Non-muscle Invasive Bladder Cancer Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

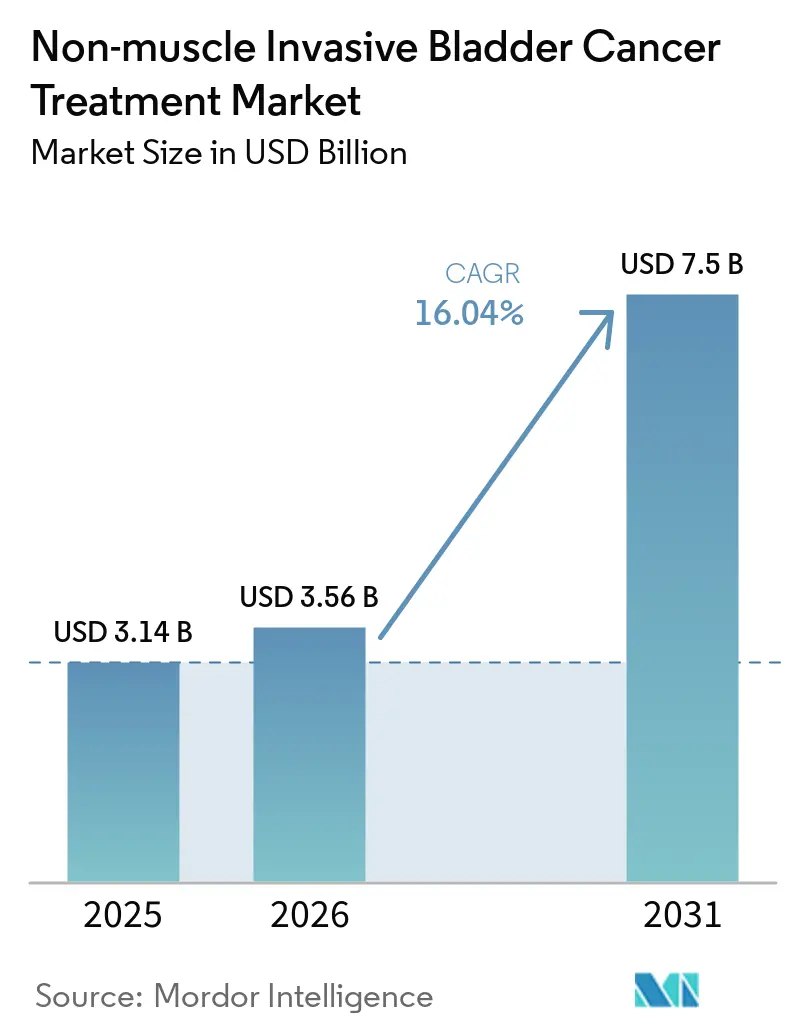

| Market Size (2026) | USD 3.56 Billion |

| Market Size (2031) | USD 7.5 Billion |

| Growth Rate (2026 - 2031) | 16.04% CAGR |

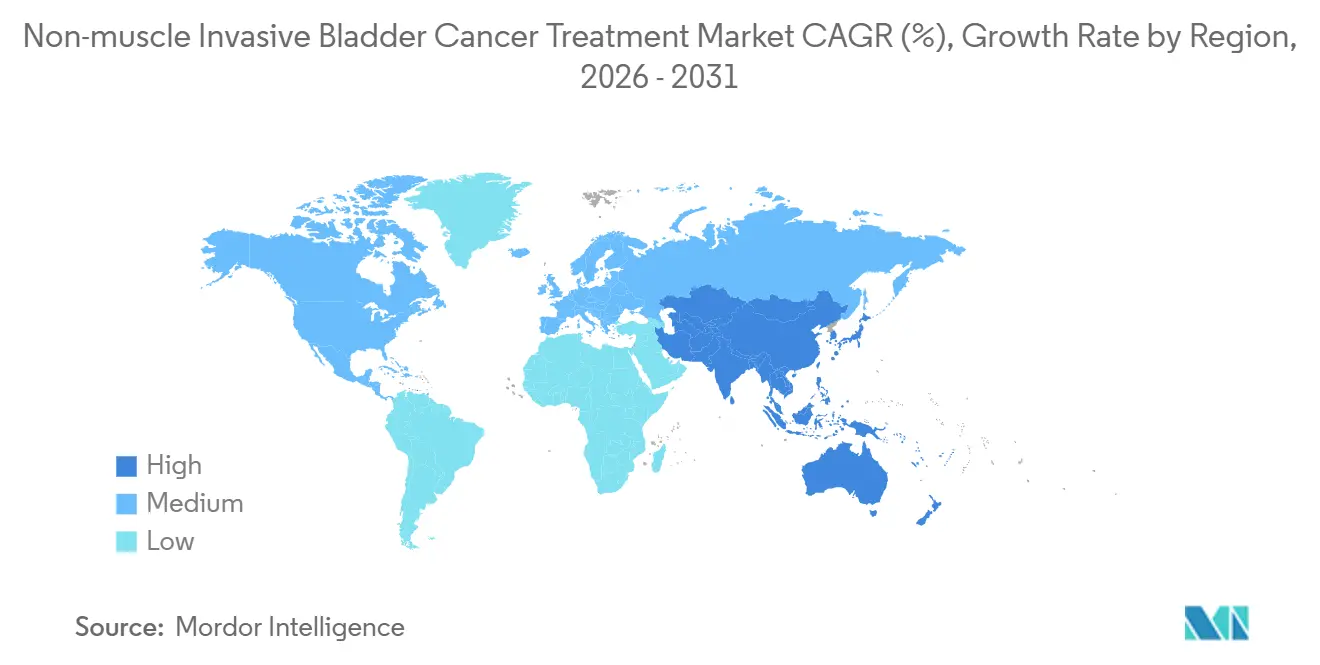

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Non-muscle Invasive Bladder Cancer Treatment Market Analysis by Mordor Intelligence

The Non-muscle Invasive Bladder Cancer Treatment Market size is projected to be USD 3.14 billion in 2025, USD 3.56 billion in 2026, and reach USD 7.5 billion by 2031, growing at a CAGR of 16.04% from 2026 to 2031.

A powerful combination of demographic aging, a sharp pivot toward immunotherapy and gene-based approaches, and mounting supply pressure on Bacillus Calmette-Guérin (BCG) is redrawing the competitive map. FDA approvals for sustained-release intravesical systems and cytokine-driven immunotherapies are compressing treatment timelines that once stretched across multiple catheterizations. Producers of recombinant BCG and adenoviral vectors are scaling bioreactor output to relieve chronic shortages, yet payers are scrutinizing five-figure price tags that dwarf legacy chemotherapy costs. Meanwhile, regional fast-track programs in China and India are expanding access to checkpoint inhibitors and low-cost mitomycin, reinforcing the market’s structural shift away from traditional, hospital-centric care.

Key Report Takeaways

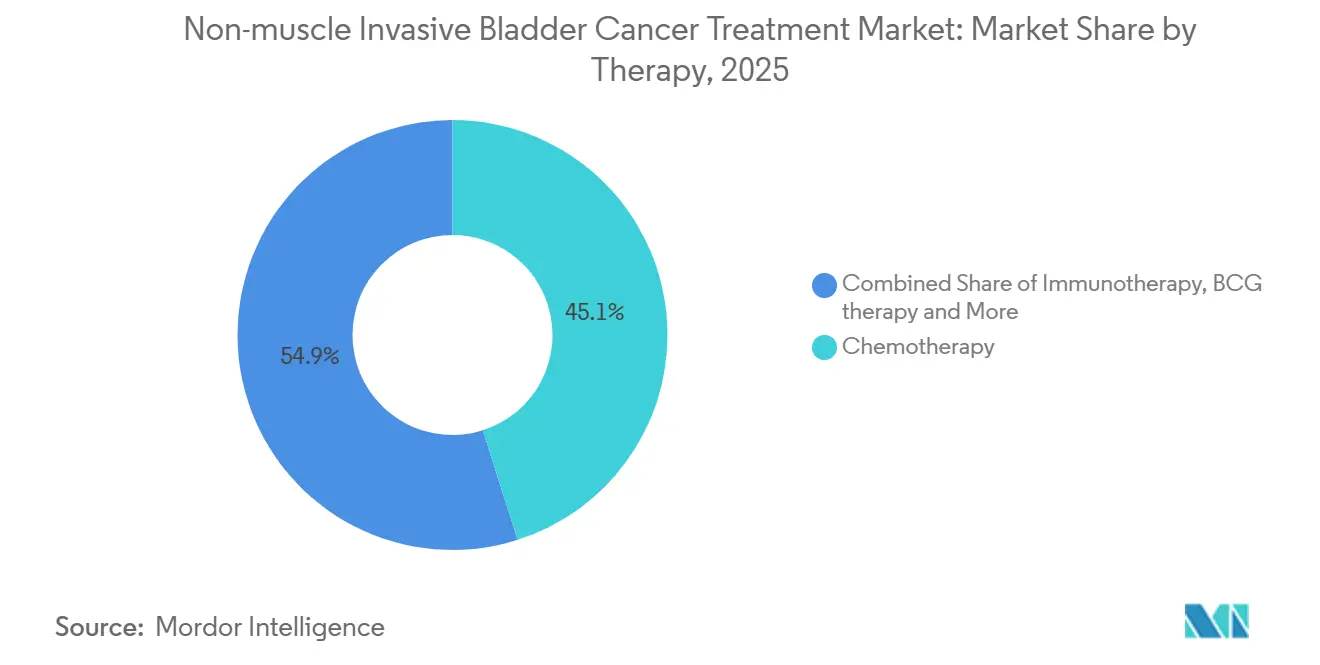

- By therapy class, chemotherapy led with 45.09% of non-muscle invasive bladder cancer treatment market share in 2025, while immunotherapy is forecast to grow at an 18.19% CAGR through 2031.

- By route, intravesical delivery captured 55.14% of the non-muscle invasive bladder cancer treatment market size in 2025 and is expected to expand at an 18.14% CAGR between 2026 and 2031.

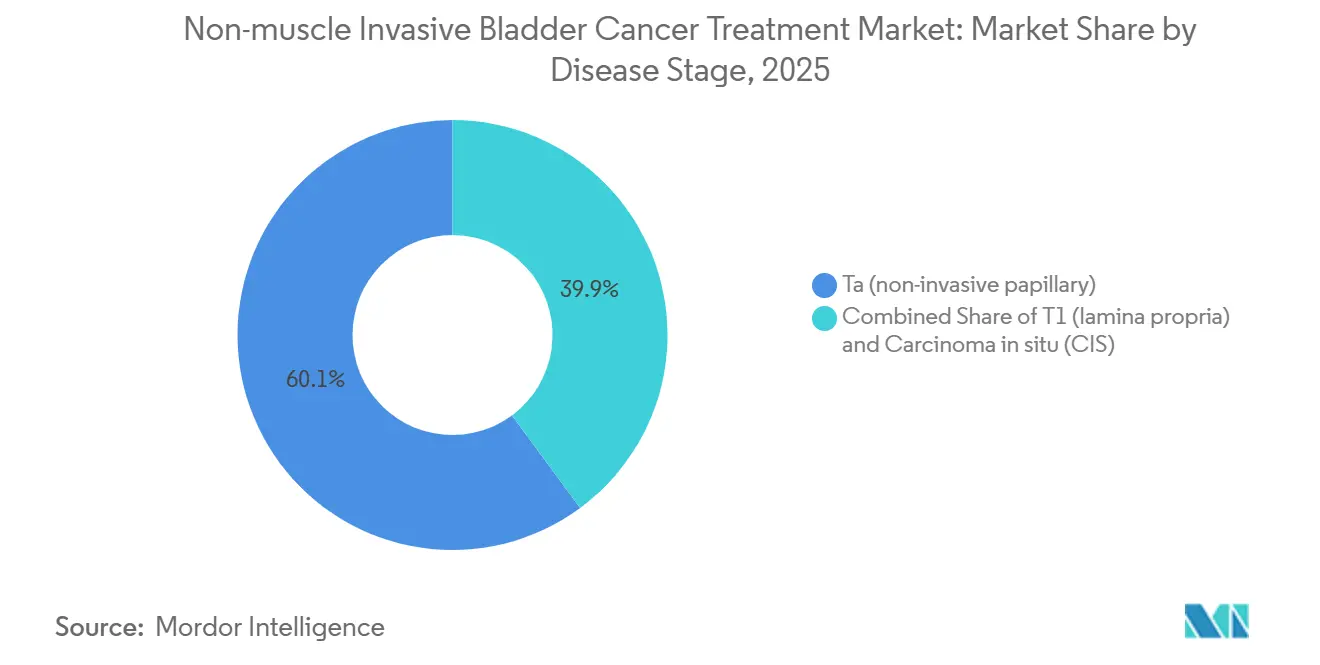

- By disease stage, Ta papillary tumors accounted for 60.12% of 2025 volume, whereas T1 lamina propria tumors will post a 17.16% CAGR through 2031.

- By end user, hospitals controlled 59.34% of 2025 revenue, but specialty clinics are on course to grow at 17.34% as single-dose gene therapies migrate to ambulatory settings.

- By geography, North America topped with 45.35% revenue in 2025, yet Asia-Pacific is projected to surge at an 18.3% CAGR to 2031, buoyed by Chinese and Indian regulatory catalysts.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Non-muscle Invasive Bladder Cancer Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Approvals expanding BCG-unresponsive care (gene therapy, IL-15, PD-1) | +4.2% | Global, with early adoption in North America & EU | Short term (≤ 2 years) |

| BCG supply constraints accelerating alternatives adoption | +3.1% | Global, most acute in North America & Asia-Pacific | Medium term (2-4 years) |

| Aging incidence base and high NMIBC share of bladder cancer | +2.8% | Global, pronounced in Europe & Japan | Long term (≥ 4 years) |

| Device-assisted intravesical therapy (HIVEC/EMDA) adoption | +2.3% | Europe core, expanding to APAC & Middle East | Medium term (2-4 years) |

| Drug-device sustained-release platforms | +2.0% | North America & EU, pilot programs in GCC | Short term (≤ 2 years) |

| Manufacturing scale-up (gene therapy, rBCG) de-bottlenecking access | +1.6% | Global, capacity concentrated in North America & EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Approvals Expanding BCG-Unresponsive Care

A wave of FDA and EMA clearances for nadofaragene firadenovec, ANKTIVA, and pembrolizumab is redefining the salvage pathway for patients who cannot mount a durable response to BCG[1]ImmunityBio, “ANKTIVA FDA Approval,” immunitybio.com. ANKTIVA’s IL-15 superagonism amplifies natural-killer cell infiltration, delivering a 62% 12-month complete response rate in the pivotal QUILT 3.032 study, twice the historical benchmark for single-agent chemotherapy. Ferring’s adenoviral p53 gene therapy addresses the TP53 mutation burden that drives 50% of high-grade tumors, while Breakthrough Therapy status for CG Oncology’s cretostimogene signals growing regulatory confidence in oncolytic platforms. Collectively, these approvals cut the lag between BCG failure and next-line therapy from 18 months to less than 6 months, mitigating the progression window that historically forced early cystectomy.

BCG Supply Constraints Accelerating Alternatives Adoption

Chronic shortages have prompted the American Urological Association to recommend gene therapy or checkpoint inhibitors as first-line options when BCG is unavailable. UroGen Pharma reported a 140% year-over-year jump in Jelmyto prescriptions during Q1 2025, underscoring a structural reordering of the treatment algorithm as physicians substitute earlier chemotherapeutic recourse for BCG-reliant pathways. Merck’s recombinant BCG, engineered in yeast to generate 15-fold higher yields, entered Phase II trials in 2024 and is on course for a 2027 launch, yet capacity gaps will persist until then. The shortfall is already funneling treatment-naïve patients into alternatives once reserved for salvage, permanently lifting baseline demand for immunotherapy.

Aging Incidence Base and High NMIBC Share of Bladder Cancer

Bladder cancer incidence rises sharply beyond age 65, and 75% of new diagnoses are non-muscle invasive, cementing a broad addressable base that mirrors global demographic aging. The WHO projects the ≥65 population to hit 1.5 billion by 2030, with the steepest gains in East Asia and Southern Europe[2]World Health Organization, “Global Health Observatory Data,” who.int. Japan recorded 21,000 new NMIBC cases in 2024, driven by cohorts born before 1960 and prolonged tobacco exposure. Elderly patients often carry comorbidities that complicate frequent catheterization, heightening interest in single-dose gene therapies and device-based regimens that lower procedural intensity. European frailty-adjusted algorithms now favor one-time vector infusions over six-week BCG induction for octogenarians, reinforcing demand for durable, low-touch solutions.

Device-Assisted Intravesical Therapy Adoption

Hyperthermic intravesical chemotherapy (HIVEC) and electromotive drug administration (EMDA) augment drug penetration, converting standard mitomycin into a premium therapeutic tier. A 2024 multicenter Italian study in European Urology cut 24-month recurrence to 28% with HIVEC-mitomycin versus 46% with mitomycin alone, prompting nationwide reimbursement across 120 centers. EMDA’s pulsed current, delivered via Physion’s device, is now installed in 85 EU hospitals. Capital costs of USD 180,000–250,000 per HIVEC unit remain a barrier, but shared-service consortia in the Netherlands and Belgium help diffuse equipment across satellite clinics, unlocking incremental capacity without duplicative spending.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost vs. legacy intravesical chemo/BCG | -2.4% | Global, most pronounced in price-sensitive APAC & Latin America | Medium term (2-4 years) |

| Limited durability/retreatment burden in some therapies | -1.8% | Global, affects all therapy classes | Long term (≥ 4 years) |

| Complex biologics manufacturing and cold-chain constraints | -1.3% | Emerging markets in APAC, MEA, and South America | Medium term (2-4 years) |

| Capital/staff needs for hyperthermia/EMDA devices slow uptake | -1.1% | Community urology practices in North America & Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Cost Versus Legacy Intravesical Chemo and BCG

Nadofaragene lists at USD 189,000 per course, while a six-week BCG induction costs USD 3,500–5,000 and generic mitomycin USD 400 per instillation, leaving a 30-fold price chasm that sparks payer pushback. Medicare covers gene therapy only after BCG failure and high-grade histology, excluding intermediate-risk Ta patients who make up 60% of incident cases. Outcomes-based contracts in the U.K. and Germany oblige manufacturers to rebate 40% of therapy cost if complete response is not achieved at 12 months, throttling early uptake. In India and Brazil, where out-of-pocket spending exceeds 50%, many patients default to generic chemotherapy or proceed directly to cystectomy.

Limited Durability and Retreatment Burden

Pembrolizumab achieved a 41% 12-month complete response in BCG-unresponsive carcinoma in situ, but only 46% of responders remained disease-free at 24 months, implying many will need additional therapy inside two years. Gene-therapy redosing protocols are uncharted, and cumulative immune-related toxicity hampers indefinite checkpoint inhibitor retreatment. Persistent surveillance cystoscopies every three months, each costing USD 1,500, erode the economic advantage of avoiding cystectomy. Combination regimens like TAR-200 plus nivolumab aim to raise durability yet add toxicity and cost, limiting adoption to academic centers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Therapy: Immunotherapy Gains Momentum Over Chemotherapy’s Installed Base

Chemotherapy accounted for 45.09% of non-muscle invasive bladder cancer treatment market share in 2025, anchored by mitomycin and gemcitabine. Yet immunotherapy is set to grow at 18.19% CAGR through 2031, reflecting earlier-line use of checkpoint inhibitors and IL-15 agonists. BCG therapy remains first-line for high-risk disease, but capacity limits crimp growth. Gene therapy commands a premium that translates into outsized revenue. Device-assisted hyperthermia systems logged 22% year-over-year gains in 2025, as European centers adopted Combat Medical’s BRS.

Immunotherapy’s ascent hinges on long-term data. Keynote-057 36-month readouts due in 2026 will determine if checkpoint blockade can forestall muscle invasion. Real-world nivolumab response rates trail clinical trials, revealing a gap between controlled and community settings. Gene therapy’s single-dose convenience resonates with frail elders, yet certification bottlenecks limit clinic participation. Chemotherapy will persist in low-income regions where biologic pricing remains prohibitive, but its growth is slowing as patent cliffs erode pricing power.

By Route of Administration: Intravesical Dominance Reinforced by Sustained-Release Devices

Intravesical delivery represented 55.14% of non-muscle invasive bladder cancer treatment market size in 2025 and is projected to expand at an 18.14% CAGR through 2031. TAR-200 condenses six catheterizations into a single cystoscopic insertion, freeing clinic slots and nursing capacity. RTGel extends mitomycin contact time sixfold, enabling weekly schedules that fit community practice. Systemic PD-1 inhibitors serve multifocal disease and patients unable to catheterize, but carry higher immune-related adverse-event risk. Oral PD-1 inhibitors in Phase II target non-catheterizable cohorts but must clear durability and safety hurdles before displacing intravesical standards.

The route split is increasingly biology-driven. Tumors with high PD-L1 expression trend toward systemic therapy, while papillary Ta disease favors resurfacing-focused intravesical options. Cold-chain requirements tilt gene therapy toward accredited centers, whereas sustained-release devices need only room-temperature storage, broadening their geographic reach.

By Disease Stage: T1 Lamina Propria Gains Share as High-Risk Substages Find New Options

Ta papillary tumors delivered 60.12% of 2025 treatment volume, but T1 lamina propria lesions will register a 17.16% CAGR to 2031 as cytokine-augmented regimens improve outcomes that once mandated cystectomy. ANKTIVA combined with BCG showed a 71% complete response in T1, surpassing control arms. Hyperthermic mitomycin quadrupled lamina propria drug penetration, favoring T1 disease, while gene therapy offers an organ-sparing path for carcinoma in situ sufferers long tethered to surveillance cystoscopy.

CIS, though only 15% of incidents, drives disproportionate resource use, requiring indefinite quarterly cystoscopy. Single-visit vector infusions and sustained-release scaffolds align with the tolerance thresholds of this chronically surveilled group. Physicians increasingly tailor therapy to tumor architecture, shifting away from one-size-fits-all protocols toward biomarker-guided staging algorithms.

By End User: Specialty Clinics Capture Growth as Therapies Migrate Out of Hospitals

Hospitals controlled 59.34% of 2025 revenue but specialty clinics will grow 17.34% through 2031, capturing gene-therapy and device-assisted demand. Nadofaragene’s catheter-based delivery needs only a treatment chair and freezer, letting community urologists bypass hospital credentialing. Regional gene-therapy hubs in Florida and Texas now draw patients from 100 miles and retain higher professional-fee margins than hospital outpatient departments.

Hospitals remain vital for complex T1 and CIS cases requiring imaging, biopsies, and tumor boards. Yet payers in capitated models are steering care to lower-cost ambulatory settings. Blue Cross Blue Shield of Massachusetts trimmed hospital-based nadofaragene reimbursement by 35% in 2025, hastening the outpatient shift and catalyzing nurse-practitioner-led TAR-200 insertions.

Geography Analysis

North America generated 45.35% of 2025 revenue, anchored by the United States’ spending on NMIBC therapies. Broad Medicare coverage, rapid FDA approvals, and high disposable incomes underpin adoption of premium biologics and devices. Yet payer pressure is mounting; outcomes-based contracts and site-of-service differentials are already nudging therapy into physician offices.

Europe captured a significant share of 2025 revenue, led by Germany, France, and the United Kingdom. EMA’s PRIME designation slashed launch timelines for nadofaragene, but divergent health-technology assessments create patchwork access. Germany granted full reimbursement in 2025, while France imposed a three-year registry, delaying uptake. Shared-service HIVEC consortia and expanded compassionate-use checkpoints in Spain illustrate Europe’s pragmatic drive to balance innovation with cost containment.

Asia-Pacific is the breakout region, forecast to grow at an 18.3% CAGR through 2031. China’s November 2024 approval of pembrolizumab for BCG-unresponsive CIS, combined with domestic PD-1 biosimilars priced at USD 8,000 annually, is democratizing access[3]China National Medical Products Administration, “Drug Approval Database,” nmpa.gov.cn. India’s 2025 mitomycin generic slashed per-vial prices to INR 12,000 (USD 145), expanding uptake in tier-2 cities. Japan’s aging cohort and universal insurance position it as the region’s second-largest market, but PMDA demands for local trials delay novel entrants. South Korea’s 40% price cut for pembrolizumab in 2025 and Australia’s 2026 TAR-200 approval round out an APAC region embracing both cost-effective generics and high-value sustained-release devices.

Competitive Landscape

The non-muscle invasive bladder cancer treatment market remains moderately fragmented, with the top five players, Merck, Bristol-Myers Squibb, Ferring, Johnson & Johnson, and Roche, collectively holding a significant share in 2025. Merck and BMS leverage established PD-1 franchises to accelerate entry, while Ferring dominates the nascent gene-therapy niche. Johnson & Johnson’s device-drug strategy differentiates it from classical pharmaco peers, anchoring growth in procedure-based revenue. Roche is repositioning atezolizumab in combination trials with intravesical scaffolds.

Pure-play innovators such as CG Oncology, ImmunityBio, and UroGen Pharma carve out durable positions by targeting BCG-unresponsive and high-risk substages with oncolytic viruses, IL-15 agonists, and thermosensitive gels. Patent filings reveal strategic moves toward combination regimens; Johnson & Johnson’s TAR-200 plus atezolizumab patent anticipates synergy between sustained intravesical gemcitabine and systemic PD-L1 blockade. Foundation Medicine’s liquid biopsy CDx opens a 20–30% margin diagnostic adjacency that may soon couple with therapy.

Biosimilar vectors and checkpoint inhibitors are expected post-2030, compressing price corridors and rewarding companies with integrated diagnostics-therapeutics platforms. Market entrants focused solely on single-product portfolios risk margin squeeze unless they lock in outcomes-based contracts or tap under-served geographies with low-cost manufacturing.

Non-muscle Invasive Bladder Cancer Treatment Industry Leaders

Bristol-Myers Squibb

Ferring Pharmaceuticals

Johnson & Johnson (Janssen)

Merck & Co.

F. Hoffmann-La Roche (Roche)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Johnson & Johnson reported positive Phase 1 data for an intravesical erdafitinib-releasing system in FGFR-altered NMIBC, signaling expansion beyond gemcitabine platforms.

- July 2025: FDA granted Priority Review to TAR-200 for BCG-unresponsive high-risk NMIBC with carcinoma in situ, accelerating the review clock to six months.

Global Non-muscle Invasive Bladder Cancer Treatment Market Report Scope

As per the scope of the report, non-muscle invasive bladder cancer (NMIBC) treatment refers to the medical approaches used to manage bladder cancer that is confined to the innermost layers of the bladder wall and has not invaded the muscular layer.

The segmentation of the non-muscle invasive bladder cancer treatment market is categorized by therapy, route of administration, disease stage, end user, and geography. By therapy, the market includes BCG therapy, chemotherapy, immunotherapy, gene therapy, and device-assisted intravesical treatments. By route of administration, it is segmented into intravesical and systemic (IV/oral). By disease stage, the segmentation covers Ta (non-invasive papillary), T1 (lamina propria), and carcinoma in situ (CIS). By end user, the market is divided into hospitals, specialty clinics, and ambulatory surgical centers. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| BCG therapy |

| Chemotherapy |

| Immunotherapy |

| Gene therapy |

| Device-assisted intravesical |

| Intravesical |

| Systemic (IV/Oral) |

| Ta (non-invasive papillary) |

| T1 (lamina propria) |

| Carcinoma in situ (CIS) |

| Hospitals |

| Specialty Clinics |

| Ambulatory Surgical Centers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Therapy | BCG therapy | |

| Chemotherapy | ||

| Immunotherapy | ||

| Gene therapy | ||

| Device-assisted intravesical | ||

| By Route of administration | Intravesical | |

| Systemic (IV/Oral) | ||

| By Disease Stage | Ta (non-invasive papillary) | |

| T1 (lamina propria) | ||

| Carcinoma in situ (CIS) | ||

| By End User | Hospitals | |

| Specialty Clinics | ||

| Ambulatory Surgical Centers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the non-muscle invasive bladder cancer treatment market today?

The non-muscle invasive bladder cancer treatment market size stands at USD 3.56 billion in 2026 and is projected to reach USD 7.50 billion by 2031.

Which therapy class is growing the fastest in non-muscle invasive bladder cancer?

Immunotherapy is forecast to expand at an 18.19% CAGR between 2026 and 2031, faster than any other class, as checkpoint inhibitors and cytokine-based agents move into earlier treatment lines.

What route of administration dominates current treatment?

Intravesical delivery controls 55.14% of 2025 revenue and remains the preferred route, helped by sustained-release platforms that cut down on catheterizations.

Why is Asia-Pacific the fastest-growing regional opportunity?

Fast-track Chinese approvals for pembrolizumab and India's launch of low-cost mitomycin generics underpin an 18.3% CAGR forecast for Asia-Pacific to 2031.

How do BCG shortages influence market dynamics?

Ongoing BCG supply constraints are accelerating the adoption of gene therapies and checkpoint inhibitors as first-line alternatives in both North America and Asia-Pacific.

Page last updated on: