Nephrology And Urology Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

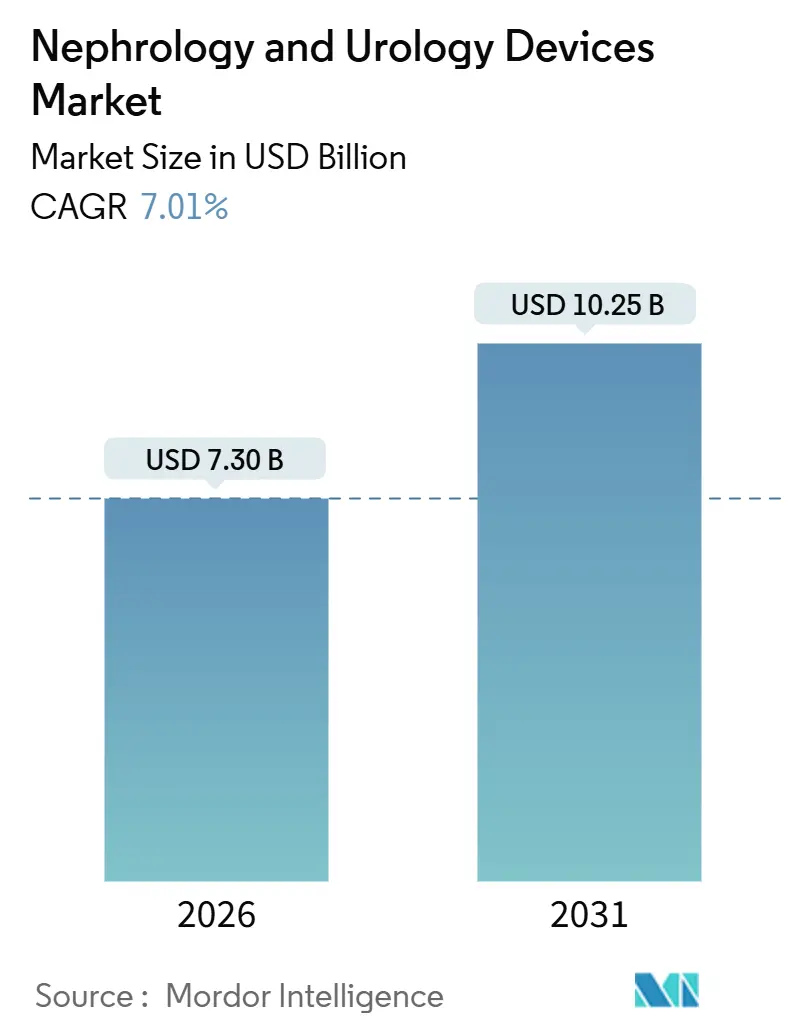

| Market Size (2026) | USD 7.30 Billion |

| Market Size (2031) | USD 10.25 Billion |

| Growth Rate (2026 - 2031) | 7.01% CAGR |

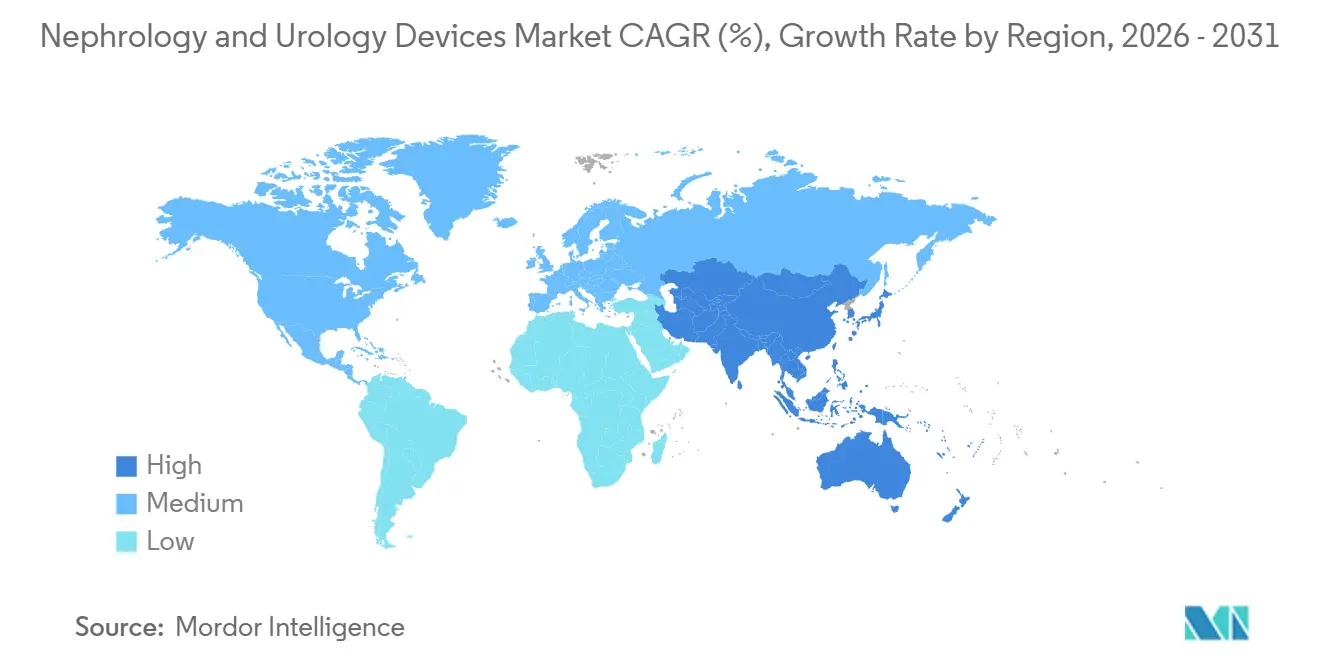

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Nephrology And Urology Devices Market Analysis by Mordor Intelligence

The Nephrology And Urology Devices Market size is estimated at USD 7.30 billion in 2026, and is expected to reach USD 10.25 billion by 2031, at a CAGR of 7.01% during the forecast period (2026-2031).

This anchors the current market size, forecast value, and expected growth trajectory. An expanding elderly population, rising chronic kidney disease prevalence, and growing preference for home-based renal replacement therapy are widening the addressable patient pool. Rapid adoption of minimally invasive surgery, coupled with artificial-intelligence-enabled procedural guidance, is improving clinical outcomes and shortening hospital stays. North America retained 42.32% revenue share in 2025, yet the Asia-Pacific region is advancing the fastest at 8.54% through 2031, supported by public investment in high-throughput dialysis infrastructure and streamlined regulatory approvals. Competitive intensity remains moderate, with top suppliers collectively accounting for 55% of revenue, leaving room for regional specialists and technology disruptors.

Key Report Takeaways

- By application, kidney diseases commanded 45.65% of the Nephrology and Urology Devices market share in 2025, while urological cancer is set to expand at a 9.76% CAGR through 2031.

- By end-user, hospitals and clinics held 58.65% of the Nephrology and Urology Devices market in 2025, whereas home-care settings are advancing at a 10.22% CAGR through 2031.

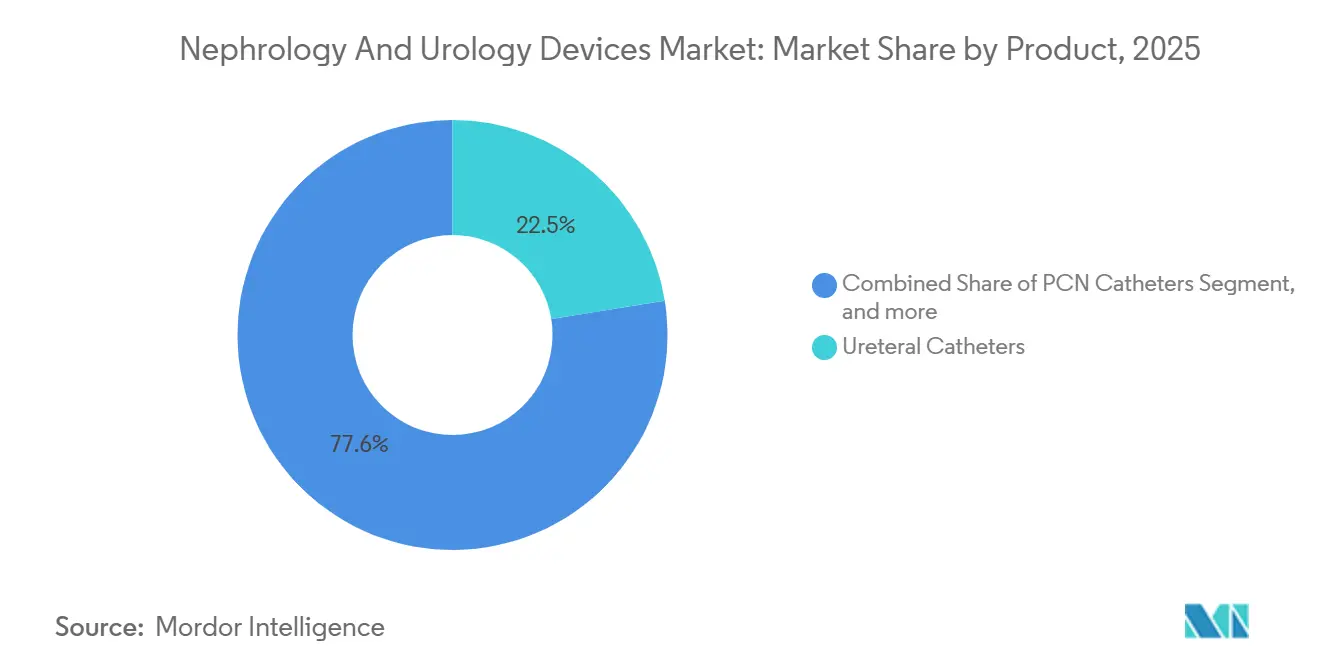

- By product, ureteral catheters captured 22.45% of revenue and are also rising at a 9.43% CAGR through 2031.

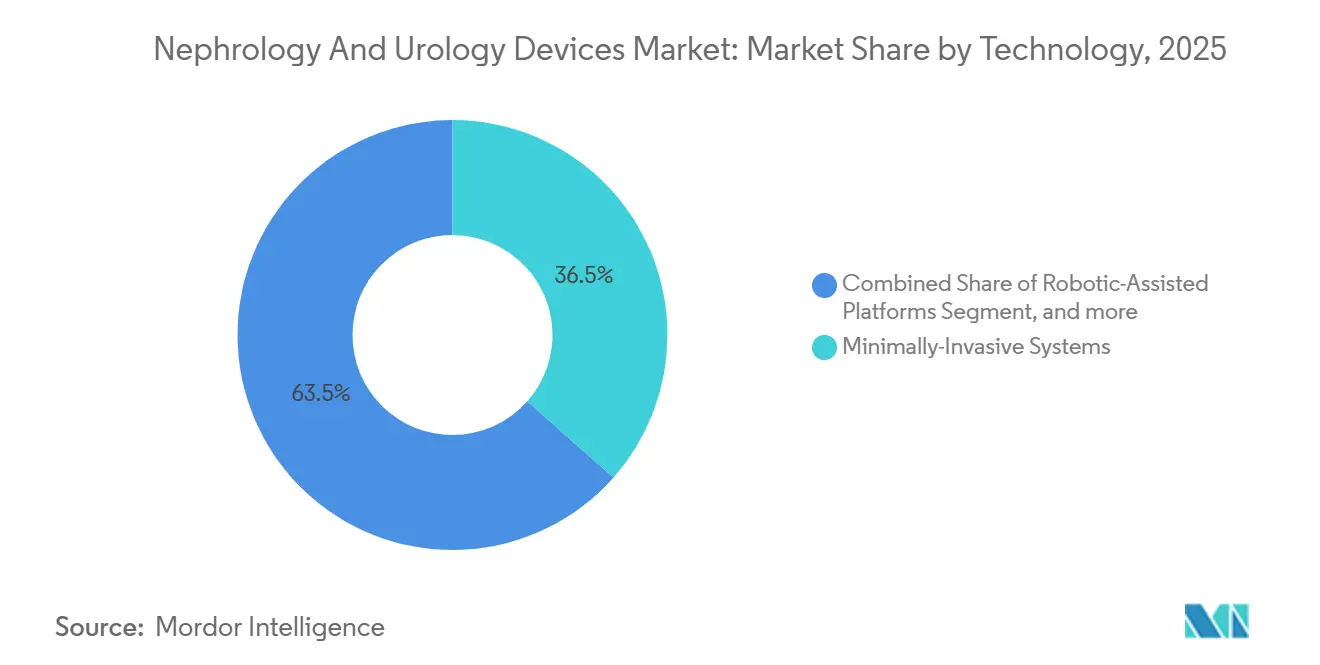

- By technology, robotic-assisted platforms accounted for 36.54% revenue in 2025 and are growing at 9.21% through 2031, reflecting clinicians’ preference for precision surgery.

- By geography, Asia-Pacific is projected to register the fastest CAGR of 8.54% through 2031, outpacing North America’s mature but steady trajectory.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Nephrology And Urology Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating global burden of chronic kidney disease and urinary disorders | +1.8% | Global, with acute pressure in APAC and MEA | Long term (≥ 4 years) |

| Expansion of high-throughput dialysis infrastructure in emerging economies | +1.5% | APAC core (China, India), spill-over to MEA and South America | Medium term (2-4 years) |

| Rapid adoption of minimally invasive and robotic urologic procedures | +1.3% | North America & EU, early gains in Japan and South Korea | Short term (≤ 2 years) |

| Integration of artificial intelligence in diagnostics and procedural guidance | +1.0% | North America, EU, pilot deployments in urban APAC centers | Medium term (2-4 years) |

| Surge in home-based renal care and portable treatment platforms | +1.2% | North America, Western Europe, gradual uptake in urban Latin America | Medium term (2-4 years) |

| Growing public-private investment in next-generation bioartificial kidney R&D | +0.8% | United States (NIDDK funding), EU Horizon programs, early-stage in Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Global Burden of Chronic Kidney Disease and Urinary Disorders

Chronic kidney disease affected 850 million people worldwide in 2026, reflecting a 29% climb since 2019 and expanding the user base for dialysis access devices, ureteral stents, and stone-management systems[1]The Lancet, “Global Burden of Kidney Disease,” LANCET.COM. Urolithiasis incidence rose 15% over the past five years, especially among adults aged 40–60, a trend linked to higher sodium intake and sedentary lifestyles[2]Journal of the American Society of Nephrology, “Trends in Urolithiasis Incidence,” JASN.ORG. The World Health Organization projects kidney disease to become the fifth leading cause of years of life lost by 2030, highlighting the need for scalable treatment infrastructure. Manufacturers are responding with single-use nitinol stone baskets that reduce procedural time 20%, lowering per-case costs in high-volume centers. Conservative forecasts still indicate a 3% yearly rise in end-stage renal disease through 2035, ensuring stable demand for vascular-access catheters and peritoneal dialysis consumables.

Expansion of High-Throughput Dialysis Infrastructure in Emerging Economies

China added 1,200 new dialysis centers in 2025, while India allocated USD 450 million to expand capacity in smaller cities, bringing treatment within 50 kilometers for many rural patients. Public-private partnerships accelerate rollout; Fresenius now operates 350 clinics in India under a franchise model that spreads capital expenditure, and similar expansions are unfolding in Indonesia and Vietnam via government tenders that rose 40% in 2025. Suppliers with local distribution and service capacity, such as Nipro and Terumo, win preferential procurement agreements by bundling training and maintenance, reinforcing their footprint. The infrastructure build-out broadens addressable demand for dialyzers, bloodlines, and ancillary urology consumables, fueling the nephrology and urology devices market.

Rapid Adoption of Minimally Invasive and Robotic Urologic Procedures

Robotic-assisted platforms handled 120,000 urological cases in the United States in 2025, with prostatectomy and partial nephrectomy accounting for 65% of that volume. Hospitals justify the USD 2 million capital cost by citing a 1.8-day average length of stay for robotic prostatectomy versus 3.2 days after open surgery, thereby shaving readmission penalties under value-based payment models. Disposable ureteroscopes, such as Boston Scientific’s LithoVue Elite, remove the need for reprocessing, curbing cross-contamination risk and appealing to ambulatory centers that lack dedicated sterilization capacity. Vendors shift from durable-goods sales to per-procedure consumable revenue, smoothing cash flow even when capital budgets tighten. Early adoption in Japan and South Korea signals an Asian inflection, helped by payer coverage for robotic prostatectomy and government incentives for minimally invasive surgery.

Integration of Artificial Intelligence in Diagnostics and Procedural Guidance

Machine-learning algorithms now predict acute kidney injury 48 hours before serum creatinine elevation, enabling nephrologists to intervene sooner and avoid costly intensive care admissions. During ureteroscopy, real-time image recognition classifies stone composition with 90% accuracy, guiding laser settings that shorten fragmentation time by 15%. The FDA granted breakthrough-device status to three AI-based renal-function monitors in 2025, underscoring regulatory appetite for decision-support software. CMS followed by adding a distinct reimbursement code for procedures that use FDA-cleared AI tools, creating a payment incentive for hospitals to adopt them. Edge-computing prototypes deployed in urban Brazil and South Africa process data locally, proving viable in regions with limited cloud connectivity.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital and consumable costs limiting adoption in resource-constrained settings | -1.2% | Sub-Saharan Africa, South Asia, rural Latin America | Long term (≥ 4 years) |

| Stringent and divergent regulatory approval pathways across major markets | -0.9% | Global, with acute friction between FDA and EU MDR | Medium term (2-4 years) |

| Inadequate reimbursement frameworks for home and wearable dialysis solutions | -0.7% | Emerging markets in APAC, MEA, and South America | Medium term (2-4 years) |

| Supply chain vulnerabilities for medical-grade polymers and semiconductor components | -0.6% | Global, with concentration risk in Northeast Asia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital and Consumable Costs Limiting Adoption in Resource-Constrained Settings

A single hemodialysis machine costs USD 15,000–25,000, while annual consumables per patient exceed USD 12,000 in high-income markets, figures that dwarf the USD 150 per-capita health spend in sub-Saharan Africa. Fewer than 5% of end-stage renal disease patients in the region receive dialysis, and those who do often exhaust household savings within six months, leading to catastrophic financial hardship. Holmium-laser lithotripters priced around USD 80,000 remain confined to tertiary centers, forcing rural patients to delay treatment until complications arise. Manufacturers offer refurbished equipment at 40% discounts and tiered pricing for consumables, yet weak insurance coverage and fragmented procurement limit uptake. Until governments allocate dedicated renal budgets or multilateral donors subsidize equipment, adoption gaps will persist across low-income settings.

Stringent and Divergent Regulatory Approval Pathways Across Major Markets

The European Union’s Medical Device Regulation, fully enforced in 2024, requires new clinical investigations for devices previously cleared under the older directive, adding 18–24 months to timelines and raising compliance costs by 30%. By contrast, the FDA’s 510(k) pathway allows substantial-equivalence claims that speed time-to-market but provide less post-market surveillance, prompting firms to prioritize U.S. launches for early revenue. Japan’s sakigake designation offers fast-track review for breakthrough devices, yet mutual-recognition agreements remain limited, forcing manufacturers to duplicate testing and quality audits across regions. A 2025 MedTech Europe survey found that 60% of urology device startups were delaying international expansion by at least 2 years because they lacked the resources to navigate parallel tracks. Slow harmonization under the International Medical Device Regulators Forum means duplicative costs will persist until consensus standards emerge, likely after 2028.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Catheters and Stents Drive Volume, Lithotripters Capture Premium Tier

The ureteral catheters accounted for 22.45% of market share in 2025, underscoring the segment’s centrality to both diagnostic and therapeutic care. Single-use designs already represent 70% of unit sales because infection-control protocols and reimbursement incentives discourage reprocessing. Manufacturers differentiate through anti-encrustation polymers and hydrophilic coatings that minimize indwelling irritation. Higher-priced stone-management devices, including holmium laser lithotripters, attract premium reimbursement in North America and Europe; Asian and Latin American facilities often prefer lower-cost pneumatic systems, but rising disposable income is shifting preferences toward laser platforms. Suppliers leverage recurrent consumable demand, such as optical fibers and single-use baskets, to sustain margins even when capital budgets tighten.

Stone-management devices occupy a smaller slice of revenue yet command higher average selling prices, enhancing vendor profitability. Drug-eluting urinary stents coated with antimicrobial or anti-inflammatory agents reduce infection and encrustation risks, shortening length of stay and lowering readmission penalties. Teleflex’s hydrophilic-coated guidewires illustrate incremental innovation that trims insertion force by 40%, translating to shorter procedure times. Percutaneous nephrostomy catheters are increasingly used as tumors compress ureters, and clinicians increasingly opt for polyurethane shafts that resist kinking during prolonged drainage. Collectively, these trends signal that suppliers able to combine material science with procedure-specific design will capture outsized growth within the nephrology and urology devices market.

By Application: Kidney Diseases Anchor Demand, Oncology Accelerates

Kidney diseases accounted for 45.65% of nephrology and urology devices market share in 2025, buoyed by a worldwide installed base of 3.5 million dialysis patients who require frequent consumables and access devices. Each hemodialysis patient uses about 150 dialyzers annually, providing predictable revenue that insulates suppliers from cyclical swings in capital equipment. The oncology subsegment is the fastest-growing, registering a 9.76% CAGR to 2031 as minimally invasive partial nephrectomy and bladder-tumor ablation displace open surgery. Higher diagnosis rates among aging populations in North America, Europe, and parts of Asia are driving demand for single-use scopes and robotic platforms tailored for delicate resections. Benign prostatic hyperplasia procedures, including water-vapor therapy, remain a mid-tier growth driver, thanks to ambulatory settings that lower overall care costs.

Bladder disorders and incontinence technologies exhibit steady mid-single-digit growth tied to demographic aging and rising obesity prevalence. Intermittent catheters optimized for self-use highlight user-centric design, while sacral neuromodulators extend battery life and wireless programmability. Urolithiasis cases fluctuate with dietary and climatic factors, yet global warming and higher dietary sodium intake suggest an increase in volume over the long term. Congenital anomalies and trauma remain small yet high-value niches that reward suppliers with specialized portfolios and tight surgeon relationships. Overall, application-level diversification smooths revenue volatility across the nephrology and urology devices market.

By Technology: Minimally Invasive Systems Dominate, Robotics and AI Accelerate

In 2025, minimally invasive systems captured 36.54% of the technology-segment market share in the Nephrology and Urology Devices market, with a projected CAGR of 9.21% through 2031. The cost of flexible ureteroscopes dropped from USD 50,000 in 2020 to under USD 30,000, improving access for mid-tier hospitals, especially in the Asia-Pacific region. Robotic platforms, led by Intuitive Surgical’s 8,500-unit installed base, performed 120,000 urological procedures in the U.S. in 2025 and are expanding in Japan and South Korea due to favorable reimbursement policies. Hospitals justify the USD 2 million investment in robotic systems as they reduce hospital stays and readmission penalties. Single-use ureteroscopes, such as Boston Scientific’s LithoVue Elite, enhance cash flow predictability and eliminate cross-contamination risks.

AI-integrated tools accounted for less than 5% of the market in 2025 but attracted significant R&D investments, driven by FDA breakthrough device designations and reimbursement incentives. Real-time algorithms classify stone composition with 90% accuracy, reducing fragmentation time by 15%. Medtronic’s AI-guided navigation lowers radiation exposure by 30% during percutaneous nephrolithotomy. Edge-computing prototypes tested in Brazil and South Africa validate AI workflows in bandwidth-limited regions, signaling growth in emerging markets. Regulatory clarity, expected with the FDA’s software-as-a-medical-device guidance in 2027, is likely to accelerate adoption and diversify revenue streams.

By End-User: Hospitals Lead Revenue, Home Care Rises Fastest

In 2025, hospitals and clinics accounted for 58.65% of the market, driven by high-capital equipment requirements for complex procedures such as percutaneous nephrolithotomy. Academic centers invested in robotic systems and shock-wave lithotripters, leveraging multidisciplinary teams and volume discounts. Ambulatory surgical centers increased their share of U.S. urological procedures to 35%, up from 22% in 2020, as payers favored outpatient settings. Dialysis chains like Fresenius and DaVita standardized device purchasing through captive clinic networks, ensuring predictable consumable demand. Home-care settings, growing at a 10.22% CAGR through 2031, benefited from bundled-payment models and rising adoption of home dialysis. Portable systems, such as Quanta’s SC+ unit, expanded access to rural and disaster zones while reducing infrastructure costs. These shifts reflect a transition from hospital-centric to decentralized, patient-focused delivery models in the market.

Geography Analysis

North America retained 42.32% revenue share in 2025, supported by substantial payer reimbursement and high procedure volumes. Medicare’s bundled payment of roughly USD 240 per dialysis session creates a predictable floor for device demand, and private insurers typically pay 30% to 50% more. Canada’s single-payer model negotiates aggressive discounts, yet steady volumes offset lower unit prices. Mexico’s flourishing private-hospital segment doubled the number of robotic-surgery installations between 2023 and 2025, driven by medical tourism and domestic wealth growth. These dynamics sustain a mature but steady growth path for the nephrology and urology devices market in North America.

Asia-Pacific is the fastest-growing region, with 8.54% growth through 2031, driven by public health programs in China and India that treat dialysis as an essential service. China’s state insurance now reimburses dialysis nationwide, while India’s national program aims to add 5,000 new centers by 2028, anchoring long-term demand for equipment. Japan’s demographic profile 33% of citizens are over 65 drives uptake of incontinence and BPH devices, whereas South Korea expanded reimbursement for robotic prostatectomy, fueling a 40% jump in 2025 procedure volumes. Australia’s fast-track regulatory pathway for AI-integrated ureteroscopes further enhances regional innovation diffusion. Suppliers that localize manufacturing and service capabilities stand to capture the expansion of the nephrology and urology devices market in Asia-Pacific.

Europe presents a mixed picture. Germany’s DRG system incentivizes efficiency, nudging hospitals toward single-use devices that reduce sterilization overhead, while the United Kingdom’s centralized procurement emphasizes cost, slowing innovation uptake. Southern Europe lags in capital budgets but relies on EU structural funds for dialysis infrastructure, offering periodic procurement spikes. The Middle East invests heavily in dialysis as part of broader health-system reforms. At the same time, Africa progresses unevenly, with urban hubs adopting advanced urology technologies and rural areas relying on donor support. South America has a two-tier system: private insurers cover high-end devices in Brazil and Argentina, while public systems face tight budgets, limiting the adoption of advanced technology. These diverse trajectories require tailored go-to-market strategies across the nephrology and urology devices market.

Competitive Landscape

The nephrology and urology devices market is moderately concentrated, with the top five companies accounting for 55% of the revenue. This concentration creates opportunities for regional firms and emerging technology players to establish their presence. Baxter leverages its vertical integration—from dialyzers to renal pharmaceuticals—to secure multiyear contracts with major dialysis organizations. Fresenius, with its extensive network of 4,200 clinics, benefits from a captive customer base for its proprietary devices and consumables, ensuring consistent upstream demand. Boston Scientific and Medtronic capitalize on cross-selling opportunities from their cardiovascular and robotics divisions to strengthen their position in the urology segment. Medtronic’s acquisition of Mazor Robotics’ navigation assets highlights the strategic alignment between robotics and interventional nephrology.

Disruptive innovation in the market is focused on portability and AI. Quanta Dialysis Technologies has introduced a 9.5-kilogram hemodialysis machine designed for rural clinics and disaster relief scenarios. Outset Medical’s all-in-one system eliminates the need for external water treatment, reducing installation costs by 60%. Olympus and Karl Storz are leading patent filings for AI-enabled stone classification algorithms, signaling the emergence of new competitive battlegrounds. Suppliers are increasingly integrating hardware with software ecosystems to lock in users through analytics and decision-support subscriptions. To mitigate supply-chain risks and comply with regional procurement mandates, manufacturers are shifting operations to India and Southeast Asia, optimizing cost structures across the nephrology and urology devices sector.

While scale advantages remain significant, they are not insurmountable. Startups in the portable device segment are outsourcing production to contract manufacturers, reducing fixed costs and accelerating regulatory approvals. Established players are countering this trend through strategic acquisitions; for example, Teleflex’s acquisition of Palette Life Sciences expands its portfolio with hydrophilic-coating intellectual property. The race to develop bioartificial kidneys is attracting both corporate and venture capital investment, with Fresenius committing USD 50 million to establish a dedicated R&D center. As payer incentives and patient preferences evolve, companies aligning their portfolios with home-care and AI-integrated technologies are well-positioned to gain a competitive edge in the nephrology and urology devices market.

Nephrology And Urology Devices Industry Leaders

Fresenius Medical Care AG & Co. KGaA

Baxter International Inc.

Boston Scientific Corporation

Becton, Dickinson and Company

B. Braun Melsungen AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: FDA approved the ProVee System, a prostatic urethral stent for the treatment of patients with benign prostatic hyperplasia (BPH).

- December 2024: The RELIEF ureteral stent received FDA clearance as the first and only stent approved for the prevention of vesicoureteral reflux, a significant cause of patient discomfort. RELIEF’s unique suture design allows the ureteral orifice to open and close naturally, thereby preventing vesicoureteral reflux.

Global Nephrology And Urology Devices Market Report Scope

As per the scope of the report, nephrology and urology devices are specialized medical tools used to diagnose and treat kidney, bladder, and urinary tract conditions. They include equipment like stents, guidewires, and catheters. These devices help manage diseases such as kidney failure, urinary incontinence, and other urological disorders.

The Nephrology and Urology Devices Market is Segmented by Product (Ureteral Catheters, PCN Catheters, Urinary Stents, Stone Management Devices, Urology Guidewires, Renal Dilators, and Other Products), Application (Urolithiasis, Urological Cancer, BPH, Bladder Disorders & Incontinence, Kidney Diseases, and Other Applications), End-User (Hospitals & Clinics, ASCs, Dialysis Centers, Home-Care Settings, and Other End-Users), Technology (Minimally-Invasive, Robotic, Disposable, and AI-Integrated), and Geography (North America, Europe, Asia-Pacific, MEA, and South America). The Market Forecasts are Provided in Terms of Value (USD). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Ureteral Catheters |

| PCN Catheters |

| Urinary Stents |

| Stone Management Devices (Stone Baskets, Lithotripters) |

| Urology Guidewires |

| Renal Dilators |

| Other Products |

| Urolithiasis |

| Urological Cancer |

| Benign Prostatic Hyperplasia (BPH) |

| Bladder Disorders & Incontinence |

| Kidney Diseases |

| Other Applications |

| Hospitals & Clinics |

| Ambulatory Surgical Centers |

| Dialysis Centers |

| Home-Care Settings |

| Other End-Users |

| Minimally-Invasive Systems |

| Robotic-Assisted Platforms |

| Disposable / Single-Use Devices |

| AI-Integrated Diagnostics & Procedure Support |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Ureteral Catheters | |

| PCN Catheters | ||

| Urinary Stents | ||

| Stone Management Devices (Stone Baskets, Lithotripters) | ||

| Urology Guidewires | ||

| Renal Dilators | ||

| Other Products | ||

| By Application | Urolithiasis | |

| Urological Cancer | ||

| Benign Prostatic Hyperplasia (BPH) | ||

| Bladder Disorders & Incontinence | ||

| Kidney Diseases | ||

| Other Applications | ||

| By End-User | Hospitals & Clinics | |

| Ambulatory Surgical Centers | ||

| Dialysis Centers | ||

| Home-Care Settings | ||

| Other End-Users | ||

| By Technology | Minimally-Invasive Systems | |

| Robotic-Assisted Platforms | ||

| Disposable / Single-Use Devices | ||

| AI-Integrated Diagnostics & Procedure Support | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the Nephrology and Urology Devices market?

The market stands at USD 7.30 billion in 2026, with a forecast value of USD 10.25 billion by 2031.

How fast is the market expected to grow?

It is projected to expand at a 7.01% CAGR between 2026 and 2031.

Which region is growing the quickest?

Asia-Pacific is set to advance at an 8.54% CAGR through 2031, outpacing all other regions.

Which application generates the most revenue?

Kidney diseases lead with 45.65% of 2025 revenue, driven by high dialysis consumable demand.

What segment is seeing the fastest technology growth?

Robotic-assisted platforms are growing at 9.21% due to surgeon preference for precision and quicker recovery times.

Who are the leading companies in this space?

Baxter, Fresenius, Boston Scientific, Medtronic, and B. Braun together hold 55% of global revenue.

Page last updated on: