Nordics Frontline Worker Technology Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

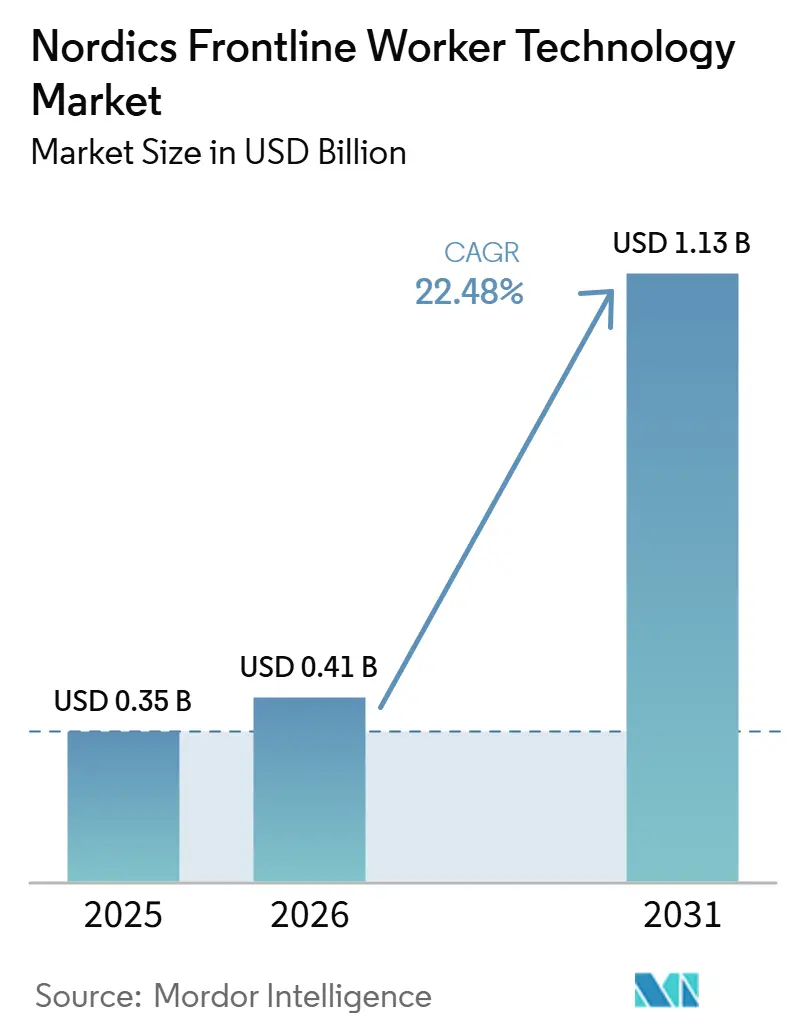

| Base Year Market Size (2025) | USD 0.35 Billion |

| Market Size (2026) | USD 0.41 Billion |

| Market Size (2031) | USD 1.13 Billion |

| Growth Rate (2026 - 2031) | 22.48% CAGR |

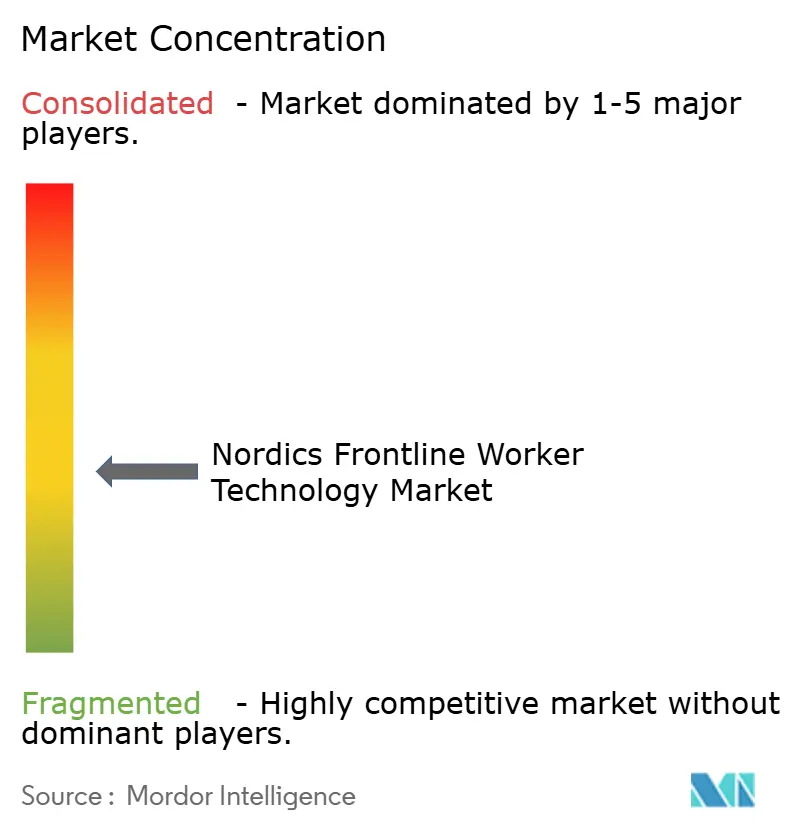

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Nordics Frontline Worker Technology Market Analysis by Mordor Intelligence

The Nordics frontline worker technology market size is projected to expand from USD 0.35 billion in 2025 and USD 0.41 billion in 2026 to USD 1.13 billion by 2031, registering a CAGR of 22.48% between 2026 and 2031. The market is growing because labor shortages across Sweden, Norway, Denmark, Finland, and Iceland are no longer short-term staffing issues, and employers now treat frontline technology as a core operating tool rather than an optional efficiency layer. Demand is also rising because cloud delivery has already become the default enterprise model in the region, which makes new deployments easier to approve and faster to scale across distributed workforces. Buying behavior is shifting from basic communication tools toward platforms that combine scheduling, execution, analytics, compliance, and AI inside daily workflows. Competitive activity is moving in the same direction, with vendors strengthening integration depth, audit readiness, and mobile usability as customers move from pilot programs to broader rollouts. The strongest opportunities remain in settings where labor pressure, multisite coordination, and compliance demands overlap, especially across healthcare, manufacturing, retail, logistics, and field operations.

Key Report Takeaways

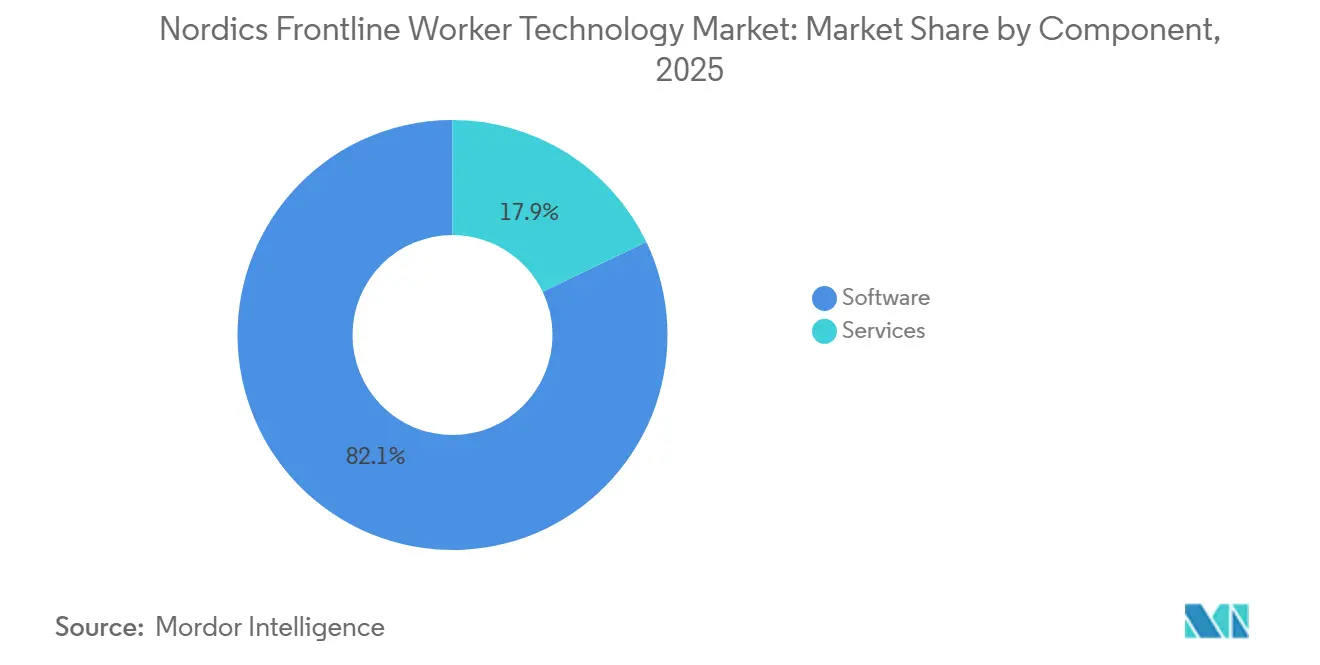

- By component, software held 82.11% share in 2025, while services are projected to expand at 23.18% CAGR through 2031.

- By deployment mode, cloud-based delivery accounted for 81.66% of the Nordics frontline worker technology market in 2025 and is projected to expand at a 24.66% CAGR through 2031.

- By organization size, large enterprises held 71.11% of the Nordics frontline worker technology market share in 2025, while SMEs are projected to expand at 26.91% CAGR through 2031.

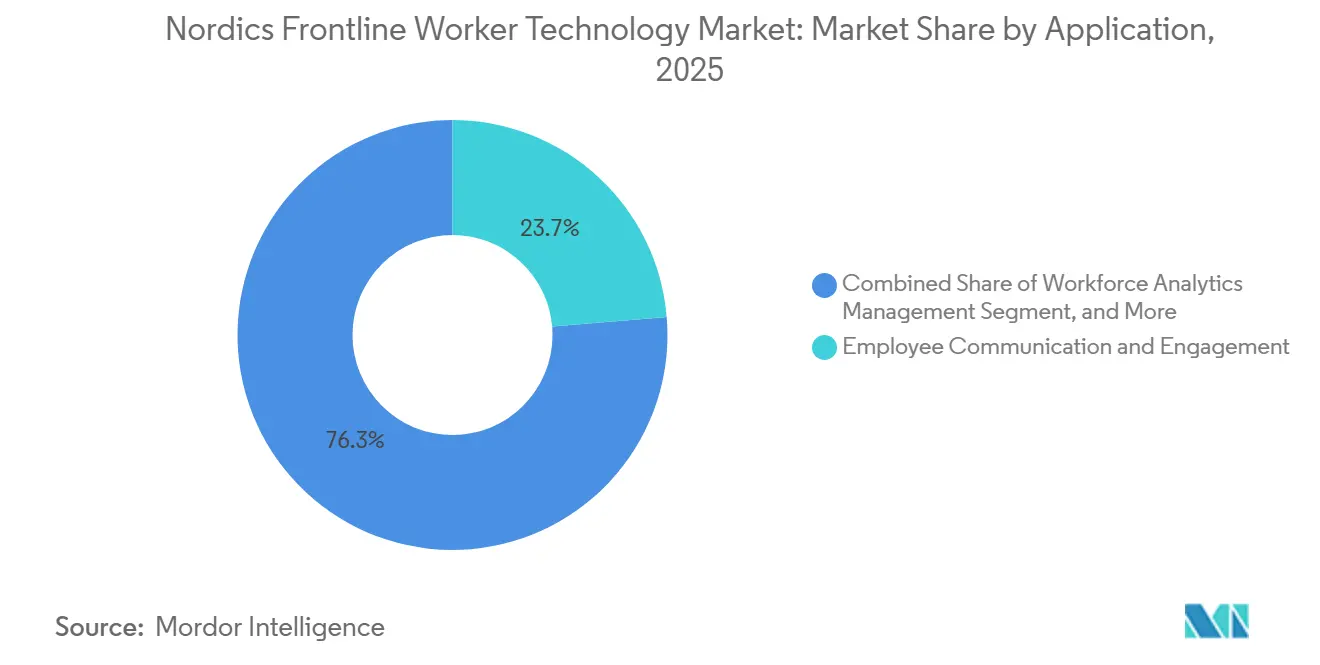

- By application, employee communication and engagement accounted for 23.66% of the Nordics frontline worker technology market size in 2025, while workforce analytics and performance management are projected to expand at 28.33% CAGR through 2031.

- By end-user industry, industrial manufacturing accounted for 31.11% share in 2025, while healthcare and life sciences are projected to expand at 29.14% CAGR through 2031.

- By geography, Sweden held 36.66% share in 2025, while Finland is projected to expand at 31.22% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Nordics Frontline Worker Technology Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Labor Scarcity Across Field and Store Operations | +6.8% | Nordics-wide, most acute in Sweden and Norway | Short term (≤ 2 years) |

| Shift Toward Real-Time Task Orchestration for Distributed Workforces | +5.1% | Nordics-wide, highest in Sweden and Denmark | Medium term (2-4 years) |

| Enterprise Demand for Audit-Ready Safety and Compliance Workflows | +3.5% | Nordics-wide, strongest in Norway energy and Finland pharma manufacturing | Medium term (2-4 years) |

| Multisite Operations Adopting Unified Worker Visibility Platforms | +2.6% | Nordics-wide, highest in Sweden and Denmark | Medium term (2-4 years) |

| Edge AI Enabling Context-Aware Worker Guidance without Constant Connectivity | +1.9% | Finland and Norway, especially remote and offshore industrial sites | Long term (≥ 4 years) |

| Expansion of Shared-Device and BYOD-Enabled Frontline Access Models | +1.4% | Nordics-wide, highest in Sweden and Denmark | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Labor Scarcity Drives Adoption Across Field and Store Operations

Acute labor shortages across stores, care settings, field services, and production sites have pushed the Nordics frontline worker technology market further into core operating budgets. Sweden recorded 10,500 vacancies in service, care, and shop sales occupations in 2025, while total shortages across frontline occupational groups reached 61,000, indicating a broad staffing gap rather than an isolated function.[1]Statistics Sweden, “Job Openings and Recruitment Needs 2025,” scb.se Norway also reported persistent shortages in healthcare, construction, and industrial trades in its 2025 enterprise survey, which confirms that the labor constraint extends across different parts of the regional economy. The wider European pattern points in the same direction, as the European Labor Authority identified persistent labor shortages across several frontline occupations in 2025. The World Economic Forum also noted in 2025 that 80% of the global workforce is made up of non-desk workers, which reinforces why productivity tools aimed at frontline roles now attract broader strategic attention. In the Nordics, aging populations, high social mobility, and limited labor supply for physically demanding roles mean employers increasingly rely on workflow software, automation, and mobile coordination tools to maintain stable daily operations.

Real-Time Task Orchestration Redefines Distributed Workforce Coordination

The Nordics frontline worker technology market is also advancing because large employers want tighter control over execution across stores, warehouses, plants, and field teams. WorkJam’s January 2026 platform release added embedded AI that can trigger tasks, flag exceptions, and connect with external systems to resolve issues, demonstrating how vendors are moving from communication functions to direct workflow execution.[2]WorkJam, “WorkJam Raises the Bar for Frontline Operations Platforms With Major Release,” workjam.com This matters because distributed frontline operations generate constant streams of information around task completion, shift handoffs, missed actions, and compliance gaps, and legacy HR systems rarely capture that activity in a structured way. The installed base for these tools is already meaningful, as Quinyx reported that 42% of Nordic frontline workers used a company-provided communication platform in 2024. Once communication access is in place, employers can add task management, exception handling, and real-time operational visibility without rebuilding the user environment from the start. That progression is helping the Nordics' frontline worker technology market move from basic connectivity to coordinated execution across large, multisite workforces.

Enterprise Demand for Audit-Ready Safety and Compliance Workflows

Safety and compliance needs are creating another durable layer of demand across the Nordics frontline worker technology market, especially in energy, healthcare, pharmaceutical manufacturing, and construction. The EU AI Act, Regulation (EU) 2024/1689, entered into force in August 2024 and classifies certain AI systems used in employment settings, including performance monitoring and task management, as high-risk uses that require stronger controls and auditability.[3]European Commission, “AI Act: Shaping Europe’s Digital Future,” digital-strategy.ec.europa.eu That standard raises the value of platforms that are designed with risk management, data governance, human oversight, and reliable audit trails built into the product. WorkJam’s 2026 release highlighted HIPAA compliance alongside ISO 27001, SOC II Type 2, and CSA Star certifications, which illustrates how vendors are using compliance depth as a buying trigger rather than a supporting feature. In practical terms, customers in regulated settings now want digital proof of training, task completion, safety checks, and escalation paths that can withstand internal review and external scrutiny. That requirement extends the value of frontline platforms beyond communication and into controlled execution, documentation, and accountability.

Multisite Operations Converge on Unified Worker Visibility Platforms

Unified visibility across dispersed sites is becoming increasingly important as retailers, logistics operators, and manufacturers seek consistent execution across large frontline workforces. Zebra Technologies and Oxford Economics reported in 2025 that intelligent frontline investments can improve productivity, revenue, and profitability in manufacturing environments, strengthening the business case for broader connected worker rollouts.[4]Zebra Technologies, “Zebra Showcases AI for the Frontline at Inaugural Frontline AI Summit,” zebra.com The deeper value comes from the data these systems reveal, because a unified platform can show where shift coverage is uneven, where tasks stall, and where site-level compliance varies in ways that local managers often miss. Microsoft’s customer story with Coop Norge showed how a large Nordic retailer used Teams and related collaboration tools to improve communication and change management across its workforce, which supports the broader push toward shared digital coordination environments. As more organizations centralize workforce data and daily task flows, the gap widens between enterprises that can see execution patterns in real time and those still operating through fragmented local processes. That shift is supporting further adoption in the Nordics frontline worker technology market, particularly where operational scale makes inconsistency expensive.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy Integration Across HR, Payroll, POS, And EHS Systems | -3.8% | Nordics-wide, largest enterprises most affected | Medium term (2-4 years) |

| Privacy Concerns Around Worker Tracking And Behavioral Monitoring | -3.4% | Nordics-wide, most acute in Norway and Denmark | Short term (≤ 2 years) |

| Fragmented Device Fleet Management Across Sites And Vendors | -2.2% | Nordics-wide, especially high in industrial manufacturing | Medium term (2-4 years) |

| Union And Employee Pushback Against Algorithmic Scheduling And Monitoring | -1.8% | Nordics-wide, most pronounced in Norway and Sweden | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Legacy System Complexity Slows Frontline Platform Integration

Legacy integration remains one of the clearest practical limits on the pace of the Nordics frontline worker technology market. Large organizations across the region often use separate local systems for payroll, scheduling, ERP, point-of-sale, safety reporting, and workforce administration, and those systems were not originally built to exchange data smoothly with modern frontline platforms. SOTI’s 2025 mobility report identified fragmented legacy systems, manual processes, and inconsistent back-end support as major barriers to frontline mobility programs in healthcare and industrial settings. SAP’s 2025 Norwegian case example for SNP also noted that the legacy environment did not align with the needs of a distributed workforce, requiring the company to invest in deeper integration across HR and payroll systems before frontline data could flow properly. The burden is even heavier in a pan-Nordic rollout because labor reporting and local systems differ across Sweden, Norway, Denmark, Finland, and Iceland. As a result, service timelines often stretch, early returns are harder to show, and some customers delay wider deployments until integration risk is reduced.

Privacy Rules and Worker Monitoring Concerns Limit Feature Scope

Privacy concerns are another strong restraint, as worker tracking and behavioral monitoring face greater acceptance limits in the Nordics than in many other markets. Finland’s Act on Privacy in Working Life adds sector-specific procedural requirements on top of general data protection rules, which raises the compliance threshold for employers and vendors that want to monitor employee behavior or location in detail. The EU AI Act adds another layer because employment-related AI uses require stronger governance, oversight, and documentation when they affect workers directly. The ALMA-AI research, published by the Finnish Institute of Occupational Health and EU-OSHA, found that 3 out of 4 Nordic frontline workers experience algorithmic management, and the study linked heavier algorithmic oversight to higher psychosocial stress, reduced autonomy, and greater time pressure. Those findings matter because they shape union positions, internal governance standards, and the range of product features employers feel comfortable activating. In practice, many deployments move ahead with communication, scheduling, and task guidance first, while more intrusive monitoring features face slower approval paths.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Dominates, But Services Gain Strength Through Integration Needs

Software commanded 82.11% of the market in 2025, keeping it firmly at the center of the Nordics' frontline worker technology market. That lead reflects the region’s long history of enterprise spending on cloud HR, scheduling, communication, and analytics platforms. Many large employers already had a digital base in place before frontline-specific modules became a major buying category. That existing stack makes it easier to add execution, engagement, or analytics tools without replacing the full operating backbone. The dominant purchasing pattern is therefore expansion on top of existing systems rather than full replacement, which helps software retain the largest role across current spending.

Services are projected to grow at a 23.18% CAGR from 2026 to 2031, making them the fastest-growing component of the Nordics frontline worker technology market. This does not suggest that software is weakening. It instead reflects the growing effort needed to connect frontline platforms with payroll, ERP, safety, and workforce systems across multiple countries and sites. Strada Global’s 2025 Workday deployment work in the Nordics showed how employers increasingly rely on specialist implementation partners to simplify complex transformations. SOTI’s 2025 research supports the same pattern, as integration complexity and fragmented back-end environments continue to slow mobility deployments. Over time, recurring support, optimization, and expansion work should keep service revenue growing alongside core subscriptions rather than replacing them.

By Deployment Mode: Cloud Becomes The Standard Delivery Model

Cloud-based deployment held 81.66% of the Nordics frontline worker technology market share in 2025, underscoring the region's alignment with remote, scalable, subscription-led delivery. Organizations entering the category now usually start with cloud-first assumptions rather than comparing every deployment mode from the beginning. This is possible because identity management, enterprise cloud procurement, and data hosting frameworks were already mature across the Nordics before frontline software demand accelerated. That maturity shortens approval cycles and reduces hesitation around mobile access, system updates, and multi-location rollouts. It also supports faster addition of new functions such as analytics, AI assistance, and workflow automation once the core platform is live.

Cloud is also projected to expand at a 24.66% CAGR through 2031, indicating the lead model is still widening rather than stabilizing. Visma’s cloud-first development of Nordic HR and payroll infrastructure shows that even compliance-sensitive workforce systems are moving in the same direction. Hybrid deployment still holds a place in highly regulated environments where partial local control remains important. On-premises systems continue to appear in replacement cycles at legacy-heavy accounts, but they are losing ground in new buying decisions. The opportunity for vendors lies in hybrid-to-cloud migration, where customers want lower integration costs without giving up operational control. Over the forecast period, offline task support, local device processing, and cloud-synchronized analytics are likely to work together more frequently, further reinforcing cloud as the control layer for the Nordics frontline worker technology market.

By Organization Size: Large Enterprises Lead Spending While SMEs Move Faster

Large enterprises held 71.11% of the market in 2025, reflecting the concentration of frontline-heavy sectors in large Nordic employers. Grocery retail, manufacturing, healthcare, and logistics all include operators with large workforces, multiple sites, and centralized procurement structures. Those conditions made large enterprises the earliest practical buyers because they could absorb enterprise licensing and manage the first wave of integration work. Workday’s 2025 customer examples from BDO Norway and Sopra Steria Scandinavia show how Nordic enterprises increasingly expect connected HR, finance, and analytics environments rather than isolated tools. Once a large employer proves the value of better frontline coordination, that result often shapes expectations across the rest of the sector.

SMEs are projected to grow at a 26.91% CAGR from 2026 to 2031, making them the fastest-growing segment in the Nordics frontline worker technology market. The main reason is that cloud delivery and mobile-first product design have lowered the need for heavy upfront infrastructure. WorkJam’s 2026 release added offline task functionality and a simpler mobile configuration, directly supporting customers with limited IT support capacity. Microsoft also introduced a BYOD onboarding wizard for Teams frontline workers in May 2026, helping employers use personal Android and iOS devices when company hardware rollouts are harder to fund. Smaller operators in construction, hospitality, and food service face the same staffing and coordination pressures as large firms, but they have less room to carry ongoing inefficiency. That makes focused, modular deployments attractive, and it supports a land-and-expand pattern that differs from the broader suite purchases seen in large enterprises.

By Application: Communication Leads Adoption While Analytics Gains Momentum

Employee communication and engagement accounted for 23.66% of the Nordics frontline worker technology market size in 2025, making it the largest application entry point. This position is logical because frontline digitization usually starts with access to information, alerts, announcements, and two-way communication. Employers need a reliable way to reach dispersed workers before they can scale more advanced workflows around tasks, learning, or performance. Quinyx reported that 42% of Nordic frontline workers used a company-provided communication platform in 2024, indicating that the first layer of adoption is already established among a meaningful part of the addressable workforce. That installed base gives vendors a ready path to cross-sell task execution, scheduling, analytics, and compliance functions once usage becomes routine.

Workforce analytics and performance management are projected to grow at a 28.33% CAGR through 2031, making it the fastest-rising application in the Nordics frontline worker technology market. This reflects a change in what buyers expect after communication tools are already in place. Once organizations can connect workers digitally, they want clearer evidence of whether staffing, task flow, and execution quality are improving. That increases interest in dashboards, performance indicators, operational heat maps, and data that link frontline activity to broader business outcomes. At the same time, scheduling, learning, safety, and compliance applications continue to grow because they solve immediate day-to-day problems across retail, manufacturing, healthcare, and logistics. The next phase of adoption is therefore less about adding isolated modules and more about combining communication, execution, and measurement inside a single operational workflow.

By End-User Industry: Manufacturing Holds The Largest Base While Healthcare Advances Fastest

Industrial manufacturing accounted for a 31.11% share in 2025, making it the largest end-user segment in the Nordics frontline worker technology market. The region has a dense base of engineering, automotive, process, electronics, and industrial firms that depend on structured shop-floor execution, quality control, safety reporting, and connected worker support. Manufacturers also benefit from the compounding value of execution data, as repeated frontline activities can be tracked, standardized, and improved over time. Zebra Technologies’ connected factory framework highlighted visibility, quality, and workforce augmentation as key areas where digital frontline tools improve plant operations. That operating context makes manufacturing a natural anchor for spending, as use cases are frequent, measurable, and closely tied to production reliability.

Healthcare and life sciences are projected to expand at a 29.14% CAGR from 2026 to 2031, making it the fastest-growing end-user vertical. Public health systems across the Nordics are under pressure to improve service delivery while facing labor shortages and budget constraints. Sweden’s National Board of Health and Welfare reported in 2026 that digital support for frontline care personnel and AI-integrated welfare technology are both expanding across municipalities. That direction supports rising demand for mobile documentation, scheduling support, internal communication, and workflow coordination within care settings. Healthcare also requires stricter documentation and compliance than many other verticals, which underscores the value of platforms that combine usability with audit-ready process control. As a result, the Nordics frontline worker technology market is seeing healthcare move from an emerging use case toward one of the most important growth engines in the forecast period.

Geography Analysis

Sweden held 36.66% of the Nordics frontline worker technology market share in 2025, making it the regional leader by value. The country combines the largest economy in the Nordics with a dense mix of manufacturing, retail, logistics, and public services that rely heavily on frontline labor. Statistics Sweden reported 61,000 shortages across frontline occupational groups in 2025, which helps explain why workforce technology is receiving sustained operating attention. Sweden also benefits from a strong innovation base, ranking 2nd globally in the 2024 Global Innovation Index. Finland is projected to grow at a 31.22% CAGR through 2031, supported by pressure on the healthcare workforce and a technology-intensive industrial base. Technology Industries of Finland projected demand for 14,000 new skilled workers each year over the coming decade, which underlines the structural labor challenge facing employers. Finland’s Ministry of Economic Affairs and Employment also reported in late 2025 that 45% of wage earners worked at organizations already using AI, rising to 70% at firms with 200 or more employees, which indicates a broad institutional base for operational AI adoption.

Denmark remains an important part of the Nordics frontline worker technology market because its retail and logistics sectors are active users of digital workflow tools. Scandit’s 2026 last-mile materials highlight proven smart data-capture use cases among major parcel and postal operators, which are relevant to Danish logistics environments where scan-based work is constant. The country’s strong digital operating culture makes it easier for employers to introduce mobile-first frontline workflows without having to build basic user familiarity from scratch. Norway also holds a differentiated position because labor shortages remain visible across healthcare, construction, and industrial trades, according to NAV’s 2025 enterprise survey. Norway’s offshore and industrial environments also raise demand for safety-critical, connected worker solutions that can work under harsher conditions than those found in standard retail settings.

Iceland is smaller in absolute scale, but its digital readiness and concentration in tourism, retail, healthcare, and fisheries still create meaningful frontline coordination needs. Mobile-first deployment models suit Iceland well because the workforce can often be reached effectively through shared-device and BYOD structures rather than large enterprise hardware fleets. Across all 5 countries, high labor costs and strong digital familiarity support adoption once employers can show a clear operational return. The result is a regional market where structural labor pressure, digital maturity, and compliance-aware buying behavior combine to support continued growth in the Nordics frontline worker technology market through 2031.

Competitive Landscape

The Nordics frontline worker technology market remains moderately fragmented, with broad enterprise platforms and specialized frontline vendors competing from different starting points. Microsoft, SAP SE, Oracle, and Workday benefit from existing enterprise account relationships and deeper links to HR, finance, and identity systems. Specialist providers such as WorkJam, Scandit, ProGlove GmbH, Beekeeper AG, Quinyx AB, and Techstep ASA compete more directly on workflow depth, mobile usability, frontline-specific features, and deployment speed. This creates a two-layer structure where large suite providers offer platform breadth while focused vendors often win on operational fit inside specific use cases. The competitive balance is being shaped less by headline functionality alone and more by how well each vendor can connect daily frontline activity with broader enterprise systems.

Several recent moves show how vendors are trying to strengthen their position in the Nordics frontline worker technology market. WorkJam’s January 2026 release embedded AI directly into workflows, added real-time KPI widgets, and expanded compliance credentials, which support its push toward larger regulated deployments. Microsoft’s May 2026 frontline updates added a BYOD onboarding wizard and expanded access to Frontline Agent features, improving its reach in cost-sensitive deployments and among organizations using personal devices. Blackline Safety’s 2026 going-private transaction with Francisco Partners shows that connected safety platforms are attracting infrastructure-scale capital, especially where recurring revenue and compliance value are already established. Zebra Technologies is also pushing beyond hardware into integrated operational intelligence, supported by its 2025 frontline AI positioning and factory workflow materials. These moves show that vendors are expanding through compliance strength, AI-enabled execution, capital backing, and tighter workflow control.

The open space in the market sits where Nordic compliance needs, workforce consultation norms, and embedded AI execution meet. Vendors that can support GDPR-aware deployments, practical integration, and low-friction mobile adoption should have an advantage over firms that rely solely on basic communication functions. Point solutions without strong links to payroll, ERP, safety, or scheduling data are more exposed as buyers increasingly evaluate total operational fit. At the same time, the number of capable competitors remains high enough to keep the Nordics frontline worker technology market from looking concentrated, especially as global suites and regional specialists continue to overlap across accounts.

Nordics Frontline Worker Technology Industry Leaders

Microsoft Corporation

SAP SE

Workday, Inc.

Zebra Technologies Corporation

Honeywell International Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Blackline Safety Corp. received final regulatory approval and shareholder approval for its going-private transaction with Francisco Partners Management, L.P., with the arrangement expected to close on or about June 30, 2026. The transaction values Blackline Safety at up to USD 850 million, including a contingent value right tied to an annualized recurring revenue target of USD 145 million by October 2027, positioning the connected safety platform for accelerated product investment under private equity ownership.

- June 2026: Scandit released SDK 8.0, introducing AI-driven smart data capture that transitions frontline scanning from single-barcode reads to full contextual understanding, enabling workers to receive automated decisions and workflow guidance in a single action. The release repositions Scandit’s platform as a workflow orchestration and operational intelligence layer for retail, logistics, and manufacturing frontline operations.

- May 2026: Microsoft introduced a BYOD onboarding wizard for Microsoft Teams frontline workers on personal Android and iOS devices, substantially reducing deployment friction for organizations unable to provision company-owned hardware at scale. The update also made Frontline Agent, an AI-powered in-workflow assistant, available to Microsoft 365 Copilot license holders across frontline environments.

- April 2026: Blackline Safety Corp. entered into a definitive arrangement agreement with an affiliate of Francisco Partners Management, L.P. for a go-private transaction at up to USD 9.50 per share, representing a 35% premium to the 20-day volume-weighted average price of its TSX-listed shares, with total consideration of up to USD 850 million.

Nordics Frontline Worker Technology Market Report Scope

The Nordics frontline worker technology market refers to the ecosystem of software and services designed to empower non-desk employees who primarily execute their duties outside a traditional office setting. This includes tools that facilitate communication, task management, scheduling, knowledge sharing, and performance tracking for workers in sectors such as retail, manufacturing, healthcare, and logistics across the Nordic region. The market encompasses cloud-based, on-premises, and hybrid deployment models tailored to the operational and security needs of organizations of varying sizes, from small and medium enterprises to large corporations. Key applications include workforce scheduling and coordination, safety and compliance management, and learning enablement, all aimed at improving operational efficiency, employee engagement, and real-time decision-making at the edge of business operations. The market scope is defined by the revenues generated by technology vendors and service providers across the Nordic countries, specifically Denmark, Norway, Sweden, Finland, and Iceland.

The Nordics Frontline Worker Technology Market Report is Segmented by Component (Software and Services), Deployment (Cloud-Based, Hybrid, and On-Premises), Organization Size (Large Enterprises, and Small and Medium Enterprises), Application (Employee Communication and Engagement, Workforce Execution and Task Management, Workforce Scheduling and Coordination, Learning and Knowledge Enablement, Workforce Analytics and Performance Management, Safety and Compliance Management, and Other Applications), End-User Industry (Retail and E-Commerce, Industrial Manufacturing, Healthcare and Life Sciences, Transportation and Logistics, Hospitality, Construction, Government and Public Administration, and Other Industries), and Geography (Denmark, Norway, Sweden, Finland, and Iceland). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud-Based |

| Hybrid |

| On-Premises |

| Large Enterprises |

| Small and Medium Enterprises |

| Employee Communication and Engagement |

| Workforce Execution and Task Management |

| Workforce Scheduling and Coordination |

| Learning and Knowledge Enablement |

| Workforce Analytics and Performance Management |

| Safety and Compliance Management |

| Other Applications |

| Retail and E-Commerce |

| Industrial Manufacturing |

| Healthcare and Life Sciences |

| Transportation and Logistics |

| Hospitality |

| Construction |

| Government and Public Administration |

| Other Industries |

| Denmark |

| Norway |

| Sweden |

| Finland |

| Iceland |

| By Component | Software |

| Services | |

| By Deployment | Cloud-Based |

| Hybrid | |

| On-Premises | |

| By Organization Size | Large Enterprises |

| Small and Medium Enterprises | |

| By Application | Employee Communication and Engagement |

| Workforce Execution and Task Management | |

| Workforce Scheduling and Coordination | |

| Learning and Knowledge Enablement | |

| Workforce Analytics and Performance Management | |

| Safety and Compliance Management | |

| Other Applications | |

| By End-User Industry | Retail and E-Commerce |

| Industrial Manufacturing | |

| Healthcare and Life Sciences | |

| Transportation and Logistics | |

| Hospitality | |

| Construction | |

| Government and Public Administration | |

| Other Industries | |

| By Geography | Denmark |

| Norway | |

| Sweden | |

| Finland | |

| Iceland |

Key Questions Answered in the Report

What is the size outlook for the Nordics frontline worker technology space?

The Nordics frontline worker technology market size is projected to grow from USD 0.35 billion in 2025 and USD 0.41 billion in 2026 to USD 1.13 billion by 2031 at a 22.48% CAGR.

Which country leads regional demand?

Sweden led with 36.66% share in 2025 because of its larger economy, strong industrial base, and broad frontline labor shortages.

Which country is growing the fastest through 2031?

Finland is projected to expand at 31.22% CAGR, supported by healthcare workforce pressure and a technology-intensive manufacturing base.

Which end-user sector has the strongest growth outlook?

Healthcare and life sciences is the fastest-growing end-user vertical, with a projected 29.14% CAGR through 2031, driven by mobile documentation, communication, and workforce coordination needs.

Which application area currently leads adoption?

Employee communication and engagement held the largest application share at 23.66% in 2025 because most frontline digitization programs begin with information access and internal communication.

What is the main factor supporting adoption across the region?

Persistent labor shortages across care, retail, field, and industrial roles are pushing employers to use digital workflow tools to maintain execution quality without matching headcount growth.

Page last updated on: