Multi-Agent Enterprise Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

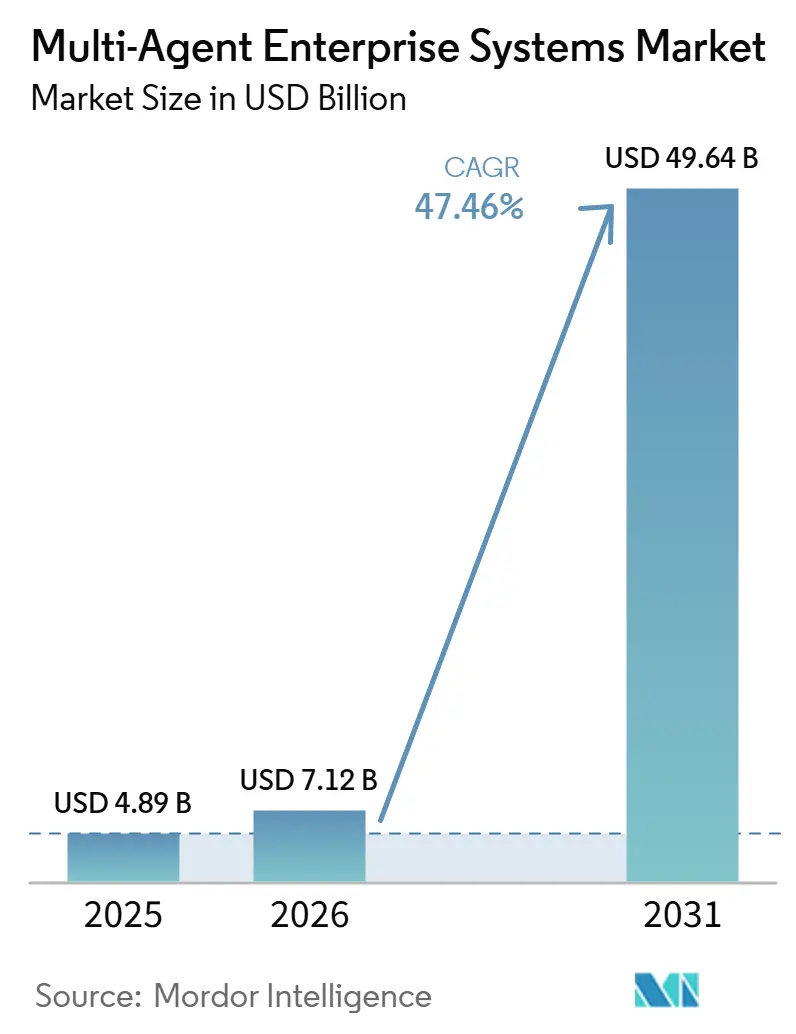

| Market Size (2026) | USD 7.12 Billion |

| Market Size (2031) | USD 49.64 Billion |

| Growth Rate (2026 - 2031) | 47.46% CAGR |

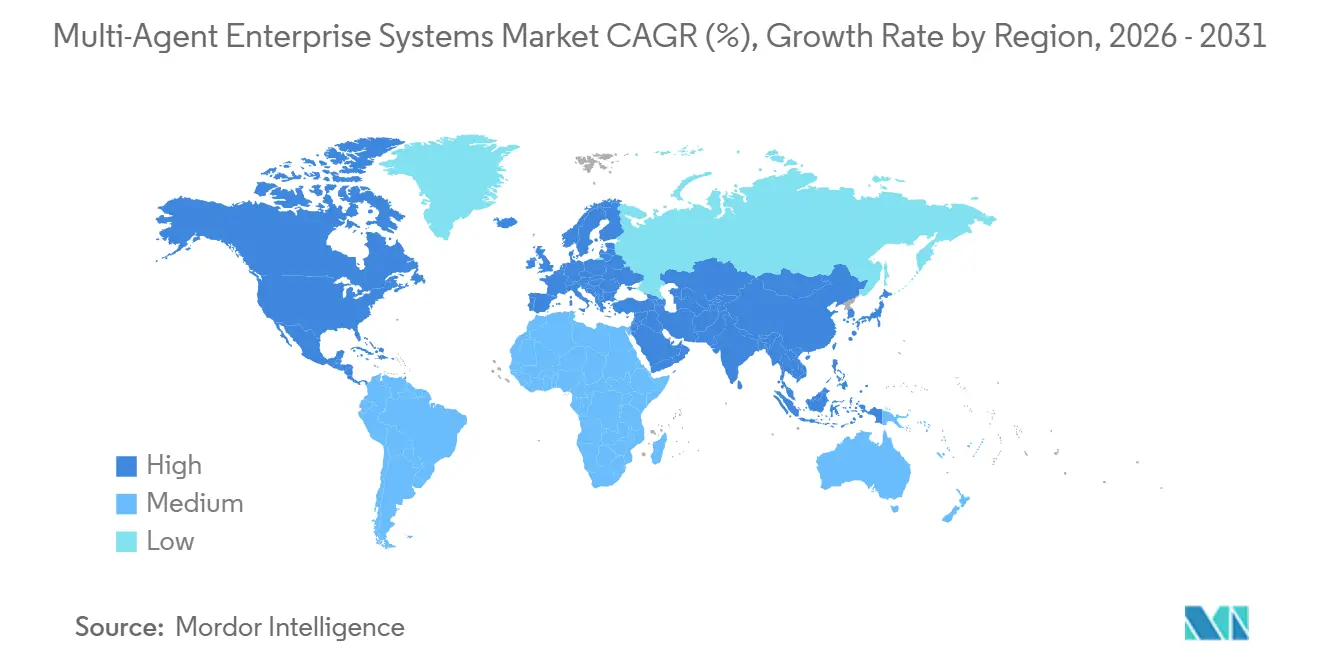

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Multi-Agent Enterprise Systems Market Analysis by Mordor Intelligence

The Multi-Agent Enterprise Resource Planning market size is projected to expand from USD 4.89 billion in 2025 and USD 7.12 billion in 2026 to USD 49.64 billion by 2031, registering a CAGR of 47.46% between 2026 and 2031. Growing preference for distributed agent ecosystems over monolithic ERP stacks is accelerating adoption, as enterprises seek autonomous coordination across finance, supply chain, and customer-facing workflows. The commercialization of open-source orchestration frameworks, the maturation of hyperscaler platforms, and rapid advances in generative AI reasoning have moved multi-agent systems from pilot experiments into business-critical infrastructure. Buyers now emphasize cost-to-serve, resilience, and time-to-value, prompting vendors to deliver consumption-priced cloud services, pre-built agent libraries, and low-code development studios. Although regulatory clarity remains uneven, jurisdictions with risk-based frameworks are pulling ahead in production rollouts, creating regional growth asymmetries.

Key Report Takeaways

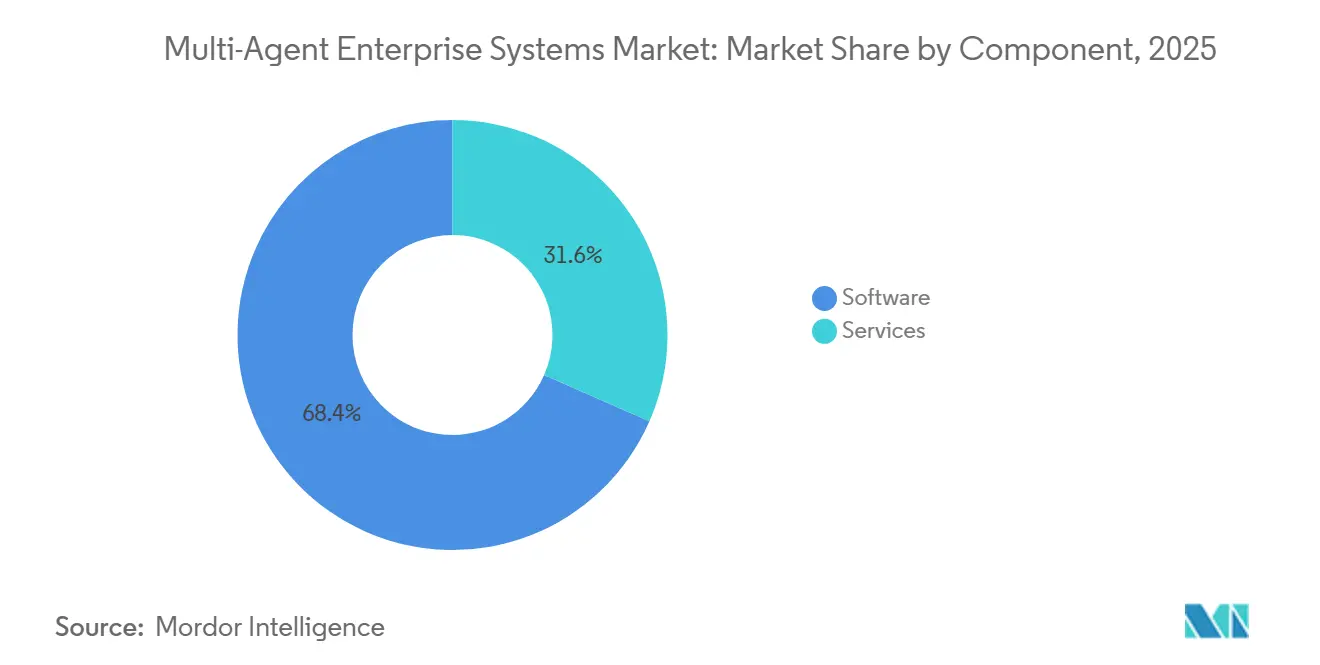

- By component, Software led with 68.43% revenue share in 2025, while Services are projected to grow at a 47.86% CAGR through 2031.

- By deployment mode, Cloud captured 61.32% of the Multi-Agent Enterprise Resource Planning market share in 2025; Hybrid architectures record the fastest projected CAGR at 48.06% through 2031.

- By application, Customer Service Automation accounted for 29.74% of 2025 revenue, whereas Legal and Compliance Automation is forecast to expand at a 48.46% CAGR through 2031.

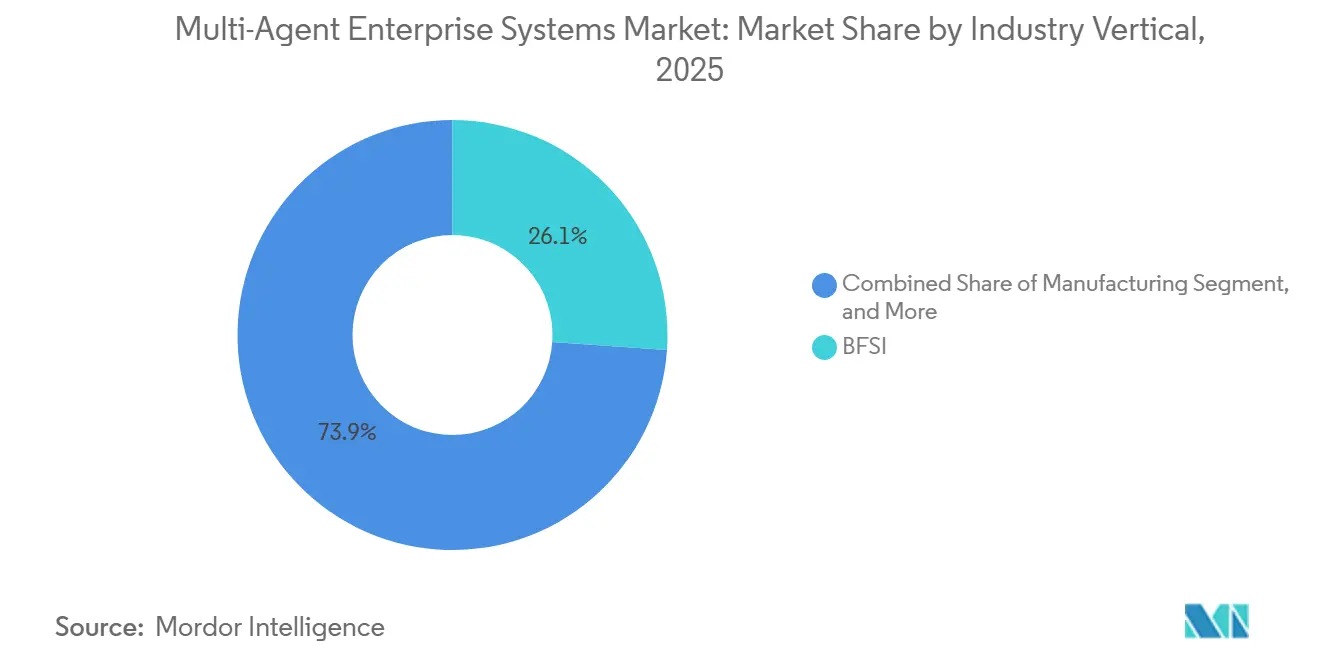

- By industry vertical, Banking, Financial Services, and Insurance commanded 26.11% share in 2025; Healthcare is advancing at a 48.66% CAGR through 2031.

- By enterprise size, Large Enterprises accounted for 64.53% of 2025 demand, while Small and Medium Enterprises show a 47.67% CAGR outlook to 2031.

- By geography, North America accounted for 38.49% of revenue in 2025, yet Asia-Pacific is on track for the highest CAGR of 48.82% between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Multi-Agent Enterprise Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated Enterprise Hyper-Automation Mandates | +12.3% | Global, strongest in North America and Europe | Short term (≤ 2 years) |

| Convergence of Generative AI with Multi-Agent Orchestration | +11.8% | Global technology hubs across three major regions | Medium term (2-4 years) |

| Expansion of Cloud-Native Agent Platforms by Hyperscalers | +9.7% | North America, Western Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Rapid Growth in Open-Source Frameworks such as LangChain, AutoGen, CrewAI | +7.4% | Developer communities worldwide, notably India | Short term (≤ 2 years) |

| Integration of Multi-Agent Systems into Industrial IoT for Smart Manufacturing | +6.9% | Asia-Pacific core with global spillover | Long term (≥ 4 years) |

| Emerging Agent Marketplaces Enabling SME Adoption | +5.2% | Asia-Pacific and South America SMEs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerated Enterprise Hyper-Automation Mandates

Corporate boards are mandating end-to-end digital execution to release labor for higher-value tasks, and multi-agent orchestration is central to that objective. IBM documented a 75% cut in accounts-payable cycle time and USD 5.7 million in yearly savings for firms adopting its watsonx Orchestrate agents.[1]IBM Newsroom, “IBM Unveils watsonx Orchestrate Agent Catalog,” ibm.com Agentic automation surpasses robotic process automation by reasoning over unstructured inputs and adapting to exceptions, turning regulatory document review, audit preparation, and customer dispute resolution into straight-through processes. Sectors facing margin compression, retail, logistics, and business-process outsourcing, show the highest urgency, funneling budget from legacy workflow tools into agent programs. The economic payback period now averages under 12 months for well-scoped finance or procurement pilots, fueling management confidence to expand rollouts. Governments encouraging productivity gains to offset labor shortages, particularly in Japan and Germany, further amplify near-term demand.

Convergence of Generative AI with Multi-Agent Orchestration

Large language models evolved from single-turn chat to goal-directed agents that plan, call tools, and self-correct, creating a universal interface for enterprise data. OpenAI’s February 2026 pact with Amazon Bedrock embeds its models natively inside AWS, trimming latency and compliance overhead for cross-cloud data movement. SAP’s Joule Studio lets business analysts chain agents to ERP records with drag-and-drop widgets, widening the talent pool beyond data scientists.[2]SAP News Center, “SAP Launches Joule Studio,” sap.com Multimodal models that parse text, code, images, and tables now generate SQL, craft emails, and trigger invoices from a single prompt, collapsing user training curves. Nonetheless, probabilistic outputs still raise reliability flags in finance and healthcare, so many deployments insert human checkpoints or deterministic fallback rules. Vendors are prioritizing guardrail APIs, policy engines, and verifiable execution logs to address those risks and accelerate adoption in heavily regulated domains.

Expansion of Cloud-Native Agent Platforms by Hyperscalers

Hyperscalers package template agents, vector databases, and governance tooling into fully managed suites, shrinking deployment cycles from months to weeks. Microsoft Azure AI Studio ships role-based agent blueprints and monitors token spend in real time. AWS Bedrock allows customers to swap underlying models without recoding workflow logic, preventing hard vendor lock-in while still anchoring workloads on AWS infrastructure. Google Cloud’s Vertex AI Agent Builder integrates with BigQuery and Looker, enabling data teams to orchestrate analytics, reporting, and knowledge-base updates through conversational agents. These platforms commoditize infrastructure, moving competitive advantage to pre-trained domain agents, curated data connectors, and partner marketplaces. Strategic alliances, such as ServiceNow leveraging NVIDIA NIM microservices for low-latency inference, underscore the race to differentiate on performance and ecosystem depth.

Rapid Growth in Open-Source Frameworks Such as LangChain, AutoGen, CrewAI

Open-source toolkits exploded in popularity because they give engineering teams fine-grained control and escape-hatch flexibility. LangChain has become the default for chaining model calls, tool invocations, and memory modules in Python, while AutoGen emphasizes conversational multi-agent collaboration and CrewAI applies role-based coordination to enterprise workflows. Contributors share patterns weekly, shortening experimentation loops and diffusing best practices globally. Enterprises often prototype internally on open-source stacks before migrating to supported commercial versions for production, in line with service-level agreements. Hybrid deployments run open-source orchestration as a control plane, with managed inference, observability, and security provided by a commercial substrate. This layered architecture optimizes both cost and agility, though firms must still allocate resources to patch management and to managing community-driven roadmap volatility.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack of Interoperability Standards Across Agent Frameworks | -4.8% | Multi-vendor environments worldwide | Short term (≤ 2 years) |

| Scarcity of Skilled Agent-Engineering Talent | -4.2% | Major technology hubs in three regions | Medium term (2-4 years) |

| Escalating API and Compute Costs for Multi-Agent Workloads | -3.6% | Cost-sensitive SMEs and emerging markets | Short term (≤ 2 years) |

| Regulatory Uncertainty Around Autonomous Decision-Making | -2.9% | Europe strictest, U.S. and Asia-Pacific evolving | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Lack of Interoperability Standards Across Agent Frameworks

Enterprises wrestling with LangChain, AutoGen, and CrewAI discover that agents cannot readily communicate with one another without custom bridges. Anthropic proposed the Model Context Protocol in November 2024 to create a universal message format, but competing draft standards threaten to splinter adoption. Fragmentation forces IT teams to standardize on a single stack or to fund bespoke translation layers, both of which raise costs and latency. Hybrid-cloud rollouts heighten complexity because on-premise agents face firewall, authentication, and data-residency constraints when coordinating with cloud peers. Standards bodies such as IEEE and ISO have not yet finalized technical specifications, so CIOs remain cautious about multi-vendor compositions for business-critical workflows. This friction dampens near-term scaling and tempers otherwise aggressive investment roadmaps.

Scarcity of Skilled Agent-Engineering Talent

Demand for prompt engineers, reinforcement-learning specialists, and orchestration architects far exceeds supply. LinkedIn’s 2024 talent report logged more than 250,000 open AI positions in the United States alone, with 65% of employers citing acute hiring challenges. Compensation premiums range from 20% to 40% above conventional software roles, squeezing mid-market budgets. Universities are racing to update curricula, but graduate pipelines will not materially ease shortages until 2027. Firms are upskilling existing developers through vendor academies and partnering with system integrators, yet onboarding still drags project timelines. Low-code agent builders help address the skills gap, though they cannot fully replace the deep architectural expertise needed for complex orchestration, governance, and performance tuning.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Gain as Complexity Rises

Software generated the majority of revenue, but Services' growth mirrors the rising complexity of deployments. In 2025, Software captured 68.43% of the overall Multi-Agent Enterprise Resource Planning market revenue, buoyed by platform licenses and API metering. Providers monetize orchestration engines, security layers, and monitoring dashboards that scale with token volume. Enterprises favor subscription pricing to match spend with realized business outcomes, and consumption transparency is a board-level metric.

The Services segment, forecast to grow at a 47.86% CAGR, expands as system integrators assume responsibility for agent design, reinforcement learning, and continuous prompt tuning. Consulting firms such as Tata Consultancy Services and Cognizant broadened generative AI practices, adding industry-specific agent libraries for healthcare and manufacturing clients.[3]Tata Consultancy Services, “TCS AI.Cloud Expansion,” tcs.com Ongoing support contracts encompass ethical-AI validation, data-pipeline hardening, and injection-attack testing, creating annuity revenue streams that increasingly rival software billings.

By Deployment Mode: Hybrid Architectures Bridge Compliance and Agility

Cloud deployments dominated with a 61.32% share in 2025, primarily due to their ability to provide elastic compute resources and instant access to foundation models. However, regulated sectors are driving a significant shift toward hybrid topologies. Financial institutions and healthcare providers, for instance, prefer to keep sensitive records on-premises while routing low-risk workloads through public cloud inference endpoints. This approach has led to a projected compound annual growth rate (CAGR) of 48.06% for hybrid deployment modes. Additionally, the European Union AI Act has further accelerated this trend by mandating in-house oversight for high-risk applications, ensuring compliance and security.

To address these evolving needs, vendors are now offering agent gateway appliances that facilitate seamless orchestration between on-premise clusters and cloud APIs. These appliances enforce policy compliance and provide observability during the hand-off process. While on-premise deployments remain essential for industries such as defense contractors and air-gapped utilities, their growth has been slower due to capital expenditure constraints. Looking ahead, the Multi-Agent Enterprise Resource Planning market is expected to be driven by the adoption of flexible architectures. These architectures abstract the physical location of workloads, enabling organizations to implement uniform governance and management practices regardless of where the workloads are deployed.

By Application: Legal and Compliance Automation Surges

Customer Service Automation accounted for 29.74% of 2025 revenue, demonstrating a significant and sustained investment in chatbots and ticket-routing systems. However, legal teams are emerging as the fastest adopters of automation technologies. Legal and Compliance Automation is projected to grow at a robust CAGR of 48.46%, driven by agents' ability to read and interpret statutes, compare them with internal controls, and automatically draft policy updates. For instance, Salesforce’s Agentforce module highlights how agents can escalate complex customer cases only after exhausting scripted remediation processes, effectively reducing average handle times and improving efficiency.

In the finance domain, agents leverage Optical Character Recognition (OCR) and classification technologies to streamline invoice reconciliation processes. Meanwhile, IT operations agents use telemetry data to autonomously identify and resolve incidents, minimizing downtime and enhancing operational reliability. In supply chain management, robotic process agents play a pivotal role in synchronizing factory equipment and managing delivery fleets, creating a seamless integration of digital and physical workflows. Collectively, these applications drive consistent demand for low-latency agent interactions, which serve as a cornerstone for the sustained growth of the Multi-Agent Enterprise Resource Planning market.

By Industry Vertical: Healthcare Adoption Accelerates

BFSI generated 26.11% of revenue in 2025 through fraud analysis, credit scoring, and trade settlement agents. These agents have been instrumental in automating processes that traditionally required significant manual intervention, thereby improving efficiency and reducing operational costs. However, hospitals and life-science firms are now outpacing this sector with a remarkable 48.66% CAGR. Healthcare providers are increasingly deploying agents for clinical documentation and prior-authorization workflows, which have historically consumed substantial clinician time. By automating these processes, providers are not only enhancing operating margins but also improving patient throughput and overall care delivery.

Similarly, the manufacturing sector is leveraging agents integrated with industrial IoT sensors to optimize operations. These agents are used to schedule predictive maintenance, reduce downtime, and fine-tune energy consumption, which is further supported by platforms like Siemens’ Industrial Copilot marketplace. In the retail sector, pricing and assortment agents dynamically adjust promotions and inventory based on real-time demand signals, enabling retailers to respond swiftly to market changes. Telecom carriers are also adopting network-optimization agents that self-balance traffic across heterogeneous infrastructure, ensuring seamless connectivity and improved service quality. These vertical expansions are driving a diversified Multi-Agent Enterprise Resource Planning market share mix, which helps mitigate the impact of cyclicality in any single sector and ensures sustained growth across industries.

By Enterprise Size: SME Adoption via Marketplaces

Large Enterprises contributed 64.53% of 2025 revenue because they command in-house AI staff, dedicated budgets, and complex process landscapes ripe for automation. These organizations benefit from the ability to deploy advanced multi-agent systems across various departments, enabling streamlined operations and significant cost savings. The Multi-Agent Enterprise Resource Planning market size for SMEs, however, is scaling quickly at a 47.67% CAGR as marketplaces remove entry barriers. This growth is driven by the increasing availability of cost-effective solutions tailored to smaller businesses, which often lack the resources of larger enterprises. Monday.com’s Agentalent.ai lists pre-trained agents priced per transaction, allowing cash-constrained firms to pilot workflows without capital outlay.

Pay-as-you-go billing de-risks experimentation, enabling SMEs to adopt automation technologies without committing to significant upfront investments. Additionally, templated governance artifacts assure compliance for ISO-certified sectors, providing smaller firms with the confidence to integrate these solutions into their operations. Vendor roadmaps increasingly target SMB playbooks such as bookkeeping, e-commerce fulfillment, and social-media scheduling, enabling the technology to permeate beyond Fortune 500 corridors. This shift is expected to democratize access to advanced automation tools, leveling the playing field for smaller businesses. Greater SME penetration will expand the total addressable user base and drive ecosystem diversity, compelling platform operators to maintain affordable compute tiers while fostering innovation across the market.

Geography Analysis

North America maintained a 38.49% market share in the Multi-Agent Enterprise Resource Planning market in 2025, thanks to hyperscaler dominance, capital access, and dense pools of agent-engineering talent. U.S. banks, retailers, and healthcare networks launched large-scale deployments in production, catalyzed by mature cloud governance frameworks and aggressive cost-optimization mandates. Canada follows with banking and public-sector pilots, while Mexico’s automotive suppliers connect shop-floor robots through local agent clusters. API and compute spend, however, is rising sharply, driving enterprises to compress token footprints by fine-tuning smaller models and caching deterministic sub-flows.

Asia-Pacific is set for a 48.82% CAGR, the highest globally, propelled by China’s smart-manufacturing subsidies, Japan’s labor-scarcity response, and India’s IT-services export engine. Factory owners embed agents into supervisory control systems to orchestrate assembly lines and reduce scrap rates, supported by national AI+Industry incentives. Indian system integrators re-skill 100,000 employees for agent engineering, bundling workflow libraries into global delivery contracts. Start-ups across Southeast Asia provide templated agents for micro-SMEs, leveraging regional cloud nodes that comply with data-sovereignty laws. Interoperability limitations and restricted cross-border data flow remain friction points, yet localized marketplaces in ASEAN economies mitigate those gaps.

Europe, South America, and the Middle East and Africa present heterogeneous adoption curves. The European Union AI Act requires conformity assessments, pushing firms to prioritize explainable agents and sandbox testing before go-live. Germany and France lead industrial and financial deployments, whereas southern economies adopt at a steadier pace. Brazil and Argentina gain traction in retail andagriculturale use cases, offsetting currency volatility by denominated consumption billing in USD to stabilize vendor contracts. Gulf Cooperation Council nations are investing in greenfield smart-city programs, tying agents into energy, mobility, and public service platforms. Africa’s uptake remains nascent outside South Africa and Egypt, though pan-regional telcos plan network-optimization agents to cut opex.

Competitive Landscape

Competition spans hyperscaler clouds, incumbent ERP vendors, automation specialists, and open-source stewards, resulting in moderate fragmentation. Microsoft, Amazon Web Services, and Alphabet bundle agent orchestration tightly with compute and data services, raising platform stickiness. SAP and Oracle retrofit suites with Joule Studio and generative assistants to preserve ERP install bases against cloud-native challengers. Salesforce, ServiceNow, and UiPath inject agentic logic into CRM, IT service management, and RPA franchises, turning existing datasets into training corpora.

Open-source leaders, LangChain Inc. and CrewAI Inc., commercialize distribution through managed orchestration, enterprise support, and curated agent templates, translating community pulls into subscription revenue. Industrial giants Siemens and ABB fold agents into control-system portfolios, enabling cyber-physical synchronization on factory floors. NVIDIA courts every segment by offering NIM inference microservices that cut latency and GPU cost per token, positioning itself as the neutral silicon substrate of choice.[4]NVIDIA Blog, “NIM Microservices Accelerate AI Agents,” nvidia.com

Mergers and partnerships intensify as stakeholders race to fill capability gaps and lock down ecosystems. Hyperscalers scout for specialist start-ups to cement vertical footholds, while integrators sign exclusive reseller pacts to guarantee talent pipelines. Absence of mature interoperability standards may favor players with large installed bases, yet enterprises still value openness, suggesting convergent evolution toward quasi-standard protocols will unfold over the next three years.

Multi-Agent Enterprise Systems Industry Leaders

Microsoft Corporation

IBM Corporation

Alphabet Inc.

Amazon Web Services, Inc.

OpenAI LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Monday.com launched Agentalent.ai, an agent marketplace that allows SMEs to hire ready-to-run AI agents for social media management, financial reporting, and customer service.

- March 2026: Siemens expanded Industrial Copilot with a third-party agent marketplace that integrates with its programmable logic controllers and SCADA systems.

- February 2026: OpenAI models are now natively accessible on Amazon Bedrock, enabling enterprises to build cross-service, multi-agent workflows without cross-cloud data movement.

- January 2026: IBM unveiled the watsonx Orchestrate Agent Catalog, bundling partner content and reporting a 75% reduction in processing time for early adopters.

Global Multi-Agent Enterprise Systems Market Report Scope

The Multi-Agent Enterprise Resource Planning (ERP) market comprises integrated software and service solutions that enhance enterprise operations by leveraging multiple autonomous agents. These agents collaborate to streamline and optimize business functions, including finance, supply chain management, human resources, and customer relationship management. By automating repetitive tasks and enabling real-time decision-making, multi-agent ERP systems help organizations improve efficiency, reduce operational costs, and adapt to dynamic business environments.

The Multi-Agent Enterprise Resource Planning Market Report is Segmented by Component (Software, and Services), Deployment Mode (Cloud, On-Premise, and Hybrid), Application (Customer Service Automation, IT Operations, Finance and Accounting, Supply Chain Management, and Robotics and Autonomous Vehicles), Industry Vertical (BFSI, Manufacturing, Healthcare, Retail and E-Commerce, IT and Telecommunications, and Other Verticals), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud |

| On-Premise |

| Hybrid |

| Customer Service Automation |

| IT Operations |

| Finance and Accounting |

| Supply Chain Management |

| Robotics and Autonomous Vehicles |

| BFSI |

| Manufacturing |

| Healthcare |

| Retail and E-Commerce |

| Information Technology and Telecommunications |

| Other Industry Verticals |

| Large Enterprises |

| Small and Medium Enterprises |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Component | Software | ||

| Services | |||

| By Deployment Mode | Cloud | ||

| On-Premise | |||

| Hybrid | |||

| By Application | Customer Service Automation | ||

| IT Operations | |||

| Finance and Accounting | |||

| Supply Chain Management | |||

| Robotics and Autonomous Vehicles | |||

| By Industry Vertical | BFSI | ||

| Manufacturing | |||

| Healthcare | |||

| Retail and E-Commerce | |||

| Information Technology and Telecommunications | |||

| Other Industry Verticals | |||

| By Enterprise Size | Large Enterprises | ||

| Small and Medium Enterprises | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How fast will spending on multi-agent ERP grow between 2026 and 2031?

Overall outlays are projected to rise at a 47.46% CAGR, taking the total Multi-Agent Enterprise Resource Planning market size from USD 7.12 billion in 2026 to USD 49.64 billion by 2031.

Which region will add the most incremental revenue by 2031?

Asia-Pacific is expected to contribute the largest absolute gain, expanding at a 48.82% CAGR on the back of manufacturing and SME adoption.

What deployment model is gaining favor in regulated industries?

Hybrid architectures are emerging as the default because they let firms keep sensitive data on-premise while leveraging cloud inference for lower-risk tasks, growing at 48.06% CAGR.

Why are services growing faster than software licenses?

Enterprises need system integrators for agent design, reinforcement learning, and continuous prompt tuning, pushing Services to a 47.86% CAGR versus more modest software growth.

Which application area will see the fastest expansion?

Legal and Compliance Automation is set to surge at 48.46% CAGR as agents handle contract review, regulatory reporting, and audit-trail generation.

What talent gap is slowing deployments?

Shortages in prompt engineering and multi-agent orchestration skills are inflating salaries by up to 40%, delaying projects despite growing demand.

Page last updated on: