North America AI Copilot Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

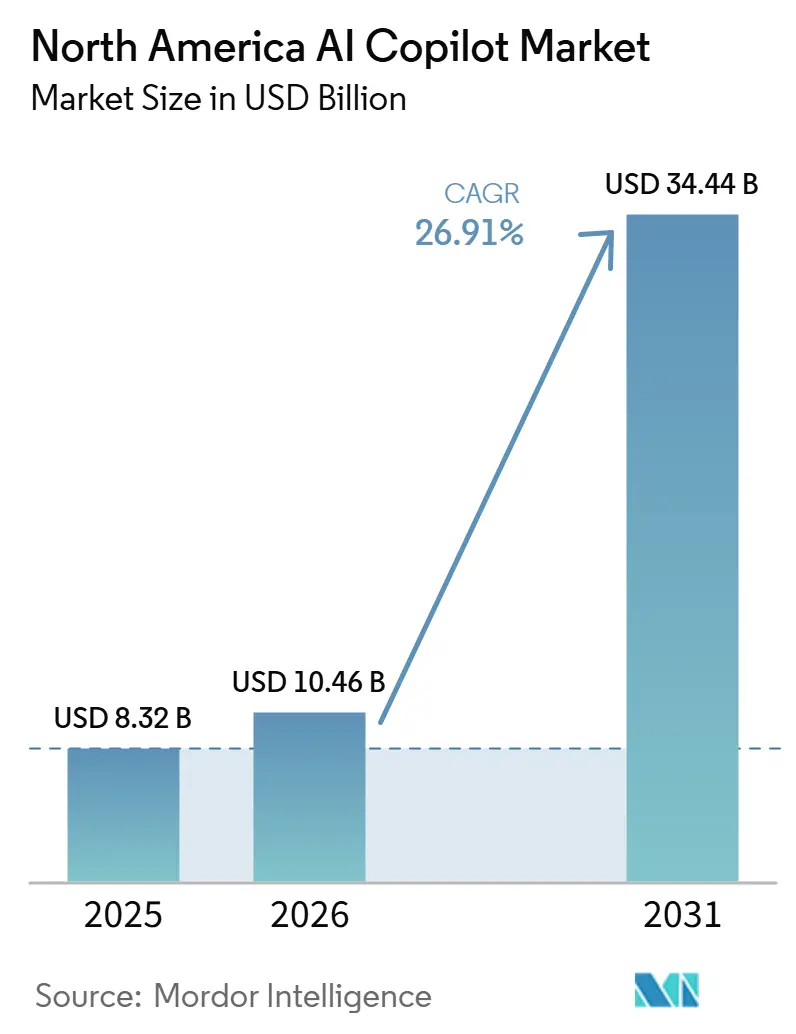

| Base Year Market Size (2025) | USD 8.32 Billion |

| Market Size (2026) | USD 10.46 Billion |

| Market Size (2031) | USD 34.44 Billion |

| Growth Rate (2026 - 2031) | 26.91% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America AI Copilot Market Analysis by Mordor Intelligence

The North America AI copilot market size is projected to expand from USD 8.32 billion in 2025 and USD 10.46 billion in 2026 to USD 34.44 billion by 2031, registering a CAGR of 26.91% between 2026 and 2031. The North America AI copilot market is growing as enterprises across the region move from pilots to wider workflow deployment in daily business functions. Demand is supported by productivity needs, mature cloud infrastructure, and the spread of platform-native copilots that integrate with the software stacks companies already use. Competition is shifting away from a single-model race toward platform depth, governance controls, and the quality of enterprise data that grounds output reliability. The North America AI copilot market is also benefiting from stronger returns at firms that had already improved data hygiene in systems such as SharePoint, Salesforce, and ServiceNow before large-scale copilot rollouts. Security and compliance expectations are reinforcing this adoption path, as regulated buyers increasingly seek auditable AI tools that align with existing procurement and governance standards.

Key Report Takeaways

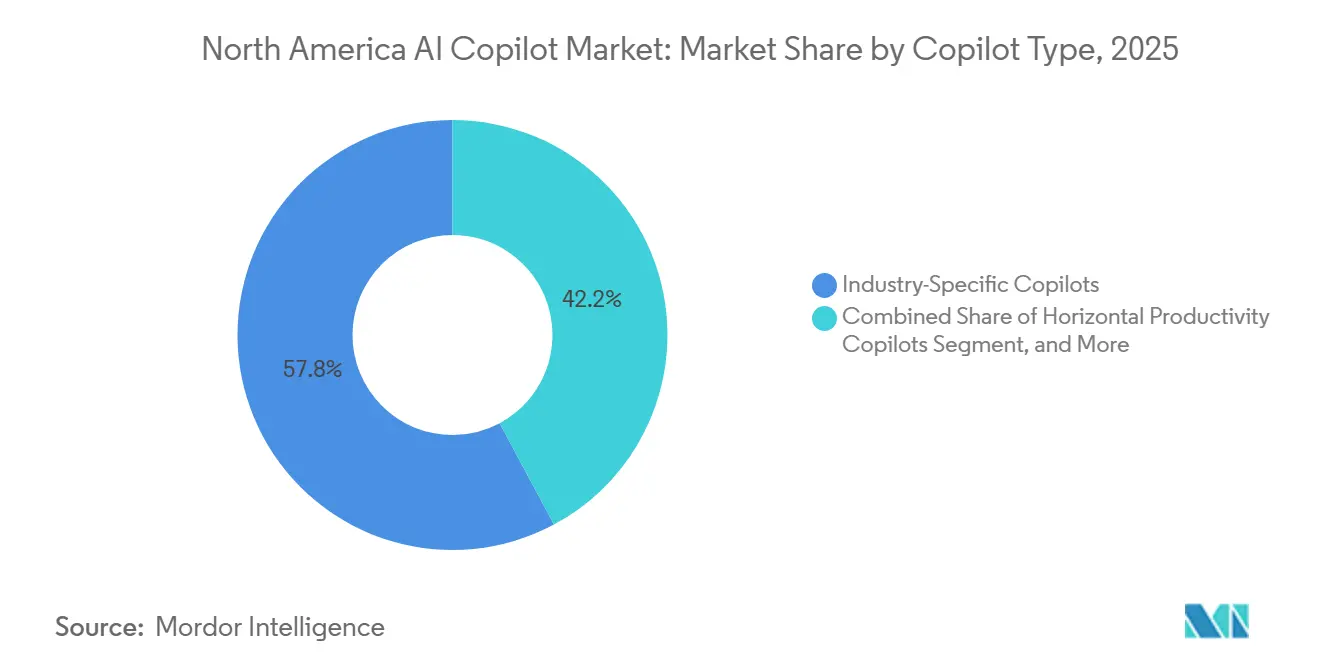

- By copilot type, Horizontal Productivity Copilots led with 42.18% share in 2025, while Industry-Specific Copilots are projected to expand at a 29.24% CAGR through 2031 in the North America AI copilot market.

- By deployment, cloud-based models accounted for 75.41% of the North America AI copilot market size in 2025, while hybrid deployment is projected to record the highest CAGR at 28.83% through 2031.

- By organization size, large enterprises held 70.62% share in 2025, while small and medium enterprises are projected to grow at a 29.41% CAGR through 2031.

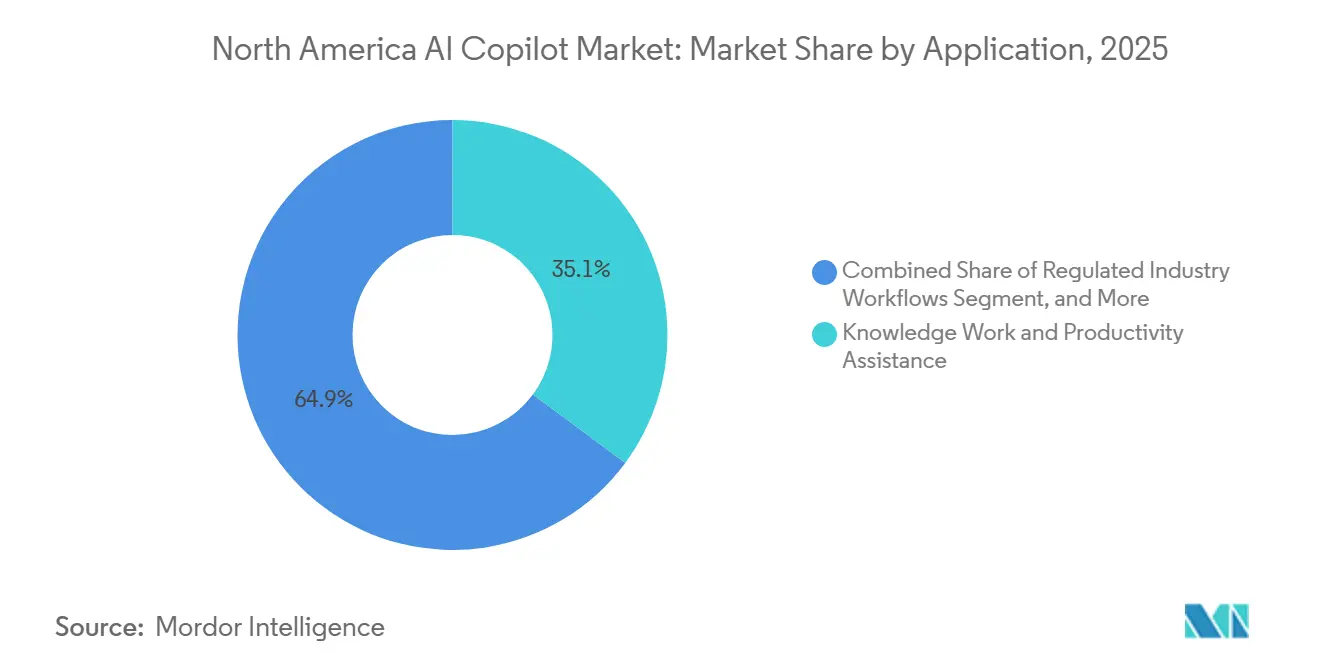

- By application, knowledge work and productivity assistance captured 35.14% of the market in 2025, while regulated industry workflows are projected to grow at a 28.76% CAGR through 2031.

- By end-user industry, IT and telecommunication accounted for 25.36% share in 2025, while government and administration are projected to expand at a 29.82% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America AI Copilot Market Trends and Insights

Drivers Impact Analysis*

| river | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Enterprise Productivity Gains from Copilot Workflows | +5.5% | Global, concentrated in North America | Medium term (2-4 years) |

| Microsoft 365 Distribution Reach Across Knowledge Work | +5.0% | United States dominant, Canada secondary | Short term (≤ 2 years) |

| Demand For Code, Content, and Knowledge Automation In Regulated Enterprises | +4.5% | North America and EU | Medium term (2-4 years) |

| Secure Enterprise AI Stack Expansion on North America Cloud Infrastructure | +4.0% | North America | Medium term (2-4 years) |

| Faster Internal Adoption Through Low-Friction SaaS Procurement | +3.5% | North America and Western Europe | Short term (≤ 2 years) |

| Vendor Consolidation Around Native Copilot Bundles | +3.0% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Enterprise Productivity Gains From Copilot Workflows

Enterprise productivity gains from copilot-led workflows are a central demand driver for the North America AI copilot market. OpenAI reported in December 2025 that 75% of surveyed workers saw better speed or output quality, while enterprise users linked AI support to 40 to 60 minutes saved in an active workday, and data scientists and engineers reported up to 80 minutes saved daily.[1]OpenAI Staff, “The State of Enterprise AI 2025 Report,” OpenAI, openai.com Those time savings matter most in communications-heavy roles where drafting, summarizing, reviewing, and searching take a large share of the workday. Companies are also seeing value in faster onboarding because employees can use copilots to surface internal knowledge without waiting for manual support from senior staff. That effect reduces training friction in complex operating environments and helps teams reach stable output sooner after hiring. It also explains why finance leaders are paying closer attention to copilots as labor-efficiency tools rather than as isolated software experiments.

Microsoft 365 Distribution Reach Across Knowledge Work

Microsoft's distribution advantage across everyday knowledge work continues to shape the North America AI copilot market. The company's commercial Microsoft 365 base gives it a direct path into organizations that already rely on Word, Excel, Outlook, Teams, and related data layers for daily work. Microsoft News reported in June 2026 that Infosys, TCS, and Wipro scaled Microsoft 365 Copilot to more than 300,000 employees in under 6 months, which showed how quickly large organizations can move once deployment barriers are low.[2]Microsoft Security Team, “New Tools and Guidance, Announcing Zero Trust for AI,” Microsoft Security Blog, microsoft.com The strategic advantage comes from selling into existing tenancy, not from convincing enterprises to adopt a separate greenfield tool with new habits and new controls. This shortens evaluation cycles and increases switching costs because enterprise data already resides in Microsoft-connected systems. As more workflows are grounded in that internal data, competing productivity copilots have a narrower opening even when output quality appears strong in isolated tests.

Demand For Code, Content, and Knowledge Automation in Regulated Enterprises

Demand from regulated enterprises is expanding the North America AI copilot market, as compliance-heavy work creates a clear need for faster, more auditable process support. FINRA dedicated a section to generative AI in its 2026 Annual Regulatory Oversight Report, published in December 2025, and called out hallucinations and bias as risks that firms must test and monitor over time.[3]FINRA Staff, “2026 FINRA Annual Regulatory Oversight Report,” Financial Industry Regulatory Authority, finra.org That regulatory attention is not only a warning signal, it also gives internal sponsors a stronger case for enterprise-grade copilots that offer traceability and formal controls. Companies in healthcare and life sciences have been making similar moves, treating AI as a support tool for regulated documentation and workflow discipline. This changes the buyer conversation from simple productivity gains to process quality, audit readiness, and policy compliance. It also raises the value of vendors that can package automation with governance rather than offering general-purpose AI alone.

Secure Enterprise AI Stack Expansion on North America Cloud Infrastructure

The secure enterprise AI stack that sits on North America's cloud infrastructure is another strong support for the North America AI copilot market. Microsoft announced its Zero Trust for AI framework in March 2026, extending Zero Trust principles across data ingestion, model training, deployment, and agent behavior, with a dedicated assessment pillar planned for summer 2026. This matters because enterprise buyers do not only want model access; they want policy controls that align with existing cybersecurity programs. Domestic infrastructure capacity also helps because sensitive workloads can stay closer to the user and within preferred legal and governance boundaries. That is especially important in financial services, healthcare, government, and critical infrastructure settings where cross-border movement of sensitive data can slow or block adoption. As a result, infrastructure depth and security architecture are becoming part of the product decision, not just background technical conditions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Enterprise Data Residency and Prompt Leakage Concerns | -1.8% | Global | Medium term (2-4 years) |

| Hallucination Risk In High-Stakes Business Workflows | -1.5% | Global | Short term (≤ 2 years) |

| Copilot License Stacking And Budget Scrutiny | -1.2% | North America | Short term (≤ 2 years) |

| Fragmented Integration Across Legacy Applications and Data Silos | -1.0% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Enterprise Data Residency and Prompt Leakage Concerns

Enterprise data residency and prompt leakage concerns remain significant constraints on adoption at scale. Buyers in legal, financial, healthcare, and public sector settings often need proof that sensitive prompts, records, and derived outputs remain under acceptable control. Those requirements become harder when multiple cloud services, third-party models, and internal repositories are involved in a single workflow. The mitigation path involves dedicated environments, zero-retention terms, stronger data loss prevention, and closer policy enforcement, but these steps usually add review time and cost. Mid-sized organizations bear this burden most, as they often seek the same protections as large enterprises but lack the same procurement capacity. This keeps rollout cycles longer than the excitement around copilots might suggest, even when the business case looks strong.

Hallucination Risk in High-Stakes Business Workflows

The risk of hallucination in high-stakes business workflows also limits how quickly copilots can move into record-based decisions and compliance-sensitive tasks. NIST's Generative Artificial Intelligence Profile, released in July 2024 as NIST AI 600-1, classified confabulation as 1 of 12 primary generative AI risk categories and outlined testing expectations before deployment. In practical terms, a fabricated citation, unsupported number, or incorrect legal statement can create downstream audit, client, or regulatory problems that are expensive to fix later. FINRA's December 2025 report reinforced this concern by placing AI accuracy and monitoring within a firm's supervisory obligations. That means productivity gains do not remove the need for human checks in sensitive workflows, and those review layers reduce some of the speed advantage. Until reliability controls become easier to standardize, many organizations will expand copilots in phases rather than opening access across every business process at once.[4]National Institute of Standards and Technology, “Artificial Intelligence Risk Management Framework, Generative Artificial Intelligence Profile (NIST AI 600-1),” NIST, nist.gov

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Copilot Type: Horizontal Copilots Lead, Vertical Intelligence Accelerates

Horizontal Productivity Copilots accounted for 42.18% of the North America AI copilot market in 2025. Their lead came from broad use across email handling, document drafting, meeting summaries, spreadsheet work, and everyday search tasks inside common productivity suites. Many enterprises already had the necessary licenses, identity controls, and data structures in place before Copilot activation, reducing friction at deployment time. Functional Workflow Copilots are also gaining ground because platforms in HR, finance, and sales are becoming better at embedding AI into process-specific tasks rather than simple chat assistance. Technical and Engineering Copilots serve a narrower user base, but they remain important because output quality is easier to judge in code, testing, and incident response environments.

Industry-Specific Copilots are projected to grow at a 29.24% CAGR from 2026 to 2031. That pace reflects the fact that domain-adapted tools can show clearer returns in regulated or specialized environments than broad productivity copilots usually can. Healthcare documentation, legal research support, and financial analysis grounded in proprietary data each create a strong case for premium pricing and lower churn. SAP announced in May 2026 that Anthropic's Claude would serve as the primary agentic reasoning layer within the SAP Business AI Platform and support Joule agents across SAP's enterprise base. This move showed how large software vendors are turning general-purpose models into business-specific interfaces tied to enterprise systems. In the North America AI copilot market, vendors that combine strong models with proprietary vertical data are likely to hold the most defensible positions as adoption deepens.

By Deployment: Cloud Leads, Hybrid Meets Sovereignty Demands

Cloud-based deployment accounted for 75.41% of the North America AI copilot market size in 2025. This lead reflected the dominance of SaaS delivery via Microsoft 365, Salesforce, Google Workspace, and related enterprise software. Cloud delivery helped vendors release features faster, update models without local upgrades, and lower the infrastructure burden placed on customers. On-premises deployment still mattered in defense, intelligence, and critical infrastructure settings where air-gapped or tightly isolated environments remained essential. GitHub introduced enterprise-managed settings for AI governance in June 2026, giving organizations a way to enforce standards centrally across Copilot clients and narrowing a part of the governance gap between cloud and local deployments.

Hybrid deployment is projected to expand at a 28.83% CAGR through 2031. Its growth is being driven by enterprises that need both cloud innovation speed and stronger control over highly sensitive workloads. Financial services, healthcare, and government buyers often cannot route every prompt and every document through public endpoints without raising compliance questions. Hybrid architectures give them a path to keep selected workloads in private environments while still using public cloud capacity for lower-risk tasks. AWS highlighted this pattern in April 2026 through its discussion of distributed agentic AI workloads across hybrid cloud services and localized infrastructure. This split model adds orchestration complexity, but it better aligns with the operational realities of large enterprises than a purely cloud-only or purely on-premises approach.

By Organization Size: Enterprises Dominate, SME Adoption Accelerates

Large enterprises held 70.62% of the North America AI copilot market in 2025. They moved first because they already had larger cloud budgets, enterprise software contracts, internal security teams, and the governance structure needed for controlled rollout. Many of these organizations tested copilots during 2023 and 2024, then expanded more broadly during 2025 after they had clearer operating rules and stronger internal support. That early lead still matters because it lets them refine access controls, training programs, and workflow redesign before smaller peers catch up. It also creates a compounding effect where better data hygiene and stronger AI fluency improve the value of each additional deployment.

Small and medium enterprises are projected to grow at a 29.41% CAGR from 2026 to 2031. Microsoft launched Microsoft 365 Copilot Business in December 2025 at USD 21 per user per month, lowering the entry barrier for smaller buyers who wanted bundled enterprise-grade AI within familiar tools. The OECD reported in December 2025 that AI adoption among smaller firms was still lagging that of large enterprises, but was rising quickly as tools became easier to access and seat costs declined. Intuit's February 2026 partnership with Anthropic also widened access to AI agents for mid-market businesses through QuickBooks and related platforms. The result is that smaller firms are entering the North America AI copilot industry through simpler bundled products rather than through custom AI projects.

By Application: Knowledge Work Leads, Regulated Workflows Gain Ground

Knowledge Work and Productivity Assistance held 35.14% of the North America AI copilot market in 2025. This segment remained the largest because it covers the broadest set of tasks, including drafting, summarizing, communication support, note capture, and research synthesis. The installed base of productivity software seats gave this use case an immediate audience and made time savings easier to observe in daily work. Software engineering, customer and employee service, sales and marketing, and business process operations formed the next layer of demand because their workflows already had measurable outputs and digital records. The North America AI copilot market share held by knowledge work also reflected how quickly enterprises could deploy support tools in communication-heavy roles compared with more tightly controlled operational settings.

Regulated Industry Workflows are projected to grow at a 28.76% CAGR through 2031. These workflows include compliance documentation, regulatory reporting, audit support, and clinical decision support, where process discipline matters as much as speed. Salesforce said in February 2026 that more than 180 organizations selected Agentforce IT Service within 4 months of general availability, which showed that structured workflow automation can scale quickly when the business case is clear. Enterprises are increasingly treating AI in regulated operations as a way to improve consistency and control when human oversight remains in place. That positioning supports a higher willingness to pay because the value is tied to both risk management and efficiency. It also encourages longer vendor relationships once copilots become part of recurring audit and reporting routines.

By End-User Industry: IT Leads, Government Adoption Accelerates

IT and telecommunication accounted for 25.36% of the North America AI copilot market in 2025. The sector led because it has the highest concentration of developers, DevOps teams, network operations staff, and digital service groups that can use copilots in daily execution. These buyers also tend to have stronger internal comfort with software experimentation and faster feedback loops for measuring utility. BFSI remained the second-largest end-user segment because compliance reporting, customer service, and document-heavy processes give it a clear case for AI support under formal controls. Healthcare and life sciences, retail and e-commerce, industrial manufacturing, education and research institutions, media and entertainment, and energy and utilities also continued building domain-specific use cases across the region.

Government and administration are projected to expand at a 29.82% CAGR from 2026 to 2031. The Office of Management and Budget's 2025 Federal Agency AI Use Case Inventory covered 3,611 AI use cases across 56 agencies, which showed that federal adoption had moved well beyond isolated pilots. FedScoop reported in 2026 that more than 75% of CFO Act agencies deployed at least 1 major AI chatbot to at least 10,000 employees in 2025. Microsoft's September 2025 OneGov agreement with the U.S. General Services Administration then widened access to Microsoft 365 Copilot for federal users and reinforced procurement momentum into 2026. In the North America AI copilot market, public sector scale is now becoming a demand anchor rather than a niche opportunity.

Geography Analysis

The United States accounted for 88.42% of the North America AI copilot market share in 2025. Its lead came from the region's largest installed base of enterprise software, the highest density of AI-native vendors, and broad access to large business customers that can scale deployment once returns are proven. The White House published its National Policy Framework for Artificial Intelligence in March 2026 and signaled a sector-led regulatory approach, which reduced some uncertainty for enterprise buyers compared with a wholly new overarching governance system. Federal demand also supported scale because the OneGov agreement extended copilot access across large parts of government through September 2026. The United States is likely to remain the clear anchor of the North America AI copilot market through 2031, even as growth broadens elsewhere in the region.

Canada remained the second-largest geography within the North America AI copilot market in 2025. Its position is supported by a strong enterprise technology base and by a pan-Canadian policy environment that keeps attention on AI infrastructure and sector adoption. Canadian deployment conditions continue to favor vendors that can support stronger data residency, transparency, and auditability requirements for cross-border information handling. Financial services and healthcare are especially important because provincial privacy expectations make configurable governance features a practical buying requirement rather than an optional add-on.

Mexico is projected to grow at a 30.14% CAGR from 2026 to 2031, making it the fastest-expanding geography in the region. Nearshoring has increased the relevance of engineering copilots and industrial workflow automation as North American supply chains shift more activity into Mexico. A wider digital economy and a larger mid-market business base in cities such as Monterrey, Guadalajara, and Mexico City are also supporting growth. The strongest upside will likely go to vendors that invest early in Spanish-language and bilingual workflow support as adoption moves beyond subsidiaries of U.S.-headquartered firms.

Competitive Landscape

The North America AI copilot market has a dual-tier structure with a concentrated platform layer and a broader specialist layer. Microsoft, Google, and Salesforce anchor the platform side because they bundle Copilot capabilities into software environments that enterprises already use for communication, CRM, collaboration, and workflow management. This gives them a strong commercial advantage because buyers can evaluate AI within existing contracts, identities, and data systems rather than opening a separate procurement path. The specialist layer is wider and includes companies focused on code support, enterprise search, vertical deployment, and custom model services. As a result, the North America AI copilot market is concentrated at the top of the stack, but still open enough for specialists who solve narrow problems well.

Microsoft's advantage is rooted in its distribution, deep governance, and the value of its surrounding data layer. Google responded in April 2026 by launching the Gemini Enterprise Agent Platform and backing it with a USD 750 million partner fund, which shifted the competitive discussion toward ecosystem breadth and partner-created agents. Salesforce has taken a process-native approach with Agentforce, while ServiceNow has focused on AI governance and workflow control across IT and business operations. These moves show that leading vendors are competing through integration and control planes, not through model branding alone. They also show why enterprises increasingly compare copilots on fit with systems of record, governance, and workflow depth rather than on generic chat performance.

White space remains strongest in regulated vertical copilots, multi-agent oversight, and simplified SME offerings with solid governance. Smaller companies such as Glean, Cohere, and Sourcegraph are using that space to target buyers who want enterprise AI benefits without relying on multi-tenant public cloud architectures. SAP's May 2026 Anthropic integration strengthened its position by embedding stronger reasoning inside the SAP Business AI Platform for ERP-linked use cases. Microsoft also widened its platform reach in June 2026 when Copilot Cowork reached general availability with integrations across Dynamics 365, Microsoft Fabric, and third-party enterprise plugins. In this environment, governance credibility, integration depth, and access to proprietary enterprise data are becoming harder to separate from product value itself.

North America AI Copilot Industry Leaders

Microsoft Corporation

Google LLC

Salesforce, Inc.

OpenAI, Inc.

ServiceNow, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2026: OpenAI designated GPT-5.6 as the preferred model across Microsoft 365 Copilot in Word, Excel, PowerPoint, Chat, and Cowork. Microsoft accesses GPT-5.6 both natively through Azure and directly via API, confirming OpenAI's continued central role in Microsoft's productivity AI stack following the April 2026 commercial agreement restructuring.

- July 2025: Microsoft announced the general availability of Sales Agent and Service Agent inside Microsoft 365 Copilot and Dynamics 365, extending agentic AI into customer-facing revenue and service workflows. The launch also introduced Dynamics 365 Sales and Customer Service plugins for Copilot Cowork.

- June 2026: Microsoft Copilot Cowork reached general availability worldwide, with integrations across Dynamics 365 ERP and CRM applications, Microsoft Fabric, and third-party enterprise plugins including Moodys, Morningstar, S&P Global Energy, and LSEG.

- May 2026: SAP and Anthropic announced that Claude will serve as the primary reasoning and agentic capability embedded in the SAP Business AI Platform, powering Joule agents unveiled at SAP Sapphire, and deepening Anthropic's enterprise reach across SAP's global ERP customer base.

North America AI Copilot Market Report Scope

The North America AI copilot market includes AI assistants built into software to help humans and automate tasks using large language models. These tools provide real-time suggestions, analyze data, and run workflows across various industries in the US, Canada, and Mexico. Driven by strong tech infrastructure and top AI talent, these copilots help organizations improve efficiency and accelerate digital transformation.

The North America AI Copilot Market Report is Segmented by Copilot Type (Horizontal Productivity Copilots, Functional Workflow Copilots, Technical and Engineering Copilots, and Industry-Specific Copilots), Deployment (Cloud-Based, Hybrid, and On-Premises), Organization Size (Large Enterprises, and Small and Medium Enterprises), Application (Knowledge Work and Productivity Assistance, Software Engineering and Technical Operations, Customer and Employee Service Operations, Sales, Marketing and Revenue Enablement, Business Process and Enterprise Operations, and Regulated Industry Workflows), End-User Industry (IT and Telecommunication, BFSI, Healthcare and Life Sciences, Retail and E-Commerce, Industrial Manufacturing, Education and Research Institutions, Media and Entertainment, Government and Administration, Energy and Utilities, and Other End-User Industries), and Geography (United States, Canada, and Mexico). The Market Forecasts are Provided in Terms of Value (USD).

| Horizontal Productivity Copilots |

| Functional Workflow Copilots |

| Technical and Engineering Copilots |

| Industry-Specific Copilots |

| Cloud-Based |

| Hybrid |

| On-Premises |

| Large Enterprises |

| Small and Medium Enterprises |

| Knowledge Work and Productivity Assistance |

| Software Engineering and Technical Operations |

| Customer and Employee Service Operations |

| Sales, Marketing and Revenue Enablement |

| Business Process and Enterprise Operations |

| Regulated Industry Workflows |

| IT and Telecommunication |

| BFSI |

| Healthcare and Life Sciences |

| Retail and E-Commerce |

| Industrial Manufacturing |

| Education and Research Institutions |

| Media and Entertainment |

| Government and administration |

| Energy and Utilities |

| Other end-user industries |

| United States |

| Canada |

| Mexico |

| By Copilot Type | Horizontal Productivity Copilots |

| Functional Workflow Copilots | |

| Technical and Engineering Copilots | |

| Industry-Specific Copilots | |

| By Deployment | Cloud-Based |

| Hybrid | |

| On-Premises | |

| By Organization Size | Large Enterprises |

| Small and Medium Enterprises | |

| By Application | Knowledge Work and Productivity Assistance |

| Software Engineering and Technical Operations | |

| Customer and Employee Service Operations | |

| Sales, Marketing and Revenue Enablement | |

| Business Process and Enterprise Operations | |

| Regulated Industry Workflows | |

| By End-User Industry | IT and Telecommunication |

| BFSI | |

| Healthcare and Life Sciences | |

| Retail and E-Commerce | |

| Industrial Manufacturing | |

| Education and Research Institutions | |

| Media and Entertainment | |

| Government and administration | |

| Energy and Utilities | |

| Other end-user industries | |

| By Geography | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

What is the size outlook for the North America AI copilot space?

The North America AI copilot market size stood at USD 10.46 billion in 2026 and is forecast to reach USD 34.44 billion by 2031 at a 26.91% CAGR.

Which copilot type currently leads regional demand?

Horizontal Productivity Copilots led in 2025 with 42.18% share because they fit broad daily tasks such as drafting, summarizing, and communication support.

Which deployment model is expanding the fastest?

Hybrid deployment is projected to grow the fastest at a 28.83% CAGR as enterprises balance cloud speed with stronger control over sensitive workloads.

Why are regulated sectors becoming important buyers?

Financial services, healthcare, and government increasingly see copilots as tools for compliant documentation, reporting, and workflow discipline when human oversight remains in place.

What is driving adoption among smaller businesses?

Lower-cost bundled offers such as Microsoft 365 Copilot Business, easier access to AI tools, and platform partnerships for mid-market workflows are improving adoption conditions for SMEs.

Which country offers the strongest growth opportunity after the United States?

Mexico stands out with a projected 30.14% CAGR through 2031, supported by nearshoring, manufacturing intelligence needs, and a widening digital business base.

Page last updated on: