Nordic Corrugated Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 4.11 Billion |

| Market Size (2026) | USD 4.27 Billion |

| Market Size (2031) | USD 5.08 Billion |

| Growth Rate (2026 - 2031) | 3.53% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Nordic Corrugated Packaging Market Analysis by Mordor Intelligence

The Nordic corrugated packaging market size is projected to expand from USD 4.11 billion in 2025 and USD 4.27 billion in 2026 to USD 5.08 billion by 2031, registering a CAGR of 3.53% between 2026 to 2031. Growing e-commerce fulfillment centers, stringent regional bans on single-use plastics, and export-oriented food sectors that insist on fiber-based transit solutions are reshaping demand patterns. Sweden’s mature recycling loops, Denmark’s cold-chain build-out, and pan-Nordic seafood exports that prefer wet-strength grades collectively keep the Nordic corrugated packaging market on a steady upward track. Investments in water-efficient mills and digital inkjet presses are accelerating box customization while helping converters meet Nordic Swan Ecolabel criteria. Consolidation among pan-European integrators and alliances among mid-tier converters are boosting supply security and service reach across the Nordic corrugated packaging market.

Key Report Takeaways

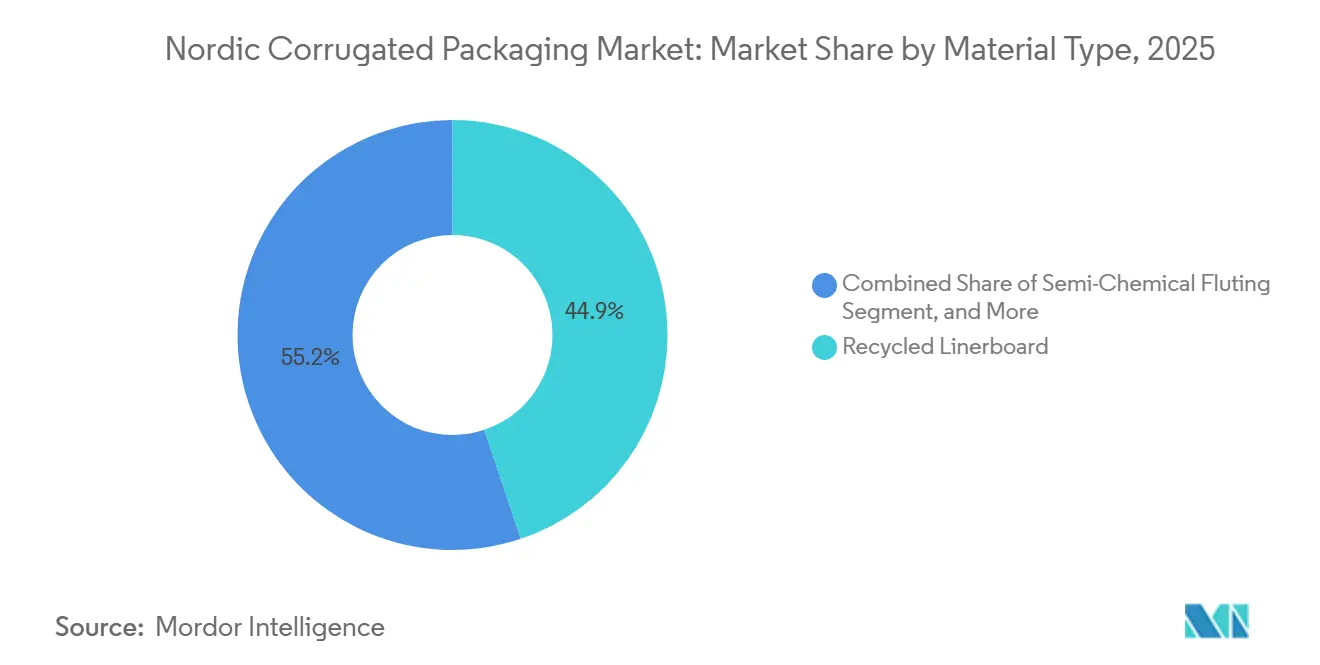

- By material type, the recycled linerboard segment captured 44.85% of the Nordic corrugated packaging market share in 2025.

- By flute type, the Nordic corrugated packaging market size for e flute is projected to grow at an 4.47% CAGR through 2031.

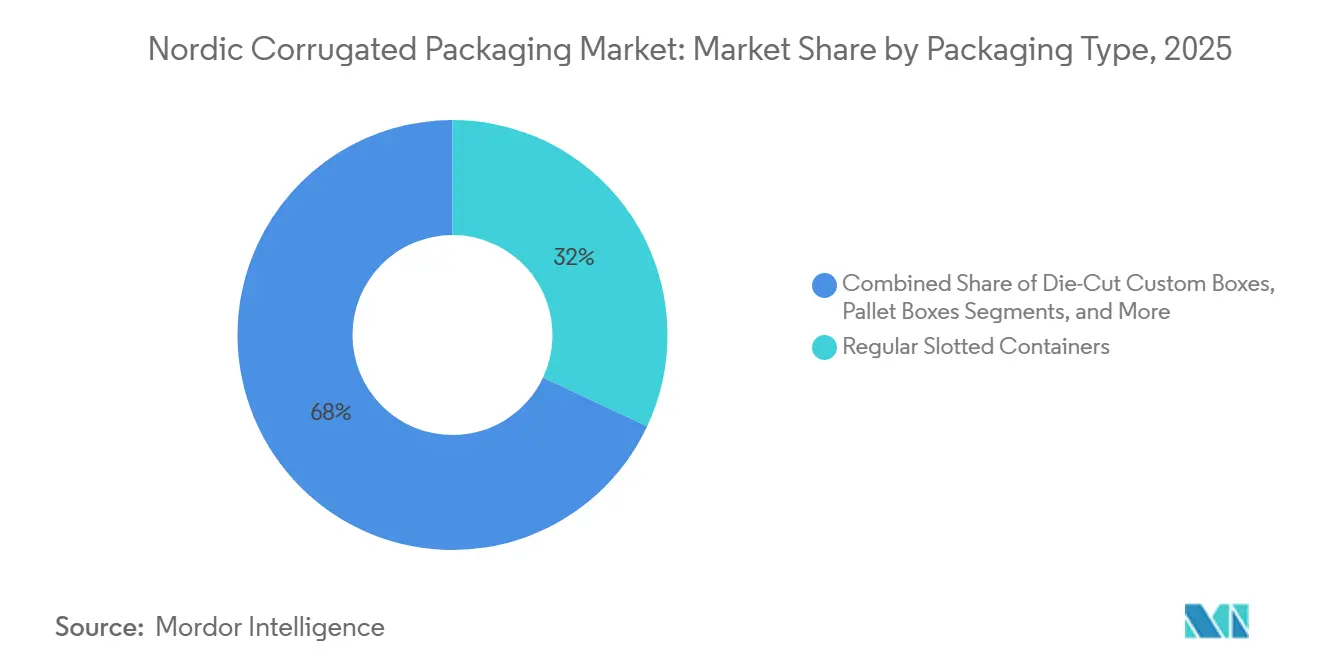

- By packaging type, the regular slotted containers segment captured 31.97% of the Nordic corrugated packaging market share in 2025.

- By wall type, the Nordic corrugated packaging market size for triple-wall is projected to grow at an 4.76% CAGR through 2031.

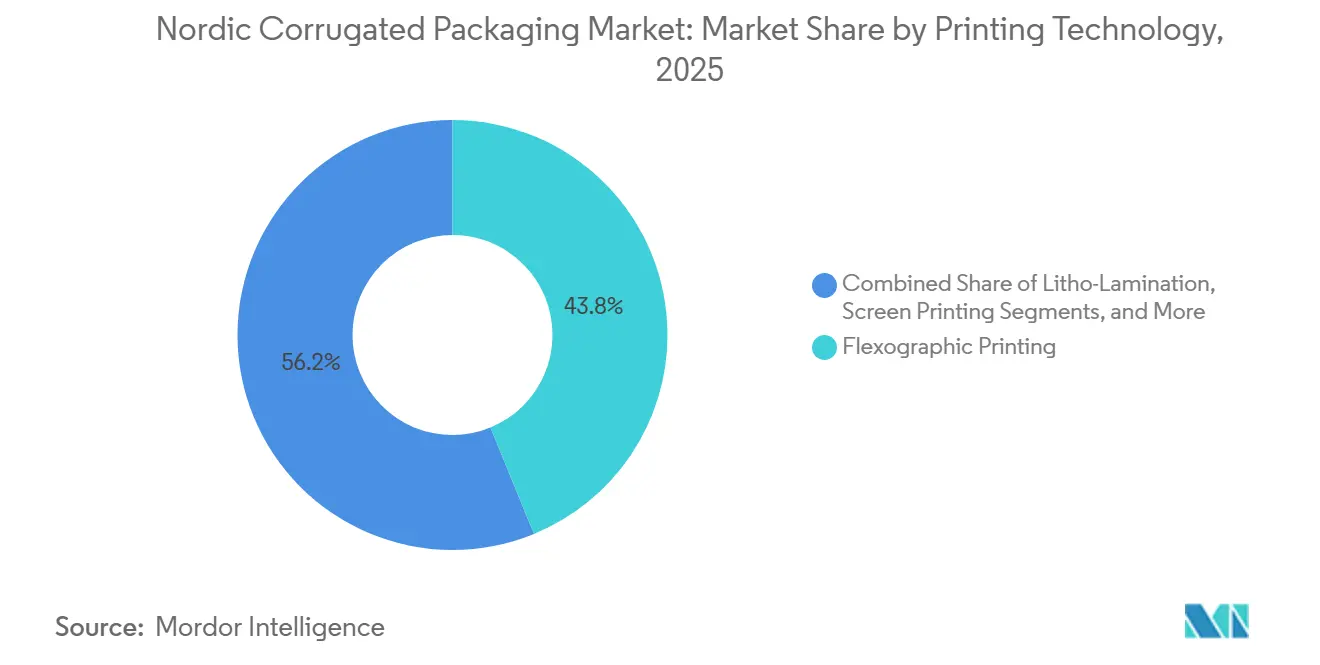

- By printing technology, the flexographic printing segment captured 43.81% of the Nordic corrugated packaging market share in 2025.

- By end-user industry, the Nordic corrugated packaging market size for pharmaceuticals is projected to grow at an 4.33% CAGR through 2031.

- By country, Sweden captured 34.68% of the Nordic corrugated packaging market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Nordic Corrugated Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising E-commerce Logistics Acceleration | +1.2% | Sweden, Denmark, Norway | Medium term (2-4 years) |

| Regulatory Shift Toward Recyclable Packaging | +0.9% | All Nordic countries, EU-wide | Long term (≥ 4 years) |

| Growth in Processed Food and Beverage Exports | +0.7% | Sweden, Denmark, Finland | Medium term (2-4 years) |

| Expansion of Nordic Seafood Exports Requiring Wet-Strength Grades | +0.4% | Norway, Iceland, Denmark | Medium term (2-4 years) |

| Nearshoring-Led Electronics Output | +0.3% | Sweden, Finland, Baltic partnerships | Short term (≤ 2 years) |

| Craft-Brewery Demand for Custom Boxes | +0.2% | Sweden, Denmark, urban centers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising E-Commerce Logistics Acceleration

Online grocery and non-food penetration keeps growing, shifting demand from pallet-load master cartons toward smaller automation-ready boxes that drop straight into last-mile networks. Smurfit WestRock engineered a collapsible box with reinforced corners and single-hand lids for Denmark-based Nemlig, enabling flat inbound delivery and automated erection within existing crate lines. Sweden’s household collection rates feed high-quality recycled liner back to Nordic corrugated packaging market converters, closing the fiber loop and lowering carbon intensity. Ranpak’s Cut’it EVO line rationalized eight box types down to one at Swedish fulfillment hubs, trimming void fill and freight volume. The EU Packaging and Packaging Waste Regulation, coming into force in 2026, imposes recyclability thresholds that reinforce the switch to fiber-based shippers.

Regulatory Shift Toward Recyclable Packaging

EU rules ban selected single-use plastics by 2030 and embed recycled-content quotas, prompting retailers and brand owners to pivot toward fiber solutions that secure eco-modulation fee discounts. Stora Enso’s EUR 1.1 billion (USD 1.24 billion) consumer board line in Oulu, Finland, produces kraftliners up to 33% lighter, slashing transport emissions while meeting direct food-contact rules. Nordic Swan Ecolabel criteria push converters to water-based inks that align with the Swiss Ordinance and Nestlé safety lists. These combined levers keep the Nordic corrugated packaging market firmly on a sustainability trajectory.

Growth in Processed Food and Beverage Exports

Inflation-driven demand for long-shelf-life foods is boosting frozen-meal and dairy exports from Sweden and Denmark, prompting a shift toward moisture-resistant corrugated alternatives to expanded polystyrene. VPK’s PetaFresh seafood boxes carry verified environmental product declarations that satisfy EU Ecolabel rules for transport packs. DS Smith’s DryPack grade withstands direct ice contact inside refrigerated containers bound for Asia, protecting Norwegian salmon from liner delamination. T-Emballage’s single-sheet 9-pack corrugated carrier meets Sweden’s farm-sales limits, illustrating how custom formats unlock craft-brewery exports.

Expansion of Nordic Seafood Exports Requiring Wet-Strength Grades

Norwegian salmon and Icelandic cod volumes keep climbing, with buyers demanding corrugated that survives ice melt and humidity spikes during intercontinental flight legs. Semi-chemical fluting combines virgin fiber strength with recycled content, delivering the wet resistance seafood shippers need. DS Smith and VPK ship pre-erected boxes certified under Nordic Swan, capturing share from plastic foam crates. Environmental product declarations for these grades enable exporters to document life-cycle gains for premium retailers in Japan and North America.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Recycled Paper Price Volatility | -0.6% | All Nordic countries, EU supply chain | Short term (≤ 2 years) |

| Competition from Returnable Plastic Crates | -0.4% | Sweden, Denmark, Norway | Medium term (2-4 years) |

| Water-Scarcity Constraints on Nordic Mills | -0.3% | Sweden, Finland, Norway | Long term (≥ 4 years) |

| Dependence on Imported Virgin Fiber | -0.2% | All Nordic countries | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Recycled Paper Price Volatility

Old corrugated container prices spiked in April 2025, squeezing converters on fixed-price supply contracts. Progroup’s waste-to-energy assets mute the hit, but Nordic independents without mill ownership saw EBITDA erosion and deferred digital-press upgrades. Smurfit WestRock plc wrote off USD 73 million in accelerated depreciation linked to EMEA mill closures to rebalance capacity. Converters are now negotiating fiber cost pass-through clauses and exploring vertical-integration partnerships that tie box output more tightly to liner supply.

Competition From Returnable Plastic Crates

Reusable plastic crates dominate Nordic grocery loops for high-rotation produce, boasting low per-trip costs when return distances are short. A Fraunhofer study cited by FEFCO confirms their carbon advantage below the 200-kilometer back-haul threshold.[1]FEFCO, “European Federation of Corrugated Board Manufacturers,” fefco.org Corrugated converters offer hybrid solutions, such as Smurfit WestRock’s crate-compatible box, which balances recyclability with automation. Shelf-ready displays and farm-sales formats, where single-use economics prevail, remain a bright spot for the Nordic corrugated packaging market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Recycled Linerboard Remains Anchor While Wet-Strength Grades Accelerate

Recycled linerboard held 44.85% of the Nordic corrugated packaging market share in 2025 as municipal collection systems in Sweden and Denmark fed high-quality post-consumer fiber back into local mills. Virgin Kraftliner services premium pharmaceutical and electronics loads that cannot risk contaminants, but its role is comparatively smaller and price-sensitive. Semi-chemical fluting is projected to post a 4.82% CAGR through 2031 as seafood exporters order wet-strength grades that retain crush resistance after ice contact.

Nordic corrugated packaging market size gains in this segment will also benefit from lighter-weight kraftliners made at Stora Enso’s Oulu line, which cut basis weight by one-third without sacrificing stiffness. Prices for imported virgin pulp remain vulnerable to currency swings, but American Industrial Partners’ 2026 takeover of International Paper’s Polish mills secures a regional softwood supply base. Klingele’s mills in Germany, France, and Brazil funnel virgin and recycled liners into its three Nordic plants, shielding customers from spot-market volatility.

By Flute Type: E Flute Gains Favour in Pharmaceuticals

B flute retained 38.41% share in 2025 by balancing cushioning with paper efficiency, fitting everyday e-commerce shippers and processed-food trays that enter automated erection lines. E flute, however, is forecast to grow at a 4.47% CAGR, as drug manufacturers favor its slim 1.5-millimeter profile, which accommodates more vials per pallet layer while still printing pharmacy barcodes crisply. Canon’s corrPress iB17 outputs 1200-dpi water-based graphics on E flute at 8,000 m² per hour, enabling Nordic converters to combine serialization and branding in a single inline pass.[2]PrintIndustry.news, “Canon corrPress iB17 Launch,” printindustry.news

A flute and double-wall hybrids still serve bulky electronics and glassware bound for regional fulfillment hubs, leveraging greater cushioning at modest material cost increases. Pharmaceutical 2-D matrix codes and temperature-sensitive inks require substrates with tight caliper control, a specification E flute effortlessly meets, further reinforcing its adoption curve. Packaging engineers now benchmark flute choice not only on edge-crush tests but also on optical scanning fidelity for traceability systems. Nordic converters thereby position E flute as the workhorse for high-value, data-rich shipments, narrowing B flute’s long-time dominance.

By Packaging Type: Displays Ride Retail Format Change

Regular slotted containers accounted for 31.97% of revenue in 2025 for everyday shipping, but point-of-purchase displays are on track for a 4.73% CAGR as Swedish farm sales rules unlock shelf-ready brewery boxes. T-Emballage’s nine-bottle pack assembles from a single sheet, meets the 3-liter legal cap, and showcases craft labels in retail coolers. Brands prize these displays for high-impact graphics and labor-saving shelf drops, which shorten replenishment time while amplifying impulse buys in urban supermarkets. Because display kits usually ship flat and erect in store, converters earn higher square-meter revenues on fewer liners, lifting overall Nordic corrugated packaging market share for premium die-cut formats.

DS Smith’s handle-equipped flat carrier was adopted by on-farm taprooms seeking recyclable gift packs. Such high-graphics displays lean heavily on digital inkjet, a capability spreading fast in the Nordic corrugated packaging industry. Pallet boxes remain essential for bulky industrial exports, but the value pool shifts toward lightweight display units as e-commerce platforms experiment with curated in-store pickup corners that rely on shelf-ready packs for rapid restock. This retail convergence ensures shelf-ready formats will continue to capture incremental Nordic corrugated packaging market share through 2031.

By Wall Type: Triple-Wall Supports Electronics Nearshoring

Single-wall boxes covered 32.76% of shipments in 2025, but triple-wall formats will expand at a 4.76% CAGR through 2031, riding a wave of electronics modules assembled in Baltic plants for Nordic and EU OEMs. Klingele’s Norrköping site laminates three flutes into pallet-sized crates that hit edge-crush targets above 200 lb/in, eliminating plastic corner posts. This performance leap positions triple-wall to capture a larger share of the Nordic corrugated packaging market within heavy-duty export corridors.

Progroup’s sheetfeeder + converter park in Germany trims lead times for Nordic customers who order custom triple-wall blanks. Double-wall stays relevant for beverage and processed-food export cases needing moderate stacking strength. As sustainability audits tighten, buyers note that cradle-to-gate CO₂ per kilogram shipped is lower in engineered triple-wall crates than in mixed-material crates, strengthening its claim to future gains in the Nordic corrugated packaging market.

By Printing Technology: Digital Inkjet Reaches Production Speed

Flexography retained 43.81% share in 2025, yet digital inkjet will rise 4.58% per year as run lengths shrink and SKU counts multiply. BHS-Agfa Jetliner Xceed runs 2.8-meter webs at 300 m/min using water-based inks, offering cost parity with flexo above 20,000 m². Those breakthroughs steadily elevate digital’s market share in Nordic corrugated packaging, especially in Denmark and Sweden, where craft-beer and cosmetics brands demand vivid, fast-changing artwork.

Koenig and Bauer Durst’s food-safe ink sets extend the addressable pool to point-of-sale displays and frozen-meal cartons. Screen and hybrid systems retain a sliver for very short runs, but the Nordic corrugated packaging market is clearly trending toward full-width single-pass inkjet. These efficiencies ensure digital technologies continue to expand their share of the Nordic corrugated packaging market, though legacy flexo will remain irreplaceable for commodity private-label cartons that crave bottom-cent prices.

By End-User Industry: Cold-Chain Pharma Sets the Pace

E-commerce maintained its lead with a 27.44% share in 2025, but pharmaceuticals will deliver the highest 4.33% CAGR as biologics pipelines lengthen and Nordic CDMOs expand freezer storage capacity. Digital print enables on-box serialization that meets EU traceability requirements, while E flute’s slim profile maximizes payload capacity in insulated shippers. Processed foods, beverages, and seafood remain volume bedrocks, but pharma’s value-weighted orders nudge average selling prices upward, cushioning converters from commodity price swings.

Processed foods and seafood exports remain volume mainstays, especially where semi-chemical fluting prevents delamination in icy holds. Craft beverages soak up point-of-sale displays, a niche set to expand under farm sales allowances. Personal-care and cosmetics brands leverage flush-cut E flute sleeves to replace laminated folding cartons, betting on recyclability claims to woo eco-oriented millennials. This diversified end-user matrix limits downside risk during cyclical slumps and stabilizes the outlook for Nordic corrugated packaging market size through 2031.

Geography Analysis

Sweden accounted for 34.68% of the Nordic corrugated packaging market revenue in 2025, with closed-loop recycling systems that provide abundant post-consumer fiber. National e-commerce operators automate box erection at scale, pushing demand for digitally printed single-wall formats. Denmark is projected to grow fastest at a 4.61% CAGR because pharmaceutical cold-chain hubs around Copenhagen contract out large volumes of E flute shippers tagged with variable data.

Norway’s seafood exporters specify wet-strength semi-chemical fluting for ice-packed salmon, securing a stable Nordic market for corrugated packaging and driving an uplift in triple-wall and specialty liner demand. VPK’s PetaFresh and DS Smith’s DryPack platforms continue to replace EPS foam cartons on Asia routes. Finland benefits from Stora Enso’s USD 1.24 billion Oulu line that back-integrates kraftliners for frozen-food cartons shipped across continental Europe.

Across every nation, the August 2026 EU recyclability deadline acts as the shared policy denominator, accelerating the cross-border pivot from single-use plastics to advanced corrugated designs. Iceland plays a smaller role but tops per-capita craft-beer exports, fostering boutique box runs that digital presses now serve profitably. The pending EU Packaging and Packaging Waste Regulation, aligned across Nordic parliaments, further harmonizes recycling targets and amplifies the collective pull toward fiber solutions.[3]EUWID Pulp and Paper, “Progroup,” euwid-paper.com

Competitive Landscape

The Nordic corrugated packaging market is moderately concentrated: the top five groups account for roughly 60% of regional box sales. Mondi’s 2025 purchase of Schumacher Packaging’s Western Europe plants added more than 1 billion m² of capacity and two solid-board mills, escalating vertical-integration pressure.[4]Mondi Group, “Acquisition of Schumacher Packaging,” mondigroup.com International Paper’s USD 2.47 billion goodwill write-down tied to the DS Smith deal signaled tough operating margins but also foreshadowed selective mill shuttering that could tighten containerboard supply.

Family-owned Klingele and VPK anchor the Blue Box Partners alliance, sharing mill output and logistics to match the service breadth of integrated majors while touting lower bureaucracy and sustainability credentials. Smaller independents, including Enklapack and Kroonpak, leverage design studios, rapid CAD sampling, and water-based digital presses to win short-run brewery and cosmetics orders. Technology investment therefore becomes a battlefield, as Canon’s corrPress, HP PageWide web presses, and BHS-Agfa Jetliner rigs push single-pass inkjet closer to flexography on speed and cost.

Technology partnerships, such as BHS-Agfa and Canon’s entrance with corrPress, are redrawing competitive lines around automation capabilities rather than sheer volume. Retail legislation and digital print economics together create white-space segments where agile converters can outmaneuver behemoths. Yet those behemoths still wield economies of scale in kraftliner and recycled-fiber sourcing, a key advantage whenever OCC prices swing sharply.

Nordic Corrugated Packaging Industry Leaders

Smurfit WestRock plc

International Paper Company

Mondi plc

Rengo Co. Ltd.

Model Holding AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Progroup secured Akarton as an on-site converter at its PW05 sheetfeeder in Schüttorf, restoring aligned board-to-box flow and trimming truck mileage within Germany’s Lower Saxony cluster.

- January 2026: American Industrial Partners finalized the purchase of International Paper’s Global Cellulose Fibers division, which includes Polish pulp assets vital to Nordic virgin-fiber imports.

- January 2026: VPK raised its equity stake in Ribble Packaging and reinforced capacity at its Halden plant, enhancing supply for wet-strength seafood boxes.

- October 2025: Canon introduced the corrPress iB17 single-pass inkjet press for corrugated sheets up to 1.7 m wide and 8 mm thick, rated for 8,000 m² h annualized to 15 million m².

Nordic Corrugated Packaging Market Report Scope

The Nordic corrugated packaging market is the regional industry in Sweden, Norway, Denmark, Finland, and Iceland that manufactures, processes, and distributes paper-based packaging materials made from fluted corrugated sheets. The market encompasses the production of various containerboard grades, including linerboard and fluting, which are converted into structural formats such as single-face, single-wall, and multi-wall boards.

The Nordic Corrugated Packaging Market Report is Segmented by Material (Virgin Kraft Linerboard, Recycled Linerboard, Corrugating Medium, Semi-Chemical Fluting, and Other Materials), Flute Type (A Flute, B Flute, C Flute, E Flute, and F Flute), Packaging Type (Regular Slotted Containers, Die-Cut Custom Boxes, Folding Cartons, Point-of-Purchase Displays, Pallet Boxes, and Other Packaging Types), Wall Type (Single-Wall, Double-Wall, Triple-Wall, and Single Face), Printing Technology (Flexographic Printing, Digital Inkjet Printing, Litho-Lamination, Screen Printing, and Other Printing Technologies), End-User Industry (Processed Foods, Fresh Food and Produce, Beverages, Electrical Products, Personal Care and Cosmetics, E-commerce Fulfillment Centers, Pharmaceuticals, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Virgin Kraft Linerboard |

| Recycled Linerboard |

| Corrugating Medium |

| Semi-Chemical Fluting |

| Other Materials |

| A Flute |

| B Flute |

| C Flute |

| E Flute |

| F Flute |

| Regular Slotted Containers |

| Die-Cut Custom Boxes |

| Folding Cartons |

| Point-of-Purchase Displays |

| Pallet Boxes |

| Other Packaging Types |

| Single-Wall |

| Double-Wall |

| Triple-Wall |

| Single Face |

| Flexographic Printing |

| Digital Inkjet Printing |

| Litho-Lamination |

| Screen Printing |

| Other Printing Technologies |

| Processed Foods |

| Fresh Food and Produce |

| Beverages |

| Electrical Products |

| Personal Care and Cosmetics |

| E-commerce Fulfillment Centers |

| Pharmaceuticals |

| Other End-User Industries |

| Sweden |

| Denmark |

| Norway |

| Finland |

| Iceland |

| By Material Type | Virgin Kraft Linerboard |

| Recycled Linerboard | |

| Corrugating Medium | |

| Semi-Chemical Fluting | |

| Other Materials | |

| By Flute Type | A Flute |

| B Flute | |

| C Flute | |

| E Flute | |

| F Flute | |

| By Packaging Type | Regular Slotted Containers |

| Die-Cut Custom Boxes | |

| Folding Cartons | |

| Point-of-Purchase Displays | |

| Pallet Boxes | |

| Other Packaging Types | |

| By Wall Type | Single-Wall |

| Double-Wall | |

| Triple-Wall | |

| Single Face | |

| By Printing Technology | Flexographic Printing |

| Digital Inkjet Printing | |

| Litho-Lamination | |

| Screen Printing | |

| Other Printing Technologies | |

| By End-User Industry | Processed Foods |

| Fresh Food and Produce | |

| Beverages | |

| Electrical Products | |

| Personal Care and Cosmetics | |

| E-commerce Fulfillment Centers | |

| Pharmaceuticals | |

| Other End-User Industries | |

| By Country | Sweden |

| Denmark | |

| Norway | |

| Finland | |

| Iceland |

Key Questions Answered in the Report

What is the projected Nordic corrugated packaging market size by 2031?

The market is forecast to reach USD 5.08 billion by 2031, up from USD 4.27 billion in 2026.

Which Nordic country will grow fastest in corrugated packaging through 2031?

Denmark is expected to post the quickest 4.61% CAGR, driven by cold-chain pharma investments and craft-brewery expansion.

Why is E flute gaining popularity among Nordic converters?

Thin profile, compatibility with water-based digital inkjet, and compliance with drug-serialization rules make E flute ideal for pharmaceutical and cosmetics cartons.

How are seafood exports shaping material choices?

Norwegian and Icelandic shippers specify semi-chemical fluting that resists ice melt, fueling a segment CAGR of 4.82% for wet-strength grades.

What technology trend is most disruptive to traditional flexo printing?

Full-width single-pass digital inkjet systems from Canon, BHS-Agfa, and HP push production speeds above 300 m/min, cutting plate costs and enabling variable-data graphics at scale.

How exposed are Nordic converters to recycled-paper price swings?

Firms without integrated mills face margin pressure when OCC prices spike, which shaved an estimated 0.6 percentage points off CAGR potential over the 2025-2026 window.

Page last updated on: