North America Deck Design Software Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

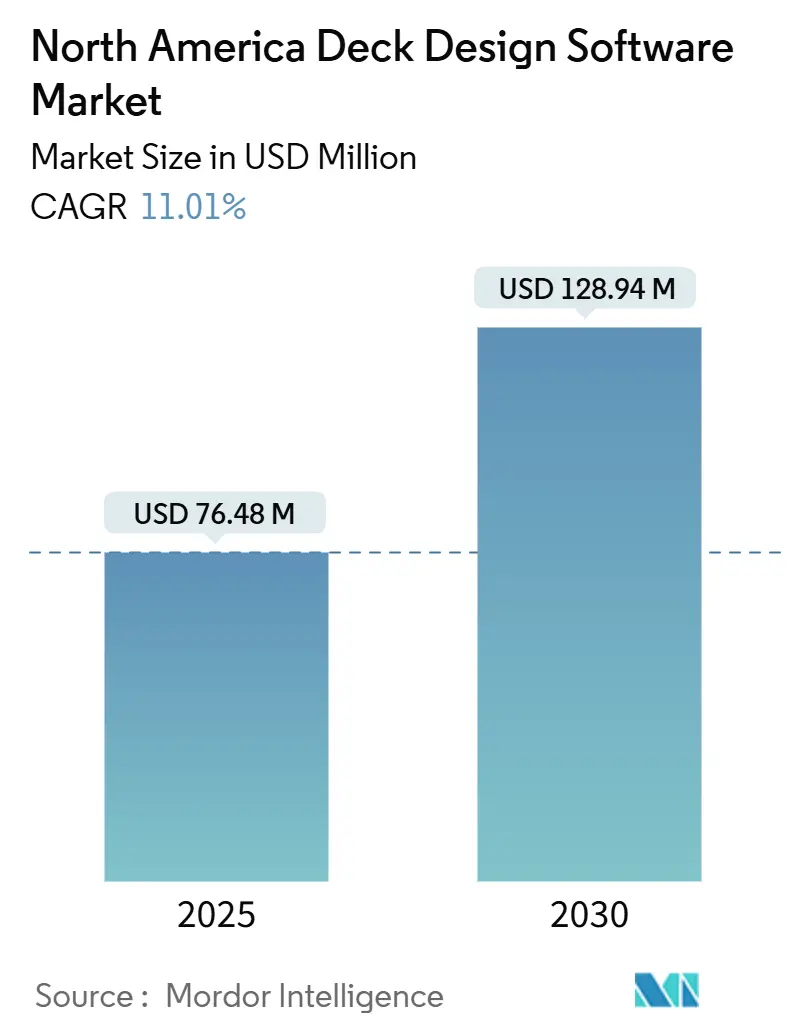

| Market Size (2025) | USD 76.48 Million |

| Market Size (2030) | USD 128.94 Million |

| Growth Rate (2025 - 2030) | 11.01% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Deck Design Software Market Analysis by Mordor Intelligence

The North America deck design software market size is estimated at USD 76.48 million in 2025 and is projected to reach USD 128.94 million by 2030, representing a 11.01% CAGR. This growth is driven by renovation demand from the aging housing stock, post-pandemic DIY momentum, and widespread access to cloud-based 3D visualization, which places professional-grade tools in the hands of homeowners and contractors. Subscription pricing accelerates adoption by lowering up-front costs, while integrated design-to-purchase workflows offered by home-improvement retailers streamline project execution. Smart-home integration requirements and stricter building-code compliance further expand the addressable user base. Competitive intensity rises as CAD incumbents, niche platforms, and retailer-backed tools chase market share through AI-driven automation, collaboration features, and ecosystem partnerships.

Key Report Takeaways

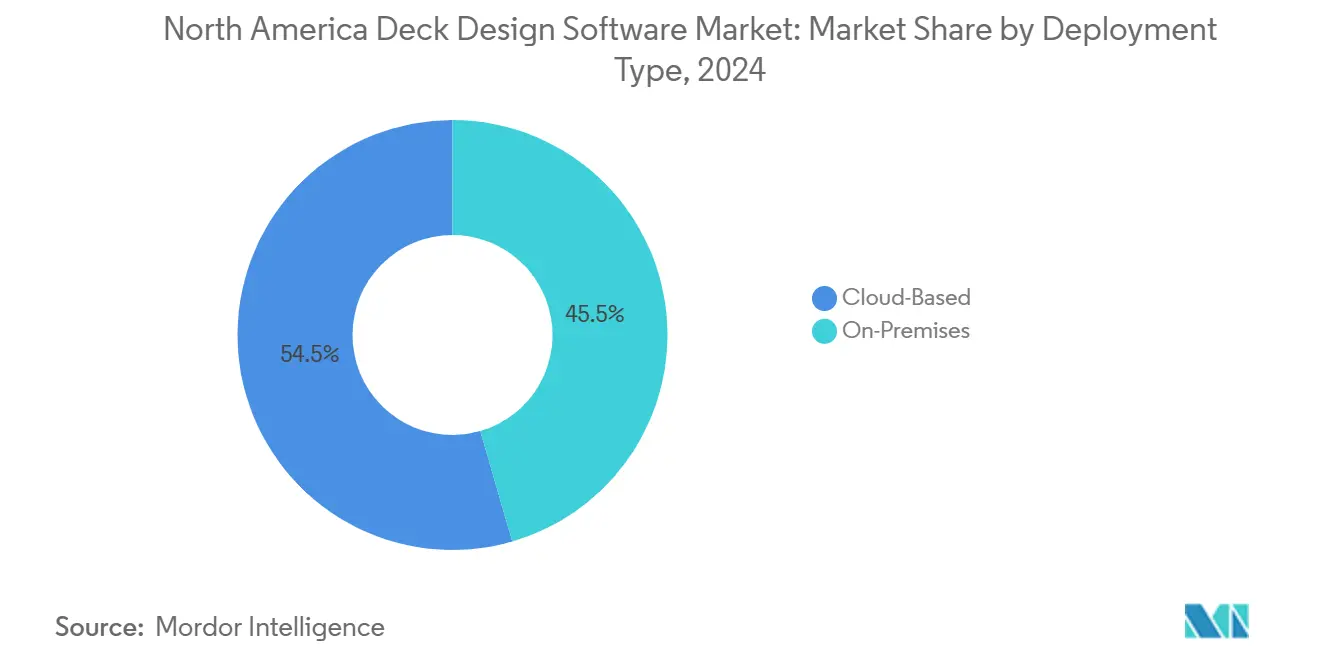

- By deployment type, the cloud segment led with a 54.48% market share of the North America deck design software market in 2024. Cloud solutions are projected to expand at a 12.14% CAGR through 2030.

- By operating system, windows accounted for a 61.59% share of the North America deck design software market size in 2024. Web-based platforms are advancing at a 13.01% CAGR to 2030.

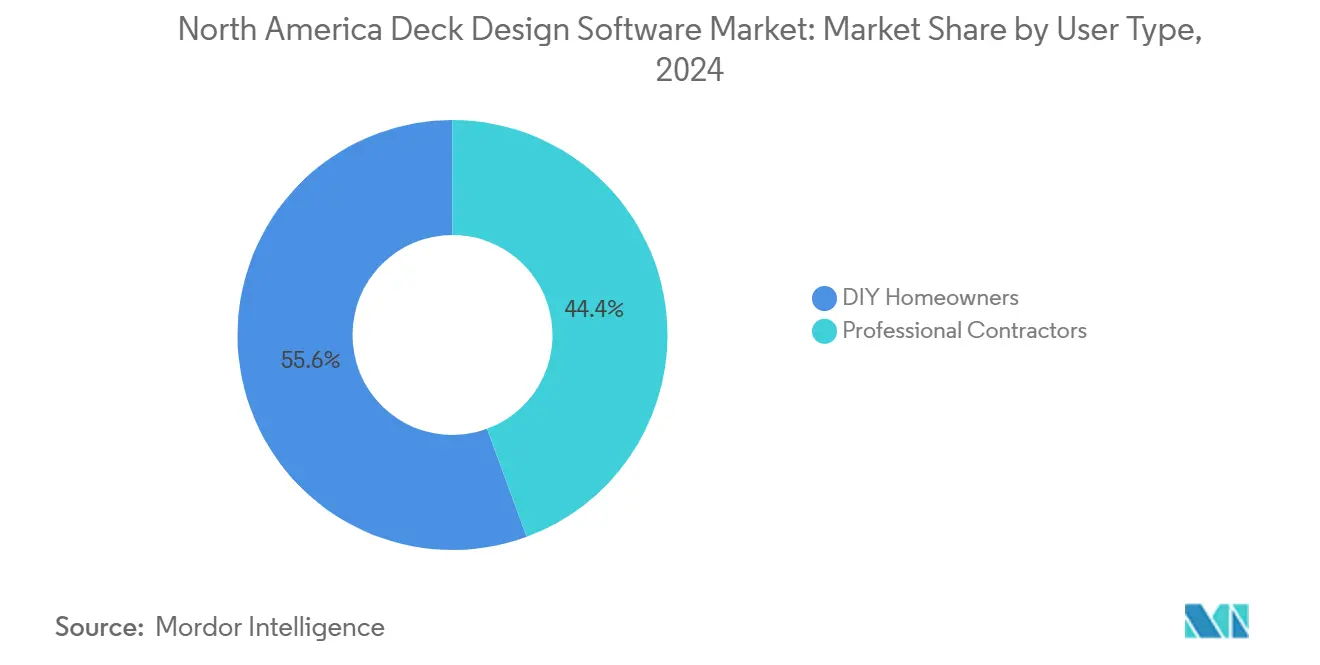

- By user type, DIY homeowners held a 55.62% share of the North America deck design software market size in 2024. Professional contractors are growing at the fastest rate, with a 12.18% CAGR through 2030.

- By license model, subscription plans accounted for a 66.01% revenue share in 2024. Subscription plans are projected to post an 11.48% CAGR between 2025 and 2030.

- By geography, the United States commanded 77.53% of market share in 2024, and Mexico is forecast to record the fastest 11.94% CAGR through 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Deck Design Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing adoption of DIY home-improvement platforms | +2.80% | United States suburbs | Medium term (2-4 years) |

| Expansion of online lumber and decking retailers integrating design tools | +2.10% | United States and Canada | Short term (≤2 years) |

| Rising smart-home integration requirements in outdoor living spaces | +1.90% | United States premium markets | Long term (≥4 years) |

| Increasing availability of cloud-based 3D visualization capabilities | +2.40% | Urban centers across North America | Short term (≤2 years) |

| Regulatory push for building-code compliance documentation | +1.20% | Canada and select U.S. states | Medium term (2-4 years) |

| Accelerated housing renovations due to aging housing stock | +1.70% | Mature suburbs in United States and Canada | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of DIY Home-Improvement Platforms

DIY platforms bundle step-by-step guidance, permit support, and material calculators, allowing homeowners to manage projects that once required professional oversight. Retailers embed these tools into e-commerce sites, letting users move from concept to cart without friction. Enhanced design-to-purchase links raise attachment rates for fasteners, stains, and accessories, lifting retailer margins. As user interfaces simplify and tutorials proliferate, the North America deck design software market reaches first-time renovators who equate intuitive visuals with project confidence. The trend remains strongest in suburban areas where detached housing dominates and labor costs remain elevated.

Expansion of Online Lumber and Decking Retailers Integrating Design Tools

Digital lumber suppliers now position themselves as end-to-end solution providers. Embedded configurators auto-generate bills of materials, price quotes, and delivery schedules that sync with real-time inventory. This vertical integration captures value normally lost to third-party estimators and accelerates order conversion for price-sensitive DIY segments. Vendors that license their engine to multiple retailers gain a rapid distribution channel across North America, enlarging the North America deck design software market footprint among buyers who previously relied on spreadsheets or manual sketches.

Rising Smart-Home Integration Requirements in Outdoor Living Spaces

Interoperability standards such as Matter 1.3 allow deck planners to specify lighting zones, weather-triggered pergolas, and IoT irrigation at the design stage.[1]Connectivity Standards Alliance, “Matter 1.3 Delivers Enhanced Device Types, Improved Interoperability, and New Capabilities,” csa-iot.org Suppliers now bundle device catalogs and wiring diagrams in software libraries, positioning the deck as an extension of whole-home automation. Premium contractors differentiate themselves through integrated outdoor living packages, which in turn drive demand for advanced software validation and visualization. The result is an expanding premium tier within the North America deck design software market.

Increasing Availability of Cloud-Based 3D Visualization Capabilities

Cloud rendering unlocks photorealistic output on modest hardware, shrinking entry barriers for small contractors and homeowners. Lumion’s real-time ray-tracing release in 2024 cut video export times by fivefold. Browser-based collaboration lets clients, inspectors, and suppliers review live models, trimming costly change orders. As cloud data centers proliferate, latency falls, making real-time walkthroughs standard across the North America deck design software market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Interoperability With Professional CAD and BIM Workflows | -1.8% | United States and Canada professional markets | Medium term (2-4 years) |

| Data Security Concerns Among Enterprise Contractors | -1.1% | United States enterprise segment, emerging in Canada | Short term (≤ 2 years) |

| Steep Learning Curve for Advanced 3D Modelling Features | -0.9% | Global, particularly affecting DIY segment adoption | Long term (≥ 4 years) |

| Dependence on High-Speed Internet for Cloud Rendering | -0.7% | Rural markets across North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Interoperability With Professional CAD and BIM Workflows

Contractors juggling multi-platform projects lose time re-entering data when deck software cannot exchange files with mainstream CAD suites. Although Autodesk and Nemetschek signed an interoperability pact in 2024,[2]Autodesk, “Autodesk and Nemetschek Group Announce Interoperability Agreement,” adsknews.autodesk.com specialized deck tools remain slow to adopt open standards. The gap encourages workarounds that erode productivity, limiting professional uptake and capping premium revenue.

Data Security Concerns Among Enterprise Contractors

High-profile breaches targeting construction management platforms in 2024 triggered stricter information-security clauses in institutional contracts. Enterprise contractors hesitate to store proprietary designs on third-party clouds without SOC 2 or FedRAMP certifications. Vendors able to evidence encryption, regional data residency, and audit trails overcome objections, yet smaller platforms face resource constraints that slow certification.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Type: Cloud Solutions Raise Collaboration Standards

Cloud deployments already hold 54.48% share and are set to advance at a 12.14% CAGR, cementing their status as the dominant architecture for the North America deck design software market size. Rapid scaling, automatic updates, and multi-party collaboration are particularly well-suited for contractors handling multiple concurrent jobs. The network effect intensifies as user-generated libraries grow and templates circulate among peers. On-premises systems stay relevant in tightly regulated sectors that mandate in-house servers, yet their relative share declines yearly. Continuous encryption improvements and region-specific data centers erode traditional security objections, expanding the cloud’s addressable base within the North America deck design software market.

Field anecdotes confirm the shift. Trimble’s SketchUp surpassed 1 million active cloud subscribers in late 2024.[3]Trimble, “SketchUp Surpasses 1 Million Active Subscribers,” sketchup.com Contractors cite faster client approvals and reduced hardware spending as prime motivators. The software vendor landscape now competes on integration breadth and collaboration UX rather than raw modeling horsepower. For new entrants, subscription-first models reduce piracy risk and furnish predictable cash flow for R&D, reinforcing cloud supremacy.

By Operating System: Web-First Workflows Accelerate

Windows devices accounted for 61.59% usage in 2024, yet web-based platforms post the fastest 13.01% CAGR. Browser-native tools eliminate installer friction and sync seamlessly between laptops on site and tablets in showrooms, appealing to DIY users and busy contractors. macOS usage grows within design-centric firms attracted to Apple’s graphics optimization. Progressive web apps deliver near-native speed, erasing prior performance gaps. The trend signifies a pivot toward device-agnostic experiences that broaden the North America deck design software market, especially among younger homeowners accustomed to SaaS productivity suites.

Developers capitalize by releasing modular interfaces that down-load only required code on demand, optimizing bandwidth consumption in regions with variable connectivity. Vendors leveraging WebGL and WASM produce photorealistic renders previously confined to desktop GPUs, smoothing the learning curve and enhancing cross-platform parity in the North America deck design software market.

By User Type: Professional Contractors Propel Premium Features

DIY homeowners maintain a 55.62% share, favoring intuitive drag-and-drop layouts and material-cost calculators. Professional contractors, expanding at 12.18% CAGR, invest in structural-load analysis, code-compliance modules, and integration with broader project-management suites. Their adoption boosts revenue per user because pros subscribe to multi-seat plans and specialized plug-ins. The North America deck design software market size benefits from upselling opportunities as contractors demand features such as automated permit-application packets and integrated smart-device wiring diagrams.

Software roadmaps now schedule simultaneous feature sets tailored for both cohorts: visual-first interfaces for novices and granular parameter controls for engineers. Vendors that harmonize the two without compromising usability build defensible moats around user communities.

By License Model: Subscription Revenue Model Becomes Standard

Subscriptions represented 66.01% revenue in 2024 and are on track for an 11.48% CAGR. Continuous feature delivery, cloud storage, and technical support outweigh the appeal of perpetual licenses. Vendors segment offerings into monthly DIY tiers and annual professional tiers, capturing lifetime value across user stages.

One-time licenses linger in corporate procurement frameworks requiring capital expenditure classification; however, vendors like Graphisoft have announced sunset plans for perpetual options, underscoring a systemic SaaS transition. Recurring revenue funds faster R&D cycles, enabling a virtuous loop that strengthens platform stickiness in the North America deck design software market.

Geography Analysis

The United States contributes 77.53% of 2024 revenue, underpinned by robust retail ecosystems and codified DIY culture. Building-code fragmentation complicates nationwide rollouts, yet it also raises switching costs, sheltering incumbents. Canada values compliance automation, leveraging the National Building Code to standardize product requirements, which results in premium software purchases.

Canada exhibits elevated software spending per project due to provincial regulators enforcing strict compliance. The National Building Code of Canada 2020 serves as the baseline, while climate-related provisions require snow-load calculations and frost-protection design. Professional contractors and architects favor platforms that merge structural analysis with photorealistic renderings, enabling clients to visualize the four-season usability of their projects. Language bimodality necessitates dual-interface capability, further differentiating mature vendors.

Mexico, posting an 11.94% CAGR, benefits from BIM mandates for public projects over USD 54 million and rising middle-class expenditure on home upgrades. Language localization and flexible payment gateways become critical success factors, as does the ability to run on mid-range hardware common in emerging urban clusters. Vendors customizing modules for regional codes and financing norms secure first-mover advantages as the North America deck design software market diversifies beyond its U.S. base.

Competitive Landscape

The North America deck design software market shows moderate fragmentation. CAD giants leverage cross-suite bundling, while niche outfits differentiate through deck-specific libraries and retail APIs. Recent M&A confirms a strategic pivot toward ecosystem depth. Oldcastle APG’s 2024 purchase of Yardzen integrates design with material distribution, creating an end-to-end pathway from concept to jobsite.

Stanley Black & Decker’s acquisition of MSUITE expands digital jobsite management, signaling tool manufacturers’ intent to own workflow data. Nemetschek Group’s acquisition of Manufacton enhances modular construction planning, expanding its reach beyond building envelopes to encompass outdoor structures.

Technology roadmaps converge on AI-assisted design automation, smart device catalogs, and code compliance engines. Platforms embed real-time collaboration dashboards that align homeowners, contractors, and inspectors, trimming cycle times. Feature gaps center on interoperable data exchange; vendors partnering on open schemas position themselves for enterprise deals. Pricing pressure intensifies as freemium mobile apps gain traction among DIYers, forcing incumbents to tier offerings without cannibalizing premium SKUs. On balance, innovation speed and integration breadth outweigh scale alone in securing long-term share within the North America deck design software market.

North America Deck Design Software Industry Leaders

Trimble Inc.

Chief Architect, Inc.

Idea Spectrum, Inc.

Trex Company, Inc.

The AZEK Company Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Lumion launched Lumion Cloud, enabling real-time visualization collaboration for designers and contractors.

- March 2025: ALLPLAN acquired Manufacton to integrate AI-driven offsite production optimization into its portfolio.

- November 2024: Oldcastle APG acquired Yardzen, marrying digital landscape design with materials distribution.

- November 2024: Trimble SketchUp has crossed the one-million-subscriber milestone, underscoring the cloud's scalability.

North America Deck Design Software Market Report Scope

| Cloud-Based |

| On-Premises |

| Windows |

| macOS |

| Web-Based (Browser) |

| Professional Contractors |

| DIY Homeowners |

| Subscription |

| One-Time License |

| Freemium |

| United States |

| Canada |

| Mexico |

| By Deployment Type | Cloud-Based |

| On-Premises | |

| By Operating System | Windows |

| macOS | |

| Web-Based (Browser) | |

| By User Type | Professional Contractors |

| DIY Homeowners | |

| By License Model | Subscription |

| One-Time License | |

| Freemium | |

| By Geography | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

How large is the North America deck design software market in 2025?

The market size is USD 76.48 million in 2025.

What annual growth rate is expected through 2030?

The market is projected to grow at an 11.01% CAGR.

Which deployment model shows the highest growth?

Cloud solutions lead, advancing at a 12.14% CAGR.

Which user segment is expanding quickest?

Professional contractors are growing fastest at 12.18% CAGR.

Which country offers the highest growth potential?

Mexico is set to post an 11.94% CAGR through 2030.

Page last updated on: