New Zealand Customer Data Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

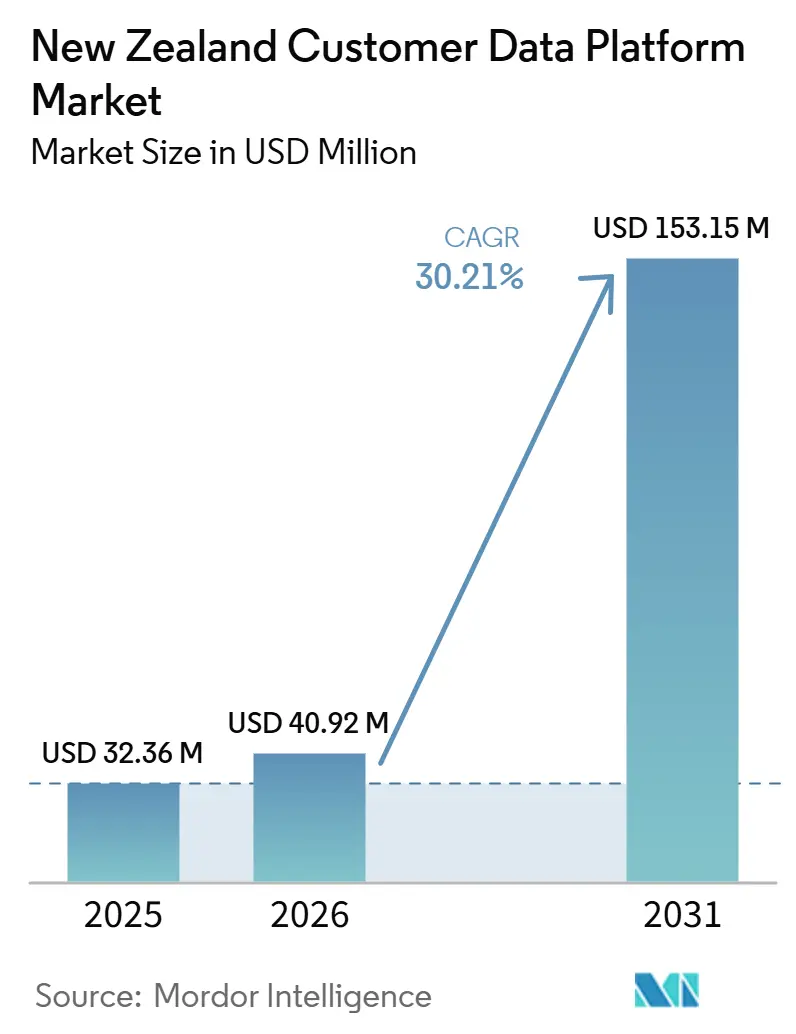

| Base Year Market Size (2025) | USD 32.36 Million |

| Market Size (2026) | USD 40.92 Million |

| Market Size (2031) | USD 153.15 Million |

| Growth Rate (2026 - 2031) | 30.21% CAGR |

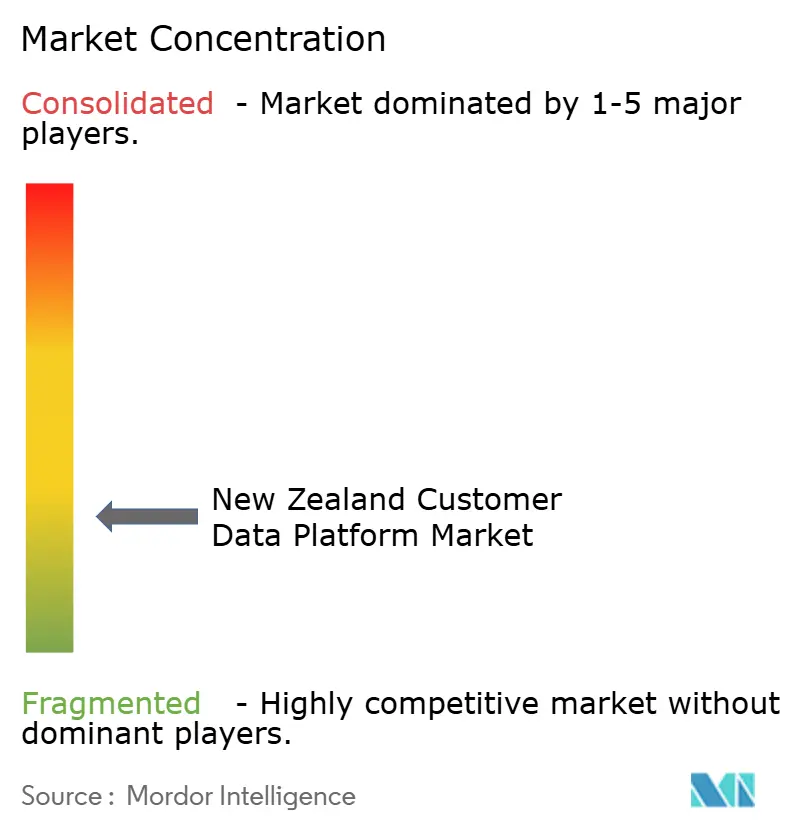

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

New Zealand Customer Data Platform Market Analysis by Mordor Intelligence

The New Zealand customer data platform market size was valued at USD 32.36 million in 2025 and is forecast to reach USD 153.15 million by 2031, growing at a CAGR of 30.21% from 2026 to 2031. The New Zealand customer data platform market is expanding as enterprises shift away from fragmented records and toward unified, consent-aware customer profiles that can support activation across marketing, service, and analytics workflows. Regulatory change is also increasing the importance of interoperable, traceable customer data management, especially in sectors where data sharing, consent handling, and audit readiness now affect procurement decisions. Demand is further supported by the country’s concentrated retail, media, and financial services base, where a smaller number of large data holders can move faster on collaboration, measurement, and identity matching once the right platform is in place. Vendor competition is increasingly shaped by AI functionality, cloud compatibility, and the ability to work across warehouse, application, and channel environments without adding heavy duplication or governance overhead. This leaves the greatest opportunity in solutions that simplify activation, reduce integration friction, and help both large enterprises and smaller firms move raw customer data into measurable commercial use.

Key Report Takeaways

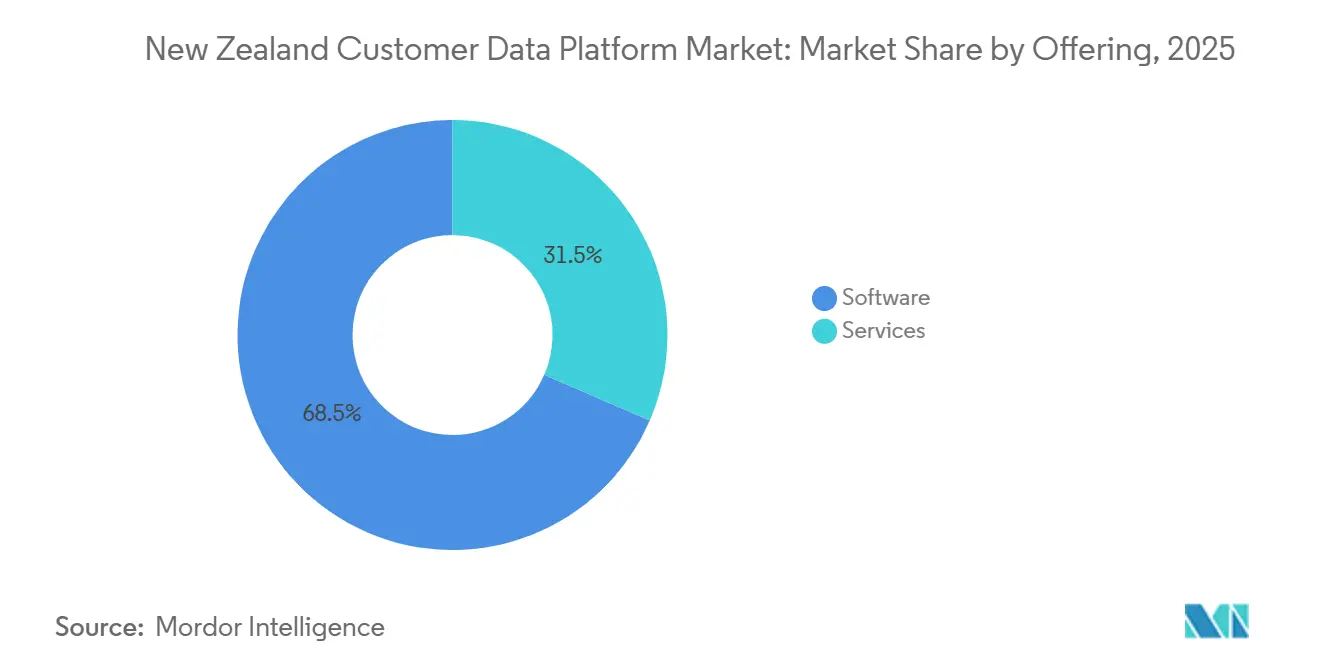

- By offering, software held 68.49% share of the New Zealand customer data platform market in 2025, while services are projected to expand at a 33.09% CAGR through 2031.

- By deployment mode, cloud accounted for 71.22% share of the New Zealand customer data platform market in 2025 and is projected to expand at a 32.40% CAGR through 2031.

- By organization size, large enterprises held 70.14% share of the New Zealand customer data platform market in 2025, while small and medium enterprises are projected to grow at a 32.76% CAGR through 2031.

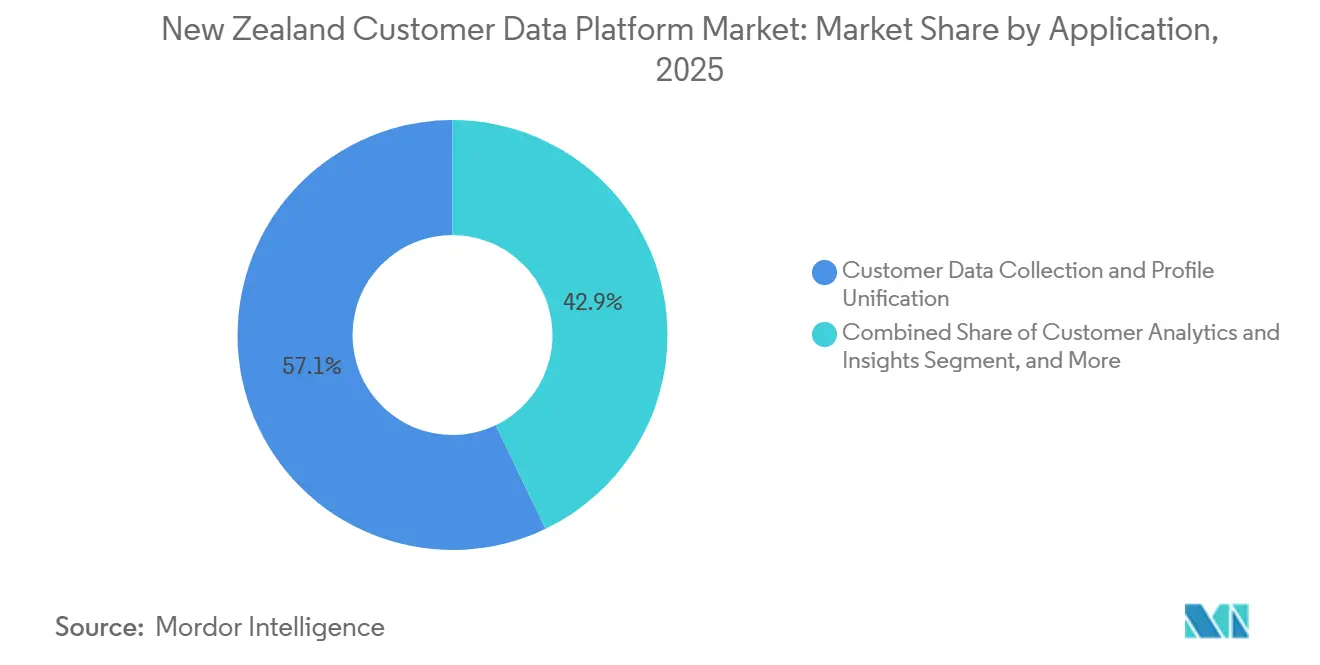

- By application, customer data collection and profile unification accounted for 57.12% of the market share in 2025, while audience segmentation and personalization are projected to expand at a 31.98% CAGR through 2031.

- By end-user industry, retail and e-commerce held 28.44% share of the New Zealand customer data platform market in 2025, while banking, financial services, and insurance are projected to grow at a 31.67% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

New Zealand Customer Data Platform Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Need for Unified Customer Profiles | +7.5% | National, with early gains in Auckland and Wellington business hubs | Short term (≤ 2 years) |

| Rising Demand for Personalized Customer Experiences | +6.8% | National, strongest in retail-dense Auckland and Hamilton | Short term (≤ 2 years) |

| Acceleration of First-Party Data Strategies | +5.2% | National, with APAC spillover from joint Australia and New Zealand CDP deployments | Medium term (2-4 years) |

| Artificial Intelligence and Machine Learning Enabled Customer Activation | +4.5% | National, with early adoption gains in BFSI and telecom | Medium term (2-4 years) |

| Warehouse-Native Data Activation and Reverse ETL Adoption | +3.2% | National, led by Snowflake and Databricks user base | Medium term (2-4 years) |

| Real-Time Identity Resolution for Always-On Engagement | +2.8% | National, focused in omnichannel retail and media sectors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Need for Unified Customer Profiles

The New Zealand customer data platform market is being driven first by the simple need to consolidate scattered customer records into a single usable profile across stores, apps, web journeys, loyalty systems, and service channels. Many enterprises already collect enough data to personalize outreach, but disconnected systems still prevent them from recognizing the same customer across business units and touchpoints. Motorcorp Distributors Limited used Salesforce Data Cloud to unify customer and vehicle data from multiple global and local systems, demonstrating that even a focused business case can depend on profile stitching before downstream activation begins. The commercial value of a unified profile also increases because segmentation, measurement, attribution, and suppression rules work more effectively once the profile is stable and up to date. Amperity’s January 2026 launch of its Customer Data Agent also reflected this shift from passive data storage toward active use of identity-resolved data in live segments and journeys. As more firms in the New Zealand customer data platform market treat profile quality as a foundation rather than a feature, vendors with stronger identity resolution and cleaner activation workflows are likely to keep gaining attention.

Rising Demand for Personalized Customer Experiences

The New Zealand customer data platform market is also benefiting from the need to personalize customer interactions across digital and assisted channels without losing speed or consistency. Personalization is no longer limited to campaign messaging, as firms now seek real-time offers, service prompts, retention actions, and journey decisions that respond to current behavior. Spark New Zealand used Tealium’s real-time CDP with its Kapello AI decisioning engine to activate first-party data across customer touchpoints, demonstrating how CDP value increasingly depends on execution rather than storage alone. This demand is especially relevant in retail, telecom, and banking, where products are easy to compare, and experience quality often shapes conversion and retention more than product differences. Retail research published in 2025 also showed that personalization remained a major priority for brands, even as execution lagged due to fragmented systems and tool sprawl. That gap continues to favor platforms in the New Zealand customer data platform market that can connect data, intelligence, and activation within a single operational layer.

Acceleration of First-Party Data Strategies

The New Zealand customer data platform market is gaining support from the wider shift toward first-party data ownership as third-party identifiers lose reliability and regulatory tolerance tightens. This change matters because firms can no longer treat customer data strategy as a media issue only, since identity, consent, and activation now sit closer to core operating infrastructure. Adobe launched Real-Time CDP Collaboration in Australia and New Zealand in May 2025 to help brands and publishers collaborate on first-party audiences without exposing underlying customer data, demonstrating the region's move toward consent-based audience matching. IAB New Zealand also highlighted the growing appeal of composable CDP models, which reflects a broader effort to keep first-party assets under enterprise control while still enabling downstream activation. As this model spreads, the New Zealand customer data platform market is likely to reward vendors that help firms activate owned data across media, loyalty, analytics, and AI use cases without forcing them into rigid platform structures. The practical result is that firms that delayed first-party investment now face a higher catch-up cost than those that already built stable consented records and reusable profile logic.

Artificial Intelligence and Machine Learning Enabled Customer Activation

AI and machine learning are also shaping the New Zealand customer data platform market as CDPs move from record unification to live decisioning and next-best-action support. This shift matters because firms want customer data systems to do more than organize data; they want those systems to recommend actions and trigger responses while the interaction is still relevant. Westpac New Zealand’s recognition for its use of the FICO Platform reflected work on hyper-personalization and omni-channel engagement, showing that AI-led decisioning has already moved into real financial services use cases in the country.[1]FICO Marketplace, “Westpac NZ Boosts Hyper-Personalization with FICO Platform,” FICO Marketplace, marketplace.fico.com ANZ Bank’s collaboration with Bud Financial, supported by Nvidia AI technology, also pointed to rising demand for natural language analytics and more advanced customer segmentation in banking operations across Australia and New Zealand. Generative AI is also reducing implementation friction because coding and orchestration tasks can now be handled more quickly within composable environments. That combination of better decisioning and lower build effort is widening the addressable opportunity in the New Zealand customer data platform market beyond the earliest large-enterprise adopters.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data Privacy and Consent Management Complexity | -3.5% | National, with heightened sensitivity in financial services and healthcare | Short term (≤ 2 years) |

| Integration Burden across Legacy and Cloud Systems | -2.8% | National, acute for enterprises with pre-cloud ERP and CRM infrastructure | Medium term (2-4 years) |

| Skills Gap in Customer Data Engineering and Activation | -2.2% | National, most acute in secondary cities and the SME tier | Medium term (2-4 years) |

| Budget Scrutiny for Multi-Tool MarTech Stack Consolidation | -1.8% | National, most pronounced in retail and media sectors under margin pressure | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data Privacy and Consent Management Complexity

The New Zealand customer data platform market is facing a real brake from privacy and consent requirements that are slowing deployment, making it more expensive, and making it more dependent on governance design. The Customer and Product Data Act 2025 raised the compliance stakes for regulated users by creating civil and criminal exposure around consumer data right obligations, including penalties for serious breaches by body corporates. The Privacy Amendment Act 2025 also introduced IPP 3A, effective from May 1, 2026, which requires organizations to notify individuals when their information is collected indirectly from third-party sources. That matters directly to CDP users because suppression rules, preference centers, ingestion logic, and downstream activation controls all need to reflect those obligations. ASI’s 2026 compliance guidance for IPP 3A also underscored the operational burden that these requirements place on IT and data teams. As a result, buyers in the New Zealand customer data platform market are placing greater weight on auditability and consent handling, even when those capabilities lengthen selection and implementation cycles.

Integration Burden Across Legacy and Cloud Systems

The New Zealand customer data platform market also faces a slower pace of adoption where enterprises still run hybrid environments that combine older core systems with newer cloud engagement tools. The issue is not only technical connectivity, because firms must also decide which source is authoritative, how conflicts are resolved, and how much latency is acceptable before data becomes less useful for activation. JB Hi-Fi’s work with Amperity highlighted the challenge of consistently identifying customers across channels, households, and changing personal details, a problem that often requires deeper engineering than buyers expect at the start of a project. This burden is heavier in sectors that still use pre-cloud ERP and CRM systems or have highly controlled data estates. Tealium’s June 2025 CloudStream launch, built around zero-copy orchestration, reflected the market need to simplify data movement and reduce duplication across complex environments. Until cloud migration deepens, implementation complexity will remain a significant drag on some parts of the New Zealand customer data platform market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Software Leads as Services Scale for Integration Complexity

Software accounted for 68.49% of the New Zealand customer data platform market share in 2025, which shows that buyers still prefer packaged platforms for identity resolution, segmentation, orchestration, and reporting. That preference reflects the need for faster deployment, predictable licensing, and direct connectivity with marketing, commerce, analytics, and service tools already used by enterprise teams. In the New Zealand customer data platform industry, software also benefits from the fact that many buyers want an operational system rather than a custom-built environment that depends on scarce internal engineering talent. The strength of the software segment also aligns with the country’s growing use of cloud data infrastructure and SaaS applications across retail, telecom, and financial services environments. Vendors in this segment are competing on usability, embedded AI, data governance controls, and support for both packaged and composable deployment models.

The New Zealand customer data platform market size for services is projected to expand at a 33.09% CAGR between 2026 and 2031 as enterprises seek help with implementation, identity logic, integration design, consent controls, and ongoing optimization. Services are projected to grow which indicates that buying the platform is only part of the work. Managed service needs are growing because many deployments now connect multiple data sources, multiple activation channels, and multiple teams that do not always share the same operating standards. This increases the influence of local partners and specialists, especially when buyers need to connect global platforms with regional data structures or are limited in-house capacity. Over time, the relationship between software and services is likely to remain complementary, with software driving the installed base and services driving time-to-value, adoption depth, and renewal confidence.

By Deployment Mode: Cloud Dominates as Hybrid Configurations Address Governance Gaps

Cloud captured 71.22% of the market in 2025 and is projected to grow at a 32.40% CAGR through 2031, making it the clear center of current deployment activity. The New Zealand customer data platform market favors cloud architectures because they enable real-time streaming, elastic scale, API-based integration, and cross-channel activation with lower operational friction. Cloud deployment also aligns with buyer expectations for faster updates, reduced infrastructure management burden, and stronger integration with warehouse, commerce, and campaign ecosystems. This structure supports the broader shift toward event-driven customer data operations, where profile refresh, segmentation, and activation need to occur continuously rather than in batches. The segment’s strength also reflects the practical reality that many leading vendors now develop their newest AI and orchestration capabilities first in cloud-based environments.

On-premises deployment still matters in government, healthcare, and other controlled settings where migration pace is slower, and governance rules remain stricter. Hybrid models are therefore emerging as a practical middle path, allowing firms to maintain sensitive data controls while leveraging cloud resources for identity processing, orchestration, and activation. Mitre 10 New Zealand’s Snowflake AI Data Cloud implementation for personalization and pricing optimization illustrated how firms can modernize customer data use without abandoning governance discipline. Tealium’s CloudStream release also showed how vendors are adapting to this demand by enabling zero-copy orchestration across distributed environments. As a result, cloud remains dominant, but hybrid architecture is likely to stay important for buyers who want flexibility without compromising governance.

By Organization Size: Large Enterprises Anchor Demand as SMEs Build Momentum

Large enterprises held 70.14% of the New Zealand customer data platform market in 2025, supported by the scale and complexity of their customer data environments. These organizations generate higher interaction volumes and face greater revenue risk from poor identity resolution, weak personalization, and inconsistent cross-channel service. They also have larger budgets, more formal data governance structures, and stronger incentives to connect customer data across marketing, service, commerce, and analytics teams. This makes them the natural early adopters of enterprise-grade CDP platforms, especially in retail, telecommunications, media, and financial services. In the New Zealand customer data platform industry, large accounts also tend to shape vendor roadmaps because they demand deeper controls, stronger interoperability, and broader support across multiple use cases.

Small and medium enterprises are projected to expand at a 32.76% CAGR through 2031, making them the fastest-growing organizational segment. Growth in this tier is being supported by modular products, simplified onboarding, and commerce-native integrations that reduce implementation effort. Vendors that can package segmentation, automation, and first-party data handling into lighter workflows are better positioned to move beyond the enterprise core. Klaviyo’s February 2026 emphasis on the Klaviyo Data Platform and its strong Q1 2026 revenue growth reflected the commercial traction of SME-oriented customer data and activation tools. The implication for the New Zealand customer data platform market is that future volume growth will increasingly come from buyers who need simpler deployment and faster activation rather than from those pursuing large custom builds.

By Application: Data Unification Holds the Base as Personalization Lifts Growth

Customer data collection and profile unification accounted for 57.12% of the application segment in 2025, confirming that most deployments still begin with the need to consolidate fragmented records into a single, governed environment. This application remains foundational because every later use case depends on accurate identity matching, stable records, and clearer data lineage. For many organizations, the first commercial gain from a CDP comes not from automation alone, but from reducing duplication, improving record confidence, and creating one consistent customer view across teams. The New Zealand customer data platform market, therefore, still relies heavily on unification as the point of entry, even as more advanced use cases gain budget. This pattern also explains why vendors continue to invest in identity resolution, ingestion flexibility, and profile governance rather than focusing only on downstream activation features.

Audience segmentation and personalization are projected to grow at a 31.98% CAGR through 2031, making them the fastest-moving application areas. Once firms stabilize their data layer, they usually shift their attention to revenue-focused uses such as targeted engagement, customer journey refinement, and decisioning based on recent behavior. Spark New Zealand’s use of Tealium with Kapello AI showed how a real-time customer data layer can support continuous activation rather than static reporting.[2]Tealium, “How Spark New Zealand Scaled Real-Time Personalisation with Tealium and Kapello,” Tealium, tealium.com Consent and preference management are also becoming more visible application needs as privacy obligations extend beyond storage into notification, suppression, and channel-level execution. The result is that the New Zealand customer data platform market is moving steadily from basic aggregation toward operational use cases that require speed, AI support, and stronger coordination between data and engagement systems.

By End-User Industry: Retail Leads Today While BFSI Sets the Pace Ahead

Retail and e-commerce accounted for 28.44% of the New Zealand customer data platform market in 2025, making the sector the largest current adopter. The sector’s lead reflects its daily need to connect browsing, purchase, loyalty, fulfillment, and service data while responding quickly to shifts in pricing and customer expectations. Retail buyers also tend to feel the impact of weak identity resolution more quickly because even small breaks in personalization or attribution can affect repeat purchase rates and margin performance. Mitre 10 New Zealand’s work with Snowflake on personalization and pricing optimization showed how retailers in the region are using governed data environments to support customer-facing decisions. Media, telecom, healthcare, industrial, and government users remain important as well, but retail continues to provide a clear commercial case for unified, action-ready profiles.

Banking, financial services, and insurance are projected to expand at a 31.67% CAGR through 2031, making them the fastest-growing end-user group. This growth reflects the overlap between compliance pressure, customer trust requirements, fraud sensitivity, and the need for more relevant digital interactions across channels. Westpac New Zealand’s use of the FICO Platform for hyper-personalization and omni-channel engagement showed how banks are using governed decisioning environments to support customer-facing improvements. ANZ Bank’s work with Bud Financial and Nvidia AI also pointed to a broader shift toward analytics-led segmentation and natural-language customer insights in regional banking operations. In the New Zealand customer data platform market, BFSI is therefore moving beyond back-office data control and using CDP capabilities more directly as a growth, service, and trust lever.

Geography Analysis

The New Zealand customer data platform market is geographically concentrated around Auckland and Wellington because they host a large share of the country’s enterprise activity and digital decision-making roles. Auckland remains the clearest commercial center for the New Zealand customer data platform market because major retail, telecom, media, and financial services groups operate there, and many leading vendors maintain local presence or partner coverage around that base. This concentration matters because early adoption usually follows data volume, channel complexity, and access to implementation support. The market also benefits from being treated with Australia as a shared commercial zone by several technology vendors, which gives local buyers access to APAC product rollouts and regional case material sooner than a stand-alone market of this size might otherwise receive. Adobe’s Real-Time CDP Collaboration launch across Australia and New Zealand in May 2025 reflected that pattern directly. TVNZ’s July 2025 collaboration with Adobe also showed how a New Zealand publisher could become an early operational reference point for privacy-aware audience matching in the region.

Wellington forms the second important axis because public sector institutions and healthcare organizations there have stronger needs for governance of data architecture, compliance, and controlled analytics. That makes Wellington relevant not just for procurement volume, but also for the types of deployment models that gain traction, especially in hybrid and tightly governed environments. Health NZ’s National Data Platform, built on Snowflake hosted on AWS with Accenture and Acumen BI, demonstrated how large-scale public-sector data consolidation is progressing in the country. This kind of activity supports the view that geography in the New Zealand customer data platform market is influenced as much by institutional structure as by population size alone. It also reinforces the demand for vendors that can handle public-sector controls while still supporting near-real-time use cases.

Outside those two centers, Christchurch, Hamilton, and Dunedin are more likely to support lighter SaaS-led deployments tied to mid-market retail, logistics, and service use cases. These locations matter for long-term growth because future expansion depends on moving beyond the enterprise core and reaching firms that need lower-touch onboarding and clearer time-to-value. The New Zealand customer data platform market is therefore likely to reward vendors that can sell and implement remotely, support partner-led delivery, and reduce the need for on-site technical resources. Platforms with strong commerce integrations, simpler data models, and modular pricing are better suited to that provincial demand profile. Geography in this market is not only about where demand exists today; it is also about which vendors can adapt their operating model to reach a broader range of businesses over the forecast period.

Competitive Landscape

The New Zealand customer data platform market remains moderately fragmented, with global platform vendors competing alongside composable and warehouse-native specialists across different buyer needs. Adobe, Salesforce, SAP, Tealium, Segment, RudderStack, Snowplow, and Amperity all appear in the competitive field, but they are not all competing on the same basis. Some vendors emphasize breadth across customer experience systems, while others focus on identity resolution, warehouse compatibility, zero-copy data movement, or AI-enabled decisioning. This keeps competition active across enterprise, mid-market, and technical buyer segments rather than allowing one model to dominate the whole market. The New Zealand customer data platform market also shows a divide between buyers who want a single operational platform and those who prefer a more composable stack with tighter warehouse control.

Recent product moves show how quickly the competitive lines are shifting. Tealium introduced AI at the Edge and AI Decisioning in May 2026, extending its platform toward real-time processing and in-platform decision support rather than limiting its role to collection and routing. Adobe unveiled its CX Enterprise Coworker in April 2026 across Adobe Experience Platform, Real-Time CDP, Customer Journey Analytics, and Journey Optimizer, further strengthening its position in agentic workflow support.[3]Adobe, “Adobe Unveils CX Enterprise Coworker to Build Agentic-Enabled Workflows for Customer Experience Orchestration,” Adobe News, news.adobe.com Salesforce’s Summer 2026 release also strengthened Data Cloud activation and multi-agent orchestration, which supports its push to keep customer data, workflow, and collaboration closer together. In the New Zealand customer data platform market, these moves matter because buyers increasingly compare vendors on how well they support both governed data operations and direct business action.

Competition is also being reshaped by convergence between data infrastructure and marketing execution. BlueConic’s acquisition of Blueshift in June 2026 combined first-party data management with AI-powered cross-channel execution, which signaled a clear move toward integrated customer growth platforms. RudderStack’s June 2026 launch of RudderAI for Snowflake users showed similar pressure from warehouse-native providers to add agentic workflow support across the customer data lifecycle. Amperity’s 2026 launches around customer data agents and real-time customer context also reinforced identity-led activation as a durable point of differentiation. This leaves the New Zealand customer data platform market open to several winning models, especially in healthcare, government, and the SME tier, where no single vendor structure has closed the field.

New Zealand Customer Data Platform Industry Leaders

Salesforce, Inc.

Oracle Corporation

Adobe Inc.

SAP SE

Twilio Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: BlueConic acquired Blueshift on June 17, 2026, combining BlueConic's first-party data CDP with Blueshift's AI-powered cross-channel marketing platform to create an integrated customer growth engine executing across email, push, in-app, SMS, and web. The acquisition marks a decisive convergence between CDP infrastructure and marketing execution within a single platform architecture, with direct implications for vendors in the New Zealand market that still sell data management and campaign orchestration as separate products.

- June 2026: Salesforce released its Summer '26 product update on June 15, 2026, introducing multi-agent orchestration, real-time data activation through Data Cloud, and Slack-first AI workflows as part of its agentic enterprise strategy. These enhancements strengthen Salesforce's CDP positioning for New Zealand enterprise clients across retail, banking, and telecommunications.

- June 2026: RudderStack launched RudderAI at Snowflake Summit 26 on June 2, 2026, introducing a suite of CLI, Model Context Protocol tools, and agents that enable agentic workflows across the customer data lifecycle. The release extends RudderStack's warehouse-native CDP capabilities specifically for Snowflake customers managing complex multi-source data environments.

- May 2026: Tealium unveiled AI at the Edge, AI Decisioning, and new in-platform features on May 7, 2026, extending its hybrid CDP with real-time AI processing capabilities across its 1,300+ integration ecosystem. These capabilities are directly relevant to Tealium's existing New Zealand deployments, including the Spark NZ real-time personalization architecture built on Tealium and the Kapello AI decisioning engine.

New Zealand Customer Data Platform Market Report Scope

The New Zealand Customer Data Platform (CDP) Market comprises software platforms and associated services that help organizations collect, unify, manage, and activate customer data from multiple online and offline sources to create persistent, comprehensive customer profiles. These platforms support audience segmentation, personalization, customer journey orchestration, analytics, and consent management, helping organizations enhance customer engagement and marketing effectiveness. The growing adoption of data-driven marketing strategies, the increasing number of digital transformation initiatives, and the rising demand for personalized customer experiences across industries drive the market. These solutions enable organizations to improve customer insights, optimize omnichannel engagement, and strengthen regulatory compliance in customer data management.

The New Zealand Customer Data Platform Market Report is Segmented by Offering (Software, and Services), Deployment Mode (Cloud, On-Premises, and Hybrid), Organization Size (Large Enterprises, and Small and Medium Enterprises), Application (Customer Data Collection and Profile Unification, Audience Segmentation and Personalization, Marketing Campaign and Customer Journey Orchestration, Customer Analytics and Insights, Consent and Preference Management, and Other Applications), and End-User Industry (Retail and E-Commerce, Banking, Financial Services, and Insurance [BFSI], Healthcare and Life Sciences, Information Technology and Telecom, Media and Entertainment, Industrial Manufacturing, Government and Public Administration, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud |

| On-Premises |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises |

| Customer Data Collection and Profile Unification |

| Audience Segmentation and Personalization |

| Marketing Campaign and Customer Journey Orchestration |

| Customer Analytics and Insights |

| Consent and Preference Management |

| Other Applications |

| Retail and E-Commerce |

| Banking, Financial Services, and Insurance (BFSI) |

| Healthcare and Life Sciences |

| Information Technology and Telecom |

| Media and Entertainment |

| Industrial Manufacturing |

| Government and Public Administration |

| Other End-User Industries |

| By Offering | Software |

| Services | |

| By Deployment Mode | Cloud |

| On-Premises | |

| Hybrid | |

| By Organization Size | Large Enterprises |

| Small and Medium Enterprises | |

| By Application | Customer Data Collection and Profile Unification |

| Audience Segmentation and Personalization | |

| Marketing Campaign and Customer Journey Orchestration | |

| Customer Analytics and Insights | |

| Consent and Preference Management | |

| Other Applications | |

| By End-User Industry | Retail and E-Commerce |

| Banking, Financial Services, and Insurance (BFSI) | |

| Healthcare and Life Sciences | |

| Information Technology and Telecom | |

| Media and Entertainment | |

| Industrial Manufacturing | |

| Government and Public Administration | |

| Other End-User Industries |

Key Questions Answered in the Report

How large is the New Zealand customer data platform market?

The New Zealand customer data platform market was valued at USD 32.36 million in 2025 and is forecast to reach USD 153.15 million by 2031 at a 30.21% CAGR from 2026 to 2031.

Which offering segment leads spending in this space?

Software led with 68.49% share in 2025, while services are expected to grow faster at a 33.09% CAGR through 2031.

Why are businesses in New Zealand investing more in customer data platforms?

The main reasons are the need for unified customer profiles, stronger personalization, first-party data strategies, and AI-enabled activation across channels.

Which deployment model is seeing the strongest adoption?

Cloud led with 71.22% share in 2025 and is also projected to grow at a 32.40% CAGR, supported by demand for real-time and scalable activation.

Which end-user group is creating the biggest current demand?

Retail and e-commerce held the largest share at 28.44% in 2025, reflecting the need to connect data across browsing, loyalty, purchase, and service journeys.

Which end-user group is likely to grow the fastest through 2031?

BFSI is projected to expand at a 31.67% CAGR through 2031 as banks increase focus on governed data use, trust, and more relevant digital engagement.

Page last updated on: