North America Coiled Tubing Services Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

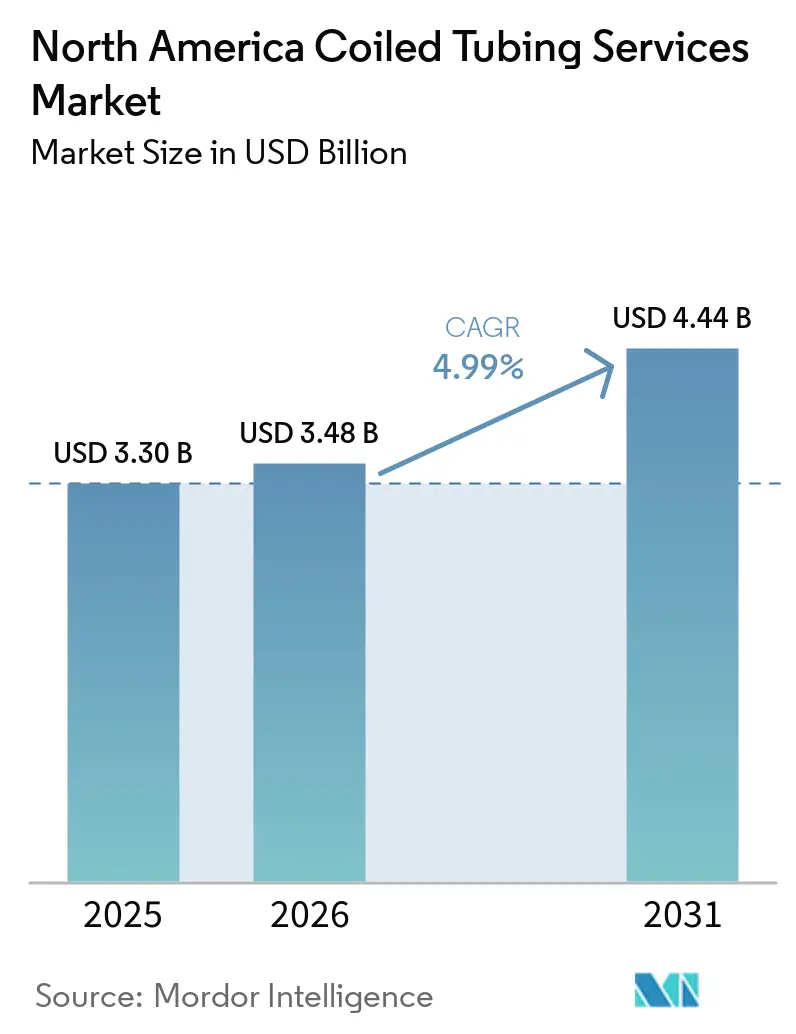

| Base Year Market Size (2025) | USD 3.30 Billion |

| Market Size (2026) | USD 3.48 Billion |

| Market Size (2031) | USD 4.44 Billion |

| Growth Rate (2026 - 2031) | 4.99% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Coiled Tubing Services Market Analysis by Mordor Intelligence

The North America Coiled Tubing Services Market size is expected to grow from USD 3.30 billion in 2025 to USD 3.48 billion in 2026 and is forecast to reach USD 4.44 billion by 2031 at 4.99% CAGR over 2026-2031. Sustained shale productivity, longer lateral lengths, and rising deepwater abandonment needs are keeping activity levels high even as rig deployment moderates. Operators increasingly favor rig-less interventions to restore flow in aging horizontals, a shift that stabilizes demand across economic cycles. Real-time fiber-optic telemetry, electrified units, and automated control systems are moving from premium options to baseline specifications, compressing margins for fleets that rely on legacy hydraulic equipment. Meanwhile, diversification into geothermal and carbon-capture well servicing is creating counter-cyclical revenue streams that hedge crude price volatility.

Key Report Takeaways

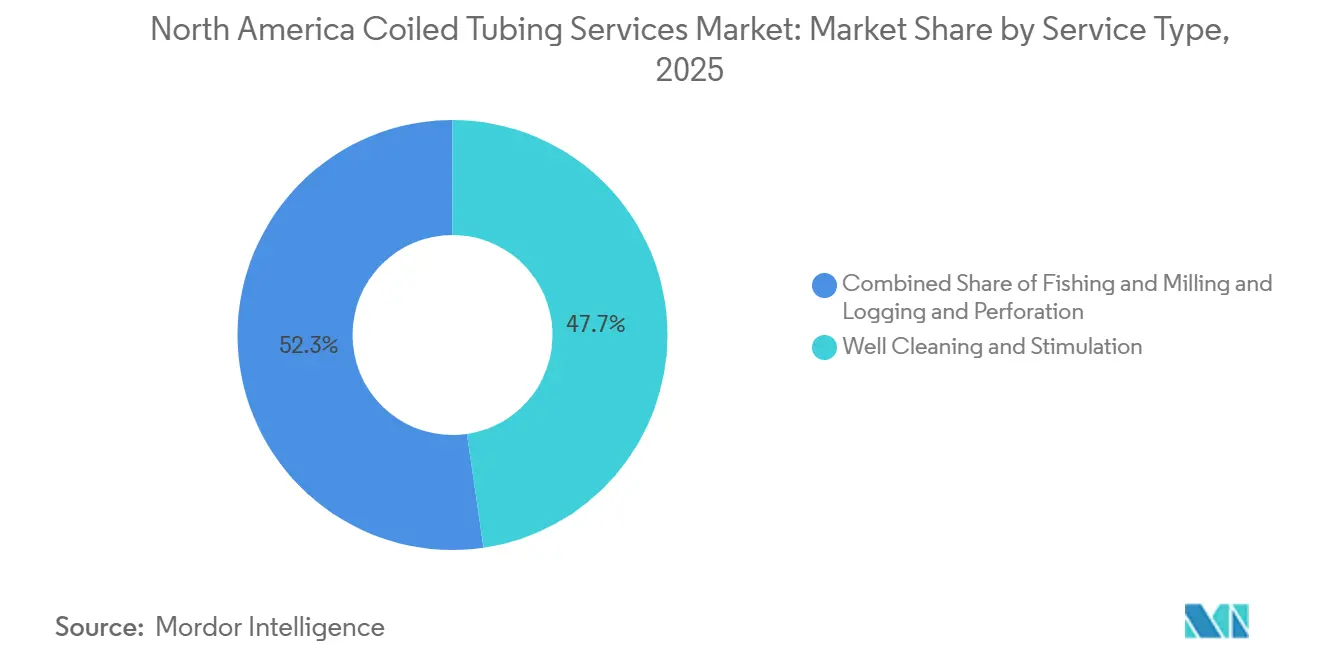

- By service type, well cleaning and stimulation captured 47.7% of the North America coiled tubing services market share in 2025 and is advancing at a 5.3% CAGR through 2031.

- By pipe diameter, 2-to-2.5-inch units will record the fastest 5.6% CAGR, while up to 2-inch strings retained 39.5% of the North America coiled tubing services market size in 2025.

- By application, well intervention dominated with 59.2% revenue share in 2025 and will maintain a 5.2% CAGR through 2031.

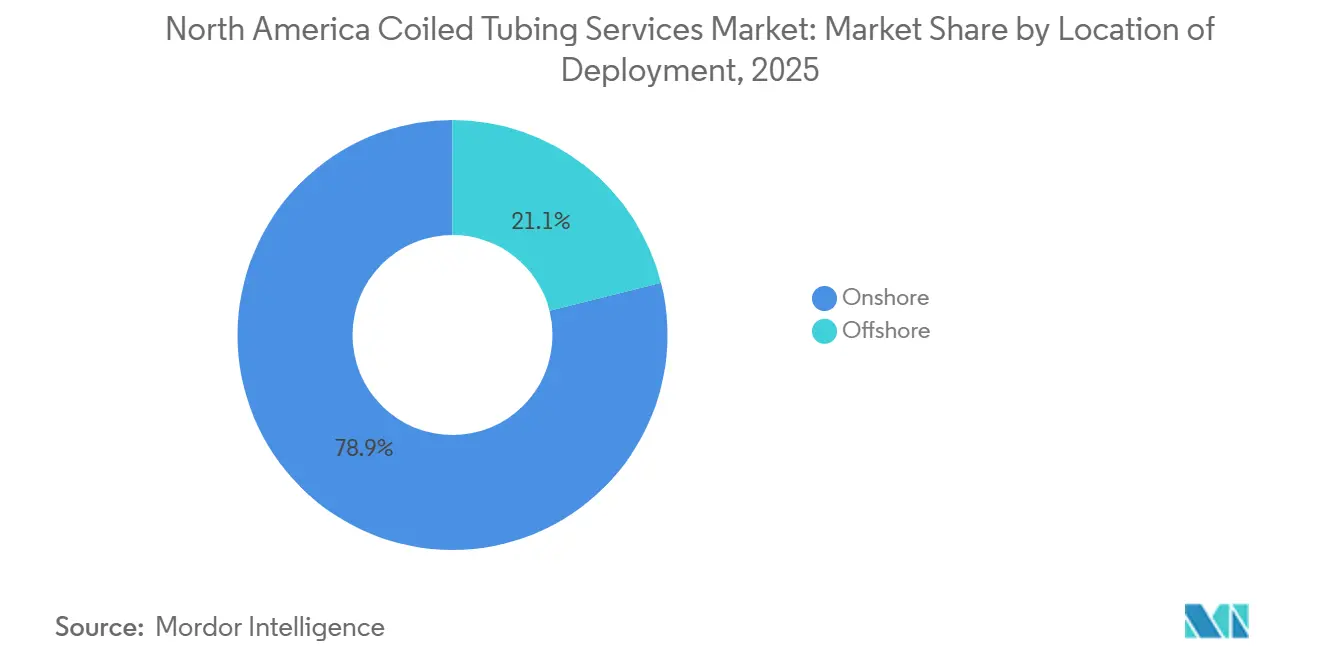

- By deployment location, offshore revenue is forecast to grow at 6.1% CAGR, outpacing the larger onshore segment that held 78.9% of 2025 revenue.

- By geography, the United States accounted for 75.6% of 2025 sales and is set to grow at a 5.4% CAGR on the back of Permian Basin activity.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Coiled Tubing Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shale-driven well-intervention boom | + 1.8% | United States (Permian, Eagle Ford, Bakken), Western Canada Sedimentary Basin | Medium term (2–4 years) |

| Rig-less CT cost advantage for mature wells | + 1.2% | United States (all major basins), Canada (Alberta, Saskatchewan) | Long term (≥ 4 years) |

| Automation & real-time data adoption | + 1.0% | North America-wide, early gains in Permian and Gulf of Mexico deepwater | Medium term (2–4 years) |

| Geothermal & CCUS retrofit demand | + 0.6% | United States (Texas Gulf Coast, California, Utah geothermal), Canada (Alberta CCUS hubs) | Long term (≥ 4 years) |

| Electrified/Hybrid CT units for ESG goals | + 0.4% | North America-wide, concentrated in jurisdictions with emissions reporting mandates | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Electrified/Hybrid CT Units for ESG Goals

KLX Energy Services’ Whisper Series electric unit cut diesel use by 40% on a Permian project, helping operators meet Scope 1 targets under Canada’s CAD 80-per-tonne carbon price [4]KLX Energy Services, “Whisper Series Electric Coiled Tubing,” klxes.com. While power-grid access still limits deployment in remote Bakken fields, pad sites with electricity infrastructure are seeing sub-18-month paybacks through fuel savings.

Rig-Less CT Cost Advantage for Mature Wells

Mobilizing a workover rig costs USD 15,000–25,000 per day and often requires a week on location, whereas a coiled tubing unit can rig up in four hours at rates below USD 10,000 per day. The 30–50% cost reduction and up to 80% lower emissions in plug-and-abandonment projects encourage operators in Texas, Oklahoma, and Alberta to adopt rig-less techniques when WTI trades near USD 70 per barrel [1]HydraWell, “HydraCT Plug-and-Abandonment Case Study,” hydrawell.com.

Automation & Real-Time Data Adoption

Fiber-optic systems such as Baker Hughes’ TeleCoil and Schlumberger’s ACTive transmit downhole pressure and temperature to surface in real time, preventing costly fishing runs and reducing non-productive time by roughly 20% [2]Baker Hughes, “TeleCoil Real-Time Intervention,” bakerhughes.com. Operators now regard “blind” interventions as unacceptable in high-value horizontals where a single mis-step can erase USD 0.5 million in revenue.

Geothermal & CCUS Retrofit Demand

The U.S. Department of Energy identifies coiled tubing as a preferred method for carbon-capture well monitoring because it can deploy logging tools without killing the well. Schlumberger recently boosted a geothermal plant’s output by 14 MW after a coiled-tubing acid wash, proving the technology’s cross-sector relevance [3]Schlumberger, “ACTive Fiber-Optic Intervention Technology,” slb.com.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Crude-oil price volatility | -0.8% | North America-wide, most acute in U.S. shale basins and Canadian oil sands | Short term (≤ 2 years) |

| Skilled CT workforce shortage | -0.5% | United States (Permian, Bakken, Eagle Ford), Canada (Alberta, Saskatchewan, British Columbia) | Medium term (2–4 years) |

| Stringent HSE regulations | -0.4% | United States (OSHA jurisdiction), Canada (provincial OH&S), Mexico (STPS oversight) | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Crude-Oil Price Volatility

WTI averaged in the mid-USD 60s during 2025, squeezing operator cash flow and trimming discretionary workover budgets. While EIA now projects USD 87 per barrel for 2026, the agency’s forecast revision history keeps decision-makers cautious, leading many to lock in long-term contracts or pivot toward geothermal and CCUS work where revenues decouple from oil benchmarks.

Skilled CT Workforce Shortage

U.S. oilfield services employment fell 2.3% in 2025, and turnover among coiled tubing crews topped 20% as workers migrated to construction jobs. NOV injector automation trims crew size from five to three, but complex fishing or milling still requires seasoned hands that take 12–18 months to train.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Stimulation Leads, Logging Gains Traction

Well cleaning and stimulation accounted for 47.7% of the North America coiled tubing services market size in 2025 and is set for a 5.3% CAGR through 2031. Multi-well pad developments in the Permian favor coiled tubing acid circulations that avoid shutting in adjacent wells. Integrated logging-while-cleaning packages, made possible by real-time fiber optics, eliminate separate wireline mobilizations and cut intervention time by 30%.

Logging and perforation revenues, though smaller, are compounding as operators capture production diagnostics during routine cleanouts. Fishing and milling remain critical for stuck tools in ultra-deep horizontals; Cudd Energy Services’ 31,000-foot string exemplifies how providers combine reach with tensile strength for high-risk retrievals. The service mix is pivoting toward higher-margin, telemetry-enabled offerings, squeezing margins for crews restricted to commodity cleanouts.

By Pipe Diameter: Ultra-Deep Drives Mid-Range Growth

Strings up to 2 inches held 39.5% of 2025 sales, yet the 2-to-2.5-inch category will clock the fastest 5.6% CAGR as STEP Energy Services’ UDx fleet pushes interventions to 35,000 feet in Wolfcamp D wells. Larger diameters deliver greater flow rates for acid and proppant removal while withstanding higher collapse pressures.

Tubing above 2.5 inches remains niche, serving Canadian steam-assisted gravity drainage wells that demand thermal resilience. Copper Tip Energy’s 2-⅞-inch strings operate at 3,700 meters in 300 °C service, highlighting the extreme-condition envelope where oversize tubing still plays.

By Application: Intervention Dominance Reflects Aging Well Base

Intervention work captured 59.2% of 2025 revenue and is expanding at 5.2% CAGR as more than 900,000 U.S. wells drilled before 2015 enter decline. Schlumberger has logged over 330 Gulf of Mexico deep-water interventions, many executed with coiled tubing that avoided expensive rig mobilizations.

Completion-phase plug milling retains a steady slice, while drilling with coiled tubing is limited to niche sidetrack jobs. Providers that bundle stimulation, logging, and fishing into turnkey packages earn premium pricing, whereas fleets offering only commodity completion support face utilization risk.

By Location of Deployment: Offshore Outpaces Onshore Growth

Onshore pads produced 78.9% of 2025 revenue thanks to fleet scale and rapid mobilization. Yet offshore demand will outstrip with a 6.1% CAGR as Gulf operators address plug-and-abandon mandates. EnerMech’s 2025 Hoover Diana award underscores the savings of rig-less deep-water abandonment, where coiled-tubing day rates, though 2–3× higher than land jobs, remain well below semisubmersible mobilization costs.

Land-focused fleets are emphasizing chassis with 80,500-pound payloads such as NOV’s Ultra-High Capacity unit to improve logistics on congested Permian leases. The bifurcation between low-cost onshore efficiency and high-spec offshore complexity is widening, creating two distinct competitive arenas within the broader North America coiled tubing services market.

Geography Analysis

The United States generated 75.6% of 2025 sales and will post a 5.4% CAGR through 2031 as Permian gross production climbs from 6.2 million b/d in 2024 to a projected 6.8 million b/d in 2027. Longer laterals raise intervention frequency, while Gulf of Mexico deep-water wells command USD 1 million–5 million per intervention, bolstering revenue density.

Canada growth is driven by oil-sands thermal wells and conventional workovers in Alberta and Saskatchewan. Trican’s September 2025 purchase of Iron Horse added 10 high-capacity units capable of 8,000-meter runs, positioning the firm for seasonal turnaround surges where wages have risen 3.6–4.0% annually. Pipeline constraints and labor shortages temper growth, but carbon-capture hubs in Alberta promise steady long-run demand.

Mexico, though smallest, is the fastest grower as Pemex and private concessionaires tackle mature onshore fields and deep-water Gulf wells. Schlumberger’s ACTive case study doubled production on an onshore job, validating high-spec packages in a market where regulatory complexity rewards operators able to navigate procurement frameworks.

Competitive Landscape

North America Coiled Tubing Services Market is semi consolidated. Schlumberger, Halliburton, and Baker Hughes dominate high-spec deep-water work, leveraging proprietary telemetry such as ACTive and TeleCoil. Regional specialists STEP Energy Services, Trican, Calfrac excel in onshore pads with localized logistics. Welltec’s December 2024 purchase of Pipesnake brings robotic conveyance into integrated packages, signaling a shift toward intervention “ecosystems” that combine coiled tubing, tractors, and downhole robotics.

Technology is the principal differentiator. Providers offering real-time data reduce non-productive time by up to 20% and win multi-year master-service agreements at premium rates. Advances in electrified units and automated injectors offset the workforce squeeze and align with ESG metrics, putting fleets reliant on diesel-hydraulic equipment at risk of under-utilization.

White-space expansion into geothermal and CCUS wells is accelerating. Azure Holdings formed a USD 14 million joint venture in November 2024 targeting stripper-well abandonment and carbon-storage monitoring, illustrating how nimble entrants can carve niches outside traditional oil and gas cycles. Overall, technology adoption, automation, and service bundling dictate share movement more than sheer fleet count.

North America Coiled Tubing Services Industry Leaders

Schlumberger Limited

Halliburton Company

Baker Hughes Company

Weatherford International plc

Calfrac Well Services Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Trican Well Service Ltd. acquired Iron Horse Coiled Tubing Inc. The transaction, involving both cash and equity consideration, enhanced Trican’s coiled tubing fleet and service capabilities in Canada. This acquisition aligns with the growing demand for well intervention and completion services, where coiled tubing plays a vital role.

- August 2025: Reeflex Solutions Inc., through Coil Solutions Inc., expanded its partnership with GOES GmbH to globally distribute coiled tubing injectors and associated intervention equipment. This initiative strengthens equipment supply chains and improves technology availability, indirectly supporting fleet expansion in the U.S. and Canadian markets.

- June 2025: EnerMech secured a contract from ExxonMobil to deliver a comprehensive flowline decommissioning package for the Hoover Diana development in the Gulf of Mexico. The project scope includes decommissioning subsea flowlines, marking EnerMech’s first significant decommissioning campaign in the region. A specialized team from EnerMech’s Energy Solutions division will execute the project, integrating multiple service lines such as coiled tubing, pressure pumping, chemical services, filtration, separation, and pipeline gauging. The operations include flushing, pigging, and filling subsea pipelines to safely remove hydrocarbons and prepare for decommissioning. Specific tasks involve umbilical flushing, pipeline flushing, seawater fill operations for the subsea flowline loop, nitrogen flushing via subsea vessel, coiled tubing services, and final seawater filling for the Northern Diana flowline.

- March 2025: Tenaris showcased its latest coiled tubing solutions at the 2025 SPE/ICoTA Well Intervention Conference and Exhibition, held at the Woodlands Waterway Marriott Hotel and Convention Center in The Woodlands, Texas. Tenaris experts presented insights into its coiled tubing portfolio, which offers high reliability across various applications, including milling frac plugs, fishing, drilling, fracturing, logging, perforating, and stimulation operations.

North America Coiled Tubing Services Market Report Scope

Coiled Tubing Services (CTS) are specialized operations in the oil and gas industry that utilize a continuous, flexible steel pipe deployed from a reel to perform well intervention tasks without interrupting production. These services enable efficient activities such as well cleaning, stimulation, logging, perforation, and mechanical repairs. Their capability to operate in live wells enhances safety, minimizes downtime, and reduces operational costs, making them an effective solution for maintaining and optimizing oil and gas well performance.

The North America coiled tubing services market is segmented by service type, pipe diameter, application, location of deployment, and geography. By service type, the market is segmented into well cleaning and stimulation, logging and perforation, and fishing and milling. By pipe diameter, the market is segmented into up to 2 in, 2 to 2.5 in, and above 2.5 in. By application, the market is segmented into drilling, completion, and well intervention. By location of deployment, the market is segmented into onshore and offshore. By geography, the market is segmented into the United States, Canada, and Mexico. The report also covers the market sizes and forecasts for the North America coiled tubing services market across these key countries. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Well Cleaning and Stimulation |

| Logging and Perforation |

| Fishing and Milling |

| Up to 2 in |

| 2 to 2.5 in |

| Above 2.5 in |

| Drilling |

| Completion |

| Well Intervention |

| Onshore |

| Offshore |

| United States |

| Canada |

| Mexico |

| By Service Type | Well Cleaning and Stimulation |

| Logging and Perforation | |

| Fishing and Milling | |

| By Pipe Diameter | Up to 2 in |

| 2 to 2.5 in | |

| Above 2.5 in | |

| By Application | Drilling |

| Completion | |

| Well Intervention | |

| By Location of Deployment | Onshore |

| Offshore | |

| By Geography | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

How large will the North America coiled tubing services market be by 2031?

It is forecast to reach USD 4.44 billion by 2031, growing at a 4.99% CAGR from 2026 to 2031.

Which service type generates the most revenue?

Well cleaning and stimulation, holding 47.7% of 2025 revenue and expanding at a 5.3% CAGR through 2031.

Why is offshore demand growing faster than onshore?

Gulf of Mexico plug-and-abandon mandates and high-value deep-water interventions push offshore revenue to a 6.1% CAGR, outpacing land-based jobs.

What technology trends are redefining service quality?

Real-time fiber-optic telemetry, electrified coiled tubing units, and automated injectors cut non-productive time and meet ESG targets.

How are providers mitigating labor shortages?

Automation reduces crew sizes, while long-term training and retention programs keep seasoned specialists on high-spec fleets.

Page last updated on: