Neurosurgery Surgical Power Tools Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

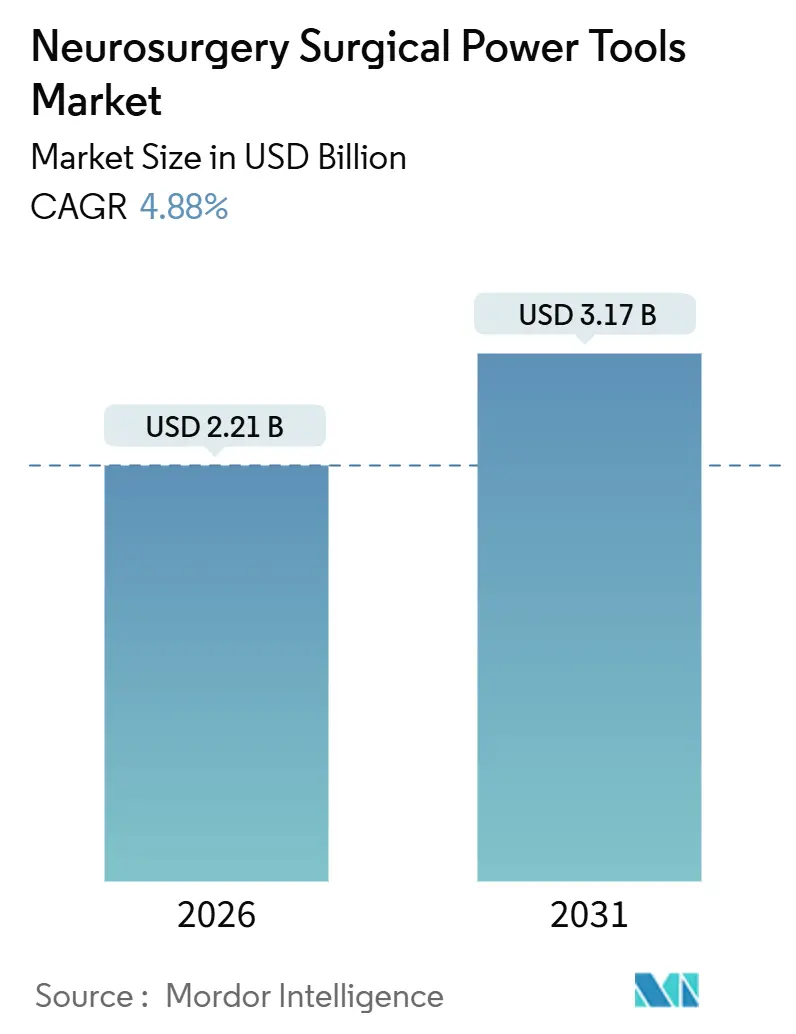

| Market Size (2026) | USD 2.21 Billion |

| Market Size (2031) | USD 3.17 Billion |

| Growth Rate (2026 - 2031) | 4.88% CAGR |

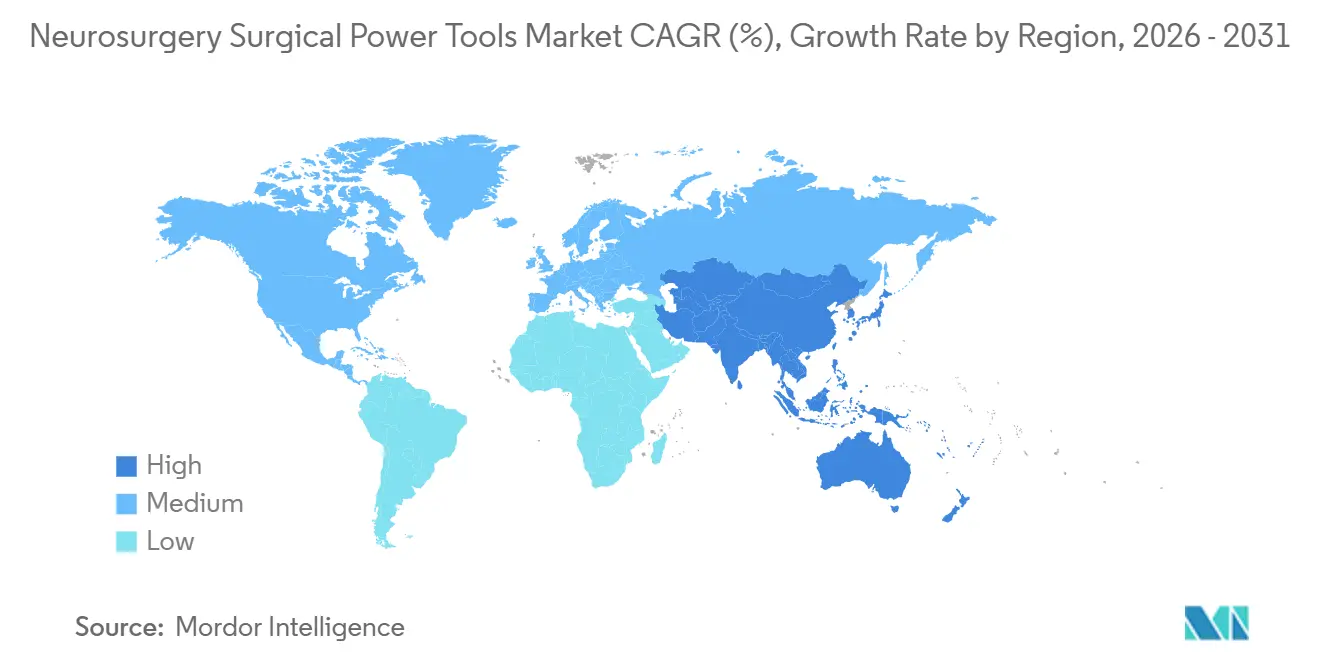

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Neurosurgery Surgical Power Tools Market Analysis by Mordor Intelligence

The Neurosurgery Surgical Power Tools Market size is estimated at USD 2.21 billion in 2026, and is expected to reach USD 3.17 billion by 2031, at a CAGR of 4.88% during the forecast period (2026-2031).

Demand is anchored by rising stroke, traumatic brain injury, and tumor volumes that keep procedure counts high even as capital budgets stay tight. Hospital purchasing decisions now weigh navigation-robotics integration, cordless workflow efficiency, and infection-control features alongside torque performance, which tempers price elasticity. Workforce shortages in several low- and middle-income regions are restraining total case volumes, yet ambulatory surgical centers (ASCs) in the United States, Germany, China, and India are absorbing lower-acuity cranial biopsies and single-level decompressions, thereby expanding installed base opportunities. Competitive dynamics favor modular ecosystems that allow hospitals to add drill, saw, or reamer handpieces incrementally rather than commit to a full console at the outset.

Key Report Takeaways

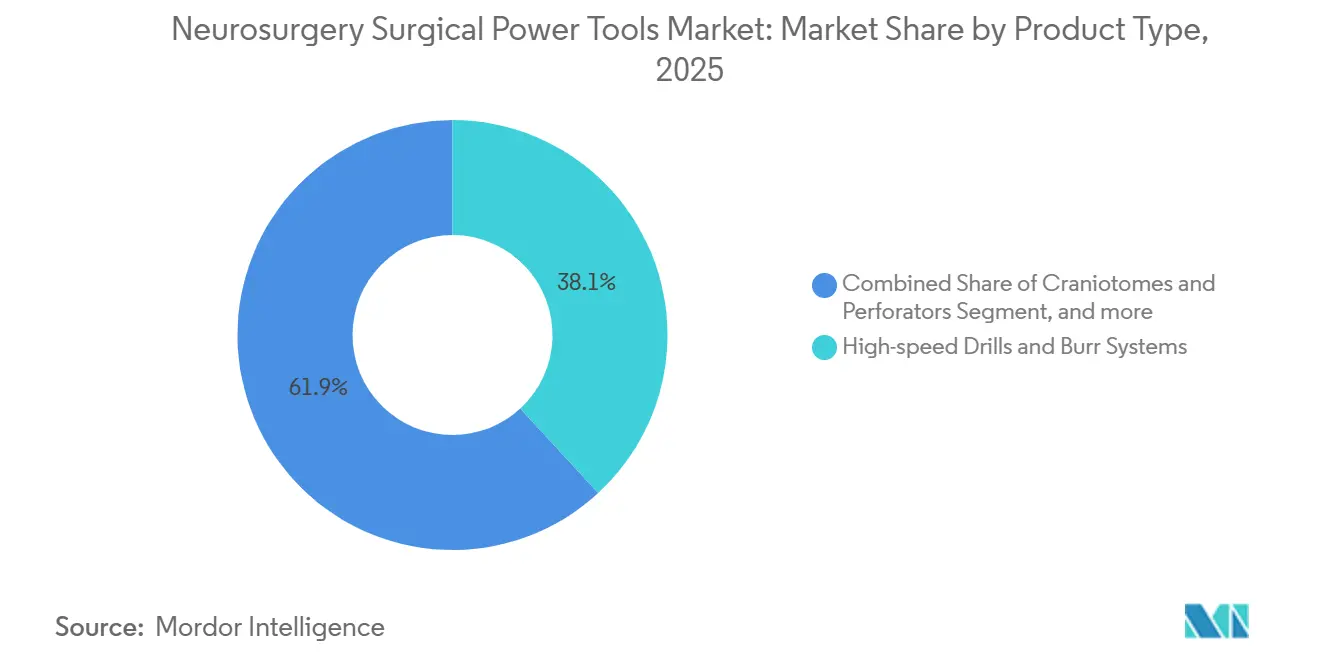

- By product type, high-speed drills and burr systems led the neurosurgery surgical power tools market with 38.14% market share in 2025, while battery-powered platforms are forecast to expand at a 7.18% CAGR through 2031.

- By power source, electric corded systems retained 43.12% of 2025 revenue, whereas battery platforms will record the highest growth at 7.18% through 2031.

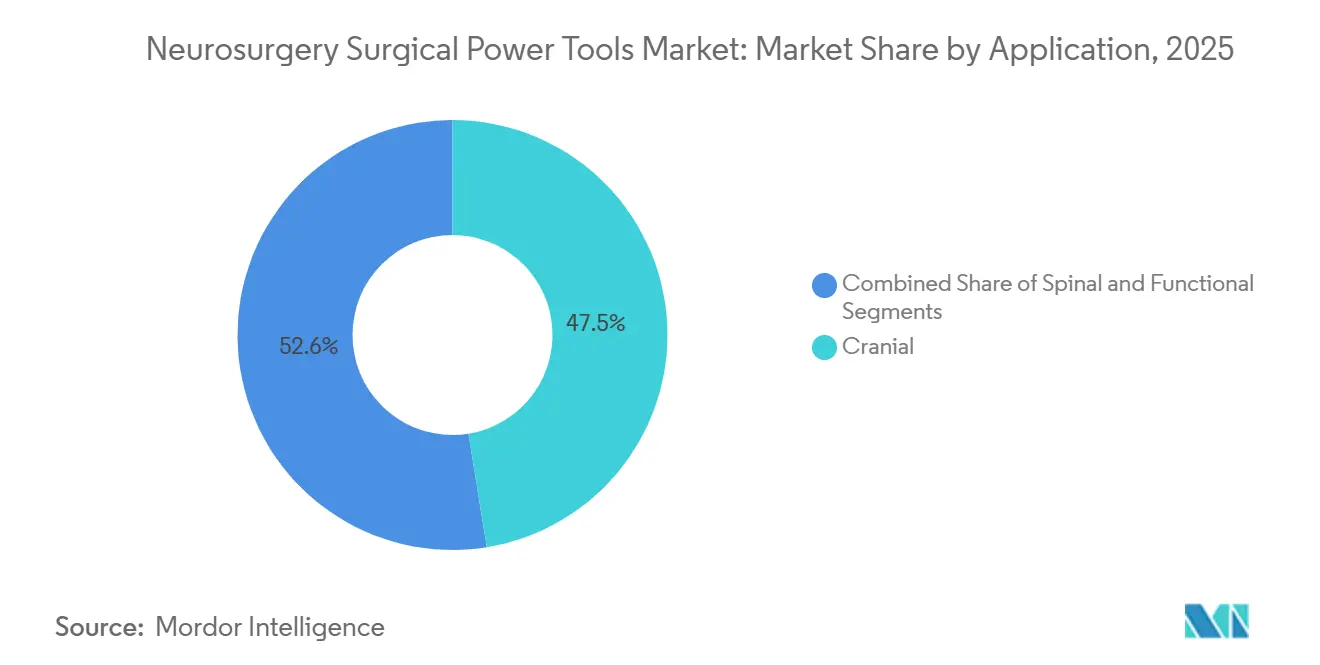

- By application, cranial procedures captured 47.45% of the neurosurgery surgical power tools market size in 2025, and spinal procedures are advancing at a 7.03% CAGR to 2031.

- By end user, hospitals accounted for 47.89% of global revenue in 2025, yet ASCs are projected to post a 5.43% CAGR through 2031 as payers steer appropriate cases to outpatient settings.

- By geography, North America held 49.67% revenue share in 2025, while Asia-Pacific is expected to grow at a 6.57% CAGR through 2031 on the back of public-hospital expansion and surgeon training initiatives.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Neurosurgery Surgical Power Tools Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising neurosurgical caseload and disease burden | +1.2% | Global, highest absolute volumes in Asia-Pacific and North America | Long term (≥ 4 years) |

| Adoption of minimally invasive cranial and spine procedures | +1.0% | North America and EU lead; Asia-Pacific adoption accelerating post-2025 | Medium term (2–4 years) |

| Advances in high-speed drills and console ecosystems (navigation/robotics integration) | +0.9% | North America, Western Europe, Japan, South Korea, Singapore | Medium term (2–4 years) |

| Shift toward cordless/battery systems supporting ASC workflows | +0.8% | North America core; EU following; limited MEA/Latin America penetration | Short term (≤ 2 years) |

| Bedside cranial access expansion via auto-stop battery drills | +0.6% | Trauma centers worldwide; fastest uptake in North America and EU | Short term (≤ 2 years) |

| Infection-control pressure accelerating semi-disposable burrs/perforators | +0.5% | Europe and North America, with growing interest in developed Asia-Pacific hubs | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rising Neurosurgical Caseload and Disease Burden

Neurological conditions affected 3.1 billion individuals in 2024, with stroke and traumatic brain injury accounting for most disability-adjusted life years lost. Newly diagnosed brain and central nervous system cancers numbered 321,731 that year, sustaining demand for craniotomy and decompression work that relies on high-speed burr systems. Surgeon capacity has not kept pace; China recorded only 0.94 neurosurgeons per 100,000 residents in 2024, and densities are lower in India and much of Africa. This mismatch increases the premium on drills that shorten operating time and incorporate auto-stop features to ease the learning curve. Europe and North America also face accelerating caseloads as populations age, with degenerative spine disease and aneurysm incidence rising sharply after age 65. Together, these factors guarantee that the neurosurgery surgical power tools market continues to post procedure growth even where capital budgets lag.

Adoption of Minimally Invasive Cranial and Spine Procedures

Endoscopic endonasal skull-base surgery, tubular spinal decompression, and percutaneous pedicle fixation require compact drill profiles and precise depth control. United States endoscopic spine cases rose at a 20% compound annual rate between 2017 and 2022, even though absolute volumes remained modest, illustrating how quickly new techniques can take off once surgeons see early success. Battery drills with integrated torque-limiting sensors reduce the risk of dural breach, an outcome that can otherwise extend length of stay by 3 to 5 days. Payers reinforce the shift by reimbursing minimally invasive (MIS) codes at rates more favorable than for open surgery, especially in ASCs. Vendors that fail to miniaturize handpieces or embed real-time navigation risk losing share, as MIS growth will outpace open volumes through 2031.

Advances in High-Speed Drills and Console Ecosystems

Navigation and robotics are now bundled with drill consoles that cost more than USD 1 million per suite. Medtronic’s Mazor X Stealth Edition overlays CT and MRI datasets in real time and has cut screw misplacement by 30% in fusion cases. Stryker’s Q Guidance and Globus Medical’s ExcelsiusGPS offer comparable accuracy gains, making software ecosystem lock-in—rather than raw torque—the decisive factor in capital bids. Because retraining surgeons can entail 10 to 15 proctored cases, hospitals tend to stick with incumbents, further concentrating the neurosurgery surgical power tools market. The resulting barrier opens space for agnostic modular solutions that field surgical planning APIs without proprietary limits.

Shift Toward Cordless Battery Systems Supporting ASC Workflows

The United States counted 6,300 Medicare-certified ASCs in 2025, collectively performing 3.4 million procedures, and neurosurgical codes are being added to the outpatient list each review cycle. Cordless drills streamline turnover by eliminating consoles and cabling, a priority where 15-minute room flips are the norm. Modern lithium-ion packs supply 60 to 90 minutes of continuous high-speed drilling and now include Bluetooth telemetry that warns staff when the charge drops below 20%. ASCs favor single-vendor charging stations that can handle drills, saws, and reamers to keep the footprint minimal. Hospitals still rely on corded units for multi-level fusions or skull-base vascular cases where unlimited runtime is essential, preserving a two-tier product mix within the neurosurgery surgical power tools market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital and lifecycle costs for premium neurosurgery platforms | -1.1% | Global, most acute in LMIC public hospitals and smaller ASCs | Long term (≥ 4 years) |

| Neurosurgical workforce shortages limiting adoption in LMICs | -0.9% | Asia-Pacific, Africa, and Latin America | Long term (≥ 4 years) |

| Aerosolization risk with high-speed drilling requiring added controls | -0.6% | North America and EU regulatory focus; Asia-Pacific adoption lagging | Medium term (2–4 years) |

| OR noise exposure and surgeon fatigue influencing device selection | -0.5% | Global, heightened attention in North America and EU | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

High Capital and Lifecycle Costs for Premium Neurosurgery Platforms

Bundles that pair a drill console with navigation and robotics can exceed USD 1 million per room, while annual service contracts add an additional 10% to 15% to the purchase price. Capital committees, therefore, rank neurosurgery below cath labs and hybrid operating rooms in many budget cycles, extending replacement intervals beyond seven years. Constraints are most severe in Latin America and parts of Africa, where public tenders can take two years to complete and often prioritize consumables. Pay-per-use leasing is emerging, but only vendors with dense service networks can guarantee uptime and regulatory compliance. Because such networks are expensive to build, market entry remains difficult for new challengers.

Aerosolization Risk with High-Speed Drilling

High-speed cutting produces aerosols that contain bone fragments and potential pathogens. A 2024 American Journal of Infection Control study measured particle concentrations above 10,000 /m³ during craniotomy, prompting U.S. regulators to recommend negative-pressure ORs with HEPA filtration[1]American Journal of Infection Control, “Particle Load During Craniotomy,” ajicjournal.org. Upgrading ventilation costs USD 15,000 to USD 25,000 per room, with annual filter expenses of USD 2,000 to USD 3,000, squeezing margins at smaller centers. Facilities that defer these investments often restrict the use of high-speed drills, thereby reducing addressable volumes. Manufacturers developing suction-integrated handpieces that capture debris at source may gain a pricing premium as infection-control standards tighten in Europe and North America.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Drills, Retain Core Share as Modular Attachments, Spread

High-speed drills and burr systems accounted for 38.14% of 2025 revenue, reflecting their central role in tumor debulking, skull-base access, and decompression. The neurosurgery surgical power tools market size for this segment is expected to reach USD 1.04 billion by 2031, growing with a 4.6% CAGR as procedure volumes rise. Reamers and drivers will outpace overall growth at 6.09% thanks to expanding spinal fusion demand and surgeons’ preference for platforms that allow attachments to be swapped without re-sterilization. Craniotomes equipped with auto-stop sensors are gaining steady placement in trauma bays where every minute of decompression improves neurological outcomes. Microdebriders and shavers are migrating from ENT to pituitary and clival work, and their integration into console ecosystems raises utilization rates.

Hospitals and ASCs alike now favor systems that house drills, reamers, drivers, and saws on a single motor body, which lowers inventory carrying costs and pushes vendors to design universal couplings. Early adopters report 15% to 20% shorter sterile-processing cycles because fewer instrument trays are needed per case. Market share concentration is highest in cranial kits, yet spinal-focused attachments will narrow the gap by 2031. Smaller entrants position ultra-compact drills for bedside craniectomy, carving a niche insulated from large console suppliers but accounting for less than 3% of total spending.

By Power Source: Battery Growth Outstrips Corded Dominance

Electric corded units held 43.12% neurosurgery surgical power tools market share in 2025, a lead built on unlimited runtime and deep integration with navigation stacks inside tertiary centers. The segment is forecast to grow modestly at 3.1% annually as replacement needs in mature markets offset slower installation elsewhere. Conversely, battery platforms will expand at 7.18% CAGR to 2031, propelled by ASC proliferation in North America and policy-driven outpatient migration in Germany, Australia, and Japan. Improved lithium-ion chemistry now delivers continuous drilling times that match typical cranial cases, eroding one of the last technical barriers to cordless adoption.

Runtime telemetry sent to a central monitor lets circulating nurses swap packs proactively, virtually eliminating intraoperative delays. Pneumatic devices, once a European staple, now occupy under 5% share because hospitals prefer electronics that interface smoothly with digital OR control panels. Vendors lagging on battery performance risk ceding the fast-growing mid-acuity outpatient segment, even if their corded lines remain profitable. For emerging economies where power outages occur, dual-mode systems that accept either a battery or a mains supply offer resilience and are being piloted in India and South Africa beginning in 2026.

By Application: Spine Surges While Cranial Remains Bedrock

Cranial work accounted for 47.45% of revenue in 2025, a testament to the constant demand for tumor, trauma, and vascular interventions. That proportion will slip toward 44% by 2031 because spinal procedures are increasing at a 7.03% CAGR on the back of aging populations and the spread of minimally invasive decompression. U.S. hospital discharge data show more than 350,000 fusion surgeries per year and early adoption of robot-guided pedicle screw placement, both of which favor modular drill platforms. The neurosurgery surgical power tools market size tied to spinal applications is projected to reach USD 1 billion by 2031, narrowing the historical gap with cranial applications.

Functional neurosurgical procedures, such as deep-brain stimulation for movement disorders, occupy a small but premium niche that demands sub-millimeter accuracy. These operations push vendors to refine ergonomic grips, improve vibration dampening, and integrate with stereotactic frames. Over the forecast window, ASCs will absorb single-level decompressions and biopsies, but multilevel fusions and aneurysm clippings will remain hospital-based. Vendors tailoring handpieces for each anatomical site, rather than selling one-size units, are winning preference scores in value-analysis committees.

By End User: ASC Expansion Reshapes Procurement Models

Hospitals accounted for 47.89% of 2025 spending, reflecting their mandate for complex cranial and multi-level spine surgery that requires blood products, ICU beds, and navigation robotics. Average replacement cycles for consoles stretch six to seven years, and many centers negotiate enterprise-wide contracts that bundle drills with imaging and implants. The ASC channel, however, is increasing at a 5.43% CAGR, punching above its historical weight as payers look to trim facility fees. ASCs typically purchase two or three battery handpieces per room and standardize chargers across specialties, a model that minimizes capital outlay but lifts disposables consumption.

Neurosurgery specialty hospitals, although fewer in number, order full robotics suites to attract self-pay international patients, especially in Singapore and the United Arab Emirates. They also serve as reference sites where vendors demonstrate next-generation consoles. In Latin America and parts of Asia, public hospitals with limited budgets lease drill motors and pay per case for navigation software, a service model pioneered by smaller entrants and now mimicked by Stryker and Medtronic to defend share. Across all sites, warranty and uptime guarantees increasingly figure into tender scoring, driving manufacturers to invest in predictive maintenance analytics.

Geography Analysis

North America accounted for 49.67% of 2025 revenue, as dense neurosurgical capacity and favorable reimbursement offset premium console prices. Hospitals credit navigation-robotics systems with lower revision rates, which underpins returns on USD 1 million capital outlays. ASCs numbered 6,300 in 2025 and treated 3.4 million Medicare beneficiaries, expanding the cordless installed base for low-acuity cranial and spine work[2]Centers for Medicare & Medicaid Services, “Medicare-Certified Facilities Report,” cms.gov. Expected regulatory updates continue to add outpatient codes, ensuring that the neurosurgery surgical power tools market will sustain mid-single-digit growth even as hospital procurement slows.

Europe trails on growth, hampered by austerity-driven capital freezes and procurement cycles that can exceed two years for equipment valued above EUR 500,000. Germany alone recorded 222,158 inpatient neurosurgical cases in 2023, but tender rules require value-for-money analyses that slow console purchases. The European Medicines Agency enforces strict post-market surveillance, making local service infrastructure critical. Yet once a device passes health-technology assessment thresholds, long framework agreements tend to lock in supplier relationships, creating annuity revenue streams.

Asia-Pacific will post the fastest regional growth at 6.57% through 2031 as public-hospital construction in China and India accelerates and surgeon-training programs narrow workforce gaps. China’s neurosurgeon density of 0.94 per 100,000 population highlights an unmet need, and India lags further behind. Portable battery drills that cap torque automatically are popular in provincial hospitals where operator experience varies. Mature markets like Japan and South Korea are focusing on replacing first-generation consoles with AI-enabled systems to improve precision for aging cohorts. The Middle East and Africa remain nascent, with projects clustered in Riyadh, Abu Dhabi, and Johannesburg, yet infrastructure investments tied to national health-care visions could lift demand after 2028. South America shows selective upside in Brazil and Mexico where private groups fund MIS spinal suites despite currency volatility.

Competitive Landscape

The neurosurgery surgical power tools market is moderately concentrated. Medtronic, Stryker, and Johnson & Johnson’s DePuy Synthes division together command 60% to 65% of global revenue. Their advantage stems from bundled deals that incorporate drill motors, navigation software, robotic arms, and multi-year service, increasing switching costs for hospitals[3]Medtronic plc, “Press Release FDA Clearance Mazor X Stealth Edition,” medtronic.com. They also compete on AI-driven planning tools that recommend optimal screw paths or drill speeds; these features have already cut pedicle screw misplacement rates by about 30% in clinical series cited by academic centers.

Mid-size competitors such as B. Braun, Conmed, and Karl Storz focus on form-factor innovation. B. Braun’s semi-disposable burr line reduces sterile processing effort, appealing to European ASCs coping with tightened infection control standards. Conmed’s latest battery drill offers a 90-minute runtime that matches full cranial cases, while Karl Storz has partnered with Brainlab to overlay trajectories on endoscopic views, catering to expanded endonasal surgery. Each company garners a share in sub-segments yet lacks the broad portfolio to displace the top three globally.

Start-ups and university spin-outs are applying machine learning to adaptive drill control and predictive maintenance. Regulatory uncertainty around continuously learning algorithms has slowed rollouts, but the U.S. Food and Drug Administration’s Digital Health Center of Excellence published draft guidance in 2025 that clarifies pre-market approval routes. Vendors that can verify outcome improvements in real-world data are likely to win payer support when bundled payments tighten after 2027.

Neurosurgery Surgical Power Tools Industry Leaders

Stryker

Medtronic

B. Braun SE

Zimmer Biomet

Johnson & Johnson

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Arthrex, one of the global leaders in minimally invasive surgical technology, launched Synergy Power, a versatile and reliable battery-powered system designed for a wide variety of orthopedic applications.

- March 2025: Olympus Corp., one of the global medical technology companies committed to making people’s lives healthier, safer, and more fulfilling, launched its first AI-powered clinical decision tool through a strategic partnership with software firm Ziosoft.

Global Neurosurgery Surgical Power Tools Market Report Scope

As per the scope of the report, neurosurgery surgical power tools are specialized devices designed to assist in precise surgical procedures on the brain and nervous system. They include drills, saws, and aspirators that enable accurate removal of tissue or bone. These tools enhance surgical efficiency, safety, and patient outcomes.

The Neurosurgery Surgical Power Tools Market Report is Segmented by Product Type (High-Speed Drills & Burr Systems, Craniotomes & Perforators, Reamers & Drivers, Microdebriders/Shavers, and Saws), Power Source (Electric, Battery-Powered, and Pneumatic), Application (Cranial, Spinal, and Functional/Other), End User (Hospitals, Ambulatory Surgical Centers, and Neurosurgical Specialty Centers), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| High-speed Drills & Burr Systems |

| Craniotomes & Perforators |

| Reamers & Drivers |

| Microdebriders/Shavers |

| Saws |

| Electric |

| Battery-Powered |

| Pneumatic |

| Cranial |

| Spinal |

| Functional/Other neuro procedures |

| Hospitals |

| Ambulatory Surgical Centers |

| Neurosurgical specialty centers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | High-speed Drills & Burr Systems | |

| Craniotomes & Perforators | ||

| Reamers & Drivers | ||

| Microdebriders/Shavers | ||

| Saws | ||

| By Power Source | Electric | |

| Battery-Powered | ||

| Pneumatic | ||

| By Application | Cranial | |

| Spinal | ||

| Functional/Other neuro procedures | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Neurosurgical specialty centers | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What CAGR is projected for the neurosurgery surgical power tools market to 2031?

The market is forecast to expand at a 4.88% CAGR between 2026 and 2031 based on confirmed hospital and ASC purchasing plans.

Which product type currently leads global revenue?

High-speed drills and burr systems held 38.14% of worldwide revenue in 2025, driven by their central role in cranial procedures.

Why are battery-powered systems growing faster than corded platforms?

ASCs favor cordless workflow efficiency and newer lithium-ion packs now provide up to 90 minutes of continuous drilling, removing runtime concerns.

Which region is expected to grow the fastest through 2031?

Asia-Pacific is projected to post a 6.57% CAGR as China and India build neurosurgical capacity and invest in modern instrumentation.

How does navigation integration affect vendor switching costs?

Bundling drills with navigation and robotics raises retraining requirements to 10-15 proctored cases, making hospitals reluctant to change suppliers.

What safety innovation addresses aerosolization risks during drilling?

Integrated suction-irrigation handpieces capture bone dust at the source, reducing airborne particles and helping facilities comply with new ventilation standards.

Page last updated on: