North America Customer Data Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

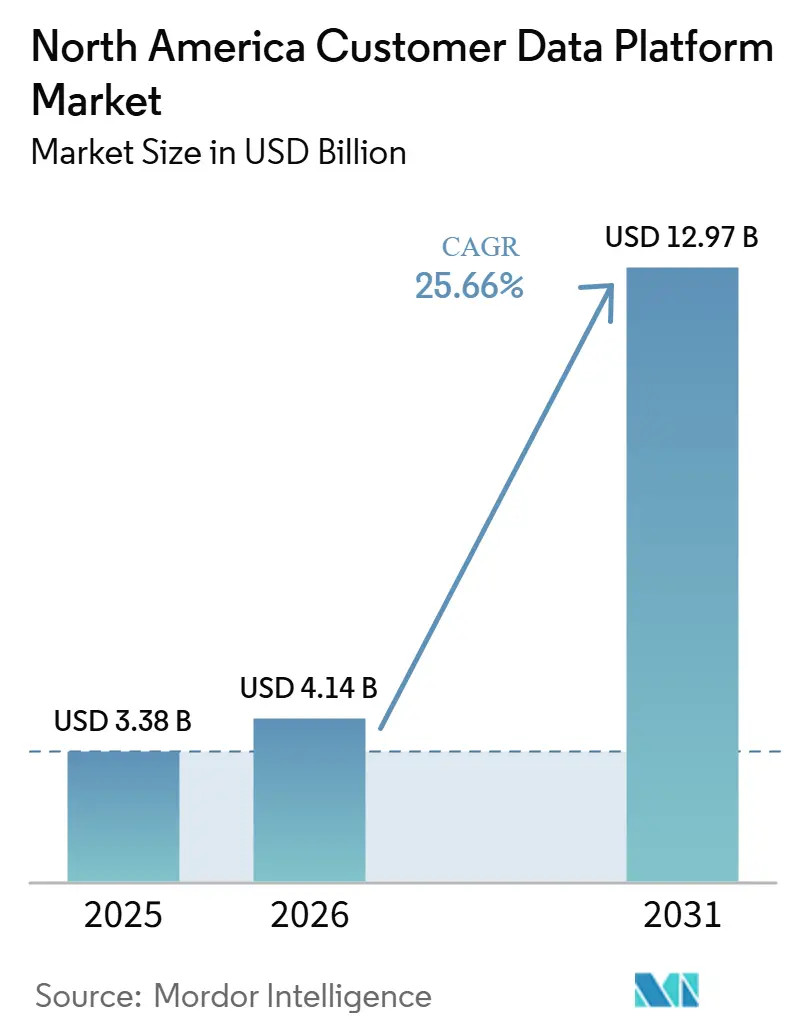

| Base Year Market Size (2025) | USD 3.38 Billion |

| Market Size (2026) | USD 4.14 Billion |

| Market Size (2031) | USD 12.97 Billion |

| Growth Rate (2026 - 2031) | 25.66% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Customer Data Platform Market Analysis by Mordor Intelligence

The North America customer data platform market size is projected to expand from USD 3.38 billion in 2025 and USD 4.14 billion in 2026 to USD 12.97 billion by 2031, registering a CAGR of 25.66% between 2026 to 2031. Growth in the North America customer data platform market is being supported by the shift toward consented first-party data, which remains central as brands rebuild targeting and personalization around directly held customer information. Demand is also rising because GenAI agents now need fast access to unified profiles, transaction history, and behavioral signals, which pushes buyers to upgrade from simple data collection toward systems that can support real-time decisioning. Cloud-native deployment models continue to reduce implementation friction, and that has widened the addressable base beyond early enterprise adopters into operators that need faster time-to-value and lower operating complexity. Buyers who built CDP foundations before 2024 are now using those systems to improve conversion, marketing productivity, and cross-channel coordination, which keeps follow-on investment active across analytics, activation, and governance layers. Competitive pressure is also increasing because incumbent vendors still hold the broadest enterprise relationships, while composable and warehouse-native challengers are using architectural flexibility, lower data duplication, and stronger AI alignment to win attention in the North America customer data platform market.

Key Report Takeaways

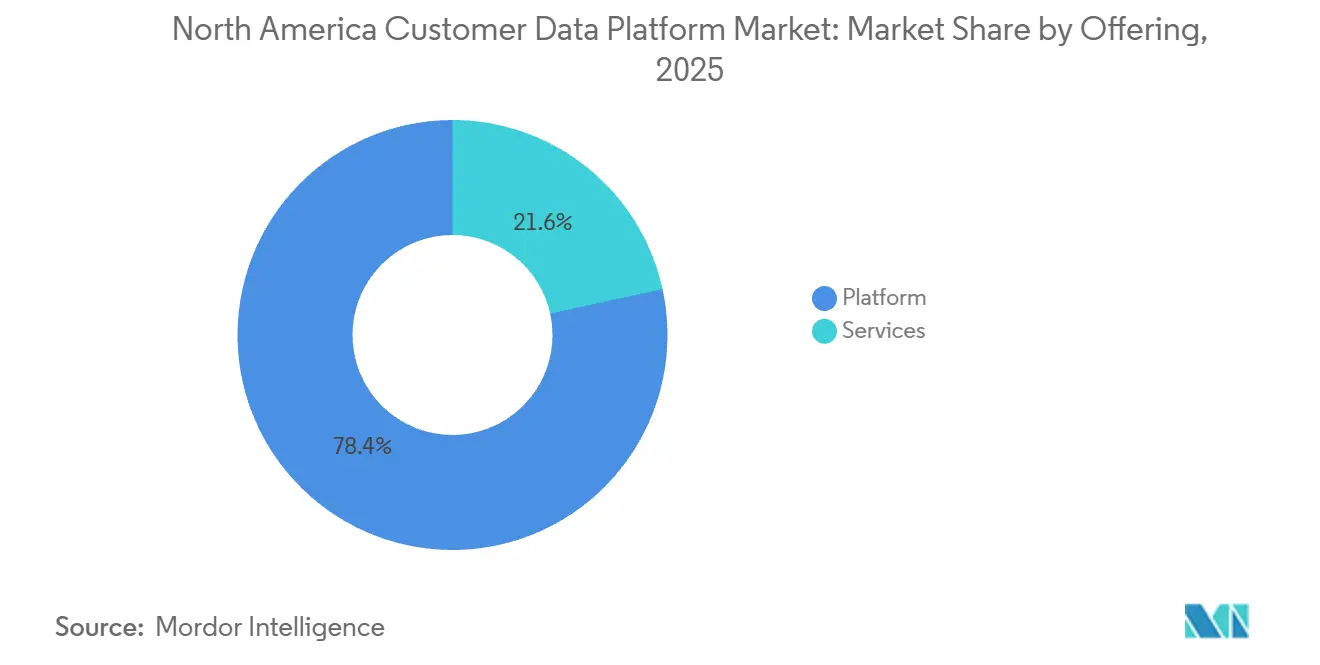

- By offering, platform held 78.43% of revenue of the North America customer data platform market in 2025, while services is projected to expand at a 28.14% CAGR through 2031.

- By deployment mode, cloud accounted for 61.84% of revenue in 2025, while hybrid is projected to advance at a 29.21% CAGR through 2031.

- By organization size, large enterprises held 72.36% share of the North America customer data platform market in 2025, while SMEs are projected to record the highest CAGR at 29.74% through 2031.

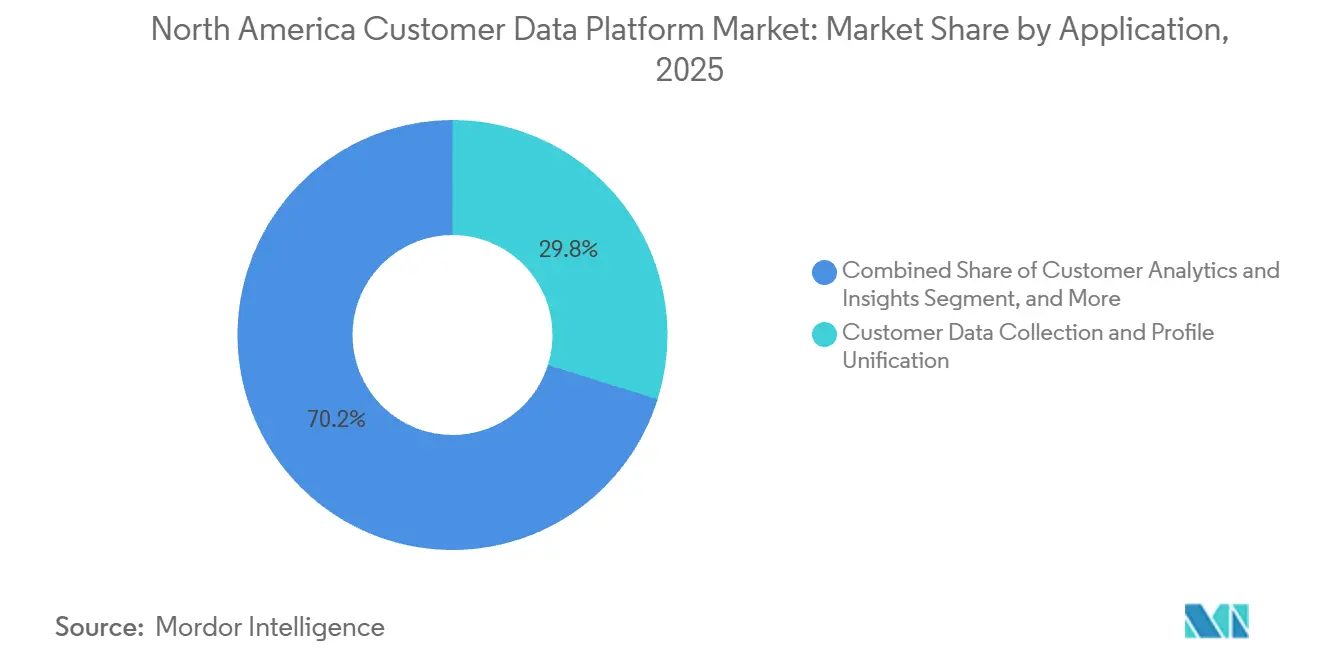

- By application, customer data collection and profile unification captured 29.84% of revenue in 2025, while customer analytics and insights is projected to expand at a 30.16% CAGR through 2031.

- By end-user industry, retail and e-commerce accounted for 24.76% of revenue in 2025, while healthcare and life sciences is projected to grow at a 30.42% CAGR through 2031.

- By geography, the United States held 81.18% of revenue in 2025, while Mexico is projected to expand at a 28.36% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Customer Data Platform Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Third-Party Cookie Phase-Out Accelerates First-Party Data Unification | +5.2% | Global, strongest in United States and Canada where CCPA and PIPEDA compliance create penalty-backed urgency | Short term (≤ 2 years) |

| GenAI Customer Agents Require Low-Latency Unified Profiles | +4.8% | United States, early adoption in Canada, spillover to Mexico | Medium term (2-4 years) |

| Cloud-Native CDP Adoption Shortens Deployment Cycles | +3.9% | United States and Canada, gaining in Mexico with hyperscaler infrastructure buildout | Short term (≤ 2 years) |

| Privacy-First Personalization Increases Demand for Consent-Aware Activation | +3.3% | United States, Canada, Mexico | Medium term (2-4 years) |

| Warehouse-Native Composable Architectures Reduce Data Duplication Costs | +2.8% | United States and Canada, early-stage in Mexico | Long term (≥ 4 years) |

| Healthcare and BFSI Omnichannel Engagement Expands Services Demand | +2.2% | United States, Canada, nascent in Mexico | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Third-Party Cookie Phase-Out Accelerates First-Party Data Unification

Google’s April 2025 decision to move from a fixed cookie removal path toward a user-choice model removed the original deadline, but it did not restore the value of third-party signals for brands that had already started rebuilding identity strategy around owned data. Safari and Firefox had already restricted cross-site cookies for years, so the North America customer data platform market still benefits from the broader structural shift toward durable first-party identity and permissioned activation. Adobe reported in 2024 that 78% of brands had adopted a CDP as a foundation for first-party data strategy, which shows that many buyers had already reset their architecture before Chrome changed direction. The same study also showed that 49% of marketers still relied on third-party cookies in 2024, which leaves a meaningful migration pool that is likely to keep spending active through the 2026 to 2028 period. That shift favors platforms that can combine identity resolution, consent intake, and privacy-safe audience activation without forcing buyers to rebuild those functions across disconnected tools. It also makes the North America customer data platform market more technically demanding because the user-choice model splits audiences into signal-rich opted-in users and signal-poor opted-out users, which raises the importance of profile enrichment and modeling accuracy.

GenAI Customer Agents Require Low-Latency Unified Profiles

The rise of GenAI-powered customer agents has added a fresh demand layer to the North America customer data platform market because autonomous service and commerce workflows now depend on immediate access to unified identity, purchase history, and live behavioral context. Batch-oriented data environments can support analysis, but they are less suited for customer agents who need current profile states during service interactions, product recommendations, and post-purchase orchestration. Databricks introduced CustomerLake in June 2026 as an agentic CDP embedded in its lakehouse, bringing identity resolution, audience creation, and AI-driven activation into a governed environment without data duplication.[1]Databricks, “Introducing CustomerLake, The Agentic CDP Embedded in Databricks,” Databricks Blog, databricks.com Adobe also unveiled CX Enterprise Coworker in April 2026 on Adobe Experience Platform, which showed that major vendors are aligning CDP infrastructure more closely with AI agent orchestration and open standards. This creates an advantage for composable and warehouse-native models because organizations that prioritized real-time data access earlier are now better prepared for agentic use cases without major architectural reversal. As a result, the North America customer data platform market is moving beyond profile unification alone and toward environments where activation speed and governed AI access become part of the core buying decision.

Cloud-Native CDP Adoption Shortens Deployment Cycles

Cloud-native delivery has changed the implementation profile of the North America customer data platform market by reducing the long setup cycles that once kept adoption concentrated among very large enterprises. Prebuilt connectors, managed environments, and warehouse integrations are helping buyers move initial ingestion and orchestration programs from long project windows into much shorter operational timelines. Tealium’s May 2026 launch of AI at the Edge showed that vendors are now extending cloud-native value beyond hosting and into in-platform intelligence and real-time decisioning. Twilio reported in 2025 that customers synced nearly 10 trillion rows of data to cloud warehouses in a single year, underscoring the scale mismatch between modern data volumes and older on-premises approaches. Centralized lineage, audit visibility, and consent log management also make cloud-native environments easier to align with the cybersecurity and governance expectations that gained more weight under California’s 2026 regulatory updates. These advantages continue to support faster adoption in the North America customer data platform market, especially where buyers want quicker deployment without giving up control over governance and data movement.

Privacy-First Personalization Increases Demand for Consent-Aware Activation

Privacy requirements are becoming a direct product differentiator in the North America customer data platform market because buyers increasingly prefer platforms that can encode and enforce consent at the profile level rather than attach it later through a separate tool. California’s regulations, effective January 1, 2026, expanded expectations around automated decision-making technology risk assessments, cybersecurity audits for qualifying businesses, and recognition of global privacy control signals, which all increase the value of native consent-aware workflows.[2]California Privacy Protection Agency, “Law and Regulations, California Consumer Privacy Act Regulations,” CPPA, cppa.ca.gov The California Attorney General’s USD 2.75 million settlement with Disney in 2026 sharpened the cost of noncompliance and raised the urgency of traceable consent enforcement in activation programs. Adobe’s February 2025 general availability of Real-Time CDP Collaboration in the United States showed how vendors are turning privacy-safe audience activation into a product and revenue opportunity rather than treating it only as a compliance burden. Similar pressure from Colorado, Connecticut, Quebec, and Mexico’s LFPDPPP broadens the relevance of these capabilities beyond California and keeps privacy-led demand active across the regional buying base. This dynamic helps the North America customer data platform market because it ties customer experience spending more closely to governance infrastructure that organizations cannot easily defer.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented Legacy Data Models Extend Implementation Timelines | -2.8% | United States, Canada, less severe in Mexico where greenfield deployments are more common | Long term (≥ 4 years) |

| Persistent Privacy Engineering Burden Slows Cross-Channel Activation | -2.2% | United States, Canada, Mexico | Medium term (2-4 years) |

| Skilled CDP Integration Talent Remains Concentrated in Major Hubs | -1.6% | United States, limited availability in Canada outside Toronto and Vancouver, scarce in Mexico | Long term (≥ 4 years) |

| High Total Cost of Ownership Limits Enterprise-Wide Rollouts | -1.4% | United States and Canada, SME segment across all geographies | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented Legacy Data Models Extend Implementation Timelines

Legacy data fragmentation remains one of the clearest operational constraints on the North America customer data platform market, as many large enterprises still store customer records across CRM, ERP, loyalty, commerce, and point-of-sale systems built in different eras. Those systems often use different identifiers and business rules, which makes automated reconciliation difficult even before downstream activation logic is configured. CDP Institute data from January 2026 showed that composable and warehouse-native vendors recorded 7.8% organic employment growth, compared with an industry average of 1.3%, which points to sustained investment in specialized integration and identity work. The challenge becomes more severe when organizations try to unify records across brands or lines of business, because duplicate and conflicting customer states can reduce personalization accuracy rather than improve it. SAP’s March 2026 agreement to acquire Reltio showed how central master data management has become for AI-ready customer environments across SAP and non-SAP estates. Buyers who delay upstream data remediation often stretch deployment timelines, raise first-year delivery risk, and weaken expected returns even when the selected CDP product itself performs as designed.

Persistent Privacy Engineering Burden Slows Cross-Channel Activation

The North America customer data platform market also faces a continuing drag from the privacy engineering effort required to keep activations compliant with evolving laws, browser signals, and channel-specific controls. Each new legal update can require changes to consent logic, suppression rules, data-sharing settings, and visible customer preference handling across analytics, personalization, advertising, and service layers. California’s 2026 regulations require businesses to recognize and process browser-level global privacy control signals, which adds practical integration work across several systems that rarely sit under a single vendor contract. This creates an uneven operating burden because large enterprises can spread that work across specialized legal, engineering, and platform teams, while many smaller buyers wait for vendor-managed updates before expanding activation programs. That delay can limit the pace at which SMEs move from simple campaign use cases toward wider orchestration and analytics deployments in the North America customer data platform market. The result is that privacy readiness not only affects compliance posture, but it also shapes which vendors can sustain adoption outside the largest enterprise accounts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Platform Leadership Still Shapes Spending Mix

Platform accounted for 78.43% of 2025 revenue, which kept software subscription spending at the center of the customer data platform market size in the region during the current deployment phase. That concentration reflects how early and mid-stage buyers still prioritize the core system that can unify identity, connect data sources, and support governed activation across channels. Services, however, is forecast to grow at a 28.14% CAGR through 2031, which shows that implementation, optimization, and managed operations are becoming more important as programs deepen. The North America customer data platform market is therefore moving from initial product selection toward a broader operating model that includes onboarding support, identity graph maintenance, and ongoing configuration work. This pattern suggests that spending in the customer data platform industry is shifting from a one-time acquisition decision toward a longer program model with recurring operational dependency.

As deployment maturity rises, buyers are learning that total program cost extends well beyond platform list pricing, especially when audience design, integration support, model tuning, and channel activation require outside help over several years. That matters because services can become a practical lock-in layer even when the software contract looks flexible on paper. Klaviyo’s February 2026 rollout of the Klaviyo Data Platform to enterprise-tier merchants showed how vendors are productizing functions that were often handled by services partners, including unified profiles, behavioral event consolidation, purchase history, and predictive value scoring.[3]Klaviyo Investor Relations, “Klaviyo Expands AI Agents to Power the Autonomous B2C CRM,” Klaviyo News, investors.klaviyo.com Vendors that can move more operational work into product may defend margin better, but buyers may still need services where underlying data estates remain fragmented or governance needs are unusually strict. For that reason, the North America customer data platform market is likely to keep a strong platform core while also giving services a larger role in long-term account economics.

By Deployment Mode: Hybrid Models Answer Control and Scale Needs

Cloud held 61.84% of the 2025 deployment mix, which made it the largest current model and the clearest near-term expression of customer data platform market share by deployment. Hybrid is projected to expand at a 29.21% CAGR through 2031, which makes it the fastest-growing mode as buyers try to balance sovereignty, latency, and operating flexibility. On-premises remains relevant in regulated environments, especially where audit trails, internal policy controls, or data residency needs still limit full cloud migration. The North America customer data platform market is therefore not moving in a straight line from on-premises to cloud, because many organizations now want a mixed architecture that fits different data and activation workloads. This shift reflects an enterprise's need to keep sensitive data closer to controlled environments while still using the cloud for analytics, training, and scalable processing.

Rokt mParticle’s early 2025 launch of a hybrid CDP built on the Snowflake AI Data Cloud offered a visible proof point for this direction by combining streaming data pipelines with batch processing in a unified interface. California’s January 2026 automated decision-making and cybersecurity requirements also added pressure on operating models because organizations subject to audits may find it easier to separate local control layers from less sensitive activation workloads. That makes hybrid architecture a response to both technical and regulatory needs rather than a temporary stop along the road to full cloud adoption. The on-premises segment may lose relative weight, but it still serves as a compliance and sovereignty layer within larger multi-environment deployments. This is why the North America customer data platform market continues to reward vendors that can support more than one deployment path without forcing a strict architectural choice.

By Organization Size: SMEs Expand the Reach of Adoption

Large enterprises held 72.36% of revenue in 2025, which gave them the leading customer data platform market share because they adopted earlier, spent more per contract, and managed wider data estates. SMEs are projected to grow at a 29.74% CAGR through 2031, which signals that the next wave of expansion is coming from buyers that were previously priced out or operationally excluded. Usage-based pricing, self-serve onboarding, and connector libraries are lowering barriers that once made advanced CDP programs practical only for resource-rich enterprises. The North America customer data platform market is therefore broadening from a top-heavy client base into a more distributed demand structure, even though large organizations still set many architecture and governance standards. This shift also changes vendor positioning because ease of deployment and packaged workflows matter more when internal engineering capacity is limited.

Klaviyo’s Q1 2026 performance, with USD 285 million in quarterly revenue and 167,000 paying customers, showed that a platform built for B2C operators and mid-market brands can scale without depending only on large enterprise accounts. The SME opportunity still varies by country, because adoption in the United States and Canada remains concentrated in digital-first retail, media, and direct-to-consumer models, while Mexico’s demand is more closely tied to the formalization of commerce infrastructure. Smaller firms also frequently buy CDP-adjacent functions inside broader marketing automation products rather than purchase a standalone platform, which can blur the edge of the addressable base for dedicated vendors. That keeps growth prospects strong, but it also means supplier competition stretches beyond pure-play CDPs into adjacent customer engagement stacks. The North America customer data platform market will likely see the most durable SME wins go to vendors that combine low-friction onboarding with enough governance to support expansion beyond entry-level campaign use cases.

By Application: Analytics Moves to the Center of Spending

Customer data collection and profile unification held 29.84% of 2025 application revenue, which made it the largest current application layer and an important marker of customer data platform market size by use case. Customer analytics and insights is projected to grow at a 30.16% CAGR through 2031, which shows that spending is moving from collection toward prediction, scoring, and decision support. This transition reflects a maturing North America customer data platform market where many buyers have already completed the first stage of identity and ingestion work. Once profile foundations are in place, the next spend priority shifts toward churn detection, lifetime value modeling, next-best-action design, and more precise customer intelligence. That change also raises the value of clean governance and low-latency access because analytics is only as useful as the freshness and consistency of the profile underneath it.

Twilio reported in 2025 that predictive trait usage across its platform rose by 57%, which points to faster adoption of analytics-led workflows ahead of the broader category average. The other application groups, including segmentation and personalization, journey orchestration, and consent management, are also moving forward, but they are increasingly being used as linked workflow stages rather than isolated point functions. Consent and preference management remains smaller by revenue, yet it carries unusual strategic weight because legal deadlines can force investment even when broader experience spending is being reviewed. California’s January 2026 requirement to honor and confirm global privacy control signals increased the operating importance of this layer and pushed governance closer to senior management attention. In practical terms, the North America customer data platform market is becoming less about data capture alone and more about what organizations can reliably decide and activate once data has been unified.

By End-User Industry: Healthcare And Life Sciences Gains Speed

Retail and e-commerce represented 24.76% of 2025 end-user revenue, which made it the largest vertical and a clear benchmark for the customer data platform market size across industries. Healthcare and life sciences is projected to grow at a 30.42% CAGR through 2031, making it the fastest-expanding vertical as regulated engagement models become more digitally coordinated. Retail still leads because it produces dense customer touchpoints across browsing, carts, purchases, returns, and loyalty interactions, which naturally suit profile unification and personalization. The North America customer data platform market has historically centered on those retail patterns, but current growth is spreading into sectors where engagement paths are more regulated and operationally sensitive. That is why healthcare’s growth stands out, because it suggests the value of unified profiles is being recognized in settings where governance and trust requirements are much stricter than in commerce.

Healthcare adoption is being supported by omnichannel patient engagement programs, including follow-up communication, adherence reminders, preventive outreach, and guided service journeys that need timely and accurate profile views. Databricks described a composable healthcare pattern in which a HIPAA-compliant lakehouse stores central patient data while the CDP layer lets nontechnical teams build segments and coordinate outreach without direct database access. BFSI remains important for services revenue because customer data is dispersed across banking, insurance, lending, and wealth environments that require difficult reconciliation before activation can begin. Manufacturing and government are still earlier in adoption, with use cases centered more on dealer networks or citizen services than broad consumer-style personalization. Media, entertainment, IT, and telecom continue to focus their programs on subscription value, churn reduction, and cross-sell, which keeps the North America customer data platform market diversified even as retail remains the largest current revenue anchor.

Geography Analysis

The United States held 81.18% of 2025 revenue, which gave it the dominant customer data platform market share within the region and made it the clear anchor for supplier scale, product development, and enterprise deployment depth. Its position reflects the combined effect of a very large digital advertising base, deep cloud adoption, strong systems integrator coverage, and the headquarters presence of many leading vendors. The Mordor Intelligence global CDP assessment also showed that North America accounted for 47.32% of global revenue in 2025, reinforcing the regional weight of the United States within the wider category structure. In the United States, future growth is likely to come less from basic profile setup and more from analytics upgrades, AI integration, and deeper activation workflows. California’s January 2026 amendments on automated decision-making, cybersecurity audits, and global privacy control signal handling increased the configuration burden for U.S. deployments and strengthened the case for platforms with native consent management.

Canada was the second-largest country in the North America customer data platform market in 2025, although its revenue base remained much smaller than that of the United States. Canadian demand is being shaped by the interaction between PIPEDA and Quebec’s Law 25, which together keep consent, transparency, and data handling discipline central to enterprise platform choice. ICEX noted for 2026 that Canadian small and mid-sized merchants are expected to invest more actively in AI-integrated platforms, including solutions linked to ecosystems such as Salesforce and Shopify. Canada’s growth profile is steadier than that of Mexico, but BFSI and retail continue to provide solid demand for unified data and cross-sell personalization.

Mexico is projected to expand at a 28.36% CAGR through 2031, making it the fastest-growing geography in the North America customer data platform market and the most dynamic regional opportunity by forecast pace. Growth is being supported by rising e-commerce activity, higher smartphone use, and broader awareness of LFPDPPP obligations among retailers, fintechs, and financial institutions. CDP Institute’s July 2025 update showed rising employment and funding momentum across the Americas, with strong movement outside the United States, where greenfield deployments often face fewer legacy model constraints.[4]CDP Institute, “CDP Industry Statistics 2026, Market Size and Trends,” CDP.com, cdp.com Mexico’s fintech base adds to this outlook because many firms are cloud-native, API-oriented, and consumer-facing, which fits modular CDP rollout patterns well. Infrastructure constraints outside major hubs still limit the pace of cloud-heavy deployment in some secondary markets, but that pressure is expected to ease as hyperscaler capacity expands over time.

Competitive Landscape

The North America customer data platform market remains moderately concentrated at the top, with Salesforce, Adobe, and Oracle holding the broadest revenue footprints through established enterprise ties and deep ecosystem integration. Those leaders benefit from installed bases, broad channel relationships, and the ability to connect CDP functions with sales, service, analytics, and content products already used by large customers. At the same time, the field below the top tier remains fragmented, which keeps pricing pressure and feature innovation active across the category. CDP Institute reported in July 2025 that the market included more than 208 CDP vendors globally, while North America accounted for 84% of industry funding and 62% of employment, highlighting how much product activity remains concentrated in this region. That backdrop means the North America customer data platform market is led by a few scaled vendors, but not closed to challengers that can offer a stronger architecture or a faster route to measurable activation outcomes.

One major strategic pattern is convergence, because incumbent platforms are adding analytics, consent management, and agentic orchestration inside the core product to defend against specialist competitors. Adobe’s April 2026 CX Enterprise Coworker announcement showed how a major platform is linking autonomous workflow design directly to its existing experience and CDP environment.[5]Adobe, “Adobe Unveils CX Enterprise Coworker to Build Agentic-Enabled Workflows for Customer Experience Orchestration,” Adobe News, news.adobe.com Databricks’ June 2026 introduction of CustomerLake pushed the same market in another direction by embedding CDP capabilities inside the data infrastructure layer, which strengthens the appeal of warehouse-native operating models. SAP’s March 2026 agreement to acquire Reltio signaled another structural move, because it pulled master data management closer to AI-ready customer environments and suggested tighter overlap between MDM and CDP decision layers. These moves show that the North America customer data platform market is being reshaped as much by platform boundary shifts as by head-to-head feature competition.

Open opportunity still exists in mid-market BFSI, smaller healthcare systems, and Mexican enterprise accounts that need stronger governance than lightweight commerce tools provide, but do not want the weight of a fully bespoke enterprise stack. That gap has given room to challengers that emphasize packaged workflows, modular deployment, and faster proof of value. Rokt mParticle’s June 2026 launch of Performance Engine reflected this shift toward outcome-led positioning, where the promise centers on revenue lift and audience performance rather than on profile depth alone. Hightouch’s June 2026 launch of Lifecycle Studio showed a similar effort to move from warehouse-native data access toward marketer-ready campaign execution through agentic workflow design. This keeps the North America customer data platform market competitive because challengers are not only competing on architecture, they are also competing on how directly they connect unified data to measurable business results.

North America Customer Data Platform Industry Leaders

Salesforce, Inc.

Oracle Corporation

Adobe Inc.

SAP SE

Twilio Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Rokt mParticle launched the Performance Engine, a suite anchored by an autonomous Audience Agent that converts first-party CDP data into measurable revenue lift through AI-powered match-rate optimization and audience expansion across Google and Meta platforms, extending mParticle's positioning from data infrastructure to performance outcomes.

- June 2026: Hightouch launched Lifecycle Studio, an agentic marketing workspace that enables lifecycle and CRM teams to build production-ready, personalized cross-channel campaigns from a single prompt, positioning itself as an AI-native CDP challenger within Gartner's Magic Quadrant for CDPs.

- June 2026: Bloomreach deepened its partnership with Databricks as a launch partner for CustomerLake, integrating Loomi AI personalization capabilities directly with the new agentic CDP to enable real-time, AI-driven campaign execution across email, web, and additional channels.

- May 2026: Tealium unveiled AI at the Edge and AI Decisioning as new in-platform features, reinforcing its hybrid CDP positioning by adding real-time contextual intelligence and autonomous decisioning directly within its data orchestration layer for enterprise clients.

North America Customer Data Platform Market Report Scope

The North America Customer Data Platform (CDP) market comprises software platforms and associated services that collect, unify, manage, and activate customer data from multiple online and offline sources to create persistent, unified customer profiles. These platforms enable organizations to deliver personalized, privacy-compliant, and omnichannel customer experiences through capabilities such as identity resolution, audience segmentation, real-time data activation, customer journey orchestration, analytics, and consent management.

The North America Customer Data Platform Market Report is Segmented by Offering (Platform, and Services), Deployment Mode (Cloud, On-Premises, and Hybrid), Organization Size (Large Enterprises, and SMEs), Application (Customer Data Collection and Profile Unification, Audience Segmentation and Personalization, Marketing Campaign and Customer Journey Orchestration, Customer Analytics and Insights, Consent and Preference Management, and Other Applications), End-User Industry (Retail and E-Commerce, BFSI, Healthcare and Life Sciences, IT and Telecom, Media and Entertainment, Industrial Manufacturing, Government and Public Administration, and Other End-User Industries), and Geography (United States, Canada, Mexico). The Market Forecasts are Provided in Terms of Value (USD).

| Platform |

| Services |

| Cloud |

| On-Premises |

| Hybrid |

| Large Enterprises |

| SMEs |

| Customer Data Collection and Profile Unification |

| Audience Segmentation and Personalization |

| Marketing Campaign and Customer Journey Orchestration |

| Customer Analytics and Insights |

| Consent and Preference Management |

| Other Applications |

| Retail and E-Commerce |

| BFSI |

| Healthcare and Life Sciences |

| IT and Telecom |

| Media and Entertainment |

| Industrial Manufacturing |

| Government and Public Administration |

| Other End-User Industries |

| United States |

| Canada |

| Mexico |

| By Offering | Platform |

| Services | |

| By Deployment Mode | Cloud |

| On-Premises | |

| Hybrid | |

| By Organization Size | Large Enterprises |

| SMEs | |

| By Application | Customer Data Collection and Profile Unification |

| Audience Segmentation and Personalization | |

| Marketing Campaign and Customer Journey Orchestration | |

| Customer Analytics and Insights | |

| Consent and Preference Management | |

| Other Applications | |

| By End-User Industry | Retail and E-Commerce |

| BFSI | |

| Healthcare and Life Sciences | |

| IT and Telecom | |

| Media and Entertainment | |

| Industrial Manufacturing | |

| Government and Public Administration | |

| Other End-User Industries | |

| By Geography | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

What is the size outlook for the North America customer data platform market?

The North America customer data platform market stood at USD 3.38 billion in 2025, is valued at USD 4.14 billion in 2026, and is forecast to reach USD 12.97 billion by 2031 at a 25.66% CAGR.

Which factor is pushing adoption most strongly across the region?

The strongest current push comes from the move toward consented first-party data, reinforced by cookie disruption, privacy enforcement, and the need for unified profiles.

Which deployment model is growing the fastest in North America?

Hybrid deployment is projected to grow the fastest, at a 29.21% CAGR through 2031, as enterprises balance cloud scale with sovereignty and audit needs.

Which customer group is creating the next wave of demand?

SMEs are the fastest-growing organization-size segment, with a 29.74% CAGR, helped by usage-based pricing, self-serve onboarding, and easier integrations.

Which application area is becoming the main growth engine?

Customer analytics and insights is the fastest-growing application at a 30.16% CAGR, showing that spending is moving from data collection toward prediction and decision support.

Which country offers the fastest future expansion in the region?

Mexico is projected to expand at a 28.36% CAGR through 2031, supported by e-commerce growth, fintech adoption, and rising attention to consent-compliant first-party data infrastructure.

Page last updated on: