Neonatal And Prenatal Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

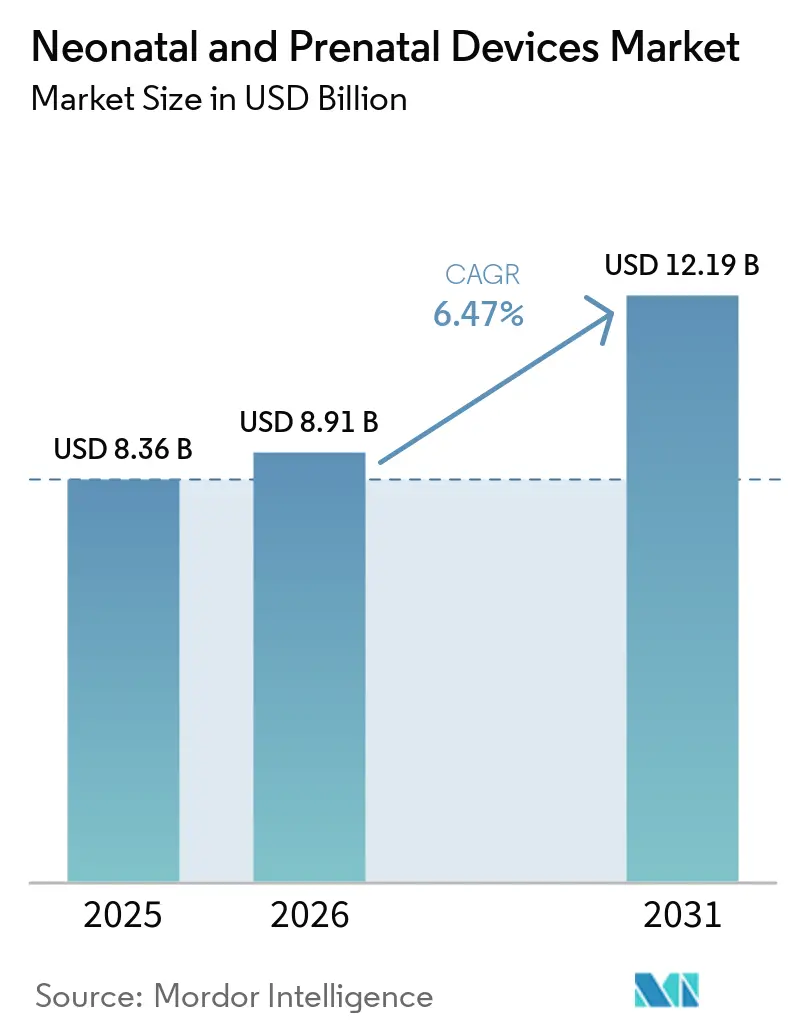

| Market Size (2026) | USD 8.91 Billion |

| Market Size (2031) | USD 12.19 Billion |

| Growth Rate (2026 - 2031) | 6.47% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Neonatal And Prenatal Devices Market Analysis by Mordor Intelligence

The Neonatal And Prenatal Devices Market size is projected to expand from USD 8.36 billion in 2025 and USD 8.91 billion in 2026 to USD 12.19 billion by 2031, registering a CAGR of 6.47% between 2026 to 2031.

Demand resilience comes from rising care complexity rather than expanding birth volumes, as United States preterm birth rates hold at 10.4% while neonatal mortality before day 28 has fallen 43%. Increasing adoption of AI-enabled ultrasound, portable incubators, and remote monitoring widens treatment access and lowers costs at a time when hospitals weigh capacity investments against reimbursement uncertainty. Competitive activity accelerates as leading brands partner with software companies to defend share and as low-cost innovators pursue underserved rural and emerging-market segments. Reimbursement reforms supporting distributed care finally give commercial traction to home-based neonatal monitoring, reshaping the neonatal and prenatal devices market growth trajectory.

Key Report Takeaways

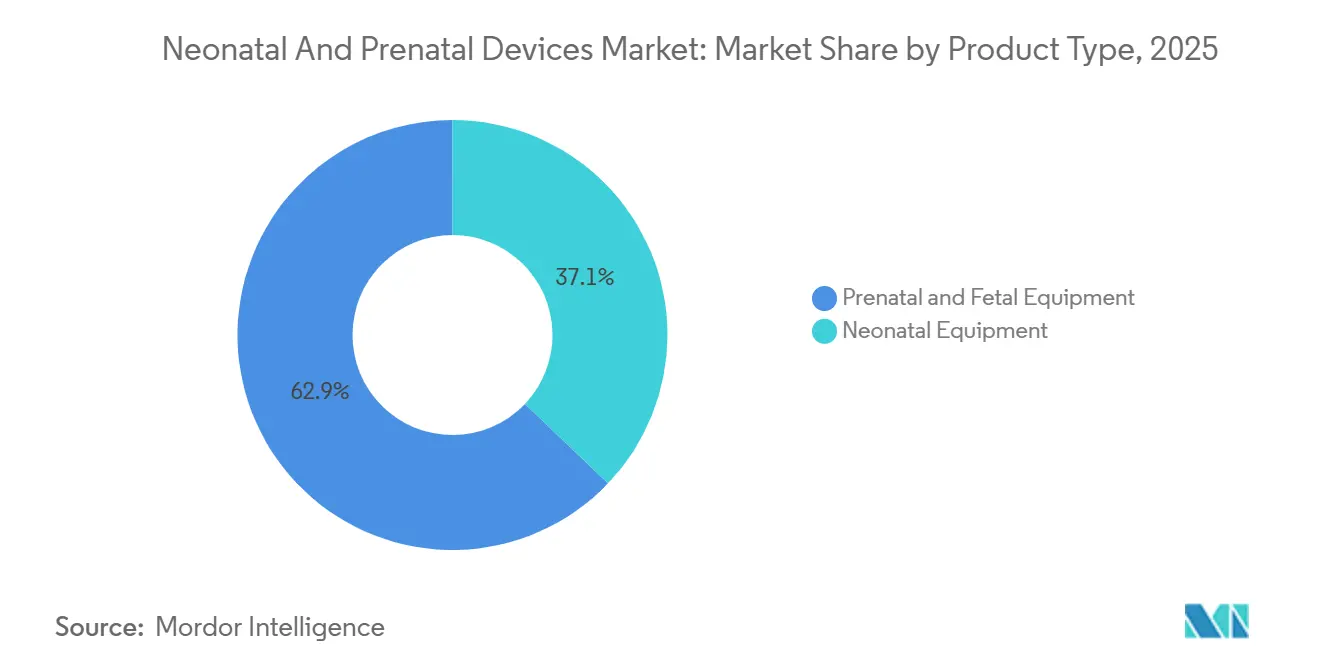

- By product type, prenatal and fetal equipment led with 62.88% revenue share in 2025; neonatal equipment is projected to expand at a 9.53% CAGR to 2031.

- By technology, non-invasive monitoring commanded 51.68% of the neonatal and prenatal devices market size in 2025 and is advancing at a 7.46% CAGR through 2031.

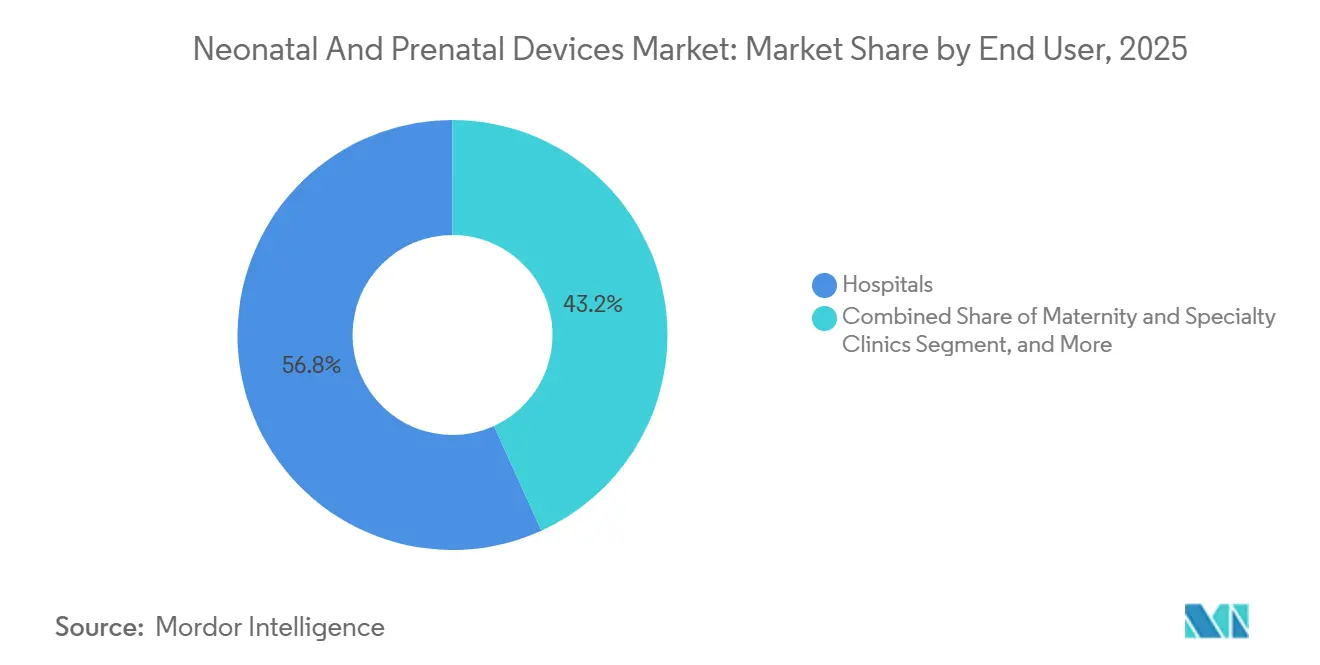

- By end user, hospitals held 56.79% of the neonatal and prenatal devices market share in 2025, while home and remote care settings record the fastest projected CAGR at 8.43% through 2031.

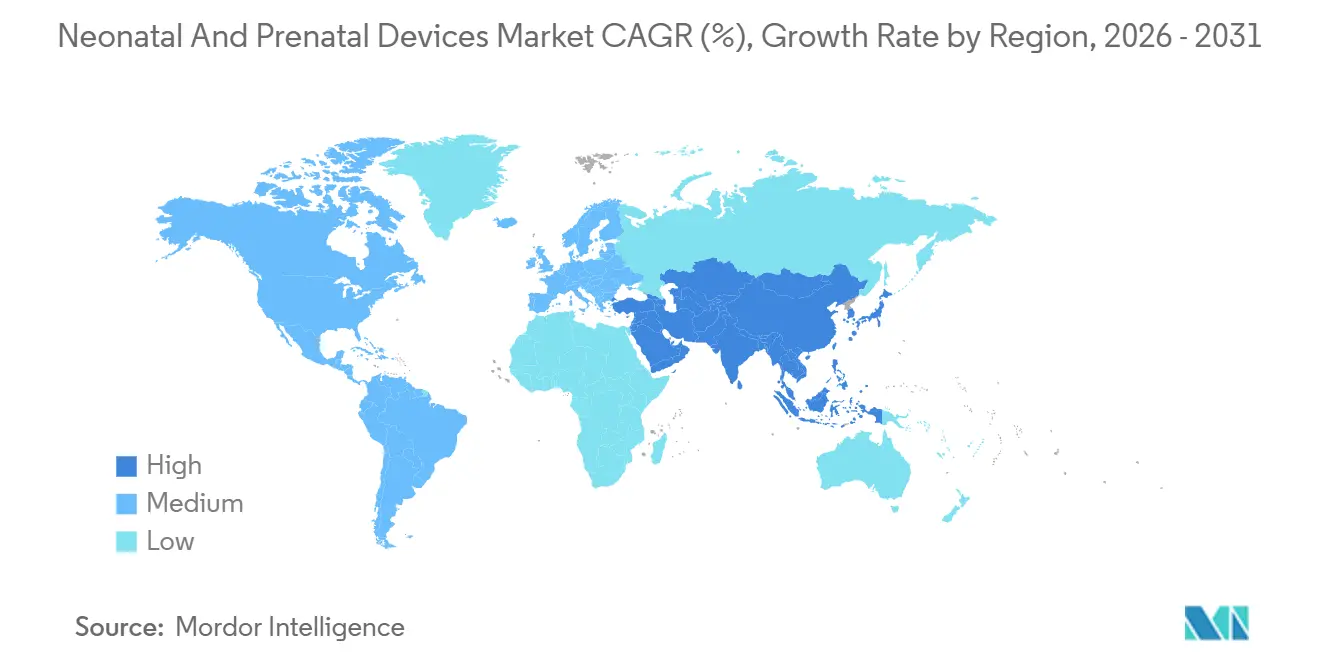

- By geography, North America represented 36.88% of 2025 revenue, but Asia-Pacific is forecast to post the highest regional CAGR of 8.84% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Neonatal And Prenatal Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Incidence of Preterm Births | +1.2% | Global, with highest impact in North America and Sub-Saharan Africa | Medium term (2-4 years) |

| Growth In High-Risk Pregnancy & Prenatal Screening Volumes | +0.8% | Developed economies, expanding to emerging markets | Short term (≤ 2 years) |

| Expansion of NICU Capacity in Emerging Markets | +1.5% | APAC core, spill-over to MEA and Latin America | Long term (≥ 4 years) |

| Government-Supported Universal Fetal Monitoring Programs | +0.9% | EU and select APAC countries | Medium term (2-4 years) |

| AI-Enabled Remote Neonatal Monitoring Adoption in Home Settings | +1.1% | North America and EU, early adoption in urban APAC | Short term (≤ 2 years) |

| Development of Low-Cost Portable Incubators for Off-Grid Clinics | +0.7% | Sub-Saharan Africa, rural India, and Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Preterm Births

Persistently high preterm delivery rates keep the neonatal and prenatal devices market under structural demand pressure. United States data show 373,902 preterm births in 2023, and rates remain highest among Black infants at 14.7% and American Indian or Alaska Native infants at 12.4%. Multiple pregnancies, which are seven times more likely to be preterm than singleton pregnancies, amplify equipment needs as fertility treatments rise. Hospitals, therefore, accelerate investment in advanced incubators, ventilators, and predictive analytics that can flag sepsis or necrotizing enterocolitis earlier than manual observation. Together, these factors translate into steady volume for life-support devices even as overall birth totals plateau in developed economies.

Growth in High-Risk Pregnancy & Prenatal Screening Volumes

Maternal age is rising in most high-income nations, lifting the proportion of pregnancies classified as high-risk and fueling demand for sophisticated prenatal imaging. Women aged 40 and older experienced 14.6% preterm birth rates in 2023, well above the national average. AI-based ultrasound now detects 95% of neural tube defects, while machine-learning classification algorithms reach 71.5% diagnostic accuracy in test datasets.[1]Frontiers in Pediatrics, “Machine Learning in Neonatal Imaging,” frontiersin.org Clinical uptake accelerates because remote ultrasound reviews allow specialists to serve community clinics, closing the gap created by the fall in first-trimester prenatal care coverage to 76.1% in 2023. Wearable maternal monitors combine heart-rate, blood-oxygen, and activity sensors to manage smoking and gestational diabetes risks in real time. Digital care pathways reduce unnecessary in-person visits without compromising outcomes, lowering system costs, and encouraging payer reimbursement for connected prenatal devices.

Expansion of NICU Capacity in Emerging Markets

Asia-Pacific governments continue multi-year investment programs to expand neonatal intensive care capacity. China’s CARE-Preterm cohort now tracks more than 10,000 very preterm infants treated across 60 NICUs, signaling large-scale training and technology adoption. Staffing levels at Chinese maternal and child health institutions are climbing each year, with favorable projections through 2026. Local manufacturers also scale exports to Europe and the United States, reshaping competitive dynamics and keeping price pressure on legacy multinationals. These moves, together with infrastructure spending in India, Indonesia, and Vietnam, underpin the fastest regional growth outlook for the neonatal and prenatal devices market.

AI-Enabled Remote Neonatal Monitoring Adoption in Home Settings

Early discharge programs for infants with feeding difficulties now bundle FDA-cleared remote monitoring kits that track weight trends, respiration, and oxygen saturation from home, reducing average length of stay by two days per patient.[2]Nature, “Remote Monitoring Cuts NICU Stay,” nature.com The SNOO Smart Sleeper became the first device authorized to maintain infant supine sleep position, holding babies in safe alignment 98.7% of monitored time in trials.[3]Happiest Baby, “SNOO Smart Sleeper Clinical Data,” happiestbaby.com Masimo donated USD 100,000 worth of Stork Smart Home Baby Monitoring Systems to March of Dimes to support hospital-to-home transitions, and each system connects seamlessly with the company’s SET pulse-oximetry algorithms. Epidermal electronic sensors now adhere without tape and transmit continuous heart-rate and temperature data, reducing skin injury risk and improving parental confidence. Field tests in rural Guatemala show smartphone-based decision support powered by edge AI can guide midwives through fetal assessments despite limited broadband access.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Declining Birth Rates in Developed Economies | -1.8% | North America, EU, developed APAC countries | Long term (≥ 4 years) |

| High Capital Cost & Reimbursement Hurdles | -1.1% | Global, with acute impact in emerging markets | Medium term (2-4 years) |

| Limited Skilled Neonatal Care Staff in Rural Hospitals | -0.9% | Rural areas globally, concentrated in North America and Sub-Saharan Africa | Medium term (2-4 years) |

| Supply-Chain Disruptions for Critical Electronic Components | -0.7% | Global, with highest impact in import-dependent regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Declining Birth Rates in Developed Economies

Global fertility is projected to slide to 1.83 by 2050 and 1.59 by 2010, well below the replacement rate, cutting the underlying volume addressable by the neonatal and prenatal devices market in the wealthiest countries. The United States reported a 2% birth decline and 3% drop in the general fertility rate during 2023. Maternity unit closures compound access problems; more than 200 rural hospitals shut labor-and-delivery services, leaving 2.3 million women in “maternity care deserts”. Socioeconomic factors—delayed marriage, higher education, and childcare expenses—continue to suppress birth numbers, and policy incentives have shown only modest success in France, South Korea, and Singapore. Lower absolute births mean suppliers must pivot toward higher acuity equipment and ancillary home monitoring services to sustain revenue growth in developed regions.

High Capital Cost & Reimbursement Hurdles

Device makers face long regulatory timelines and opaque payment rules that slow adoption, which shaves 1.1 percentage points from baseline CAGR. The United States medical device market demands separate coding and coverage determinations beyond FDA clearance, extending payback periods for new neonatal solutions. Over 25% of rural hospitals operated at a loss in FY 2022, and many eliminated obstetric services because reimbursements cannot offset round-the-clock staffing needs. COVID-19 exposed fragile electronics supply chains, and continuing chip shortages elevate capital expense for monitors and imaging platforms. FDA user fees for 2025 add further cost, although discounts for small businesses partially mitigate the burden. Collectively, these pressures push providers toward rental, subscription, and pay-per-scan models, changing how the neonatal and prenatal devices market monetizes technology.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Neonatal Equipment Outpaces Prenatal Growth

Neonatal equipment revenue is expected to rise at a 9.53% CAGR through 2031, outstripping the prenatal and fetal category, even though prenatal devices held 62.88% of the neonatal and prenatal devices market in 2025. The neonatal and prenatal devices market size tied to incubators grows fastest because hospitals upgrade to portable, battery-powered units that cost a fraction of traditional models yet meet ISO temperature stability standards. Low-resource facilities in Bangladesh confront a 20,000-unit gap, and compact systems priced around GBP 250 reduce procurement barriers and stimulate government tenders. Phototherapy systems adopt longer-lasting LEDs that cut power consumption 60%, encouraging adoption in off-grid clinics. Ventilation platforms integrate predictive algorithms that flag respiratory distress minutes earlier than conventional alarms, which helps caregivers intervene before oxygen saturation drops to critical thresholds.

Prenatal and fetal equipment, while still the most significant contributor to the neonatal and prenatal devices market revenue, advances at a slower pace because penetration is already high among tertiary care centers. AI-enhanced ultrasound, typified by GE HealthCare’s Voluson Signature line, reduces scan-to-report time by up to 40% without compromising diagnostic accuracy. Fetal MRI expands its role in central-nervous-system anomaly detection when ultrasound findings are inconclusive, creating a smaller but higher value subsegment. Remote fetal pulse oximeters link to telehealth portals so that obstetricians can watch high-risk pregnancies from afar, which is valuable in regions where 2.3% of mothers receive no prenatal care. However, market maturity and tightening hospital budgets temper growth relative to neonatology-focused devices, driving suppliers to focus R&D resources on postnatal applications.

By Technology: Non-Invasive Monitoring Dominates Through Innovation

Non-invasive platforms accounted for 51.68% of neonatal and prenatal devices market revenue in 2025 and are projected to grow 7.46% annually, reflecting payer and clinician preference for lower infection risk solutions. Camera-based photoplethysmography measures pulse wave velocity without skin contact, while radar sensors monitor respiration through blankets, preventing electrode-related skin trauma in very-low-birth-weight infants. Finnish maternity wards documented a 41% drop in neonatal encephalopathy after introducing synchronized maternal pulse and fetal heart-rate evaluation, underlining safety gains that support reimbursement. Near-infrared brain spectroscopy migrated from research to bedside after Class II FDA classification enabled streamlined clearance pathways, expanding real-time cerebral oxygen monitoring.

Invasive technologies remain crucial for the sickest neonates who need arterial blood-gas measurement, yet growth lags due to infection-control protocols and nurse workload. Hybrid systems that switch between non-invasive and invasive modes according to acuity allow clinicians to minimize catheter dwell time, marrying safety with data depth. Wireless modules simplify line management and cut alarm fatigue because AI algorithms adjust alert thresholds based on patient trend data. These developments reinforce the structural shift toward intelligent monitoring rather than siloed device categories, an evolution that will define premium value in the neonatal and prenatal devices industry.

By End User: Home Care Disrupts Hospital Dominance

Hospitals still represented 56.79% of 2025 global sales, but home and remote care settings show the strongest forward momentum at 8.43% CAGR, confirming a gradual decentralization of the neonatal and prenatal devices market. Clinical programs using connected scales, sleep pods, and pulse oximeters shortened average NICU length of stay by two days, saving USD 4,500 per infant episode on ward costs. The Stork platform from Masimo, which leverages hospital-grade SET algorithms, demonstrates how consumer-grade packaging can deliver medical-grade performance when FDA clearance is built.

Maternity clinics and outpatient centers deploy portable ultrasound consoles that weigh less than 6 kg and stream images to cloud PACS for specialist review, reducing patient travel and freeing hospital radiology slots. Ambulatory surgical centers broaden their scope to include neonatal procedures such as patent ductus arteriosus closure using miniaturized catheters that allow same-day discharge. Government toolkits, such as the United States HHS Newborn Supply Kit, show policymakers backing distributed care by providing essentials directly to families. This approach achieved 97% satisfaction and eased postpartum anxiety. As payers finalize remote-monitoring reimbursement frameworks, suppliers will shift marketing dollars toward the home channel, especially in countries with capitated payment systems that favor lower total-care costs.

Geography Analysis

North America commanded 36.88% of global revenue in 2025, anchored by large NICU footprints, robust private insurance coverage, and a regulatory environment that favors continuous innovation. Yet structural headwinds arise from a 2% annual birth decline, and more than 200 rural hospitals have shuttered labor wards, restricting access outside metro centers. Canada’s single-payer model continues to buy premium equipment, but constrained budgets lengthen replacement cycles. Mexico’s social-security hospitals adopt mid-range monitors as they balance cost and rising acuity.

Asia-Pacific is projected to expand at a 8.84% CAGR through 2031, making it the fastest-growing region within the neonatal and prenatal devices market. China alone commits billions of renminbi to neonatal infrastructure, while India’s production-linked incentive scheme shifts device assembly onshore, lowering landed costs. Japanese and South Korean hospitals pursue AI imaging to manage aging clinical workforces, ensuring that premium segments continue to grow despite stagnant birth volumes. Southeast Asian nations, including Indonesia and Vietnam, open new maternal-child hospitals under public-private-partnership models, importing mid-tier incubators and monitors that balance feature sets with price.

Europe advances at a steadier clip as Medical Device Regulation deadlines prioritize compliance spending over green-field expansion, though unified rules simplify pan-EU launches for AI-driven software. Middle East and Africa, along with South America, remain nascent but strategically important because mobile-first infrastructure enables leapfrogging to cloud-connected devices without the legacy cost of wired networks. Portable incubators and solar-powered monitors see highest traction in these geographies, validating the global relevance of frugal innovation.

Competitive Landscape

The market studied is a consolidated market, owing to the presence of various small and large market players. Incumbent suppliers retain moderate control, yielding a neonatal and prenatal devices market concentration best described as balanced between scale leaders and a wide field of specialists. GE HealthCare deploys a multi-pronged strategy that combines inorganic growth, such as the USD 51 million Intelligent Ultrasound acquisition, with cloud partnerships using AWS generative-AI services to automate image interpretation. Masimo, with 2024 healthcare revenue of USD 1.39 billion, extends its strong neonatal pulse-oximetry franchise into the home segment and aligns with advocacy groups like March of Dimes to reinforce clinical credibility. Philips, Samsung Medison, and Getinge integrate AI modules into existing hardware to lock in customer ecosystems, as seen in Getinge’s FDA 510(k) win for the Talis clinical decision-support platform.

Start-ups pursue unmet needs through targeted inventions. Novocuff raised USD 26 million to develop a device that mechanically supports the cervix to prevent preterm birth, addressing an intervention gap in pregnancies under 30 weeks’ gestation. NeoPrediX, backed by Springhood Ventures, applies predictive analytics to newborn vital signs, enabling early detection of hyperbilirubinemia and hypoglycemia. Inventors of the MOM inflatable incubator received global media attention because their GBP 250 design costs 99% less than conventional systems, offering governments a scalable answer to equipment shortages.

Supply-chain risk drives reshoring strategies. United States legislation incentivizes domestic semiconductor fabrication, and several device majors have announced assembly lines in Texas and Arizona to buffer component availability. European players diversify printed-circuit-board sourcing to Poland and the Czech Republic, reducing dependence on Asia. Chinese manufacturers invest in redundant tooling inside coastal and inland provinces to mitigate shipping delays. These capacity adjustments shape bargaining power on both price and delivery schedules, ultimately influencing hospital buying decisions worldwide.

Neonatal And Prenatal Devices Industry Leaders

Atom Medical Corporation

GE Healthcare

Getinge AB

Koninklijke Philips N.V.

Natus Medical Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Shvabe, a holding company within Rostec State Corporation, delivered dozens of critical neonatal and intensive care medical devices to Crimea. The latest supply chain deployment features specialized equipment, including intensive care incubators, phototherapeutic lamps, inhalation anesthesia machines, and respiratory humidifiers.

- May 2025: GE HealthCare partnered with Raydiant Oximetry to advance fetal monitoring technologies, focusing on improving accuracy and effectiveness of prenatal care monitoring devices through enhanced oximetry capabilities.

- March 2025: GE HealthCare and NVIDIA announced collaboration to develop autonomous X-ray and ultrasound technologies, leveraging AI-enabled software to address healthcare staff shortages and automate repetitive imaging tasks in high-volume settings.

- January 2025: GE HealthCare unveiled enhanced Voluson Expert Series ultrasound systems with FDA 510(k) clearance, featuring AI-powered tools including SonoLyst suite for automated measurements and focus on early detection in high-risk pregnancies.

Global Neonatal And Prenatal Devices Market Report Scope

As per the scope of this report, fetal monitoring devices are vital tools that are routinely used in gynecology and obstetrics interventions to examine fetal health during labor and delivery. Neonatal devices are extensively used in the Neonatal Intensive Care Units (NICUs), where complex machines and monitoring devices are designed for the unique needs of tiny babies.

The neonatal and prenatal devices market is segmented by product type, technology, and end user. By product type, the market is segmented into prenatal and fetal equipment and neonatal equipment. By technology, the market is segmented into invasive monitoring and non-invasive monitoring. By end user, the market is segmented into hospitals, maternity & specialty clinics, home & remote care settings, and ambulatory surgical centers. Geographically, the market is segmented across North America, Europe, the Asia-Pacific region, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Prenatal & Fetal Equipment | Ultrasound & Ultrasonography Devices |

| Fetal Doppler | |

| Fetal MRI | |

| Fetal Heart Monitors | |

| Fetal Pulse Oximeters | |

| Other Prenatal & Fetal Equipment | |

| Neonatal Equipment | Incubators |

| Neonatal Monitoring Devices | |

| Phototherapy Equipment | |

| Respiratory Assistance & Monitoring Devices | |

| Other Neonatal Care Equipment |

| Invasive Monitoring |

| Non-Invasive Monitoring |

| Hospitals |

| Maternity & Specialty Clinics |

| Home & Remote Care Settings |

| Ambulatory Surgical Centers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Prenatal & Fetal Equipment | Ultrasound & Ultrasonography Devices |

| Fetal Doppler | ||

| Fetal MRI | ||

| Fetal Heart Monitors | ||

| Fetal Pulse Oximeters | ||

| Other Prenatal & Fetal Equipment | ||

| Neonatal Equipment | Incubators | |

| Neonatal Monitoring Devices | ||

| Phototherapy Equipment | ||

| Respiratory Assistance & Monitoring Devices | ||

| Other Neonatal Care Equipment | ||

| By Technology | Invasive Monitoring | |

| Non-Invasive Monitoring | ||

| By End User | Hospitals | |

| Maternity & Specialty Clinics | ||

| Home & Remote Care Settings | ||

| Ambulatory Surgical Centers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the neonatal and prenatal devices market?

The market was valued at USD 8.91 billion in 2026 and is forecast to reach USD 12.19 billion by 2031.

Which product segment is growing fastest?

Neonatal equipment is expanding at a 9.53% CAGR due to portable incubators and AI-driven respiratory monitors.

How significant is non-invasive monitoring in this market?

Non-invasive platforms held 51.68% of 2025 revenue and are projected to grow 7.46% yearly as hospitals prioritize infection-free data capture.

Why is Asia-Pacific seen as the key growth region?

Large-scale NICU investment in China and India plus supportive manufacturing incentives push the region toward a 8.84% CAGR through 2031.

How are home-based devices impacting market dynamics?

Remote monitoring reduces hospital length of stay and is expected to post the fastest end-user CAGR at 8.43%, shifting revenue toward consumer-facing platforms.

Page last updated on: