Nasopharyngeal Swabs Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

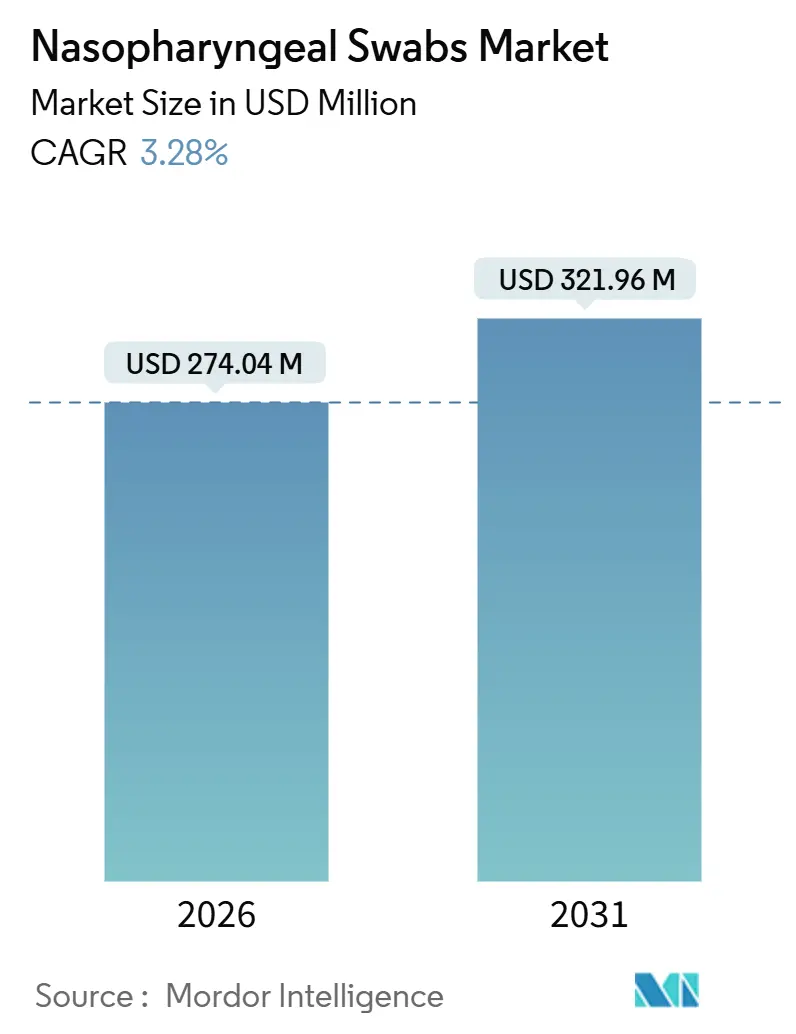

| Market Size (2026) | USD 274.04 Million |

| Market Size (2031) | USD 321.96 Million |

| Growth Rate (2026 - 2031) | 3.28% CAGR |

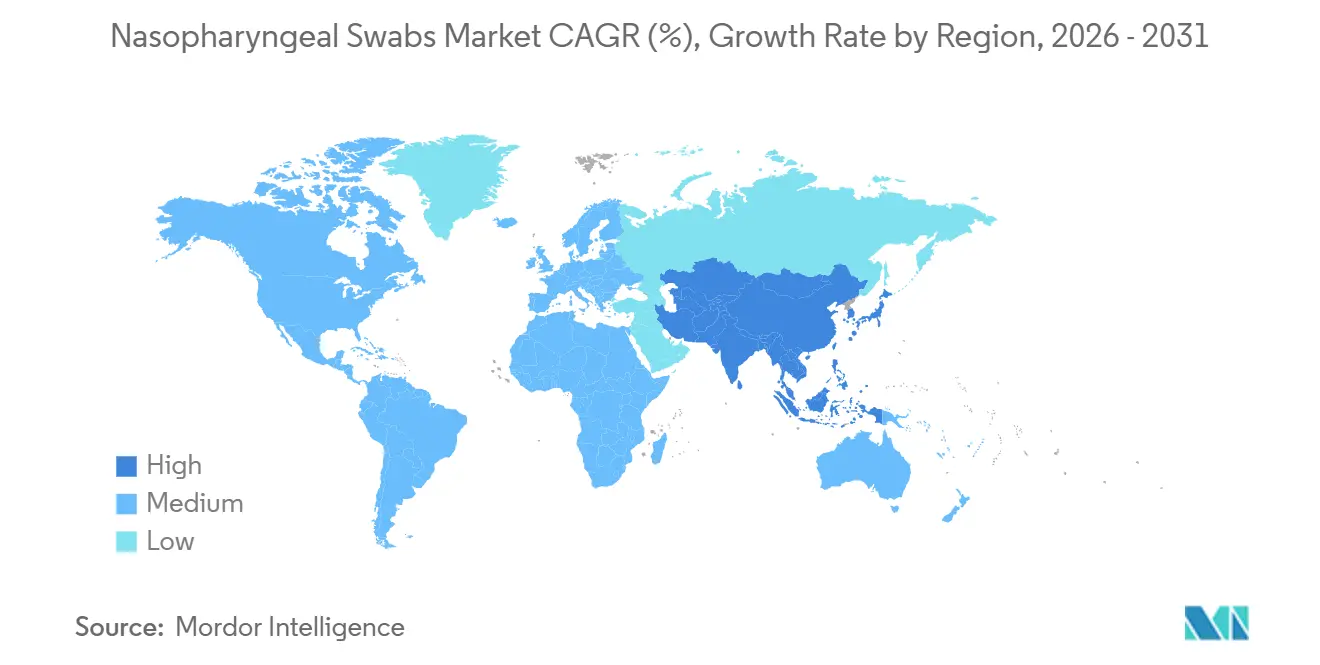

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Nasopharyngeal Swabs Market Analysis by Mordor Intelligence

The Nasopharyngeal Swabs Market size is estimated at USD 274.04 million in 2026, and is expected to reach USD 321.96 million by 2031, at a CAGR of 3.28% during the forecast period (2026-2031).

Demand is no longer driven solely by emergency stockpiling; instead, routine respiratory surveillance, wider adoption of multiplex assays, and a shift toward home-based diagnostics support a steady purchasing cadence. Twelve U.S. FDA–cleared combination flu–COVID home-test kits launched during 2024–2025 have placed nasopharyngeal collection inside everyday medicine cabinets, creating recurring consumer-driven orders that complement institutional procurement cycles. Design advances, particularly flocked and foam geometries, are improving viral-RNA recovery, lowering false-negative rates, and reinforcing premium pricing strategies among established suppliers. Geographically, capacity additions in China and India underpin a 6.35% growth trajectory in Asia-Pacific, while North America’s onshoring mandates ensure baseline volumes for domestic plants. Competitive intensity remains moderate because ISO 13485 certification, stringent FDA 510(k) pathways, and sustainability compliance collectively raise the cost of market entry.

Key Report Takeaways

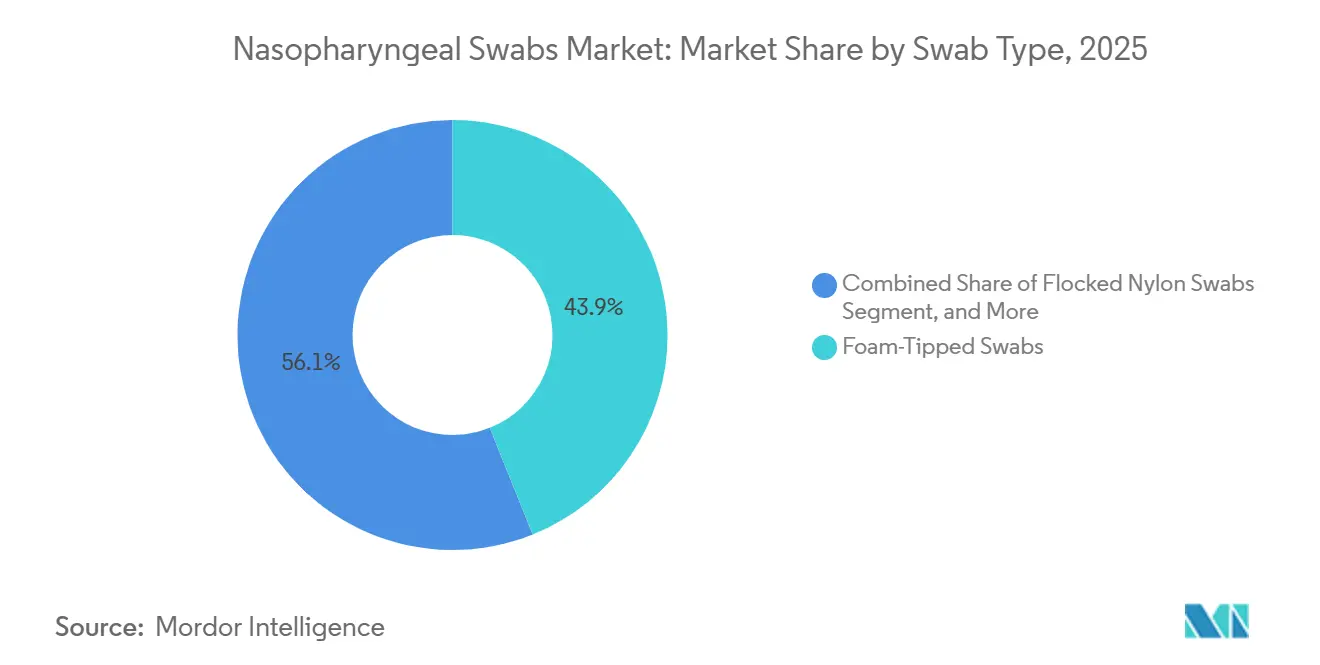

- By swab type, foam-tipped designs led with 43.91% revenue share in 2025; non-woven variants are projected to advance at a 4.38% CAGR to 2031.

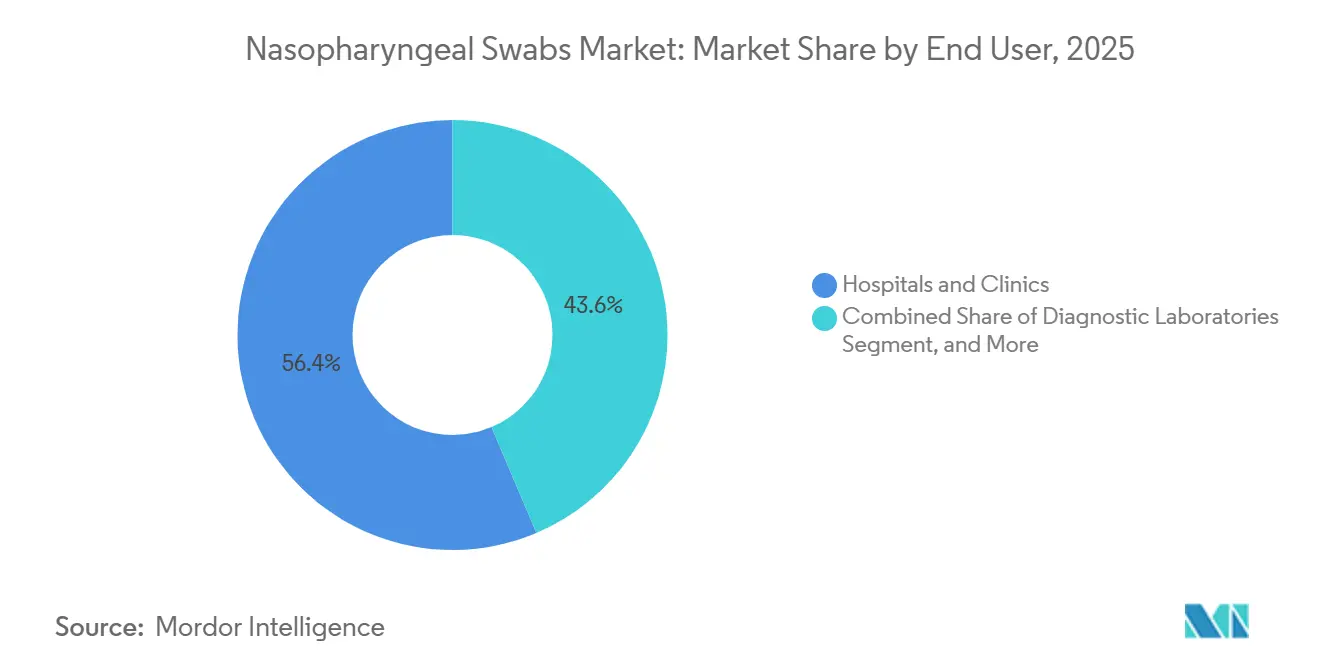

- By end user, hospitals and clinics held 56.38% of the nasopharyngeal swabs market share in 2025, while home-care settings are poised for the fastest 4.81% CAGR through 2031.

- By geography, North America accounted for 39.03% of the 2025 volume, whereas the Asia-Pacific is expected to expand at a 6.35% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Nasopharyngeal Swabs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sustained Demand for Respiratory Infection Diagnostics | +0.9% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Public-Health Surveillance Stock-Piling Programs | +0.6% | North America, Europe, APAC (China, India, Australia) | Long term (≥ 4 years) |

| Advances in Flocked & Foam-Tip Designs | +0.5% | Global, led by North America and Europe | Medium term (2-4 years) |

| Expansion of Point-of-Care & At-Home Testing | +0.8% | North America, Europe, with spillover to APAC urban centers | Short term (≤ 2 years) |

| On-Shoring Mandates & Domestic Procurement Incentives | +0.4% | North America and Europe, emerging in India | Medium term (2-4 years) |

| Automation-Ready Proprietary Swab Geometries | +0.3% | North America, Europe, select APAC hubs (Japan, South Korea) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Sustained Demand for Respiratory Infection Diagnostics

Seasonal co-circulation of influenza and SARS-CoV-2 has stabilized at levels 35% above the pre-2020 baseline, locking in elevated swab volumes even after the acute pandemic phase.[1]Centers for Disease Control and Prevention, “FluView Weekly Report,” cdc.gov Multiplex molecular panels now account for 62% of U.S. respiratory tests, and each panel requires a nasopharyngeal specimen, effectively tripling per-patient swab use. The WHO’s Global Influenza Surveillance and Response System expanded to 156 countries by late 2025 and supports multi-year procurement contracts that smooth factory utilization. Steady demand enables suppliers to optimize production runs and lower unit costs, reinforcing the economic rationale for continued capacity expansion.

Public-Health Surveillance Stockpiling Programs

BARDA committed USD 220 million through 2026 to underwrite three U.S. swab plants, while Canada’s Public Health Agency signed a five-year framework to sustain an 80 million-unit reserve.[2]Biomedical Advanced Research and Development Authority, “Domestic Swab Capacity Grants,” medicalcountermeasures.gov India’s Atmanirbhar Swab Initiative subsidizes 1.2 billion units of annual domestic capacity to cut import reliance below 30% by 2027. Such contracts privilege supply security over price, supporting margin premiums, but they also introduce quarterly ordering spikes that test logistics networks.

Advances in Flocked & Foam-Tip Designs

Copan’s FLOQSwabs delivered 23% higher viral-RNA yield than rayon comparators in a 2024 Journal of Clinical Microbiology trial, enhancing PCR sensitivity. Puritan’s dual-density foam tip cut patient discomfort scores by 31% without compromising sample adequacy. Becton, Dickinson, and Company integrated a breakpoint for standardized immersion depth, reducing pre-analytical specimen failures in automated labs. These refinements elevate swabs from low-margin consumables to precision collection tools and deter price-only entrants.

Expansion of Point-of-Care & At-Home Testing

The FDA cleared eight over-the-counter nasopharyngeal kits during 2024–2025; each bundle includes a swab with integrated antigen or molecular cartridges for 15-minute results. Quidel’s QuickVue At-Home Flu+COVID kit achieved 94% concordance with professional collection, validating self-collection for mainstream retail sale. In Europe, CE-IVD authorization now covers 14 self-collection product families, anchoring a retail channel that rival hospital volumes. Consumer-friendly packaging and smartphone guidance encourage repeat purchases and broaden the user base beyond clinical settings.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth of Saliva & Breath Sampling Alternatives | -0.6% | North America, Europe, select APAC urban markets | Medium term (2-4 years) |

| Stringent Regulatory & QC Compliance Costs | -0.3% | Global, most acute in North America and Europe | Long term (≥ 4 years) |

| Sustainability Push Against Single-Use Plastics | -0.2% | Europe, emerging in North America and APAC | Long term (≥ 4 years) |

| Post-Pandemic Inventory Overhang at Agencies | -0.4% | North America, Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growth of Saliva & Breath Sampling Alternatives

OraSure’s saliva PCR received FDA clearance in March 2025 with 91% sensitivity relative to nasopharyngeal RT-PCR, removing the discomfort barrier for community testing. Breath-aerosol devices earned three Emergency Use Authorizations for influenza and COVID during 2024–2025, promoting non-invasive screening at airports and large events.[3]U.S. Food and Drug Administration, “Emergency Use Authorizations List,” fda.gov A 2025 meta-analysis in The Lancet affirmed diagnostic equivalence of saliva testing within 5 days of symptom onset. Reimbursement parity is narrowing, as private insurers in eight U.S. states equalized payment in 2025 potentially redirecting specimen volumes away from swabs by 2029.

Stringent Regulatory & QC Compliance Costs

ISO 13485 certification now costs USD 180,000–350,000 per mid-sized plant, while new FDA sterility guidance adds USD 12,000 per variant for endotoxin validation. China’s 2024 GMP inspections cited 18% of audited swab makers for environmental nonconformities, forcing production pauses and spot price spikes. Heightened compliance favors incumbents with dedicated regulatory teams and slows the pace of new-entrant disruption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Swab Type: Automation-Driven Upside for Non-Woven Designs

Non-woven swabs will outpace the nasopharyngeal swabs market average with a 4.38% CAGR to 2031, reflecting rising laboratory automation that values uniform fiber orientation and rigid shafts. Foam-tipped designs capture 43.91% of 2025 revenue, securing first place because reduced insertion force improves patient compliance, yet their compressibility challenges robotic pick-and-place systems. Flocked nylon swabs deliver the highest viral-RNA yield but carry a 12%-18% price premium that limits public-health penetration. Non-woven variants balance cost and automation readiness, achieving 99.5% robotic transfer success rates in 3,000-plus specimen labs. Others—including rayon and cotton—remain niche options for veterinary and environmental sampling.

Hospitals continue to validate flocked designs for critical care, but high-throughput reference labs are centralizing on non-woven geometries that integrate seamlessly into liquid-handling robots. Flocked swabs secured 14 new FDA clearances during 2024–2025, showing innovation momentum; however, process tweaks have narrowed yield gaps between flocked and non-woven tips, eroding the justification for higher pricing in price-sensitive settings. Foam-tipped products dominate pediatric and geriatric use cases thanks to their lower insertion force of 0.8–1.2 newtons, a critical factor when repeated testing is required. These performance-versus-price trade-offs shape procurement algorithms as health systems standardize kits across large patient populations.

By End User: Home-Care Settings Reshape Distribution

Hospitals and clinics accounted for 56.38% of the 2025 demand, but home-care settings will grow at a 4.81% CAGR, nearly 50% above the nasopharyngeal swabs market average. Government reimbursement reforms push lower-acuity testing out of high-cost facilities, while retail pharmacy chains stock FDA-cleared self-collection kits that deliver lab-quality results in minutes. Diagnostic laboratories, although the second-largest end-user segment, face margin pressure from an 8% Medicare cut to molecular panel payments in 2025.

The swab design now includes human-factors engineering depth-limiting sleeves and QR-coded video instructions, lifting self-collection accuracy to 89% in JAMA-published research. As a result, payers and employers accept home testing for disease surveillance programs. Occupational health, schools, and corrections facilities form a smaller but time-sensitive subsegment purchasing premium kits that guarantee turnaround times under 30 minutes. Hospital dominance persists for ICU and immunocompromised testing, but the channel mix is tilting inexorably toward decentralized models that value convenience.

Geography Analysis

North America commands 39.03% of global revenue, anchored by Medicare-funded respiratory panels covering 140 million beneficiaries, yet growth slowed to 1.8% in 2025 because of strategic stockpile drawdowns. Canada’s provincial mandates for six-month reserves provide predictable, contract-based demand, while Mexico expanded diagnostic coverage to 12 million citizens in 2024, thereby stimulating uptake of low-cost variants.

Europe remains the second-largest region; however, implementation of the EU Medical Device Regulation raised annual post-market surveillance costs to EUR 80,000–150,000 per product family and accelerated supplier consolidation. Country-specific procurement nuances, Germany favors domestic makers, France prizes the lowest price, and the UK blends both, complicating commercial strategies for multinationals.

Asia-Pacific is the growth engine, with a 6.35% CAGR, propelled by China’s 4,200 new county-level diagnostic centers and India’s Atmanirbhar subsidies, which are supporting 1.2 billion-unit annual capacity by 2027. The Middle East and Africa benefit from pandemic-preparedness drives, such as Saudi Arabia’s USD 42 million reserve contract, whereas South America faces currency volatility that shifts purchasing toward lower-priced Chinese imports.

Competitive Landscape

The nasopharyngeal swabs market is moderately concentrated. Puritan’s vertical integration shields margins from polypropylene price swings, while Copan’s 14-patent portfolio on flocking processes justifies a 22% price premium in accuracy-sensitive hospital tenders. SARSTEDT and Thermo Fisher differentiate via automation-friendly shaft geometries and barcode systems.

Emerging Chinese makers such as Jiangsu Huida Medical Instruments and Kangjian Medical exported 420 million units in 2025 after gaining ISO 13485 certification, pressuring incumbents with tender pricing 30%-40% lower. Technology adoption diverges by scale: top suppliers deploy inline vision inspection at 600 units per minute and achieve field-failure rates under 0.8%, whereas mid-tier producers rely on statistical sampling with 2.3% failure rate differences that sway hospital purchasing committees. Regulatory hurdles 14- to 18-month FDA 510(k) pathways costing USD 250,000 per variant continue to cap the number of new entrants and temper price erosion in developed economies.

Nasopharyngeal Swabs Industry Leaders

Thermo Fisher Scientific

Becton, Dickinson & Company

Cardinal Health

OraSure Technologies

Dynarex Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Becton Dickinson budgeted USD 65 million to add three Nebraska production lines, lifting U.S. capacity by 250 million units annually by Q3 2027.

- December 2025: BD secured EU IVDR certification for two respiratory assays on the BD MAX system, broadening molecular-testing compatibility.

- April 2024: Solventum, spun off from 3M, partnered with Cardinal Health to co-distribute specimen-collection lines across 5,000 U.S. hospitals.

Global Nasopharyngeal Swabs Market Report Scope

The Nasopharyngeal Swabs Market refers to the global medical device industry that manufactures, distributes, and sells nasopharyngeal (NP) swabs, specialized, long, flexible sampling devices designed to collect specimens from the posterior nasopharynx for diagnostic testing.

The Nasopharyngeal Swabs Market Report is segmented by swab type into foam-tipped, flocked nylon, non-woven, and others; by end user into hospitals & clinics, diagnostic laboratories, home-care settings, and others; and by geography into North America, Europe, Asia-Pacific, Middle East & Africa, and South America. Market forecasts are provided in terms of value (USD).

| Foam-Tipped Swabs |

| Flocked Nylon Swabs |

| Non-Woven Swabs |

| Others |

| Hospitals & Clinics |

| Diagnostic Laboratories |

| Home-Care Settings |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Swab Type | Foam-Tipped Swabs | |

| Flocked Nylon Swabs | ||

| Non-Woven Swabs | ||

| Others | ||

| By End User | Hospitals & Clinics | |

| Diagnostic Laboratories | ||

| Home-Care Settings | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large will the nasopharyngeal swabs market be by 2031?

The nasopharyngeal swabs market is forecast to reach USD 321.96 million by 2031, growing at a 3.28% CAGR.

Which swab type is growing fastest?

Non-woven designs are projected to grow at 4.38% CAGR thanks to their compatibility with laboratory automation.

Why are home-care settings gaining importance?

FDA-cleared self-collection kits and retail pharmacy distribution are enabling a 4.81% CAGR in home-care demand.

Which region is the strongest growth engine?

Asia-Pacific leads with a 6.35% CAGR, powered by capacity additions in China and India and rising diagnostic penetration.

What is the main restraint facing swab makers?

Emerging saliva and breath sampling alternatives could divert volumes, subtracting 0.6 percentage points from forecast CAGR.

Page last updated on: