Netherlands Co-Living Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

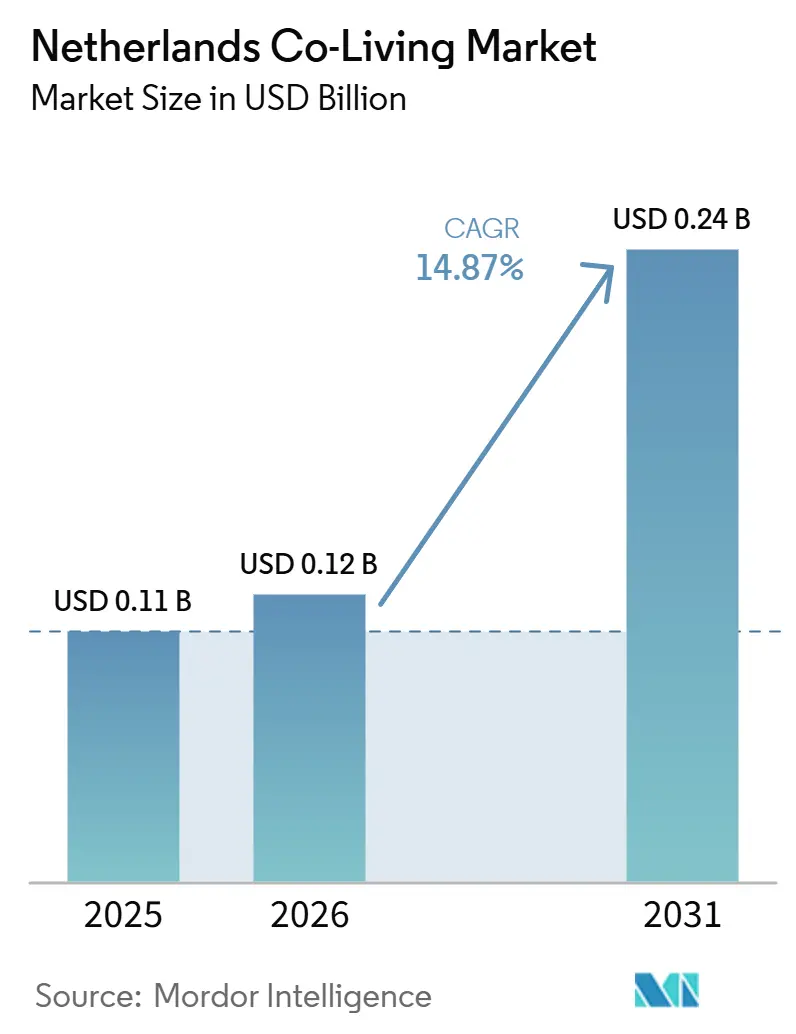

| Base Year Market Size (2025) | USD 0.11 Billion |

| Market Size (2026) | USD 0.12 Billion |

| Market Size (2031) | USD 0.24 Billion |

| Growth Rate (2026 - 2031) | 14.87% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Netherlands Co-Living Market Analysis by Mordor Intelligence

The Netherlands Co-Living Market size is projected to expand from USD 0.11 billion in 2025 and USD 0.12 billion in 2026 to USD 0.24 billion by 2031, registering a CAGR of 14.87% between 2026 to 2031.

The Netherlands co-living market is expanding because the country still faces a large housing shortfall, which keeps occupancy conditions favorable in major cities. The housing shortage stood at 396,000 homes in 2025, while only 69,000 new-build homes were completed that year against the government target of 100,000 homes a year. The Dutch parliament also received a forecast showing that 702,100 homes are needed between 2025 and 2030 to absorb household formation, reduce the shortage, and replace homes scheduled for demolition. The Netherlands co-living market is also gaining support from institutional capital, with large commitments from ABP through Greystar and Rockfield tied to new rental and student housing delivery. Growth still faces pressure from rent regulation, stricter compliance rules, and a permitting environment that remains slow in parts of the country.

Key Report Takeaways

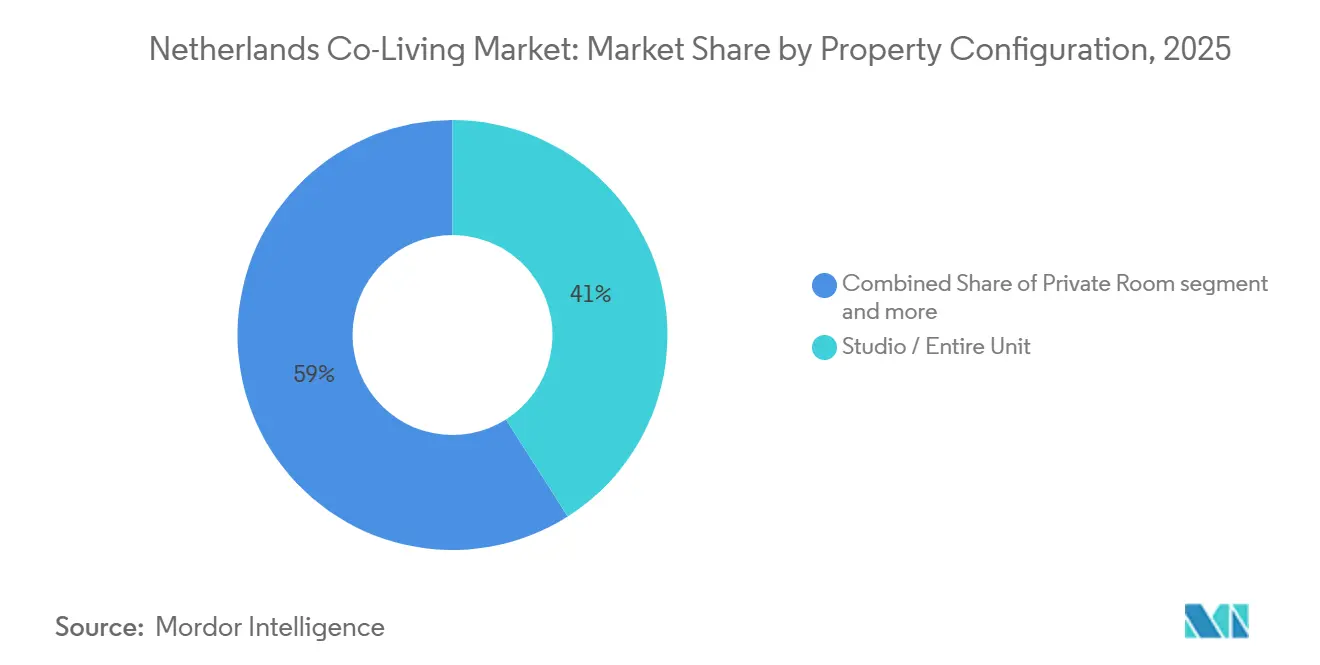

- By property configuration, studios / entire units accounted for 41% of the Netherlands co-living market share in 2025, while shared rooms are forecast to expand at a 15.50% CAGR through 2031.

- By business model, asset-light master lease / lease arbitrage accounted for 51% of the Netherlands co-living market size in 2025, while asset-light management agreement recorded the highest projected CAGR of 16.4% through 2031.

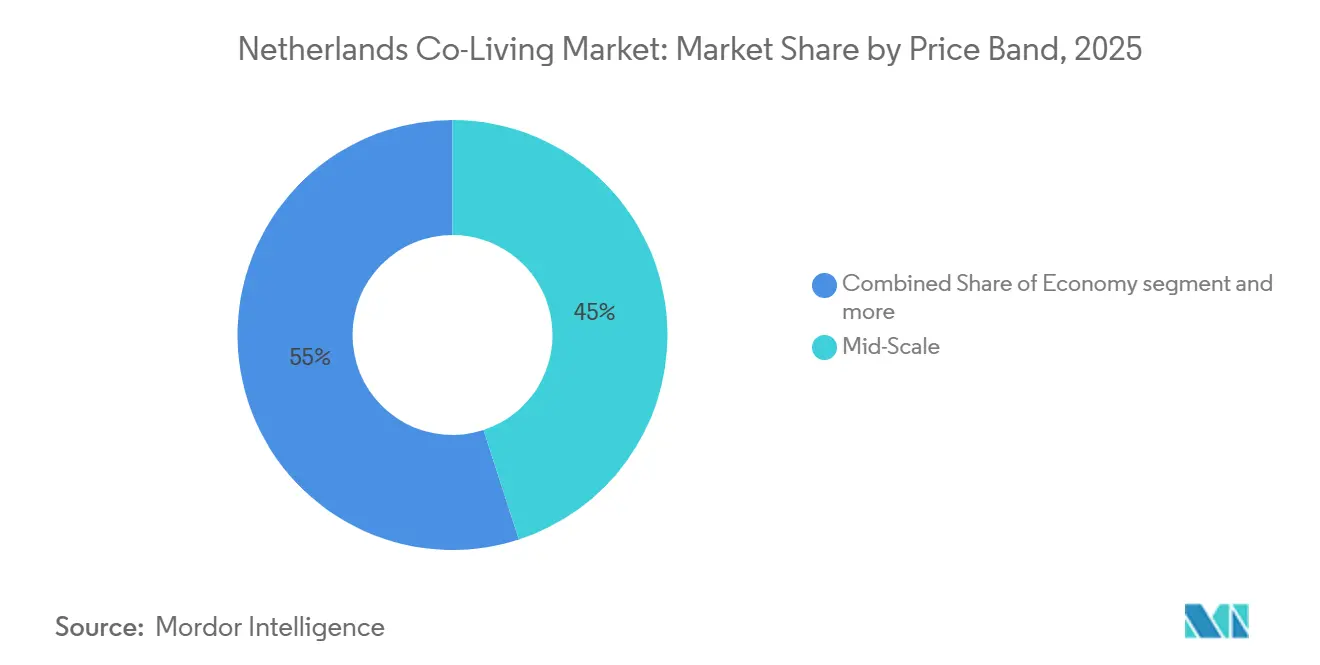

- By price band, mid-scale accounted for 45% of revenue in 2025, while premium / luxury is advancing at a 15.9% CAGR through 2031.

- By end user, working professionals accounted for 55% of revenue in 2025, while students are projected to grow at the fastest rate of 15.98% through 2031.

- By city, Amsterdam accounted for 34% of revenue in 2025, while Eindhoven is forecast to expand at a 17.00% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Netherlands Co-Living Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Severe Urban Housing Shortage Drives Co-Living Demand | +4.2% | National, acute in Amsterdam, Utrecht, and Rotterdam | Short term (≤ 2 years) |

| High Urban Rents Increase Demand for Affordable Shared Living | +2.8% | Amsterdam, Rotterdam, Utrecht core, spillover to Eindhoven | Short term (≤ 2 years) |

| Strong Inflow of International Students and Professionals Expands Occupancy | +2.5% | Amsterdam, Eindhoven, Rotterdam, Utrecht | Medium term (2-4 years) |

| Preference for Flexible and Low-Commitment Living Boosts Market Adoption | +1.8% | National, urban centers | Medium term (2-4 years) |

| Expansion of Build-to-Rent Developments Creates Co-Living Opportunities | +1.5% | Amsterdam, Utrecht, Leiden, The Hague | Medium term (2-4 years) |

| Growing Acceptance of Community-Oriented Housing Supports Market Growth | +1.2% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Severe Urban Housing Shortage Drives Co-Living Demand

The Netherlands co-living market is shaped by a housing shortage that has persisted and deepened across urban centers. The shortage reached 396,000 homes in 2025, equal to 4.8% of the national housing stock, while new completions stayed well below the stated national target[1]CBS (Statistics Netherlands), “Growth of Housing Stock Slows for Third Year in a Row,” CBS, cbs.nl. The parliamentary housing monitor also showed that 702,100 homes are required between 2025 and 2030 to meet household growth, reduce the backlog, and replace obsolete stock. This supply gap keeps pressure on conventional rental channels and supports steady demand for furnished, professionally managed shared housing. The Netherlands co-living market benefits because it can serve renters who need speed, flexibility, and a simpler onboarding process than the mainstream rental process often provides. That makes occupancy support less dependent on short-term consumer sentiment and more dependent on the underlying housing imbalance.

High Urban Rents Increase Demand for Affordable Shared Living

High rents in Dutch cities continue to push a wider set of tenants toward shared and bundled housing formats. This shift is not only about lower headline rent, because many co-living products also combine utilities, furnishings, internet access, and common-area services into a single monthly payment. That bundled structure makes cost planning easier for students, early-career workers, and international arrivals who may not want the setup costs of a standard unfurnished unit. It also helps operators position shared housing as a practical value option rather than a niche lifestyle product. As regulation tightens the mid-rental segment, some private landlords may reduce activity or reinvest selectively, which can increase the appeal of managed formats with clearer service standards. The Netherlands co-living market, therefore, gains from a wider demand base that now includes renters motivated by predictability as much as by price.

Strong Inflow of International Students and Professionals Expands Occupancy

The Netherlands co-living market continues to draw support from mobile student and professional populations that need housing soon after arrival. International students remain a core demand pool because they often need an English-language leasing process, shorter search times, and more structured access to furnished housing. Utrecht University’s reserved accommodation program demonstrates that universities already work with housing partners such as SSH, Xior, and Plaza to channel demand to managed providers. Large employers and technology clusters also sustain demand from project staff, relocated employees, and professionals on medium-term assignments. This group values flexibility, ready-to-use units, and a smoother move-in process more than long lease security in the first stage of relocation. That combination supports year-round occupancy and helps the Netherlands co-living market maintain stable demand beyond the academic calendar.

Preference for Flexible and Low-Commitment Living Boosts Market Adoption

The Netherlands co-living market is gaining traction as many renters now prefer housing that does not require long-term lease commitments, a large setup effort, or complex move-in procedures. This matters more in a market where the housing shortage remained at 396,000 homes in 2025, because tenants often need a workable option quickly rather than waiting for a conventional rental to become available. Co-living operators meet that need through furnished units, bundled services, and simpler onboarding, making the format easier to access for people new to a city or the country. The appeal is especially clear among international students, where formal accommodation pipelines, such as Utrecht University’s reserved-housing program, already direct demand toward organized housing partners rather than the open rental market. It is also relevant for young professionals entering mixed residential schemes, such as Greystar’s Merwede Block 1 in Utrecht, which combines student, mid-market, private-sector, and short-stay housing within a single project. As a result, flexibility is becoming a core reason people choose co-living, as it better fits mobile lifestyles than the standard Dutch rental process.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory Pressure on Rental Policies and Tenancy Rules Limits Market Growth | -1.8% | National, highest enforcement in Amsterdam and Utrecht | Short term (≤ 2 years) |

| High Development Costs Constrain New Co-Living Investments | -1.5% | National | Long term (≥ 4 years) |

| Limited Availability of Suitable Urban Assets Restricts New Supply | -1.2% | Amsterdam, Utrecht, spillover to Rotterdam | Medium term (2-4 years) |

| Local Opposition Delays High-Density Shared Housing Developments | -0.9% | Amsterdam, Rotterdam, Eindhoven city cores | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory Pressure on Rental Policies and Tenancy Rules Limits Market Growth

The Affordable Rent Act changed the operating conditions of the Netherlands co-living market by widening rent regulation in the residential sector. The law took effect on July 1, 2024, and properties scoring up to 186 WWS points are subject to a rent ceiling of EUR 1,157 (USD 1,238) per month on new contracts. From January 2025, municipalities received enforcement powers, including fines of up to EUR 100,000 (USD 107,000) for non-compliance. Shared accommodation is also affected because the valuation framework applies to non-self-contained residential space, which directly influences room-level pricing decisions. This narrows the pool of assets that can be converted or operated profitably under lighter capital models. The result is that larger operators with stronger fit-out budgets, better compliance systems, and the ability to upgrade assets above regulated thresholds hold a clearer advantage.

High Development Costs Constrain New Co-Living Investments

High development costs continue to slow the pace of new supply for the Netherlands co-living market. The Organisation for Economic Co-operation and Development’s 2025 survey on the Netherlands highlighted regulatory bottlenecks, environmental limits, and nitrogen-related constraints as key reasons housing delivery remains below need. These pressures matter more in co-living because many projects require higher interior standards, stronger energy performance, and more shared amenity space than a basic rental scheme. That raises the capital required before operators can reach pricing levels that support returns under the new rent regime. Smaller developers and local operators face the sharpest pressure because they lack the same level of financing depth as institutional platforms. This slows new entry and tends to concentrate expansion around players with long-duration capital and established delivery partners.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Property Configuration: Private Units Anchor Revenue as Shared Rooms Accelerate

Studio / entire unit held 41% of 2025 revenue, making it the largest property configuration in the Netherlands co-living market. This segment benefits from demand from working professionals who want privacy in sleeping and living space while still valuing shared amenities, events, and a managed building experience. Self-contained formats also give operators more room to differentiate through design, layout quality, and resident services. In a stricter regulatory setting, better-specified units can also help owners position assets more effectively within the valuation framework that now shapes rent levels in the broader rental market[2]Volkshuisvesting Nederland, “What Does the Affordable Rent Act Mean for Me?,” Volkshuisvesting Nederland, volkshuisvestingnederland.nl.

Private rooms remain important because they balance lower cost with a minimum level of personal space, keeping them relevant for students and early-career professionals. It also gives the Netherlands co-living market a format that can work across student-focused assets, mixed-use buildings, and city-center conversions. Xior’s 98% occupancy at the end of 2025 supports the wider point that well-managed shared residential assets continue to attract stable demand when location and service quality are aligned. Shared room is projected to grow at a 15.50% CAGR through 2031, reflecting a part of the tenant base that is choosing lower entry cost over privacy. This growth is being driven more by affordability pressure than by product preference. Operators that combine studios, private rooms, and shared rooms within one building can serve several budgets at once and reduce vacancy risk. That mixed configuration approach should remain important as the Netherlands co-living market expands across both premium and value-focused demand pools.

By Business Model: Master Lease / Lease Arbitrage Leads While Management Agreements Gain Ground

Asset-light master lease / lease arbitrage captured 51% of revenue in 2025, demonstrating that speed and capital efficiency still matter in the Netherlands co-living market. Under this model, operators lease whole buildings or large blocks from owners and then run the product, resident experience, and unit monetization directly. Owners benefit from a single operating counterparty and more predictable income flows, while operators benefit from a faster rollout than a development-led approach. This model has held up because housing demand is immediate, while new development remains slower due to planning and environmental constraints.

The asset-light management agreement is the fastest-growing model, with a 16.40% CAGR through 2031 in the Netherlands co-living market. This structure reduces the operator's lease liability and becomes more attractive when regulation limits margins on lower-scoring assets. Habyt’s launch of Leaze in May 2026 is a clear sign that operators are building dedicated platforms for this management-led layer of the Netherlands co-living market. The model also suits landlords who now understand the category better and want operating expertise without transferring all economics to a head lease. Own-develop-operate remains important for institutional players because it offers the greatest control over design, resident mix, and long-term asset quality. Even so, it is the most capital-intensive route and therefore remains concentrated among better-funded groups such as Greystar and other scaled residential specialists. Over time, the Netherlands co-living market is likely to support all three models, but the strongest growth is moving toward lower-balance-sheet structures paired with stronger operating systems.

By Price Band: Mid-Scale Anchors Revenue While Premium / Luxury Tier Outpaces Growth

Mid-scale accounted for 45% of revenue in 2025, giving it the largest share in the Netherlands co-living market. This segment serves working professionals, post-graduate students, and new urban renters who want a managed setting but still need reasonable monthly costs. Mid-scale products are usually judged less on headline luxury and more on layout efficiency, service reliability, and community value. In the current regulatory climate, that means operators need strong execution in fit-out, occupancy management, and building operations to protect returns.

Premium / luxury is projected to expand at a 15.9% CAGR through 2031, making it the fastest-growing price band in the Netherlands co-living market. This is supported by operator efforts to create higher-quality units, stronger amenity packages, and improved energy performance, which can support pricing above the regulated band. The Affordable Rent Act indirectly reinforces this strategy by providing stronger economics for assets that can meet higher-quality thresholds. Premium demand is also supported by international professionals who want design quality, furnished units, and a smoother relocation process. At the lower end, Economy remains relevant, but new dedicated supply is more limited because developers are prioritizing schemes with stronger operating economics. This leaves mid-scale as the largest volume tier and premium / luxury as the tier with the clearest growth momentum. Together, these 2 bands shape most of the current revenue base and most of the future product innovation in the Netherlands co-living market.

By End User: Working Professionals Anchor Revenue as Student Demand Builds

Working professionals accounted for 55% of 2025 revenue, making them the largest end-user group in the Netherlands co-living market. This segment benefits from year-round occupancy patterns and a lower reliance on academic seasonality. Professionals relocating for work often value fast move-in, furnished units, and shorter commitment periods during the first phase of relocation. That makes managed co-living especially relevant in large employment centers and technology corridors where talent mobility is high.

The student segment is projected to grow at the fastest pace, with a 15.98% CAGR through 2031 in the Netherlands co-living market. University-linked demand pipelines support this outlook, and Utrecht University’s reserved accommodation program is one clear example of structured access through partners such as SSH, Xior, and Plaza. Greystar’s Merwede Block 1 in Utrecht includes 300 student apartments within a wider 779-home scheme, which shows how student demand is being built into larger residential platforms rather than treated as a separate niche. Students remain highly relevant because they often need faster access, simpler contracts, and more structured housing channels than the open rental market provides. At the same time, the line between student housing and young professional co-living is becoming less rigid in mixed-use developments. That keeps end-user segmentation important for design and pricing, but less restrictive for asset strategy. The Netherlands co-living market, therefore, gains demand from both a stable working population and a rising student flow.

Geography Analysis

Amsterdam accounted for 34% of 2025 revenue, keeping it in the lead across the Netherlands co-living market. The city remains the most established location for international demand, premium positioning, and operator visibility. It also remains one of the most important places for capital deployment because large investors and developers can justify scale there more easily than in smaller cities. Even with tighter regulation, Amsterdam still sets the pace for the Netherlands co-living market because it combines strong tenant inflow with a broad range of potential resident profiles.

Rotterdam and Utrecht form the next major growth belt for the Netherlands co-living market. Rotterdam offers a large urban base and supports operator expansion beyond the capital, while Utrecht shows strong depth in both student and young professional demand. Greystar started construction on the 779-home Merwede Block 1 project in Utrecht in December 2025, funded within the ABP venture[3]Greystar, “ABP and Greystar Invest 500 Million in Dutch Housing Market,” Greystar, greystar.com. The project includes student, mid-market, private-sector, and short-stay units, reflecting the mixed demand profile that increasingly defines the Netherlands co-living market. Ballast Nedam Development and McAleer & Rushe Property (MRP) also completed the sale of 1,000 rental homes in Utrecht’s Cartesius district to CBRE Investment Management, which reinforces the city’s long-term investment appeal.

Eindhoven is projected to expand at a 17.00% CAGR through 2031, making it the highest-growth urban segment in the Netherlands co-living market. Its strength comes from the Brainport innovation corridor and the inflow of internationally mobile workers linked to advanced technology and manufacturing. The SSLV platform launched by ABP and Rockfield is also aimed at student cities and starter-home demand, which supports a wider city network beyond Amsterdam alone. That means the Netherlands co-living market is gradually broadening into a multi-city platform, with Amsterdam as the revenue anchor, Utrecht and Rotterdam as pipeline centers, and Eindhoven as the fastest-growing demand node.

Competitive Landscape

The Netherlands co-living market is moderately concentrated, with Greystar, Xior Student Housing, The Social Hub, and DUWO forming the leading group while a long tail of smaller operators remains active. This structure gives the largest platforms better access to capital, operating systems, university links, and city-level relationships. At the same time, the fragmented second tier means no single operator has closed off the market. The main competitive split is between institutional-scale developers and owners on one side, and lighter operating platforms on the other side. That balance keeps the Netherlands co-living market competitive, but it still favors groups that can combine compliance strength with delivery scale.

Greystar has strengthened its position through both development and capital partnerships in the Netherlands co-living market. ABP raised its commitment to Greystar’s Dutch Essential Housing Venture to EUR 920 million (USD 1.05 billion) in September 2025, and the venture now supports live projects across multiple cities. Greystar also sold OurDomain Rotterdam Blaak to Bouwinvest while retaining the role of property and community manager, demonstrating a model in which capital ownership and operating expertise are separated rather than bundled. Xior remains relevant because it pairs scale with very high occupancy, reporting 98% occupancy and a EUR 3.6 billion (USD 4.11 billion) European portfolio in 2025. That combination of scale, occupancy, and resident focus matters in the Netherlands co-living market because it supports both investor confidence and expansion discipline.

The asset-light layer is also becoming more defined in the Netherlands co-living market. Habyt launched Leaze in May 2026 as a standalone asset-light co-living brand with its own digital leasing, pricing, and booking infrastructure. That move shows how operating technology is becoming a stronger source of differentiation for management-led platforms. Rockfield’s SSLV partnership with ABP also points to a market where sustainability standards, institutional governance, and product quality will matter more in future project selection. The result is a competitive field where smaller entrants can still win at a local level, but the largest opportunities are increasingly moving toward operators that can meet institutional standards across several cities.

Netherlands Co-Living Industry Leaders

The Social Hub

Xior Student Housing

Student Experience

DUWO

SSH Student Housing

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Habyt launched Leaze as a standalone asset-light co-living brand, separating its shared-living and hospitality-led operations following divestitures of portfolios in France, Portugal, Spain, and Asia-Pacific. Leaze is equipped with proprietary digital leasing, pricing, and booking infrastructure designed for localized, smaller-scale co-living operators, representing a major strategic pivot toward technology-enabled managed co-living at the asset-light tier.

- May 2026: ABP and Rockfield Real Estate jointly launched the Student & Starter Social Living Venture (SSLV), a EUR 350 million (USD 374.5 million) fund targeting more than 2,000 affordable, sustainable homes for students and young professionals across Dutch student cities. All assets will be developed to BREEAM-NL Excellent and CRREM standards, establishing an institutional sustainability benchmark for the student co-living segment.

- December 2025: Greystar commenced construction on Merwede Block 1 in Utrecht, a 779-home development funded through the ABP Dutch Essential Housing Venture. The EUR 200 million (USD 214 million) scheme comprises 300 student apartments, 305 mid-market rentals, 89 private-sector homes, and 85 short-stay student units, with at least two-thirds featuring regulated rents. Delivery is expected in 2028.

Netherlands Co-Living Market Report Scope

The Netherlands Co-Living Market Report is Segmented by Property Configuration (Studio / Entire Unit, Private Room, and Shared Room), Business Model (Asset-Light Master Lease / Lease Arbitrage and More), Price Band (Economy, Mid-Scale, and Premium / Luxury), End User (Students, and Working Professionals), and City (Amsterdam, Rotterdam, Eindhoven, Utrecht, and More). The Market Forecasts are Provided in Terms of Value (USD).

| Studio / Entire Unit |

| Private Room |

| Shared Room |

| Asset-Light Master Lease / Lease Arbitrage |

| Asset-Light Management Agreement |

| Asset-Heavy Own-Develop-Operate |

| Economy |

| Mid-Scale |

| Premium/Luxury |

| Students |

| Working Professionals |

| Amsterdam |

| Rotterdam |

| Eindhoven |

| Utrecht |

| Rest of Netherlands |

| By Property Configuration | Studio / Entire Unit |

| Private Room | |

| Shared Room | |

| By Business Model | Asset-Light Master Lease / Lease Arbitrage |

| Asset-Light Management Agreement | |

| Asset-Heavy Own-Develop-Operate | |

| By Price Band | Economy |

| Mid-Scale | |

| Premium/Luxury | |

| By End User | Students |

| Working Professionals | |

| By City | Amsterdam |

| Rotterdam | |

| Eindhoven | |

| Utrecht | |

| Rest of Netherlands |

Key Questions Answered in the Report

How large is the Netherlands co-living space in 2031?

It is forecast to reach USD 0.24 billion by 2031, up from USD 0.11 billion in 2025, with a 14.87% CAGR from 2026 to 2031.

Which tenant group brings in the most revenue in the Netherlands?

Working professionals led with 55% of revenue in 2025 because they support more stable year-round occupancy than student-only properties.

Which city is growing fastest for shared urban living in the Netherlands?

Eindhoven is the fastest-growing city segment, with a projected 17.00% CAGR through 2031, supported by its technology and advanced manufacturing base.

Why is demand staying strong even with tighter regulation?

The housing shortage remained severe at 396,000 homes in 2025, and new completions stayed below target, which keeps pressure on the rental market and supports managed shared housing.

Page last updated on: