Neoantigen Targeted Therapies Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.46 Billion |

| Market Size (2031) | USD 3.73 Billion |

| Growth Rate (2026 - 2031) | 20.48% CAGR |

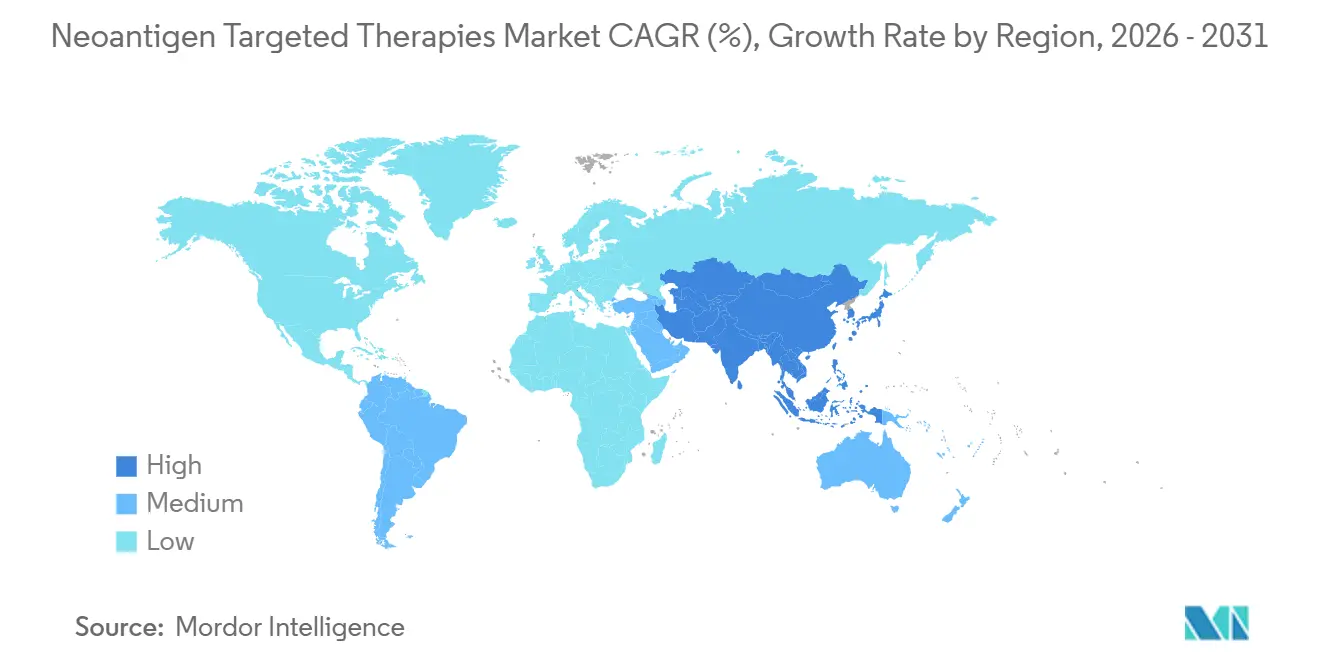

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

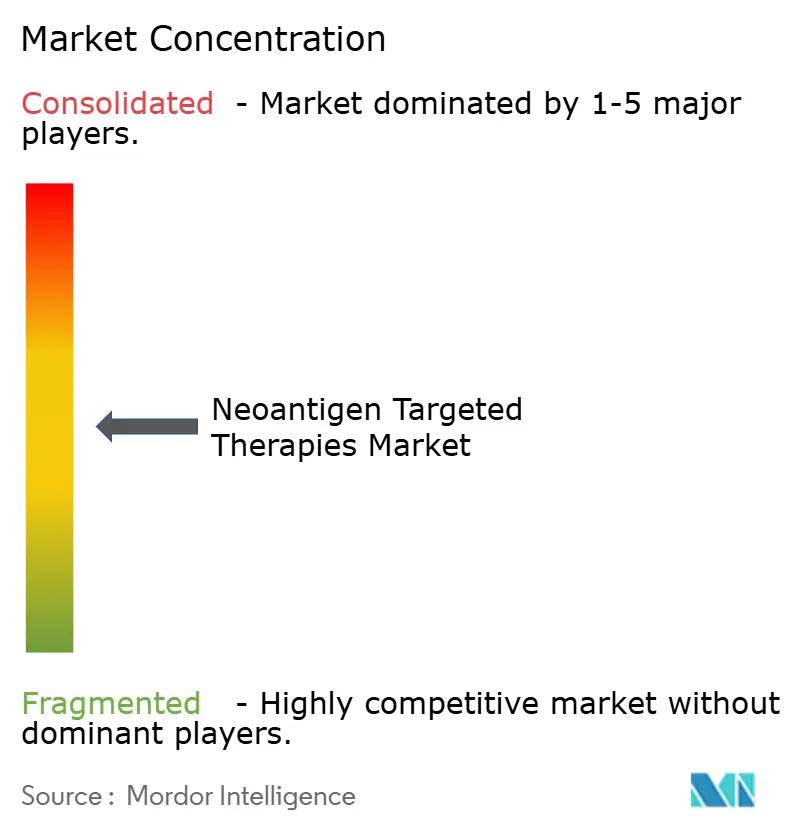

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Neoantigen Targeted Therapies Market Analysis by Mordor Intelligence

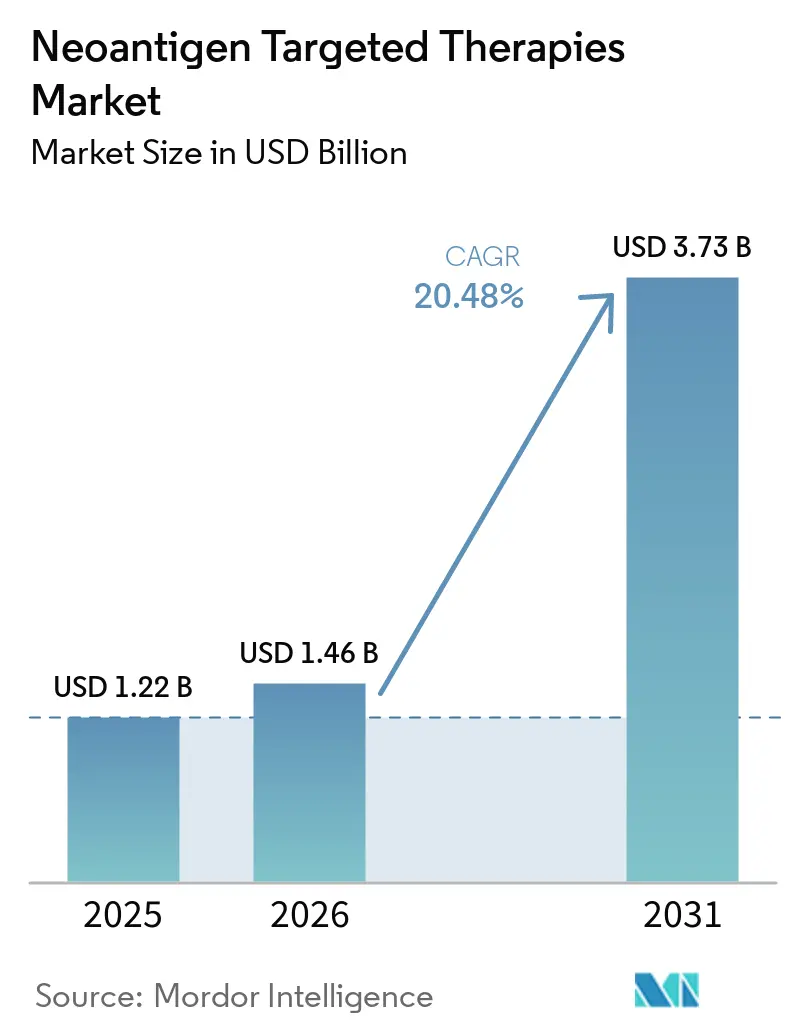

The Neoantigen Targeted Therapies Market size is projected to be USD 1.22 billion in 2025, USD 1.46 billion in 2026, and reach USD 3.73 billion by 2031, growing at a CAGR of 20.48% from 2026 to 2031.

Late-stage clinical evidence in 2026 showing durable reductions in recurrence risk when individualized vaccines are added to PD-1 therapy signals rising clinical conviction across top oncology centers. Improved epitope prediction and validation underpin delivery confidence, with modern HLA-binding algorithms demonstrating strong concordance with experimental assays and RNA sequencing confirming expression for the majority of predicted neoantigens. Minimal residual disease detection using sensitive ctDNA assays is pushing deployment earlier in the patient journey and enabling adjuvant strategies that target relapse risk rather than bulk disease. National programs, such as the NHS Cancer Vaccine Launch Pad, are structuring multi-site pathways that can move personalized vaccines from specialist centers into broader hospital networks.

Key Report Takeaways

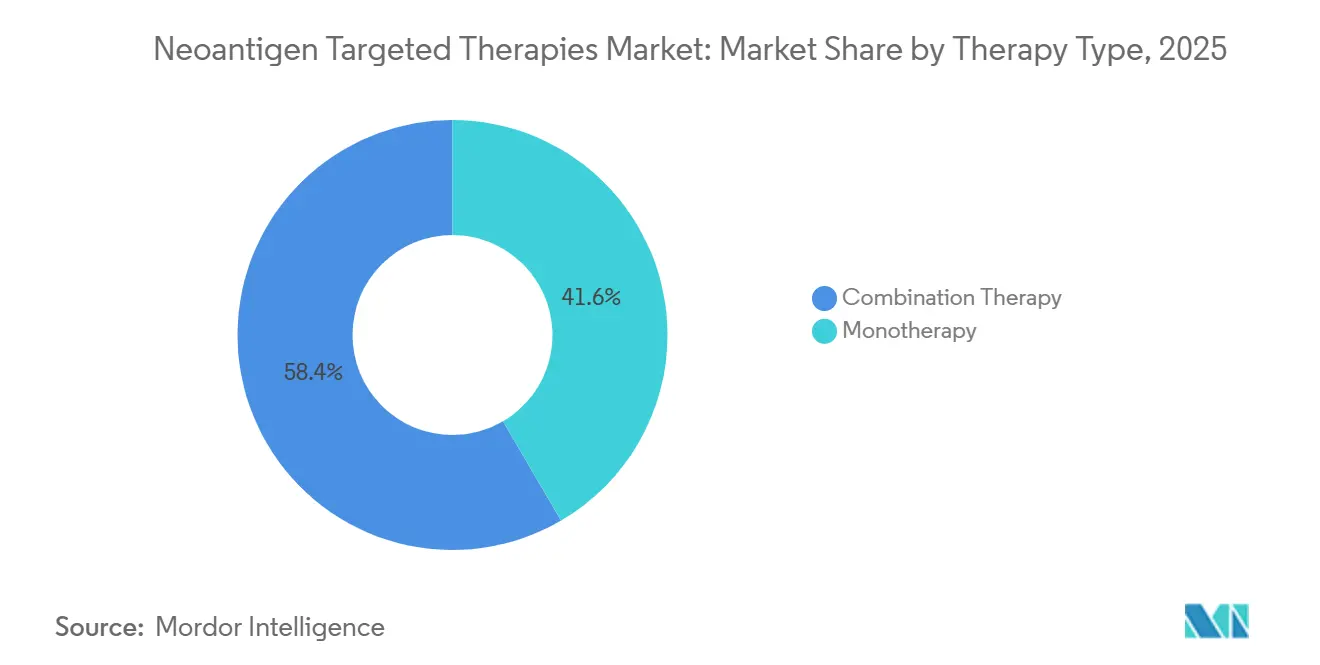

- By therapy type, combination therapy led with 58.42% revenue share in 2025, while monotherapy is projected to post the fastest growth at a 22.56% CAGR through 2031 in the neoantigen targeted therapies market.

- By cancer indication, melanoma accounted for 31.57% of 2025 revenue, and non-small cell lung cancer is forecast to expand at a 23.61% CAGR to 2031.

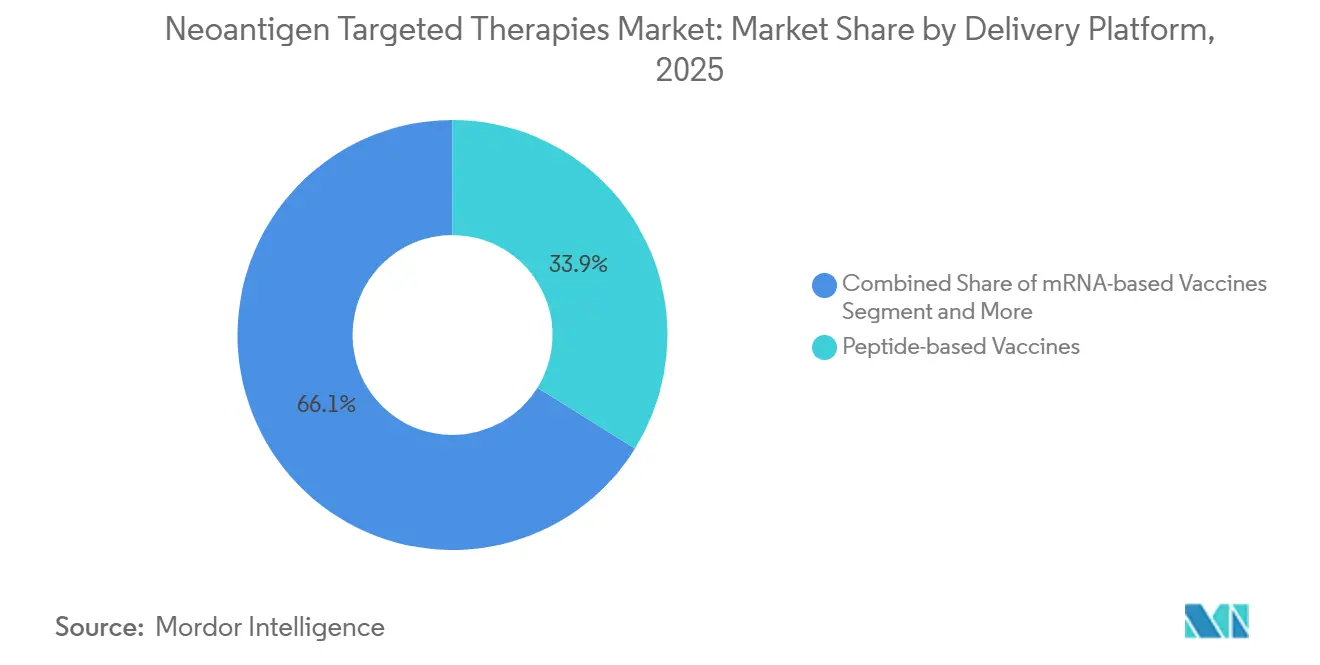

- By delivery platform, peptides held 33.86% of 2025 revenue, and mRNA platforms are expected to grow at a 21.87% CAGR during 2026-2031 in the neoantigen targeted therapies market.

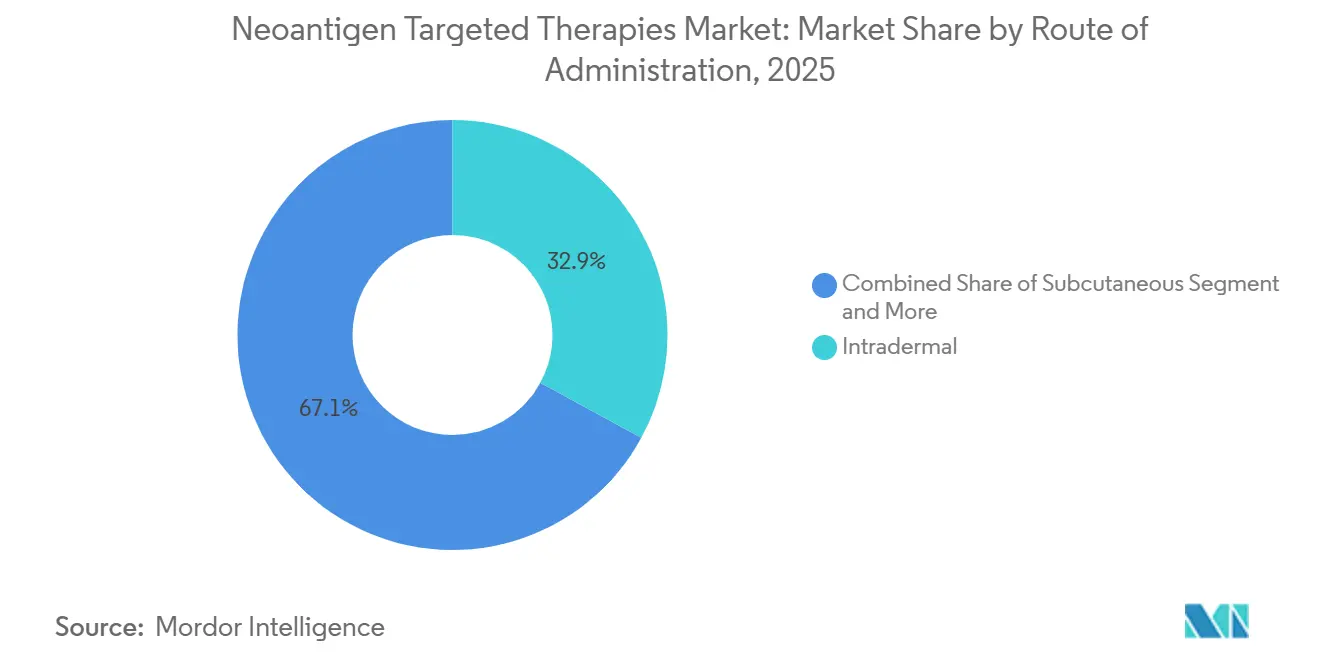

- By route of administration, intradermal injection represented 32.94% of 2025 revenue, with subcutaneous delivery projected to advance at a 23.76% CAGR to 2031.

- By end user, academic and research institutes commanded 42.58% of 2025 revenue, while tertiary care hospitals are set to record a 24.48% CAGR through 2031 in the neoantigen targeted therapies market.

- By geography, North America captured 35.23% of 2025 revenue, and Asia-Pacific is projected to grow the fastest at a 25.72% CAGR to 2031 in the neoantigen targeted therapies market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Neoantigen Targeted Therapies Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Global Cancer Incidence | + 3.2% | Global, acute in Asia-Pacific (51.8% of cases) and aging OECD markets | Short term (≤ 2 years) |

| Advances in High-Throughput Sequencing and Bioinformatics | + 4.5% | North America and EU leading, APAC infrastructure scaling rapidly | Medium term (2-4 years) |

| Positive Late-Stage Clinical Readouts in Personalized Neoantigen Immunotherapies | + 6.8% | North America Phase 3 trials, EU PRIME pathways, Asia early-phase expansion | Medium term (2-4 years) |

| Regulatory and Investor Support for Individualized Oncology | + 2.7% | UK multi-center program, FDA and EMA facilitation pathways | Short term (≤ 2 years) |

| Shift to Adjuvant or MRD-Guided Use Enabled by ctDNA-Based Patient Selection | + 1.9% | OECD markets with mature genomic infrastructure and select Asian hubs | Long term (≥ 4 years) |

| Emergence of Shared Frameshift Neoantigen Products Expanding Treatable Populations | + 1.4% | Global, with early application in Lynch syndrome programs in the US and EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Global Cancer Incidence

Global cancer incidence continues to grow, with Asia bearing a majority of cases and a large share of mortality, which elevates the urgency for new modalities that deliver lasting control.[1]World Health Organization, “GLOBOCAN 2022: Cancer Incidence and Mortality,” World Health Organization Lung, breast, and colorectal cancers accounted for the largest portions of new diagnoses in 2022, and lung and liver cancers have remained leading contributors to cancer mortality, which continues to pull demand toward new adjuvant and maintenance options. Low-dose CT programs are increasing early-stage detection in eligible populations, which widens the clinical window for adjuvant vaccination that targets minimal residual disease rather than bulky tumors. [2]Frontiers Editorial Office, “HLA-Peptide Binding Prediction and Validation,” Frontiers in Immunology Tumors with high mutational burdens like melanoma and smoking-related NSCLC offer richer pools of actionable neoantigens and remain focal points for first-wave commercialization. Pediatric cancers and low-mutational-burden sarcomas yield fewer targets, so current investment is concentrated in adult epithelial malignancies where target density and immune visibility support durable T-cell responses.

Advances in High-Throughput Sequencing and Bioinformatics

Validation of HLA-peptide binding predictions is improving, with modern tools demonstrating high concordance against experimental assays and enabling higher-confidence epitope selection. RNA sequencing corroborates the expression of a large share of predicted neoantigens, which reduces false positives and improves manufacturing utilization by filtering out low-transcript targets.[3]Editors, “Transcript-Level Confirmation of Predicted Neoantigens,” Nature Quality management in bioinformatics has become a regulatory focal point, with U.S. and European guidance pushing for audit trails, version control, and robust validation of machine-learning-based pipelines.[4]Association of Clinical Research Professionals, “Regulatory Expectations for Algorithm Validation,” ACRPThe shift from research-grade pipelines to submission-ready, auditable engines favors sponsors that combine sequencing scale with validated in silico prediction and transcript confirmation to streamline IND dossiers. As platform validation strengthens, the neoantigen-targeted therapies market benefits from shortened design-to-clinic cycles and a higher probability that manufactured batches induce the intended immune response.

Positive Late-Stage Clinical Readouts in Personalized Neoantigen Immunotherapies

Five-year follow-up in resected high-risk melanoma showed a sustained reduction in recurrence or death risk when a personalized mRNA neoantigen vaccine was combined with PD-1 therapy compared with a checkpoint inhibitor alone. Durable T-cell activity aligned with clinical outcomes in these datasets, which supports the premise that primed and persistent CD8+ responses are central to long-term recurrence control in high-risk settings. The durability observed beyond the active vaccination window is shifting clinical focus toward finite adjuvant courses that seek to establish immunologic memory instead of indefinite disease suppression. As confirmatory trials progress across additional tumor types, the neoantigen targeted therapies market is positioned to transition from early-adopter trials into structured post-surgical pathways where endpoints prioritize recurrence-free survival. Broader Phase 2 and Phase 3 programs initiated by leading sponsors in 2026 indicate expanding clinical scope across melanoma, lung, bladder, and renal cancers, which improves visibility into label expansion potential.

Regulatory and Investor Support for Individualized Oncology

The UK’s multi-year collaboration to enroll up to 10,000 patients through the Cancer Vaccine Launch Pad is building a national pathway for screening, selection, and hospital-based delivery, which strengthens logistics for individualized regimens. In parallel, regulatory accelerators from U.S. and EU agencies are streamlining evidence generation through adaptive designs and rolling submissions, especially when sponsors provide validated biomarker frameworks. PRIME and related facilitation mechanisms in Europe continue to prioritize therapies with high potential to address unmet needs, including individualized vaccines in high-risk resected settings. As governance emphasizes traceable bioinformatics and robust assay validation, sponsors with transparent computational pipelines gain an edge in time-to-approval planning for the neoantigen targeted therapies market. The net effect is a clearer regulatory runway that reduces uncertainty around trial sequencing and data sufficiency, encouraging investment in personalization at scale.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Manufacturing Complexity, Turnaround Time, and Cost per Patient | - 4.1% | Global, pronounced where decentralized GMP capacity is limited | Short term (≤ 2 years) |

| Clinical and Logistical Challenges Across Biopsy to Sequencing to Manufacturing Chain | - 2.3% | Low-resource settings and rural catchment areas | Medium term (2-4 years) |

| Uncertain Reimbursement Models for Individualized Therapies | - 3.6% | U.S. commercial payers and fragmented European HTA settings | Medium term (2-4 years) |

| Tumor Heterogeneity and Antigen Escape Limiting Durability | - 1.8% | Universal biological challenge across solid tumors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Manufacturing Complexity, Turnaround Time, and Cost per Patient

Personalized vaccine production requires a series of interdependent steps that include biopsy procurement, tumor-normal sequencing, epitope selection, and GMP manufacturing, which creates schedule pressure and cost sensitivity. Decentralized GMP capacity remains uneven across regions, which slows scale-up and complicates equitable access where courier chains or cold storage infrastructure are limited. Batch-by-batch variability and individualized quality control add layers of testing that do not amortize across large uniform lots, which is unlike conventional vaccine economics. As sponsors streamline bioinformatics selection and standardize release testing, throughput is expected to improve, yet capacity distribution remains a gating factor in near-term regional rollouts. These operational constraints temper near-term adoption curves in the neoantigen targeted therapies market until more hubs, trained personnel, and harmonized protocols expand consistent, timely delivery.

Clinical and Logistical Challenges Across Biopsy–Sequencing–Manufacturing Chain

Candidate identification requires fresh or well-preserved tumor samples with adequate cellularity, which can be challenging in community settings and for certain anatomic sites. Turnaround times must align with surgical recovery and adjuvant therapy windows, so any delay in sample transfer, sequencing, or release testing can miss the optimal immunization window. Coordinating tumor boards, pathology, pharmacy, and infusion scheduling within hospitals requires integrated workflows that many centers are still building, which affects patient throughput. In regions with sparse genomic testing infrastructure, referral pathways add travel and time burdens that can discourage enrollment outside urban centers. Improving logistics within the care pathway remains essential for timely patient selection and vaccine initiation in the neoantigen targeted therapies market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Therapy Type: Combination Gains Command Half-Plus Market on Checkpoint Synergy

Combination therapy accounted for 58.42% of 2025 revenue as clinicians layered neoantigen vaccines with PD-1 or PD-L1 inhibitors to push beyond the response ceilings of checkpoint monotherapy in many solid tumors. Monotherapy is projected to grow fastest at a 22.56% CAGR through 2031, helped by adjuvant use where limited tumor burden and validated biomarkers favor vaccine-led control. The neoantigen targeted therapies market is using combination backbones to lock in clinical benefit while platforms refine payload design and dosing schedules that aim for long-lived memory responses. In resected melanoma, a personalized mRNA vaccine plus PD-1 therapy reduced the risk of recurrence or death over checkpoint monotherapy, which validated the combination thesis and increased trial activity across other high-risk settings. As datasets accrue, sponsors are evaluating sequence and timing to balance efficacy with immune-related adverse events, with concurrent regimens gaining traction where safety and benefit are consistent.

Growing evidence for durable T-cell memory supports finite-course adjuvant vaccination, while checkpoint agents remain central for metastatic salvage or in tumors where immune suppression is substantial. As payload engineering improves, monotherapy may anchor select adjuvant regimens where biomarker-enriched cohorts show strong recurrence-free survival without added checkpoint toxicity. Sponsors are also optimizing delivery routes to broaden antigen presentation and improve T-cell priming, which can influence the relative role of monotherapy in early-stage disease.

By Cancer Indication: Melanoma Anchors Present, NSCLC Architects Expansion

Melanoma contributed 31.57% of 2025 revenue, supported by high tumor mutational burden and strong clinical visibility from advanced adjuvant programs. NSCLC is expected to expand at a 23.61% CAGR to 2031, helped by large incident populations and momentum from immuno-oncology adoption that primes the care pathway for vaccine integration. High TMB biology in melanoma and smoking-related lung cancer provides abundant neoepitopes, which align with multi-epitope payloads designed to prevent antigen escape. In CNS tumors and other immune-cold settings, delivery challenges remain, though adjunctive strategies and improved trafficking have shown survival gains in select programs. Across indications, adjuvant and MRD-guided approaches are central because they engage the immune system when disease is most vulnerable to T-cell-mediated clearance.

Evidence from dendritic cell and tumor lysate vaccines has demonstrated survival improvements in difficult settings like glioblastoma, reinforcing the potential of antigen-directed priming when delivery barriers are addressed. Renal cell carcinoma and other solid tumors with immunogenic features have shown robust antigen-specific responses in early trials, which keeps them in focus for vaccine-led adjuvant innovation. The neoantigen targeted therapies market will likely diversify from melanoma-led revenue toward larger lung and colorectal opportunities as biomarker-defined subgroups become standard in trial designs. As datasets scale, indications with validated ctDNA stratification and well-characterized neoantigen landscapes should be first to embed vaccines into routine care pathways.

By Delivery Platform: mRNA Speed Races Peptide Stability, DCs Persist Academically

Peptide vaccines held 33.86% of 2025 revenue on the strength of stability profiles and existing regulatory comfort that support diversified routes like intradermal and subcutaneous delivery. mRNA is expected to grow at a 21.87% CAGR given platform familiarity from infectious disease programs and the ability to encode multiple epitopes in a single construct. mRNA payloads have reached multi-epitope breadth within single personalized doses in active clinical programs, which increases coverage against clonal diversity. Dendritic cell approaches remain influential in academic research due to direct antigen presentation across MHC classes, although ex vivo manufacturing steps keep scale and throughput lower than in vivo platforms.

The neoantigen targeted therapies market continues to evaluate viral vectors and DNA constructs where stability and production workflows can complement peptide and mRNA strategies. Platform selection is aligning with delivery route optimization to balance breadth, depth, and durability of T-cell responses across adjuvant and MRD-positive settings. mRNA’s intrinsic immunostimulatory properties support intramuscular use without exogenous adjuvants, while peptide vaccines frequently employ adjuvanted intradermal or subcutaneous strategies to enhance antigen presentation. DNA platforms under evaluation, including oral constructs, are exploring ways to engage mucosal immunity while scaling target breadth and maintaining adequate bioavailability. The neoantigen targeted therapies industry is balancing payload capacity, manufacturing timelines, and route-specific immunogenicity to match indication needs and hospital workflows.

By End User: Academic Institutes Pioneer, Hospitals Scale Deployment

Academic and research institutes represented 42.58% of 2025 revenue, reflecting their leadership in trial initiation, biomarker method development, and early manufacturing partnerships. Tertiary care hospitals are projected to grow the fastest at a 24.48% CAGR as national and regional programs formalize enrollment and delivery pathways beyond quaternary referral centers. In the UK, a coordinated national platform spanning dozens of hospitals is standardizing patient identification, consent, and administration steps for individualized vaccines. Hospitals with existing cell therapy logistics are adapting storage, dispensing, and infusion processes to fit multi-dose personalized vaccine schedules with minimal disruption. This diffusion of operational expertise supports the transition from academic pilots to scaled adjuvant programs in the neoantigen targeted therapies market.

Academic centers continue to run a majority of mechanistic trials and translational studies that refine target selection, delivery routes, and biomarker strategies. Regional networks that connect central genomic testing with local infusion capabilities are emerging to reduce travel burdens and streamline post-surgical timelines. Growing participation from tertiary hospitals also improves real-world data capture, which strengthens evidence for coverage decisions in the medium term. As operational playbooks mature, site activation and training timelines should shorten, helping the neoantigen targeted therapies market expand within established oncology care pathways.

By Route of Administration: Intradermal Captures Langerhans, Subcutaneous Scales Adjuvants

Intradermal injection held 32.94% of 2025 revenue on evidence that dermal antigen-presenting cells boost T-cell priming compared with deeper tissue routes for peptide payloads. Subcutaneous injection is forecast to grow at a 23.76% CAGR due to adjuvant-enriched formulations that benefit from depot formation and lymphatic drainage near target nodes. Intradermal delivery has been associated with higher immunogenicity per microgram for peptide vaccines, which supports dose-sparing strategies in settings where antigen breadth is extensive. Intramuscular administration remains the norm for mRNA vaccines in active programs, leveraging vaccine infrastructure widely adopted in 2021-2023.

Intranodal or catheter-based approaches are used in niche scenarios, including adoptive cell therapy preparation and select dendritic cell protocols where direct lymph node delivery is desired. Route choice reflects platform biology and hospital capabilities, with intradermal methods aligning well to peptide adjuvant regimens and intramuscular routes aligning to mRNA constructs with inherent immunostimulation. Subcutaneous regimens are favored where depot formation and drainage patterns amplify antigen exposure to nodal APCs while fitting clinic workflows for multi-site injections. Continued route optimization is expected as sponsors map tissue pharmacology to T-cell priming and persistence, a lever that remains central to adjuvant outcomes in the neoantigen targeted therapies market. Institutional protocols will likely diversify, balancing ease of administration, patient comfort, and immunogenicity efficiency across early- and late-stage settings.

Geography Analysis

North America held 35.23% of 2025 revenue due to clinical trial density, concentration of sequencing infrastructure, and established immuno-oncology care pathways that can absorb adjuvant vaccine integration. The region continues to run pivotal studies in melanoma and lung cancer, with leading sponsors reporting extended follow-up and expansion into additional tumor types. The neoantigen targeted therapies market in North America benefits from ecosystem readiness, yet broader access will track with coverage decisions that hinge on mature recurrence-free survival data. As hospital networks adapt cell therapy workflows to vaccine logistics, time-to-first-dose post-surgery is expected to shorten, improving utilization of adjuvant windows.

Europe maintains a substantial revenue base and infrastructure depth, supported by cohesive facilitation mechanisms at the EU level and national delivery programs in priority countries. NHS England’s program provides a structured channel for enrolling patients and coordinating multi-site delivery, which broadens operational capacity beyond academic centers. The neoantigen targeted therapies market in Europe is set to benefit from coordinated trial networks and real-world data collection as patient numbers rise across adjuvant indications. Sustained focus on validated biomarkers and method transparency will support health technology assessments and pricing dialogues that shape regional uptake trajectories.

Asia-Pacific is projected to post the fastest growth at a 25.72% CAGR, supported by investment in genomic infrastructure and a rising incident cancer burden that creates strong demand for post-surgical interventions. Active academic programs and expanding trial capacity in large markets are laying the groundwork for scaled manufacturing and faster turnaround times. Population HLA distributions in select countries support shared-neoantigen strategies, which can improve unit economics in prevention or adjuvant niches. Outside APAC, targeted activity in Latin America includes early-phase initiatives focused on pathogen-linked malignancies that broaden regional immunotherapy portfolios. Across regions, the neoantigen targeted therapies market share distribution will continue to track the pace of biomarker adoption, reimbursement clarity, and the diffusion of decentralized GMP capacity from academic nodes into national hospital systems.

Competitive Landscape

The field remains competitive with multiple platform strategies, including mRNA, peptides, dendritic cells, and viral vectors, each aiming to balance breadth, durability, and speed to clinic. Merck and Moderna reported sustained five-year reductions in recurrence risk in resected melanoma and expanded their clinical footprint into additional solid tumor indications, reinforcing confidence among clinicians and trial sponsors. The neoantigen targeted therapies market is also shaped by national delivery partnerships such as the NHS Cancer Vaccine Launch Pad, which provides a high-visibility channel for large-scale enrollment and operational execution.

As clinical programs diversify, sponsors emphasize validated target selection and transparent bioinformatics pipelines to meet evolving regulatory expectations and to support payer dialogue. Companies developing shared frameshift neoantigen products are testing prevention and adjuvant opportunities in biomarker-defined groups, including Lynch syndrome, where immunogenicity has been consistently demonstrated. These programs can reduce manufacturing complexity by producing batch lots that address multiple patients, complementing fully personalized designs. mRNA programs benefit from payload versatility and familiar intramuscular administration, while peptide programs leverage intradermal or subcutaneous routes with adjuvants that concentrate antigen presentation. Academic-industry partnerships continue to be vital for trial activation, translational assays, and route optimization that influence product positioning in adjuvant care.

Neoantigen Targeted Therapies Industry Leaders

BioNTech SE

Geneos Therapeutics, Inc.

Merck & Co., Inc.

Moderna, Inc.

Transgene SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Moderna and Merck announced five-year follow-up data for mRNA-4157 (V940) combined with Keytruda in resected high-risk melanoma, demonstrating a sustained 49% reduction in recurrence or death risk (HR 0.510). The data, from the Phase 2b KEYNOTE-942 trial enrolling 157 patients, showed durability of response with consistent safety profiles, validating the individualized neoantigen therapy platform. The companies have eight Phase 2/3 trials ongoing across melanoma, NSCLC, bladder, and renal cell carcinoma.

- September 2025: Transgene reported positive randomized Phase 1 data for TG4050 in head and neck squamous cell carcinoma, achieving 100% disease-free survival after a median 30-month follow-up in all vaccine-treated patients. The individualized viral-vector vaccine, developed with NEC's AI platform, induced durable neoantigen-specific CD8+ T-cell responses persisting 24 months post-treatment, presented at ASCO 2025.

- October 2025: Evaxion Biotech presented two-year Phase 2 data for EVX-01, its AI-designed personalized peptide vaccine, at ESMO Congress 2025, showing 75% objective response rate in advanced melanoma when combined with pembrolizumab. Eleven of 12 responders maintained clinical benefit at 24 months, with 86% vaccine target precision demonstrated by the PIONEER AI platform.

Global Neoantigen Targeted Therapies Market Report Scope

As per the scope of the report, neoantigen targeted therapies are personalized cancer immunotherapies designed to target neoantigens, which are tumor-specific mutated proteins expressed only on cancer cells and not on normal tissues. These therapies stimulate the patient’s immune system, mainly T cells, to recognize and destroy tumor cells carrying these unique antigens. They include approaches such as neoantigen vaccines (mRNA, peptide, DNA) and neoantigen-specific T-cell therapies (TCR/TIL). Because they are highly personalized, they represent an emerging segment of precision oncology.

The neoantigen targeted therapies market is segmented by therapy type, cancer indication, delivery platform, end user, and route of administration. By therapy type, the market is segmented into monotherapy and combination therapy. By cancer indication, the market is segmented into melanoma, non-small cell lung cancer (NSCLC), colorectal cancer (MSI-H/dMMR), pancreatic ductal adenocarcinoma (PDAC), ovarian cancer, and Others. By delivery platform, the market is segmented into mRNA-based vaccines, peptide-based vaccines, DNA-based vaccines, and others. By end user, the market is segmented into academic & research institutes, tertiary care hospitals, and specialty oncology centers/infusion clinics. By route of administration, the market is segmented into intramuscular, subcutaneous, intradermal, and others. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers estimated market sizes and market trends for 17 countries across major regions worldwide. The report offers market value (in USD) for the above segments.

| Monotherapy |

| Combination Therapy |

| Melanoma |

| Non-small Cell Lung Cancer (NSCLC) |

| Colorectal Cancer (MSI-H/dMMR) |

| Pancreatic Ductal Adenocarcinoma (PDAC) |

| Ovarian Cancer |

| Others |

| mRNA-based Vaccines |

| Peptide-based Vaccines |

| DNA-based Vaccines |

| Others |

| Academic & Research Institutes |

| Tertiary Care Hospitals |

| Specialty Oncology Centers/Infusion Clinics |

| Intramuscular |

| Subcutaneous |

| Intradermal |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Therapy Type | Monotherapy | |

| Combination Therapy | ||

| By Cancer Indication | Melanoma | |

| Non-small Cell Lung Cancer (NSCLC) | ||

| Colorectal Cancer (MSI-H/dMMR) | ||

| Pancreatic Ductal Adenocarcinoma (PDAC) | ||

| Ovarian Cancer | ||

| Others | ||

| By Delivery Platform | mRNA-based Vaccines | |

| Peptide-based Vaccines | ||

| DNA-based Vaccines | ||

| Others | ||

| By End User | Academic & Research Institutes | |

| Tertiary Care Hospitals | ||

| Specialty Oncology Centers/Infusion Clinics | ||

| By Route of Administration | Intramuscular | |

| Subcutaneous | ||

| Intradermal | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the neoantigen targeted therapies market?

The neoantigen targeted therapies market size was USD 1.22 billion in 2025 and is forecast to reach USD 3.73 billion by 2031 at a 20.48% CAGR, supported by expanding adjuvant programs and improving bioinformatics validation.

Which therapy type leads revenue today and which will grow fastest through 2031?

Combination therapy led with 58.42% of 2025 revenue, while monotherapy is projected to grow fastest at a 22.56% CAGR through 2031 as selection tightens in adjuvant and MRD-positive settings.

Which indications are most important for near-term adoption in this space?

Melanoma anchors near-term adoption due to high TMB and mature clinical data, while NSCLC is positioned for the fastest expansion through 2031 given large patient pools and established immuno-oncology pathways.

How are delivery platforms evolving in the neoantigen targeted therapies market?

Peptides lead on stability and route flexibility, mRNA is scaling on payload breadth and familiar intramuscular use, and dendritic cell approaches persist in academic settings where direct antigen presentation is studied.

What regional factors will shape access and growth for these vaccines?

North America benefits from trial density and infrastructure, Europe leverages EU facilitation and NHS-led deployment models, and Asia-Pacific is set for the fastest growth as genomic capacity and hospital readiness expand.

What evidence supports the use of personalized neoantigen vaccines in adjuvant settings?

Five-year data in resected melanoma showed a reduction in recurrence or death when a personalized mRNA vaccine was combined with PD-1 therapy, reinforcing the focus on adjuvant strategies and MRD-guided selection.

Page last updated on: