Normal Saline For Parenteral Use Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.99 Billion |

| Market Size (2031) | USD 5.53 Billion |

| Growth Rate (2026 - 2031) | 6.74% CAGR |

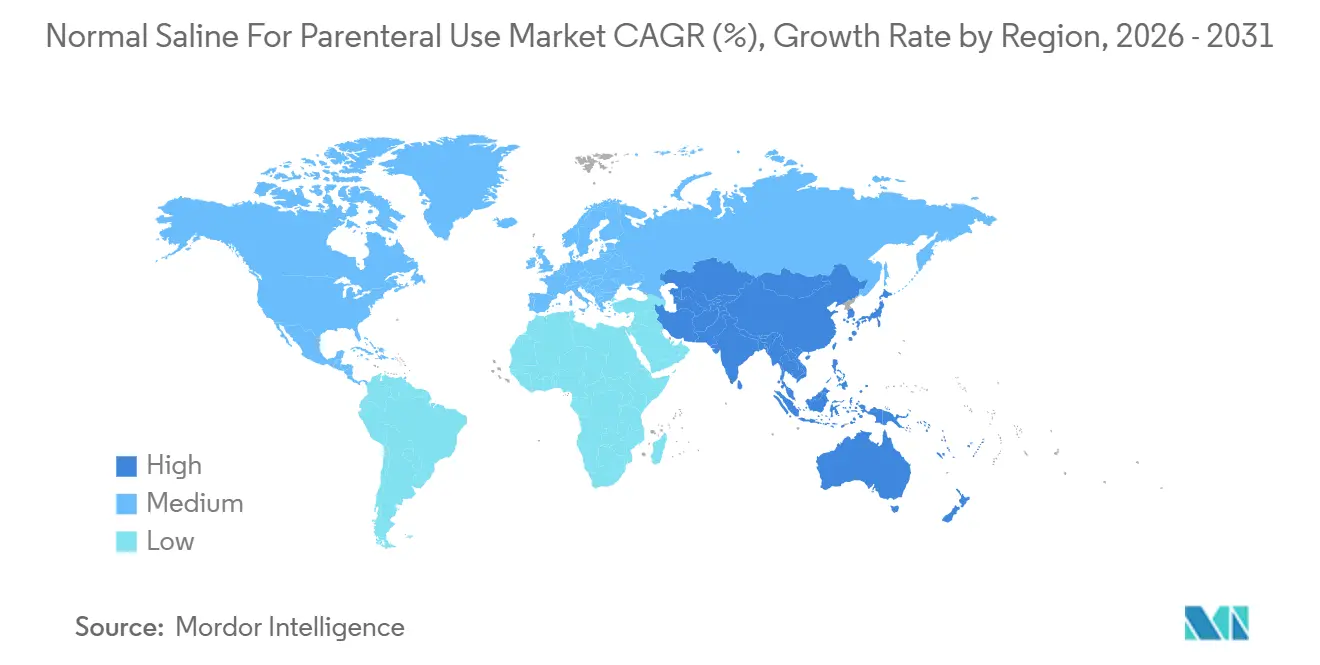

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Normal Saline For Parenteral Use Market Analysis by Mordor Intelligence

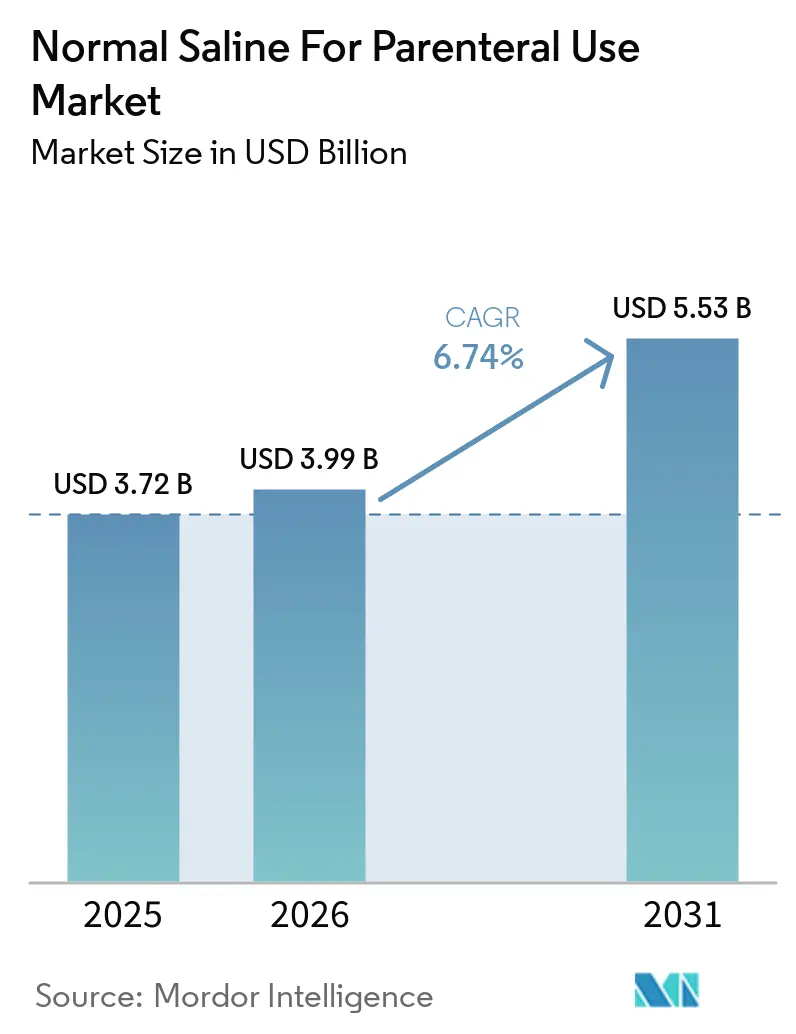

The Normal Saline For Parenteral Use Market size was valued at USD 3.72 billion in 2025 and is estimated to grow from USD 3.99 billion in 2026 to reach USD 5.53 billion by 2031, at a CAGR of 6.74% during the forecast period (2026-2031).

This growth trajectory is driven by factors such as supply-chain concentration, increasing global surgical volumes, and rapid infrastructure development in emerging economies. Following the 2024 Baxter outage, regulatory scrutiny has intensified, prompting hospitals to diversify suppliers and maintain larger safety stocks. The market is also benefiting from the migration of elective procedures to ambulatory settings, where intermediate-volume formats dominate, and from stricter infection-control standards accelerating the adoption of prefilled flush syringes. On the competitive front, three multinational corporations hold a dominant market share, while cost-efficient Asian manufacturers are capturing a growing share of tenders in Africa and Latin America. Environmental concerns over single-use plastics and a slight clinical shift toward balanced crystalloids are creating additional pressures. In response, major manufacturers are adopting non-PVC packaging and diversifying their product portfolios to mitigate these challenges.

Key Report Takeaways

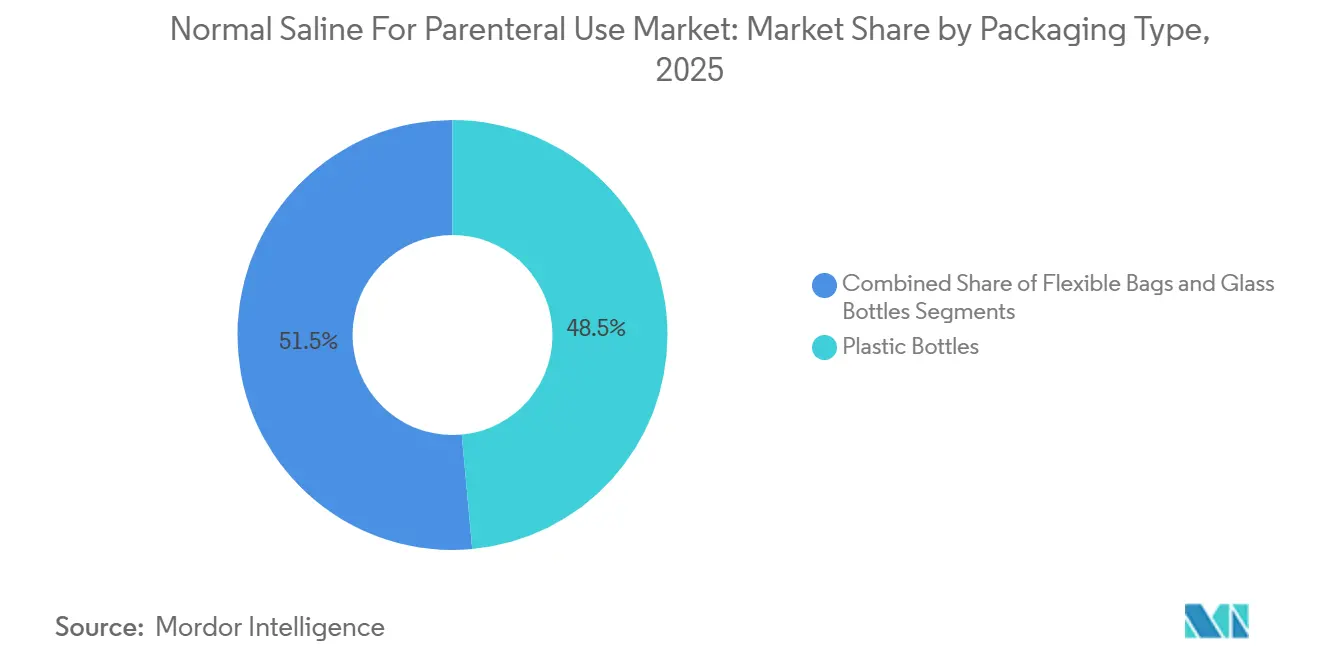

- By packaging type, plastic bottles commanded 48.54% revenue share in 2025, while flexible bags are forecast to expand at an 8.54% CAGR to 2031.

- By volume size, the 101–250 mL segment held 55.43% of the Normal Saline for Parenteral Use market share in 2025; the 251–500 mL range is projected to advance at an 8.43% CAGR through 2031.

- By application, intravenous injection accounted for a 71.34% share of the Normal Saline for Parenteral Use market size in 2025, whereas flush/catheter-lock solutions are expected to accelerate at an 8.65% CAGR through 2031.

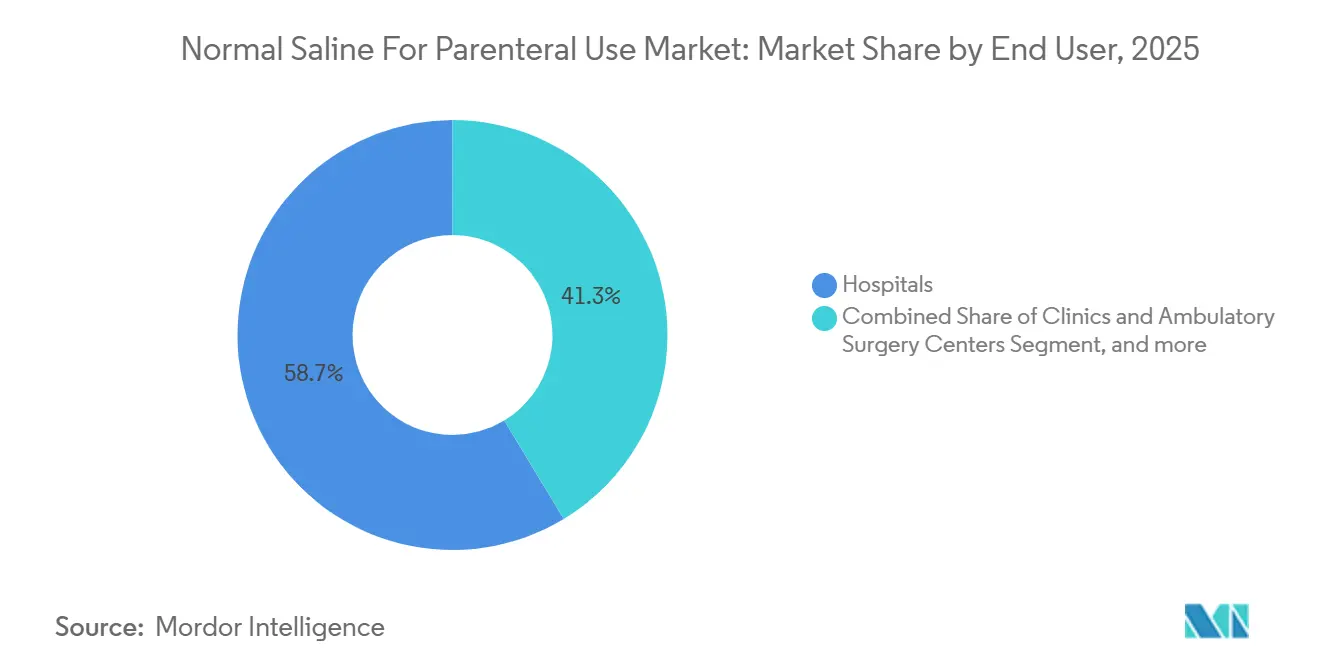

- By end user, hospitals led with 58.65% revenue share in 2025; clinics and ambulatory surgery centers are expected to be the fastest-growing channel at a 9.43% CAGR to 2031.

- By distribution channel, direct tenders and group-purchasing contracts held 48.65% of 2025 sales; distributors and wholesalers are expected to post a 9.21% CAGR across the forecast period.

- By geography, North America contributed 42.67% of 2025 revenues, while Asia-Pacific is expected to post the highest regional CAGR at 7.54% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Normal Saline For Parenteral Use Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Global Surgical Procedure Volumes | +1.8% | Global, strongest in Asia-Pacific and Middle East | Medium term (2-4 years) |

| Rising Burden of Chronic Diseases | +1.5% | North America and Europe | Long term (≥ 4 years) |

| Expansion of Healthcare Infrastructure | +1.3% | Asia-Pacific core; spillover to Middle East & Africa | Long term (≥ 4 years) |

| Adoption of Ready-to-Use Sterile IV Solutions | +1.0% | North America & Europe; moving into Asia-Pacific | Short term (≤ 2 years) |

| Supply-Chain Localization Post-Pandemic | +0.9% | North America & Europe; secondary Asia-Pacific effect | Medium term (2-4 years) |

| Growth of Home and Ambulatory Infusion | +0.7% | North America & Europe; urban Asia-Pacific centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Global Surgical Procedure Volumes

Every surgical case requires intravenous access for anesthesia, fluid resuscitation, and drug delivery, thereby directly linking procedure counts to saline demand. The United Kingdom logged 2.35 million accident-and-emergency visits in December 2024, a 7.6% year-over-year increase, signaling pent-up demand that converts into surgeries as capacity expands. Belgium performed 20,712 procedures per 100,000 residents in the latest reporting year, while sub-Saharan Africa averages below 500, underlining upside potential as emerging economies add operating theaters. In the United States, more than 6,100 Medicare-certified ambulatory surgery centers now handle high-volume orthopedic and ophthalmologic cases, cementing demand for 101–250 mL and 251–500 mL bags that balance waste with procedural flexibility. These trends align with the fastest-growing segment metrics noted in the Normal Saline for Parenteral Use market. Hospitals and ambulatory centers thus shape both baseline volume and the product-mix evolution toward intermediate sizes.

Rising Burden of Chronic Diseases and Hospital Admissions

Chronic illnesses drive frequent hospitalizations that consume large-volume parenteral fluids for hydration and drug administration. Six in 10 U.S. adults live with at least one chronic disease, leading to roughly 36 million admissions per year, each involving multiple liters of saline. Europe’s population over 65 reached 21% in 2023, elevating discharge rates to 155 per 1,000 inhabitants and sustaining steady demand for maintenance fluids. China expects more than 300 million citizens over 60 by 2025, a demographic surge that magnifies inpatient throughput outside major coastal cities. Although these volumes drive the Normal Saline for Parenteral Use market, centralized procurement schemes in China and several EU states compress unit pricing, challenging margin expansion for manufacturers without large-scale, low-cost plants. The net effect supports topline growth but pressures profitability, fostering continued consolidation.

Expansion of Healthcare Infrastructure in Emerging Economies

India expanded its hospital-bed base from 469,672 in 2005 to 849,206 by 2021, while Indonesia’s Ministry of Health targets 90% of primary care centers stocked with essential medicines by 2029. Vietnam attracted USD 200 million in sterile-injectables investment between 2023 and 2024 as regional players set up large-volume parenteral lines. China’s Kelun Group operates more than 30 IV-fluid plants and exports to 80 countries, leveraging lower labor costs to win tenders in Africa and Latin America. These build-outs shorten supply chains, introduce new regional competitors, and tilt growth to Asia-Pacific, which records the fastest CAGR within the Normal Saline for Parenteral Use market. Successful penetration of high-value North American and European tenders still hinges on meeting WHO Prequalification and stringent GMP audits.

Increasing Adoption of Ready-to-Use Sterile IV Solutions

Hospital pharmacy labor shortages and infection-prevention mandates fuel the shift from compounded products to prefilled bags and syringes. Prefilled saline flush syringes eliminate manual draws from multi-dose vials and cut touch contamination, an advantage highlighted by the Institute for Safe Medication Practices[1]Institute for Safe Medication Practices, “Safety Considerations with Prefilled Syringes,” ismp.org. Baxter’s Viaflex bags and B. Braun’s Ecoflac containers provide closed-system compatibility, aligning with Joint Commission standards and minimizing central-line infection risks. The 2024 Baxter shortage forced U.S. hospitals to adopt conservation protocols, underscoring the operational value of smaller bag sizes and ready-to-use formats during supply disruption. As manufacturing capacity normalizes, demand will revert to pre-incident trajectories but with a lasting preference for stocked, ready-to-infuse solutions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory and Quality Compliance Costs | −1.2% | North America & Europe | Long term (≥ 4 years) |

| Commodity Pricing Pressure | −0.9% | Global, heightened under centralized buying | Medium term (2-4 years) |

| Clinical Shift to Balanced Crystalloids | −0.7% | North America & Europe | Medium term (2-4 years) |

| Environmental Concerns Over Plastic Packaging | −0.5% | Europe & North America; urban Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory and Quality Compliance Requirements

Sterile-injectable plants must comply with FDA 21 CFR Part 211 and the 2022 EMA GMP Annex 1, whose tighter aseptic-process rules push greenfield capital costs up to USD 100 million[2]European Medicines Agency, “Annex 1 Manufacture of Sterile Medicinal Products,” europa.eu. The FDA issued 12 warning letters for sterile-drug violations in 2024, illustrating how even minor deviations can halt production. Baxter’s flood-induced closure revealed that stringent compliance does not fully shield against natural disasters, while the restart required extensive cleanroom requalification, delaying market re-entry. High barriers dampen new-entrant interest, keeping production concentrated among incumbents but also creating systemic risk when a single plant fails. The resulting impact trims 1.2 percentage points from the Normal Saline for Parenteral Use market’s potential CAGR in highly regulated regions.

Environmental Concerns Over Single-Use Plastic Packaging

Healthcare accounts for 5.9% of U.S. greenhouse-gas emissions, and IV bags form a visible share of single-use waste[3]Health Care Without Harm, “Health Sector Climate Footprint Report,” noharm.org. European tenders increasingly score bids on sustainability, nudging hospitals toward non-PVC packaging like B. Braun’s Ecoflac, which carries a 12% price premium yet lowers DEHP exposure. The EU Single-Use Plastics Directive does not currently cover medical devices, but rising carbon-accounting rules will increase scrutiny by 2027. Hospitals in densely populated Asian cities also explore recycling pilots, suggesting a future cost burden that established brands can absorb more readily than small entrants. The resulting drag on the Normal Saline for Parenteral Use market is modest but persistent.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Packaging Type: Flexible Bags Will Outpace Rigid Containers

The market share for plastic bottles reached 48.54% of global revenue in 2025, yet flexible bags are on track for 8.54% CAGR through 2031 due to storage efficiency and lighter freight loads. These collapsible formats lower warehouse footprint by roughly 60%, a decisive advantage for urban hospitals where space commands premium rents. B. Braun’s Ecoflac and Baxter’s Viaflex non-PVC bags already win sustainability-weighted European tenders, while cost-focused Asian facilities adopt PVC bags but may pivot if recycling mandates tighten. Plastic bottles remain preferred for manual gravity infusions in home care, where patients value rigidity and drop-rate visibility, sustaining a sizable base despite slower growth. Glass bottles now serve niche markets in parts of Africa and Latin America where reusable glassware is still sterilized, but their global share continues to erode.

Manufacturers integrate bags with closed-system transfer devices to curtail contamination, a feature that aligns with post-pandemic infection controls. Logistics savings also matter: a pallet of flexible bags weighs up to 20% less than equivalently filled rigid containers, reducing transport emissions and cost. Hospitals in the U.S. Northeast reported a nine-month payback after switching to bag formats once waste-handling fees and floor-space savings were tallied. Conversely, recyclability questions linger because multilayer polymer films complicate waste-stream sorting. Producers exploring monomaterial or chemically recyclable films may gain an edge as carbon-reporting rules tighten.

By Volume Size: Mid-Range Bags Support Ambulatory Growth

The 101–250 mL category led the Normal Saline for Parenteral Use market with a 55.43% share in 2025, driven by its fit with antibiotic dilution and routine hydration protocols. Intermediate 251–500 mL bags are the clear growth leader, advancing at an 8.43% CAGR as ambulatory surgery centers standardize on sizes that minimize waste during 60- to 180-minute procedures. Large 501–1,000 mL containers expand broadly with ICU demand but without a segment-specific tailwind.

Ambulatory migration influences mid-range uptake, as payers direct low-acuity cases away from costlier inpatient beds. This shift dovetails with home-infusion trends where portable pumps favor manageable 250 mL reservoirs. Prefilled flush syringes, typically 3–10 mL, carve a fast-growing micro-segment thanks to CLABSI mitigation programs. U.S. hospitals spend roughly USD 48,000 per CLABSI, making the syringes’ premium easily justified when infection rates drop. Yet, raw-material inflation challenges syringe profitability unless offset through highly automated assembly lines.

By Application: Infection-Control Protocols Propel Flush Solutions

Intravenous injection uses claimed 71.34% of 2025 revenue, but growth aligns with the broader market trajectory. Flush/catheter-lock solutions post the quickest pace at 8.65% CAGR through 2031, catalyzed by Joint Commission accreditation requirements that prioritize prefilled syringes for central-line maintenance. Hospitals report that mandating single-use flushes lowered reported contamination incidents by 15%, underscoring the clinical rationale. Manufacturers respond with sterile, ready-to-use packs that free nursing labor otherwise spent on drawing saline from bulk vials. Integration with closed connectors, as seen in ICU Medical’s portfolio, further streamlines workflow.

By End User: Ambulatory Settings Outperform Hospitals

Hospitals still generate 58.65% of spending, yet rise moderately annually as bed expansion plateaus in mature economies. Clinics and ambulatory surgery centers, by contrast, will grow 9.43% annually, lifted by payer incentives and technological advances that enable higher-acuity outpatient procedures. Home-health settings follow closely, as portable pumps and broader reimbursement codes extend therapy into living rooms. The pivot favors smaller bags and syringes, forcing manufacturers to adjust production mixes. Hospitals respond by forming outpatient subsidiaries, but installed compounding gear ties them to legacy large-volume formats, limiting agility.

By Distribution Channel: Wholesalers Erode GPO Dominance

Direct tenders and group-purchasing agreements controlled 48.65% of 2025 sales. Distributors and wholesalers, able to make rapid deliveries in crises, capture share at a 9.21% CAGR through 2031. McKesson, AmerisourceBergen, and Cardinal Health expand refrigerated logistics and emergency-stock programs to serve this rising demand. Online pharmacies remain niche; strict prescription rules and cold-chain challenges keep penetration modest despite moderate CAGR momentum. Dual-source strategies now rank high on procurement scorecards, favoring manufacturers capable of omnichannel supply.

Geography Analysis

North America generated 42.67% of global revenue in 2025 because of market maturity and incremental substitution by balanced crystalloids. The 2024 hurricane damage that idled Baxter’s North Cove plant revealed the risks of concentrated production; subsequent FDA conservation guidance and GPO supplier diversification have lasting effects on sourcing strategy. Canada’s single-payer system and Mexico’s role as a nearshoring location both influence regional dynamics, with Mexico’s lower labor costs attracting fresh capacity aimed at U.S. demand.

Asia-Pacific shows the fastest expansion at 7.54% CAGR through 2031, powered by infrastructure build-outs across China, India, Vietnam, and Indonesia. China’s Kelun Group exports to 80 countries, capitalizing on cost advantages, while India’s “Make in India” push strengthens domestic manufacturing and export capacity. Southeast Asian nations receive FDI that adds sterile-injectable lines, tightening regional supply chains, and reducing reliance on European imports. Mature markets such as Japan still grow, reflecting increased procedure volumes among aging populations balanced by cost-containment efforts.

Europe accounted for significant percentage of global spending in 2025. Revised Annex 1 rules increase compliance expenses, consolidating production among large players like Fresenius Kabi and B. Braun. Aging demographics continue to propel baseline demand, yet austerity measures in Southern Europe and the United Kingdom’s shift toward day-case surgery moderate overall volume. The European Union’s sustainability directives further influence packaging decisions, favoring non-PVC lines that command minor price premiums.

The Middle East & Africa and South America combined for minor share of 2025 revenue. Gulf Cooperation Council countries invest in tertiary hospitals that favor premium ready-to-use solutions, while African tenders often reward the lowest bidder, benefiting Chinese and Indian suppliers. Brazil’s universal healthcare expansion channels consistent demand but subjects suppliers to reference-pricing caps that limit margin. Overall, emerging-market growth outpaces developed regions, re-balancing the geographic portfolio of multinational producers.

Competitive Landscape

The normal saline for parenteral use market remains moderately concentrated. Baxter, Fresenius Kabi, and B. Braun collectively have a significant global share in 2025, yet the North Cove incident demonstrated that scale does not assure supply continuity. ICU Medical’s USD 2.4 billion purchase of Smiths Medical signaled a pivot to bundled therapy solutions, coupling pumps with consumables to capture higher-margin integrated revenue streams. Chinese manufacturers Kelun Group and Cisen Pharmaceutical leverage ultra-low cost bases to win price-sensitive contracts in Africa and Latin America, although stringent quality audits limit their penetration of North American and Western European tenders.

Strategic differentiation aligns with regional priorities. Western incumbents invest in non-PVC films and closed-system compatibility to meet sustainability and infection-control criteria, whereas Asian producers double down on cost optimization through high-volume plants. Process innovation remains incremental; automated filling and real-time environmental monitoring are standard, but commodity status keeps R&D outlays modest. Regulatory changes now mandate redundancy planning, favoring multinationals with geographically dispersed sites. Smaller regional producers either focus on niche flush syringes or position themselves as contract packagers for global brands.

Manufacturers also explore service bundling. Fresenius Kabi offers total IV therapy management, including pumps, accessories, and electronic inventory platforms that lock customers into multi-year agreements. B. Braun captures premium European tenders by combining Ecoflac bags with recycling partnerships that ease hospitals’ waste-diversion reporting. Meanwhile, distributor relationships tighten: McKesson and Cardinal Health sign multi-year supply-assurance contracts that penalize missed deliveries, raising the bar for operational reliability.

Normal Saline For Parenteral Use Industry Leaders

Baxter International Inc.

Fresenius Kabi AG

Kelun Group

B. Braun Melsungen AG

ICU Medical, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: According to 2 Minute Medicine, hospitalized children should be given isotonic fluids, such as 0.9% normal saline, instead of hypotonic solutions for their routine maintenance needs.

- October 2025: B. Braun Medical Inc. (B. Braun), a recognized player in infusion therapy and pharmaceutical manufacturing, launched Midazolam in 0.8% Sodium Chloride Injection in the U.S. market. The preservative-free injections will be offered in two strengths: 50 mg in 50 mL and 100 mg in 100 mL.

Global Normal Saline For Parenteral Use Market Report Scope

As per the scope of the report, normal saline for parenteral use is a sterile, isotonic solution of 0.9% sodium chloride in water, administered intravenously to maintain fluid and electrolyte balance. It is commonly used for hydration, medication delivery, and as a vehicle for other IV therapies. The solution closely mimics the body's natural plasma, ensuring safe and effective treatment.

The Normal Saline for Parenteral Use Market is Segmented by Packaging Type (Flexible Bags, Plastic Bottles, and Glass Bottles), Volume Size (≤100 mL, 101–250 mL, 251–500 mL, and 501–1,000 mL), Application (Intravenous Injection, Intramuscular Injection, Flush/Catheter Lock), End User (Hospitals, Clinics & Ambulatory Surgery Centers, and Home Healthcare Settings), Distribution Channel (Direct Tenders & Group Purchasing, Distributors/Wholesalers, and Online Pharmacies), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD) for the above segments.

| Flexible Bags |

| Plastic Bottles |

| Glass Bottles |

| ≤100 mL |

| 101 - 250 mL |

| 251 - 500 mL |

| 501 - 1 000 mL |

| Intravenous Injection |

| Intramuscular Injection |

| Flush / Catheter Lock |

| Hospitals |

| Clinics & Ambulatory Surgery Centers |

| Home Healthcare Settings |

| Direct Tenders & Group Purchasing |

| Distributors / Wholesalers |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Packaging Type | Flexible Bags | |

| Plastic Bottles | ||

| Glass Bottles | ||

| By Volume Size | ≤100 mL | |

| 101 - 250 mL | ||

| 251 - 500 mL | ||

| 501 - 1 000 mL | ||

| By Application | Intravenous Injection | |

| Intramuscular Injection | ||

| Flush / Catheter Lock | ||

| By End User | Hospitals | |

| Clinics & Ambulatory Surgery Centers | ||

| Home Healthcare Settings | ||

| By Distribution Channel | Direct Tenders & Group Purchasing | |

| Distributors / Wholesalers | ||

| Online Pharmacies | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the Normal Saline for Parenteral Use market by 2031?

The market is forecast to reach USD 5.53 billion by 2031 based on a 6.74% CAGR.

Which region will post the fastest growth through 2031?

Asia-Pacific leads with a projected 7.54% CAGR through 2031, propelled by hospital build-outs in China, India, and Southeast Asia.

Why are flexible IV bags gaining share over plastic bottles?

Flexible bags cut storage space by up to 60%, reduce freight weight, and increasingly meet sustainability requirements in major tenders.

How did the 2024 Baxter plant shutdown affect supply dynamics?

The outage removed 60% of U.S. IV fluid capacity, triggered FDA shortage declarations, and forced hospitals to diversify suppliers, reshaping purchasing contracts.

Which application segment is expanding the quickest?

Flush and catheter-lock solutions, fueled by infection-control mandates, are growing at an 8.65% CAGR through 2031.

What competitive strategies are market leaders using to maintain share?

Leaders invest in non-PVC packaging, geographic redundancy, and integrated product bundles that pair saline with infusion pumps and accessories.

Page last updated on: