Neonatal Infant Care Equipment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

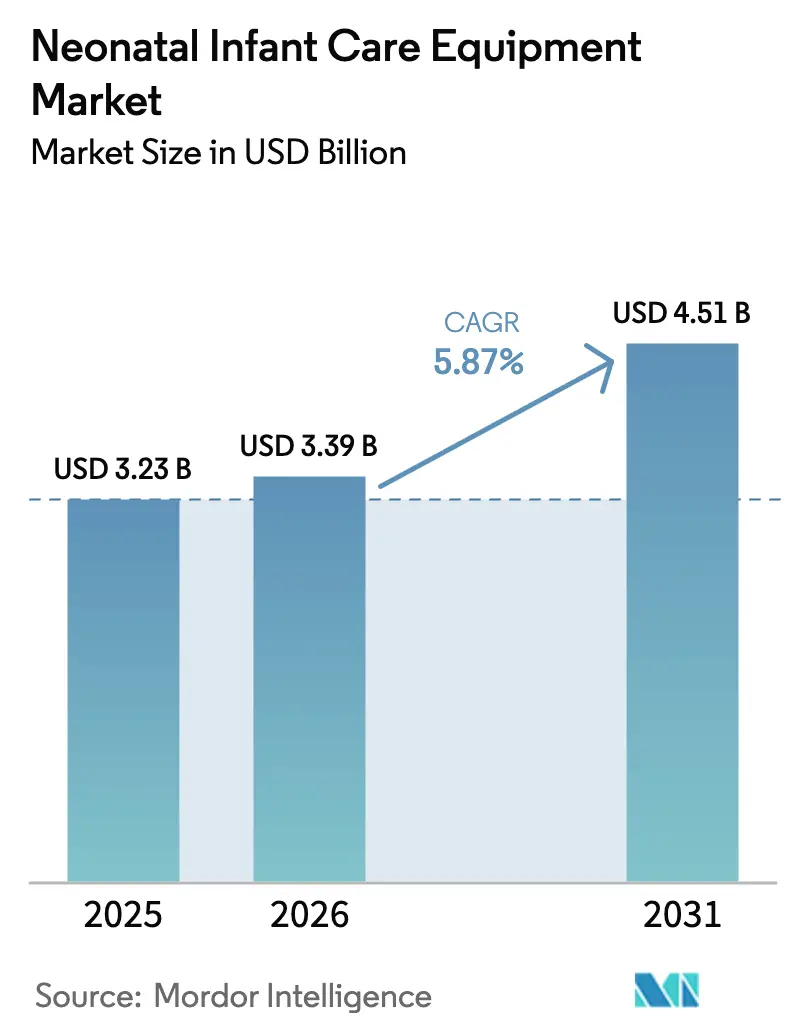

| Market Size (2026) | USD 3.39 Billion |

| Market Size (2031) | USD 4.51 Billion |

| Growth Rate (2026 - 2031) | 5.87% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Neonatal Infant Care Equipment Market Analysis by Mordor Intelligence

The Neonatal Infant Care Equipment Market size is projected to expand from USD 3.23 billion in 2025 and USD 3.39 billion in 2026 to USD 4.51 billion by 2031, registering a CAGR of 5.87% between 2026 to 2031.

Structural demand comes from 13.4 million annual preterm births, with sub-Saharan Africa and South Asia accounting for more than 60% of cases.[1]World Health Organization, “Preterm Birth,” who.int Semiconductor-constrained supply chains and the surge of AI-enabled monitors complicate retrofits for older incubators, forcing legacy vendors to choose between costly redesigns and margin erosion.[2]Office of the Assistant Secretary for Planning and Evaluation, “Semiconductor Supply Chain Deep Dive Assessment,” aspe.hhs.gov Hospitals in high-burden regions are expanding NICU bed density faster than they can train neonatal specialists, creating procurement momentum for sensor-dense devices that simplify workflows. Incubators held 32.14% product revenue in 2025, yet respiratory support devices are forecast to grow 8.43%, reflecting pandemic-era ventilator scale-up that preserved component inventories and engineering talent. Neurological care, catalyzed by Ceribell’s 2025 FDA clearance for bedside seizure detection, is the fastest-rising application at 9.61% CAGR, signaling a pivot toward integrated brain monitoring.

Key Report Takeaways

- By product, incubators held the lead with 32.14% of neonatal infant care equipment market share in 2025, whereas respiratory support devices are projected to expand at an 8.43% CAGR through 2031.

- By application, thermoregulation commanded 42.73% of the neonatal infant care equipment market size in 2025; neurological care is expected to advance at a 9.61% CAGR during the same period.

- By portability, stationary systems accounted for 72.63% of the neonatal infant care equipment market share in 2025, while wearable and patch sensors are poised to grow at a 9.52% CAGR to 2031.

- By end-user, hospitals captured 71.11% of spending in 2025; home-care settings represent the fastest lane, forecast to rise at a 9.82% CAGR through 2031.

- By technology, conventional platforms made up 64.42% of 2025 revenue, but smart and connected devices are on track for a 9.91% CAGR over 2026-2031.

- By geography, North America led with 34.51% neonatal infant care equipment market share in 2025, whereas Asia-Pacific is projected to register the highest regional growth at a 7.22% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Neonatal Infant Care Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising pre-term birth incidence | +1.2% | Global, highest in sub-Saharan Africa & South Asia | Long term (≥ 4 years) |

| Increasing NICU bed density in emerging economies | +1.1% | China, India; spill-over to Middle East & Africa, South America | Medium term (2-4 years) |

| Technological advances in integrated incubator-monitor systems | +0.9% | North America & Western Europe lead | Medium term (2-4 years) |

| AI-driven predictive neonatal monitoring adoption | +0.8% | North America, Europe, urban APAC hubs | Short term (≤ 2 years) |

| Growth of home-based neonatal care services | +0.7% | North America, Western Europe, Australia | Medium term (2-4 years) |

| Sustainability-focused equipment-upgrade mandates | +0.5% | European Union & United Kingdom | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Pre-Term Birth Incidence

Preterm births reached 13.4 million in 2020, about 10% of all live births, and the burden skews heavily toward low-resource settings. Infants born between 22 and 28 weeks need simultaneous thermoregulation, ventilation, and continuous monitoring, pushing hospitals to favor integrated systems over standalone devices. WHO’s 2024 guidelines endorse early CPAP and kangaroo mother care, spurring demand for portable warmers and home monitors that allow earlier discharge without safety loss. Falling mortality means a larger cohort of medically complex survivors, extending replacement cycles and widening the neonatal infant care equipment market. The demographic momentum ensures durable demand and underpins long-term investments in smart incubators and wearable sensors.

Increasing NICU Bed Density in Emerging Economies

China grew intensive-care bed density 32%, from 3.60 to 4.75 per 100,000 population between 2015 and 2021, under mandates for Level-III NICUs. India set aside USD 1.2 billion for 500 district-hospital NICUs during 2024-2026, though tender delays and a shortage of biomedical engineers slow fulfillment. Brazil’s SUS operates 2,200 neonatal ICU beds but funds telemedicine-linked transport incubators to bridge regional gaps.[3]Ana Paula da Silva, “Neonatal Intensive Care Infrastructure in Brazil’s Unified Health System,” Revista de Saúde Pública, ncbi.nlm.nih.gov These expansions unleash near-term procurement spikes yet reward vendors that pair hardware with remote diagnostics, because staffing lags behind bed growth.

Technological Advances in Integrated Incubator-Monitor Systems

GE HealthCare’s Giraffe Carestation logs temperature and SpO₂ events directly into hospital EMRs, cutting nurse documentation by 20 minutes per shift. Philips IntelliVue now speaks HL7-FHIR, easing interoperability bids. Dräger’s Isolette 8000 Plus uses closed-loop humidity control that lowers hypernatremia risk and shortens NICU stays by three days. Hospitals justify a 15-25% premium for connected platforms with lower adverse-event rates and reduced nurse turnover, tilting future procurement toward sensor-rich systems.

AI-Driven Predictive Neonatal Monitoring Adoption

Ceribell’s FDA-cleared headband spots seizures within two minutes, empowering bedside intervention without a neurophysiologist. A 2024 JAMA Pediatrics review showed AI sepsis models reach 75-85% sensitivity at >90% specificity. Masimo’s Root consolidates multiple waveforms into a single deterioration score that eases night-shift workloads. Pending CMS reimbursement for AI-assisted monitoring may accelerate adoption beyond academic centers into community hospitals.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High up-front cost of neonatal intensive care equipment | -0.6% | Emerging markets in APAC, Africa, South America | Medium term (2-4 years) |

| Shortage of trained neonatal care specialists | -0.5% | Global; most severe in low-resource areas | Long term (≥ 4 years) |

| Proliferation of low-cost refurbished devices | -0.4% | India, Southeast Asia, East Africa | Short term (≤ 2 years) |

| Semiconductor-sensor supply-chain volatility | -0.3% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Up-Front Cost of Neonatal Intensive Care Equipment

A fully equipped Level-III NICU bed costs USD 75,000-120,000—above many district hospitals’ annual budgets. India caps single-device buys at INR 5 million (≈ USD 60,000), forcing trade-offs between one integrated incubator and multiple basic warmers. GE HealthCare’s equipment-as-a-service leasing in Kenya shifts CapEx to OpEx, but requires creditworthy payers. Financial barriers slow premium adoption, bifurcating the neonatal infant care equipment market between urban referral centers and peripheral clinics.

Shortage of Trained Neonatal Care Specialists

WHO cites a global shortfall of 900,000 neonatal nurses, with some African nations below two per 1,000 live births. A 2024 Lancet Global Health study found 30% of ventilators idle in rural India for lack of skilled staff. Training costs USD 3,000-8,000 per nurse and faces attrition as workers migrate. Automation helps—Fisher & Paykel’s Optiflow Junior self-adjusts FiO₂—but cannot fully replace clinical judgment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Respiratory Devices Outpace Incubators as Ventilator Supply Chains Mature

Incubators supplied 32.14% of 2025 revenue but respiratory support devices are racing ahead at 8.43% CAGR, fueled by pandemic-era ventilator capacity that now targets neonates. Closed-box incubators dominate for humidity control, whereas radiant warmers excel in delivery rooms. LED phototherapy displaces halogen bulbs, cutting heat generation 40% and extending lamp life to 50,000 hours. CPAP and high-flow nasal cannula curb bronchopulmonary dysplasia, trimming lifetime costs near USD 500,000 per case. Consumables—tubing, sensors, eye shields—deliver 15% of sales and anchor razor-blade revenue models, reinforcing vendor lock-in.

Multiparameter monitors and pulse oximeters thrive under mandates for continuous SpO₂ tracking. Masimo’s low-perfusion sensor drove USD 280 million neonatal sales in 2025 MASIMO.COM. Capnographs shift to mainstream designs for <1,000 g infants. Fiber-optic phototherapy pads enable treatment during kangaroo care, aligning with WHO family-centered guidelines WHO.INT. Conductive gel warmers emerge for quiet home use, while stationary radiant heaters remain the hospital standard.

By Application: Neurological Care Surges as Seizure-Detection AI Gains Traction

Thermoregulation kept a 42.73% lead in 2025, yet neurological care grows 9.61% annually, the top gain among applications, following Ceribell’s seizure-detection clearance. Respiratory support represented 28%, buoyed by evidence that early non-invasive ventilation cuts intubation days. Jaundice management held 18%, with LED arrays tuned to bilirubin’s 460 nm absorption peak.

Routine EEG screening for very-preterm infants becomes standard in high-income NICUs; Masimo’s processed-EEG index embeds into its Root dashboard. Thermoregulation remains volume-heavy but low-margin, whereas neurological modules command premiums due to algorithm complexity and few competitors.

By Portability: Wearable Sensors Climb as Payers Fund Home Phototherapy

Stationary systems captured 72.63% of neonatal infant care equipment market size in 2025, reflecting intensive infrastructure needs. Wearable and patch sensors grow 9.52%, enabling early discharge that saves USD 8,000-12,000 per episode. Transport incubators fetch USD 25,000-40,000 and serve rural transfers.

Masimo’s Radius PPG wearable transmits vitals via Bluetooth, letting one nurse supervise six infants. Home phototherapy rentals cost USD 150-300 per week, far below a USD 2,000-3,000 hospital stay, prompting insurer coverage. By 2031, a meaningful portion of post-discharge monitoring should happen at home, rewarding cloud-ready vendors.

By End-User: Home-Care Settings Expand as Reimbursement Rewards Early Discharge

Hospitals held 71.11% outlays in 2025, but equipment fleets are aging; 40% of U.S. NICU incubators exceed 10 years in service. Specialty clinics occupy 20% as step-down units. Home-care, only 9% in 2025, is rising at 9.82% CAGR, following CMS proposals to reimburse remote jaundice and apnea monitoring.

Ceribell piloted its headband in six neurology clinics before FDA clearance, illustrating how specialty centers seed adoption. Parental-facing apps from Philips and Masimo provide setup guidance and route alarms to on-call nurses, bridging the skills gap.

By Technology: Smart Devices Gain as Interoperability Standards Mature

Conventional platforms retained 64.42% revenue in 2025, but smart devices rise 9.91% yearly, meeting EMR-integration mandates. GE HealthCare’s Mural pulls incubator, ventilator, and monitor data into one mobile view, cutting clinician footsteps and infection risk. Philips PerformanceBridge predicts component failures weeks ahead, slicing downtime 30%. Dräger’s SmartPilot View flags airway obstruction in under five minutes. Replacement cycles now favor connected products, as hospitals retiring 2015-era gear opt for devices with predictive-maintenance features.

Geography Analysis

North America took 34.51% revenue in 2025 due to 4 Level-III beds per 10,000 births and rapid AI adoption; 18 children’s hospitals installed Ceribell’s system within a year of clearance. Canada invests in tele-transport incubators for remote Indigenous areas, while Mexico earmarked MXN 2.5 billion in 2025 for NICU capacity gains. Reimbursement shifts toward bundled payments encourage earlier discharge and home monitoring.

In Europe, Germany, France, and the U.K. push energy-efficient equipment under the EU Medical Device Regulation’s green clauses. Italy and Spain replace aging fleets, while Poland and Romania tap EUR 800 million in Cohesion Funds for NICU builds.

Asia-Pacific grows fastest at 7.22% CAGR. China’s 14th Five-Year Plan devotes CNY 50 billion to maternal-child health, adding 1,200 NICUs. India funds 500 district units but faces staffing bottlenecks. Japan’s low birth rate limits volume yet favors premium smart devices; Nihon Kohden captured 35% of NICU monitor sales in 2025. Australia and South Korea pilot home-monitoring reimbursement. Southeast Asia leans on multilateral loans, often electing refurbished gear.

In the Middle East & Africa, Gulf states build high-spec facilities like Riyadh’s 60-bed NICU equipped with Giraffe incubators. Sub-Saharan Africa’s incubator penetration remains under 20% of hospitals; South Africa’s pay-per-use lease for 500 units offers a replicable model. South America accounted for 6%; Brazil bought 1,200 ventilators and 800 transport incubators in 2025, while Argentina invested USD 80 million in smart replacements.

Competitive Landscape

Key players include GE HealthCare, Philips, Drägerwerk, and Medtronic; there is also space for regional challengers. Competitive thrusts center on unified platforms, AI decision support, and bundled financing that lowers total cost. Chinese firm Mindray undercuts prices by up to 40%, while refurbished gear floods price-sensitive markets. White-space remains in home monitoring and neurological care, where Ceribell validated EEG AI but no full-suite vendor exists.

Software locks customers; GE’s Mural and Philips’ PerformanceBridge sell data subscriptions alongside hardware. Masimo purchased a neonatal-monitoring start-up in 2024 to cross-sell pulse-ox, capnography, and brain indices. EU MDR and FDA cybersecurity rules raise compliance hurdles, favoring incumbents with deep regulatory teams. Specialized cyber-vendors now partner with device makers to harden connected incubators.

Neonatal Infant Care Equipment Industry Leaders

GE HealthCare

Drägerwerk AG & Co. KGaA

Atom Medical Corporation

Medtronic plc

Koninklijke Philips N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Government hospitals in one Indian state procured radiant warmers, LED phototherapy units, and slit lamps to strengthen first-week survival rates.

- February 2026: Bracco secured FDA approval to extend Vueway (gadopiclenol) MRI contrast use to neonates, halving gadolinium dose requirements.

- January 2026: mOm Incubators gained FDA 510(k) clearance for its Essential portable incubator, enabling mother-baby proximity across diverse care settings.

Global Neonatal Infant Care Equipment Market Report Scope

Neonatal Infant Care Equipment refers to medical devices designed to support, monitor, and treat newborns, particularly premature or critically ill infants, in the Neonatal Intensive Care Unit (NICU).

The Neonatal Infant Care Equipment Market Report is segmented by Product, Application, Portability, End User, Technology, and Geography. By Product, the market is segmented into Incubators, Infant Warmers, Phototherapy Equipment, Respiratory Support Devices, Neonatal Monitoring Devices, and Consumables & Accessories. By Application, the market is segmented into Thermoregulation, Respiratory Support, Jaundice Management, Patient Monitoring, Neurological Care, and Others. By Portability, the market is segmented into Stationary Systems, Portable/Transport Incubators, and Wearable/Patch Sensors. By End User, the market is segmented into Hospitals, Specialty/Neonatal Clinics, and Home‑care Settings. By Technology, the market is segmented into Conventional Devices and Smart/Connected Devices. By Geography, the market is segmented into North America, Europe, Asia‑Pacific, Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. Market Forecasts are Provided in Terms of Value (USD).

| Incubators | Closed Box Incubators |

| Open-box Incubators | |

| Infant Warmers | Radiant Warmers |

| Conductive Warmers | |

| Phototherapy Equipment | LED Phototherapy |

| Fiber-optic Phototherapy | |

| Respiratory Support Devices | Neonatal Ventilators |

| CPAP Systems | |

| High-Flow Nasal Cannula (HFNC) | |

| Neonatal Monitoring Devices | Multiparameter Patient Monitors |

| Pulse-Oximeters | |

| Capnographs | |

| Consumables & Accessories |

| Thermoregulation |

| Respiratory Support |

| Jaundice Management |

| Patient Monitoring |

| Neurological Care |

| Others |

| Stationary Systems |

| Portable / Transport Incubators |

| Wearable / Patch Sensors |

| Hospitals |

| Specialty/Neonatal Clinics |

| Home-care Settings |

| Conventional Devices |

| Smart / Connected Devices |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Incubators | Closed Box Incubators |

| Open-box Incubators | ||

| Infant Warmers | Radiant Warmers | |

| Conductive Warmers | ||

| Phototherapy Equipment | LED Phototherapy | |

| Fiber-optic Phototherapy | ||

| Respiratory Support Devices | Neonatal Ventilators | |

| CPAP Systems | ||

| High-Flow Nasal Cannula (HFNC) | ||

| Neonatal Monitoring Devices | Multiparameter Patient Monitors | |

| Pulse-Oximeters | ||

| Capnographs | ||

| Consumables & Accessories | ||

| By Application | Thermoregulation | |

| Respiratory Support | ||

| Jaundice Management | ||

| Patient Monitoring | ||

| Neurological Care | ||

| Others | ||

| By Portability | Stationary Systems | |

| Portable / Transport Incubators | ||

| Wearable / Patch Sensors | ||

| By End-User | Hospitals | |

| Specialty/Neonatal Clinics | ||

| Home-care Settings | ||

| By Technology | Conventional Devices | |

| Smart / Connected Devices | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How fast is the neonatal infant care equipment market projected to grow to 2031?

It is set to rise from USD 3.39 billion in 2026 to USD 4.51 billion by 2031 at a 5.87% CAGR.

Which product segment is expanding the quickest?

Respiratory support devices show the highest growth at 8.43% CAGR, outpacing incubators.

Why is neurological care gaining momentum?

FDA-cleared AI tools like Ceribell’s headband enable rapid seizure detection, lifting neurological-care demand at 9.61% CAGR.

What fuels adoption of wearable neonatal sensors?

Early discharge programs and payer coverage for home phototherapy drive 9.52% CAGR growth in wearable and patch sensors.

Which region offers the strongest growth outlook?

Asia-Pacific leads with a 7.22% forecast CAGR, backed by government NICU mandates in China and India.

Page last updated on: