Niacinamide Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.29 Billion |

| Market Size (2031) | USD 1.98 Billion |

| Growth Rate (2026 - 2031) | 8.85% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

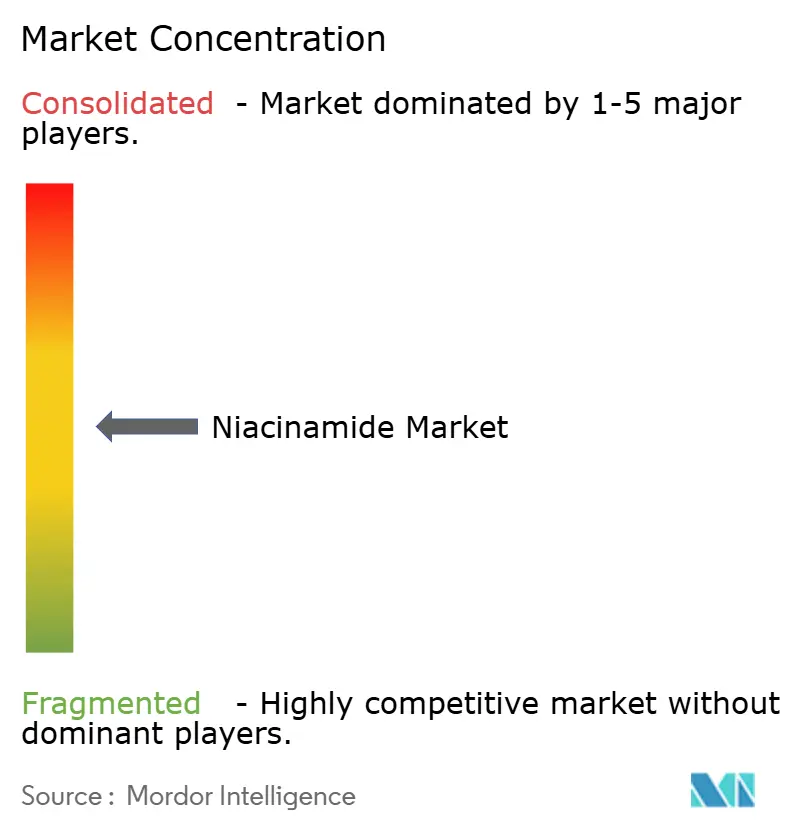

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Niacinamide Market Analysis by Mordor Intelligence

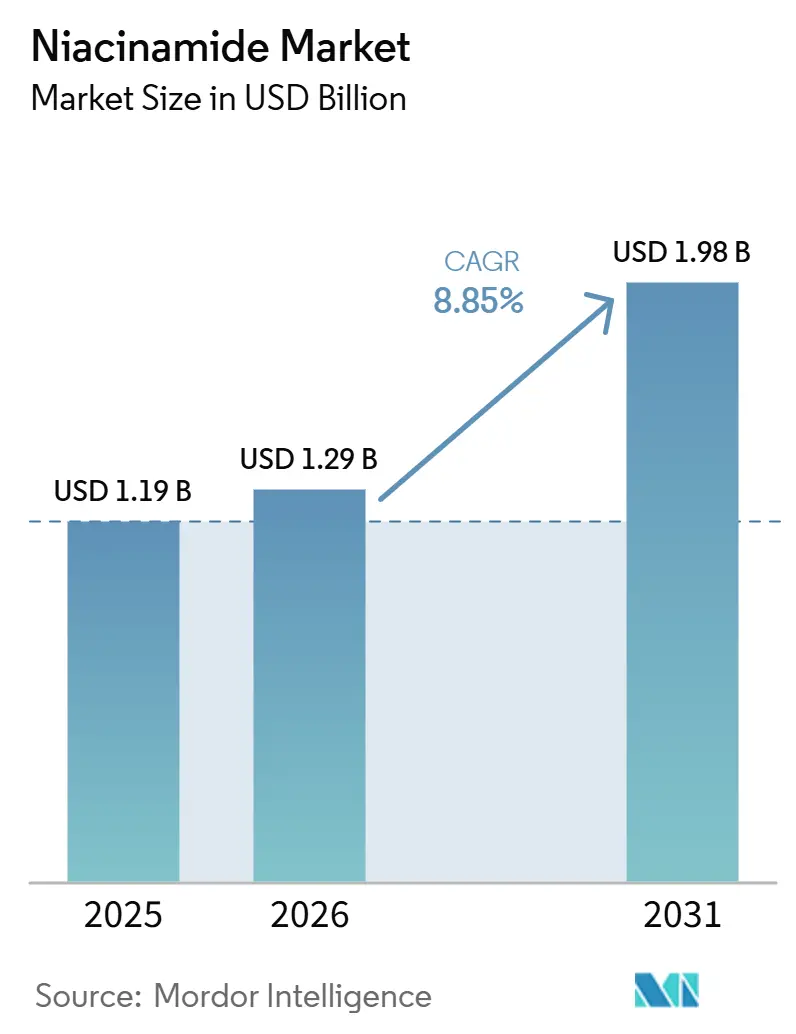

The Niacinamide Market size is expected to grow from USD 1.19 billion in 2025 to USD 1.29 billion in 2026 and is forecast to reach USD 1.98 billion by 2031 at 8.85% CAGR over 2026-2031.

The Niacinamide market is growing across several demand pools because the ingredient serves pharmaceutical, cosmetic, food fortification, nutraceutical, and animal nutrition uses at the same time. This broad use base makes the Niacinamide market less exposed to swings in any single downstream category, and it also supports a more stable procurement cycle for qualified suppliers. Demand is also moving toward higher specification material, especially where purity, residual control, and documentation matter for premium skincare and pharmaceutical positioning. Supply conditions are changing at the same time, with European portfolio exits and Asian manufacturing scale altering supplier relationships and making long-term sourcing decisions more important for buyers. The Niacinamide market also shows a clear value shift toward premium grades and better documented supply, which is where margin protection appears stronger than in commodity volume tiers.

Key Report Takeaways

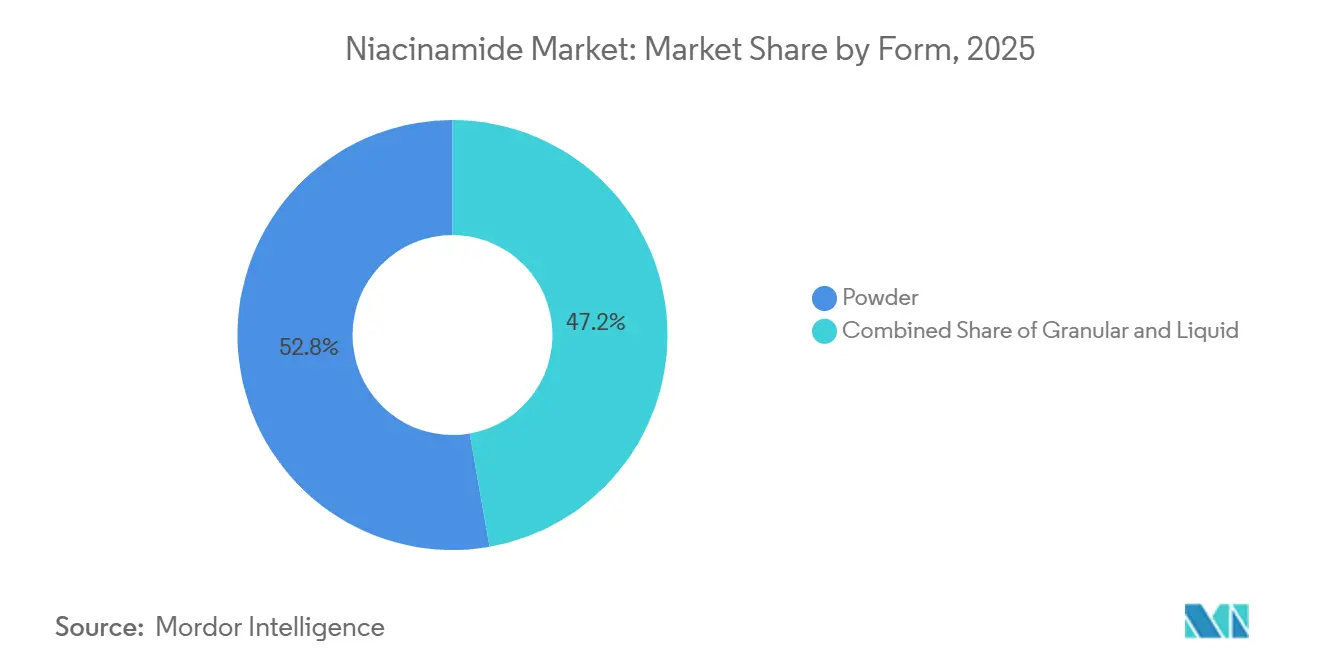

- By form, powder held 52.76% share of the Niacinamide market size in 2025, while liquid is forecast to grow at a 9.77% CAGR through 2031.

- By grade, pharmaceutical grade led with 38.13% of market value in 2025, while cosmetic grade is projected to expand at a 10.23% CAGR through 2031.

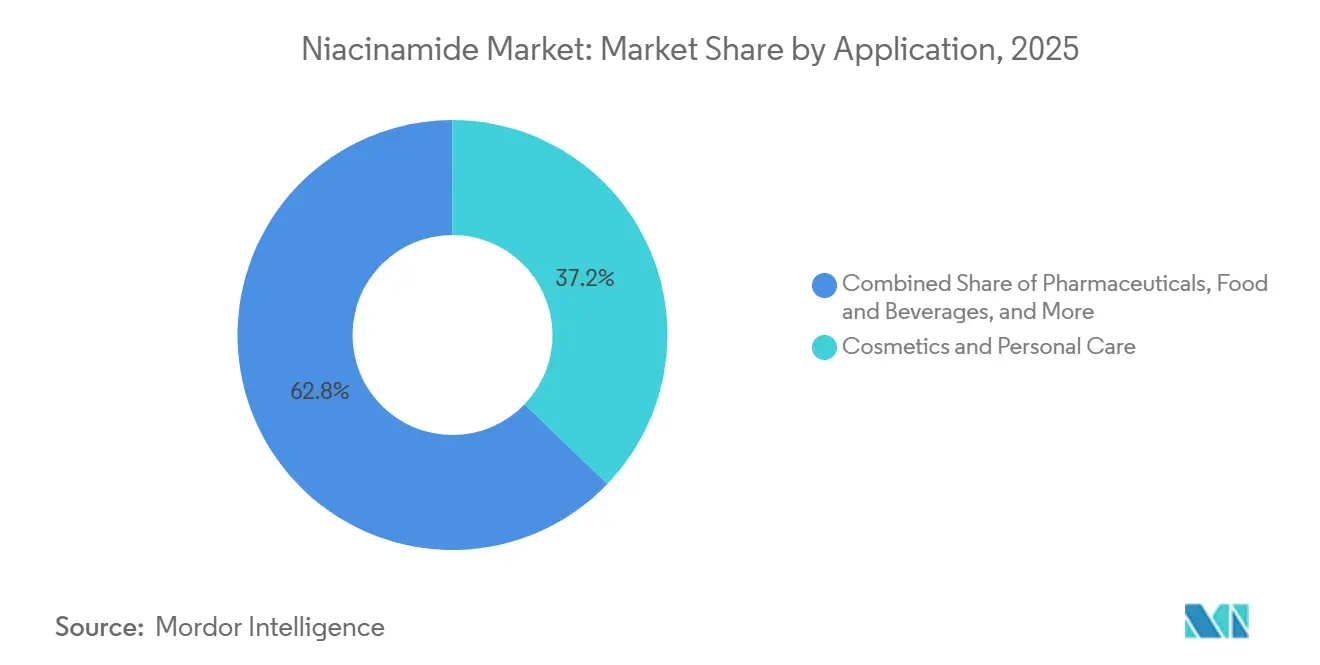

- By application, cosmetics and personal care accounted for 37.18% of market value in 2025, while human nutrition is expected to advance at a 9.91% CAGR through 2031.

- By end user, cosmetic manufacturers held 35.13% of market value in 2025, while nutraceutical companies are set to record the highest CAGR at 10.36% through 2031.

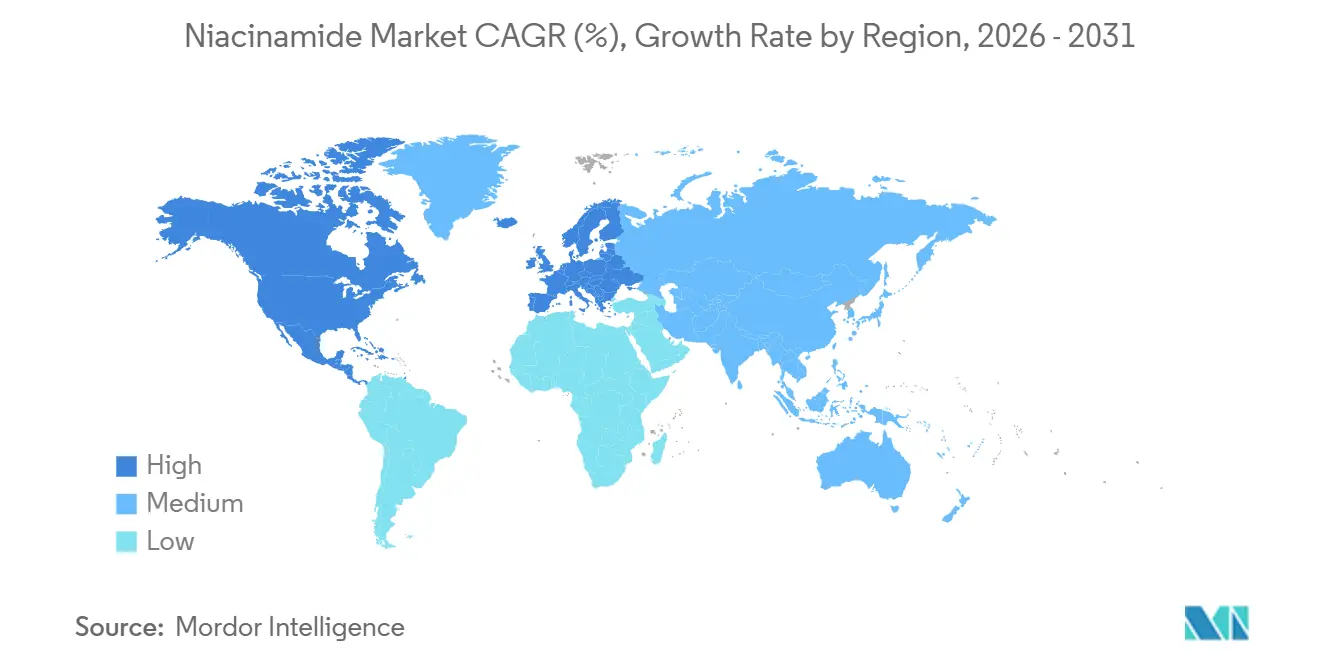

- By geography, Asia-Pacific held 42.15% of the Niacinamide market share in 2025, while North America is forecast to grow at a 9.69% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Niacinamide Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding Dermatology-Backed Skincare Adoption | +2.8% | Global, concentrated in North America, EU & North Asia | Short term (≤ 2 years) |

| Growth in Pharmaceutically Positioned Niacinamide Use | +1.9% | North America, EU, India | Medium term (2-4 years) |

| Food Fortification and Nutraceutical Label Expansion | +1.6% | Asia-Pacific, MEA, Latin America | Medium term (2-4 years) |

| Capacity Expansion in Asia-Based Manufacturing Clusters | +1.2% | APAC core, spill-over to MEA & Latin America | Long term (≥ 4 years) |

| Direct-to-Consumer Ingredient Storytelling and Clinical Claim Validation | +0.9% | North America, EU, South Korea | Short term (≤ 2 years) |

| Supply-Chain De-Risking Through Multi-Sourcing and Regional Stocking | +0.7% | Global, with early gains in India & Southeast Asia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expanding Dermatology-Backed Skincare Adoption

The Niacinamide market is benefiting from stronger dermatology support because the ingredient is no longer treated as a simple vitamin additive in skincare. A 2025 randomized trial in Dermatology and Therapy also supported niacinamide use for preventing post inflammatory hyperpigmentation in skin of color populations, which broadens the clinical relevance of the ingredient across more consumer groups. That combination of barrier support, pigment management, and broad patient relevance helps the Niacinamide market retain formulation space even as other actives receive strong marketing attention. The Niacinamide market is also supported by regulatory familiarity in cosmetics, which lowers reformulation risk for brands and makes supplier qualification more straightforward. As brands build lines around clinically recognized actives, the Niacinamide market gains from repeat use in serums, moisturizers, sunscreens, and adjacent personal care formats.

Growth in Pharmaceutically Positioned Niacinamide Use

The Niacinamide market is also being supported by its role in more pharmaceutically positioned applications, where buyers place greater weight on compliance, purity, and supply assurance. The draft points to growth beyond traditional deficiency treatment into NAD+ related uses, oncology support settings, and prescription dermatology, which raises the value profile of pharmaceutical grade material within the Niacinamide market. This matters because pharmaceutical demand tends to support stronger pricing discipline than mass cosmetic or feed channels, especially when cGMP status and batch documentation are part of supplier approval. The Niacinamide market is therefore seeing a more visible split between commodity output and higher specification supply that can serve regulated or closely supervised applications. That split is reinforced by the need for traceable distribution channels and better qualified manufacturers once downstream buyers move away from generic sourcing. The result is a Niacinamide market where pharmaceutical positioning supports both demand depth and a more defensible premium tier.

Food Fortification and Nutraceutical Label Expansion

The Niacinamide market is gaining another layer of support from food fortification programs and from the expansion of supplement labels that position vitamin B3 within broader wellness claims. The European Union food fortification framework remains important because Regulation (EC) No 1925/2006 and the 2023 update that added nicotinamide riboside chloride show that the niacin category is widening rather than narrowing in food use.[1]European Commission, “Regulation (EC) No 1925/2006 on the Addition of Vitamins and Minerals to Foods,” EUR-Lex, eur-lex.europa.eu That supports the Niacinamide market because established niacinamide demand can grow alongside newer niacin forms instead of being displaced by them. The fastest end-user growth in the draft comes from nutraceutical companies, and that fits with a supplement channel that is moving from basic nutrition toward more targeted energy, skin, and metabolic health narratives. The Niacinamide market also benefits when public health nutrition needs and premium consumer supplement demand rise at the same time, because those two demand streams respond to different economic triggers. This makes the Niacinamide market more balanced than ingredients that depend only on discretionary beauty spending.

Capacity Expansion in Asia-Based Manufacturing Clusters

The Niacinamide market continues to be shaped by Asia-based manufacturing clusters, which are influencing cost structures, grade availability, and supplier negotiations across regions. The draft shows that capacity expansion is not simply adding more output, but is also creating a clearer divide between large-scale commodity supply and premium-grade material that carries better certification and process control. That matters because the Niacinamide market does not reward all capacity equally, and buyers in pharmaceutical and premium cosmetic uses are not interchangeable with feed or basic nutrition buyers. Asian manufacturing scale still sets the cost floor for much of the Niacinamide market, especially where bulk production and export capability remain central to global trade flows. At the same time, newer qualified capacity outside the lowest cost tier can capture better margins when buyers need cGMP support, residual control, and more reliable documentation. This means the Niacinamide market is becoming more layered by grade and qualification level, not just by tonnage.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price Pressure From Commodity-Grade Producers | -0.7% | Global, most acute in APAC & Latin America | Short term (≤ 2 years) |

| Formulation Stability and pH Compatibility Constraints | -0.4% | North America, EU (premium product markets) | Medium term (2-4 years) |

| Regulatory Fragmentation Across Cosmetic and Supplement Claims | -0.5% | Global, most complex in EU & ASEAN | Medium term (2-4 years) |

| Substitution Risk From Alternative Barrier-Repair Actives | -0.3% | North America, EU, South Korea | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Price Pressure from Commodity-Grade Producers

The Niacinamide market faces pressure where supply is concentrated in commodity-grade output and producers compete mainly on price. The draft makes clear that this is most visible in feed and standard cosmetic supply, where margin protection is weaker and where any downturn in demand can quickly reopen pricing pressure across the Niacinamide market. This is also why mid-scale producers face a harder position than either very large Chinese suppliers or better differentiated premium-grade manufacturers. A major sign of this pressure was DSM-Firmenich’s February 2026 agreement to divest its Animal Nutrition and Health business, including vitamins, to CVC Capital Partners for an enterprise value of EUR 2.2 billion, which signals less appetite among European majors for lower margin vitamin exposure.[2]dsm-firmenich, “dsm-firmenich Announces Agreement to Divest Animal Nutrition and Health to CVC Capital Partners,” dsm-firmenich Press Release, our-company.dsm-firmenich.com The Niacinamide market, therefore, has a clear commodity segment where price recovery can remain fragile even when broader demand looks solid. That pressure keeps procurement teams focused on scale, cost stability, and the risk of supplier concentration in lower-value segments.

Formulation Stability and pH Compatibility Constraints

The Niacinamide market also faces a technical restraint because the ingredient is not equally easy to combine with all popular actives in premium skincare systems. The main issue in the draft is pH sensitivity, since niacinamide can convert to nicotinic acid in highly acidic environments and create flushing concerns that are hard to reconcile with premium product positioning. A 2026 study in Journal of Pharmaceutical Innovation showed that liposomal co-delivery of retinol and niacinamide improved stability, permeation, and anti-aging or brightening performance. Still, it also highlighted that advanced delivery design is often needed to overcome ordinary formulation limits. Additional 2026 research in Journal of Drug Targeting suggested greener niosome-based delivery routes that may improve future flexibility, but that route is still more relevant to future platform development than to near term mass market relief. In practical terms, the Niacinamide market can lose some speed where brands lack the R&D budget to manage co formulation complexity well. This keeps part of the Niacinamide market tilted toward larger or more technically capable brands that can absorb higher development costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Powder Anchors Volume While Liquid Captures Premium Growth

Powder held 52.76% of market value in 2025, which makes it the core volume format in the Niacinamide market because it fits established manufacturing routines across pharmaceuticals, nutraceuticals, and food processing. Its position is supported by long shelf life, easy blending, and compatibility with tablet compression and spray dry encapsulation systems used at scale. Granular form remained a secondary format and stayed more relevant in feed applications where dust-free handling is useful in large volume mixing. Liquid form was smaller in current volume terms, but it is forecast to grow at a 9.77% CAGR through 2031 as the Niacinamide market shifts toward more precise cosmetic and injectable uses. That growth profile shows that value expansion in the Niacinamide market is not always coming from the dominant format, but often from the one that solves more specialized formulation needs.

Liquid form is gaining importance because serum and solution-based products need consistent dissolution and tighter concentration control than many powder systems provide. This is especially relevant as brands pursue cleaner formulas and minimal excipient designs, where direct liquid incorporation can reduce processing steps and lower the chance of batch inconsistency. The 2026 liposomal delivery work in the Journal of Pharmaceutical Innovation also supports the longer-term appeal of liquid phase systems for advanced dermatological use, since better carrier design can improve permeation and ingredient stability. Granular material should remain useful where handling efficiency matters more than premium formulation performance, but it is less central to where the Niacinamide market is creating value. In that sense, the Niacinamide market is likely to keep powder as the anchor format while allowing liquid to capture the higher growth lane.

By Grade: Pharmaceutical Grade Holds the Base While Cosmetic Grade Lifts Value

Pharmaceutical grade held 38.13% of the market value in 2025, which gave it the largest grade position and established an important volume floor for the Niacinamide market. Its role is supported by both established therapeutic use and newer research interest linked to NAD+ related applications, which helps maintain demand beyond basic deficiency treatment. This segment also benefits from the fact that cGMP compliance and documentation create practical entry barriers, so qualified supply is not as easily replaced as commodity output. Feed grade still absorbed meaningful tonnage, but it sat at the lowest end of pricing and contributed less to value protection across the Niacinamide market. That makes pharmaceutical grade important not only for current size, but also for holding a more stable pricing position inside the Niacinamide market.

Cosmetic grade is the fastest-growing grade and is projected to expand at a 10.23% CAGR through 2031, which shows where much of the premium value shift is occurring. Buyers in this segment place more weight on residual controls, purity certificates, origin claims, and audit-ready documentation than on volume alone. That preference matters because the Niacinamide market is increasingly rewarding suppliers that can serve brand-level differentiation rather than only bulk ingredient demand. The draft also points to stronger demand for biosynthetic origin credentials and sustainability records, which helps explain why premium cosmetic supply can outperform ordinary material even when overall volumes are smaller. The Niacinamide market, therefore, looks increasingly two-tiered by grade, with pharmaceutical supply preserving the base and cosmetic grade producing the stronger uplift in value.

By Application: Cosmetics And Personal Care Leads While Human Nutrition Gains Speed

Cosmetics and personal care accounted for 37.18% of the Niacinamide market size in 2025, which made it the largest application and confirmed how firmly niacinamide is embedded in mainstream skincare routines. The segment is centered on serums, moisturizers, and sunscreens, where niacinamide’s familiarity and wide tolerance profile support repeated formulation use. A 2025 real-world study in Applied Sciences reported that niacinamide-containing preparations reduced facial spots and pigmentation areas more effectively than comparator products, which gives brands commercial support for visible performance claims. A 2025 review indexed in PubMed also described niacinamide as a multifunctional skin health and rejuvenation agent, reinforcing its broad relevance across barrier repair, pigmentation, and aging-related discussions. This keeps cosmetics central to the Niacinamide market because brand demand, clinical messaging, and consumer recognition continue to reinforce each other.

Human nutrition is projected to grow at a 9.91% CAGR through 2031 and stands out as the fastest-growing application in the Niacinamide market. The draft ties that growth to a broader repositioning of vitamin B3 from a basic nutrient toward a functional ingredient linked with energy metabolism, NAD+ support, and metabolic wellness. Pharmaceuticals should continue to expand steadily, supported by cardiovascular and deficiency-related uses, while animal nutrition remains important for volume but weaker in value terms. Food and beverages sit in a middle position because fortification programs provide support, even if the category does not generate the same premium narrative as skincare or nutraceuticals. Overall, the Niacinamide market is showing that application growth is moving toward categories where science-based consumer messaging and regulatory familiarity can coexist.

By End User: Cosmetic Manufacturers Hold Share While Nutraceutical Companies Accelerate

Cosmetic manufacturers held 35.13% of the Niacinamide market share in 2025, which made them the largest end user group in the draft and confirmed the strength of skincare-led demand. Their buying patterns are becoming more selective because the Niacinamide market now places greater weight on traceability, impurity profiles, and supplier audit readiness. That shift matters because it reduces the appeal of generic sourcing and raises the value of qualified producers with stronger process control. Pharmaceutical companies and food and beverage companies remain stable demand anchors, while animal feed producers continue to buy large volumes but contribute less to margin quality. This means the Niacinamide market is not being led only by the biggest buyers, but by the buyers whose specifications shape supplier investment.

Nutraceutical companies are forecast to grow at a 10.36% CAGR through 2031, making them the fastest expanding end user group in the Niacinamide market. Their momentum reflects the widening overlap between supplements, wellness positioning, and beauty from within product narratives that can carry higher price points. The draft also indicates that premium dietary and infant nutrition requirements are raising expectations around particle size, heavy metal control, and allergen-related documentation. That raises entry barriers in ways that favor suppliers capable of serving several regulated or specification-driven channels at once. The Niacinamide industry, therefore, is moving toward multi-certification supply models, because the best growth pockets cut across end uses rather than staying inside one isolated customer group. For the Niacinamide market, this makes flexible premium supply more valuable than a single-channel commodity scale.

Geography Analysis

Asia-Pacific held 42.15% of the Niacinamide market size in 2025, which kept it as the largest regional block in the Niacinamide market. Its lead comes from the combination of production depth and broad downstream consumption across cosmetics, nutrition, and pharmaceutical uses. The region also benefits from a supply base that ranges from commodity volume to more qualified premium output, which allows it to serve several tiers of the Niacinamide market at once. China remains central to this structure because the draft describes it as the leading production hub and a major source of cost-competitive supply. South Korea and Japan add a different role by concentrating demand for high-purity material used in dermatology-linked and prestige skincare channels.

That combination gives Asia-Pacific a dual advantage in the Niacinamide market because it supports both manufacturing scale and premium demand formation. North America is the fastest-growing geography and is projected to expand at a 9.69% CAGR through 2031, which reflects strong momentum in clinical skincare, supplements, and pharmaceutical compounding demand. The U.S. regulatory environment is becoming more important in supplier selection because implementation activity tied to the FDA’s 2026 Human Foods Program priorities is raising attention on documentation and compliance quality. The FDA’s recognition of niacinamide under 21 CFR 184.1535 also supports its established role in food-related applications.[3]U.S. Food and Drug Administration, “21 CFR 184.1535, Niacinamide,” Electronic Code of Federal Regulations, ecfr.io For the Niacinamide market, North America offers one of the clearest settings where stronger regulation and premium positioning support faster value growth.

Europe remains important because it brings stable regulatory frameworks and disciplined supplement and cosmetic channels to the Niacinamide market. The region’s food fortification structure under EU regulation and its 2023 update on niacin forms show that the category remains actively governed rather than mature and static. Germany’s Federal Institute for Risk Assessment has also proposed a maximum of 160 mg per day for nicotinamide in food supplements, which influences formulation discipline in the supplement channel.

Competitive Landscape

The Niacinamide market shows moderate concentration in premium grades and more intense rivalry in commodity tiers, which creates a split competitive structure rather than one uniform field. Large Chinese producers such as Zhejiang NHU, Hubei Guangji Pharmaceutical, and Shandong Hongda compete strongly on cost across feed and standard cosmetic material. At the same time, Indian and European-linked suppliers defend higher specification segments through compliance and purity positioning. This means the Niacinamide market does not reward scale alone, because premium buyers often care as much about certificates and traceability as about price. It also means margin pressure is not evenly distributed, since commodity output carries more exposure to oversupply and price resets. The current Niacinamide market structure, therefore, favors producers that can move between volume efficiency and specification-driven differentiation without losing credibility in either area.

One of the clearest strategic moves came from DSM-Firmenich, which agreed in February 2026 to divest its Animal Nutrition and Health business to CVC Capital Partners and thereby signaled a sharper focus away from lower-margin vitamin exposure. Another move came from BASF, which completed the sale of its Food and Health Performance Ingredients business in September 2025, showing a similar preference for moving away from commodity nutrition exposure. BASF also launched SkinNexus Collag3n with Bota Biosciences in June 2026, which points to a stronger focus on premium, science-led personal care actives rather than broad vitamin volume competition. These moves matter because they change supplier options for downstream buyers and leave more room for Asian cGMP capable producers to strengthen their position in the Niacinamide market. The Niacinamide market is therefore seeing competitive space open up in premium supply even while commodity pressure remains severe.

Another important feature is that quality differentiation is becoming a more durable advantage than basic synthesis scale in parts of the Niacinamide market. The draft highlights residual nicotinic acid control, natural origin positioning, and sustainability documentation as criteria that can justify premiums in cosmetic grade supply. That is why the Niacinamide market increasingly rewards companies that can convert technical attributes into clear commercial assurance for brand owners and pharmaceutical customers. Producers that remain stuck between low-cost mass supply and high specification premium supply face the greatest pressure, because they are squeezed from both ends. The Niacinamide industry is also watching whether emerging Chinese and Indian suppliers can extend from cost competitiveness into more advanced regulated and cosmetic channels. As that transition unfolds, the Niacinamide market is likely to stay competitive. Still, the strongest positions will belong to suppliers that combine compliance depth, process consistency, and customer-specific qualification support.

Niacinamide Industry Leaders

BASF SE

dsm-firmenich AG

Hubei Guangji Pharmaceutical Co., Ltd.

Lonza Group AG

Zhejiang NHU Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: BASF and Bota Biosciences jointly launched SkinNexus Collag3n, a 100% human-identical recombinant Collagen III fragment for the personal care market, which debuted at in-cosmetics Global in April 2026. This signals BASF's post-divestiture strategy of competing in premium, AI-developed cosmetic actives, a competitive benchmark for niacinamide suppliers in the cosmetic-actives space to assess their differentiation trajectory against.

- February 2026: DSM-Firmenich, agreed to divest its Animal Nutrition & Health (ANH) business, which includes the Vitamins, Carotenoids, and Aroma Ingredients division, to CVC Capital Partners for an enterprise value of approximately EUR 2.20 billion (~USD 2.40 billion). The transaction is expected to close by end of 2026 subject to regulatory approval.

- September 2025: BASF and Louis Dreyfus Company completed the transaction for BASF's Food and Health Performance Ingredients business, marking BASF's full exit from the commodity vitamin and nutrition ingredient space and concentrating its personal care strategy on high-value, science-differentiated actives.

Global Niacinamide Market Report Scope

The Niacinamide Market comprises the global production, distribution, and commercialization of niacinamide (nicotinamide), a water-soluble form of vitamin B3 widely used as an active ingredient across pharmaceutical, cosmetic, food, nutritional, and animal feed applications. Niacinamide is valued for its role in supporting cellular metabolism, skin barrier function, anti-inflammatory activity, and vitamin B3 supplementation. The market is driven by increasing demand for functional skincare products, growing use in dietary supplements and fortified foods, expanding pharmaceutical applications, and rising awareness of preventive health and wellness.

The niacinamide market is segmented by form, grade, application, end user, and geography. By form, it is further divided into powder, granular, and liquid. By grade, it is segmented into pharmaceutical grade, feed grade, food grade, and cosmetic grade. By application, the market is segmented into cosmetics and personal care, pharmaceuticals, Food and beverages, human nutrition, and animal nutrition. By end user, the market is segmented into pharmaceutical companies, cosmetic manufacturers, food and beverage companies, nutraceutical companies, and animal feed producers. The geography segment is further divided into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market size and forecasts in value (USD) for the above segments.

| Powder |

| Granular |

| Liquid |

| Pharmaceutical Grade |

| Feed Grade |

| Food Grade |

| Cosmetic Grade |

| Cosmetics and Personal Care | Skincare Products |

| Haircare Products | |

| Pharmaceuticals | Vitamin Deficiency Treatment |

| Cardiovascular Support | |

| Food and Beverages | |

| Human Nutrition | |

| Animal Nutrition |

| Pharmaceutical Companies |

| Cosmetic Manufacturers |

| Food and Beverage Companies |

| Nutraceutical Companies |

| Animal Feed Producers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Form | Powder | |

| Granular | ||

| Liquid | ||

| By Grade | Pharmaceutical Grade | |

| Feed Grade | ||

| Food Grade | ||

| Cosmetic Grade | ||

| By Application | Cosmetics and Personal Care | Skincare Products |

| Haircare Products | ||

| Pharmaceuticals | Vitamin Deficiency Treatment | |

| Cardiovascular Support | ||

| Food and Beverages | ||

| Human Nutrition | ||

| Animal Nutrition | ||

| By End User | Pharmaceutical Companies | |

| Cosmetic Manufacturers | ||

| Food and Beverage Companies | ||

| Nutraceutical Companies | ||

| Animal Feed Producers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size outlook for niacinamide worldwide?

The Niacinamide market stands at USD 1.19 billion in 2025 and USD 1.29 billion in 2026, and it is forecast to reach USD 1.98 billion by 2031 at an 8.85% CAGR.

Which application area leads niacinamide demand today?

Cosmetics and personal care leads with 37.18% of market value in 2025, supported by strong use in serums, moisturizers, sunscreens, and pigment management products.

Which grade is expanding the fastest through 2031?

Cosmetic grade is the fastest growing grade with a 10.23% CAGR, reflecting stronger demand for premium purity, residual control, and documented sourcing.

Why is Asia-Pacific the leading regional block?

Asia-Pacific holds 42.15% of global value because it combines large scale production with strong domestic demand across cosmetics, nutrition, and pharmaceutical uses.

What is driving the fastest growth in North America?

North America is growing at a 9.69% CAGR because clinical skincare demand, supplement expansion, and tighter documentation expectations are reinforcing premium supplier selection.

Which end user group offers the strongest future opportunity?

Nutraceutical companies show the highest growth at a 10.36% CAGR, as niacinamide is increasingly positioned around energy metabolism, NAD+ support, and wellness focused supplements.

Page last updated on: