Nigeria Construction Consulting Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

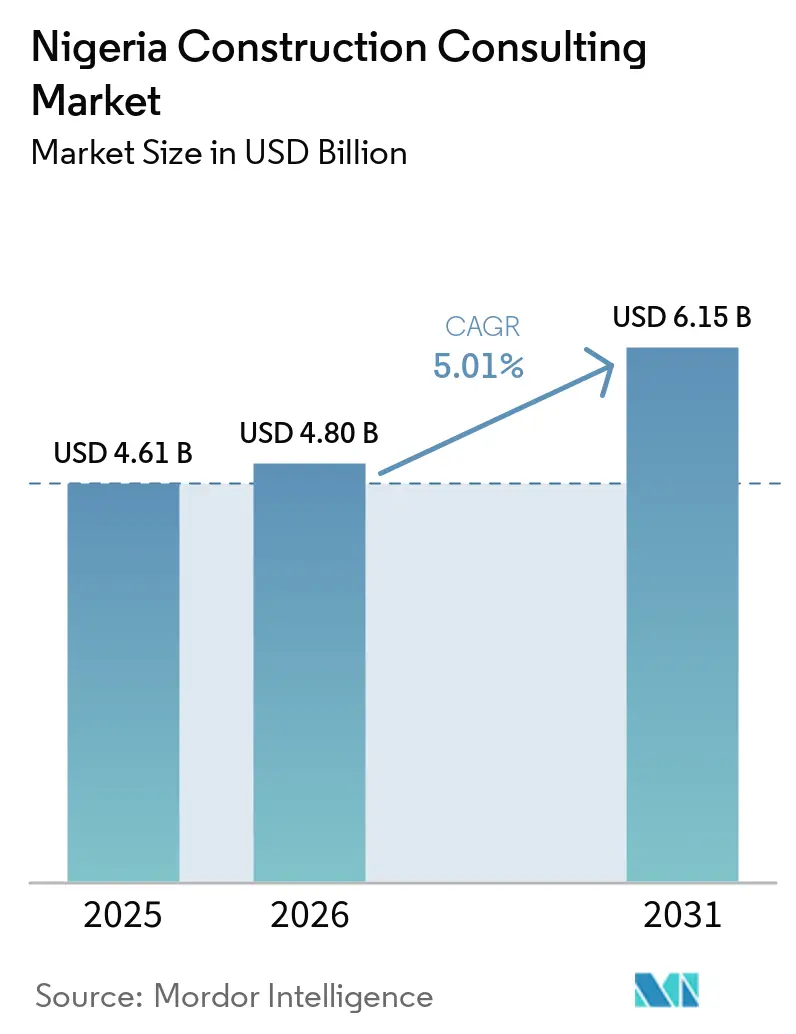

| Base Year Market Size (2025) | USD 4.61 Billion |

| Market Size (2026) | USD 4.80 Billion |

| Market Size (2031) | USD 6.15 Billion |

| Growth Rate (2026 - 2031) | 5.01% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Nigeria Construction Consulting Market Analysis by Mordor Intelligence

The Nigeria construction consulting market size is projected to expand from USD 4.61 billion in 2025 and USD 4.80 billion in 2026 to USD 6.15 billion by 2031, registering a 5.01% CAGR between 2026 and 2031. The federal government’s accelerating use of public-private partnerships, Lagos State’s USD 393.4 million 2024 infrastructure budget, and pension-fund diversification into project debt are broadening demand for advisory depth across feasibility, design, and project-management scopes. Consultants increasingly embed rapid-mobilization teams because the Infrastructure Concession Regulatory Commission (ICRC) now issues Outline and Full Business Case certificates in seven days, a timeline that favors firms with standardized toolkits. Currency turbulence remains a headline risk; the naira fell from 900 to 1,531 per USD during 2024 before modestly firming, squeezing fee margins on domestic contracts denominated in local currency yet backed by software subscriptions or expatriate salaries priced in dollars[1]Lagos Bureau of Statistics, “2024 Budget Focus on Infrastructure,” reuters.com. The USD 1 billion data-center build-out around Lekki, Ikeja, and Ikoyi is forcing advisers to add Uptime Institute Tier III/IV design skills, BIM clash detection, and on-site gas-turbine engineering to their core offerings, broadening the capability mix that clients now expect.

Key Report Takeaways

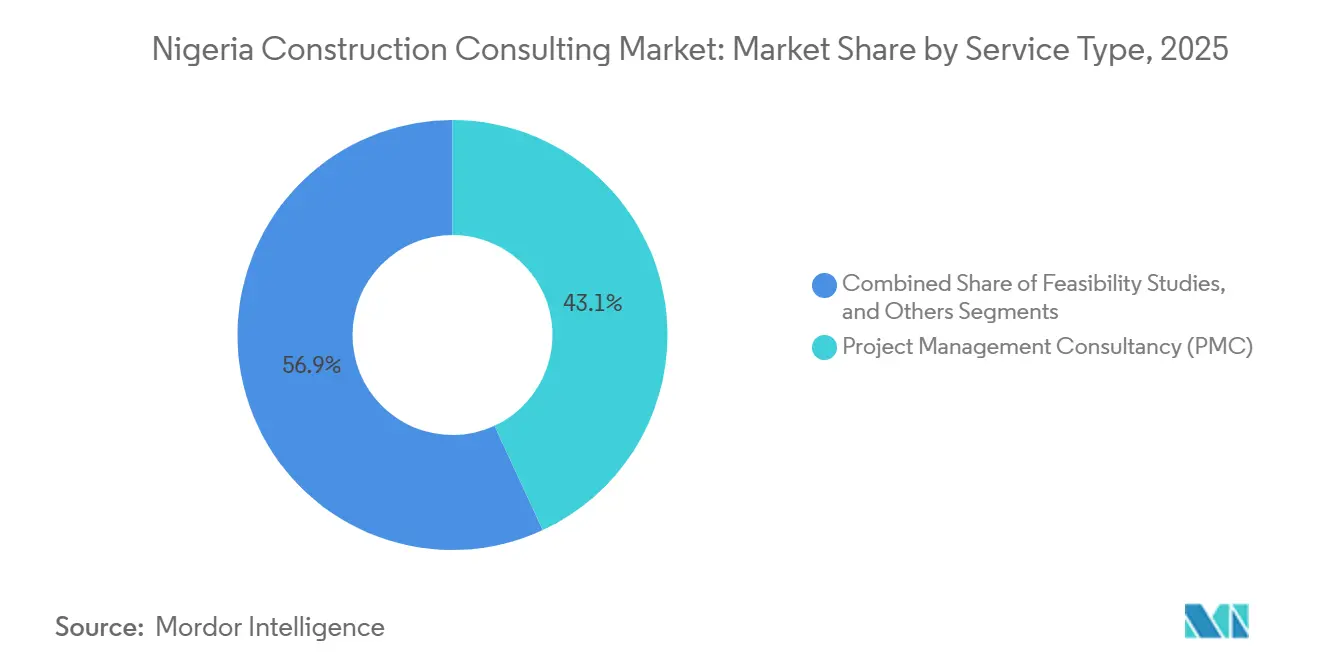

- By service type, project management consultancy held 43.10% of the Nigeria construction consulting market share in 2025, while detailed project reports are advancing at a 6.41% CAGR to 2031.

- By sector, residential consulting captured 39.45% revenue share in 2025; commercial engagements are forecast to expand at a 5.81% CAGR through 2031.

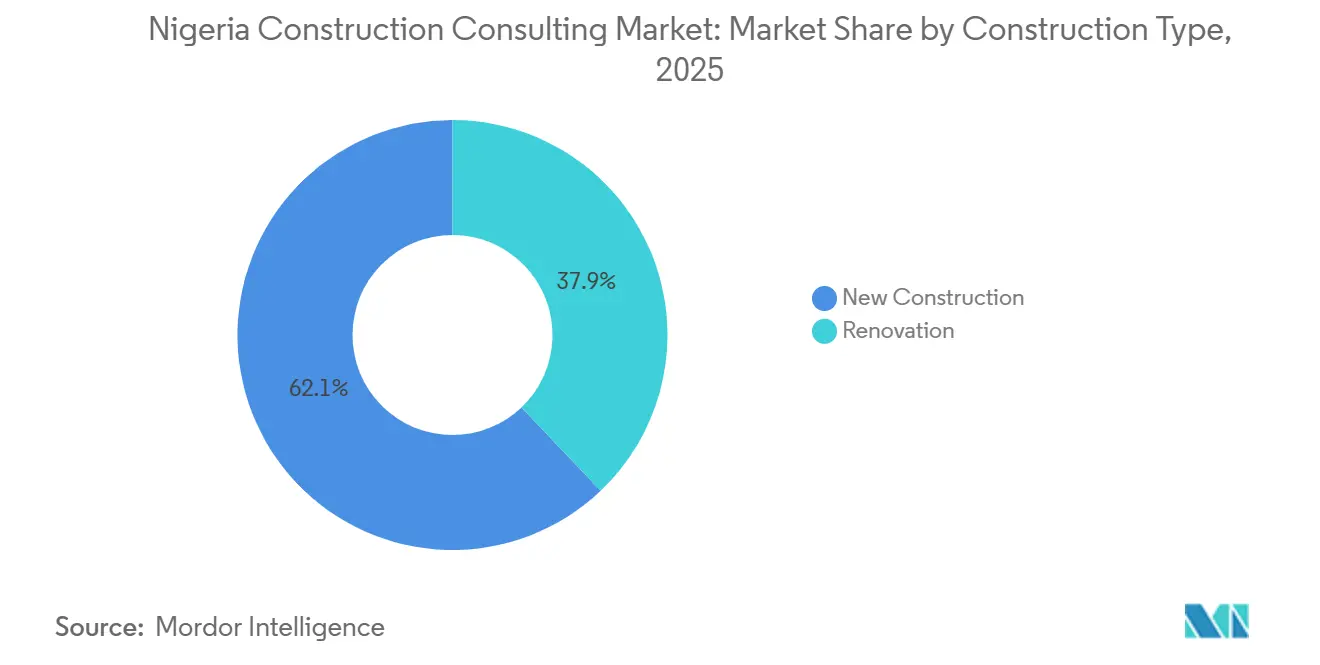

- By construction type, new-build activity accounted for a 62.10% share of the Nigeria construction consulting market size in 2025 and renovation work is projected to grow at a 6.06% CAGR to 2031.

- By investment source, public mandates represented 53.21% of 2025 expenditure, whereas privately financed projects will grow at a 5.96% CAGR between 2026 and 2031.

- By geography, Lagos led with 38.10% of 2025 revenue and is pacing the field at a 6.06% CAGR out to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Nigeria Construction Consulting Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| National Integrated Infrastructure Master Plan 2021-2043 enlarges project pipeline | +1.2% | Nationwide, concentration in Lagos, Abuja, Port Harcourt | Long term (≥ 4 years) |

| PPP reforms & Infraco financing de-risk concession advisory | +0.9% | Federal projects dominant, state adoption rising | Medium term (2-4 years) |

| Housing deficit & FMBN mortgage spur residential feasibility | +0.8% | Lagos, Abuja, Ibadan, Kano, Port Harcourt | Short term (≤ 2 years) |

| AfCFTA logistics corridors drive industrial master-planning | +0.6% | Coastal and border states | Long term (≥ 4 years) |

| Data-center boom in Lagos escalates MEP/BIM demand | +0.5% | Lekki, Ikoyi, emerging Abuja | Short term (≤ 2 years) |

| Diaspora “remote-build” trend fuels boutique PMC | +0.3% | Lagos and Abuja-centric | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

National Integrated Infrastructure Master Plan 2021-2043 enlarges project pipeline

The master plan quantifies a USD 2.3 trillion infrastructure gap and prioritizes USD 150 billion yearly outlays across transport, energy, housing, and ICT. Highway specifications now require reinforced concrete to minimize life-cycle maintenance, which lifts upfront engineering-design fees while compressing routine supervision margins. ICRC’s faster certification cadence means consultants are able to front-load multidisciplinary due diligence can monetize projects sooner. Big-ticket approvals USD 3 billion of new federal roads sanctioned during 2025 signal that aspiration is translating into executable mandates, yet the 50-project gap between certified and bankable concessions highlights lingering weaknesses in demand-tariff modeling.

PPP reforms & Infraco financing de-risk concession advisory

Mandatory insurance on PPP assets, quarterly audits, and a clarified division of roles between ICRC and the Bureau of Public Enterprises now give advisers a predictable regulatory runway. InfraCredit guarantees and the NGN 15 trillion (USD 10.7 billion) Infrastructure Fund reduce sponsor risk premia, pushing marginal schemes like the USD 2.5 billion Badagry Deep-Sea Port over the investment threshold. The USD 1.126 billion financing of Lagos-Calabar Coastal Highway Section 2 displayed how Gulf and multilateral lenders require ESG diligence aligned with Equator Principles, rewarding international consultancies with proven frameworks.

Housing deficit & FMBN mortgage spur residential feasibility

Nigeria’s 17–20 million-unit shortfall, plus Federal Mortgage Bank approvals that surged to USD 51.1 million in 2024 from USD 28.4 million in 2023, is catalyzing master-planning for mass-housing clusters. Government offtaker guarantees under Renewed Hope Cities ease developer balance-sheets, but investors now emphasize build-to-rent formats that shorten turnover, compressing design cycles and elevating modular-construction advisory. World Bank-funded land-title digitization reduces parcel delays, trimming costly feasibility reruns and favoring consultants skilled in GIS-enabled site screening.

AfCFTA logistics corridors drive industrial master-planning

Projects such as the USD 15.6 billion Abidjan–Lagos motorway and the Algiers–Lagos Trans-Sahara Highway recast Nigeria as a regional trade fulcrum. Advisory scope extends beyond transport engineering to customs-post layout, bonded‐warehouse design, and multi-modal integration that links forthcoming deep-sea ports to hinterland markets. Rising Industrial PMI—from 49.1 to 57.0 by late 2025—confirms latent warehouse demand, especially grade-B sheds close to ports where lower rents offset imperfect specifications.

Restraints Impact Analysis*

| Restraints | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Naira volatility & forex scarcity distort fee economics | -0.7% | Nationwide, Lagos and Abuja most exposed | Short term (≤ 2 years) |

| Public-sector payment delays erode cash-flows | -0.5% | Federal and state MDAs | Medium term (2-4 years) |

| Brain-drain of BIM/LEED talent constrains capacity | -0.4% | Lagos, Abuja | Long term (≥ 4 years) |

| State-level land-acquisition bottlenecks force re-work | -0.3% | Lagos, Rivers, Kano | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Naira volatility & forex scarcity distort fee economics

Sharp devaluation to 1,531 naira per USD upended fixed-price contracts denominated in local currency but tethered to imported software and expatriate payrolls. Although inflation moderated to 15.06% by February 2026, fuel costs still climbed above 50%, inflating site-visit budgets. Domestic firms lack hedging tools and often renegotiate mid-stream or exit loss-making mandates, whereas multinationals absorb swings through group treasuries. Exchange-rate uncertainty therefore nudges clients toward dollar-indexed PPP structures to ring-fence advisory budgets.

Public-sector payment delays erode cash-flows

Federal arrears reached USD 2.86 billion for 2024 contracts, and only USD 1.21 billion is budgeted for settlement in 2026, leaving a liquidity chasm. Consultants, typically paid only after contractors clear milestones, now seek advance-payment guarantees or pivot to private clients. While a presidential panel pledged to clear back-log by March 2026, historical slippage breeds skepticism and pushes advisory firms toward fee structures tied to financial close rather than post-construction certificates.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: DPR Rises as Lenders Demand Deeper Feasibility

Project management consultancy controlled 43.10% of the Nigeria construction consulting market share in 2025, reflecting decades of public-sector reliance on external supervision. Yet detailed project reports are forecast to grow at 6.41% CAGR, bolstered by multilateral lenders that mandate robust demand models, tariff analytics, and ESG baselines before disbursement. The Nigeria construction consulting market size attributable to DPR assignments is therefore set to outpace legacy PMC workstreams. International firms now deploy template DPR modules—traffic modeling engines, lifecycle-cost simulators—that compress delivery to match ICRC’s seven-day certification target.

Downstream, design-and-engineering fees are benefiting from the federal shift to concrete pavement on trunk roads, which increases structural-analysis complexity and raises billable hours per kilometer. Master-planning scopes remain modest in value but strategic; fiber backbones, edge data centers, and new special-economic zones require route optimization and zoning submissions that only a handful of specialists can deliver. As COREN compels foreign firms to staff Nigerian design offices, local-international joint ventures are emerging, subtly rebalancing competitive dynamics inside the broader Nigeria construction consulting market.

By Sector: Residential Dominates but Commercial Sets the Pace

Residential work captured 39.45% of 2025 revenue, anchored by mass-housing feasibility tied to a 17–20 million-unit supply gap. However, the commercial segment is advancing at a 5.81% CAGR, buoyed by USD 1 billion of data-center capital and adaptive-reuse projects in Ikeja that target shorter lease tenors. The Nigeria construction consulting market size tied to commercial builds will therefore expand faster than its residential counterpart. Investors chasing cloud-infrastructure demand require advisers conversant with Tier III/IV redundancy, power-purchase agreements, and Green Premium metrics.

Retail sub-formats are also fragmenting: neighborhood convenience centers are outperforming regional malls, triggering demand for lighter-spec design that emphasizes last-mile logistics. Consultants able to integrate loading-dock geometry, micro-fulfilment nodes, and traffic egress modeling into standard commercial blueprints are winning market share. Meanwhile, residential advisers pivot toward build-to-rent schemes financed by pension-fund vehicles, blending housing and income-yield dynamics into a hybrid asset class.

By Construction Type: New-Build Dominates, Renovation Accelerates

New construction accounted for 62.10% of 2025 activity, thanks to greenfield highways, ports, and housing estates. The Nigeria construction consulting market share attributable to renovation is smaller today but charting a 6.06% CAGR, led by Ikoyi and Victoria Island offices transitioning into mixed-use towers. ESG-conscious landlords turn to consultants for EDGE retrofits, solar-PV integration, and HVAC upgrades that lower operating costs and attract global tenants.

On the infrastructure side, structural-integrity assessments of third-mainland and Carter bridges exemplify how aging assets now demand specialized diagnostic consulting alongside rehabilitation design. Advisory scopes include traffic-flow diversion planning and asset-life modeling, services that command premium day rates compared with conventional supervision. As Nigeria’s asset base matures, the revenue balance inside the Nigeria construction consulting market will gradually tilt toward refurbishment, though fresh capex on greenfield corridors will keep new-build dominant into the early 2030s.

By Investment Source: Private Capital Gains in a Cash-Strapped Public Arena

Public agencies still procured 53.21% of 2025 advisory spend, yet arrears of USD 2.86 billion and constrained 2026 settlement budgets undermine trust. Private-sector outlays are running a 5.96% CAGR, elevating their proportion of the Nigeria construction consulting market size each year. Pension funds now steward USD 14.6 billion in assets, and regulators actively encourage infrastructure allocations, fostering a domestic institutional-capital pool.

Multilateral-backed blended-finance—exemplified by First Abu Dhabi Bank and Afreximbank’s underwriting of the Lagos-Calabar coastal link—offers consultants repeatable transaction templates. Fee security is higher because drawdowns sit in offshore escrow, insulating payments from local cash-call delays. Consequently, mid-tier firms actively court industrial free-zone sponsors and data-center developers rather than queue for ministry work.

Geography Analysis

Lagos accounted for 38.10% of 2025 revenue and will extend its lead at a 6.06% CAGR to 2031, fueled by the USD 1 billion data-center pipeline, Blue and Red urban-rail extensions, and the USD 1.126 billion Lagos-Calabar Coastal Highway Section 2 financing close. Industrial PMI climbed from 49.1 to 57.0 through 2025, signaling robust construction demand around Lekki’s free-trade corridors and spurring advisory mandates in logistics-warehouse design[2]Knight Frank, “H2 2025 Nigeria Real-Estate Outlook,” thenationonlineng.net. Adaptive reuse in Ikoyi and Victoria Island is accelerating renovation assignments, while decentralized business districts in Ikeja diversify workstreams beyond the island core.

Abuja’s consulting workload springs from a USD 266 million basket of roads, terminals, and Renewed Hope City access ways, yet chronic arrears—USD 2.86 billion in federal contractor debt—temper cash-flow certainty. The city’s reliance on public funding leaves advisers lobbying for PPP structuring to ring-fence payments. However, steady demand for medium-density housing still offers defensive volume.

Secondary cities such as Port Harcourt, Kano, and Calabar gain relevance through port, airport, and mining corridors. The USD 1.3 billion alumina refinery secured in March 2026 underscores mineral-sector diversification. AfCFTA-linked highways and border posts commissioned by the African Development Bank provide long-tail advisory prospects across multimodal transport and customs-post infrastructure. Consultants able to navigate multi-jurisdictional procurement and environmental clearance capture disproportionate margin on these cross-border schemes.

Competitive Landscape

Competition is fragmented: global majors such as AECOM, Arup, WSP, Mott MacDonald, and Stantec contest mandates alongside Julius Berger Consulting, Novatia, and Pandrock Associates. International firms leverage ESG credentials and structured-finance experience to dominate marquee PPP concessions, exemplified by Arup’s Lagos Water Partnership and advisory roles on the coastal highway[3]Arup, “Lagos Water Partnership,” arup.com. Domestic specialists counter with local-content fluency and construction-contractor linkages that compress design-build feedback loops; Julius Berger’s Second Niger Bridge execution feeds proprietary cost-database advantages.

Brain-drain remains a structural headwind, raising wage floors for BIM and LEED skill sets. COREN’s expatriate-quota rules compel foreign practices to embed knowledge-transfer programs, spawning joint ventures that blend global process rigor with local statutory insight. Tech adoption differentiates players: firms investing in parametric design software and drone-enabled site progress tracking win scheduling points when ICRC compresses approval timelines.

Strategically, data-center build-outs have triggered a race for Uptime-certified engineer recruitment. Equinix’s USD 140 million West Africa expansion saw advisers fast-track Tier IV topology validation under aggressive delivery milestones. At the opposite end, boutique PMCs monetize diaspora remote-build oversight through mobile-app photo logs and escrow-tied disbursement approvals, segments large firms consider sub-economic but cumulatively significant inside the wider Nigeria construction consulting market.

Nigeria Construction Consulting Industry Leaders

AECOM Nigeria

Arup Nigeria

WSP Nigeria

Mott MacDonald Nigeria

Jacobs Nigeria

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Nigeria and Africa Finance Corporation signed a USD 1.3 billion deal to build an alumina refinery processing 1 million t of bauxite annually, launching a nationwide mineral-mapping program.

- December 2025: Federal Government closed USD 1.126 billion financing for Lagos-Calabar Coastal Highway Phase 1, Section 2; advisers included SkyKapital, Earth Active UK, Hogan Lovells, and Templars.

- February 2025: Federal Executive Council approved concession of Kashimbila Integrated Cargo/Agro-Allied Airport, covering a 3,000-hectare farm and free-trade zone

Nigeria Construction Consulting Market Report Scope

| Project Management Consultancy (PMC) |

| Feasibility Studies |

| Detailed Project Reports (DPR) |

| Design & Engineering Services |

| Master Planning & Other Services |

| Residential | |

| Commercial | Office |

| Retail | |

| Industrial and Logistics | |

| Data Center | |

| Others - Institutional, Hospitality etc. | |

| Infrastructure/Civil | Transportation Infrastructure (Roadways, Railways, Airways, others) |

| Energy & Utilities | |

| Social Infrastructure | |

| Others |

| New Construction |

| Renovation |

| Public |

| Private |

| Lagos |

| Ahuja |

| Rest of Nigeria |

| By Service Type | Project Management Consultancy (PMC) | |

| Feasibility Studies | ||

| Detailed Project Reports (DPR) | ||

| Design & Engineering Services | ||

| Master Planning & Other Services | ||

| By Sector | Residential | |

| Commercial | Office | |

| Retail | ||

| Industrial and Logistics | ||

| Data Center | ||

| Others - Institutional, Hospitality etc. | ||

| Infrastructure/Civil | Transportation Infrastructure (Roadways, Railways, Airways, others) | |

| Energy & Utilities | ||

| Social Infrastructure | ||

| Others | ||

| By Construction Type | New Construction | |

| Renovation | ||

| By Investment Source | Public | |

| Private | ||

| By Key Cities | Lagos | |

| Ahuja | ||

| Rest of Nigeria | ||

Key Questions Answered in the Report

How large is the Nigeria construction consulting market in value terms for 2026?

It is estimated at USD 4.80 billion for 2026.

What CAGR is forecast for the sector between 2026 and 2031?

The market is projected to post a 5.01% CAGR over the period.

Which service type is expanding the fastest?

Detailed project reports are growing at 6.41% CAGR through 2031.

Why are commercial projects gaining share?

USD 1 billion of data-center investment and adaptive-reuse retail formats are lifting commercial consulting demand at a 5.81% CAGR.

How significant is Lagos to overall consulting revenue?

Lagos contributed 38.10% of 2025 fees and is forecast to maintain 6.06% CAGR, the fastest among Nigerian cities.

Page last updated on: