Multilayer Varistor Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

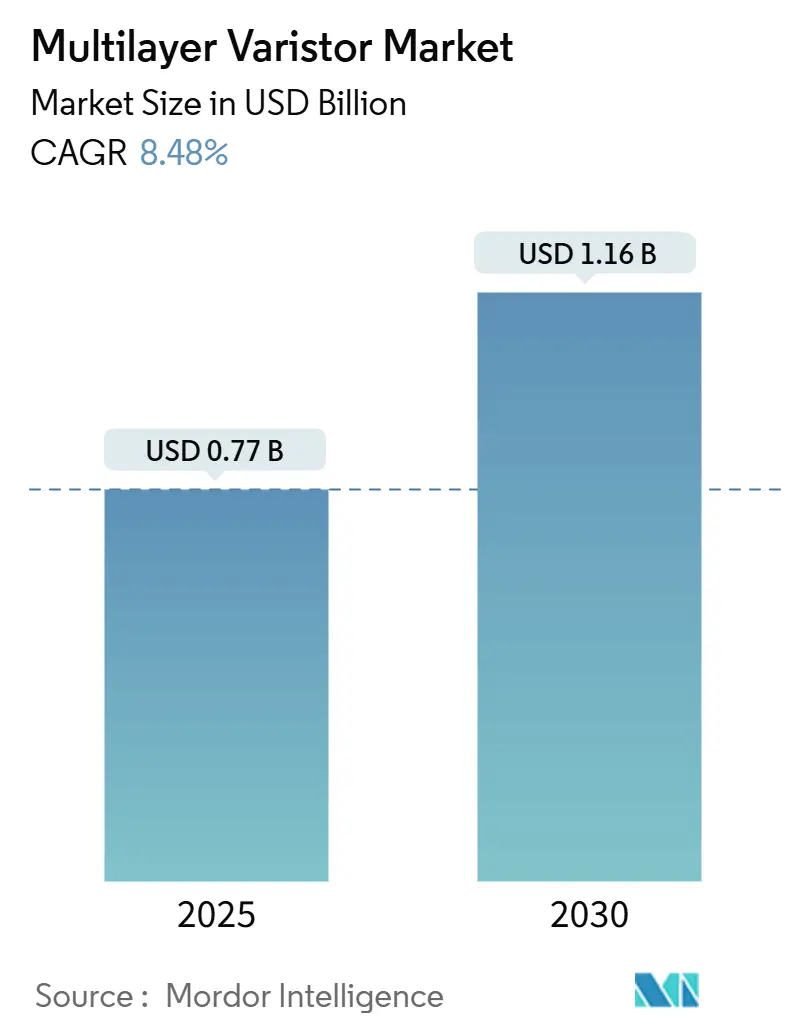

| Market Size (2025) | USD 0.77 Billion |

| Market Size (2030) | USD 1.16 Billion |

| Growth Rate (2025 - 2030) | 8.48% CAGR |

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Multilayer Varistor Market Analysis by Mordor Intelligence

The multilayer varistor market size is valued at USD 0.77 billion in 2025 and is projected to reach USD 1.16 billion by 2030, progressing at an 8.48% CAGR. Robust demand comes from 5G macro-cell deployments, battery electric vehicle (BEV) domain controllers, and edge-computing gateways that all embed high-density surge suppression. The ability of multilayer architectures to squeeze dozens of ceramic layers into sub-millimeter footprints enables designers to protect high-speed circuits without sacrificing board area, thereby setting them apart from legacy disk devices. Medium-voltage parts continue to anchor industrial and telecom designs, while low-voltage variants accelerate within wearables, where always-on radios increase electrostatic discharge (ESD) risks. Meanwhile, chip arrays that combine many varistor elements in a single package are advancing quickest because automotive programs now specify array-based protection for Ethernet backbones and sensor fusion modules. Competitive intensity remains elevated: Japanese incumbents control ceramic powders and patents, whereas Chinese rivals leverage lower labor costs to contest commodity-grade products. Together, these forces generate durable tailwinds for the multilayer varistor market as circuit densities increase and regulatory standards become more stringent.

Key Report Takeaways

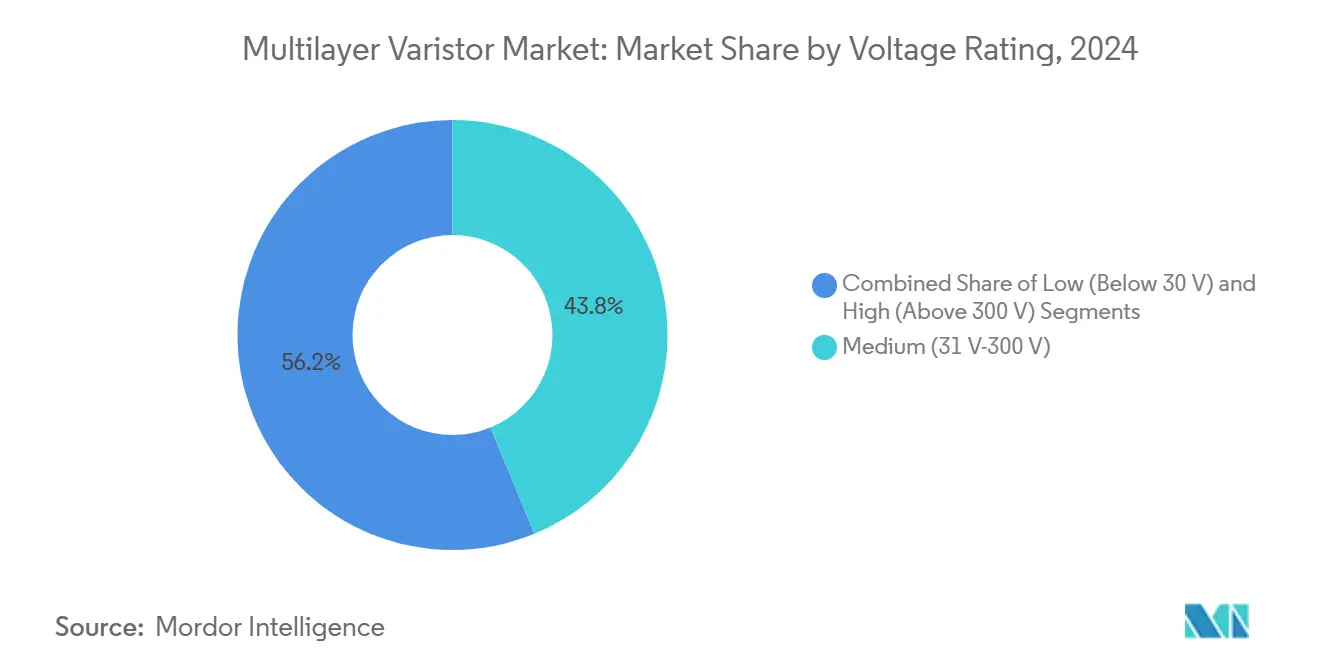

- By voltage rating, the medium band accounted for 43.78% market share of the multilayer varistor market in 2024, while the low-voltage tier is expected to grow at a 9.23% CAGR through 2030.

- By package type, surface-mount devices led with a 48.19% market share of the multilayer varistor market in 2024, whereas chip arrays are forecast to advance at a 9.19% CAGR through 2030.

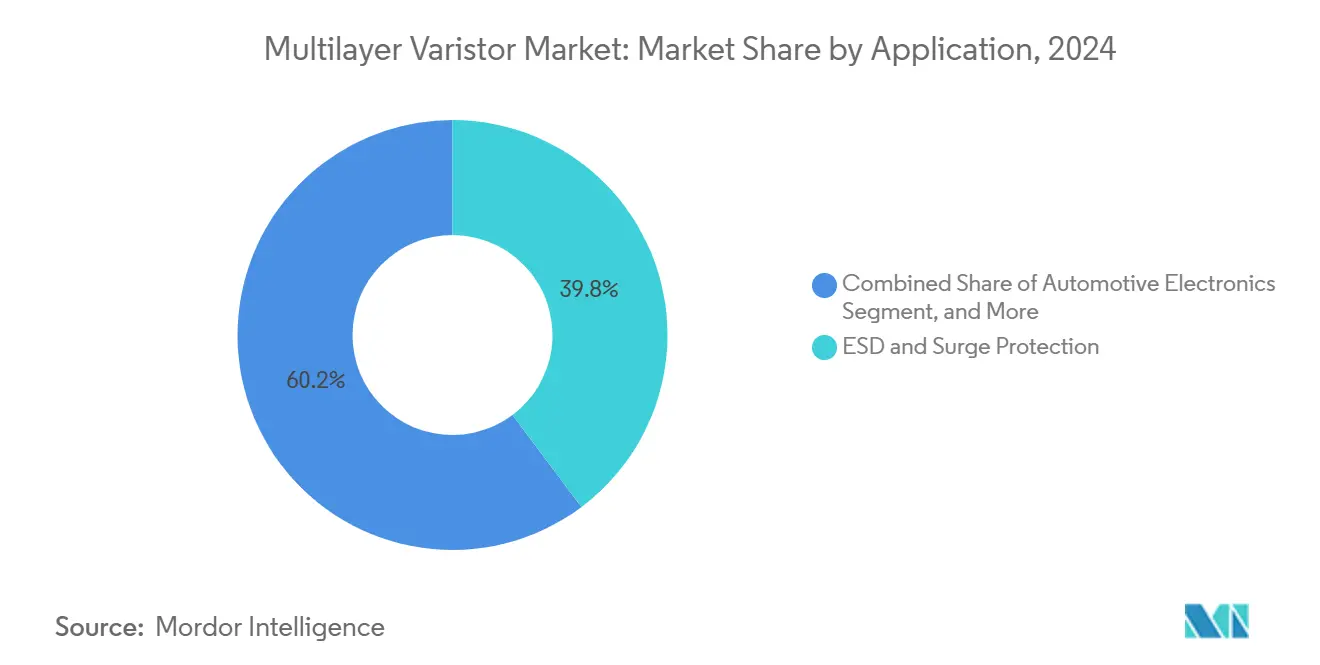

- By application, ESD and surge protection accounted for 39.76% market share of the multilayer varistor market in 2024, automotive electronics are projected to register the highest CAGR at 9.31% during 2025-2030.

- By end-user industry, consumer electronics commanded a 42.67% share in 2024; however, the automotive sector is poised to expand at a 9.37% CAGR through 2030.

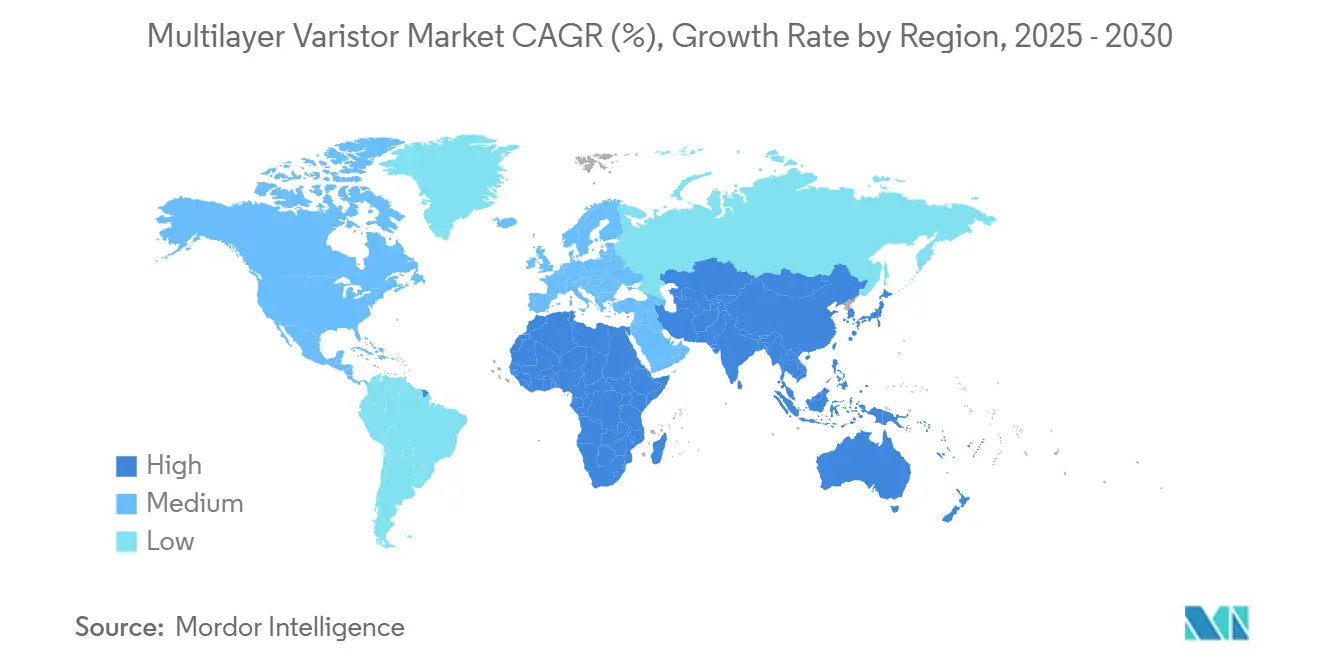

- By geography, Asia-Pacific captured 49.76% of 2024 revenue, but the Middle East is projected to deliver a 9.44% CAGR to 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Multilayer Varistor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating 5G Infrastructure Roll-Out | +1.8% | Global, with Asia-Pacific and North America leading deployment density | Medium term (2-4 years) |

| Increasing On-Board Electronics in Electric Vehicles | +2.1% | North America, Europe, China | Long term (≥4 years) |

| Surge in IoT Edge Devices Demanding Surge Protection | +1.5% | Germany, Japan, South Korea | Medium term (2-4 years) |

| Government Mandates on Grid Stability Equipment | +1.2% | Middle East, South America, India | Long term (≥4 years) |

| Miniaturization Trend in Wearable Electronics | +0.9% | North America, Europe, Asia-Pacific | Short term (≤2 years) |

| Adoption of SiC and GaN Power Devices Driving Peripheral Protection Components | +1.4% | Global automotive and renewable segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerating 5G Infrastructure Roll-Out

Telecom operators activated more than 1.7 million 5G base stations in 2024, and each macro cell can house up to 16 remote radio heads that are susceptible to lightning-induced surges exceeding 2 kV. Multilayer varistors rated 275 V-300 V are used because their capacitance above 50 pF helps prevent signal loss at gigahertz frequencies. Open RAN architectures further fragment equipment into distributed units, thereby multiplying the number of local protection points. Mandatory compliance with IEC 61000-4-5 ensures a recurring demand for these devices as carriers densify their networks to achieve sub-100 ms latency targets.[1]International Electrotechnical Commission, “IEC 61000-4-5,” webstore.iec.ch

Increasing On-Board Electronics in Electric Vehicles

BEVs now contain roughly USD 1,200 of semiconductor content per unit, up 26% from 2022. Each traction inverter and high-voltage DC-DC converter integrates multilayer varistors on gate-drive circuits to tame 1,500 V spikes that appear in under 10 ns. Automotive-grade parts must withstand 2,000 thermal cycles between -40 °C and 150 °C, as specified in AEC-Q200, thereby limiting the qualified supplier pool.[2]International Organization for Standardization, “ISO 26262,” iso.org European safety regulations that mandate advanced driver-assistance features magnify the varistor count per vehicle and lift the multilayer varistor market.

Surge in IoT Edge Devices Demanding Surge Protection

Industrial IoT deployments surpassed 14.2 billion nodes in 2024. Edge controllers are situated beside motors and solenoids that generate recurring transients, so designers embed 24 V-48 V multilayer varistors on sensor boards to meet IEC 61131-2 durability guidelines. The rise of single-pair Ethernet (IEEE 802.3cg) merges power and data over the same twisted pair, sharpening the need for asymmetric clamping solutions.[3]IEEE Standards Association, “IEEE 802.3cg-2019,” standards.ieee.org

Adoption of SiC and GaN Power Devices Driving Peripheral Protection Components

Shipments of silicon carbide and gallium nitride power semiconductors rose 38% year-on-year to 45 million units in 2024. Their high dv/dt switching introduces gate-oxide threats that multilayer varistors rated 30 V-50 V now handle inside power modules. Leading suppliers have filed patents on low-capacitance stacks with capacitance below 10 pF to avoid gate-charge penalties, underscoring the momentum behind the multilayer varistor market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply Chain Disruptions in High-Purity ZnO Powders | -0.7% | Global, acute in China-dependent chains | Short term (≤2 years) |

| Rising Competition from TVS Diodes in Low-Voltage Designs | -0.6% | North America and Europe | Medium term (2-4 years) |

| Intensifying Price Competition in Consumer-Grade Segments | -0.5% | Asia-Pacific and global consumer-electronics hubs | Short term (≤2 years) |

| Lengthy Automotive and Industrial Qualification Cycles | -0.4% | Global, centered on North America and Europe | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Supply Chain Disruptions in High-Purity ZnO Powders

Environmental audits shut down 12 secondary zinc smelters in China in 2024, driving varistor-grade ZnO spot prices up by 18%. Alternative supplies in Australia and Peru require additional calcination steps, which inflate costs and slows response times. Attempting to use lower-purity feedstock cuts energy-absorption capability by up to 20%, jeopardizing IEC 61051-1 compliance. Limited greenfield capacity will keep this restraint active through 2026.

Rising Competition from TVS Diodes in Low-Voltage Designs

Transient voltage suppressor diodes already captured 28% of the Low-Voltage circuit-protection demand in 2024. Their picosecond clamping outpaces varistors by an order of magnitude, making them appealing for high-frequency USB Power Delivery and GaN charger designs. Price gaps narrowed to under USD 0.05 per unit, forcing varistor suppliers to build hybrid arrays that spike bills of material by roughly 25%. The competitive drag is most pronounced in consumer electronics, where refresh cycles are rapid and price sensitivity is high.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Voltage Rating: Low-Voltage Tier Gains from Wearable Proliferation

The medium band retained 43.78% share in 2024, reflecting entrenched use on 48 V and 120 V rails. Yet the low-voltage slice accelerates at a 9.23% CAGR as connected wearables embed more radios and sensors, pushing the multilayer varistor market size for ≤30 V parts higher year after year. Designers specify a 10% clamping tolerance to avoid false trips during wireless charging events. High-voltage components above 300 V remain niche in photovoltaic inverters, although 800 V BEV platforms will spur gradual uptake post-2027.

Growth in the low-voltage tier benefits from single-digit capacitance levels that safeguard USB 4.0 and Thunderbolt 5 lines without degrading high-speed eye diagrams. Meanwhile, medium-voltage dominance endures because UL 1449 Type 3 surge-protective standards anchor procurement around 120 V and 240 V North American mains. This mix ensures robust momentum for the multilayer varistor market.

By Package Type: Chip Arrays Capture Automotive Design Wins

Surface-mount devices led 2024 shipments at 48.19%, but chip arrays are forecast to outpace with a 9.19% CAGR through 2030 as automotive Ethernet nodes migrate to array-based solutions. A 3 mm × 3 mm package housing 32 elements replaces 16 discrete varistors, trimming placement time by 60%. This configuration raises the multilayer varistor market share for arrays within the automotive supply chain.

Leaded radial parts linger in retrofit industrial gear; however, original equipment designs are shifting toward reflow-friendly footprints that fit automated lines. Early system-in-package prototypes even embed varistor arrays beside processors, a trend that broadens the multilayer varistor market envelope and tightens integration between protection and logic dies.

By Application: Automotive Electronics Overtakes Consumer Demand Trajectory

ESD and surge ports accounted for 39.76% of 2024 demand, but automotive electronics are expected to grow at a rate of 9.31% annually as vehicles transition from 70 to more than 120 electronic control units. Each camera module, battery-cell monitor, and inverter gate drive requires multiple varistors, thereby increasing the multilayer varistor market size embedded in vehicles. Higher automotive-grade pricing also enriches supplier margins.

Consumer applications plateau as smartphone refresh intervals lengthen, yet remain vital because flagship phones often dictate reference designs for mid-tier devices. Power-supply circuits stay steady inside data centers, while telecom small-cell nodes require fewer varistors per site, tempering volume offsets. The automotive ascent thus realigns overall market growth vectors toward long-lifecycle, qualification-heavy programs.

By End-User Industry: Automotive Sector Reshapes Demand Profile

Consumer electronics accounted for 42.67% of 2024 revenue, but automotive units are projected to grow at a 9.37% CAGR, further solidifying their increasing influence on the multilayer varistor market. Electric vehicles carry up to 220 varistors, versus 80 in combustion cars, which multiplies the dollar content threefold. Industrial equipment follows factory-automation capex cycles, while renewable energy inverters consume high-voltage parts tied to global capacity additions.

Automotive contracts, typically lasting five to seven years, provide revenue visibility that is often lacking in consumer electronics. The shift also forces suppliers to maintain AEC-Q200 laboratories, favoring incumbents with deep materials expertise. Together, these trends reposition the multilayer varistor industry toward high-reliability users over short-cycle gadgets.

Geography Analysis

Asia-Pacific secured 49.76% of 2024 turnover thanks to China’s smartphone and BEV manufacturing clout. Japan’s tier-1 automotive suppliers and South Korea’s semiconductor-equipment makers add specialized demand. Production-linked incentives are encouraging some smartphone assembly to shift toward India, yet ceramic powders still originate largely from Chinese provinces, leaving the multilayer varistor market vulnerable to regional concentration risks.

North America and Europe combine for roughly 35% of global revenue. The United States relies on multilayer varistors to protect 48 V server racks and BEV battery packs, while Europe’s software-defined vehicle push inserts more protection devices into centralized compute domains. Strict EMC and UL test requirements extend qualification timelines, but also shield entrenched suppliers.

The Middle East is forecast to grow at a rate of 9.44% per year as Saudi Arabia and the United Arab Emirates modernize their grids and install distributed solar plants that require surge suppression under IEC 61643-11. South America advances on wind-energy builds in Brazil, and Africa registers smaller but strategic demand pockets around mining and telecom infrastructure. This mosaic guarantees geographic diversity for the multilayer varistor market even as Asia remains the production nucleus.

Competitive Landscape

Global supply is moderately concentrated, with the top five vendors, TDK, Murata, Panasonic, Vishay, and Littelfuse, holding a roughly 60% share in 2024. Japanese firms dominate automotive-grade segments through vertically integrated ceramic lines and decades-long tier-1 relationships, while Chinese and Taiwanese challengers target consumer grades on cost. Hybrid arrays that combine TVS diodes and varistors, along with patent filings on sub-10 pF stacks, represent key differentiating factors.

Transient voltage suppressor diode makers are encroaching on low-voltage niches, compelling varistor suppliers to co-develop mixed-technology solutions. Automotive and industrial functional-safety standards create multi-year entry barriers; still, regional content rules in China and India reward local competitors. Raw-material integration continues as a hedge against ZnO volatility, exemplified by Vishay’s 2024 acquisition of a Taiwanese powder producer.

Emerging opportunities include electric-vehicle wireless charging pads, satellite terminals that face -55 °C to 125 °C swings, and system-in-package designs that incorporate varistor layers within substrates. Smaller entrants, such as Amotech and Fenghua Advanced, gain market share with application-specific chip arrays that bundle common-mode chokes, reflecting the evolution of the multilayer varistor market toward multifunctional protection blocks.

Multilayer Varistor Industry Leaders

TDK Corporation

Murata Manufacturing Co., Ltd.

Panasonic Holdings Corporation

Vishay Intertechnology, Inc.

KOA Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Littelfuse signed a five-year supply agreement valued at USD 95 million to deliver chip-array varistors for a U.S. electric vehicle maker’s next-generation 800 V traction inverter program.

- June 2025: TDK inaugurated a dedicated R and D center in Munich focused on developing sub-5 pF automotive varistor arrays tailored for 800 V battery electric vehicle platforms.

- April 2025: Panasonic Holdings commissioned a pilot line in Niigata, Japan to produce automotive-grade high-purity ZnO powder, reducing its reliance on imports from China by an estimated 30%.

- February 2025: Murata Manufacturing began volume production of embedded multilayer varistor substrates at its Okayama facility, enabling 5G smartphone makers to eliminate discrete protection components.

Global Multilayer Varistor Market Report Scope

The Multilayer Varistor Market Report is Segmented by Voltage Rating (Low, Medium, High), Package Type (Surface-Mount Device, Leaded Radial, Chip Arrays), Application (ESD and Surge Protection, Power Supply Circuits, Automotive Electronics, Telecom Equipment), End-User Industry (Consumer Electronics, Automotive, Industrial Equipment, Energy and Power), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

| Low (Below 30 V) |

| Medium (31 V-300 V) |

| High (Above 300 V) |

| Surface-Mount Device (SMD) |

| Leaded Radial |

| Chip Arrays |

| ESD and Surge Protection |

| Power Supply Circuits |

| Automotive Electronics |

| Telecom Equipment |

| Consumer Electronics |

| Automotive |

| Industrial Equipment |

| Energy and Power |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Voltage Rating | Low (Below 30 V) | ||

| Medium (31 V-300 V) | |||

| High (Above 300 V) | |||

| By Package Type | Surface-Mount Device (SMD) | ||

| Leaded Radial | |||

| Chip Arrays | |||

| By Application | ESD and Surge Protection | ||

| Power Supply Circuits | |||

| Automotive Electronics | |||

| Telecom Equipment | |||

| By End-User Industry | Consumer Electronics | ||

| Automotive | |||

| Industrial Equipment | |||

| Energy and Power | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current value of the multilayer varistor market?

The market stands at USD 0.77 billion in 2025 and is forecast to hit USD 1.16 billion by 2030.

Which end-user segment is growing fastest?

Automotive electronics is projected to expand at a 9.37% CAGR through 2030 due to the rising electronic content in battery electric vehicles.

Why are chip-array packages gaining popularity?

Chip arrays consolidate many protection points in one surface-mount device, shrinking board area and improving assembly reliability, a key need in automotive Ethernet and sensor modules.

How do supply chain disruptions affect varistor manufacturers?

High-purity ZnO shortages raise material costs and threaten energy-absorption performance, pressuring margins until new capacity comes online.

Which region is expected to lead growth to 2030?

The Middle East is projected to log a 9.44% CAGR, driven by smart-grid and solar-inverter installations that mandate surge protection compliance.

What differentiates multilayer varistors from TVS diodes?

Varistors absorb higher surge energy and suit a broad voltage range, while TVS diodes clamp faster, making hybrids popular in premium USB and GaN charger designs.

Page last updated on: