North America Alfalfa Hay Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2020 - 2023 |

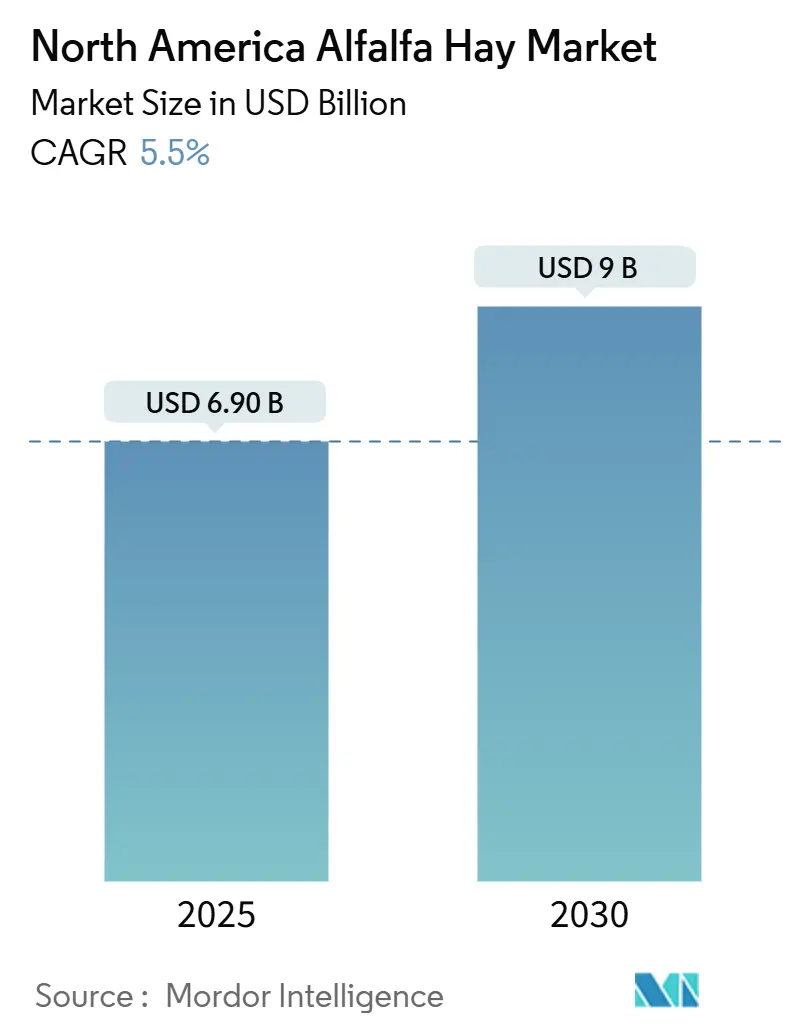

| Market Size (2025) | USD 6.90 Billion |

| Market Size (2030) | USD 9 Billion |

| Growth Rate (2025 - 2030) | 5.50% CAGR |

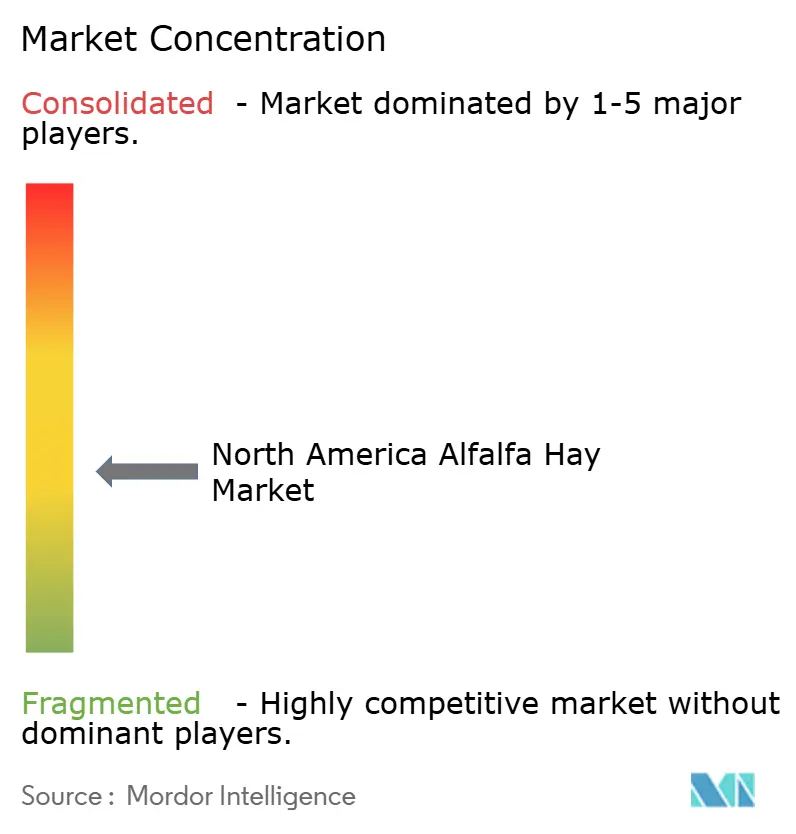

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Alfalfa Hay Market Analysis by Mordor Intelligence

The North America alfalfa hay market size is valued at USD 6.9 billion in 2025 and is projected to reach USD 9.0 billion by 2030, reflecting a 5.5% CAGR across the forecast window. Consistent demand for high-protein forage, sustained component-based milk premiums, and widening organic and non-genetically modified organism channels continue to anchor consumption. Exporters benefit from stable West Coast container flows into Asia, while regional feedlots and equine owners step in when freight volatility diverts loads toward domestic buyers. Emerging drought-tolerant cultivars and precision irrigation upgrades are raising yields per acre, partially offsetting acreage pressure in water-restricted basins. Meanwhile, poultry integrators are blending alfalfa meal into layer and broiler diets to meet pigmentation and fiber targets, quietly expanding the end-use base of the North America alfalfa hay market[1]Source: U.S. Department of Agriculture, “Quick Stats Database,” USDA.gov.

Key Report Takeaways

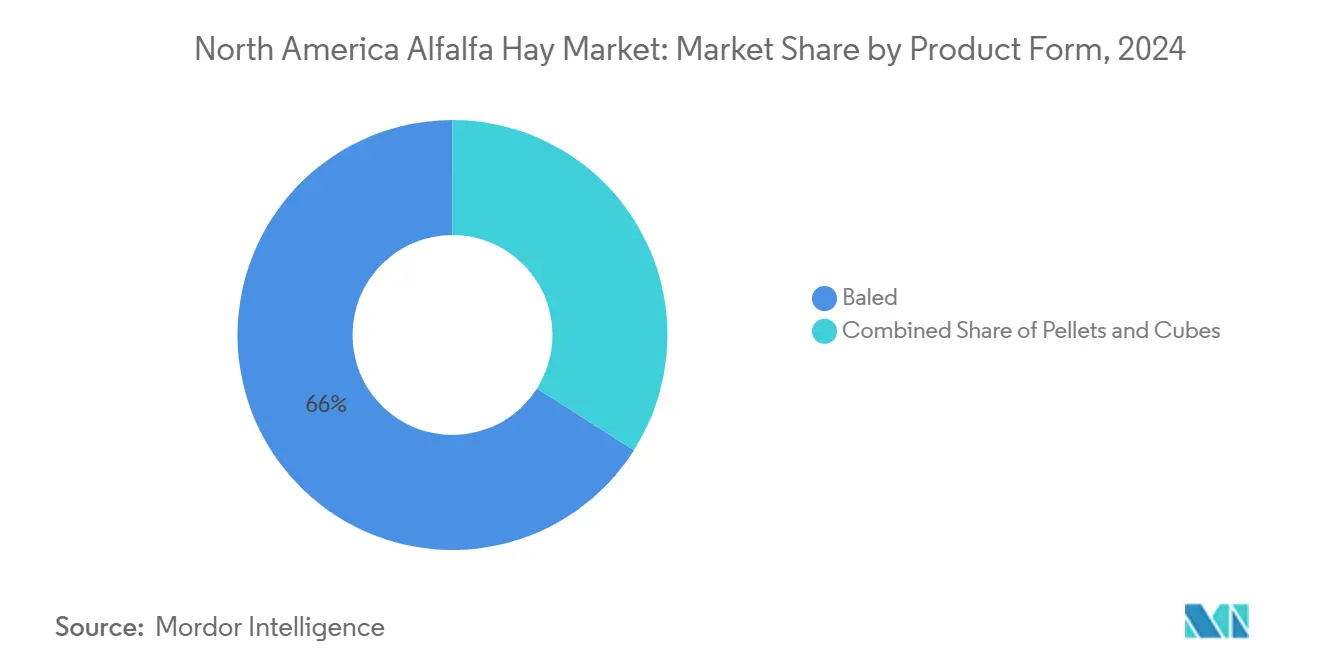

- By product form, baled alfalfa held 66.0% of the North America alfalfa hay market share in 2024, while pellets are on track for an 8.5% CAGR through 2030.

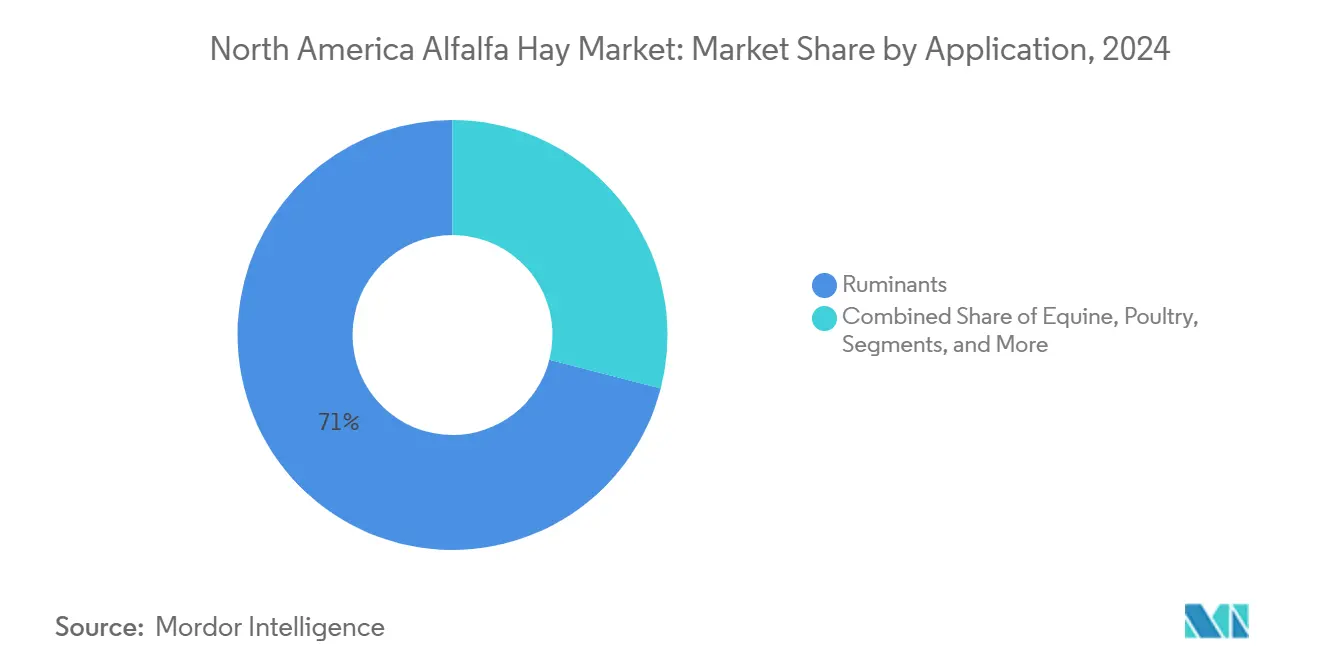

- By application, ruminants accounted for 71.0% of the North America alfalfa hay market size in 2024, whereas poultry demand is growing at a 9.2% CAGR to 2030.

- By geography, the United States accounted for an 85.0% share of the market size in 2024, and Canada is projected to register a 6.9% CAGR until 2030.

North America Alfalfa Hay Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for high-protein dairy rations | +1.2% | United States (California, Wisconsin, New York), Canada (Ontario, Quebec) | Medium term (2-4 years) |

| Growth of organic and non-GMO livestock feed programs | +0.8% | United States (Pacific Northwest, Upper Midwest), Canada (British Columbia, Alberta) | Long term (≥ 4 years) |

| Increasing alfalfa exports to Asia via West Coast ports | +1.0% | United States (Washington, Oregon, California), Canada (British Columbia) | Short term (≤ 2 years) |

| Commercialization of drought-tolerant alfalfa cultivars | +0.7% | United States (Southwest, Great Plains), Mexico (Northern states) | Long term (≥ 4 years) |

| Carbon-credit premiums for legume crop rotations | +0.4% | United States (Midwest corn belt), Canada (Prairie provinces) | Long term (≥ 4 years) |

| Robotics enabling cost-efficient large-scale baling | +0.3% | United States (Western states), Canada (Prairie provinces) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for High–Protein Dairy Rations

United States dairy cooperatives in California, Wisconsin, and New York are rewarding butterfat above 4.0% and protein above 3.3%, targets that push ration formulators to lift alfalfa inclusion to 30-40% of forage dry matter intake. March 2024 alfalfa prices averaged USD 195 per metric ton, with premium grades reaching USD 271, yet eased to USD 172 by September 2024 as favorable pasture conditions moderated substitution pressure. Each 1-point gain in neutral detergent fiber digestibility trims supplemental concentrate costs by USD 0.08 per cow per day, a saving that compounds across 300-cow herds. Herd productivity climbed 1.2% in 2024 even as inventory held near 9.4 million head, keeping forage volumes buoyant. Together, these economic factors underpin a structural pull on the North American alfalfa hay market.

Growth of Organic and Non-GMO Livestock Feed Programs

Organic livestock feed sales surpassed USD 1.8 billion in 2024, and alfalfa remains the cornerstone forage because National Organic Program standards require certified forage input. Prices command 15-25% premiums above conventional hay, offsetting the cost of three-year land transitions. Non-genetically modified organism (NGMO) verification is gaining traction in poultry supply chains that value alfalfa meal for its natural yolk pigmentation. Canadian certified acreage increased by 8% in 2024, primarily in Saskatchewan and Alberta, which helped exporters secure Japanese contracts that require non-genetically modified organism status. Compliance audits and chain-of-custody testing add USD 3-5 per metric ton in overhead, but channel premiums justify the expenditure, reinforcing organic momentum within the North American alfalfa hay market.

Commercialization of Drought-Tolerant Alfalfa Cultivars

Reduced-lignin varieties, such as HarvXtra, now cover approximately 300,000 acres in the United States, allowing growers to extend cutting intervals and harvest an additional 0.3-0.5 metric tons per acre per season [2]Source: Forage Genetics International, “HarvXtra Reduced-Lignin Alfalfa,” foragegenetics.com. Seed premiums of USD 8-12 per pound require multiyear paybacks, yet added yield and digestibility gains have proven persuasive, especially in regions subject to erratic precipitation. In the Colorado River basin, incremental yield helps offset acreage caps tied to water allocations. Further north, South Dakota and Idaho growers report more-flexible harvest windows that lower weather risk. The ongoing diffusion of these cultivars provides a modest but durable lift to the North America alfalfa hay market.

Carbon-Credit Premiums for Legume Crop Rotations

Alfalfa fixes 150-250 pounds of atmospheric nitrogen per acre each year, positioning it as a potential soil-carbon offset, as voluntary credit markets mature. Although Alberta’s Conservation Cropping Protocol expired in 2024 amid thin uptake, United States pilots run by Indigo Ag and Nori are crediting reduced synthetic nitrogen and higher soil organic carbon on rotational acres. Present carbon prices around CAD 8.50 (USD 6.43) per metric ton barely cover verification costs, but policy momentum from the California Air Resources Board keeps grower interest alive. Verified protocols could eventually reward producers with new premiums, adding an option value to planting decisions within the North America alfalfa hay industry.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Water-use restrictions in United States Southwest | -1.5% | United States (California, Arizona, Nevada), Mexico (Sonora, Baja California) | Short term (≤ 2 years) |

| Volatility in ocean-freight container rates | -0.9% | Global, with acute impact on United States West Coast export corridors | Short term (≤ 2 years) |

| Rising competition from fermented total-mixed rations | -0.5% | United States (dairy-intensive regions), Canada (Ontario, Quebec) | Medium term (2-4 years) |

| Increasing incidence of blister-beetle contamination | -0.3% | United States (Great Plains, Southeast), Mexico (Northern states) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Water-Use Restrictions in United States Southwest

Mandatory 2025 Colorado River reductions of 1.033 million acre-feet are concentrated in Arizona, Nevada, and California, curbing irrigation in Imperial Valley and Yuma, where alfalfa accounts for 32% of basin water and 62% of agricultural diversions[3]Source: Bureau of Reclamation, “Colorado River Basin Shortage Projections,” usbr.gov. The Metropolitan Water District, fallowing contracts paying USD 300 per acre-foot, has already idled 46,955 acres in Palo Verde, eliminating roughly 250,000 metric tons of forage. California's Sustainable Groundwater Management Act deadlines are tightening further, likely removing another 500,000-750,000 irrigated acres statewide by 2040. These shifts shrink regional output, elevate prices, and cap the near-term ceiling for the North America alfalfa hay market.

Rising Competition from Fermented Total-Mixed Rations

Fermented total-mixed rations improve feed efficiency by 3-5%, allowing dairies to reduce alfalfa inclusion from 35-40% to 25-30% of forage dry matter without compromising milk components. Systems cost USD 150,000-USD 500,000 but deliver paybacks in 3-5 years by reducing feed waste and mitigating acidosis incidents. Wisconsin and New York trials showed feed costs per cow dropping USD 0.30-0.50 per day while maintaining yields. If adoption spreads, as much as 750,000 metric tons of annual demand could be displaced by 2030, dampening growth prospects for the North American alfalfa hay market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Form: Baled Dominance Anchors Flexibility

Baled hay commanded 66% of the 2024 North America alfalfa hay market share, reflecting rancher preference for adaptable feeding and minimal processing equipment. Small squares earn USD 100 per metric ton premiums but represent under 10% of volume because labor costs run USD 3-5 per bale. Large squares dominate export channels, especially when compressed to 50-55 pounds per cubic foot for 40-foot containers. Round bales appeal to cow-calf operations by cutting labor 30% per metric ton despite higher weathering losses.

Pellets, projected to expand at an 8.5% CAGR, benefit from transportation savings that offset dehydration costs of USD 60-90 per metric ton. Green Prairie International’s Saskatchewan plant funnels pellets to Japanese dairies that value uniform nutrient profiles, while Western Alfalfa Milling and Standlee Premium Western Forage target retail cubes for equine and zoo clients. As these processed formats grow, the North America alfalfa hay market size for pellets and cubes is projected to capture a higher share of the revenue through 2030[4]Source: Green Prairie International, “Products and Specifications,” greenprairie.com.

By Application: Ruminants Remain Largest, While Poultry Drives Growth

Ruminants absorbed 71.0% of the 2024 North America alfalfa hay market size, anchored by California dairies that feed 35-40% alfalfa to sustain 85-pound daily yields and component premiums of USD 0.15-0.25 per hundredweight. Feedlot operators in Kansas and Nebraska include 5-8 pounds per head per day to buffer rumen health and reduce acidosis. Beef cow-calf herds switch to lower-grade alfalfa during late gestation, provided prices stay within 10% of grass hay.

Poultry applications show the fastest growth, advancing at a 9.2% CAGR through 2030, as integrators replace synthetic methionine and pigments with 2-4% alfalfa meal to enhance yolk color and fiber. Roche scale targets of 12-14 are achieved without additives, aligning with non-genetically modified organism and antibiotic-free labels. These shifts signal additional upside for the North America alfalfa hay market size in non-ruminant channels.

Geography Analysis

By geography, the United States accounted for an 85.0% share of the market size in 2024, and Canada is projected to register a 6.9% CAGR until 2030. Colorado River constraints are limiting the acreage in the Imperial Valley, yet Columbia Basin pivot irrigation continues to produce premium forage that Japanese buyers prize for its color and leaf retention. Anderson Hay and Grain Company’s Ellensburg hub alone holds 50,000 metric tons of covered storage and tops 7,300 export records, highlighting the scale advantage wielded by integrated shippers.

Canada's exports of dehydrated pellets from Saskatchewan and Alberta to Japan have decreased by 15% due to drought pressure, which has raised local prices to CAD 0.16 (USD 0.12) per pound. United States Department of Agriculture reporting shows that 66.0% of the country is in an abnormal drought as of March 2024, which is tightening forage supplies and nudging cross-border trade southward. Even so, Green Prairie International continues to serve Ontario and Quebec dairies that value dust-free pellets, underpinning a niche yet stable Canadian contribution to the North America alfalfa hay market.

Mexico imported roughly 150,000-200,000 metric tons of United States hay in 2024 to feed Chihuahua and Durango dairies. Screwworm detections slashed cross-border cattle flows by two-thirds in early 2025, resulting in reduced demand for feedlots. Trucking from Imperial Valley costs USD 0.12-0.18 per mile, adding USD 60-90 per load, and border delays increase the risk, limiting growth. Beyond the main triad, Caribbean and Central American markets remain small but could offer incremental upside as local dairy and equine industries professionalize.

Competitive Landscape

The North America alfalfa hay market is moderately fragmented, with the top five players, including Anderson Hay and Grain Company, Al Dahra ACX, Green Prairie International, Border Valley Trading, and Standlee Premium Western Forage, controlling a substantial portion of revenue. Al Dahra ACX owns 30,000 acres across the Western United States and Central Mexico and operates ten pressing plants worldwide, dispatching 94.7% of its USD 309.63 million shipment value under alfalfa’s Harmonized System code between 2021 and 2024. Anderson Hay’s large covered storage and long-term grower contracts support consistent Asian grade specifications, reinforcing customer loyalty.

Mid-tier players, such as Hay USA, Western Alfalfa Milling, and Oxbow Animal Health, differentiate themselves through proximity to Mexico, specialized cubing lines, and direct-to-consumer e-commerce, respectively. Certification-driven white space remains attractive, with organic and non-genetically modified organism (NGMO) hay commanding 15-25% premiums, but it requires strict documentation and three-year land transition periods.

Technology adoption is accelerating among larger growers who deploy soil-moisture sensors and variable-rate irrigation to reduce water usage by 0.5-0.8 acre-feet per acre. These investments, coupled with scale economies in compression and containerization, favor integrated operators as water regulations tighten, reshaping the competitive dynamics within the North American alfalfa hay industry.

North America Alfalfa Hay Industry Leaders

Anderson Hay and Grain Co.

Al Dahra ACX

Green Prairie International

Border Valley Trading

Standlee Premium Western Forage

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: The University of Minnesota Extension reported that 2025 blister-beetle populations were 30 percent above 10-year averages, attributed to consecutive mild winters that improved overwintering survival. This suggests that contamination risk will persist in alfalfa hay through the forecast period, absent significant climate shifts.

- October 2024: The Bureau of Reclamation announced mandatory Colorado River Lower Basin water reductions of 1.033 million acre-feet, effective 2025. Arizona, Nevada, and California will absorb cuts based on priority rights, impacting alfalfa acreage in the Imperial Valley and Yuma, where the crop uses 32% of the basin's water and 62% of agricultural diversions. The policy is anticipated to idle 50,000 to 75,000 acres of alfalfa over two years, thereby tightening the supply and supporting prices.

- October 2024: The United States Department of Agriculture's National Agricultural Statistics Service reported that national alfalfa prices in March 2024 averaged USD 195 per metric ton, with premium grades commanding USD 271 per metric ton. Though prices retreated to USD 172 per metric ton by September 2024, as improved pasture conditions and elevated corn silage inventories eased substitution pressure.

North America Alfalfa Hay Market Report Scope

The North America Alfalfa Hay Market Report is Segmented by Product Form (Baled, Pellets, and Cubes), Application (Ruminants, Equine, Poultry, and Others), and Geography (United States, Canada, Mexico, and Rest of North America). The Market Forecasts are Provided in Terms of Value (USD).

| Baled |

| Pellets |

| Cubes |

| Ruminants |

| Equine |

| Poultry |

| Others |

| United States |

| Canada |

| Mexico |

| Rest of North America |

| By Product Form | Baled |

| Pellets | |

| Cubes | |

| By Application | Ruminants |

| Equine | |

| Poultry | |

| Others | |

| By Geography | United States |

| Canada | |

| Mexico | |

| Rest of North America |

Key Questions Answered in the Report

How large is the North America alfalfa hay market in 2025?

The market stands at USD 6.9 billion in 2025 and is forecast to reach USD 9.0 billion by 2030.

What is the expected CAGR for alfalfa hay sales across North America?

Sales are projected to expand at a 5.5% CAGR between 2025 and 2030.

Which product form holds the largest share of regional revenue?

Baled hay led with 66.0% share in 2024.

Which end-use segment is growing the fastest?

Poultry feed applications are expanding at a 9.2% CAGR through 2030.

How are water restrictions affecting Southwest alfalfa acreage?

Mandatory Colorado River cuts and fallowing incentives have already removed over 46,000 acres in California’s Palo Verde region, with more reductions expected.

What companies dominate the market?

Anderson Hay and Grain Company, Al Dahra ACX, Green Prairie International, Border Valley Trading, and Standlee Premium Western Forage collectively control substantial portion of the revenue.

Page last updated on: