North America Art Logistics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.36 Billion |

| Market Size (2026) | USD 1.40 Billion |

| Market Size (2031) | USD 1.71 Billion |

| Growth Rate (2026 - 2031) | 4.11% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Art Logistics Market Analysis by Mordor Intelligence

The North America art logistics market size is expected to increase from USD 1.36 billion in 2025 to USD 1.40 billion in 2026 and reach USD 1.71 billion by 2031, growing at a CAGR of 4.11% over 2026-2031.

The headline numbers disguise an ongoing structural shift. Transaction counts remained firm, yet the recent collapse of ultra-high-end lots forced providers to handle smaller, more frequent shipments, compressing yields. Mexico’s accelerated growth reflects rising collector wealth and cross-border demand for Latin American contemporary pieces, although capacity outside Mexico City remains thin. Younger demographics already account for a significant portion of purchases at the major auction houses, and their insistence on blockchain tracking and low-carbon delivery is accelerating investment in digital provenance, reusable crates, and electric fleets. Finally, exclusive partnerships, such as Convelio becoming Phillips’ global partner in April 2026, signal a pivot toward vertically integrated models that bundle transport, storage, and cataloging, reshaping competitive dynamics.[1]U.S. Customs and Border Protection, “Works of Art, Collector's Pieces, Antiques, and Other Cultural Property,” cbp.gov

Key Report Takeaways

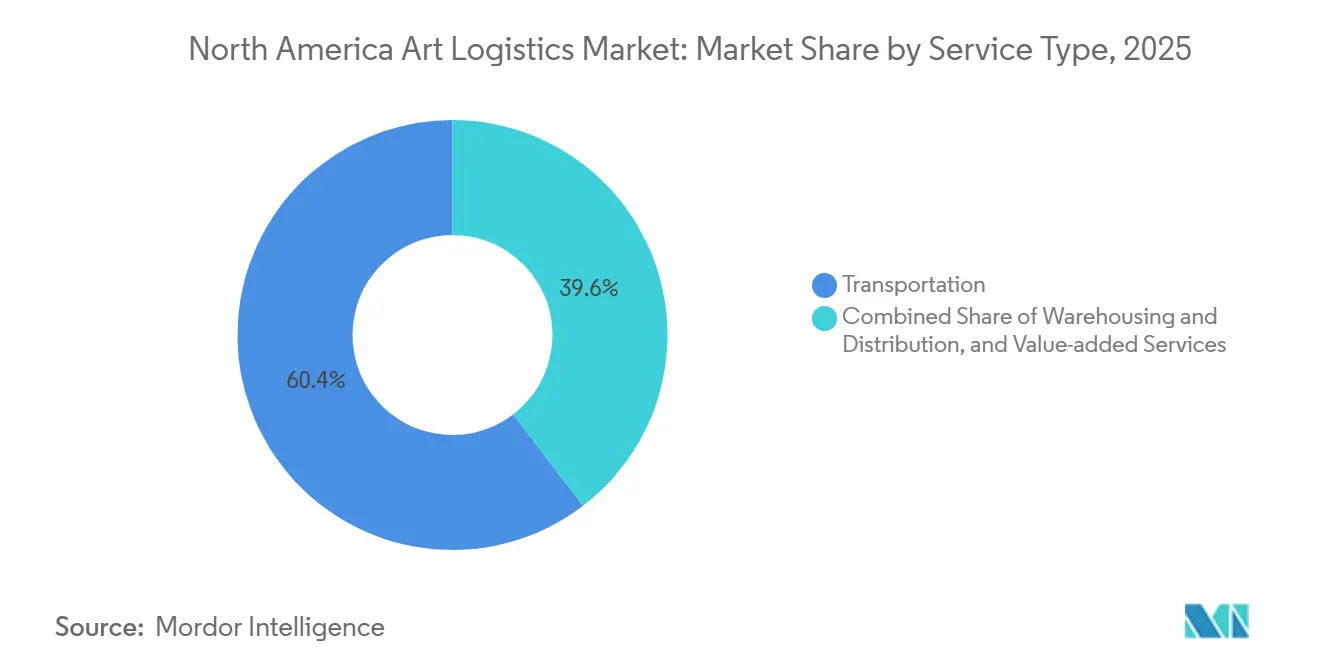

- By service type, transportation accounted for the 60.39% of the North America art logistics market share in 2025, while value-added services will advance at a 5.20% CAGR through 2031.

- By application, art dealers and galleries led with a 34.87% of the North America art logistics market size in 2025; museums represent the fastest-growing application, set to grow at a 5.08% CAGR to 2031.

- By country, the United States accounted for 90.62% of the North America art logistics market share in 2025, whereas Mexico is forecast to post the fastest 5.09% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Art Logistics Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding high-net-worth individual (HNWI) wealth and art allocation in North America | +1.2% | United States coasts, Canada (Vancouver, Toronto), Mexico (Mexico City) | Long term (≥ 4 years) |

| Rising share of Millennial and Generation Z buyers | +0.9% | United States urban centers, Canada, and Mexico | Medium term (2 – 4 years) |

| Resilient transaction volume despite lower values | +0.8% | United States (New York, Los Angeles), Canada (Toronto) | Medium term (2 – 4 years) |

| Accelerated shift to online bidding and digital sales channels | +0.6% | United States, Canada, Mexico | Short term (≤ 2 years) |

| Strong North American air-cargo capacity and demand growth | +0.5% | United States hubs (JFK, LAX), Canada (Toronto Pearson) | Short term (≤ 2 years) |

| United States museum and institutional recovery to near pre-pandemic levels | +0.4% | United States, Canada | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Expanding High-Net-Worth Individual Wealth and Art Allocation in North America

Tech and private-equity fortunes have pushed HNWI collectors to devote a substantially larger share of their wealth portfolios to art, marking a distinct increase year-over-year. This growing allocation drives demand for climate-controlled trucks, real-time tracking, and tailored insurance, which command premium pricing. The western United States already accounts for a major share of domestic art purchases, yet regional hubs like Phoenix and Seattle lack the vault capacity of New York, creating geographic arbitrage opportunities for adventurous providers. Younger HNWIs, who now make up a significant and growing segment of buyers at major auction houses, also insist on blockchain certificates and low-carbon fleets; industry leaders like Crown Fine Art have answered with meaningful emission reductions and electric vans, signaling a green pivot that laggards must match.[2]Federal Reserve Board, “Distributional Financial Accounts of the United States,” federalreserve.gov

Rising Share of Millennial and Gen-Z Buyers

A notable segment of Christie's recent clientele was younger buyers. They prize transparency and sustainability over hush-hush discretion, demanding mobile tracking, NFC-tagged reports, and reusable crates. Gander & White partnered with ROKBOX Loop to supply recyclable cases and rolled out electric vans in New York and Los Angeles, directly courting the eco-minded cohort. Price sensitivity pressures margins per job, yet higher frequency and appetite for subscription services covering transport, storage, and cataloging offer predictable cash flow for firms that adapt early.

Resilient Transaction Volume Despite Lower Values

Auction counts held up in 2025 even as typical lot values fell, creating a logistics paradox of busy schedules but slimmer margins. Dealers with annual turnover below USD 500,000 booked double-digit sales gains, yet chose cost-sensitive couriers, eroding premium fee capture. Established specialists answered with modular “à la carte” menus to compete with mass-market carriers while maintaining white-glove tiers for trophy works. Simultaneously, auction houses focused on best-in-class consignments, pivoting demand toward firms such as Crozier Fine Arts, which fields 180 climate-controlled vehicles serving more than 100 cities each week. As volumes shift down-market, scalable service bundles will decide winners.

Accelerated Shift to Online Bidding and Digital Sales Channels

Pure online sales slipped to 15% of total market value in 2025, but absolute deal counts climbed, proving that digital now complements, rather than replaces, the live saleroom. Lower-priced online lots still require professional packing, widening the mid-value shipment pool. Social media platforms directly drove purchases for approximately 34% of collectors under 35, yet many artists self-ship, fragmenting logistics. Aggregators that can bolt turnkey fulfillment onto social platforms stand to win. Regulators treat online buys like any import, so Harmonized Tariff Schedule claims, and CITES permits still slow door-to-door times, making expert compliance advice a new revenue line.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Collapse of the high-end segment (more than USD 10 million) | -0.7% | United States (New York), spillover to Canada | Short term (≤ 2 years) |

| Contraction in the global art market value | -0.5% | United States, Canada, Mexico | Short term (≤ 2 years) |

| Severe slump in contemporary (post-2000) art | -0.4% | United States urban centers, Canada | Medium term (2 – 4 years) |

| Persistent auction weakness into 2025 | -0.3% | United States (New York, Los Angeles), Canada | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Collapse of the High-End Segment (More Than USD 10 Million)

H1 2025 saw marquee failures, forcing auction houses to pull consignments and leaving white-glove fleets idle. H2 bounce, powered by the Leonard A. Lauder estate that fetched USD 527.5 million at Sotheby’s, feels episodic rather than structural. With 39 of the year’s top 50 lots hammered in New York, geographic concentration magnifies downside risk. Guarantees covered 78% of New York evening-sale value, a level that may not hold if sentiment cools in 2026, threatening shipment pipelines again.

Contraction in the Global Art Market Value

Global sales stabilized at a robust level in 2025, though still falling noticeably short of the market's recent peak. Dealer gains were muted while private sales experienced a slight decline, signaling collector caution that trims high-value cross-border moves. Localized buying rose to 71% for small dealers, reducing premium international freight demand. Tariff anxiety compounds the slide: more than half of dealers cited higher paperwork and costs, nudging collectors to source domestically. Until macro uncertainty clears, logistics volume remains skewed toward lower-value, lower-margin jobs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Value-Added Services Capture the Technology Premium

Transportation accounted for 60.39% of the North America art logistics market share in 2025, underscoring its role in transporting lots from auction to collector. Yet value-added services are on course for a 5.20% CAGR to 2031, the fastest within the North America art logistics market. Younger buyers want blockchain provenance, digital condition reports, and sustainability audits, in addition to crating and trucks. Verisart’s tie-up with Arta delivers digital certificates at the hand-off, satisfying both insurance underwriters and tech-savvy collectors. CBP’s strict documentation checks and 5- to 30-day CITES waits increase the payout for compliance consulting, lifting margins from the usual 10-15% on transport to more than 30% for bundled advisory packages.

Operational upgrades reinforce this shift. Crozier Fine Arts fitted diesel particulate filters across its 180-vehicle fleet, Gander & White rents ROKBOX Loop’s reusable crates, and Crown Fine Art is aggressively decarbonizing its operations through broad Scope 1 and 2 emissions reductions and early fleet electrification. These moves meet Millennial carbon standards while reducing long-term cost per trip. Warehousing remains vital for inventory between sale cycles, but free storage offers from Sotheby’s and Christie’s squeeze that revenue line, prompting operators to cross-sell climate monitoring, pest control, and digital cataloging. Transportation will remain the revenue heavyweight, yet profitability will hinge on stitching value-added modules into every shipment and quoting premiums where regulatory friction is highest.[3]U.S. Customs and Border Protection, “Duty on personal and commercial imports of antiques and artwork,” cbp.gov

By Application: Museums Spark the Fastest Growth

Art dealers and galleries accounted for 34.87% of the North America art logistics market size in 2025. Still, museums are set to expand at a 5.08% CAGR, the quickest among applications. Exhibition lending resumed to pre-pandemic cadence in 2025 as the Metropolitan Museum of Art and peers reinstated global loan programs. Deaccessions add fresh lanes: the Kawamura Memorial DIC Museum of Art’s Monet consignment to Christie’s demanded bespoke packing, provenance vetting, and USD-million insurance riders, each billed at premium rates.

Auction houses remain a lumpy but lucrative client set, with 2025’s Lauder sale at Sotheby’s moving 55 masterpieces and requiring synchronized pick-up, bonded storage, and high-value installs. Art fairs keep the shuttle trucks rolling; Art Basel Miami Beach’s 2025 opening-day sales soared 40% year-on-year, translating to brisk turn-and-burn transport cycles. Private collectors, especially HNWIs under 45, now request concierge subscriptions bundling transport, storage, and portfolio cataloging on an annual retainer, smoothing cash flow for logistics firms. Regulatory stringency around ivory, tortoiseshell, and wildlife components solidifies demand for institutions willing to pay for bulletproof CITES paperwork.

Geography Analysis

The United States dominated 90.62% of the North America art logistics market in 2025, energized by New York, where every top-10 global lot hammered last year. Auction turnover at Christie’s, Sotheby’s, and Phillips rebounded strongly, generating massive multibillion-dollar sales volumes, but activity was heavily skewed. Secondary metros such as Phoenix, Austin, and Miami posted the fastest collector-wealth gains, yet lack vault capacity, nudging UOVO to buy Vault Fine Art Services in Austin in January 2026. Convelio’s flagship New York hub, due autumn 2026, shows that capacity wars remain concentrated around key coasts even as inland demand rises. Customs and CITES scrutiny lengthened the United States entry clearance to as long as 30 days for wildlife-component pieces, so most firms now stage buffer inventory at bonded warehouses near JFK and LAX.

Canada offers steady but slower growth. Toronto and Vancouver anchor collector demand, and regulatory symmetry with the United States Customs eases cross-border flows, yet a significant portion of Canadian dealers cited regulatory and customs friction, including tariff paperwork, as a notable drag in 2025. Various collectors are therefore buying locally, trimming premium trans-border jobs. Shuttle operators such as Gander & White capitalize on Art Basel Miami flows but see episodic surges rather than steady lanes. Concentration risk looms: a downturn in just two Canadian metros would ripple across the country’s slim pipeline of high-value movements.

Mexico, although only a sliver of current revenue, will clock the region’s fastest 5.09% CAGR through 2031. Rising household wealth and a vibrant contemporary scene spur shipments of Latin American art northward. Yet specialized infrastructure remains mostly in Mexico City, limiting nationwide scale. CITES requirements for protected-material works add 5- to 30-day delays, deterring some cross-border imports. UOVO’s Miami and Palm Beach vaults position it as a gateway, but episodic deal flow and collectors’ preference for domestic storage temper upside. Long-run expansion hinges on rolling out climate-controlled warehouses beyond the capital and streamlining customs formalities through bilateral initiatives.[4]U.S. Customs and Border Protection, “Importing endangered species of wildlife, plants, ivory, exotic skins and animals,” cbp.gov

Competitive Landscape

Competition in the North America art logistics market is shaped by a three-way tussle among specialist handlers, auction-house captive units, and integrators. UOVO, Crozier Fine Arts, and Gander & White sit in the specialist camp, offering deep curatorial expertise, bonded storage, and bespoke insurance for USD-million works. Auction houses field in-house arms, such as Sotheby’s Art Logistics and Christie’s Fine Art Storage Services, that lock clients into proprietary networks. Global parcel giants FedEx and DHL wield unmatched air-cargo networks, but their low default liability and lighter curatorial bench constrain their share in shipments over USD 1 million.

Strategic moves underline the race for scale. Convelio’s April 2026 funding round and exclusive Phillips deal give it guaranteed auction volume and the capital to open a flagship New York hub. UOVO has pursued a roll-up strategy, snapping up TYart, Orange County Fine Art Services, and Museo Vault over the past several years. These acquisitions extend the reach into secondary wealth corridors, though integration and high real estate costs weigh on margins. Asset-light entrants such as Arta Shipping instead partner with third-party warehouses, freeing cash to build digital provenance layers, but they must still convince insurers and HNWIs of security parity.

Technology and sustainability are the new battlegrounds. Verisart, The Fine Art Ledger, and Transient Labs supply blockchain backbones that early adopters embed into service bundles. Gander & White and Crown Fine Art advertise EcoVadis scores and fleet electrification, courting younger buyers who view carbon footprint as part of service quality. Compliance capability is another moat: navigating CBP, CITES, and the United States Fish and Wildlife Service paperwork requires seasoned legal teams, tilting the field to incumbents that already invested in regulatory infrastructure. Overall, the North America art logistics market rewards firms that pair hard assets, vaults, trucks, and warehouses with data-driven workflows and green credentials.

North America Art Logistics Industry Leaders

Gander & White

UOVO

Cadogan Tate

Arta Shipping Inc.

FedEx

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Convelio raised new capital and became Phillips’ global logistics partner, while announcing a flagship New York warehouse for autumn 2026.

- January 2026: UOVO bought Vault Fine Art Services in Austin, expanding a roll-up that already includes TYart, Orange County Fine Art Services, and Museo Vault.

- January 2026: The Rock-It Company expanded its DIETL network by acquiring Delaware Freeport and three regional firms, integrating the US's only fine-art-dedicated Foreign Trade Zone into its infrastructure.

- November 2025: Sotheby’s sold Gustav Klimt’s Portrait of Elisabeth Lederer for USD 236.4 million from the Leonard A. Lauder estate, driving premium white-glove demand.

North America Art Logistics Market Report Scope

| Transportation |

| Warehousing & Distribution |

| Value-added Services (Labelling, Kitting, Consulting) |

| Art Dealers and Galleries |

| Auction Houses |

| Museums |

| Art Fairs |

| Private Collectors |

| Other Applications |

| United States |

| Canada |

| Mexico |

| By Service Type | Transportation |

| Warehousing & Distribution | |

| Value-added Services (Labelling, Kitting, Consulting) | |

| By Application | Art Dealers and Galleries |

| Auction Houses | |

| Museums | |

| Art Fairs | |

| Private Collectors | |

| Other Applications | |

| By Country | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

What is the projected value of the North America art logistics market in 2031?

The North America art logistics market size is forecast to reach USD 1.71 billion by 2031, growing at a 4.11% CAGR from 2026 to 2031.

Which service type holds the largest share in regional art logistics?

Transportation captured 60.39% of North America art logistics market share in 2025, reflecting its centrality in moving works between auctions, galleries, and collectors.

Which application segment is expected to grow fastest to 2031?

Museums are set to post the highest 5.08% CAGR, supported by a rebound in exhibition loans and rising deaccessions.

Why is Mexico the fastest-growing geography?

Mexico benefits from expanding collector wealth and cross-border trading of Latin American art, pushing the market toward a 5.09% CAGR despite infrastructure gaps in cities outside Mexico City.

How are sustainability concerns affecting logistics providers?

Younger buyers demand low-carbon fleets and reusable crates, prompting firms such as Gander & White and Crown Fine Art to adopt electric vehicles and recyclable packaging, which differentiates their services in competitive bids.

What technology trends are shaping the industry?

Blockchain provenance systems, including Verisart, The Fine Art Ledger, and NFC-enabled T.R.A.C.E., are being integrated into standard service bundles to satisfy both insurance requirements and Millennial demands for transparency.

Page last updated on: