Natural Flake Graphite Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

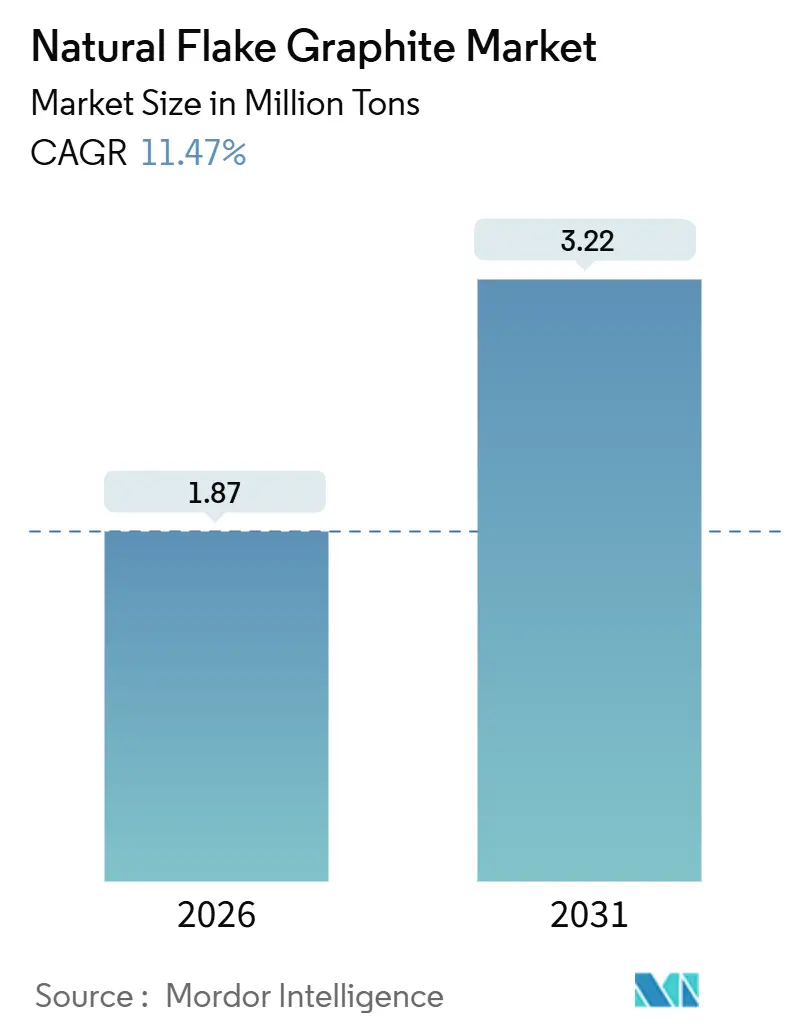

| Market Volume (2026) | 1.87 Million tons |

| Market Volume (2031) | 3.22 Million tons |

| Growth Rate (2026 - 2031) | 11.47% CAGR |

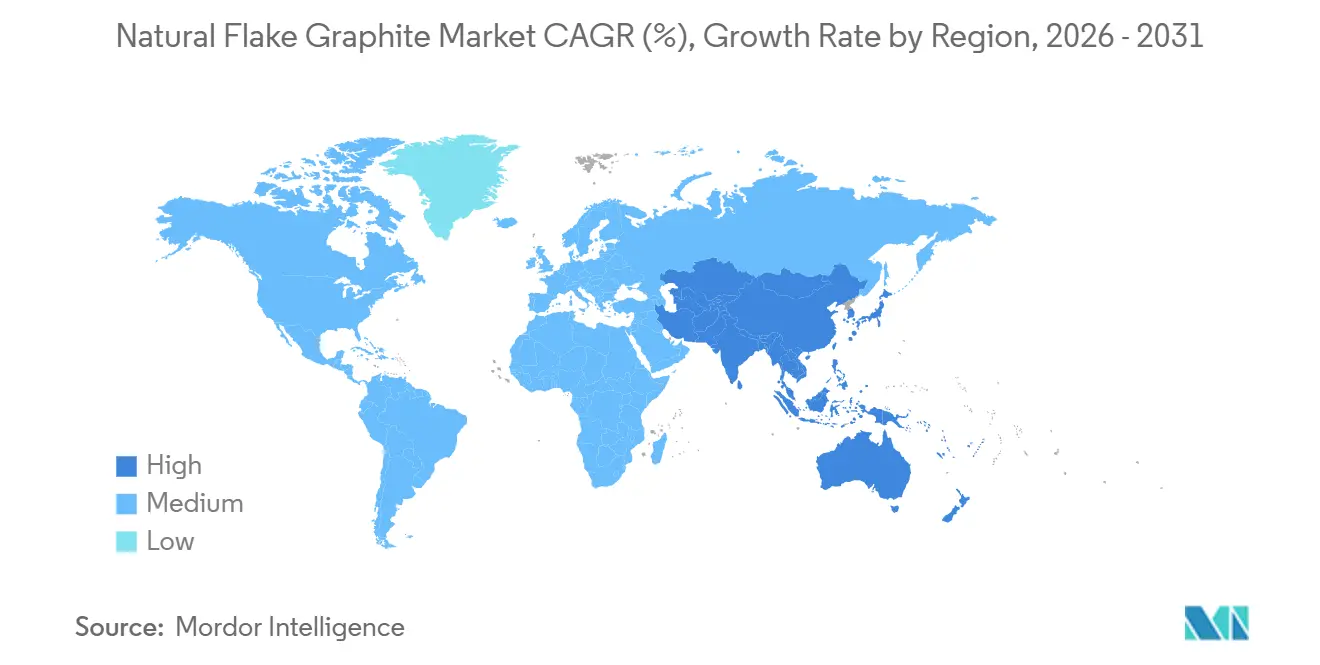

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Natural Flake Graphite Market Analysis by Mordor Intelligence

The Natural Flake Graphite Market size is estimated at 1.87 million tons in 2026, and is expected to reach 3.22 million tons by 2031, at a CAGR of 11.47% during the forecast period (2026-2031). Battery-grade anode demand is accelerating faster than any other outlet, yet supply security now depends more on where purification and spheronisation occur than on raw tonnage alone. China still dominates with the majority of mined output in 2024 and more than 90% of downstream processing capacity, creating a structural bottleneck for Western cell producers. The temporary suspension of Chinese export controls in November 2025 offered short-term price relief but reinforced the policy risk shaping long-term procurement strategies. Processing incentives already committed in the United States are catalyzing new facilities that promise to chip away at China’s grip, although meaningful volumes will not arrive before 2027.

Key Report Takeaways

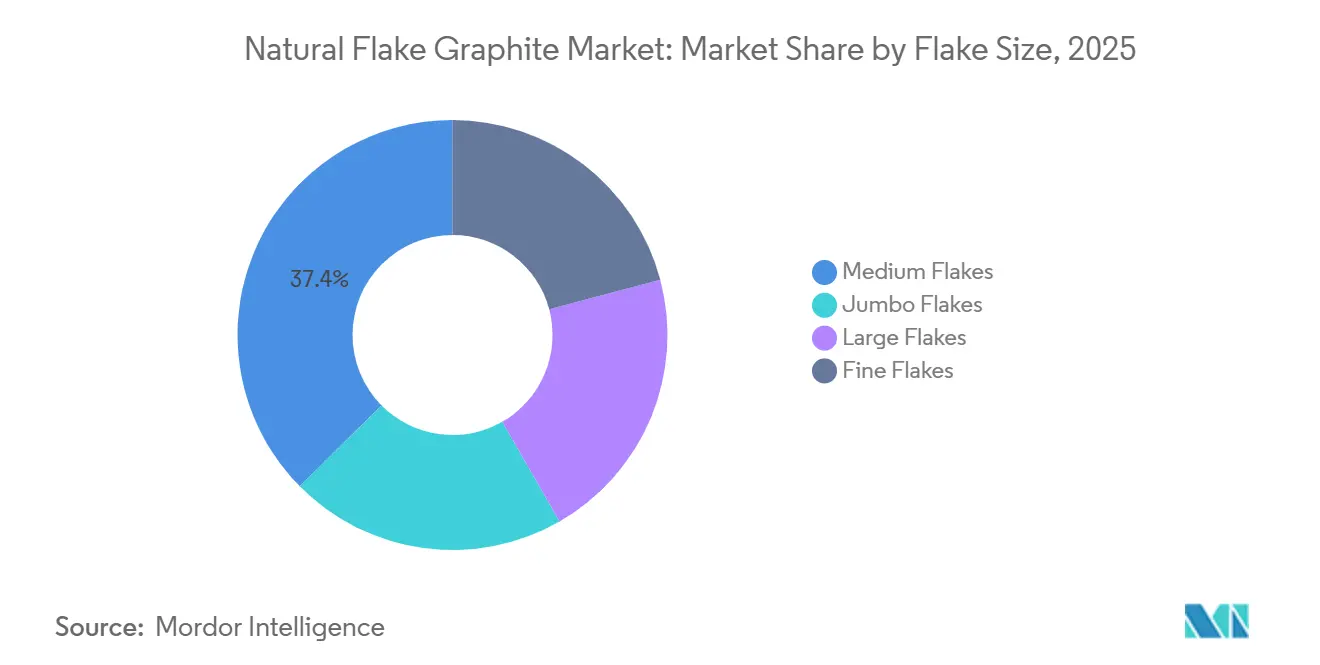

- By flake size, Medium flakes captured 37.43% of the natural flake graphite market share in 2025 and are forecast to grow at a 12.11% CAGR through 2031.

- By purity, high-carbon material grading 94% to less than 99% accounted for 37.95% of the natural flake graphite market size in 2025 and is projected to advance at a 12.22% CAGR to 2031.

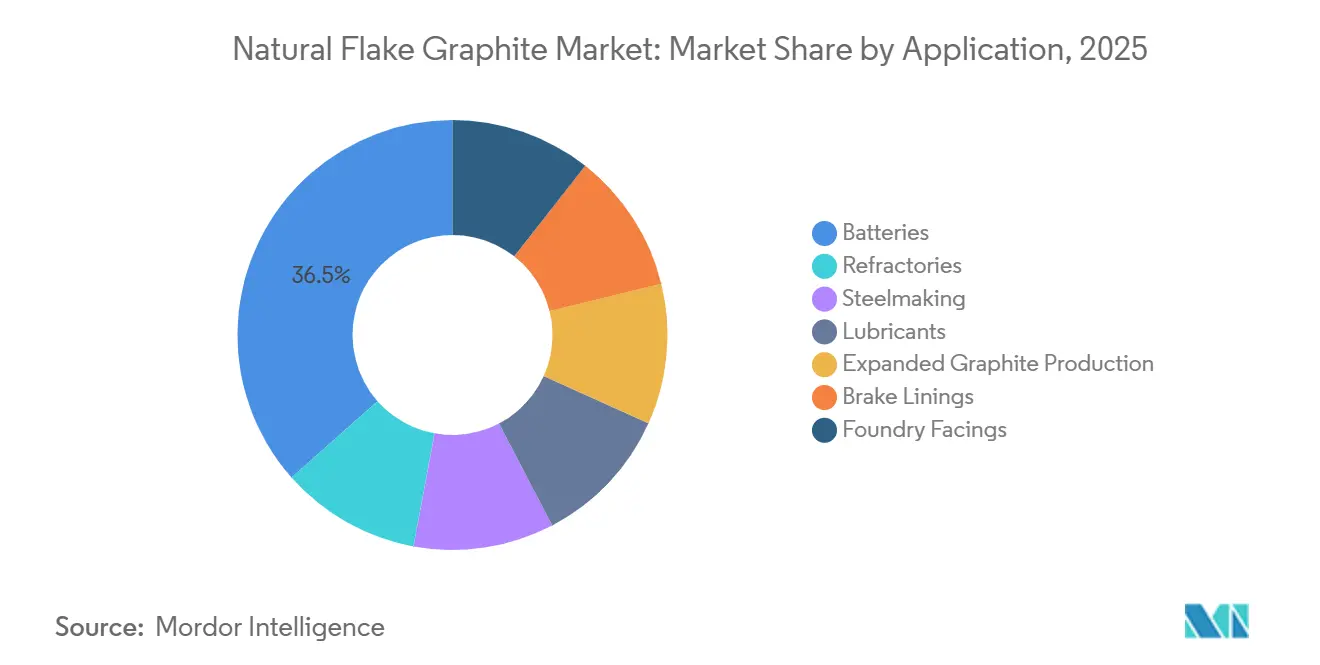

- By application, batteries commanded 36.52% of the natural flake graphite market size in 2025 and are expanding at an 18.93% CAGR, the fastest among all applications.

- By geography, Asia-Pacific held 87.11% of the natural flake graphite market share in 2025, and the region is expected to grow at a 12.20% CAGR over the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Natural Flake Graphite Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand from Li-ion battery anodes for EVs | +5.2% | Global, with concentration in China, South Korea, and emerging capacity in North America and EU | Medium term (2-4 years) |

| Chinese downstream capacity expansion and export restrictions | +2.1% | Global supply chains, most acute in North America, EU, and battery-manufacturing hubs in Asia-Pacific | Short term (≤ 2 years) |

| Cost advantage and lower lifecycle emissions vs synthetic graphite | +1.8% | Global, particularly North America and EU where carbon-intensity regulations favor natural feedstock | Long term (≥ 4 years) |

| Commercialisation of low-HF purification and spheronisation tech | +1.3% | North America, EU, and select Asia-Pacific projects (Australia, India) | Medium term (2-4 years) |

| American and EU processing incentives boosting local sourcing | +1.1% | North America (US, Canada) and EU (Germany, France, Sweden) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand From Li-ion Battery Anodes For EVs

In 2025, global sales of electric vehicles (EVs) surged significantly. This surge translates to an estimated demand for anode-grade natural graphite, especially when factoring in commercial vehicles and stationary storage. Each battery-electric passenger car requires between 50 and 70 kg of anode active material. Furthermore, with OEM qualification cycles securing offtake agreements for up to 24 months, the spot market has tightened considerably. Notably, Panasonic and LG Energy Solution have greenlit concentrate from both Mozambique and Madagascar. This endorsement underscores the capability of non-Chinese suppliers to meet stringent 99.95% carbon specifications. However, challenges persist: currently, fewer than a dozen facilities outside of China possess the capability to commercially spheronise and purify flake graphite. As a result, many emerging mines find themselves reliant on Chinese tolling services. Consequently, the natural flake graphite market remains acutely attuned to the growth trajectories of the battery sector and the ramp-up of gigafactories in both the U.S. and Europe.

Chinese Downstream Capacity Expansion and Export Restrictions

China commands a dominant share of the world's spheronisation capacity, granting Beijing substantial influence over the global natural flake graphite market. In October 2025, the Ministry of Commerce in China hinted at imposing new export controls on both natural and synthetic graphite anodes. However, just a day before these controls were set to take effect, they were abruptly suspended. This unexpected reversal led to a swift decline in medium-flake prices within a fortnight, as traders scrambled to adjust their positions. Despite this market jolt, additional Chinese anode capacity came online in 2025, with the bulk of it earmarked for major players like CATL and BYD. While the specter of renewed export restrictions looms, it's spurring a surge in processing investments in the West. Yet, factories in Louisiana and Alabama face a challenge: they will rely on imported concentrates until their domestic mines can scale up to commercial levels, a milestone anticipated after 2028.

Cost Advantage and Lower Lifecycle Emissions vs Synthetic Graphite

Natural flake graphite is priced less than synthetic graphite, derived from petroleum coke, commands a higher price range. When purified using HF, natural feedstock has lower lifecycle carbon emissions compared to synthetic production methods[1]Nature Sustainability, “Lifecycle Carbon Emissions of Natural vs Synthetic Graphite,” nature.com . Under Europe's Battery Regulation, set to take effect in 2024, carbon-footprint declarations will be mandated, with maximum thresholds introduced by 2027. This move effectively levies a tax on high-emission anodes. Consequently, automakers are increasingly eyeing the natural flake graphite market as a pivotal tool to achieve their Scope-3 objectives, leading to a dip in synthetic demand. With cell prices dropping, the pronounced cost difference and emission benefits underscore the strategic value of the natural supply.

Commercialisation of Low-HF Purification and Spheronisation Tech

While hydrofluoric acid has long been the go-to for silicate removal, its inherent toxicity and concentrated supply chains in China are spurring innovations in processing methods. EcoGraf's Kwinana demonstration plant in Western Australia showcased a groundbreaking HF-free flowsheet, achieving high carbon purity. Meanwhile, researchers from the University of Queensland have secured a license for a pulsed-electrolysis technique, significantly reducing acid usage and cutting capital expenses. Additionally, alkali-roasting trials are underway in Ontario and Madagascar, though they still rely on caustic soda, another input predominantly sourced from China. If these alternative methods can be successfully scaled, they promise to diversify chemical supply chains, alleviating a significant challenge for Western purification initiatives. Yet, every emerging process faces rigorous automotive qualifications, extending its journey to market readiness.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Environmental permitting hurdles at new mines | -1.4% | North America (US, Canada), EU (Scandinavia), and select African jurisdictions (Tanzania, Mozambique) | Medium term (2-4 years) |

| Dependency on Chinese HF and caustic soda supply chain | -0.9% | Global, most acute for non-Chinese processing facilities in North America, EU, and Australia | Short term (≤ 2 years) |

| Price volatility driven by Chinese policy interventions | -0.7% | Global, with spillover effects most pronounced in spot markets and non-contracted volumes | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Environmental Permitting Hurdles At New Mines

In North America and Europe, securing mine approvals can take several years, hindering efforts to diversify feedstock. In 2024, Quebec withheld funding for a project with a low TGC, pointing to community worries about tailings. Alaska's Graphite Creek deposit is still navigating the FAST-41 program, with a Record of Decision anticipated by September 2026. Meanwhile, projects in Africa grapple with negotiations over water use and surface rights, pushing their development timelines back by as much as two years. As a result of these setbacks, the natural flake graphite market remains closely linked to sources in China and Mozambique for the foreseeable future.

Dependency On Chinese HF And Caustic-Soda Supply Chain

Hydrofluoric acid and caustic soda account for nearly significant portion of purification operational expenditures (opex), with China dominating the scene, supplying the majority of the world's hydrofluoric acid (HF) output. In Asia, spot prices for HF surged significantly in 2024, largely due to environmental audits leading to shutdowns at Shandong plants. Meanwhile, alternative suppliers in Mexico and South Africa are commanding a premium, which is squeezing processor margins. As domestic chemical capacities take time to scale, Western purification projects find themselves still vulnerable to the very policy risks they sought to evade, hindering swift expansion in the natural flake graphite market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Flake Size: Medium Flakes Anchor Battery-Anode Feedstock

Medium flakes accounted for 37.43% of the natural flake graphite market size in 2025 and are projected to grow at a 12.11% CAGR through 2031. Their 80- to 150-mesh profile not only optimizes rounding efficiency during spheronisation but also plays a pivotal role in minimizing both yield losses and energy consumption. While large and jumbo flakes command premium prices in refractories and thermal-management films, they come with a caveat: these grades necessitate additional milling before integration into anode lines, incurring an added processing cost[2]Syrah Resources, “Investor Presentation Q3 2025,” syrahresources.com.au. Fine flakes, once a staple in lubricants, have seen their market share eroded by synthetic substitutes, leading to a notable price drop. In a strategic pivot, miners are recalibrating flotation circuits to enhance recovery of the 100- to 120-mesh fraction, a preference of anode plants, highlighting the battery sector's growing sway over the natural flake graphite market.

Syrah’s Balama mine, with its significant yield of large and jumbo flakes, strategically positions the company to capture margins in specialty niches. However, this advantage comes with the challenge of requiring additional comminution for its plant in Vidalia, Louisiana. NextSource’s Molo project skews its production distribution towards medium grades, striking a balance by reducing downstream costs but simultaneously curtailing access to premium refractory markets. Walkabout Resources’ Lindi Jumbo deposit, naturally grading at a high percentage of medium flakes, has piqued the interest of Chinese anode manufacturers eager to diversify their supply sources. With the battery demand on an upward trajectory, medium flakes are poised to remain the cornerstone of the natural flake graphite industry.

By Purity: High-Carbon Graphite Balances Cost And Processing Flexibility

Materials graded between 94% and less than 99% total graphitic carbon (TGC) commanded a 37.95% share of the natural flake graphite market and will advance at a 12.22% CAGR to 2031. Concentrates within this TGC range sidestep on-site HF plants, enabling miners to dispatch their products to specialized purifiers. These purifiers elevate the TGC to a premium 99.95% battery grade, fetching high prices per ton. Tirupati’s Vatomina operation, consistently yielding 96–97% TGC, is strategically positioned for swift qualification with anode customers. Meanwhile, Northern Graphite’s Lac des Iles mill achieved commendable carbon purity through flotation and thermal upgrading. They are now experimenting with alkali-roasting techniques, aiming for the coveted 99.5% purity, all without the use of HF.

Medium-carbon graphite, falling between 90% and less than 94%, remains a staple in brake linings and basic refractories. In contrast, low-carbon grades, ranging from 50% to 80%, have seen stagnation in their traditional applications, such as foundry coatings and pencils. Original Equipment Manufacturer (OEM) cell producers mandate a stringent 99.95% purity specification to avert lithium plating issues. This requirement propels purification houses to pursue increasingly stringent impurity thresholds. As technologies free from HF continue to evolve, there's potential for high-carbon concentrates to enjoy enhanced profit margins, underscoring their pivotal role in the natural flake graphite market.

By Application: Batteries Overtake Refractories As Dominant End-Use

Batteries absorbed 36.52% of the natural flake graphite market size in 2025 and are expanding at an 18.93% CAGR. While refractory demand, closely tied to steel output, sees modest growth, China's shift towards electric-arc furnaces is curbing graphite use per ton of steel. Though graphite electrodes account for a notable portion of the supply in steelmaking, producers are increasingly blending natural flake with needle coke to manage costs. Expanded graphite, utilized in fire-retardant panels and thermal-interface materials, is witnessing steady annual growth. This surge is bolstered by its applications in EV battery-pack sealing and data-center cooling.

Lubricants and brake linings, collectively accounting for a small share of the volume, face pressure from rising synthetic alternatives. In a notable shift, LG Energy Solution and Samsung SDI have pre-qualified non-Chinese concentrate, underscoring their confidence in a diversified supply chain. Further emphasizing this trend, CATL has inked a memorandum to assess Western Australian feedstock, highlighting that even industry behemoths recognize the strategic advantage of external sourcing. Given these dynamics, battery demand is poised to be the dominant growth driver for the natural flake graphite market.

Geography Analysis

Asia-Pacific dominated the natural flake graphite market in 2025 with 87.11% of volume and is projected to grow at a 12.20% CAGR through 2031. China's Heilongjiang and Shandong provinces serve as the backbone of the global supply chain, with Jixi city alone producing a notable amount annually. Meanwhile, India, having produced graphite in 2024, is in the process of commissioning a purification plant in Tamil Nadu under its production-linked incentive scheme. Japan, entirely reliant on imports, primarily sources its graphite from China and Madagascar. However, Panasonic has made a strategic move, approving Mozambican concentrate for its cell plants located in Nevada and Wakayama.

North America, contributing a small portion of the mined tonnage in 2025, is gearing up to process graphite annually by 2028, thanks to ramping facilities in Louisiana and Alabama. Canada's Lac des Iles mine is on track to scale up by 2026, and Northern Graphite's newly acquired asset in Namibia has the potential to add more by 2028. However, Mexico's artisanal output remains limited and not suitable for battery applications. The market is further buoyed by policy support, notably the Inflation Reduction Act's enticing USD 10 per kg credit.

Europe's presence in the mining landscape was minimal in 2025. While Norway's Skaland managed to deliver graphite targeting high-purity niches, Germany's Graphit Kropfmühl achieved commendable carbon purity on its output. The Critical Raw Materials Act, emphasizing self-sufficiency, mandates that by 2030, a significant portion of the bloc's annual battery-material demand be processed within Europe. This has catalyzed plans for an expansion in Bavaria, bolstered by guarantees from KfW. Africa's prominence is on the rise, with Mozambique, Madagascar, and Tanzania collectively exporting graphite in 2025 and gaining pre-qualification with OEMs at an accelerated pace. South America, spearheaded by Brazil's Minas Gerais mines, continues to target the lower-purity refractory markets.

Competitive Landscape

The natural flake graphite market is moderately consolidated. POSCO’s joint venture with Mineral Commodities will channel Western Australian concentrate to Gwangyang, reflecting automaker appetite for diversified anode supply. Non-Chinese mined supply in the natural flake graphite market rose in 2025. Expansion pacing hangs on permitting timelines and customer qualification cycles that stretch up to three years, suggesting incremental rather than disruptive share shifts. The competitive landscape, therefore, hinges on which players can pair ore with local purification and coating in politically stable jurisdictions.

Natural Flake Graphite Industry Leaders

Syrah Resources Limited

HAIDA GRAPHITE

Nacional de Grafite

Qingdao Jinhui Graphite Co., Ltd.

China Graphite Group Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Northern Graphite launched USE-G, a three-year research and development program funded by Germany’s Federal Ministry for Economic Affairs and Energy to develop HF-free purification and recycling routes entirely within Europe.

- January 2026: Titan Mining began producing flake graphite concentrate at its Kilbourne demonstration plant in New York, initiating the first U.S. domestic supply chain in more than seven decades.

Global Natural Flake Graphite Market Report Scope

Natural flake graphite is defined as a high-crystallinity form of carbon that occurs naturally in metamorphic rocks. It is characterized by its plate-like, fish-scale structure and is a soft, grey-to-black mineral with high thermal and electrical conductivity, lubricity, and heat resistance. It is widely used in applications such as lithium-ion batteries and refractories.

The graphite market is segmented by flake size, purity, and application. By flake size, the market is segmented into jumbo flakes, large flakes, medium flakes, and fine flakes. By purity, the market is segmented into 99.9% (high purity graphite), 94% to less than 99% (high carbon graphite), 90% to less than 94% (medium carbon graphite), 80% to less than 90% (low to medium carbon graphite), and 50% to less than 80% (low-carbon graphite). By application, the market is segmented into refractories, steelmaking, batteries, lubricants, expanded graphite production, brake linings, and foundry facings. The report also covers the market size and forecasts in 15 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of volume (Tons).

| Jumbo Flakes |

| Large Flakes |

| Medium Flakes |

| Fine Flakes |

| 99.9% (high purity graphite) |

| 94% to less than 99% (high carbon graphite) |

| 90% to lest than 94% (medium carbon Graphite) |

| 80% to less than 90% (low to medium carbon graphite) |

| 50% to less than 80% (low-carbon graphite) |

| Refractories |

| Steelmaking |

| Batteries |

| Lubricants |

| Expanded Graphite Production |

| Brake Linings |

| Foundry Facings |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Flake Size | Jumbo Flakes | |

| Large Flakes | ||

| Medium Flakes | ||

| Fine Flakes | ||

| By Purity | 99.9% (high purity graphite) | |

| 94% to less than 99% (high carbon graphite) | ||

| 90% to lest than 94% (medium carbon Graphite) | ||

| 80% to less than 90% (low to medium carbon graphite) | ||

| 50% to less than 80% (low-carbon graphite) | ||

| By Application | Refractories | |

| Steelmaking | ||

| Batteries | ||

| Lubricants | ||

| Expanded Graphite Production | ||

| Brake Linings | ||

| Foundry Facings | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How fast is the demand for natural anode material growing?

Battery applications are expanding at an 18.93% CAGR, making them the fastest-growing outlet in the natural flake graphite market.

Which flake size is preferred for EV batteries?

Medium flakes (80–150 mesh) dominate because their shape yields high rounding efficiency and captured a 37.43% share in 2025.

When will U.S. processing capacity meaningfully scale?

Vidalia, Louisiana, and Kellyton, Alabama, are slated to add capacity by 2028, reducing reliance on Chinese tolling.

What purity level do automakers require?

Cell manufacturers typically demand 99.95% carbon, which is achieved by purifying 94–less than 99% concentrate via chemical or thermal routes.

What is current market size of Natural Flake Graphite Market?

The Natural Flake Graphite Market size is estimated at 1.87 million tons in 2026, and is expected to reach 3.22 million tons by 2031, at a CAGR of 11.47% during the forecast period (2026-2031).

Page last updated on: