Netherlands Customer Data Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

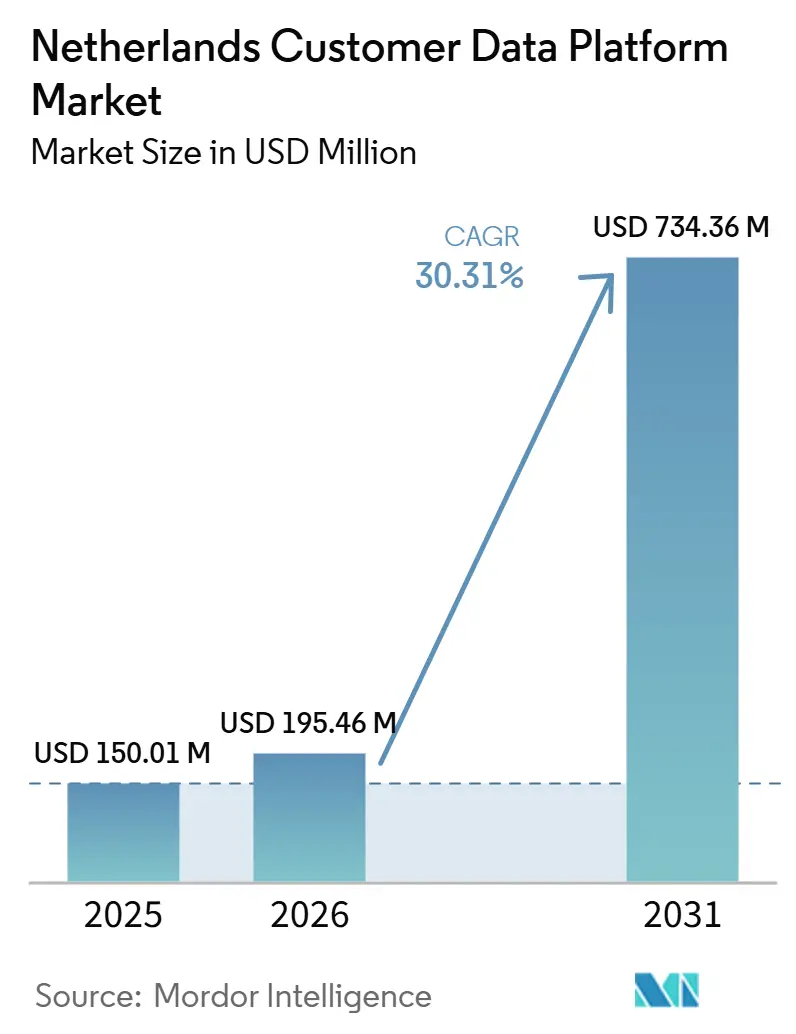

| Base Year Market Size (2025) | USD 150.01 Million |

| Market Size (2026) | USD 195.46 Million |

| Market Size (2031) | USD 734.36 Million |

| Growth Rate (2026 - 2031) | 30.31% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Netherlands Customer Data Platform Market Analysis by Mordor Intelligence

The Netherlands customer data platform market size is projected to expand from USD 150.01 million in 2025 and USD 195.46 million in 2026 to USD 734.36 million by 2031, registering a CAGR of 30.31% between 2026 to 2031. The growth path reflects a market where strong digital readiness and strict privacy expectations are moving customer data programs from optional marketing tools into core operating systems for data collection, consent handling, and activation. Dutch enterprises are increasingly consolidating fragmented customer records into unified profiles because separate tools make privacy control, channel coordination, and attribution harder to manage at scale. Cloud delivery, AI-linked workflows, and composable platform designs are also widening adoption because they let enterprises improve activation speed without rebuilding every underlying system at once. Demand is no longer tied only to retail use cases, because financial services, healthcare, and other regulated sectors now need better control over data use, auditability, and profile accuracy. Competition is rising as large global suites and specialized vendors pursue the same enterprise accounts, which is putting more emphasis on integration depth, governance features, and speed of deployment across the Netherlands customer data platform market.

Key Report Takeaways

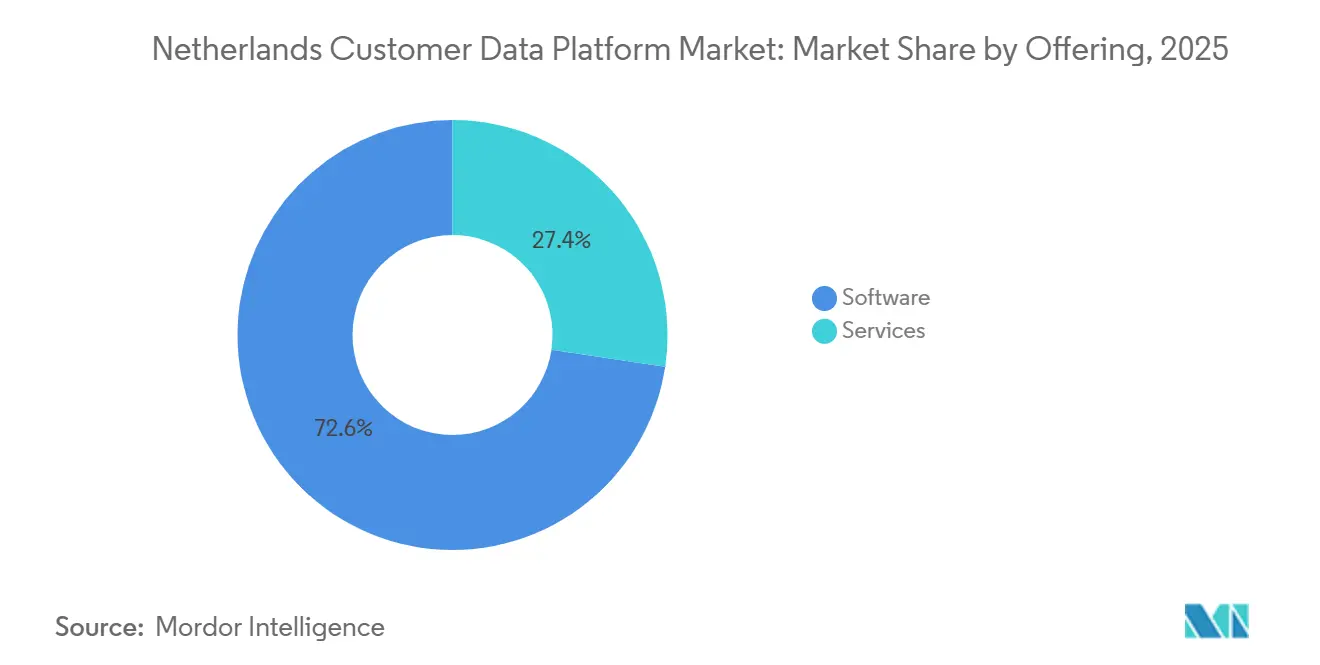

- By offering, software led with a 72.64% share in 2025, while services are projected to expand at a 31.87% CAGR through 2031.

- By deployment mode, cloud held 64.91% of the Netherlands customer data platform market share in 2025 and is expected to remain the fastest-growing deployment model at a 32.13% CAGR through 2031.

- By organization size, large enterprises accounted for 67.41% share in 2025, while SMEs are projected to record the highest CAGR at 32.24% over the forecast period.

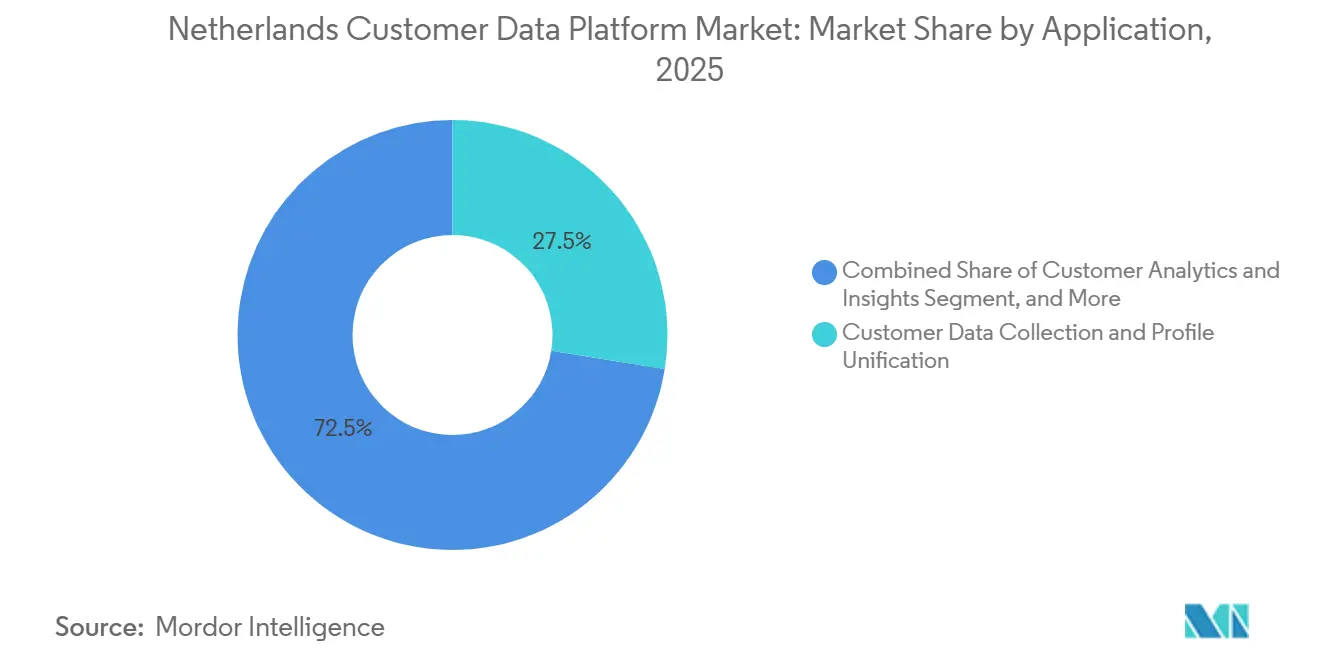

- By application, customer data collection and profile unification captured 27.53% share in 2025, while audience segmentation and personalization are expected to expand at a 33.21% CAGR through 2031.

- By end-user industry, retail and e-commerce led with a 24.69% share in 2025, while healthcare and life sciences are projected to grow at a 32.86% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Netherlands Customer Data Platform Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising First-Party Data Imperatives for Privacy-First Personalization | +5.8% | National, with highest concentration in Amsterdam, Rotterdam, and Utrecht enterprise clusters | Short term (≤ 2 years) |

| Accelerating Cookie Deprecation and Identity Resolution Needs | +5.2% | National, with spill-over to Dutch-headquartered multinationals operating across EU | Short term (≤ 2 years) |

| AI-Enabled Segmentation and Activation At Scale | +4.9% | Global, with APAC and EU enterprise segments including Netherlands among early adopters | Medium term (2-4 years) |

| Omnichannel Customer Journey Orchestration Demand | +4.4% | National, driven by retail, BFSI, and travel verticals in Randstad metro area | Medium term (2-4 years) |

| MarTech Stack Consolidation Across Dutch Enterprises | +3.6% | National, with early gains in Amsterdam and Eindhoven technology corridors | Short term (≤ 2 years) |

| Higher Conversion Pressure in E-Commerce and Retail | +3.1% | National, concentrated in Dutch e-commerce platforms serving EU cross-border markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising First-Party Data Imperatives for Privacy-First Personalization

The Netherlands customer data platform market is benefiting from a privacy setting that has become difficult for enterprises to manage with disconnected marketing tools and weak consent controls. The Dutch data protection authority has already shown a willingness to act when customer tracking and consent practices fall short, which raises the cost of leaving first-party data collection scattered across separate systems. At the same time, Dutch firms had already reached a basic digital intensity rate of 89% in 2025, far above the EU average of 71%, which means most enterprises have the operating base needed to move quickly once privacy pressure becomes commercial pressure.[1]Centraal Bureau voor de Statistiek and Eurostat, “Bedrijven Met Digitalisering in Top 3 EU, Nederlanders Digitaal Meest Vaardig,” CBS, cbs.nl This combination shifts buying behavior away from stand-alone audience tools and toward platforms that can unify identity, consent, and activation in one governed environment. As a result, the Netherlands customer data platform market is seeing demand that is tied less to short campaign goals and more to long-cycle architecture decisions that usually remain in place for several years.

Accelerating Cookie Deprecation and Identity Resolution Needs

The Netherlands customer data platform market is also being pulled forward by the need to rebuild customer recognition on data that brands can collect and control directly. In a market where privacy enforcement is already strict, the practical issue is not only whether third-party signals weaken over time, but whether enterprises can still connect visits, profiles, and outcomes in a lawful way across owned channels.[2]Autoriteit Persoonsgegevens, “Besluit Boete A.S. Watson / Kruidvat,” Autoriteit Persoonsgegevens, autoriteitpersoonsgegevens.nl Adobe’s general availability launch of Real-Time CDP Collaboration in February 2025 showed that large vendors are investing in privacy-preserving ways to work with first-party data, signaling that identity and collaboration problems are now central product priorities rather than side capabilities. That matters in the Dutch market because brands cannot rely on broad tracking assumptions and then retrofit compliance later. The result is a more durable adoption case for identity resolution, profile stitching, and consent-aware segmentation across the Netherlands customer data platform market.

AI-Enabled Segmentation and Activation At Scale

AI has become a more direct growth driver for the Netherlands customer data platform market because leading vendors are embedding it inside the same systems that hold governed customer profiles. Adobe introduced CX Enterprise in April 2026 with multi-agent workflow capabilities connected to Adobe Experience Platform and Real-Time CDP, which points to a market where orchestration and activation are moving closer to the underlying data layer. Salesforce also pushed this direction further in its Summer 2026 release cycle, where Data 360 and Agentforce were positioned more tightly around customer workflow automation and data-driven action. These moves reduce the need for enterprises to build separate AI layers before they can test advanced segmentation and automated activation. They also favor vendors that already have strong first-party data quality controls, because the value of AI depends on accurate identities, current permissions, and usable behavioral history across the Netherlands customer data platform market.

Omnichannel Customer Journey Orchestration Demand

The Netherlands customer data platform market is further supported by the growing need to coordinate customer journeys across online storefronts, service channels, apps, and offline interactions. ING stated that Dutch retail sales are expected to grow 4.5% in 2026, while online retail is expected to grow 7%, which means channel complexity is rising faster than the broader consumer market. The same pressure is visible in financial services, where the Dutch financial regulator observed that hyperpersonalization remains limited and uneven, leaving clear room for more advanced but better-controlled use of customer data. When companies need a consistent view of a customer across touchpoints, fragmented campaign tools stop being enough because they cannot manage timing, permissions, and measurement together. That dynamic supports broader adoption of orchestration capabilities, especially where the Netherlands customer data platform market overlaps with sectors that face both rising customer expectations and stronger documentation duties.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Data Governance Complexity Across Consent, Identity, and Activation Workflows | -3.4% | National, most acute for Dutch enterprises with cross-border EU data flows | Long term (≥ 4 years) |

| Integration Friction With Legacy CRM, DMP, and Analytics Environments | -2.8% | National, with disproportionate impact on large enterprises in BFSI and industrial manufacturing | Medium term (2-4 years) |

| Limited In-House CDP Maturity Among Mid-Market Buyers | -2.3% | National, most pronounced in SME segments outside major metropolitan areas | Medium term (2-4 years) |

| Compliance Risk From Misconfigured Data Use and Cross-Channel Activation | -1.8% | National, with EU-wide exposure for Dutch multinationals | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Data Governance Complexity Across Consent, Identity, and Activation Workflows

The Netherlands customer data platform market still faces a meaningful brake from the amount of control work required once enterprises connect consent capture, profile identity, and downstream activation. Dutch enforcement signals have made it clear that data handling cannot be treated as a background setting, because flawed tracking logic or incomplete transparency can become a regulatory issue very quickly. In finance, the AFM has already noted that firms remain cautious with more tailored online choice environments, which shows that legal and governance uncertainty still limits how fast institutions will scale fine-grained personalization. In healthcare, the publication of NCS 7560 for self-assessment of electronic patient record systems adds another layer of structure around how digital records and related processes are reviewed. The result is that many buyers move more slowly than the technology would allow, because governance design, internal approvals, and audit readiness take longer than software configuration across the Netherlands customer data platform market.

Integration Friction With Legacy CRM, DMP, and Analytics Environments

The Netherlands customer data platform market is also constrained by the practical difficulty of connecting modern CDP layers to older CRM, analytics, and enterprise systems that were built in different investment cycles. This problem is especially visible in large organizations because they already have extensive customer records, channel tools, and reporting structures that cannot be replaced in a single project. SAP’s April 2026 expansion with Google Cloud, which connected SAP Business Data Cloud, BigQuery, and SAP Engagement Cloud, underlined how strong enterprise demand has become for more direct links between core data environments and activation layers. Salesforce and Adobe are pushing a similar direction by tightening the connection between governed customer data and campaign execution, which shows that integration pain remains one of the most important barriers to faster rollout. Even when enterprises decide to proceed, this friction lengthens implementation cycles, raises service dependence, and keeps some deployments narrower than the full opportunity visible in the Netherlands customer data platform market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Software Dominates, Services Investment Accelerates

Software held 72.64% of the Netherlands customer data platform market share in 2025, which showed that most buyers still preferred a platform-led purchase over a service-led one when they first formalized customer data management. That leadership makes sense in a market where enterprises need durable systems of record for identity, profiles, permissions, and activation rules rather than isolated campaign support tools. The Netherlands also entered this phase with high digital readiness, as 89% of businesses met the basic digital intensity threshold in 2025, which reduced the foundational barriers to packaged software adoption. Privacy enforcement adds to software demand because enterprises need consistent controls and repeatable workflows once customer data is used across multiple teams and channels. In that setting, software remains the anchor of the Netherlands customer data platform market even when deployment models and activation use cases keep changing.

Services is projected to grow at a 31.87% CAGR through 2031, which shows that implementation difficulty is rising even while packaged software remains the larger revenue pool. Much of that demand comes from the work required to configure consent logic, unify records from multiple systems, govern data movement, and operationalize new AI or orchestration features in live environments. Bloomreach’s June 2026 partnership launch for Databricks CustomerLake reflected the wider shift toward architectures where customer data and activation logic span more than one system, which tends to increase advisory and integration work rather than reduce it.[3]Bloomreach, “Bloomreach Deepens Partnership With Databricks, Extending AI Personalization Across Email, Web, and More Through New CustomerLake Integration,” Bloomreach, bloomreach.com SAP’s effort to connect its customer engagement layer more closely with broader enterprise data environments points to the same direction, because enterprises increasingly expect the CDP to sit inside a wider governed stack rather than on its own. For that reason, services growth is strengthening the software core of the Netherlands customer data platform market rather than replacing it.

By Deployment Mode: Cloud Leads in Share and Speed

Cloud accounted for 64.91% share of the Netherlands customer data platform market size in 2025 and is projected to expand at a 32.13% CAGR through 2031, which gave it both the leading installed base and the fastest growth path. This double lead suggests that cloud adoption in the Netherlands customer data platform market is still climbing rather than flattening, even though cloud is already well established across enterprise software. The country’s digital readiness helps explain that position, because high business digital intensity lowers the operational friction of adopting managed infrastructure and connected data services. Cloud also fits the need for faster orchestration across multiple channels, where real-time profile updates and scalable compute matter more than fixed in-house capacity. As privacy and activation requirements change, cloud models give enterprises more room to adjust without rebuilding the entire system landscape.

On-premises deployments still matter in regulated environments where data handling rules, internal policy, or legacy architecture make immediate migration difficult. Hybrid models therefore remain relevant because they let enterprises move activation and analytics forward while keeping sensitive records or older systems in place during transition. Vendor strategy also supports this direction, since SAP, Adobe, Salesforce, and Bloomreach are all building tighter links between customer engagement tools and broader cloud data environments rather than assuming that every buyer will replace everything at once.[4]SAP SE, “SAP and Google Cloud Build What Comes Next in AI and CX,” SAP News Center, news.sap.com That staged flexibility is one reason cloud remains the clearest growth engine in the Netherlands customer data platform market. It also means deployment decisions are now less about location alone and more about how fast an enterprise can connect identity, consent, analytics, and activation under one operating model.

By Organization Size: Large Enterprises Set the Baseline, SMEs Accelerate Fastest

Large enterprises held 67.41% share in 2025, which reflected their stronger budgets, larger data estates, and greater urgency to manage customer activity across brands, business units, and countries. In many cases, large enterprises were also the first organizations to feel the full weight of fragmented customer systems because they operated more channels, more data sources, and more internal users. That makes them natural early anchors for the Netherlands customer data platform market, especially where governance and customer experience both matter at scale. The broader Dutch digital base supports this pattern, since high enterprise digitization makes formal CDP adoption more achievable once the business case becomes clear. Large accounts are therefore shaping vendor road maps, pricing models, and implementation approaches across the Netherlands customer data platform market.

SMEs are projected to grow at a 32.24% CAGR through 2031, which shows that the addressable base is widening even if large enterprises still account for most current revenue. This shift points to simpler buying paths, more modular activation needs, and greater interest in starting with a specific use case rather than a full enterprise transformation. As vendors add more packaged AI, better workflow automation, and tighter integration into broader commercial stacks, the effort needed for a smaller buyer to reach useful outcomes continues to fall. SMEs still face capability gaps in governance, implementation, and ongoing data operations, so growth is likely to remain uneven across sectors and regions. Even so, the faster rise of smaller buyers is expanding the depth of the Netherlands customer data platform market beyond its original large-enterprise base.

By Application: Data Unification Anchors the Stack, Personalization Leads Growth

Customer data collection and profile unification accounted for 27.53% share in 2025, which confirms that the first requirement in this market is still to create a usable, governed, and continuously updated customer record. That role remains central because downstream functions such as segmentation, orchestration, analytics, and preference management do not work reliably when identity is weak or when records are split across tools. Dutch enforcement conditions reinforce this order of spending, since enterprises need clear control over what data is held, how it was obtained, and where it can be used. Adobe’s workaround privacy-preserving collaboration also shows that large vendors see governed first-party data as the base layer for future activation models rather than a separate compliance topic. This is why data unification continues to anchor the Netherlands customer data platform market even as more visible activation use cases attract executive attention.

Audience segmentation and personalization are projected to grow at a 33.21% CAGR through 2031, which makes it the fastest-rising application once the data foundation is in place. The demand side is supported by rising commercial pressure in digital commerce, where the Netherlands e-commerce sector is forecast to grow significantly by 2031. Financial services adds another source of headroom because the AFM found that hyperpersonalization remains limited, which means many institutions have not yet fully translated customer data into tailored decision environments. As vendors add built-in AI and orchestration, the jump from profile building to action becomes shorter, which should keep this application ahead of the rest of the Netherlands customer data platform market. Consent and preference management also rise in importance within the same stack because more automated personalization only works when permissions remain clear and defensible.

Application

| X | Y |

|---|---|

| Customer Data Collection and Profile Unification | 26.73% |

| Combined Share of Customer Analytics and Insights Segment, and More | 73.27% |

| Source: Mordor Intelligence | |

By End-User Industry: Retail Leads, Healthcare Opens the Next Growth Cycle

Retail and e-commerce led with a 24.69% share in 2025, which reflected the direct link between customer recognition, conversion performance, and repeat engagement in a highly digital buying environment. The Netherlands customer data platform market has naturally found strong demand in this segment because retail brands usually face the fastest feedback loop between better profiles and better revenue outcomes. The sector continues to expand, with both traditional and online retail maintaining strong momentum, keeping pressure on merchants to enhance personalization, attribution, and journey design. Looking further ahead, the e‑commerce industry is expected to reach significant scale, reinforcing retail as the largest commercial base for CDP adoption in the Netherlands.

Healthcare and life sciences are projected to record a 32.86% CAGR through 2031, which makes it the fastest-growing end-user segment in the market. Growth here is less about conventional campaign activity and more about the rising need to structure data, permissions, records, and patient-related workflows with greater consistency. The publication of NCS 7560 for self-assessment of electronic patient record systems shows that the Dutch healthcare setting is moving toward more formalized digital review standards, which supports demand for better-governed data environments. This creates a different adoption path from retail, but it still favors platforms that can unify profiles, document permissions, and support controlled activation or communication processes. As these requirements deepen, healthcare is likely to become one of the most strategically important expansion areas inside the Netherlands customer data platform market.

Geography Analysis

The Netherlands customer data platform market remained centered in the Randstad corridor in 2025, where Amsterdam, Rotterdam, The Hague, and Utrecht concentrate a large share of enterprise buying, digital services capacity, and high-frequency customer engagement activity. Amsterdam is especially important because it combines international business presence, advanced digital commerce, and a strong base of technology providers that support marketing, analytics, and customer operations. This geographic concentration is reinforced by the broader ICT footprint in the country, where more than 100,000 ICT companies were active in 2025, of which 94% were service providers. That service-heavy structure helps the Netherlands customer data platform market by enabling buyers to access implementation support, data engineering, and adjacent software capabilities without leaving the main business clusters. It also means that once one enterprise in a sector adopts a new customer data model, peer organizations in the same corridor can respond quickly because the required skills and partner networks are already nearby.

Within Europe, the Netherlands customer data platform market stands out because high digital maturity and strong privacy scrutiny exist at the same time rather than one without the other. Dutch businesses rank among Europe’s most digitalized, yet privacy enforcement remains visible enough that enterprises cannot treat governance as a later-stage adjustment. This makes the country a useful proving ground for vendors that want reference deployments suited to broader EU conditions. The same feature also raises the quality threshold for buyers, because Dutch enterprises usually want stronger consent handling and cleaner integration design before they scale activation.

A second geographic pattern is the spread of opportunity beyond classic retail centers into regulated and specialized clusters. Financial services activity supports demand in large urban areas, while healthcare-related needs are creating new room for adoption where data governance and record quality are becoming more formalized. The country’s e-commerce scale also keeps national relevance high, because cross-border digital trade and intense domestic competition both increase the value of accurate customer profiles and coordinated activation. Over time, this should make the Netherlands customer data platform market less dependent on one vertical or one city cluster, even though the Randstad area is likely to remain the operational core. In effect, geography in this market is shaped less by simple regional size and more by where regulation, digital intensity, and customer interaction density meet.

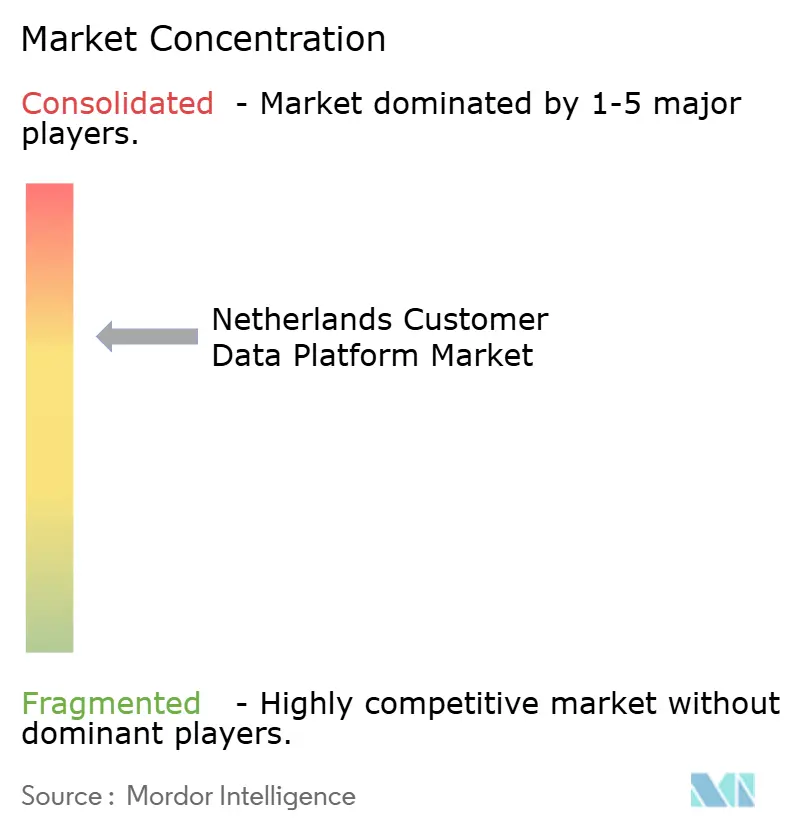

Competitive Landscape

The Netherlands customer data platform market shows a moderately concentrated vendor structure, with large software suites competing against specialist providers that focus on privacy, composability, or selected activation use cases. Global platforms such as Adobe, Salesforce, SAP, Oracle, and Microsoft remain strong because they can connect customer data functions with wider CRM, analytics, and enterprise workflow investments. At the same time, specialist names such as Bloomreach, BlueConic, Tealium, Amperity, and Zeotap remain relevant because buyers often want faster deployment, clearer use-case fit, or stronger independence from a single suite vendor. This creates a market where the main competitive question is not whether enterprises will buy a CDP, but which operating model they trust most for integration, activation, and governance. That balance keeps the Netherlands customer data platform market competitive without making it structurally fragmented.

Recent strategic moves show how suppliers are trying to win on platform depth rather than only on point functionality. SAP renamed SAP Emarsys to SAP Engagement Cloud in February 2026, which signaled a broader push to place customer engagement more centrally inside the wider SAP stack. SAP then expanded its Google Cloud partnership in April 2026 to connect SAP Business Data Cloud, Google BigQuery, and SAP Engagement Cloud more directly, which strengthened its case with enterprises that want governed data and activation in the same operating flow. Adobe also broadened its position through Real-Time CDP Collaboration and CX Enterprise, which tied privacy-preserving data use more closely to orchestration and AI-enabled action. Bloomreach’s Databricks CustomerLake partnership added another example, showing that lakehouse-linked personalization is becoming a stronger part of the competitive mix.

White space remains clear in sectors where packaged retail-style use cases do not fully match buyer needs. Healthcare, government, and some industrial environments still require deeper controls, slower deployment paths, and stronger audit logic than many mainstream offerings were originally designed to provide. That gap favors vendors that can combine governed data management with practical activation and lower integration friction. It also explains why partnerships around major cloud data environments now matter more, because they reduce duplication and make customer data programs easier to justify to internal stakeholders. Overall, the Netherlands customer data platform market is competitive enough to prevent any simple winner-takes-all outcome, yet concentrated enough that platform breadth, installed relationships, and ecosystem fit still shape who wins the largest accounts.

Netherlands Customer Data Platform Industry Leaders

Adobe Inc.

Salesforce, Inc.

Oracle Corporation

SAP SE

Amperity, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Bloomreach announced a launch partnership for Databricks CustomerLake, a new agentic CDP, deepening its integration of Loomi AI personalization with Databricks’ governed lakehouse infrastructure. The collaboration enables enterprise marketing teams to activate unified customer data across personalization channels without duplicating sensitive data outside the lakehouse.

- April 2026: SAP expanded its partnership with Google Cloud to connect SAP Business Data Cloud, Google BigQuery, and SAP Engagement Cloud into a real-time AI-powered customer engagement architecture, enabling Dutch SAP enterprise customers to activate CDP-grade personalization without exporting data from SAP’s governed environment.

- February 2026: SAP renamed SAP Emarsys to SAP Engagement Cloud, signaling the platform’s evolution from a standalone marketing automation solution into a core enterprise engagement layer embedded across the SAP portfolio. SAP Engagement Cloud, enterprise edition, launched simultaneously with advanced multi-brand and multi-region governance capabilities.

- February 2025: Adobe announced the general availability of Real-Time CDP Collaboration in the United States, enabling advertisers and publishers to identify high-value audiences through first-party data collaboration in a privacy-preserving environment, a capability directly aligned with the Netherlands’ cookie enforcement environment.

Netherlands Customer Data Platform Market Report Scope

The Netherlands Customer Data Platform Market refers to the business landscape for platforms and services that consolidate customer data from multiple sources into centralized customer profiles. These solutions enable identity resolution, real-time data integration, segmentation, personalization, and analytics, helping Dutch enterprises deliver consistent omnichannel customer experiences. Strong digital adoption, advanced e-commerce ecosystems, and strict compliance with the EU GDPR and Dutch Autoriteit Persoonsgegevens (AP) guidelines influence the market. The market also focuses on AI-driven personalization and scalable martech integration across the retail, finance, and telecom sectors.

The Netherlands Customer Data Platform Market Report is Segmented by Offering (Software, and Services), Deployment Mode (Cloud, On-Premises, and Hybrid) Organization Size (Large Enterprises, and Small and Medium Enterprises), Application (Customer Data Collection and Profile Unification, Audience Segmentation and Personalization, Marketing Campaign and Customer Journey Orchestration, Customer Analytics and Insights, Consent and Preference Management, and Other Applications), and End-User Industry (Retail and E-Commerce, Banking, Financial Services, and Insurance (BFSI), Healthcare and Life Sciences, IT and Telecom, Media and Entertainment, Industrial Manufacturing, Government and Public Administrationm and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud |

| On-Premises |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises |

| Customer Data Collection and Profile Unification |

| Audience Segmentation and Personalization |

| Marketing Campaign and Customer Journey Orchestration |

| Customer Analytics and Insights |

| Consent and Preference Management |

| Other Applications |

| Retail and E-Commerce |

| Banking, Financial Services, and Insurance (BFSI) |

| Healthcare and Life Sciences |

| IT and Telecom |

| Media and Entertainment |

| Industrial Manufacturing |

| Government and Public Administration |

| Other End-User Industries |

| By Offering | Software |

| Services | |

| By Deployment Mode | Cloud |

| On-Premises | |

| Hybrid | |

| By Organization Size | Large Enterprises |

| Small and Medium Enterprises | |

| By Application | Customer Data Collection and Profile Unification |

| Audience Segmentation and Personalization | |

| Marketing Campaign and Customer Journey Orchestration | |

| Customer Analytics and Insights | |

| Consent and Preference Management | |

| Other Applications | |

| By End-User Industry | Retail and E-Commerce |

| Banking, Financial Services, and Insurance (BFSI) | |

| Healthcare and Life Sciences | |

| IT and Telecom | |

| Media and Entertainment | |

| Industrial Manufacturing | |

| Government and Public Administration | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the 2026 size of the Netherlands customer data platform sector?

The 2025 market size stands at USD 150.01 million, and further it reaches USD 195.46 million in 2026 and is projected to reach USD 734.36 million by 2031 at a 30.31% CAGR.

Which offering type leads revenue in the Netherlands customer data platform space?

Software led with a 72.64% share in 2025 because enterprises still anchor adoption around a governed platform before adding higher levels of services.

Which deployment model is growing fastest in the Netherlands?

Cloud is the fastest-growing deployment model with a 32.13% CAGR through 2031, and it also held the largest share at 64.91% in 2025.

Why are Dutch companies investing more in customer data platforms now?

Strong digital readiness, tighter privacy expectations, and the need to unify customer identities across channels are pushing enterprises to move away from fragmented data tools.

Which application area is expanding the fastest?

Audience segmentation and personalization is projected to grow at a 33.21% CAGR, supported by stronger conversion pressure and wider use of AI-enabled activation.

Which end-user segment offers the strongest future growth potential?

Healthcare and life sciences is expected to post the fastest growth at a 32.86% CAGR as data governance and structured digital record requirements become more important.

Page last updated on: