Next-Generation HBM Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

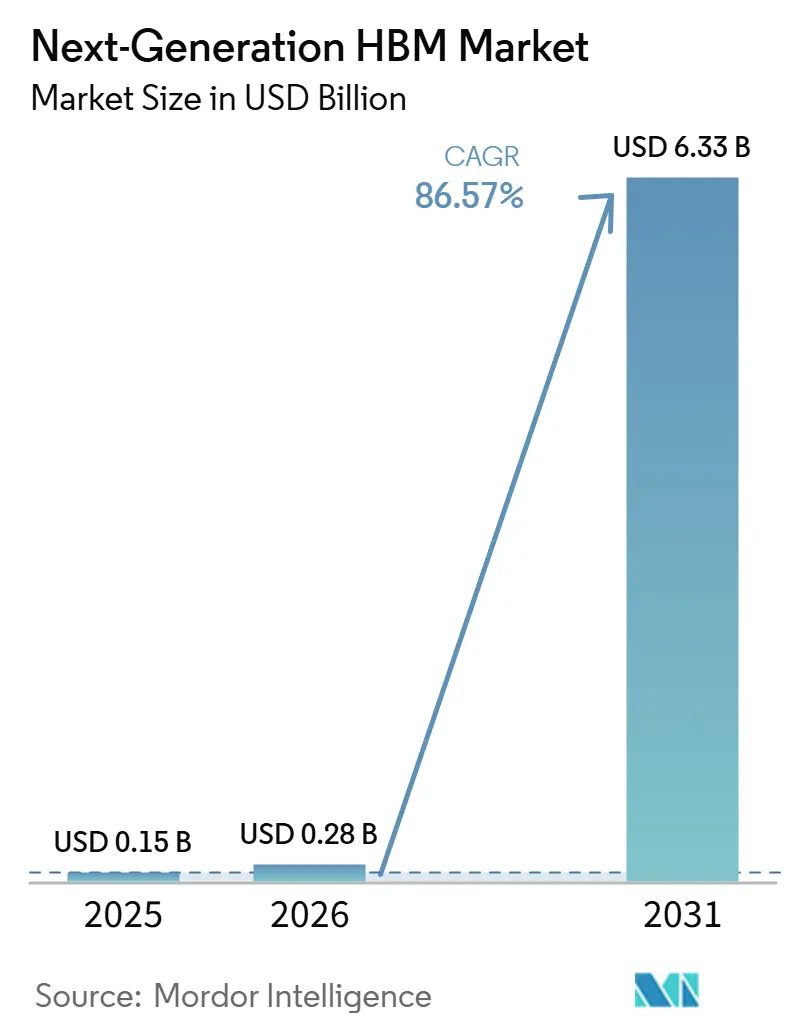

| Market Size (2026) | USD 0.28 Billion |

| Market Size (2031) | USD 6.33 Billion |

| Growth Rate (2026 - 2031) | 86.57% CAGR |

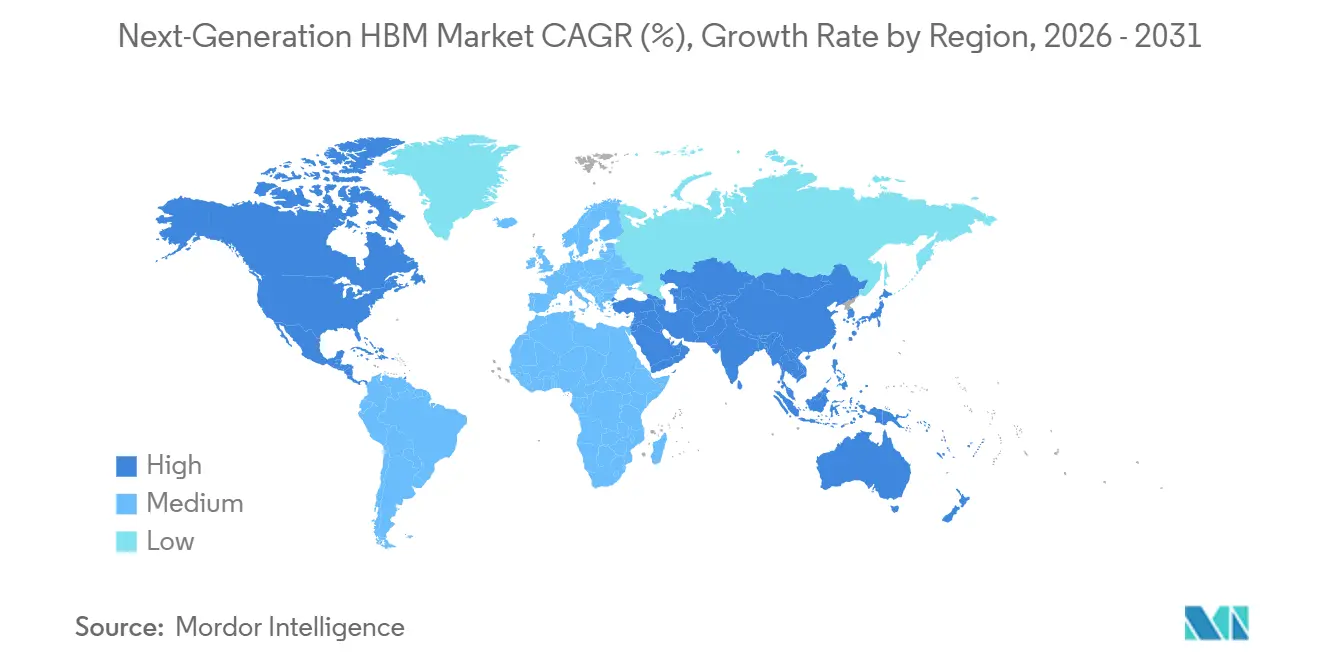

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Next-Generation HBM Market Analysis by Mordor Intelligence

The next-generation HBM market size was valued at USD 0.15 billion in 2025 and is projected to reach USD 6.33 billion by 2031, at a CAGR of 86.57% during 2026-2031. The next-generation HBM market is expanding because each new AI accelerator generation requires more memory capacity per chip and much higher memory bandwidth per system, which increases memory content even as compute unit volumes grow more slowly. The next-generation HBM market is also being shaped by the shift from standard memory supply to co-designed memory stacks, as suppliers now compete on qualification speed, yield ramp, and the ability to support custom base-die architectures for specific accelerator platforms. Demand remains heavily tied to hyperscaler and data center build-outs, which keeps purchasing concentrated and makes long-term supply agreements more important than spot availability. At the same time, packaging remains the main physical bottleneck, because memory stacks cannot convert into finished accelerator shipments until advanced integration capacity is available at scale. Export controls and the narrow supplier base add another layer of commercial discipline, but they also create space for investment in localized production, packaging, and long-term customer contracts in the next-generation HBM market.

Key Report Takeaways

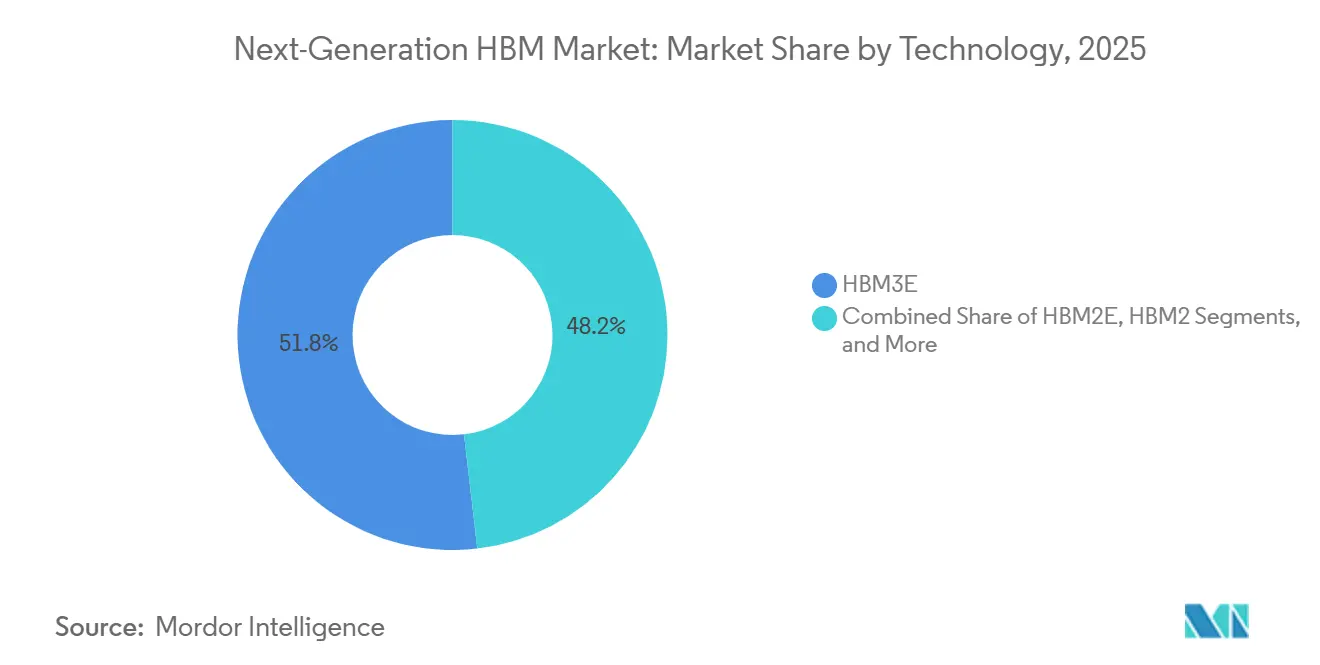

- By technology, HBM3E held 51.84% of the next-generation HBM market in 2025, while HBM4 is projected to expand at a 87.58% CAGR through 2031.

- By memory capacity per stack, 24 GB led with 47.12% of the next-generation HBM market in 2025, while 32 GB and above is projected to grow at a 87.51% CAGR through 2031.

- By processor interface, GPU accounted for 79.34% of the market share in 2025, while AI accelerators and ASICs are projected to grow at a 87.15% CAGR through 2031.

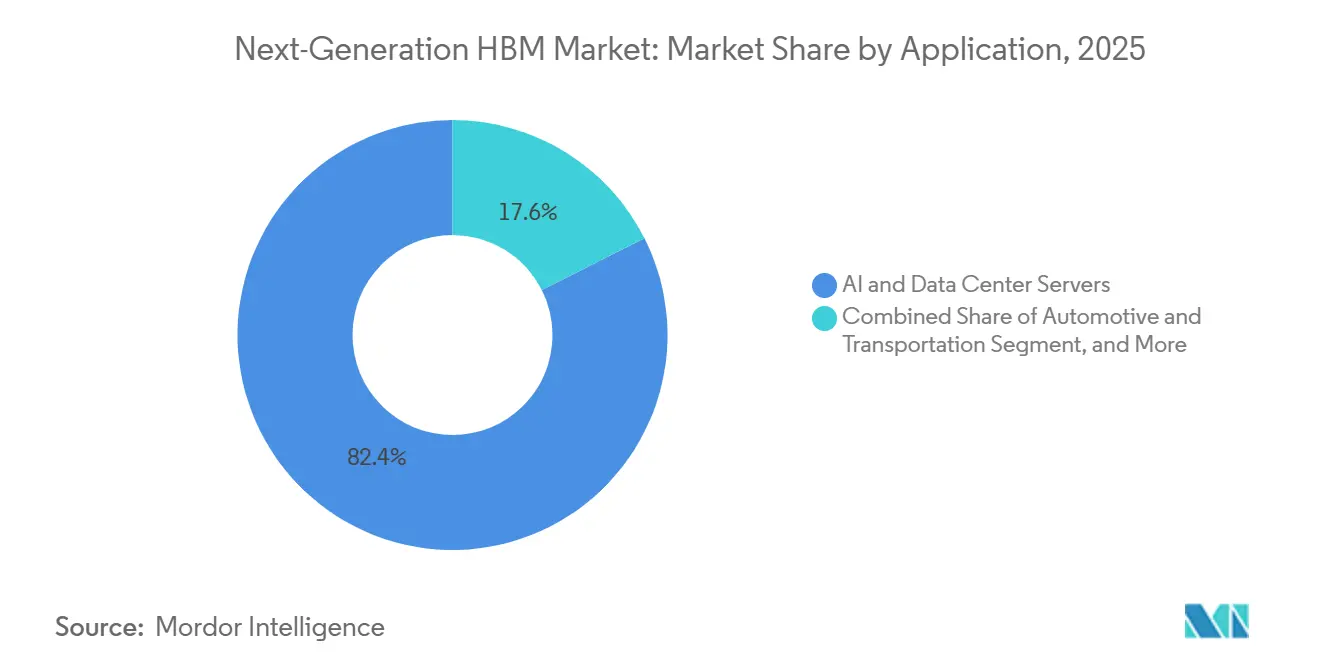

- By application, AI and data center servers held 82.43% share in 2025, while automotive and transportation are projected to expand at a 87.74% CAGR through 2031.

- By end use industry, cloud service providers accounted for 61.78% share in 2025, while enterprise data centers are projected to grow at a 87.22% CAGR through 2031.

- By geography, Asia-Pacific accounted for 71.04% of the next-generation HBM market in 2025, while North America is projected to expand at a 87.38% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Next-Generation HBM Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI Server Proliferation and GPU Attach Rates | +7.2% | Global, primarily North America and the Asia-Pacific | Short term (≤ 2 years) |

| HBM4 Adoption in Next-Generation AI Accelerators | +6.1% | Global, primarily North America and South Korea | Short term (≤ 2 years) |

| Advanced Packaging Capacity Expansion | +4.8% | Asia-Pacific core, spill-over to North America | Medium term (2-4 years) |

| Sovereign AI And Local Memory Localization Incentives | +3.2% | Asia-Pacific, North America, and Europe | Medium term (2-4 years) |

| Edge AI Inference In Automotive ADAS | +2.1% | Global, with early gains in Germany, the United States, and Japan | Medium term (2-4 years) |

| Photonics-Ready HBM Roadmaps | +1.3% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

AI Server Proliferation and GPU Attach Rates

Every major AI platform now carries a larger HBM load per processor than the previous one, indicating the next-generation HBM market is growing faster than accelerator unit demand alone. NVIDIA disclosed that Vera Rubin NVL72 uses 20.7 TB of HBM4 and 1,580 TB/s of memory bandwidth across 72 GPUs, demonstrating how quickly system-level memory intensity is rising. SK Hynix also reported that its HBM business more than doubled year over year in FY2025, confirming that AI server deployments are already translating into significant expansion in very large memory revenue. The next-generation HBM market is therefore being pulled forward by both new server installations and richer memory configurations within each installed rack. That pattern is reinforced by the move toward rack-scale AI systems, where the economic value of the platform depends on sustained memory throughput rather than raw compute density alone. As a result, suppliers that can ramp qualified volume quickly are in a stronger position than those that simply have product availability on paper.

HBM4 Adoption In Next-Generation AI Accelerators

HBM4 is driving the next-generation HBM market by combining a significant increase in bandwidth with architectural changes that enable tighter optimization for upcoming AI platforms. Micron stated that its HBM4 36 GB 12-high product delivered more than 2.8 TB/s of bandwidth and over 20% better power efficiency than HBM3E, while entering high-volume production in early 2026. Samsung also began mass production shipments of HBM4 in February 2026 and later said cumulative HBM4 sales reached USD 1 billion within 130 days, pointing to an unusually fast commercial ramp for a new memory generation. The move to HBM4 also raises technical demands, as the I/O count per die doubles compared with earlier generations, making stack yield, base-die integration, and package-level validation more difficult. In practice, that complexity limits broad participation and keeps the next-generation HBM market centered on suppliers that can pair DRAM process strength with packaging discipline. It also raises the value of custom HBM programs, which are becoming a direct differentiator in top-tier AI accelerator launches.

Advanced Packaging Capacity Expansion

Advanced packaging expansion matters because the next-generation HBM market cannot scale in finished units unless memory stacks and compute dies can be integrated in enough volume. TSMC has described ongoing work on advanced packaging roadmaps while acknowledging that next-step solutions, such as CoPoS, remain technically demanding and will arrive later than earlier expectations. TSMC and SK Hynix said FY2026 investment would rise significantly to support M15X capacity, the Yongin Semiconductor Cluster, and advanced packaging facilities in Indiana, indicating that memory suppliers now treat backend integration as a strategic growth lever rather than a supporting function. Micron also said its Taiwan Tongluo advanced packaging facility and its Singapore packaging expansion would contribute to HBM capacity on an accelerated timetable, pointing to broader industry action on packaging readiness. This means the next-generation HBM market is no longer constrained solely by front-end wafer output, because backend attachment, thermal control, and substrate alignment now determine how much qualified product reaches customers. Capacity additions in packaging, therefore, support growth directly, but they do not fully eliminate scarcity because each new node also increases process complexity.

Sovereign AI and Local Memory Localization Incentives

Government policy has become a significant demand-and-supply support factor for the next-generation HBM market, as countries now view memory access as part of AI infrastructure security. South Korea announced an AI and semiconductor investment commitment exceeding USD 900 billion through 2035, with dedicated funding for new memory fabs, an HBM packaging hub, and AI data centers. South Korea also enacted its AI Framework Act on January 22, 2026, providing regulatory clarity for high-risk AI deployment and strengthening the case for domestic AI infrastructure investment. In the United States, Micron secured CHIPS Act grants of up to USD 6.4 billion for DRAM fab construction and related capability development, which ties public funding directly to future memory supply depth.[1]Micron Technology, “Annual Report For Fiscal Year Ending August 28, 2025, Form 10-K,” U.S. SEC, sec.gov These programs do not change near-term demand concentration, but they do change the medium-term shape of supply planning, site selection, and customer contracting. Over time, that makes the next-generation HBM market more influenced by industrial policy, local resilience goals, and sovereign compute strategies than most other memory categories.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited CoWoS and SoIC Advanced-Packaging Capacity | -4.8% | Global, particularly Taiwan and South Korea | Short term (≤ 2 years) |

| Export Controls on Advanced AI Accelerators and HBM-Linked Supply Chains | -3.5% | Global, particularly China and HBM supply chain nations | Medium term (2-4 years) |

| TSV Yield Losses in High-Stack Designs | -2.1% | Global | Short term (≤ 2 years) |

| Thermal Density Limits in Ultra-High-Bandwidth Devices | -1.4% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited CoWoS and SoIC Advanced-Packaging Capacity

The largest near-term restraint on the next-generation HBM market remains the availability of advanced packaging, as qualified memory stacks still need scarce integration slots before they can ship in accelerator products. TSMC has indicated that more advanced packaging transitions, such as CoPoS, have been delayed by engineering challenges tied to glass interposer uniformity and warpage control, which keeps pressure on current packaging flows for longer. This means even well-yielding HBM output can be held back by a second bottleneck at the integration stage, especially for high-stack products that already require tighter process control. The restraint is more severe when customers need the newest configurations, because HBM4 and HBM4E products place additional demands on thermal handling, bump integrity, and package validation. Suppliers are responding with higher backend investment, but the next-generation HBM market still faces a lag between announced packaging capacity and dependable, qualified throughput. That lag keeps allocation tight, supports premium pricing, and limits how quickly supply can match the demand profile of leading AI platforms.

Export Controls on Advanced AI Accelerators And HBM-Linked Supply Chains

Export controls constrain the next-generation HBM market by introducing customer screening, licensing uncertainty, and destination restrictions on products that reside in controlled AI systems. The U.S. Bureau of Industry and Security placed HBM above a memory bandwidth density threshold of 2 GB/s per mm² under ECCN 3A090.c, as set forth in the AI Diffusion Interim Final Rule, which became effective on January 13, 2025. The revised AI chip export review policy was announced on January 15, 2026, shifting some transactions for China and Macau toward case-by-case review when performance stayed below specific ceilings. The regulatory framework does not remove demand, but it changes how suppliers plan volume allocation, contract risk, and end-market exposure. Also noted that U.S. export controls affect the advanced semiconductor ecosystem needed for products such as HBM, which adds another structural hurdle for countries seeking local high-end memory capability. As a result, the next-generation HBM market remains commercially strong, but its addressable demand is filtered by policy decisions, technical qualification, and customer budgets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: HBM3E Anchors The Current Base As HBM4 Defines The Next Cycle

HBM3E held 51.84% of the technology segment in 2025, while HBM4 is projected to expand at 87.58% CAGR through 2031. HBM3E remains important in the next-generation HBM market because it already supports meaningful deployment across current AI infrastructure and gives customers a qualified bridge while HBM4 volume ramps. NVIDIA’s current and near-term platform cadence has helped keep HBM3E relevant, since hyperscalers continue to deploy existing accelerator systems even as they prepare for the next memory generation. HBM4, however, is changing the pace of this category by offering much higher bandwidth, greater flexibility for customized designs, and stronger alignment with upcoming rack-scale AI systems. Micron said its HBM4 36 GB 12-high product exceeded 2.8 TB/s and improved power efficiency by more than 20% compared with HBM3E, which explains why customers are moving quickly to qualify the new node.

The next-generation HBM market also shows that technology leadership is no longer defined only by DRAM density or speed, because base-die design and foundry coordination now matter much more than they did in earlier memory cycles. Samsung stated that its HBM4 uses a 4-nm base die and later shipped HBM4E 12-high samples with up to 16 Gbps per pin and 3.6 TB/s bandwidth, showing how quickly the technology ladder is tightening.[2]Samsung Semiconductor, “Samsung HBM4E 12-High Sample Shipment,” Samsung Semiconductor Newsroom, samsung.com SK Hynix followed with HBM4E samples in June 2026 and highlighted custom HBM as a strategic priority, which signals that the next-generation HBM market is moving toward customer-specific optimization rather than simple standard part competition. Older generations such as HBM2, HBM2E, and HBM3 still have room in networking and legacy HPC uses, where cost and qualification history can matter more than absolute bandwidth. Even so, the transition path makes entry harder for new participants, because suppliers now need credible strength in memory process technology, advanced packaging, and base-die coordination at the same time.

By Memory Capacity Per Stack: 24 GB Anchors The Installed Base As 32 GB and Above Sets the AI Infrastructure Standard

The 24 GB tier led with 47.12% share in 2025, while 32 GB and above is projected to grow at 87.51% CAGR through 2031. The 24 GB tier sits at the center of the installed base in the next-generation HBM market because it matches the configuration used in many current AI systems and gives customers a known balance between performance, yield, and deployable volume. That installed base will not disappear quickly, as existing server fleets and procurement cycles continue to support strong demand for qualified HBM3E stacks in this capacity range. The growth center has already moved higher, however, because newer AI systems need more memory per accelerator and more bandwidth per training cluster than earlier platforms required. Micron said it shipped HBM4 48 GB 16-high samples to multiple customers in Q1 2026, indicating how quickly the product roadmap is moving beyond the current mainstream tier.

This shift matters because the next-generation HBM market for higher-capacity stacks is growing with each platform generation, and the new floor for AI-relevant memory content is steadily rising. As stack height increases, the technical burden also rises because die thinning, alignment, and thermal control become more sensitive, which can reduce effective finished-unit output even when wafer availability appears healthy. IEEE and related packaging analysis in the source draft highlighted that through-silicon-via complexity and high-stack assembly losses become more serious as more layers are added to a single package. Smaller tiers such as 4 GB, 8 GB, and 16 GB remain relevant in networking devices, edge inference hardware, and legacy compute nodes where bandwidth per dollar still shapes purchasing decisions. Still, the long-term direction of the next-generation HBM market is clear, because premium capacity tiers are becoming commercial volume products rather than isolated high-end options.

By Processor Interface: GPU Dominance Persists as ASIC Programs Reshape the Demand Structure

GPU accounted for 79.34% of the market share in 2025, while AI accelerators and ASICs are projected to grow at a 87.15% CAGR through 2031. GPUs remain the largest interface category in the next-generation HBM market because they still dominate mainstream AI training and large-scale inference procurement across hyperscalers and cloud platforms. That base remains durable because most current software stacks, deployment models, and supply relationships have been built around GPU-led accelerator systems. At the same time, the demand structure is widening as custom silicon programs gain importance, meaning HBM demand is no longer tied to a single qualification rhythm or customer archetype. Samsung said in 2026 that it was expanding HBM4 supply across NVIDIA, AMD, Broadcom, and Google programs, and it also tied HBM4 plans to custom ASIC demand from major customers.

The result is a broader, more layered next-generation HBM market, where custom AI chips add a second demand path alongside the traditional GPU channel. That second path matters because hyperscaler ASIC programs often have different volume timing, power targets, and packaging needs, which supports custom memory design and longer supply planning. CPU and FPGA interfaces still occupy smaller but durable positions, especially in technical computing and network acceleration workloads where existing HBM configurations remain sufficient. The original draft also pointed to emerging optical and tightly integrated architectures that could blur the line between processor interface and interconnect design in future generations, although current commercial demand remains centered on GPU and ASIC use cases. For now, the interface mix still favors GPU-led systems, but the fastest structural change in the next-generation HBM market is the growing role of custom silicon programs that need the same class of high-bandwidth memory.

By Application: Data Centers Define the Market as Automotive Carves Out a Structurally Distinct Growth Path

AI and data center servers held 82.43% share in 2025, while automotive and transportation are projected to grow at 87.74% CAGR through 2031. AI and data center servers dominate the next-generation HBM market because early-qualified supply has been absorbed primarily by hyperscaler infrastructure and large accelerator clusters. That concentration reflects both economics and availability, since top-tier AI platforms can justify premium pricing and also secure long-duration supply agreements more easily than smaller end markets. The next-generation HBM market size in data center use, therefore, remains the base from which all other applications develop over the forecast period. Automotive and transportation are growing faster because vehicle compute architectures are shifting toward centralized onboard processing that must handle camera, radar, LiDAR, and other sensor streams with very low latency. IEEE work cited in the source draft also showed that new HBM system designs can materially improve the efficiency of large model training and inference, pointing to broader future application depth as architectures evolve.

The application mix also shows that the next-generation HBM market is still in an early concentration phase, where one use case currently accounts for most of the volume while newer ones build technical and commercial credibility. Networking remains a meaningful secondary category because switch ASICs, DPUs, and AI traffic handling equipment need high-throughput memory to support rising data center interconnect loads. High-performance computing continues to hold space in government and scientific environments where memory bandwidth remains a core requirement, even if qualification cycles differ from hyperscaler AI procurement. Consumer electronics still has only a modest role because cost, power, and packaging complexity limit HBM adoption to a narrow set of premium devices. Automotive growth could become more strategic over time, but entry standards remain strict because safety qualification, product life cycle discipline, and supply continuity matter more here than in many other parts of the next-generation HBM market.

By End Use Industry: Cloud Providers Anchor the Base While Enterprise Data Centers Accelerate

Cloud service providers accounted for 61.78% share in 2025, while enterprise data centers are projected to record an 87.22% CAGR through 2031. Cloud providers lead the next-generation HBM market because they moved first in scaling AI training and inference clusters, and they secured supply through their purchasing scale and long planning horizons. That leadership also reflects the fact that early HBM4 and high-capacity HBM3E production has been directed toward customers that can absorb very large volumes and deploy them quickly. The enterprise data center segment is growing faster as organizations move from pilot AI projects into production environments, where they want greater control over latency, sovereignty, and internal model operations. Micron said in fiscal Q3 2026 that it had signed 16 strategic customer agreements across data center, consumer, and automotive categories, with 14 of those agreements representing nearly USD 100 billion in cumulative minimum-price revenue through calendar 2030.

That contracting behavior shows how the next-generation HBM market is shifting from opportunistic procurement toward structured allocation and multi-year volume planning. Enterprise buyers are important in this shift because they are more likely to seek predictable supply and internal infrastructure control rather than rely fully on public cloud capacity. Telecommunications operators form an emerging secondary layer, since AI inference is moving closer to the network edge for traffic management and service optimization. Automotive OEMs still represent a smaller end-use block, but they matter strategically because they bring longer design cycles and higher qualification requirements that can support stable demand once platforms are approved. Over time, the end-use mix should broaden, but the next-generation HBM market will remain anchored by cloud demand until enterprise and automotive deployments achieve larger production scale.

Geography Analysis

Asia-Pacific held 71.04% of the next-generation HBM market share in 2025. The region leads because South Korea concentrates commercial HBM production at SK Hynix and Samsung Electronics, while Taiwan remains central to advanced packaging and integration. SK Hynix reported FY2025 revenue of KRW 97,146.7 billion (USD 70.2 billion), using the IRS 2025 yearly average exchange rate provided in the source draft, and said HBM revenue more than doubled year over year.[3]Internal Revenue Service, “Yearly Average Currency Exchange Rates,” IRS, irs.gov South Korea strengthened that position in June 2026 with a national investment plan that included four new memory fabs, an HBM packaging hub, and major funding for AI data centers. The South Korean AI Framework Act, effective January 22, 2026, added a policy layer to support domestic AI infrastructure and reinforce the country’s appeal as a destination for long-term memory investment.

North America is projected to grow at 87.38% CAGR through 2031, making it the fastest-expanding regional block in the next-generation HBM market. Demand is concentrated in the United States because the largest hyperscaler and accelerator buyers are based there, and that keeps procurement power close to the leading AI platform owners. Micron, the only U.S.-based HBM producer, secured CHIPS Act grants of up to USD 6.4 billion for DRAM fab construction in Idaho and New York, while also advancing domestic HBM-related capability. SK Hynix is also building advanced packaging facilities in Indiana, which deepens North American participation beyond demand concentration alone. Europe remains a secondary demand region, led by automotive compute needs in Germany and by broader hardware policy interest in markets such as the United Kingdom.

South America and the Middle East and Africa are still early-stage regions in the next-generation HBM market, but both are gaining relevance through AI infrastructure build-outs rather than through local memory production. South America is driven mainly by cloud and enterprise data center expansion, which increases imported accelerator demand as regional AI workloads grow. The Middle East and Africa are being supported by sovereign AI and large data center ambitions, especially where governments are backing compute capacity at scale. Neither region is likely to establish indigenous HBM production during 2026-2031, so their demand outlook remains closely tied to global supply allocation, export compliance, and price discipline among the established producers.

Competitive Landscape

The next-generation HBM market is highly concentrated because SK Hynix, Samsung Electronics, and Micron Technology are the only commercial HBM producers with current relevance at the advanced end of the category. NVIDIA confirmed in June 2026 that all 3 vendors had achieved HBM4 qualification for the Vera Rubin platform, indicating that competition is now shifting from basic qualification to volume ramp, yields, and custom execution. That makes the next-generation HBM market less like a broad memory category and more like a tightly controlled supply system where only a few firms can serve the most demanding programs. SK Hynix has focused on yield leadership, custom HBM, and aggressive investment in new manufacturing and packaging capacity, including expansion plans for M15X, Yongin, and Indiana. Samsung has pursued a broader customer base by pairing NVIDIA and AMD supply with custom-ASIC opportunities, while leveraging its internal 4-nm base-die capability as a design and integration advantage.

Micron is positioning itself differently in the next-generation HBM market, with an emphasis on U.S.-based production depth, CHIPS-linked infrastructure, and a rapid HBM4 ramp aligned with future customer allocations. Micron said its HBM4 volume ramp was moving at twice the pace of HBM3E 12-high and also outlined packaging expansions in Taiwan and Singapore, which points to a strategy built around growth timing and supply assurance. Advanced packaging partners such as Amkor, ASE, and Powertech matter because overflow integration capacity has become strategically important when internal lines are tight. The next-generation HBM market is also influenced by TSMC, even though it is not an HBM producer, because packaging roadmap timing affects how fast qualified memory can reach finished accelerator platforms.[4]TSMC, “TSMC Advanced Packaging Roadmap, CoPoS Timeline Update,” TSMC Investor Relations, tsmc.com TSMC Technical guidance cited in the source draft also noted that HBM4 remains on a microbump bonding path for now, which helps preserve testability and yield control during the ramp stage.

The competitive pattern therefore favors firms that can combine memory design, stack quality, backend integration, and customer-specific execution inside the same delivery model. Regulatory factors also matter in the next-generation HBM market, because export controls shape which customers each supplier can serve and how attractive certain destinations are for premium allocation. The most important strategic moves over the last cycle have been SK Hynix expanding capacity and custom HBM focus, Samsung broadening HBM4 supply across GPU and ASIC customers, and Micron accelerating both HBM4 output and packaging schedules. Those moves show that the market is not competing on price-led share gains, but on who can secure packaging, sustain yields, and meet the delivery windows of a small number of very large AI buyers.

Next-Generation HBM Industry Leaders

SK Hynix Inc.

Samsung Electronics Co., Ltd.

Micron Technology, Inc.

NVIDIA Corporation

Taiwan Semiconductor Manufacturing Company Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: South Korea announced a national investment commitment exceeding USD 900 billion through 2035, with USD 518 billion for 4 new memory fabs, USD 52 billion for an HBM packaging hub, and USD 356 billion for AI data centers, with Samsung Electronics and SK Hynix designated as anchor investors at a presidential briefing, the largest single national semiconductor investment plan announced to date.

- June 2026: SK Hynix shipped HBM4E 12-high samples to major customers at up to 16 Gbps per pin and more than 20% energy efficiency improvement over HBM4, 3 weeks after Samsung's first HBM4E sample shipment, compressing the generational competitive window to less than 1 quarter between the 2 leading suppliers.

- May 2026: Samsung Electronics shipped HBM4E 12-high samples globally at up to 16 Gbps pin speed and 3.6 TB/s per-stack bandwidth, the first seventh-generation HBM samples shipped by any company, advancing preparation for NVIDIA Vera Rubin Ultra and AMD Helios platforms where HBM4E is expected to be the primary memory configuration.

- April 2026: SK Hynix reported Q1 2026 revenue of KRW 52,576.3 billion (USD 37.6 billion) and operating profit of KRW 37,610.3 billion (USD 26.9 billion) at a 72% operating margin, a quarterly record, driven by HBM, high-capacity server DRAM, and eSSD products, the company announced plans to invest KRW 19 trillion (USD 13.6 billion) in a new South Korean manufacturing plant and pulled forward the Yongin Semiconductor Cluster first fab opening by 3 months to February 2027.

Global Next-Generation HBM Market Report Scope

The next-generation HBM market covers advanced high-bandwidth memory solutions, including HBM3, HBM3E, and emerging HBM4 technologies, designed to deliver higher data transfer rates, greater bandwidth, improved power efficiency, and compact form factors for data-intensive applications. The market scope includes memory stacks, related packaging technologies, and integration across applications such as artificial intelligence, high-performance computing, data centers, graphics processing, networking, and advanced consumer and enterprise electronics.

The Next-Generation HBM Market Report is Segmented by Technology (HBM2, HBM2E, HBM3, HBM3E, and HBM4), Memory Capacity Per Stack (4 GB, 8 GB, 16 GB, 24 GB, and 32 GB and Above), Processor Interface (GPU, CPU, AI Accelerator and ASIC, FPGA, and Other Processor Interfaces), Application (AI and Data Center Servers, Networking, High-Performance Computing, Consumer Electronics, Automotive and Transportation, and Other Applications), End Use Industry (Cloud Service Providers, Enterprise Data Centers, Telecommunications Operators, Automotive OEMs, and Other End Use Industries), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| HBM2 |

| HBM2E |

| HBM3 |

| HBM3E |

| HBM4 |

| 4 GB |

| 8 GB |

| 16 GB |

| 24 GB |

| 32 GB and Above |

| GPU |

| CPU |

| AI Accelerator and ASIC |

| FPGA |

| Other Processor Interfaces |

| AI and Data Center Servers |

| Networking |

| High-Performance Computing |

| Consumer Electronics |

| Automotive and Transportation |

| Other Applications |

| Cloud Service Providers |

| Enterprise Data Centers |

| Telecommunications Operators |

| Automotive OEMs |

| Other End Use Industries |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| Taiwan | |

| India | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By Technology | HBM2 | |

| HBM2E | ||

| HBM3 | ||

| HBM3E | ||

| HBM4 | ||

| By Memory Capacity per Stack | 4 GB | |

| 8 GB | ||

| 16 GB | ||

| 24 GB | ||

| 32 GB and Above | ||

| By Processor Interface | GPU | |

| CPU | ||

| AI Accelerator and ASIC | ||

| FPGA | ||

| Other Processor Interfaces | ||

| By Application | AI and Data Center Servers | |

| Networking | ||

| High-Performance Computing | ||

| Consumer Electronics | ||

| Automotive and Transportation | ||

| Other Applications | ||

| By End Use Industry | Cloud Service Providers | |

| Enterprise Data Centers | ||

| Telecommunications Operators | ||

| Automotive OEMs | ||

| Other End Use Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| Taiwan | ||

| India | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the current and future value of the next-generation HBM space?

The next-generation HBM market size was USD 0.15 billion in 2025 and is projected to reach USD 6.33 billion by 2031, with a CAGR of 86.57% during 2026-2031.

Which technology node leads today, and which one is growing fastest?

HBM3E held the largest technology share at 51.84% in 2025, while HBM4 is projected to grow fastest at an 87.58% CAGR through 2031.

Why are AI servers driving so much demand for high-bandwidth memory?

New AI platforms need much more memory per accelerator and much more bandwidth per rack, which raises HBM content even when compute shipments do not rise at the same pace.

Which application area dominates current demand?

AI and data center servers led with an 82.43% share in 2025, showing that hyperscaler and large accelerator deployments still define the current demand base.

Which end users are creating the strongest growth opportunity through 2031?

Cloud service providers held the largest share at 61.78% in 2025, while enterprise data centers are projected to grow fastest at 87.22% CAGR as internal AI deployments move into production.

Which region matters most for supply and which one is expanding fastest?

Asia-Pacific led with 71.04% share in 2025 because of production and packaging concentration, while North America is projected to grow fastest at 87.38% CAGR through 2031 because of hyperscaler demand and domestic manufacturing support.

Page last updated on: