Myanmar Data Center Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

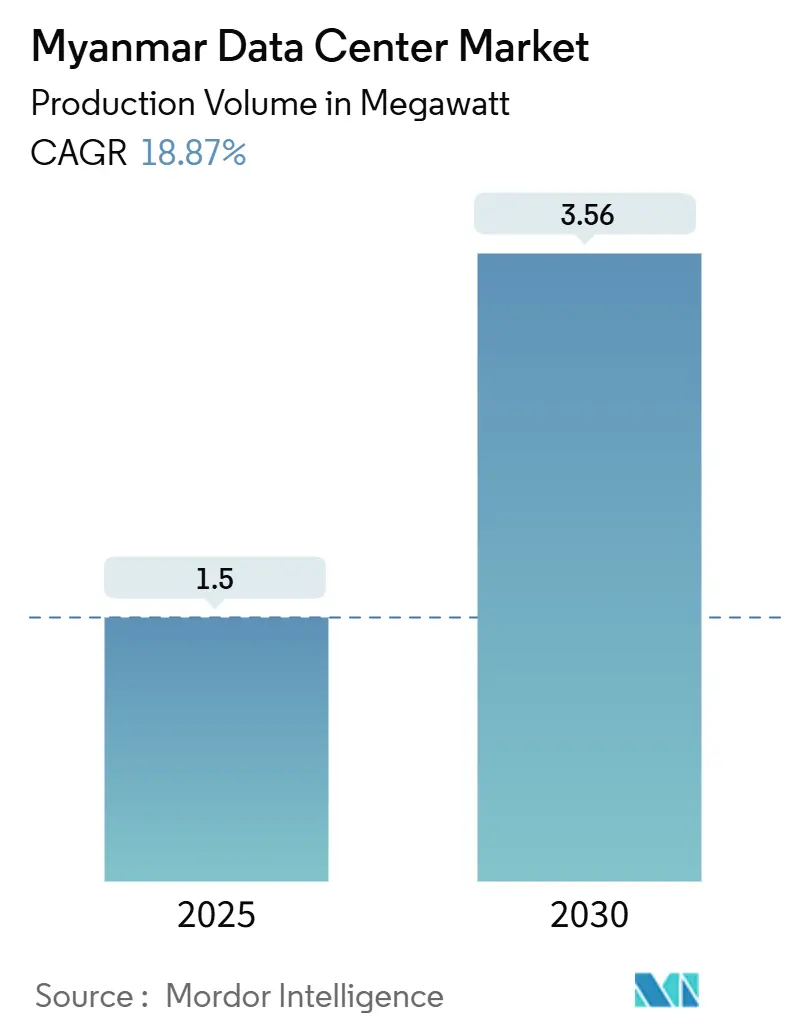

| Market Volume (2025) | 1.5 megawatt |

| Market Volume (2030) | 3.56 megawatt |

| Growth Rate (2025 - 2030) | 18.87% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Myanmar Data Center Market Analysis by Mordor Intelligence

The Myanmar data center market size is projected to reach 3.56 MW by 2030, advancing at an 18.87% CAGR over the 2025-2030 period, following an installed IT load of 1.5 MW in 2025. Rising mobile internet penetration, rapid fintech adoption, and the government’s Digital Economy Roadmap 2025 are combining to lift enterprise and consumer demand for secure, low-latency computing capacity. Intensifying 5G rollouts by operators such as MPT and ATOM are driving the need for dense edge-node requirements, which favors colocation builds in Yangon and Mandalay. E-payments processed by KBZPay alone now exceed USD 9 billion annually, illustrating the transaction volumes that are pushing investors toward highly resilient facilities. Meanwhile, new submarine and terrestrial fiber routes, most notably the MIST cable, shrink international latency and make the Myanmar data center market attractive for serving cross-border workloads

Key Report Takeaways

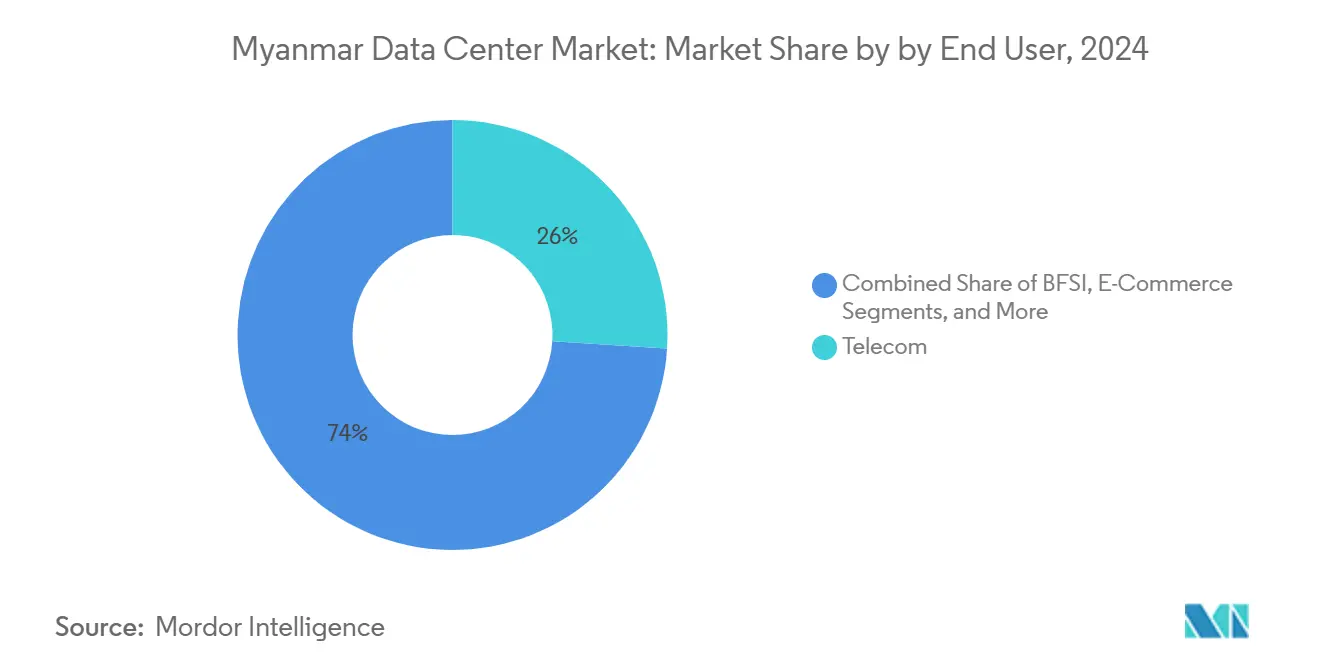

- By end-user, telecommunications companies accounted for a 26% share of the Myanmar data center market size in 2024, whereas cloud service providers are projected to grow at a 19.60% CAGR from 2024 to 2030.

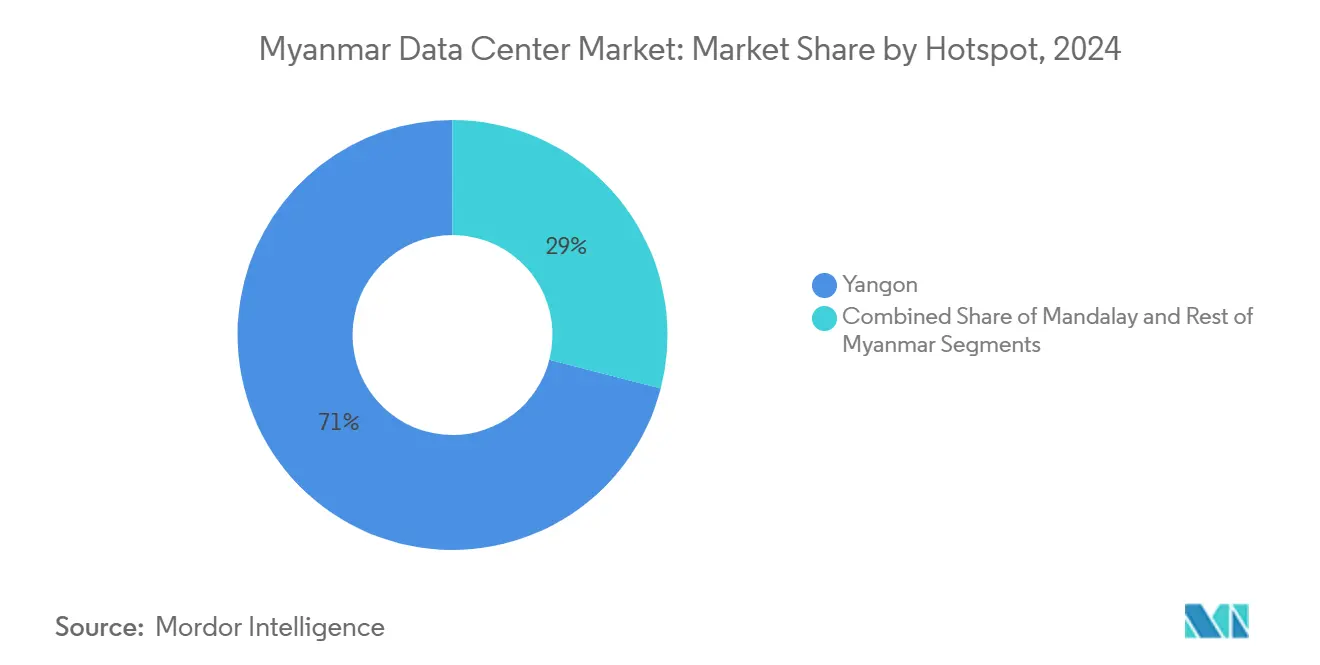

- By hotspot, Yangon led the Myanmar data center market with 71% of the market share in 2024, while Mandalay is forecast to expand at a 17.80% CAGR through 2030.

Myanmar Data Center Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government "Myanmar Digital Economy Roadmap 2025" funding | +3.20% | National, with early gains in Yangon, Mandalay | Medium term (2-4 years) |

| Surge in OTT/video streaming bandwidth demand | +2.80% | Urban centers, expanding to secondary cities | Short term (≤ 2 years) |

| Roll-out of 4G/5G towers by MNOs boosting edge nodes | +4.10% | National coverage with Yangon, Mandalay priority | Medium term (2-4 years) |

| Incoming ASEAN and China-Myanmar international fiber routes | +2.30% | Border regions and major cities | Long term (≥ 4 years) |

| Fast-growing fintech and mobile-money transactions | +3.70% | Urban and semi-urban areas | Short term (≤ 2 years) |

| Mandalay Technopark tax-holiday for Tier-III builds | +1.40% | Mandalay region specifically | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government Digital Economy Roadmap Accelerates Infrastructure Investment

The Ministry of Transport and Communication earmarks spectrum, tax incentives, and capacity-building funds that directly translate into higher demand for carrier-neutral white space in the Myanmar data center market. [1] International Trade Administration, “Burma – Digital Economy,” trade.gov Mandatory data-sovereignty rules introduced under the 2025 Cybersecurity Law compel local hosting of e-government and critical financial datasets. Digital ID enrollment of 37 million citizens feeds petabyte-scale storage requirements for biometric images and encryption keys. Ministries now run federated cloud sandboxes that pilot AI-based public service chatbots, raising compute density needs in Tier III rooms. Vendors positioning greenfield sites within the Thilawa SEZ secure seven-year income-tax holidays, which accelerate payback periods for high-capex builds.

5G Network Deployment Drives Edge Computing Expansion

ATOM’s partnership with ZTE to modernize BSS stacks highlights the increasing processing demands as massive-MIMO radios come online in Yangon and Mandalay. Peak download speeds of nearly 1 Gbps shorten last-mile bottlenecks and compel operators to deploy micro-data centers for radio-access-network caching. MPT’s fiber-to-the-home footprint, now covering half the country, provides the backhaul stability that hyperscalers require for content-delivery nodes.[2]Mobile World Live, “MPT Takes FTTH Footprint to Half of Myanmar,” mobileworldlive.com Latency-sensitive sectors, such as gaming and interactive retail, are beginning to migrate to colocation racks positioned close to 5G aggregation hubs, thereby expanding the Myanmar data center market in suburban districts. Antenna densification also propels power-density specifications upward, sparking interest in liquid-cooling retrofits.

Surge in OTT and Video-Streaming Bandwidth Demand

Daily streamed minutes on leading platforms climbed above 120 million in 2024, doubling rack-level throughput needs in operator-hosted caching farms. Content distributors cache high-definition and 4K files locally to avoid transit charges on international circuits, expanding the Myanmar data center market footprint in carrier hotels near cable landing sites. Rising creator-economy applications accelerate uplink traffic, necessitating symmetrical bandwidth and storage closer to source. Compression innovations temper bandwidth growth yet elevate compute cycles for real-time transcoding, boosting CPU-dense server orders. Advertisers adopt AI-based contextual ad-placement engines that draw on local data lakes, reinforcing domestic hosting obligations under emerging privacy codes.

Fintech Revolution Generates Unprecedented Data Processing Demands

KBZPay’s 6 million active wallets and USD 9 billion annual transaction value set a benchmark for payment data velocity. Fraud-detection engines now run multivariate anomaly scoring in sub-second windows, pushing banks to reserve contiguous racks for graphics-processing accelerators. CB Bank’s API-first architecture publishes more than 200 endpoints to ecosystem partners, amplifying concurrent-session counts into the tens of thousands. The Central Bank’s financial-inclusion roadmap channels donor funding into shared KYC utilities that must be hosted domestically, driving up colocation occupancy in Yangon. Capital-markets platforms eye real-time clearing, further stretching compute-latency budgets and underscoring the Myanmar data center market’s role in underpinning secure fintech scale-out.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic grid instability and reliance on diesel gensets | -4.80% | National, particularly severe in rural areas | Short term (≤ 2 years) |

| Capital-controls limiting foreign currency repatriation | -2.10% | National, affecting foreign investors | Medium term (2-4 years) |

| Scarcity of Uptime-accredited facility engineers | -1.90% | Urban centers with technical skill gaps | Long term (≥ 4 years) |

| Monsoon-season flood risk elevating site CAPEX | -1.70% | Coastal and river delta regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Power Grid Instability Constrains Operational Reliability

Available generation capacity fell by 2.5 GW between 2021 and 2024, limiting grid uptime in Yangon to as little as four hours per day during peak-load months. Data center operators therefore budget diesel fuel for nearly 60% of annual runtime, lifting OPEX and carbon intensity. Hydropower’s share, once 57%, declined as water levels receded, while LNG projects stalled under import-permit delays. Investors have reacted by specifying parallel medium-voltage feeds and on-site fuel storage sized for 72-hour autonomy, adding 6-8 percentage points to project capex. Although new emergency tenders aim to inject 1,072 MW by 2026, timelines remain uncertain, muting near-term growth in the Myanmar data center market.

Monsoon Flooding Risks Elevate Infrastructure Costs

Hydrological models based on three decades of Landsat data identify extensive flood plains around Yangon and Pathein, forcing developers toward costlier elevated sites [3]Frontiers in Environmental Science, “Operational Flood Risk Index Mapping for Disaster Risk Reduction Using Earth Observations,” frontiersin.org. Designs now incorporate 1.5 m raised floors, triple-layer drainage, and IP-rated switchgear, swelling build costs by up to 25%. Seasonal logistics disruptions complicate heavy-equipment delivery schedules and inflate insurance premiums. Operators introduce AI-enabled weather-alert dashboards that interface with emergency power-down protocols, yet residual risk drives financiers to demand higher covenants. While upstream mitigation programs are planned, they will take multiple monsoons to matter, sustaining caution among would-be entrants to the Myanmar data center market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User: Telecom Leadership Yields to Cloud Transformation

Telecommunications carriers retained 26% of Myanmar data center market share in 2024 as they internalized RAN aggregation, voicemail, and core-network packet functions. Yet, spectrum license fees cap their capex headroom, prompting partnerships with neutral-host providers that can absorb infrastructure costs. As OTT platforms poach SMS and voice revenue, carriers shift their focus to managed-hosting bundles, cross-connecting enterprise clients to public cloud availability zones.

Cloud service providers will dominate incremental demand, advancing at a 19.60% CAGR through 2030, as enterprise ERP, CRM, and analytics workloads migrate to the cloud. Early adopters in banking report 30% opex savings from cloud-native architectures, drawing peers into SaaS procurement cycles. The Myanmar data center market size for cloud tenants is expected to surpass telecom usage by 2028, if planned regional zones materialize. BFSI workloads require low-latency, in-country data stores to meet emerging privacy obligations, prompting banks to reserve entire suites in Yangon facilities. Manufacturing pilots around industrial IoT sensors buttress steady demand, particularly from export-oriented plants near the Chinese border.

By Hotspot: Yangon Dominance Faces Mandalay Challenge

Yangon commanded 71% of the Myanmar data center market share in 2024, supported by three international cable landing stations and the Thilawa SEZ’s seven-year tax holiday. The city’s concentration of banks, telecom headquarters, and government ministries ensures a baseline colocation demand and fosters peering density, which lowers transit costs for hyperscalers. However, land pricing has increased by more than 40% since 2022, and grid unreliability is prompting operators to adopt expensive dual-fuel gensets, thereby stretching PUE targets. Local councils are now tightening zoning permits, lengthening approval cycles for new buildings, and encouraging investors to explore secondary metropolitan areas.

Mandalay’s emergence reshapes the Myanmar data center market, as its Zone 2 tax incentives shorten breakeven horizons while real estate costs remain 30% below Yangon’s average. The Myanmar data center market size for Mandalay is projected to triple by 2030, growing at a 17.80% CAGR, aided by smart-city pilots showcasing fiber-optic street furniture and municipal Wi-Fi. Centrally located within the national fiber grid, Mandalay enables latency-balanced traffic routing between northern trade corridors and Yangon. Operators exploit cheaper hydro availability from Upper Yeywa to meet green-energy objectives, although evacuation-line stability remains an open issue. Smaller Tier-II towns now vie for micro-edge pods, but clear anchor tenants are yet to crystallize.

Geography Analysis

Yangon’s dominance stems from its robust subsea connectivity, including SEA-ME-WE 5, AAE-1, and the impending MIST system, which provides more than 24 Tbps of total design capacity and anchors the bulk of current hyperscale interest. The city hosts an estimated 20 carrier meet-me rooms, easing peering for cloud on-ramps and CDN nodes. Nevertheless, diesel reliance pushes average PUE toward 1.9, well above regional peers, underscoring operational-cost headwinds for the Myanmar data center market. Thilawa’s customs-duty relief further incentivizes equipment imports, but urban congestion extends fiber-laying permits past six months.

Mandalay enjoys a strategic centrality, linking the northern jade-mining belts, eastern Shan trade routes, and the populous Ayeyarwady Basin. The municipal government bankrolls fiber backbones that interconnect industrial parks, delivering sub-10 ms round-trip latency to most regional gateways. Smart-city proofs-of-concept showcase real-time traffic control and public Wi-Fi, feeding local edge-compute deployments. Land parcels average USD 40 per square meter, compared with USD 65 in Yangon, which lowers entry barriers for the Myanmar data center market. Grid power draws from hydropower in Upper Yeywa and solar farms in Kyaukse, opening possibilities for renewable PPAs despite network-stability caveats.

The Rest-of-Myanmar cluster is nascent yet promising. MPT’s FTTH expansion to half the country extends the backbone to secondary cities such as Bago and Mawlamyine, creating initial demand for micro-pods. Government electrification targets envisage universal access by 2030, unlocking potential for rural edge caching that serves e-commerce and e-learning platforms. Border towns tied to China’s digital-silk-road corridors secure terrestrial fiber-loop resilience, positioning them as fail-over sites for the Myanmar data center market. However, monsoon-season logistics and skills shortages temper near-term rollout scale.

Competitive Landscape

The Myanmar data center market remains fragmented, with no single operator exceeding a 15% footprint. Local incumbents, such as ATOM Myanmar and KBZ Gateway, leverage their spectrum assets and banking relationships to cross-sell co-location services; however, capital constraints limit the scaling of multi-megawatt services. International entrants NTT Ltd, Digital Edge, and EdgeConneX adopt hub-and-spoke models, pairing core campuses in Singapore or Johor with edge builds inside Myanmar to capture latency-sensitive loads.

Digital Edge’s USD 1.6 billion funding round in January 2025 underwrites the development of a 10 MW phased campus in Yangon, featuring hybrid super-capacitor energy storage that mitigates grid volatility. NTT’s edge strategy hinges on integrating its MIST cable landing site with an envisioned Tier IV data center, creating a low-latency path to Chennai and Singapore. EdgeConneX’s Jakarta expansion signals appetite for contiguous ASEAN coverage, enabling customers to replicate workloads across multiple fault domains.

Sustainability differentiators surface as competitive levers. Digital Edge secured Platinum Ecovadis certification in 2024, while NTT pilots immersion-cooling rigs that claim 30% energy savings. Local operators explore rooftop solar hybrids, yet financing remains difficult because lenders demand sovereign-risk premiums. The path toward consolidation will accelerate as greenfield projects scale beyond local funding capacity; minority stake sales to regional infrastructure funds have already begun.

Myanmar Data Center Industry Leaders

KBZ Gateway Co. Ltd.

ATOM Myanmar

Myanmar Posts & Telecommunications (MPT)

Mytel

Ooredoo Myanmar

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Digital Edge Holdings raised more than USD 1.6 billion to fund continued platform expansion across Asia.

- January 2025: NTT DATA earmarked over USD 10 billion for global data-center builds, including a 68.5-acre campus in Johor Bahru, Malaysia.

- January 2025: AWS launched the Asia Pacific (Thailand) Region, pledging USD 5 billion investment that strengthens regional cloud spill-over into Myanmar.

- January 2025: Myanmar enacted the Cybersecurity Law (State Administration Council Law No 1/2025), outlining duties for critical information-infrastructure operators.

- December 2024: EdgeConneX acquired 45,000 sqm in Bekasi, lifting its Jakarta hyperscale campus to more than 200 MW.

Myanmar Data Center Market Report Scope

The Myanmar Data Center Market is Segmented by End-User (BFSI, Cloud Service Providers, E-Commerce, Government, Manufacturing, Media and Entertainment, Telecom, and Other End-Users), and Hotspot (Yangon, Mandalay, and Rest of Myanmar). The Market Forecasts are Provided in Terms of Volume (MW Capacity).

| BFSI |

| Cloud Service Providers |

| E-Commerce |

| Government |

| Manufacturing |

| Media and Entertainment |

| Telecom |

| Other End-Users |

| Yangon |

| Mandalay |

| Rest of Myanmar |

| By End-User | BFSI |

| Cloud Service Providers | |

| E-Commerce | |

| Government | |

| Manufacturing | |

| Media and Entertainment | |

| Telecom | |

| Other End-Users | |

| By Hotspot | Yangon |

| Mandalay | |

| Rest of Myanmar |

Key Questions Answered in the Report

How big will the Myanmar data center market be by 2030?

Installed IT load is projected to reach 3.56 MW in 2030, growing at an 18.87% CAGR from the 2025 base of 1.5 MW.

Which city is attracting the most new data center builds?

Yangon still captures 71% current share, but Mandalay is expanding fastest, growing at 17.80% CAGR through 2030 as tax incentives and lower land costs lure developers.

Which customer group is driving the next wave of capacity demand?

Cloud service providers are the fastest-growing end-user segment, advancing at 19.60% CAGR as local enterprises adopt cloud-first strategies.

What is the biggest operational hurdle for data center operators in Myanmar?

Chronic grid instability forces facilities to rely heavily on diesel generation, adding cost and complicating sustainability targets.

How does new submarine cable capacity affect Myanmar’s digital economy?

Systems such as the MIST cable lower latency to Singapore and India, enabling domestic facilities to serve cross-border workloads and boosting foreign investment interest.

What regulatory change should investors monitor?

The 2025 Cybersecurity Law introduces data-sovereignty and critical-infrastructure protection duties that will shape facility design and compliance spending.

Page last updated on: