubled customer satisfaction scores, and increased profitability by up to 25%. In March 2026, BCG stated that demand-based AI scheduling tools at a large hospital system were projected to deliver USD 125 million to USD 150 million in savings and reduce attrition by 30%. These examples show that buyers are no longer focusing solely on incremental efficiency gains. They are increasingly comparing software spend against lower temporary labor use, faster onboarding, and fewer disruptions. Vendors that can prove those outcomes with built-in measurement tools are improving their position in the North America frontline worker technology market.

Expansion of AI-Guided Work Instructions at the Point of Use

AI-guided work instructions are becoming a structural part of the North America frontline worker technology market because they move knowledge delivery closer to the actual task. In January 2026, a generative AI coach in a manufacturing control tower improved productivity by more than 40% and cut repair times by 95% at a Lenovo facility. This matters because dynamic guidance can narrow the gap between novice and experienced workers during live operations. It also favors platforms that can connect wearable devices, workflow software, and enterprise systems in a single environment. Augmentir’s April 2025 launch of its Industrial AI Agent Studio showed how vendors are moving from static software interfaces toward specialized AI agents for skills, safety, quality, and maintenance workflows. As this model spreads, the North America frontline worker technology market is likely to reward vendors with open connectors and practical deployment paths instead of isolated AI features.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented Legacy Systems Slow Enterprise Rollouts | -2.8% | US, Canada, Mexico | Short term (≤ 2 years) |

| Frontline Change Fatigue and Adoption Resistance | -2.2% | US-wide with higher pressure in high-turnover sectors | Medium term (2-4 years) |

| Device Hygiene, Durability, and Support Complexity | -1.5% | US, Canada | Medium term (2-4 years) |

| Data Privacy and Worker Monitoring Concerns | -1.8% | California and other high-regulation US states, Canada | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fragmented Legacy Systems Slow Enterprise Rollouts

Legacy system fragmentation continues to slow the North America frontline worker technology market, especially in complex industrial settings. Many enterprises still operate with ERP systems, manufacturing execution systems, SCADA platforms, radio tools, and paper workflows that were never designed to easily share data. That creates longer testing cycles, heavier integration work, and added dependence on specialized consultants before a rollout can move into production. The issue is more severe in utilities and pharmaceutical operations because workflow changes often need documented validation before they can be approved for live use. Gartner was cited in the input as identifying integration complexity as the top barrier to operational AI deployment, which supports the same pattern seen across frontline rollouts. This means some of the most digitally invested enterprises still move slowly in the North America frontline worker technology market because deeper legacy estates create more dependencies, not fewer.

Frontline Change Fatigue and Adoption Resistance

Adoption resistance remains a practical limit on the North America frontline worker technology market because many frontline deployments fail at the change-management stage rather than at the product stage. A March 2025 study cited in the input found that 30% of frontline workers said their employer lacked adequate technology to support new hires, suggesting that earlier tool rollouts had already left trust gaps within the workforce. The same study also reported that 90% of frontline managers missed annual performance targets because of team skill shortages, which helps explain why poorly handled deployments face skepticism. Vendors are responding by bundling structured adoption programs, phased rollouts, and peer champion models into their implementations. In March 2026, UKG reported that 75% of frontline workers said technology made it easier to manage their work schedules, indicating that a visible personal benefit is often the clearest path to adoption. The North America frontline worker technology market, therefore, depends not only on software quality but also on whether workers see the platform as useful rather than intrusive.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Segment Accelerates as Deployment Complexity Grows

Software held 80.21% of the North America frontline worker technology market share in 2025 within the component mix, reflecting how quickly enterprises expanded platform deployments after the pandemic. Services are forecast to record the faster growth rate at a 26.72% CAGR through 2026-2031. This shift shows that buyers are moving beyond basic license purchases and paying more attention to implementation success. The North America frontline worker technology market is therefore seeing stronger demand for integration, training, managed support, and deployment services. That demand is directly tied to the complexity of connecting frontline platforms to ERP, MES, and operational technology environments.

Earlier adopters often tried to manage deployments with internal IT resources, but many organizations later returned to vendors and partners for structured rollout support. That pattern is increasing service revenue because enterprises want fewer delays and better adoption outcomes. Outcome-based contracting also supports the services mix because some buyers now pay for uptime gains, onboarding improvements, or productivity targets rather than only per-seat subscriptions. McKinsey reported in January 2026 that leading operations companies invested USD 3 in process revamping and USD 5 in scaling and adoption for every USD 2 spent on technology, which shows how heavily successful deployments depend on execution support. As a result, the North America frontline worker technology industry is gradually moving toward a revenue mix where deployment capability matters almost as much as software breadth.

By Deployment: Cloud-Based Model Dominates as Edge Architecture Matures

Cloud-based deployment accounted for 78.05% of the North America frontline worker technology market size in 2025, and the same model is projected to expand at a 25.58% CAGR through 2031. This combination of scale and growth shows how strongly enterprises now prefer centrally managed platforms. Cloud infrastructure supports automatic updates, multi-site visibility, centralized device management, and easier data aggregation across distributed workforces. Those benefits are especially important in the North America frontline worker technology market because many employers need to manage large frontline populations across stores, warehouses, plants, and service sites. It also supports the spread of AI-enabled use cases that need shared data and model access.

Even so, frontline execution does not depend solely on cloud connectivity. Many work environments still need edge processing and local caching because connectivity gaps remain common on shop floors, docks, yards, and remote sites. Vendors that support offline-first performance while synchronizing with cloud back ends are better placed to serve these conditions. Hybrid and on-premises models remain relevant in healthcare, pharmaceuticals, and government settings, where data residency and validation requirements remain high. The North America frontline worker technology industry is therefore not moving away from edge capabilities, but is organizing them around a cloud-managed architecture.

By Organization Size: SMEs Narrow the Technology Access Gap

Large enterprises held 74.39% of the North America frontline worker technology market in 2025 because they had larger IT budgets, dedicated rollout teams, and stronger vendor relationships. SMEs are projected to grow faster at a 26.44% CAGR through 2026-2031. This gap shows that smaller employers are catching up as SaaS pricing and mobile-first delivery reduce the barriers that once limited adoption. The North America frontline worker technology market is therefore broadening beyond enterprise-scale deployments. A major factor is that supplier compliance expectations from large customers are pushing smaller partners to adopt digital communication, safety, and traceability tools.

This effect is especially evident in the US-Mexico manufacturing corridor, where smaller suppliers serve multinational retailers and OEMs with increasingly stringent reporting requirements. Per-seat subscriptions have also made it easier for smaller businesses to start with a narrow use case and expand after results become visible. Vendors are responding with lighter implementation models, simpler packaging, and partner-led go-to-market approaches. SHRM noted that consumer-like app usability is helping reduce training barriers to frontline technology adoption, particularly for smaller employers with limited internal support capacity. The North America frontline worker technology market is therefore drawing more of its incremental growth from SMEs than it did in earlier adoption cycles.

By Application: Analytics Layer Emerges as ROI Validation Engine

Employee communication and engagement accounted for 26.89% of the application mix in 2025, indicating that many organizations initially focused on closing the communication gap between managers and deskless workers. Workforce analytics and performance management are projected to grow the fastest at a 25.12% CAGR through 2031. This pattern suggests that the North America frontline worker technology market is moving from basic connectivity toward measurable performance management. Communication, task management, scheduling, learning, and safety workflows still form the operating base of many deployments. At the same time, analytics is gaining ground because executive teams want proof that frontline tools improve output, retention, and process consistency.

Safety and compliance management are also becoming increasingly important in construction, industrial manufacturing, and healthcare, as documented workflows now carry greater operational value. AI is influencing this mix as a shared layer rather than a separate application category. In March 2026, BCG reported that AI-based scheduling tools reduced average hold times by 15% to 30% and lowered transfer rates by 20% to 30% at a state agency call center. That kind of result helps explain why buyers want analytics tools that can show operational outcomes in plain language. The North America frontline worker technology market is thus giving more weight to applications that validate return on investment, not only those that digitize communication.

By End-User Industry: Logistics Growth Reshapes the Market's Vertical Mix

Retail and e-commerce accounted for 25.45% of the end-user mix in 2025, keeping the segment in the lead due to its large frontline workforce and established use of scheduling, scanning, and task tools. Transportation and logistics are forecast to grow the fastest at a 24.87% CAGR through 2031. This points to a gradual change in the North America frontline worker technology market as warehouse, freight, and distribution operations become more digitized. Retail remains important because the scale of daily frontline coordination continues to create a strong need for communication and knowledge tools. The input also noted that frontline employees in US retail spent 14 hours per week helping coworkers address knowledge gaps, resulting in significant productivity losses and reinforcing the case for better connected-worker platforms.

Industrial manufacturing, healthcare and life sciences, hospitality, construction, and government and public administration all contribute to the North America frontline worker technology market through different operational needs. Healthcare demand is supported by scheduling optimization and workflow automation, while manufacturing demand is tied to guided work, quality, and safety. Transportation and logistics are expanding faster as nearshoring increases freight and warehouse activity across the US-Mexico corridor. The input also highlighted that regulatory expectations for traceability and safety are pushing logistics operators toward real-time digital workflows. That combination is shifting more future opportunities in the North America frontline worker technology market toward logistics-led use cases.

Geography Analysis

The United States accounted for 83.44% of the North America frontline worker technology market in 2025, making it the dominant country in the region. This position reflects the scale of US retail, healthcare, logistics, and manufacturing workforces, as well as a mature cloud infrastructure base. Compliance also plays a central role because federal and state frameworks are pushing employers toward auditable frontline systems. California’s worker surveillance and employee data rules are strengthening that pressure by raising expectations for governance and data handling in workplace technology.[2]California State Legislature, “AB-1221 Workplace Surveillance Tools (2025-2026),” California Legislative Information, leginfo.legislature.ca.gov The North America frontline worker technology market remains heavily anchored in the United States because large multi-site employers there can scale deployments faster than peers elsewhere in the region.

Canada remained the second-largest geography in the North America frontline worker technology market. Demand is being shaped by healthcare digitization, regulated workplace practices, and the need to support distributed operations across remote sites. Long-term care facilities and remote community health environments are raising demand for connected communication, scheduling, and task management tools. Resource industries such as mining, forestry, and energy also create demand for offline-capable platforms because standard cloud-first tools are not always practical in remote locations.

Mexico is projected to record the fastest regional CAGR at 25.91% through 2026-2031 in the North America frontline worker technology market. Nearshoring inflows are expanding manufacturing and logistics capacity in border states, which is increasing the need for digitized quality, safety, and communication workflows. Multinational customer requirements are also accelerating adoption because maquiladoras are being asked to meet supplier audit expectations more consistently. This creates a strong case for vendors that can support shared platforms across US headquarters operations and Mexican production sites.

Competitive Landscape

The North America frontline worker technology market is moderately fragmented, with no single vendor holding a commanding position across every sub-segment. Competition spans hardware providers, enterprise software companies, and pure-play frontline platforms, which keeps the field active and layered. Zebra Technologies and Honeywell are both extending beyond devices into software and workflow support to protect their role in frontline operations. Zebra announced the acquisition of Elo Touch Solutions for USD 1.3 billion in August 2025, which expanded its reach in connected frontline experiences across retail, hospitality, healthcare, and industrial settings. Honeywell also launched Performance+ for Guided Work in January 2026 to deliver AI-guided task instructions for supply chain operations.

Enterprise software vendors are competing in the North America frontline worker technology market by embedding frontline-specific automation into broader workflow environments. ServiceNow introduced its Industrial Connected Workforce solution in June 2026 to digitize standard operating procedures into AI-guided tasks delivered at the point of need. That move shows how major workflow platforms are working to close the gap between factory-floor execution and enterprise back-office systems. Pure-play vendors are responding by emphasizing integration depth, operational fit, and faster time-to-value. Augmentir’s connector expansion for platforms such as IBM Maximo, AVEVA, and SAP illustrates how this part of the North America frontline worker technology market is competing through interoperability.

The white-space opportunity in the North America frontline worker technology market sits where AI orchestration, rugged delivery, and governance requirements overlap. Samsara’s June 2026 Agent Studio launch demonstrated how vendors are enabling operators to build or deploy AI agents without custom development. Honeywell’s June 2026 safety software release showed a parallel push toward live visibility and alerts in hazardous work environments.[3]Honeywell, “Honeywell Launches New Performance+ for Guided Work to Enable Faster, Smarter Supply Chain Operations,” Honeywell, honeywell.com As compliance expectations rise, vendors with stronger governance architecture and deployment credibility are likely to be more competitive in regulated use cases.

North America Frontline Worker Technology Industry Leaders

Zebra Technologies Corporation

Honeywell International Inc.

Datalogic S.p.A.

Microsoft Corporation

Oracle Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: ServiceNow expanded its strategic partnership with Microsoft to integrate ServiceNow AI Control Tower with Microsoft Agent 365, enabling governance of AI agents across the Microsoft 365 toolset used by frontline workers. The integration addresses the agent sprawl risk that enterprises face as AI deployments multiply across communication, scheduling, and analytics applications.

- June 2026: At HANNOVER MESSE, ServiceNow unveiled its Industrial Connected Workforce solution, which digitizes standard operating procedures into AI-guided, step-by-step tasks and delivers contextual knowledge at the point of need, directly addressing the digital gap between factory-floor execution and enterprise back-office systems.

- June 2026: Samsara launched new agentic capabilities for physical operations, including a first-of-its-kind Agent Studio that enables teams to deploy pre-configured AI agents or build custom agents from scratch for logistics and field operations, removing the need for custom development that had limited agentic AI deployment at the frontline.

- June 2026: Honeywell launched enhanced industrial software providing real-time visibility into worksite safety, extending its connected worker portfolio with monitoring and alerting capabilities designed for hazardous industrial environments.

North America Frontline Worker Technology Market Report Scope

The North America Frontline Worker Technology Market includes technology solutions and platforms that equip frontline employees across the United States and Canada with digital tools for communication, collaboration, task management, training, workflow automation, and operational support. The market covers mobile workforce applications, wearable technologies, digital work instructions, workforce productivity platforms, and connected worker solutions used across key sectors such as manufacturing, healthcare, retail, logistics, construction, and energy. High enterprise technology adoption, ongoing workforce digitization initiatives, and increasing investment in connected worker ecosystems support market growth. The market aims to improve workforce productivity, operational efficiency, employee experience, safety, and real-time decision-making across frontline operations.

The North America Frontline Worker Technology Market Report is Segmented by Component (Software, and Services), Deployment (Cloud-Based, Hybrid, and On-Premises), Organization Size (Large Enterprises, and Small and Medium Enterprises), Application (Employee Communication and Engagement, Workforce Execution and Task Management, Workforce Scheduling and Coordination, Learning and Knowledge Enablement, Workforce Analytics and Performance Management, Safety and Compliance Management, and Other Applications), End-User Industry (Retail and E-Commerce, Industrial Manufacturing, Healthcare and Life Sciences, Transportation and Logistics, Hospitality, Construction, Government and Public Administration, and Other End-User Industries), and Geography (United States, Canada, and Mexico). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud-Based |

| Hybrid |

| On-Premises |

| Large Enterprises |

| Small and Medium Enterprises |

| Employee Communication and Engagement |

| Workforce Execution and Task Management |

| Workforce Scheduling and Coordination |

| Learning and Knowledge Enablement |

| Workforce Analytics and Performance Management |

| Safety and Compliance Management |

| Other Applications |

| Retail and E-Commerce |

| Industrial Manufacturing |

| Healthcare and Life Sciences |

| Transportation and Logistics |

| Hospitality |

| Construction |

| Government and Public Administration |

| Other End-User Industries |

| United States |

| Canada |

| Mexico |

| By Component | Software |

| Services | |

| By Deployment | Cloud-Based |

| Hybrid | |

| On-Premises | |

| By Organization Size | Large Enterprises |

| Small and Medium Enterprises | |

| By Application | Employee Communication and Engagement |

| Workforce Execution and Task Management | |

| Workforce Scheduling and Coordination | |

| Learning and Knowledge Enablement | |

| Workforce Analytics and Performance Management | |

| Safety and Compliance Management | |

| Other Applications | |

| By End-User Industry | Retail and E-Commerce |

| Industrial Manufacturing | |

| Healthcare and Life Sciences | |

| Transportation and Logistics | |

| Hospitality | |

| Construction | |

| Government and Public Administration | |

| Other End-User Industries | |

| By Geography | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

What is the 2026 value of the North America frontline worker technology market?

The North America frontline worker technology market stood at USD 6.09 billion in 2026 and is forecast to reach USD 15.36 billion by 2031 at a 20.32% CAGR.

Which component generates the largest revenue in frontline worker technology across North America?

Software remained the largest component, with an 80.21% share in 2025, reflecting the strong move toward platform-led deployments.

Why are cloud-based platforms leading adoption across frontline workplaces in North America?

Cloud-based deployment held 78.05% share in 2025 and is also projected to grow at a 25.58% CAGR because it supports centralized management, updates, and data visibility across large workforces.

Which organization size is growing fastest in this space?

SMEs are expected to post the fastest growth at a 26.44% CAGR through 2031 as SaaS pricing and mobile-first delivery reduce adoption barriers.

Which application area is expanding the fastest in frontline worker technology?

Workforce analytics and performance management is projected to grow at a 25.12% CAGR because employers want clearer proof of productivity, retention, and workflow gains.

Which country offers the fastest growth opportunity in North America?

Mexico is projected to grow the fastest at a 25.91% CAGR through 2031, supported by nearshoring, supplier compliance needs, and expanding manufacturing and logistics capacity.

Page last updated on: