North America Dipeptidyl Peptidase-4 (DPP-4) Inhibitors Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

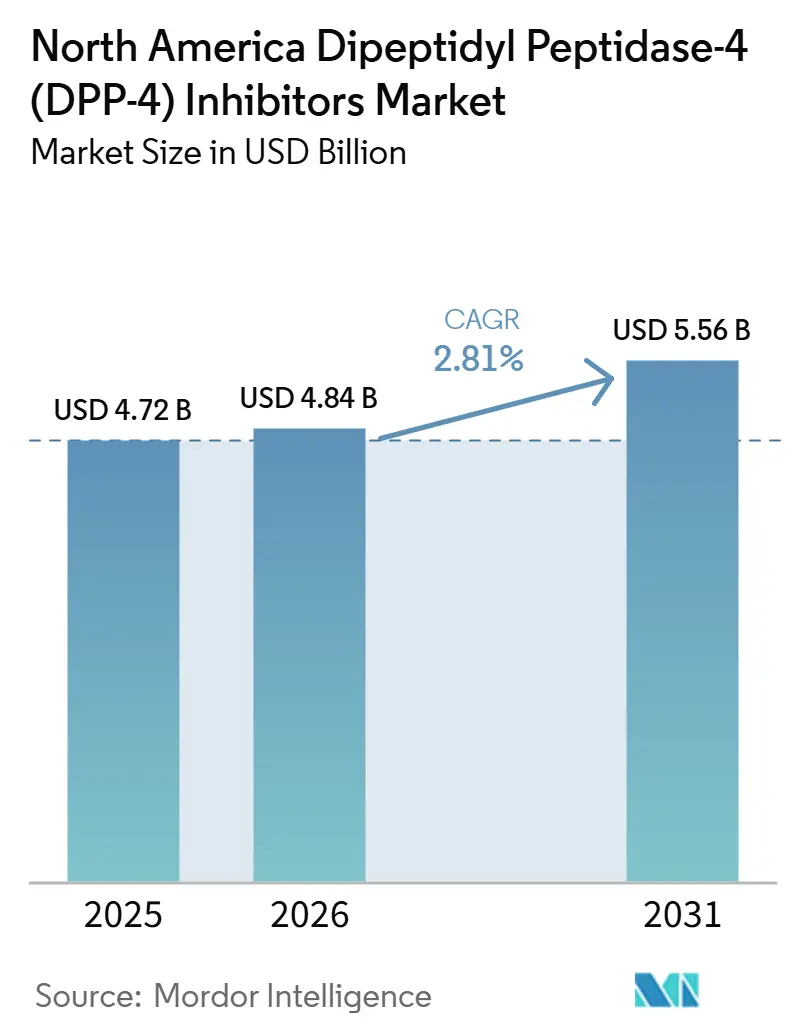

| Base Year Market Size (2025) | USD 4.72 Billion |

| Market Size (2026) | USD 4.84 Billion |

| Market Size (2031) | USD 5.56 Billion |

| Growth Rate (2026 - 2031) | 2.81% CAGR |

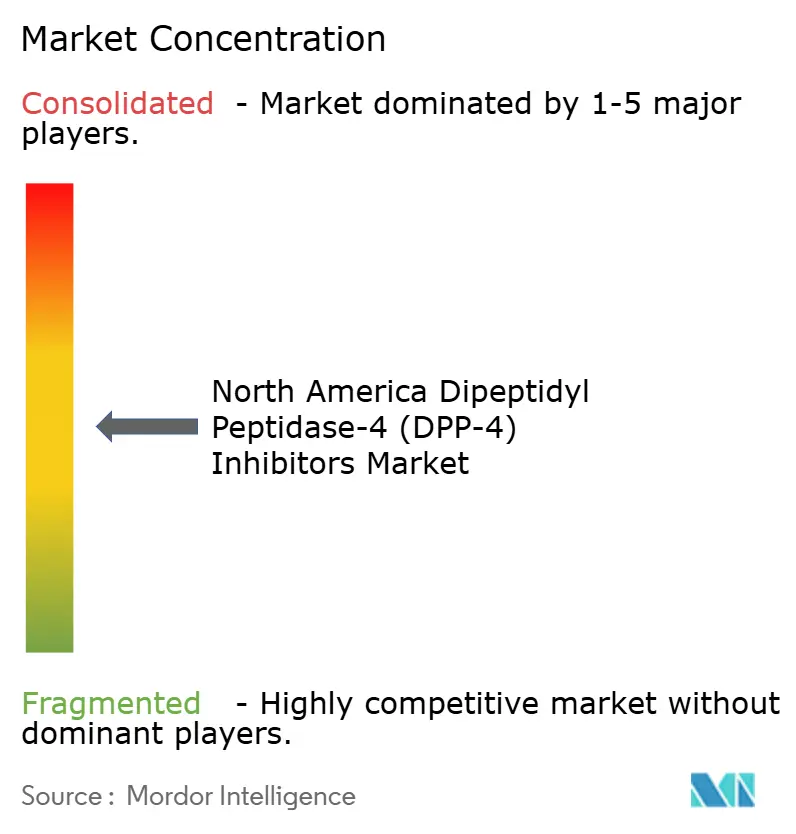

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Dipeptidyl Peptidase-4 (DPP-4) Inhibitors Market Analysis by Mordor Intelligence

The North America Dipeptidyl Peptidase-4 Inhibitors Market size is projected to expand from USD 4.72 billion in 2025 and USD 4.84 billion in 2026 to USD 5.56 billion by 2031, registering a CAGR of 2.81% between 2026 to 2031.

The North America DPP-4 inhibitors market is moving through a transition in which sitagliptin keeps its leading drug position while generic entry broadens treatment access and reduces branded pricing power. The region also carries the highest macroeconomic burden from diabetes mellitus globally at 0.3% of GDP, which keeps long-term demand for oral glucose-lowering therapies structurally firm even as treatment preferences evolve. The United States remained the core revenue base with 83.7% of regional sales in 2025, and the care system still serves a very large patient pool because 40.1 million people in the country had diabetes, and 11.0 million adults remained undiagnosed. Even with rising competitive pressure from newer classes, the North American DPP-4 inhibitors market still holds a durable place among older adults, people who need oral therapy, and patients who cannot readily use alternatives because tolerability and treatment simplicity remain important in routine maintenance care. The competitive structure of the North America DPP-4 inhibitors market is therefore shifting from a branded originator model toward a broader multi-manufacturer environment, where volume can rise while pricing becomes harder to defend.

Key Report Takeaways

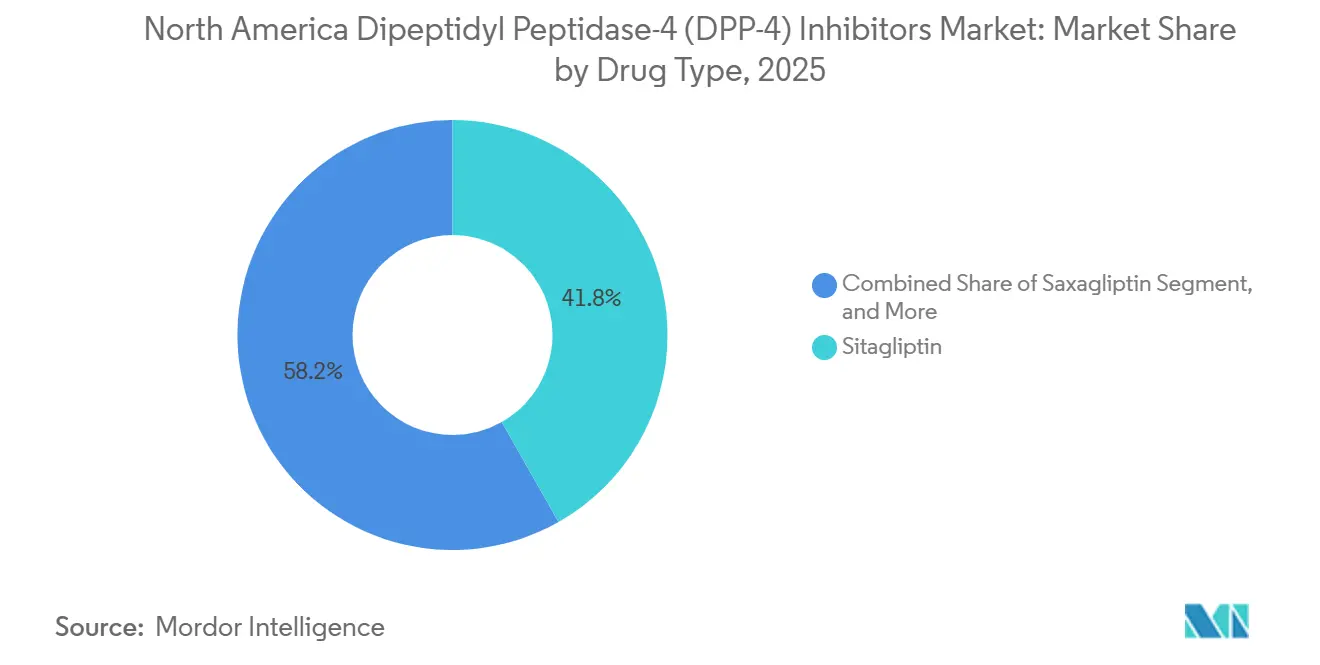

- By drug type, sitagliptin held 41.83% of revenue in 2025 and also remained the fastest growing drug with 3.38% CAGR through the forecast period.

- By medication type, branded medication held 76.38% of the North America DPP-4 inhibitors market share in 2025, while generic medication recorded the highest projected CAGR at 4.08% through 2031.

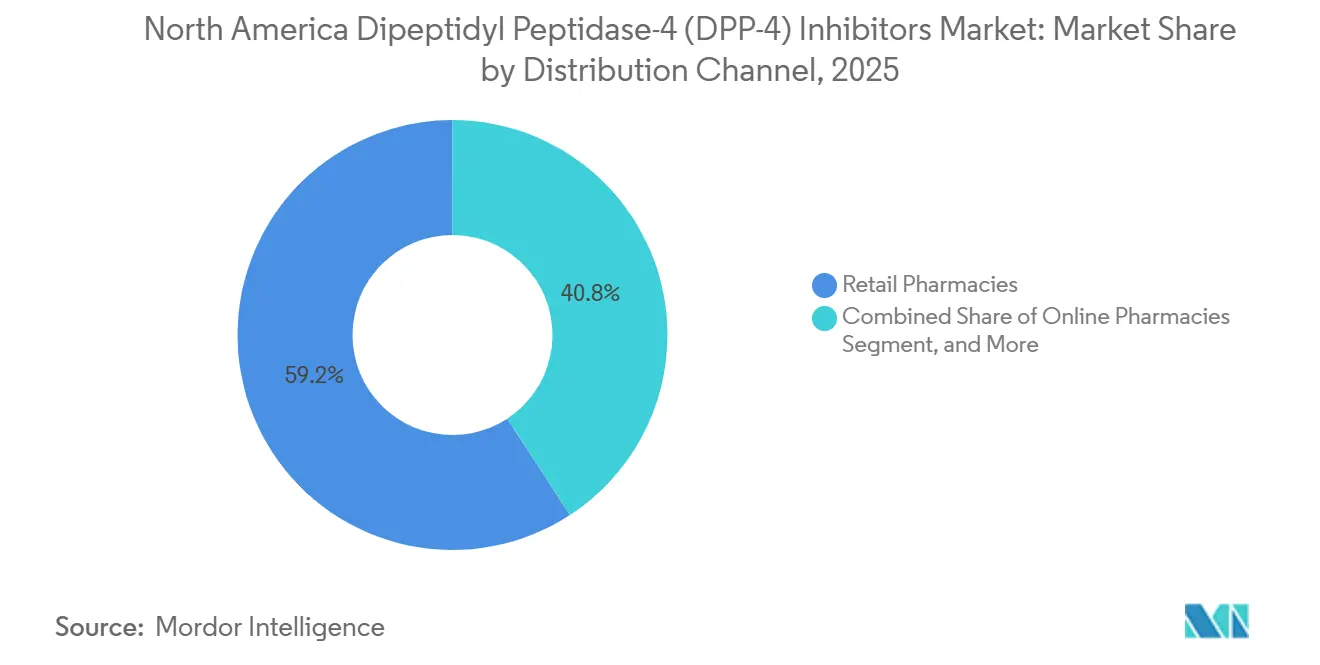

- By distribution channel, retail pharmacies accounted for 59.16% of the North America DPP-4 inhibitors market size in 2025, while online pharmacies advanced at the fastest CAGR of 4.32% through 2031.

- By geography, the United States held 83.72% of the North America DPP-4 inhibitors market share in 2025, while Mexico posted the highest projected CAGR at 5.98% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Dipeptidyl Peptidase-4 (DPP-4) Inhibitors Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Type 2 Diabetes Burden Across North America | +0.6% | United States and Mexico primarily, Canada secondary | Long term (≥ 4 years) |

| Preference for Oral, Low-Hypoglycemia Therapies in Older Adults | +0.5% | United States, Canada | Medium term (2-4 years) |

| Genericization and Formulary Repositioning of Legacy Brands | +0.4% | United States primarily, spillover into Mexico and Canada | Short term (≤ 2 years) |

| Medicare and PBM Coverage for Cost-Conscious Maintenance Therapy | +0.4% | United States | Short term (≤ 2 years) |

| CV Safety Differentiation and Renal-Dose Simplicity in Mixed-Comorbidity Patients | +0.3% | United States and Canada | Medium term (2-4 years) |

| Prescription Conversion from Injectable to Oral Maintenance Therapy | +0.2% | United States and Canada | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Type 2 Diabetes Burden Across North America

The North America DPP-4 inhibitors market continues to draw support from a diabetes burden that remains large, persistent, and still underdiagnosed across major countries. High-income North America recorded the highest increase in age-standardized type 2 diabetes incidence among world regions between 1990 and 2021, which points to a demand base that is not easing.[1]Frontiers in Endocrinology, “Global Burden and Risk Factors of Type 2 Diabetes Mellitus from 1990 to 2021, with Forecasts to 2050,” Frontiers Media, frontiersin.org In the United States, 40.1 million people had diabetes as of 2023, representing 12.0% of the total population, and 11.0 million adults remained undiagnosed, which keeps the treated pool open to further expansion as screening improves. Mexico adds another layer of demand because 13.6 million adults lived with diabetes in 2024, and 41.3% of cases were undiagnosed, leaving a large untreated group that can move into medication use over time. The ENSANUT 2021 to 2024 survey also showed that national type 2 diabetes prevalence reached 17.0% and only 33% of diagnosed patients achieved glycemic control, which supports continuing use of affordable oral therapies as access improves. As a result, the North America DPP-4 inhibitors market keeps a wide underlying patient base even when competitive intensity rises in higher value treatment lines.

Preference for Oral, Low-Hypoglycemia Therapies in Older Adults

The North America DPP-4 inhibitors market also benefits from the fact that older adults often need glucose lowering agents with simple use patterns and a low risk of hypoglycemia. The American Diabetes Association stated in its 2025 standards that DPP-4 inhibitors carry low hypoglycemia risk and are weight neutral, which makes them suitable for many adults aged 65 and older who face polypharmacy or fall risk.[2]American Diabetes Association, “Standards of Care in Diabetes 2025, Older Adults,” Diabetes Care, diabetesjournals.org A June 2026 study in Cardiovascular Diabetology found notable safety signals for SGLT2 inhibitors in adults aged 80 and older, which can preserve room for DPP-4 use in a fast growing super elderly cohort. A separate 2025 study in Drugs & Aging showed lower rates of hypoglycemia, falls, and fractures for DPP-4 inhibitors versus sulfonylureas in older adults, which reinforces their role in routine maintenance therapy. This clinical profile matters because 52.1% of U.S. adults aged 65 and older had prediabetes, so the future treatment pool in this age group remains large. These care patterns help the North America DPP-4 inhibitors market hold relevance even while newer therapies draw attention in broader cardiometabolic care.

Genericization and Formulary Repositioning of Legacy Brands

The North America DPP-4 inhibitors market is being reshaped by generic sitagliptin, which is changing both affordability and revenue mix at the same time. Apotex launched generic sitagliptin tablets and sitagliptin and metformin hydrochloride tablets in the United States in June 2026, and the products were eligible for 180-day shared exclusivity, which confirms that the transition from protected brand to broader access is now active. That shift matters because cost-sensitive patients who were previously limited by branded pricing can enter maintenance therapy more easily once multiple suppliers build presence. It also changes formulary conversations because payers can keep an established oral class in use at a lower cost while preserving therapy options for older adults and mixed comorbidity patients. In that setting, the North America DPP-4 inhibitors market can still expand in treated patient count even when branded revenue concentration softens.

Medicare and PBM Coverage for Cost-Conscious Maintenance Therapy

The North American DPP-4 inhibitors market is also influenced by payer structures that increasingly push diabetes treatment toward cost-controlled maintenance options. A RAND published study in the Journal of General Internal Medicine found that the median share of diabetes drugs with coinsurance in Medicare prescription drug plans rose sharply between 2023 and 2024, showing that access design is becoming more financially selective for patients.[3]Journal of General Internal Medicine, “Trends in Medicare Part D Formulary Coverage for Non-Insulin Diabetes Medications, 2020–2024,” Springer, doi.org In this environment, lower-cost DPP-4 products can remain useful when plans try to manage long-term medication spending without disrupting oral treatment continuity. That is especially relevant in the United States because Medicare-linked patients make up a large and growing share of the diabetes population and often require stable chronic therapy rather than frequent regimen switching. The class also benefits from its practical fit in maintenance care because oral administration, broad familiarity, and a comparatively mild hypoglycemia profile align well with long-term use. Together, these conditions keep the North American DPP-4 inhibitors market tied closely to payer decisions even when competitive pressure shifts first line attention toward other drug categories.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| GLP-1 Receptor Agonist Substitution in Treatment Algorithms | -0.5% | United States primarily, with spillover into Canada | Short term (≤ 2 years) |

| Patent Expiry and Rapid Price Erosion in Branded Sitagliptin and Related Products | -0.4% | United States primarily | Short term (≤ 2 years) |

| Prior-Authorization Pressure and Step-Therapy Controls on Branded Oral Antidiabetics | -0.2% | United States | Short term (≤ 2 years) |

| Safety Signal Sensitivity Around Heart Failure and Pancreatic Risk in Labeling and Prescribing | -0.1% | United States and Canada | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

GLP-1 Receptor Agonist Substitution in Treatment Algorithms

The clearest restraint on the North American DPP-4 inhibitors market is the steady movement of treatment algorithms toward GLP-1 receptor agonists and, in some settings, other newer therapies with stronger cardiometabolic positioning. The shift narrows the addressable pool for DPP-4 inhibitors in patients with high body mass index, established cardiovascular disease, or a stronger need for weight reduction, where prescribers often look beyond older oral classes first. It also limits future pricing power because branded DPP-4 products must compete in a care model where therapeutic differentiation is being judged more heavily on outcomes beyond glycemic control. At the same time, the arrival of generic sitagliptin can soften some volume loss by keeping the class affordable for patients who still need oral treatment, but it cannot fully offset the pressure on branded value. The United States feels this restraint most strongly because commercial payer management, specialist prescribing patterns, and faster adoption of premium diabetes therapies all raise the intensity of substitution. As a result, the North America DPP-4 inhibitors market is likely to preserve a narrower but still important role rather than recover broad first line preference.

Safety Signal Sensitivity Around Heart Failure and Pancreatic Risk in Labeling and Prescribing

The North America DPP-4 inhibitors market also faces a restraint from class-level caution around heart failure and pancreatic safety, especially in patients with heavier comorbidity burdens. A 2024 real-world analysis using the FDA Adverse Event Reporting System identified a pancreatitis reporting signal for DPP-4 inhibitors with a reporting odds ratio of 13.2, which keeps safety perception under close review even when those findings do not apply equally across every molecule. This caution tends to reinforce payer review, label awareness, and physician selectivity, especially when other diabetes drug classes are already competing for the same patients. It also makes weaker branded products more exposed at the point where generic price erosion is already reducing room for premium positioning. The effect is not a collapse in class use, because clinicians still distinguish between individual products and specific patient profiles, but it does slow broader expansion. In practical terms, the North American DPP-4 inhibitors market remains usable in well-selected maintenance therapy settings while carrying less flexibility in higher-risk treatment pathways.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Type: Sitagliptin Extends Volume Leadership Into the Generic Era

Sitagliptin captured 41.83% of revenue in 2025, giving it the leading position within the North America DPP-4 inhibitors market and the clearest base for continued scale during the forecast period. The molecule benefits from long prescriber familiarity, broad historical use, and a well-understood place in oral diabetes management, which keeps it central even as the market moves into a lower-priced phase. Sitagliptin also remained the fastest-growing drug type with a CAGR 3.38% through 2031, which is unusual for the largest segment but logical in a period shaped by generic availability and wider access. In June 2026, Apotex launched generic sitagliptin tablets and sitagliptin and metformin hydrochloride tablets in the United States, adding concrete evidence that supply is broadening beyond the originator model. That timing matters because the North American DPP-4 inhibitors market can now pull in patients who were previously priced out of the class while still relying on a molecule that physicians already know well.

The second layer of the drug type picture is defined by how other molecules serve narrower but still important niches within the North American DPP-4 inhibitors industry. Linagliptin retained a meaningful role because no renal dose adjustment is needed across chronic kidney disease stages, which makes it especially relevant when prescribers treat older adults with renal impairment. Saxagliptin and alogliptin face a more constrained path because safety caution has weighed on their positioning, leaving less room for wide commercial expansion. Vildagliptin remained limited in North America because its regional footprint is far narrower than the leading products and does not change the overall category structure. These conditions leave sitagliptin as the main anchor of volume, while the remaining molecules compete more on clinical fit than on broad market reach. The result is a segment in which leadership is stable, but the terms of that leadership are moving from brand strength toward accessibility and substitution.

By Medication Type: Generic Wave Reshapes Revenue Architecture

Branded medication held 76.38% of segment revenue in 2025, which shows how strongly the North America DPP-4 inhibitors market had been shaped by protected products and established originator franchises. This branded base reflected the commercial strength of products such as Januvia, Janumet, and Tradjenta, along with the slower pace of generic conversion before 2026. Even so, generic medication is forecast to expand at a 4.08% CAGR through 2031, making it the fastest-growing medication type as sitagliptin supply widens and affordability improves. The branded side, therefore, remains larger at the start of the forecast window, but its revenue concentration is set to weaken as more lower-cost alternatives secure payer acceptance. This shift is central to the North American DPP-4 inhibitors market because it changes the balance between value capture and prescription volume rather than simply replacing one supplier with another.

The longer implication is that the North American DPP-4 inhibitors industry will look less like a premium brand category and more like a mixed market where pricing discipline matters at every level. Generic entry should expand access among cost-sensitive patients, but it will also make it harder for legacy brands to preserve historic margins unless they offer a clear clinical advantage or strong combination positioning. That leaves branded products more dependent on patients who need specific dosing features, renal convenience, or established tolerability in long-term maintenance settings. At the same time, generic competition is likely to broaden manufacturer participation and reduce concentration around a small number of originators. This movement does not eliminate the role of brands, because some products still benefit from differentiated clinical fit and delayed generic pressure. It does, however, mean that the segment is becoming structurally more volume-led than price-led.

By Distribution Channel: Online Pharmacies Gain Ground as Retail Networks Contract

Retail pharmacies accounted for 59.16% of distribution channel revenue in 2025, which made them the largest channel in the North America DPP-4 inhibitors market size at the start of the forecast period. Their lead reflects long-standing prescription fill behavior, broad local access, and the routine use of chain and independent stores for chronic diabetes therapy. Even with that large installed base, online pharmacies are projected to grow at a 4.32% CAGR through 2031, making them the fastest-growing distribution channel. The appeal is straightforward because DPP-4 inhibitors fit refill-based care very well, do not require refrigeration, and can be managed easily in recurring digital dispensing models. That practical fit gives the North American DPP-4 inhibitors market a natural path toward higher online penetration as patients look for lower prices and convenient repeat ordering.

Retail pharmacies are still expected to remain the main revenue channel because they handle broad prescription traffic and support patient access across urban and community settings. Hospital pharmacies play a narrower role, mostly tied to inpatient diabetes management, integrated systems, and more controlled formulary use where product choice can reflect local care protocols. Online growth, however, should keep accelerating as generic sitagliptin becomes easier to source through digital platforms and price transparency improves for maintenance medication users. This matters because channel expansion can reinforce generic uptake faster than a store-led model alone, especially when refill schedules are predictable. The segment, therefore, combines a stable retail core with a rising digital path that fits the evolving economics of long-term diabetes treatment. In effect, channel change supports the broader transition of the North American DPP-4 inhibitors market from protected brand franchises toward lower-cost recurring use.

Geography Analysis

The United States accounted for 83.72% of regional revenue in 2025, which made it the main commercial center of the North America DPP-4 inhibitors market. Its scale comes from a large treated population, a complex but deep payer infrastructure, and steady prescription demand for chronic diabetes maintenance therapy. The country also carries a very large underlying patient base because 40.1 million people had diabetes and 11.0 million adults remained undiagnosed, which means treatment demand can still widen as detection improves. Older adults add another layer of support because 52.1% of adults aged 65 and older had prediabetes, giving prescribers a continued stream of patients who may later require oral agents with manageable safety profiles. Even with heavy competition from newer drug classes, the United States remains the place where pricing, channel shifts, and generic adoption will shape the broader direction of the North America DPP-4 inhibitors market first.

Mexico is the fastest-growing geography with a 5.98% CAGR through 2031, and that pace reflects both disease burden and treatment underuse within the North America DPP-4 inhibitors market size. The country had 13.6 million adults living with diabetes in 2024, and the age-standardized prevalence reached 16.4%, which already placed it among the region's highest need areas. Diabetes attributable deaths reached 123,365 in 2024 and diabetes related health expenditure stood at USD 19.5 billion, which shows the scale of the pressure on the health system and the need for more affordable chronic therapy options. The 41.3% undiagnosed rate also matters because it indicates that active treatment demand is still materially below the true patient pool. When combined with low glycemic control rates, this keeps Mexico as the clearest growth pocket in the North America DPP-4 inhibitors market.

Canada holds a smaller share of regional demand, but it remains part of the North America DPP-4 inhibitors market through steady chronic disease management needs and a structured reimbursement setting. The country contributes a more stable and measured profile than the United States or Mexico because its treatment base is established and its formulary pathways are comparatively disciplined. DPP-4 inhibitors therefore, remain relevant mainly where patients need oral therapy simplicity, low hypoglycemia risk, or a practical option within broader diabetes management plans. That leaves Canada as a supporting geography rather than a growth engine, but it still adds continuity to regional demand and helps sustain a balanced three-country market structure.

Competitive Landscape

The North America DPP-4 inhibitors market has historically been led by a small innovator group, but that structure is now loosening as generic participation expands. Merck remained the most visible originator because the Januvia and Janumet franchise set the commercial tone for sitagliptin over many years and established the class at large scale. Boehringer Ingelheim and Eli Lilly held an important position through Tradjenta, especially in patients where renal dose simplicity improved the product's clinical fit. AstraZeneca also remained part of the branded field through saxagliptin, although its commercial room was narrower than that of the leading products. This leaves the North America DPP-4 inhibitors market with a branded core that is still influential, but no longer able to control the category in the same concentrated way as before.

The strongest strategic move in 2026 came from generic sitagliptin launches, because they changed access dynamics faster than most other developments in the category. In June 2026, Apotex launched generic sitagliptin tablets and sitagliptin and metformin hydrochloride tablets in the United States, and the products were eligible for 180 day shared exclusivity, which marked a major step in the market's move toward multi supplier competitioN. Merck, meanwhile, entered the loss of exclusivity phase with the Januvia and Janumet franchise recording USD 574 million in Q1 2026 revenue, down from USD 796 million in Q1 2025, which shows how quickly branded erosion can appear once generic timing becomes visible. Boehringer Ingelheim responded through positioning rather than price, continuing to lean on linagliptin's no renal dose adjustment profile to protect its place in selected patient groups. Together, these moves show that the North America DPP-4 inhibitors market is now being shaped by defensive brand strategy on one side and scaled generic entry on the other.

A third strategic example came from supply chain localization, which matters because stable production supports continuity in a category built on long term refills. In October 2025, Boehringer Ingelheim launched local production of Tradjenta at its Zhangjiang human drug production base in Shanghai, strengthening supply support for the linagliptin franchise and reducing dependence on a narrower manufacturing footprint. As more Indian, Canadian, and multinational generic manufacturers move into the category, competitive advantage is likely to depend increasingly on dependable supply, formulary reach, and price discipline rather than on new molecule creation. The North America DPP-4 inhibitors market therefore remains moderately concentrated in legacy brand influence, but it is clearly moving toward a more fragmented operating model.

North America Dipeptidyl Peptidase-4 (DPP-4) Inhibitors Industry Leaders

AstraZeneca

Boehringer Ingelheim

Eli Lilly and Company

Merck and Co.

Novartis

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Apotex Corp. launched generic sitagliptin tablets and sitagliptin/metformin hydrochloride tablets in the United States, both AB-rated to Merck's Januvia and Janumet and eligible for 180-day shared exclusivity. Available in 25 mg, 50 mg, and 100 mg strengths, the products expand affordable DPP-4 access for millions of patients previously constrained by the branded pricing of USD 600 to 700 per month.

- May 2026: Sandoz launched generic sitagliptin tablets and sitagliptin/metformin tablets in the United States under 180-day shared exclusivity, co-entering the market alongside Apotex ahead of Merck's November 2026 core patent expiration. The dual manufacturer simultaneous launch signaled an organized market entry coordinated through prior settlement agreements with Merck.

- December 2025: Watson Labs, now Viatris, received FDA approval for generic sitagliptin phosphate, AB-rated to Januvia, becoming the first company to secure full generic equivalence approval for the North American DPP-4 market's largest molecule, paving the way for commercial launch under settlement terms with Merck.

- October 2025: Boehringer Ingelheim officially launched local production of Tradjenta, linagliptin, at its Zhangjiang human drug production base in Shanghai, consolidating an Asia Pacific supply hub that supports North American distribution continuity and reduces single source API risk for the linagliptin franchise.

North America Dipeptidyl Peptidase-4 (DPP-4) Inhibitors Market Report Scope

| Sitagliptin |

| Saxagliptin |

| Linagliptin |

| Alogliptin |

| Vildagliptin |

| Other Drug Types |

| Branded Medication |

| Generic Medication |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| United States |

| Canada |

| Mexico |

| By Drug Type | Sitagliptin |

| Saxagliptin | |

| Linagliptin | |

| Alogliptin | |

| Vildagliptin | |

| Other Drug Types | |

| By Medication Type | Branded Medication |

| Generic Medication | |

| By Distribution Channel | Hospital Pharmacies |

| Retail Pharmacies | |

| Online Pharmacies | |

| By Country | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

What is the 2031 value forecast for North America DPP-4 inhibitors?

The North America DPP-4 inhibitors market is forecast to reach USD 5.56 billion by 2031, rising from USD 4.84 billion in 2026 at a 2.81% CAGR over 2026 to 2031.

Which drug type leads DPP-4 inhibitor sales in North America?

Sitagliptin led the drug type segment with 41.83% revenue share in 2025 and also remained the fastest-growing drug type through the forecast period.

Why do DPP-4 inhibitors still matter when newer diabetes drugs are available?

They remain useful for older adults and patients who need oral therapy with low hypoglycemia risk, and ADA guidance continues to support that clinical fit.

Which country is driving the fastest expansion in the region?

Mexico is the fastest growing country segment with a 5.98% CAGR through 2031, supported by high diabetes prevalence, a large undiagnosed pool, and low glycemic control rates.

How is generic sitagliptin changing the competitive picture?

Generic launches are widening access and reducing branded pricing power, which shifts competition from brand control toward volume, supply reliability, and formulary reach.

Page last updated on: