Netherlands Green IT Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

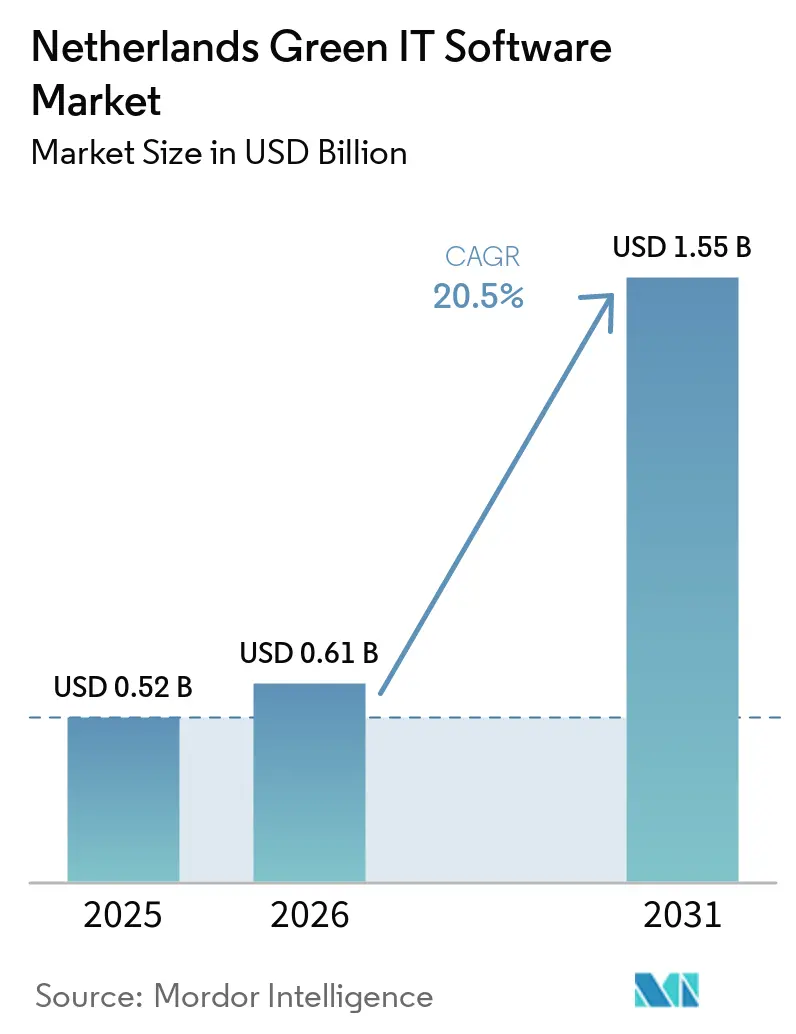

| Base Year Market Size (2025) | USD 0.52 Billion |

| Market Size (2026) | USD 0.61 Billion |

| Market Size (2031) | USD 1.55 Billion |

| Growth Rate (2026 - 2031) | 20.50% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Netherlands Green IT Software Market Analysis by Mordor Intelligence

The Netherlands Green IT Software Market size was valued at USD 0.52 billion in 2025 and is estimated to grow from USD 0.61 billion in 2026 to reach USD 1.55 billion by 2031, at a CAGR of 20.5% during the forecast period (2026-2031). The Dutch Climate Act provides this space with a durable policy base, as the country remains legally committed to deeper emissions cuts through 2030, 2040, and 2050. CSRD reporting from the 2024 financial year moved sustainability software from a discretionary purchase to an operational requirement for many in-scope enterprises. Adoption still has room to deepen, as many organizations continue to manage sustainability workflows in spreadsheets, with manual checks, and across disconnected internal systems. Demand now extends beyond disclosure needs because manufacturers require emissions visibility, data centers need tighter energy management, and public buyers increasingly expect supplier transparency. Legislative timing questions have not stalled procurement, as companies still need time to build audit-ready reporting, supplier data collection, and internal control workflows before stricter compliance cycles mature.

Key Report Takeaways

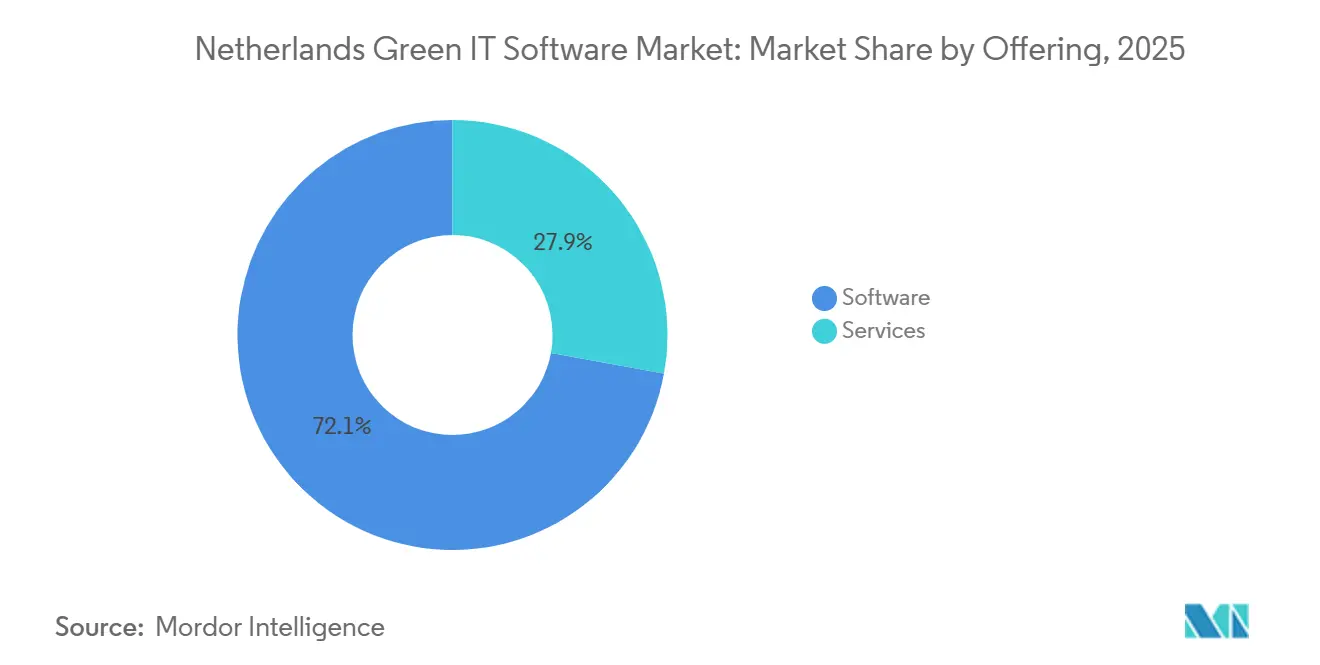

- By offering, software held 72.13% in 2025 and is projected to expand at a 21.45% CAGR through 2031.

- By deployment, cloud-based deployments accounted for 74.24% in 2025 and are projected to grow at a 22.34% CAGR through 2031.

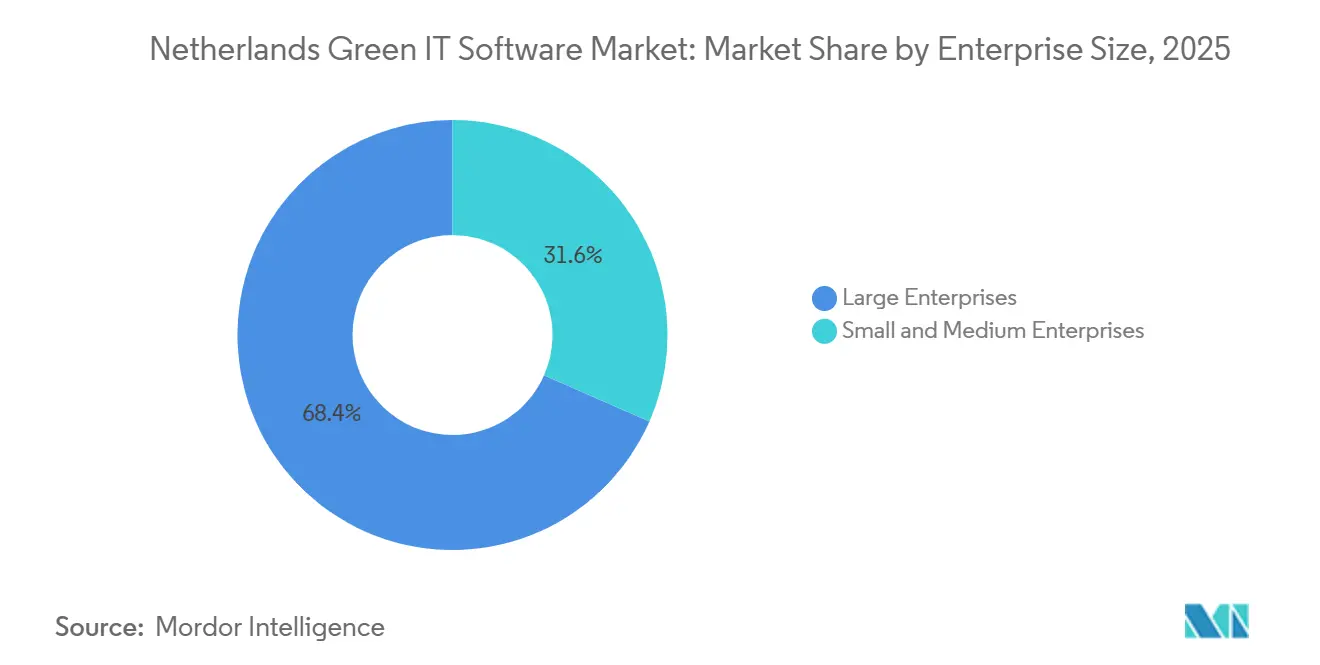

- By enterprise size, large enterprises held 68.42% in 2025, while SMEs are projected to expand at a 23.52% CAGR through 2031 in the Netherlands green IT software market.

- By solution type, carbon management software led with 31.67% in 2025, while sustainability reporting is projected to expand at a 22.92% CAGR through 2031.

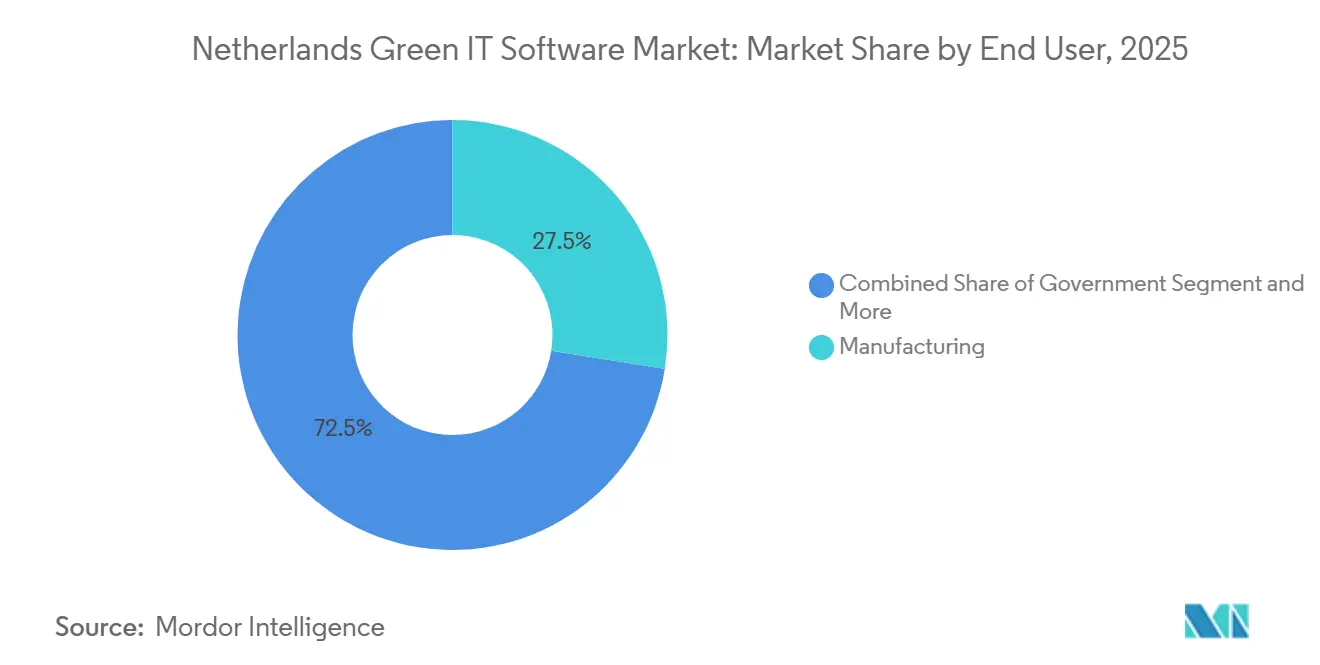

- By end user, manufacturing accounted for 27.51% in 2025, while government is projected to grow at a 25.31% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Netherlands Green IT Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| CSRD And ESG Disclosure Pressure | +5.2% | National, with early gains in Amsterdam, Rotterdam, and Utrecht corporate hubs | Short term (≤ 2 years) |

| Rising Scope 1, Scope 2, And Scope 3 Carbon Accounting Demand | +4.1% | National, concentrated in South Holland and North Brabant industrial corridors | Medium term (2-4 years) |

| Net-Zero Procurement Requirements Across Public And Large Private Buyers | +3.3% | National, with procurement clusters in The Hague and Amsterdam | Medium term (2-4 years) |

| Net Congestion And Dynamic Energy Cost Optimization Needs | +2.8% | North Holland and Amsterdam Metropolitan Area, most constrained grid zones | Short term (≤ 2 years) |

| AI-Enabled Automation Of ESG Data Collection And Control Testing | +2.1% | Global, with concentrated early adoption in Amsterdam and Rotterdam technology corridors | Long term (≥ 4 years) |

| Integration Demand With ERP, Finance, And Facility Management Stacks | +1.4% | National, with stronger uptake in ERP-dense manufacturing and logistics hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

CSRD And ESG Disclosure Pressure On Dutch Enterprises

CSRD remains the clearest trigger for software buying in the Netherlands green IT software market because it turns sustainability reporting into a structured reporting and controls exercise rather than a voluntary communications task. Companies now need data lineage, document trails, workflow approvals, and digital reporting formats that spreadsheets and basic internal tools do not handle well. This has made dedicated software more relevant for large enterprises first, but it also shapes buying decisions for suppliers that feed data into those larger reporting chains. The policy direction still supports this shift because Dutch climate commitments remain formal, long-dated, and embedded in national law, which keeps sustainability governance high on corporate agendas. [1]Government Of The Netherlands, “Mitigating Climate Change,” Government of the Netherlands, government.nl The result is that the Netherlands green IT software market continues to benefit from a broadening compliance cycle that is moving from pure reporting to internal controls, assurance readiness, and recurring disclosure management.

Rising Scope 1, Scope 2, And Scope 3 Carbon Accounting Demand

The Netherlands green IT software market is also benefiting from the growing complexity of Scope 1, Scope 2, and Scope 3 accounting, especially as firms move from direct emissions tracking to value-chain-level reporting. Large Dutch enterprises increasingly need supplier, logistics, procurement, and operations data in a single system, which underscores the value of software that can normalize inputs across different business units. This matters even more in a trade-oriented economy where manufacturers, logistics operators, and service providers work through dense supplier networks and cross-border reporting relationships. The pressure on SMEs is rising as well, as larger customers are already requesting sustainability information from non-reporting suppliers, expanding demand beyond the directly regulated base. [2]Ministry Of Economic Affairs, “Duurzaamheidsinformatie, De Effecten Van De CSRD Op Het MKB,” Rijksoverheid, rijksoverheid.nl In practice, that makes the Netherlands' green IT software market more dependent on networked data capture, supplier engagement tools, and repeatable carbon-calculation workflows than on simple internal emissions logs.

Net-Zero Procurement Requirements Across Public And Large Private Buyers

Public procurement now serves as a practical adoption channel in the Netherlands' green IT software market because it embeds sustainability requirements into software, reporting, and supplier management processes. Government bodies are not only direct users of disclosure tools but also shape vendor behavior by requesting better emissions and sustainability data in tenders and contract reviews. Large private buyers in finance, energy, manufacturing, and retail are extending the same logic to their supplier bases, thereby widening adoption among firms not yet under direct reporting rules. The long-term climate plan strengthens this pattern by providing buyers with a clearer policy runway for emissions reductions, resource management, and reporting improvements over the next decade. That keeps the Netherlands' green IT software market supported by procurement-led demand, even when formal rule implementation moves more slowly than buyers had initially expected.

Net Congestion And Dynamic Energy Cost Optimization Needs

The Netherlands' green IT software market is not being driven solely by reporting, because energy availability and cost management have become software buying issues in their own right. Dutch data centers consumed 5,100 GWh in 2024, which represented 4.6% of national electricity use, and that level of power demand raised the commercial value of monitoring, optimization, and efficiency tools. [3]Statistics Netherlands, “Data Centres Consume 4.6 Percent of the Netherlands’ Electricity,” CBS, cbs.nl The Dutch Data Center Association also reported a record investment expectation of more than EUR 1.4 billion (USD 1.51 billion) for 2025, with sustainability and energy efficiency embedded in those spending plans. When power access is constrained and energy costs remain material, software that helps operators shift loads, improve visibility, and reduce waste becomes easier to justify on operational grounds. That gives the Netherlands green IT software market a second demand stream that is less exposed to the timing of formal disclosure rules.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented Data Ownership Across Finance, Operations, And Suppliers | -2.8% | National, most acute in supply-chain-intensive sectors in South Holland and Zeeland port regions | Medium term (2-4 years) |

| Limited In-House ESG And Carbon Accounting Expertise In Mid-Market Firms | -2.2% | National, with proportionally higher impact in regions with high SME density including Randstad and Eindhoven | Short term (≤ 2 years) |

| Integration Complexity With Legacy Building And Energy Systems | -1.7% | National, particularly in older industrial regions with aging building and energy infrastructure | Medium term (2-4 years) |

| Data Quality And Auditability Gaps In Supplier Scope 3 Inputs | -1.4% | Global supply chains, with Dutch multinationals and logistics firms most exposed | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented Data Ownership Across Finance, Operations, And Suppliers

Fragmented data ownership remains a core implementation barrier in the Netherlands' green IT software market because the required inputs are spread across finance, procurement, facilities, operations, HR, and supplier networks. Many companies understand what they need to report, but they still struggle to identify who owns each dataset, how often it changes, and which team can validate it. This slows deployments because the software's value emerges only after the organization agrees on governance, controls, and internal process flows. The issue is sharper in supply-chain-heavy businesses where upstream data comes from partners with different formats, systems, and reporting maturity. The Rijksoverheid study on SME spillover effects shows that sustainability data requests are already moving through corporate value chains, underscoring the need for clean ownership models before software can deliver reliable outputs.

Limited In-House ESG And Carbon Accounting Expertise In Mid-Market Firms

Limited internal expertise is another practical brake on the Netherlands green IT software market, especially among mid-sized firms that receive data requests before they build dedicated sustainability teams. Many of these businesses can purchase software, but they still need help with selecting emission factors, defining reporting boundaries, setting up workflows, and implementing review controls. This creates a gap between technical product capability and day-to-day user readiness, which can extend onboarding cycles and reduce early utilization. It also pushes vendors to add templates, guided workflows, and managed support rather than relying only on self-service product design. The wider SME effect described by the Dutch government suggests this capability gap will remain important because data obligations are spreading through customer and supplier relationships faster than internal staffing models are changing. [4]Ministry Of Economic Affairs, “Duurzaamheidsinformatie, De Effecten Van De CSRD Op Het MKB,” Rijksoverheid, rijksoverheid.nl

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Software Platforms Led The Spending Base

Software held a 72.13% share of the Netherlands' green IT software market in 2025 and is projected to expand at a 21.45% CAGR through 2031. This lead reflects the shift from manual sustainability tracking to systems that manage calculation logic, workflow approvals, evidence storage, and structured disclosures in a single environment. Buyers increasingly prefer software because the reporting burden does not end with one filing cycle, and recurring updates favor a platform model over repeated project work. The Netherlands green IT software market has therefore tilted toward cloud-native tools that can update templates, rule sets, and disclosure workflows without long redevelopment cycles. This also helps enterprises that must coordinate finance, operations, and sustainability teams through a shared process rather than through isolated spreadsheets.

Services still play an important role in the Netherlands green IT software industry because implementation, training, data mapping, and assurance preparation remain difficult tasks for first-time adopters. Many buyers still need external help to connect facilities data, supplier records, and finance systems before the platform delivers reliable outputs. That keeps services relevant during the early deployment period, especially for companies moving from fragmented internal files to formal reporting stacks. At the same time, the long-run balance still favors software because more of the setup and checking work is being embedded into guided workflows and automation layers. SAP’s May 2026 launch of sustainability AI agents shows how enterprise vendors are trying to push more readiness, mapping, and optimization work directly into the product layer. [5]SAP News Center, “Autonomous Enterprise, New Sustainability AI Agents,” SAP News Center, news.sap.com

By Deployment: Cloud Architecture Remained The Default Model

Cloud-based deployment held a 74.24% share of the Netherlands green IT software market in 2025 and is projected to grow at a 22.34% CAGR through 2031. This dominance reflects the need to handle multi-framework reporting in an environment where disclosure requirements, calculation methods, and control workflows continue to evolve. Cloud deployments are easier to maintain when companies need recurring changes to data models, supplier questionnaires, reporting templates, and digital filing outputs. They also fit the current buying preference for subscription software that can be rolled out across multiple teams and locations with less local infrastructure work. For many buyers in the Netherlands' green IT software market, the value of cloud lies as much in update speed and consistent control as in lower deployment friction.

On-premises deployments still have a place in the market, especially among institutions with tighter data-handling rules, internal hosting preferences, or legacy architecture commitments. Hybrid models are also meaningful because some multinationals want cloud-based reporting layers while keeping transaction systems and sensitive records in existing internal environments. That makes deployment choice less about ideology and more about the balance between agility, integration depth, and control. Vendors that can support both rapid cloud workflows and structured enterprise integration remain well placed, especially where finance-grade auditability matters. SAP’s current product direction also supports this trend by linking sustainability functions to existing enterprise data environments rather than treating them as standalone tools.

By Enterprise Size: Large Enterprises Led While SMEs Accelerated Faster

Large enterprises held 68.42% of the Netherlands green IT software market share in 2025, while SMEs are projected to expand at a 23.52% CAGR through 2031. Large companies led early adoption because they were closer to direct reporting obligations, had broader internal data footprints, and faced earlier pressure to formalize controls and assurance readiness. They also had the budget to procure integrated platforms rather than relying on spreadsheets, point tools, or limited internal systems. In the Netherlands' green IT software market, large-enterprise demand has centered on software that combines carbon accounting, governance workflows, narrative preparation, and review controls in a single stack. That buyer group will stay important because it sets expectations for downstream suppliers and often determines the data standards used across broader value chains.

SMEs, however, are becoming the fastest-growing group because adoption is increasingly being driven by customers rather than by direct legal scope alone. The Dutch government’s study on the effects of CSRD on SMEs confirmed that non-reporting businesses are already being asked to provide sustainability information to larger corporate clients. This creates a large demand pool for simpler, faster, and lower-cost tools that can generate usable emissions and disclosure outputs without full enterprise complexity. The Netherlands green IT software industry is responding with lighter onboarding models, more templates, and workflow guidance that reduces dependence on external advisors. As this supplier-led pressure widens, SME adoption will keep rising because commercial continuity increasingly depends on the ability to provide structured sustainability data.

By Solution Type: Carbon Management Anchored The Base While Reporting Grew Faster

Carbon management software accounted for 31.67% of the Netherlands green IT software market size in 2025, while sustainability reporting is projected to grow at a 22.92% CAGR through 2031. Carbon management led because most organizations entered the space through emissions measurement, footprint creation, and basic reduction tracking before they built broader governance and reporting functions. These tools remain foundational because they provide the raw calculations and activity data that later feed external disclosures and internal planning. In the Netherlands, the green IT software market has established a carbon management base that still supports renewal and module expansion. Sustainability reporting is now growing faster because companies need stronger workflow control, auditability, and disclosure formatting as reporting matures.

ESG reporting platforms remain strategically important because they expand the scope beyond carbon into governance, social indicators, and broader narrative management. Decarbonization planning tools are also gaining traction as organizations move from measuring historical emissions to testing future pathways and target scenarios. SAP’s current roadmap, which includes regulatory-readiness and footprint-optimization agents, reflects how vendors are integrating accounting, reporting, and planning into a single environment rather than keeping them separate. Energy and resource management software adds another layer because Dutch data centers and industrial sites need operational efficiency alongside disclosure compliance. Statistics Netherlands and the Dutch Data Center Association both point to the scale of energy use and investment in this part of the economy, which supports the ongoing role of optimization software in the broader solution mix.

By End User: Manufacturing Kept The Largest Share While Government Grew Fastest

Manufacturing accounted for 27.51% of the Netherlands green IT software market share in 2025, while the government is projected to expand at a 25.31% CAGR through 2031. Manufacturing led because process-heavy operations create direct energy, emissions, and resource visibility needs that are difficult to manage through manual tools. These firms also face pressure from suppliers, customers, and financiers to produce better sustainability data with stronger controls. BFSI remains an important buyer group because it operates under multiple disclosure, risk, and governance expectations, which increases the value of integrated data and reporting workflows. Energy, utilities, and retail also support the Netherlands green IT software market through their need for supply-chain visibility, emissions tracking, and operational efficiency.

Government is growing the fastest because public bodies are both software users and procurement gatekeepers, which gives their buying behavior a wider effect across vendor and supplier ecosystems. The national climate plan supports this direction by setting a longer-term policy path that keeps emissions management and reporting capacity relevant across public institutions. Healthcare and construction are emerging more gradually, yet both have reasons to adopt more structured reporting and carbon management tools as sustainability expectations spread. Construction links software demand to building performance, documentation, and project-level reporting, while healthcare adoption is tied to institutional sustainability targets and operational accountability. The Netherlands green IT software industry will therefore continue to broaden its end-user base even though manufacturing and government remain the clearest volume and growth anchors.

Competitive Landscape

The Netherlands green IT software market remains moderately fragmented, with global enterprise vendors, specialist sustainability platforms, and Dutch-native providers all competing for different buyer profiles. Large enterprises often gravitate toward vendors that can connect sustainability workflows with finance, ERP, and internal control environments, which favors broader software suites. Specialist platforms still retain space because many buyers value deeper carbon accounting, supplier data handling, and a narrower product focus. Local and regional providers also matter because they can tailor onboarding, language support, and template design to Dutch reporting needs and SME buying behavior. This mix keeps the Netherlands green IT software market open enough for new entrants, while still rewarding vendors that can prove auditability, product depth, and integration quality.

Competition is now shifting from simple data capture toward full workflow coverage. SAP’s May 2026 sustainability AI agent launch showed that major enterprise vendors are trying to automate readiness checks, footprint analysis, and scenario work inside the broader enterprise software environment. Workiva’s Sustainability Disclosure Agent and its Intelligent Sustainability rollout point in the same direction, where reporting vendors are adding guided narrative generation, standards mapping, and multi-source data handling to raise switching costs. Persefoni’s AI Analytics Agent also reflected a push toward easier emissions analysis and planning through natural-language-style interaction. These moves show that the Netherlands' green IT software market is becoming more product-led, with automation, usability, and cross-functional workflow support becoming key differentiators.

The main strategic divide now sits between ERP-embedded approaches and best-of-breed platforms. Some buyers prefer tighter alignment of financial data and stronger control integration, while others want greater flexibility across fragmented systems and supplier networks. Dutch-native offerings can still compete where they simplify SME onboarding, support local reporting expectations, or address CO₂-related operational workflows more directly. The Netherlands green IT software market, therefore, still looks unlikely to collapse into a single dominant architecture, because buyer needs remain too varied across enterprise scale, deployment preferences, and use-case depth.

Netherlands Green IT Software Industry Leaders

Wolters Kluwer N.V.

Beeminds B.V.

Bright Cape B.V.

Greenly SAS

MasterSustainability.Today B.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Workiva launched the Workiva Sustainability Disclosure Agent on June 15, 2026, an agentic AI solution that scans existing company disclosures against ESRS and IFRS S1 and S2 requirements, identifies compliance gaps, recommends next steps, and generates standards-aligned narrative drafts. The tool targets enterprises managing the evolving Omnibus-adjusted ESRS landscape and is commercially significant for Dutch Wave 1 reporters transitioning to revised disclosure scope requirements.

- May 2026: SAP announced new sustainability AI agents at SAP Sapphire on May 15, 2026, with general availability targeted for the end of 2026. The suite includes a Sustainability Regulatory Readiness Agent for CSRD materiality mapping, a Footprint Optimization Agent reducing carbon scenario simulation time from approximately 1 day to 20 minutes, and a Packaging Compliance Agent delivering over 50% reduction in manual compliance review hours, targeting enterprise buyers in Dutch manufacturing and logistics verticals.

- September 2025: Workiva unveiled Intelligent Sustainability at its Amplify event on September 9, 2025, introducing agentic AI capabilities, unified data automation, and a modernized controls experience for sustainability teams operating within the Office of the CFO platform. The rollout included multi-source data ingestion, AI-assisted narrative generation for regulatory filings, and enhanced integration with financial reporting workflows.

- June 2024: Workiva launched Workiva Carbon, an integrated carbon data management and reporting solution supporting CSRD, SEC climate disclosure rules, and California SB 253 compliance. The product positioned Workiva as an end-to-end platform connecting carbon accounting data with financial-grade disclosure workflows, relevant to Dutch multinationals managing cross-jurisdictional reporting obligations.

Netherlands Green IT Software Market Report Scope

The Netherlands Green IT Software Market Report is Segmented by Offering (Software, Services), Deployment (Cloud-Based, On-Premises, and Hybrid), Enterprise Size (Large Enterprise, and SMEs), Solution Type (Carbon Management, ESG Reporting, Decarbonization, and Energy Management), and End User (IT and Telecom, BFSI, Manufacturing, Energy, Retail, Government, and more). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud-Based |

| On-Premise |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises |

| Carbon Management & Accounting Software |

| ESG Reporting & Compliance Software |

| Sustainability Data Management Platforms |

| Decarbonization Planning Software |

| Energy & Resource Optimization Software |

| IT and Telecom |

| BFSI |

| Manufacturing |

| Energy and Utilities |

| Retail and E-Commerce |

| Government |

| Healthcare |

| Construction and Infrastructure |

| Other End-User Industries |

| By offering | Software |

| Services | |

| By Deployment | Cloud-Based |

| On-Premise | |

| Hybrid | |

| By Enterprise Size | Large Enterprises |

| Small and Medium Enterprises | |

| By Solution Type | Carbon Management & Accounting Software |

| ESG Reporting & Compliance Software | |

| Sustainability Data Management Platforms | |

| Decarbonization Planning Software | |

| Energy & Resource Optimization Software | |

| By End User | IT and Telecom |

| BFSI | |

| Manufacturing | |

| Energy and Utilities | |

| Retail and E-Commerce | |

| Government | |

| Healthcare | |

| Construction and Infrastructure | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the current and forecast size of the Netherlands green IT software market?

The Netherlands green IT software market is valued at USD 0.61 billion in 2026 and is projected to reach USD 1.55 billion by 2031, growing at a 20.50% CAGR from 2026 to 2031.

Which offering leads spending in the Netherlands green IT software space?

Software led the market with a 72.13% share in 2025, reflecting the need for recurring reporting, audit trails, workflow approvals, and structured disclosure capabilities.

Why is cloud deployment dominant in this space?

Cloud-based deployment held 74.24% in 2025 because buyers need faster regulatory updates, easier multi-team access, and less maintenance burden across changing disclosure requirements.

Why are SMEs adopting these tools faster now?

SMEs are the fastest-growing enterprise-size segment at a 23.52% CAGR through 2031 because larger clients increasingly request sustainability data from suppliers even before direct legal obligations apply.

Which end-user group leads demand and which one is growing fastest?

Manufacturing held the largest end-user share at 27.51% in 2025, while government is projected to grow the fastest at a 25.31% CAGR through 2031.

What is shaping vendor competition in the Netherlands most strongly?

Competition is shifting toward workflow depth, automation, and integration, with vendors adding AI-enabled readiness checks, disclosure support, and better links to ERP, finance, and operational systems.

Page last updated on: