Netherlands Pet Treats Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

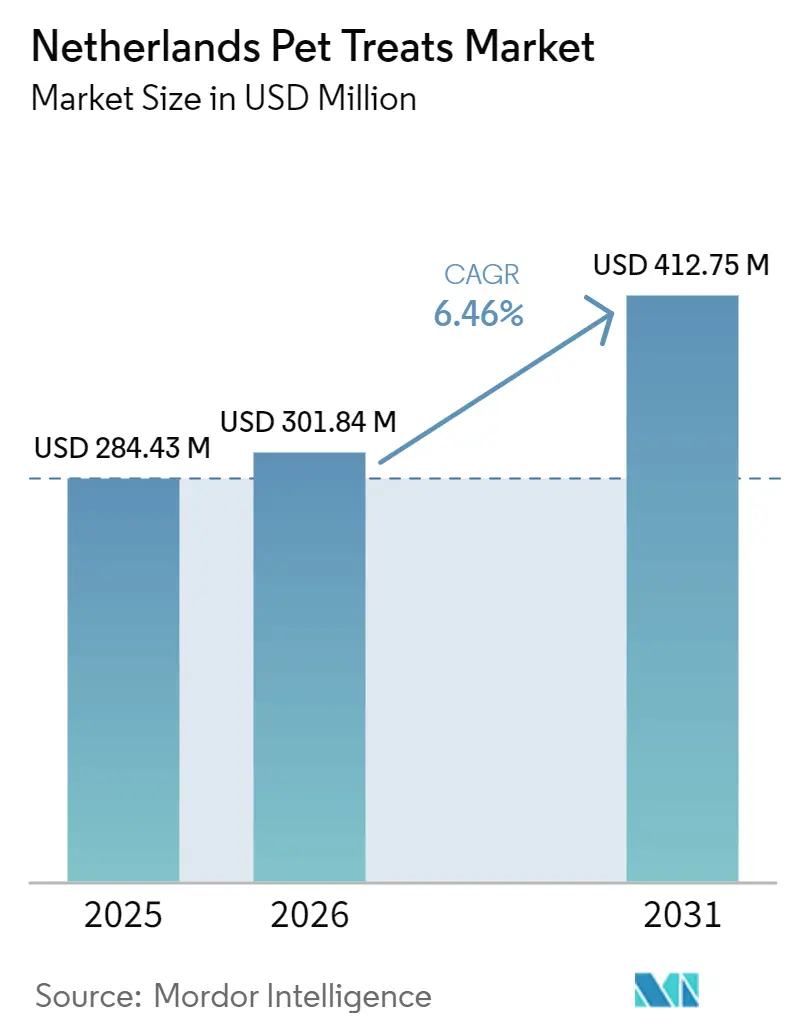

| Base Year Market Size (2025) | USD 284.43 Million |

| Market Size (2026) | USD 301.84 Million |

| Market Size (2031) | USD 412.75 Million |

| Growth Rate (2026 - 2031) | 6.46% CAGR |

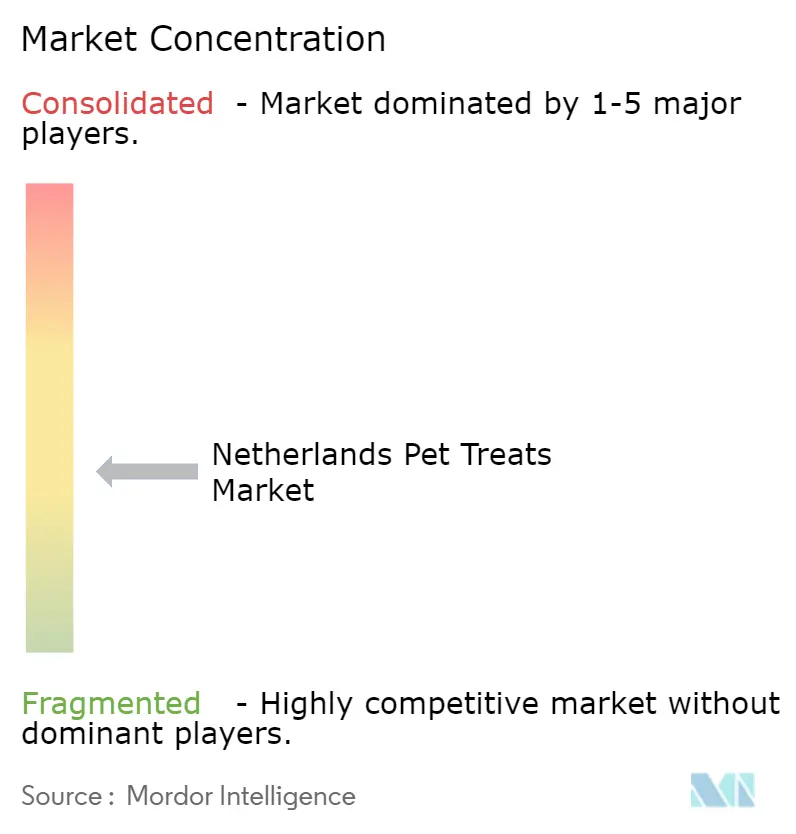

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Netherlands Pet Treats Market Analysis by Mordor Intelligence

The Netherlands pet treats market was valued at USD 284.43 million in 2025 and is projected to grow from USD 301.84 million in 2026 to USD 412.75 million by 2031, registering a CAGR of 6.46% over the period from 2026 to 2031. The market benefits from a well-established companion animal culture and the Netherlands strategic position within the European pet food supply chain. Strong domestic manufacturing capabilities and an efficient distribution network support product innovation, broad product availability, and timely market access across both domestic and neighboring European markets. Growing pet humanization is encouraging owners to purchase premium and functional treats that promote dental health, digestion, immunity, and overall wellness. The continued expansion of specialty retail and e-commerce channels is further supporting premiumization and product differentiation, while regulatory compliance requirements and fluctuations in raw material costs continue to influence product development, pricing strategies, and competitive positioning across the market.

Key Report Takeaways

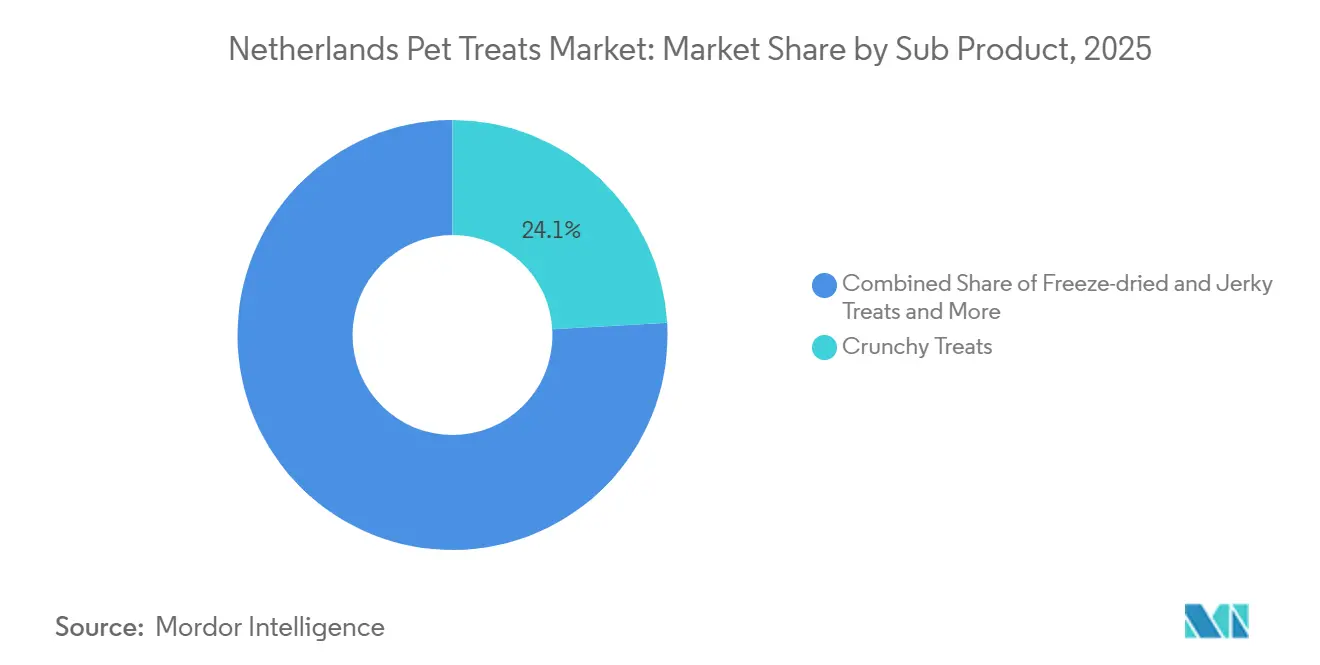

By sub product, the Netherlands pet treats market share for the crunchy treats segment accounted for the largest 24.1% in 2025, while freeze-dried and jerky treats are forecast to grow at the fastest CAGR of 7.6% from 2026 to 2031.

By pets, dogs held the largest 42.7% share in 2025, while the Netherlands pet treats market size for cats is forecast to grow at the fastest CAGR of 7.4% from 2026 to 2031.

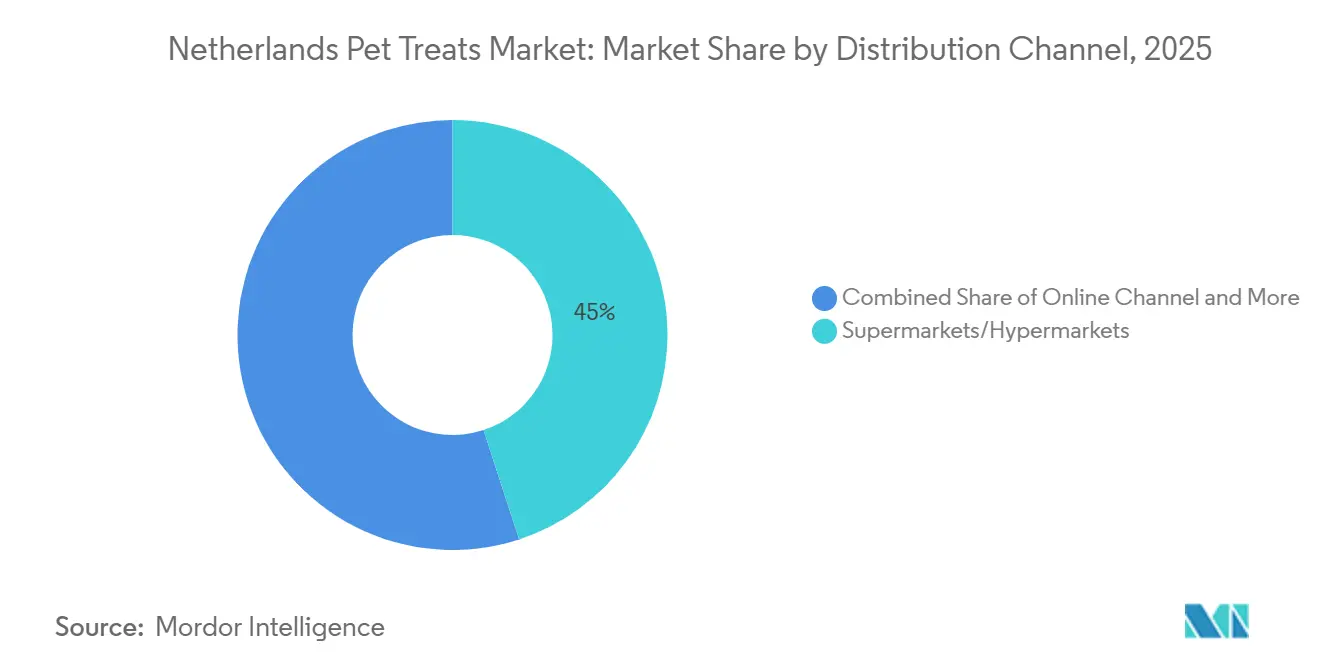

By distribution channel, supermarkets/hypermarkets led with the largest 45.0% share in 2025, while the online channel was projected to grow at the fastest CAGR of 7.9% from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Netherlands Pet Treats Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Pet humanization and wellness-led treat purchases | +1.5% | Netherlands, concentrated in Randstad urban centers | Short term (≤ 2 years) |

| Premiumization and willingness to pay for functional claims | +1.3% | Netherlands and broader Benelux, with spillover to Germany and Belgium | Medium term (2-4 years) |

| Growth of reward-based training and daily reinforcement use cases | +0.8% | National, with early adoption among urban millennial pet owners | Short term (≤ 2 years) |

| E-commerce and subscription replenishment for high-frequency purchases | +0.9% | National, strongest in Amsterdam, Utrecht, and Rotterdam metro areas | Medium term (2-4 years) |

| Sustainability, traceability, and clean-label ingredient preference | +0.7% | Netherlands and Germany, with secondary influence in Belgium and France | Long term (≥ 4 years) |

| Expansion of human-grade, natural, and limited-ingredient portfolios | +1.0% | Netherlands, with spillover to the other region and Scandinavia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Pet Humanization and Wellness-Led Treat Purchases

Pet humanization remains a key growth driver for the Netherlands pet treats market, as owners increasingly incorporate treats into their pets' daily care and wellness routines. According to the Dutch Pet Trade Association (Dibevo) and the Dutch Pet Association (NVG), the Netherlands had 3 million cats in 2025, with 23% of households owning at least one cat, indicating a large and stable companion animal population that supports sustained demand for premium pet products. This growing emotional bond between owners and pets is driving higher spending on natural, functional, and health-oriented treats, including dental, calming, and mobility-support formulations, supporting long-term market growth.

Premiumization and Willingness to Pay for Functional Claims

Premiumization is supporting value growth in the Netherlands pet treats market as consumers increasingly favor products with functional and health-related benefits. According to the Dutch Pet Trade Association (Dibevo) and the Dutch Pet Association (NVG), Dutch households spent an average of EUR 68 (USD 74) per month on pets in 2025, including EUR 53 (USD 58) on pet food and EUR 15 (USD 16) on pet supplies. This reflects a strong willingness to invest in higher-value pet products. This spending pattern supports demand for premium treats with dental care, calming, digestive health, and natural ingredient claims, encouraging manufacturers to expand their scientifically formulated and function-focused product portfolios.

E-Commerce and Subscription Replenishment for High-Frequency Purchases

E-commerce is strengthening the Netherlands pet treats market by making repeat purchases of premium and functional products more convenient for pet owners. The country's high level of online shopping supports subscription-based purchasing and provides access to a wider assortment of pet treats than is typically available in physical stores. According to Statistics Netherlands (CBS), 80.4% of people aged 12 years and older purchased goods or services, including pet food such as pet treats, online during the three months preceding the 2025 survey, reflecting the country's strong digital purchasing culture[1]Source: Statistics Netherlands (CBS), “Digitalisering en kenniseconomie 2025,” cbs.nl.. This widespread adoption enables manufacturers and retailers to expand recurring sales through subscription models, personalized recommendations, and direct-to-consumer channels for pet treats.

Sustainability, Traceability, and Clean-Label Ingredient Preference

Sustainability and ingredient transparency are increasingly influencing purchasing decisions in the Netherlands pet treats market, as consumers seek environmentally responsible and clean-label products. This trend is encouraging manufacturers to invest in recyclable packaging, traceable ingredient sourcing, and natural formulations. A notable example is Mars, Incorporated, which introduced recyclable mono-polypropylene pouches for its WHISKAS wet cat food across selected European markets in 2025, replacing multi-material packaging to improve recyclability[2]Source: Mars, Incorporated, “Mars Debuts Recyclable Pet Food Pouches for WHISKAS,” mars.com.. This packaging initiative reflects the growing emphasis on sustainable pet food packaging and supports wider adoption of environmentally conscious pet treats and premium nutrition products in markets such as the Netherlands.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw material price volatility for animal proteins and specialty inputs | -1.2% | Netherlands and broader European Union, most acute for freeze-dried and jerky stock keeping units | Short term (≤ 2 years) |

| Tightening claim substantiation and ingredient compliance requirements | -0.8% | European Union wide, with Netherlands enforcement through the Netherlands Food and Consumer Product Safety Authority (NVWA) | Medium term (2-4 years) |

| Shelf-space pressure from private label and retailer-controlled assortments | -0.7% | National, concentrated in Albert Heijn, Jumbo, and Lidl channels | Medium term (2-4 years) |

| Functional treat credibility risk, especially for overstated health claims | -0.6% | Netherlands, with secondary spillover risk in Germany and Belgium | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Raw Material Price Volatility for Animal Proteins and Specialty Inputs

Raw material price volatility remains a significant challenge for the Netherlands pet treats market, as premium treats rely heavily on high-quality poultry proteins such as chicken. Rising meat prices increase production costs and make it difficult for manufacturers to maintain premium quality while keeping products competitively priced. According to the European Commission's Poultry Market Situation (April 2026), the European Union weekly average broiler price reached EUR 298 (USD 339) per 100 kg in April 2026, remaining at historically elevated levels[3]Source: European Commission, “Meat and Eggs Market Situation (June 2026),” agriculture.ec.europa.eu.. Higher poultry procurement costs directly affect manufacturers of protein-rich pet treats, limiting pricing flexibility and reducing profit margins, particularly in premium and freeze-dried product segments.

Tightening Claim Substantiation and Ingredient Compliance Requirements

Tightening claim substantiation and ingredient compliance requirements are increasing compliance costs in the Netherlands pet treats market, particularly for products marketed with functional benefits such as dental care, calming, digestive health, and joint support. According to the European Pet Food Industry Federation (FEDIAF), the 2025 edition of the Nutritional Guidelines introduced updated nutrient tables and clarified annexes to align with the latest scientific knowledge and regulatory requirements in European countries, including the Netherlands. These revisions require manufacturers to review formulations, technical documentation, and product labeling prior to commercialization. As a result, companies incur additional validation, reformulation, and packaging costs, which can delay product launches and create greater challenges for smaller pet treat manufacturers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sub Product: Crunchy Formats Dominant, Freeze-Dried Gaining Fast

The Netherlands pet treats market share for the crunchy treats segment accounted for the largest 24.1% in 2025. This position is supported by widespread availability across supermarkets and specialty pet stores, competitive price points, and strong consumer familiarity with everyday reward and dental care applications. These products appeal to a broad range of dog owners due to their ease of storage, simple portioning, and suitability for routine feeding. Manufacturers also benefit from established production processes and high-volume retail distribution, which allow crunchy treats to remain the foundation of category sales across the Dutch pet treats market.

Freeze-dried and jerky treats are forecast to grow at the fastest CAGR of 7.6% from 2026 to 2031. Growth is driven by increasing consumer preference for minimally processed, protein-rich products with transparent ingredient lists and premium positioning. Pet owners are becoming more attentive to nutritional quality and sourcing practices, prompting manufacturers to introduce single-protein recipes, limited-ingredient formulations, and natural preservation methods. These formats align with the broader premiumization trend, enabling suppliers to differentiate on product quality rather than price. Continued innovation in functional ingredients further supports long-term expansion within this premium sub-product segment.

By Pets: Dogs Anchor Volume, Cats Drive Incremental Growth

Dogs accounted for the largest share of 42.7% in 2025, maintaining their position as the dominant pet segment. Regular treat-giving habits, training routines, and preventive dental care continue to support higher consumption among dog owners. Manufacturers offer a broader assortment of flavors, textures, and functional products for dogs than for other companion animals, increasing shelf presence across retail channels. Frequent product innovation, strong brand recognition, and established purchasing behavior continue to reinforce demand, enabling the dog segment to generate consistent sales and remain the primary contributor to overall market value.

Cats are forecast to grow at the fastest CAGR of 7.4% from 2026 to 2031. Rising interest in species-specific nutrition, enrichment products, and functional health benefits is encouraging manufacturers to expand specialized cat treat portfolios. Premium formats such as lickable treats, freeze-dried protein snacks, and dental formulations are gaining greater consumer acceptance as they address changing feeding preferences and indoor lifestyles. Companies are also investing in improved palatability and nutritional formulations tailored to feline requirements. These developments position cat treats as the fastest-growing opportunity within the market, while complementing its established dependence on dog-focused products.

By Distribution Channel: Supermarkets Lead Value, Online Accelerates Share

Supermarkets/hypermarkets accounted for a 45.0% share in 2025, making them the dominant distribution channel. Their position is supported by the convenience of one-stop shopping, wide product assortments, and frequent promotional campaigns that encourage impulse purchases alongside regular grocery shopping. Large retail chains provide manufacturers with nationwide visibility while supporting high-volume sales of mainstream and premium products. Established relationships between retailers and major pet food companies also ensure consistent product availability, making supermarkets and hypermarkets the primary purchasing destination for pet treats across the Netherlands.

The online channel is projected to grow at the fastest CAGR of 7.9% during 2026 to 2031. Growing consumer preference for home delivery, subscription purchasing, and access to wider product assortments continues to drive digital sales. Online platforms allow brands to present detailed nutritional information, ingredient transparency, and customer reviews, supporting purchases of premium and functional products. Digital retailers also offer greater visibility for niche products that receive limited shelf space in physical stores. As personalized shopping experiences continue to improve, online channels are projected to capture a growing share of premium pet treat demand.

Geography Analysis

The Netherlands pet treats market benefits from a well-developed pet care ecosystem, advanced retail infrastructure, and strong regional trade connectivity, enabling rapid commercialization of premium and functional pet products. The country's strategic location supports efficient distribution across the European Union while facilitating imports of ingredients and finished products from neighboring markets. A mature grocery sector, extensive specialty pet retail network, and expanding e-commerce ecosystem provide manufacturers with multiple sales channels. These advantages allow suppliers to introduce innovative formulations quickly while maintaining broad product availability and efficient inventory replenishment throughout the domestic market.

Consumer demand varies across different parts of the country, reflecting differences in retail infrastructure and purchasing behavior. Urban regions such as Amsterdam, Rotterdam, Utrecht, and The Hague demonstrate stronger adoption of premium, natural, and functional pet treats due to greater access to specialty retailers and online fulfillment services. Rural areas continue to rely more heavily on supermarkets and local retail outlets for routine pet purchases, supporting demand for mainstream products. This geographic diversity encourages manufacturers to develop channel-specific product assortments and pricing strategies that address varying consumer preferences across the Netherlands.

Regional manufacturing and distribution networks continue to shape the Netherlands pet treats market by improving product availability across domestic and neighboring European markets. The country's established logistics infrastructure and strategic location support the efficient movement of pet treat products throughout the region. In December 2025, The Nutriment Company acquired Netherlands-based pet treat manufacturer Antos B.V., with Antos' logistics facility becoming the company's strategic Benelux distribution hub. This investment strengthens regional supply capabilities, expands access to natural pet treats across European markets, and reinforces the Netherlands as an important production and distribution center for premium companion animal treats.

Competitive Landscape

The Netherlands pet treats market is moderately fragmented, with major players including Mars, Incorporated, Nestlé S.A., Hill's Pet Nutrition, Inc. (Colgate-Palmolive Company), VAFO Group a.s., and United Petfood Producers NV competing alongside regional producers and domestic premium brands. Global companies benefit from extensive distribution networks, established brand recognition, and broad product portfolios spanning functional, natural, and everyday pet treats. Regional manufacturers strengthen competition through private-label production and specialized offerings tailored to evolving consumer preferences. Continuous product innovation in clean-label ingredients, functional nutrition, and premium formulations helps companies differentiate their offerings and maintain long-term market positioning.

Competition continues to intensify as companies expand premium and species-specific portfolios while strengthening manufacturing and retail partnerships throughout the Netherlands. Multinational suppliers leverage research capabilities and marketing investments to launch products addressing dental care, digestive health, mobility support, and natural nutrition. Regional companies remain competitive by offering locally produced, grain-free, organic, and limited-ingredient pet treats that appeal to health-conscious consumers. Private-label manufacturers also continue expanding their presence through supermarket retailers, increasing pricing pressure across mainstream product categories while creating additional opportunities in premium and functional pet treat segments.

Acquisitions and brand expansion are shaping competition in the Netherlands pet treats market as manufacturers strengthen their presence in premium and natural pet nutrition categories. Companies are increasingly investing in acquisitions and brand expansion to broaden product offerings and improve distribution across Europe. The expanded product portfolio and distribution network enhance the company's ability to serve premium pet treat demand, encouraging greater innovation and competitive differentiation across the Dutch market.

Netherlands Pet Treats Industry Leaders

Mars, Incorporated

Nestlé S.A.

Hill's Pet Nutrition, Inc. (Colgate-Palmolive Company)

VAFO Group a.s.

United Petfood Producers NV

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Antos B.V. was acquired by The Nutriment Company Sweden AB, expanding the group's portfolio of natural dog and cat treats and strengthening its distribution network across the Benelux region and the broader European pet nutrition market.

- April 2024: General Mills completed the acquisition of Edgard and Cooper, a European premium natural pet food brand. The acquisition expanded the company's premium pet food portfolio across Europe and strengthened its long-term growth strategy in the Netherlands pet nutrition market.

- January 2024: VAFO Group a.s. acquired Dagsmark Petfood Oy, expanding its premium pet food portfolio and manufacturing presence in Northern Europe. The acquisition strengthened VAFO's regional supply network, supporting the distribution of premium dog and cat food products across European markets, including the Netherlands.

Netherlands Pet Treats Market Report Scope

Pet treats are complementary food products given to pets as rewards, snacks, or training aids rather than as complete meals. They are used to reinforce positive behavior, support dental health, deliver functional benefits such as joint or digestive care, and strengthen the bond between pets and their owners. The Netherlands pet treats market report is segmented by sub-product (dental treats, crunchy treats, soft and chewy treats, freeze-dried and jerky treats, and other treats), by pets (cats, dogs, and other pets), and by distribution channel (convenience stores, online channel, specialty stores, supermarkets/hypermarkets, and other channels). The market forecasts are provided in terms of value (USD) and volume (metric tons).

| Dental Treats |

| Crunchy Treats |

| Soft and Chewy Treats |

| Freeze-dried and Jerky Treats |

| Other Treats |

| Cats |

| Dogs |

| Other Pets |

| Convenience Stores |

| Online Channel |

| Specialty Stores |

| Supermarkets/Hypermarkets |

| Other Channels |

| By Sub Product | Dental Treats |

| Crunchy Treats | |

| Soft and Chewy Treats | |

| Freeze-dried and Jerky Treats | |

| Other Treats | |

| By Pets | Cats |

| Dogs | |

| Other Pets | |

| By Distribution Channel | Convenience Stores |

| Online Channel | |

| Specialty Stores | |

| Supermarkets/Hypermarkets | |

| Other Channels |

Key Questions Answered in the Report

How large is the Netherlands pet treats market in 2026 and where is it headed by 2031?

The Netherlands pet treats market stands at USD 301.84 million in 2026 and is forecast to reach USD 412.75 million by 2031 at a 6.46% CAGR.

Which sub product category leads pet treats sales in the Netherlands?

Crunchy treats accounted for the largest 24.1% share in 2025, supported by wide supermarket reach and strong familiarity in daily use.

Which pet segment is growing fastest in the Netherlands pet treats space?

Cats are the fastest growing pet segment with a 7.4% CAGR through 2026 to 2031, helped by rising indoor ownership and stronger demand for species-specific treats.

Why are online sales rising in pet treats across the Netherlands?

Online sales are rising because repeat treat use fits subscription and replenishment models, and digital shelves can support deeper premium and functional assortments.

Page last updated on: