Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

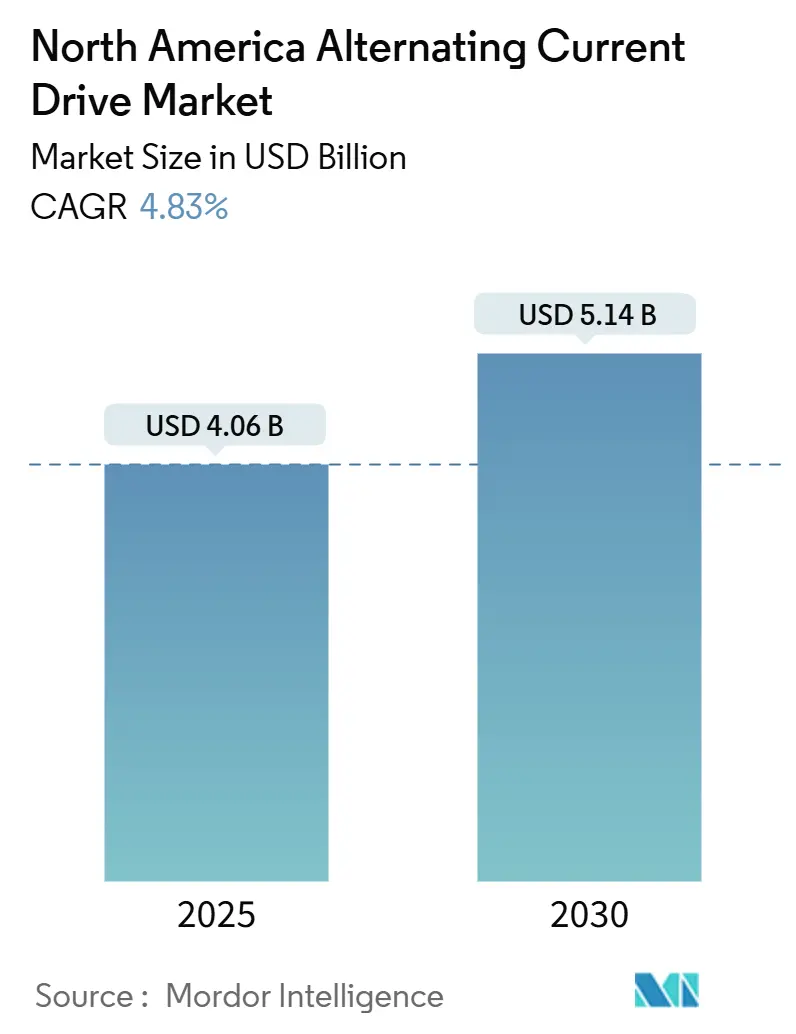

| Market Size (2025) | USD 4.06 Billion |

| Market Size (2030) | USD 5.14 Billion |

| Growth Rate (2025 - 2030) | 4.83% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Alternating Current Drive Market Analysis by Mordor Intelligence

The North America alternating current drive market size is valued at USD 4.06 billion in 2025 and is projected to reach USD 5.14 billion by 2030, advancing at a 4.83% CAGR across the forecast horizon. Growing brownfield retrofits tied to nearshoring, a pivot toward medium-voltage solutions, and new grid-interactive use cases are reshaping both technology roadmaps and commercial strategies in the North America alternating current drive market. Large utilities now incentivize active-front-end topologies that support demand-response, while federal efficiency rules tighten standby-loss limits, collectively lifting replacement demand. Medium-voltage and high-power segments benefit from capital-intensive projects in oil & gas, municipal water, and data-center cooling, whereas low-voltage drives maintain volume leadership but exhibit slower unit growth. Competitive intensity remains moderate: the five leading suppliers collectively command roughly 55% revenue, yet no single firm dominates niche applications such as harmonic-mitigated or regenerative drives, keeping the North America alternating current drive market open to specialists focused on edge AI and grid services.

Key Report Takeaways

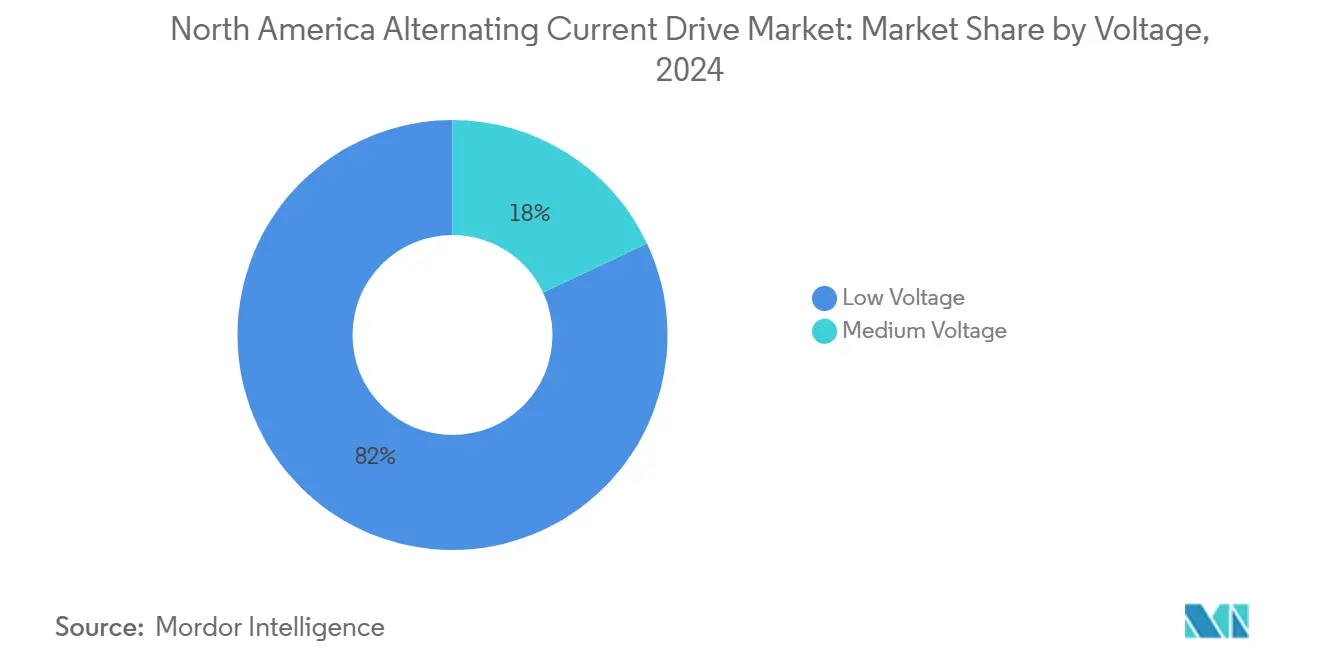

- By voltage, low-voltage units secured 82% of the North America alternating current drive market share in 2024, while medium-voltage drives are forecast to grow at an 8.5% CAGR through 2030.

- By power rating, low-power drives in the 1–100 kW band accounted for 47% of the North America alternating current drive market size in 2024, whereas high-power drives above 500 kW are set to expand at a 7.8% CAGR to 2030.

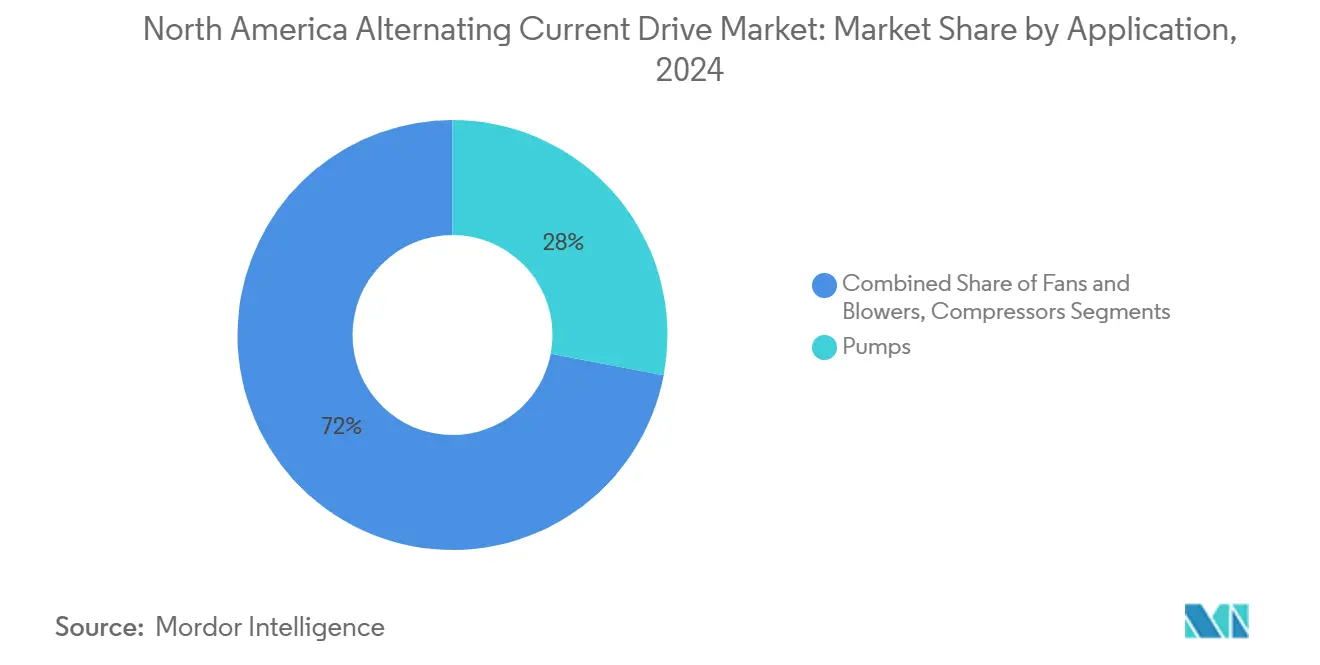

- By application, pumps led with a 28% revenue share in 2024, but HVAC systems are advancing at a 9.2% CAGR through 2030 due to stringent building energy codes.

- By end-user, oil and gas retained a 31% share in 2024, yet water and wastewater utilities are poised for an 8.7% CAGR on Infrastructure Investment and Jobs Act funding.

- By country, the United States held 86% of 2024 sales, although Canada is projected to post the fastest 7.9% CAGR thanks to CAD 93 billion in clean-economy tax credits.

North America Alternating Current Drive Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ease of Regulation on Energy Efficiency Implementation | +0.6% | United States, Canada | Medium term (2-4 years) |

| Emerging Demand for Sensorless Drives | +0.4% | United States, Canada | Long term (≥4 years) |

| Rising Investments in Industrial Automation Across North America | +1.2% | United States, Canada, Mexico nearshoring zones | Short term (≤2 years) |

| Adoption of AI-Enabled Predictive Maintenance Algorithms in AC Drives | +0.8% | United States, Canada | Medium term (2-4 years) |

| Nearshoring Manufacturing Leading to Retrofit Opportunities in United States and Mexico | +1.0% | United States, Mexico | Short term (≤2 years) |

| Integration of Variable Frequency Drives with Smart Grid Demand Response Programs | +0.7% | United States, Canada | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Investments in Industrial Automation Across North America

Industrial automation capital outlays reached USD 78 billion in 2024, with motion control and drives accounting for 18% of the expenditure. Reshoring announcements totaled 244,940 new U.S. manufacturing jobs that same year, and a third of them came from electrical equipment, magnifying immediate demand for low-voltage drives in conveyors, mixers, and packaging lines.[1]Reshoring Initiative, “2024 Report,” reshorenow.org Inflation Reduction Act credits covering up to 30% of qualifying electrification capex further strengthen purchase economics for retrofit projects. Although discrete automation orders softened due to inventory normalization in Europe and Asia, project-driven process automation continued to sustain mid-single-digit growth, favoring suppliers proficient in hazardous-area certifications and multi-motor coordination. Consequently, the North America alternating current drive market is experiencing a pivot from high-volume component sales toward integrated, domain-specific solutions that bundle safety, networking, and analytics.

Nearshoring Manufacturing Leading to Retrofit Opportunities in United States and Mexico

Foreign direct investment into Mexico reached USD 43.9 billion in 2023, and landed-cost advantages already exceed 35% compared with China. U.S. incumbents are upgrading legacy fixed-speed motors to protect competitiveness, while newly built Mexican factories specify energy-efficient drives at inception to satisfy Norma Oficial Mexicana standards and utility rebate programs. Schneider Electric allocated USD 700 million through 2027 for new medium-voltage capacity in Tennessee and expanded robotics facilities in North Carolina, positioning itself close to nearshored production clusters. Persistent 26-week lead times for insulated-gate bipolar transistor modules have accelerated dual-sourcing and on-shore semiconductor assembly, mitigating supply risk but slightly inflating bill-of-material costs. Collectively, these moves channel retrofit and greenfield demand toward medium-voltage offerings, expanding the total addressable base for the North America alternating current drive market.

Adoption of AI-Enabled Predictive Maintenance Algorithms in AC Drives

AI inference is shifting from cloud servers to drive controllers, enabling sub-500 ms latency torque optimization. Siemens’ Xcelerator Digital Drivetrain and ABB’s ACS8080 embed edge modules that learn vibration signatures and predict bearing failure four to six weeks ahead of time. Given that unexpected downtime in process plants costs USD 50,000–USD 250,000 per hour, edge AI reduces maintenance spend by up to 30% while stretching asset life.[2]ABB, “ACS8080 Launch Details,” abb.com Compliance with IEC 62443 is now required in bids serving critical infrastructure, increasing cybersecurity rigor but offering differentiation for vendors with OT-friendly secure-boot firmware. This trend enriches the functional spec of medium-voltage drives and reinforces software-as-a-service revenue streams inside the North America alternating current drive market.

Integration of Variable Frequency Drives with Smart Grid Demand-Response Programs

OpenADR 3.0 allows variable-frequency drives to receive real-time pricing cues, letting industrial facilities trim peak use by 12%–18% with negligible production impact. NREL tests confirm the monetary upside, especially in states applying time-of-use tariffs. The Department of Energy’s 2024 rulemaking mandates efficiency labels and stricter standby thresholds, nudging buyers toward active-front-end converters capable of reactive-power injection. Utilities in Texas and Alberta now pay USD 50–USD 150 per kilowatt of curtailable load, turning drives into revenue-generating assets rather than pure energy savers. As a result, grid-interactive features are becoming a standard line item in request-for-proposal documents across the North America alternating current drive market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Prices of AC Drives | -0.5% | United States, Canada | Short term (≤2 years) |

| Harmonic Distortion Compliance Costs | -0.6% | United States, Canada | Medium term (2-4 years) |

| Semiconductor Supply Chain Disruptions Affecting IGBT Availability | -0.8% | United States, Canada, Mexico | Short term (≤2 years) |

| Shortage of Skilled Installers for Medium-Voltage Drives | -0.4% | United States, Canada | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Semiconductor Supply Chain Disruptions Affecting IGBT Availability

Lead times for IGBT modules lengthened from 12 weeks pre-pandemic to 26 weeks in early 2024 as automotive electrification and solar inverters competed for capacity. STMicroelectronics and Mitsubishi Electric, representing 40% of global supply, kept products on allocation through mid-2024. Spot-market premiums touched 40% for high-current modules, compelling drive makers to re-design boards for alternate die fits and, in some cases, substitute pricier silicon-carbide MOSFETs. Medium-voltage projects are disproportionately hit because each build uses bespoke stacks; commissioning delays of three to six months have become common and knock on to project cash flows. Accordingly, the North America alternating current drive market braces for periodic supply shocks that temper near-term revenue conversion despite robust order books.

Harmonic Distortion Compliance Costs

IEEE 519-2022 tightens total demand distortion ceilings and lowers individual harmonic-order thresholds, pushing end-users to adopt either passive LC filters that add roughly 10% system cost or active-front-end converters that lift capex by up to 30%. Eaton estimates facilities operating non-compliant drives incur utility penalties of USD 0.02–USD 0.05 per kWh, amounting to USD 15,000–USD 40,000 yearly for a 500 kW load. Semiconductor cost deflation is narrowing the active-front-end premium, yet upfront investment remains a barrier for smaller operators. Vendors with integrated harmonic mitigation are therefore advantaged, but price-sensitive buyers delay upgrades, marginally curbing the growth trajectory of the North America alternating current drive market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Voltage: Medium-Voltage Drives Emerge as Growth Engine

Medium-voltage units, typically 2.3–13.8 kV, are projected to register an 8.5% CAGR through 2030, well above the 4.83% broader pace for the North America alternating current drive market. These systems cost three to five times more than low-voltage equivalents but unlock 2%–4% efficiency gains in motors above 1,000 HP, yielding sub-18-month paybacks in continuous-duty operations. Low-voltage devices, although holding 82% share, confront saturation in conveyor, fan, and basic pump duties. Utilities in Texas, California, and Alberta now extend demand-response incentives to loads over 1 MW, steering project specifications toward medium-voltage architectures.

Large capital projects underscore the shift. Oil-sand pipelines in Alberta, municipal water tunnels under the Great Lakes, and gigawatt-scale hydrogen electrolyzer plants across the Gulf Coast all rely on medium-voltage drives for multi-megawatt compressors and pumps. Suppliers are responding with modular stacks, predictive-diagnostic firmware, and arc-flash-rated enclosures that cut field-installation hours by 25%. As a result, the North America alternating current drive market size attributable to medium-voltage platforms is set to widen from USD 0.73 billion in 2025 to nearly USD 1.1 billion in 2030, even as low-voltage volumes stay flat.

By Power Rating: High-Power Drives Take Share in Capital-Intensive Sectors

High-power drives above 500 kW will grow 7.8% annually as pipeline compression, metals rolling, and large water pumping schemes proliferate. Low-power drives remain dominant at 47% of 2024 shipments; nonetheless, growth pivots toward heavier ratings where regenerative braking and liquid cooling deliver outsized lifecycle savings. Siemens extended its offering by acquiring ebm-papst’s Industrial Drive Technology unit, signaling interest in embedded motor-drive packages across the spectrum from 50 W to multiple megawatts.

Project visibility is strong: Chevron’s Tengiz expansion specified 47 variable-speed drives exceeding 2 MW, while Canadian water authorities require regenerative features for every pump above 750 kW to win capital grants. Thermal management remains the key hurdle. Vendors now deploy redundant fan arrays and liquid-cooled heatsinks that raise unit cost by USD 8,000–USD 15,000 but ensure derating-free service up to 50 °C ambient. The North America alternating current drive market size for high-power units should advance from roughly USD 0.62 billion in 2025 to USD 0.90 billion in 2030.

By Application: HVAC Demand Surges on Data-Center Build-Outs

HVAC drives clock a 9.2% CAGR, the fastest among applications, helped by explosive data-center capacity that is forecast to top 1,800 MW by 2026. Pumps still occupy 28% application share, mainly in water distribution and chemical dosing, yet chiller compressors, air handlers, and cooling towers claim larger incremental volumes. DOE’s 2024 regulation forces variable-speed compressors in ≥5-ton rooftop units, propelling retrofit uptake in older commercial buildings.

Data-center developers favor liquid-cooling solutions with inverter-driven pumps and redundant fan trays to meet PUE targets below 1.3. Utility demand-response payments yield USD 100 per kW for curtailable HVAC load, making grid-interactive drives cost-neutral within two years. Consequently, HVAC will account for almost 18% of incremental revenue added to the North America alternating current drive market by 2030.

By End-User Industry: Water Utilities Outpace Oil and Gas

Water and wastewater plants benefit from USD 50 billion in federal funding, advancing at an 8.7% CAGR as municipalities replace aging pumps and add VFD-equipped pressure zones. Oil & gas still account for 31% of 2024 demand, but project sanctioning slows amid energy transition uncertainty. American Society of Civil Engineers notes that 30% of U.S. water mains exceed 50 years of age, making variable-speed retrofits imperative to maintain service pressure while lowering leak risk.

Chemical processing, food and beverage, and pulp and paper industries collectively contribute a quarter of the market revenue, aided by state energy rebates that reimburse 50% of harmonic-mitigation add-ons. Mining outfits adopt drives to cut diesel use in escalators and fans at remote pits. The ongoing decarbonization push, therefore, diversifies the North America alternating current drive market, cushioning it against cycles in any single vertical.

Geography Analysis

The United States anchored 86% of 2024 revenue in the North America alternating current drive market, yet growth moderates as discrete OEM automation stabilizes after an inventory drawdown. Federal spending USD 50 billion for municipal water upgrades and a 30% tax credit for electrification supports pump and HVAC demand, while data-center hubs in Texas and Virginia add megawatt-scale cooling loads.[3]U.S. Department of the Treasury, “Inflation Reduction Act Credits,” treasury.gov Medium-voltage supply chains remain stretched; end-users increasingly order hardware 12–18 months ahead to secure delivery slots.

Canada posts the fastest 7.9% CAGR thanks to CAD 93 billion (USD 67.26 billion) in Clean Economy Investment Tax Credits and four EV battery gigafactories under construction, each requiring hundreds of medium-voltage drives for slurry mixing, coating, and formation lines. Strategic Innovation Fund grants unlock additional demand in critical-mineral processing, where variable-speed mills and conveyors improve energy efficiency by 15%–20%. Lead times for 6 kV drives in Ontario peaked at 32 weeks during 2024, prompting local integrators to stock spares and kits.

Mexico, though not separately itemized, is an emerging growth lever. Manufacturing FDI expands 20% per year, and landed-cost gaps versus China widen to an expected 45% by 2030. Norma Oficial Mexicana efficiency codes align with DOE rules, enabling harmonized product lines for cross-border projects. Together, these developments broaden the addressable base for the North America alternating current drive market.

Competitive Landscape

Siemens broadened its reach with ebm-papst Industrial Drive Technology, adding low-voltage mechatronics that complement its multi-megawatt portfolio. WEG’s USD 400 million purchase of Regal Rexnord’s industrial motors business adds 10 factories and narrows the share gap with ABB, hinting at future leadership jockeying.

Technology is the main battleground. Schneider Electric’s USD 700 million U.S. expansion bankrolls AI test labs and robotics centers, underlining a pivot toward software-intensive edge solutions. Eaton’s role in the EU Shift2DC project could disrupt AC architectures if DC distribution gains traction, although commercial headwinds persist due to entrenched three-phase infrastructure. Vendors differentiate via cybersecurity compliance, grid-service features, and service network breadth, erecting barriers for low-cost Asian entrants.

Skill shortages in medium-voltage commissioning create a service moat for incumbents. ABB and Rockwell Automation operate certified-technician academies that guarantee a 72-hour on-site response, an SLA that many challengers cannot match. Consequently, specialists in harmonic mitigation, regenerative topologies, and edge AI continue to carve profitable niches within the broader North America alternating current drive market.

North America Alternating Current Drive Industry Leaders

ABB Ltd.

Danfoss A/S

Schneider Electric SE

Rockwell Automation, Inc.

Yaskawa Electric Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Schneider Electric confirmed a USD 700 million U.S. investment plan through 2027 to expand medium-voltage manufacturing and create more than 1,000 jobs.

- November 2024: ABB introduced the modular ACS8080 medium-voltage drive with integrated edge diagnostics for oil and gas, mining, and water clients.

- October 2024: ABB unveiled a speed-controlled medium-voltage motor-drive package that eliminates external cabling and reduces harmonics.

- June 2024: Eaton joined the EU Shift2DC consortium to pioneer medium- and low-voltage DC grids for industry and data centers.

North America Alternating Current Drive Market Report Scope

The North America alternating current (AC) drive market refers to the industry for electronic devices that control the speed and torque of electric motors by varying the motor’s input frequency and voltage. These drives improve energy efficiency, process control, and operational flexibility across a wide range of industrial and commercial applications. The market encompasses various voltage classes, power ratings, and end-user industries across the United States and Canada.

The North America Alternating Current Drive Market Report is Segmented by Voltage (Low, Medium), Power Rating (Micro, Low, Medium, High), Application (Pumps, Fans and Blowers, Compressors, Conveyors, HVAC Systems, Others), End-User Industry (Oil and Gas, Chemical and Petrochemical, Food and Beverages, Water and Wastewater, Power Generation, Metal and Mining, Pulp and Paper, HVAC, Discrete Industries), and Geography (United States, Canada). The Market Forecasts are Provided in Terms of Value (USD).

By Voltage

| Low |

| Medium |

By Power Rating

| Micro (<1 kW) |

| Low (1 – 100 kW) |

| Medium (101 – 500 kW) |

| High (>500 kW) |

By Application

| Pumps |

| Fans and Blowers |

| Compressors |

| Conveyors |

| HVAC Systems |

| Others |

By End-User Industry

| Oil and Gas |

| Chemical and Petrochemical |

| Food and Beverages |

| Water and Wastewater |

| Power Generation |

| Metal and Mining |

| Pulp and Paper |

| HVAC |

| Discrete Industries |

By Country

| United States |

| Canada |

| By Voltage | Low |

| Medium | |

| By Power Rating | Micro (<1 kW) |

| Low (1 – 100 kW) | |

| Medium (101 – 500 kW) | |

| High (>500 kW) | |

| By Application | Pumps |

| Fans and Blowers | |

| Compressors | |

| Conveyors | |

| HVAC Systems | |

| Others | |

| By End-User Industry | Oil and Gas |

| Chemical and Petrochemical | |

| Food and Beverages | |

| Water and Wastewater | |

| Power Generation | |

| Metal and Mining | |

| Pulp and Paper | |

| HVAC | |

| Discrete Industries | |

| By Country | United States |

| Canada |

Key Questions Answered in the Report

What is the 2025 value of the North America alternating current drive market?

The North America alternating current drive market size stands at USD 4.06 billion in 2025.

What is the 2025 value of the North America alternating current drive market?

The market is projected to expand at a 4.83% CAGR between 2025 and 2030.

Which voltage class is growing the quickest?

Medium-voltage drives are forecast to post the fastest 8.5% CAGR, outpacing low-voltage units.

Why are HVAC applications gaining traction?

Data-center cooling and stricter building-energy codes drive a 9.2% CAGR in HVAC-related drive demand.

Which country shows the highest growth rate?

Canada leads regional growth with a projected 7.9% CAGR, supported by clean-economy tax credits and EV battery investments.

Which industry is set to add the most incremental demand?

Water and wastewater utilities, fueled by USD 50 billion in federal infrastructure funding, are expected to grow at an 8.7% CAGR.

Page last updated on: