Mucopolysaccharidosis Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.28 Billion |

| Market Size (2030) | USD 4.98 Billion |

| Growth Rate (2026 - 2031) | 8.72% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

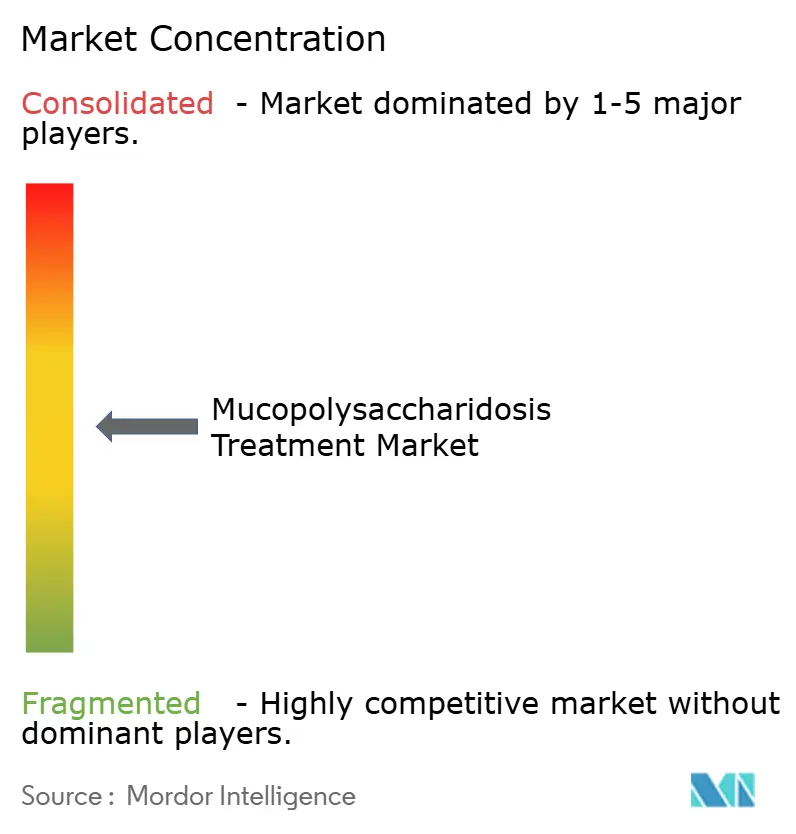

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mucopolysaccharidosis Treatment Market Analysis by Mordor Intelligence

The Mucopolysaccharidosis Treatment Market size is estimated at USD 3.28 billion in 2026, and is expected to reach USD 4.98 billion by 2030, at a CAGR of 8.72% during the forecast period (2026-2030).

Mandatory newborn screening, regulatory traction for blood-brain-barrier-penetrant enzymes, and a flood of venture capital into central-nervous-system-targeted gene therapies are converging to reshape care pathways. Enzyme replacement therapy (ERT) retains volume leadership, yet gene therapy is moving rapidly from experimental status to commercial reality as pivotal trials yield positive cerebrospinal fluid enzyme data. Home-infusion models are compressing per-patient treatment costs by 15% to 20%, creating payer headroom for high-priced one-time vectors. Competitive intensity is bifurcating: incumbent ERT oligopolists rely on manufacturing scale and payer contracts, while gene-therapy insurgents court investor capital and regulatory designations to de-risk curative modalities.

Key Report Takeaways

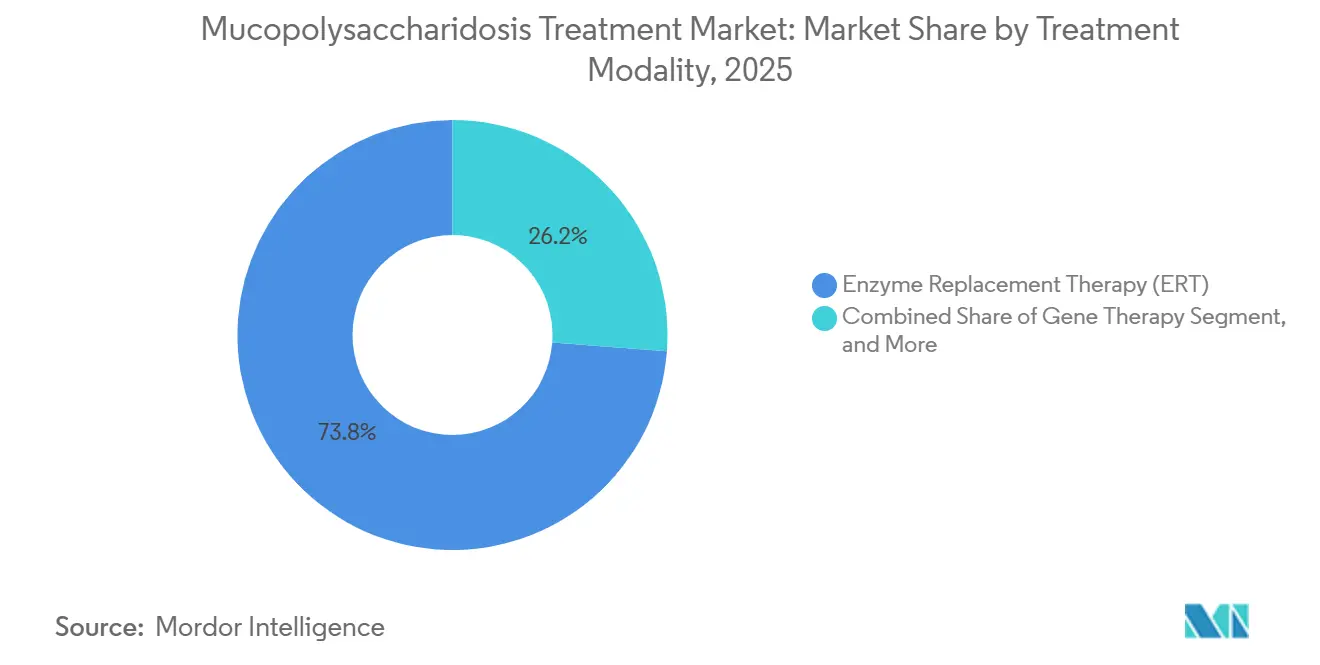

- By treatment modality, enzyme replacement therapy captured 73.81% of the mucopolysaccharidosis treatment market share in 2025, whereas gene therapy is projected to post the fastest 9.26% CAGR through 2031.

- By MPS type, MPS IV (Morquio A/B) led with 33.17% revenue share in 2025, while MPS III is forecast to register the highest 10.17% CAGR to 2031.

- By end user, hospitals accounted for 45.72% of the mucopolysaccharidosis treatment market in 2025, yet home infusion is on track for an 11.66% CAGR through 2031.

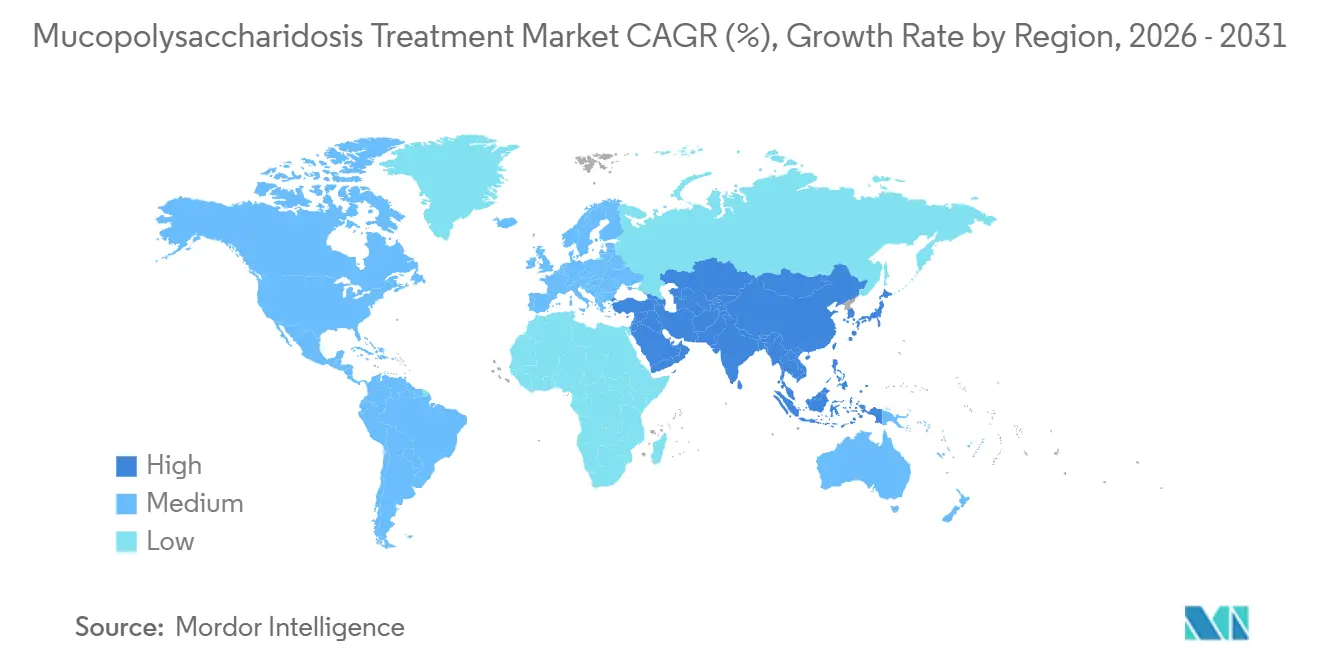

- By geography, North America accounted for 41.43% of revenue in 2025, while Asia-Pacific is poised for the fastest 13.42% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Mucopolysaccharidosis Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding Newborn Screening Mandates | +1.8% | North America, Europe, Japan, Australia | Medium term (2-4 years) |

| Regulatory Momentum for BBB-Penetrant ERT | +1.5% | Japan first, global ripple | Short term (≤ 2 years) |

| Venture Capital for CNS-Targeted Gene Therapy | +1.2% | North America, Europe, spillover to Asia-Pacific | Medium term (2-4 years) |

| Rapid Home-Infusion Adoption | +0.9% | North America, Western Europe, Australia | Short term (≤ 2 years) |

| Prenatal ERT Protocols | +0.6% | North America, select European centers | Long term (≥ 4 years) |

| AI-Driven Patient-Finding Platforms | +0.7% | Digitally mature health systems worldwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expanding Newborn Screening Mandates

Mandatory inclusion of MPS I and MPS II in state panels has shortened diagnostic journeys from a median of 4.2 years to under six months, with 47 U.S. jurisdictions now screening for MPS I and 18 for MPS II.[1]Health Resources and Services Administration, “Recommended Uniform Screening Panel,” hrsa.gov Early identification allows ERT before irreversible organ damage, lifting five-year survival from 68% to 91% in screened cohorts.[2]Genetics in Medicine, “Early ERT Outcomes,” gimjournal.org Payers now see pre-symptomatic therapy lowering lifetime hospitalization costs by USD 1.2 million per patient, a dynamic that is motivating policymakers in the European Union to consider adding additional subtypes to national screening programs.

Regulatory Momentum for BBB-Penetrant ERT Approvals

Japan’s March 2024 green light for pabinafusp alfa ushered in the first enzyme engineered to traverse the blood-brain barrier. Seventy-two percent of patients showed stabilization or gains on Vineland Adaptive Behavior Scales after 52 weeks, a benchmark unmet by previous idursulfase regimens. ArmaGen’s fusion construct for MPS I entered late-stage U.S. trials in November 2024, with interim cerebrospinal fluid enzyme data expected mid-2026. These advances expand the addressable market because neuronopathic phenotypes represent 42% of cases but historically accounted for only 18% of ERT spending.

Surging Venture Investment in CNS-Targeted Gene Therapies

Developers raised USD 890 million across 2024-2025, with 63% earmarked for mucopolysaccharidosis programs. REGENXBIO’s USD 150 million January 2025 financing supports RGX-121’s filing, while Sangamo closed a USD 120 million injection from Pfizer to push ST-920 into the clinic. Trial infrastructure is scaling in lockstep, doubling global study sites from 34 to 67 between 2023 and 2025, which cut median enrollment time by more than half.

Rapid Adoption of Home-Infusion Models in High-Income Markets

Home delivery of ERT rose from 12% of total infusions in 2022 to 28% in 2025 across OECD countries. A 1,847-patient registry found no anaphylaxis and identical mild reaction rates to those in hospital settings, while cutting per-infusion cost from USD 3,200 to USD 1,800. BioMarin’s 2024 U.S. program lifted adherence to 94% and reduced emergency visits 38% within six months.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Reimbursement Caps for Ultra-High-Cost Biologics | -1.4% | Europe, Commonwealth, select U.S. payers | Short term (≤ 2 years) |

| Manufacturing Yield Bottlenecks for High-Dose AAV | -0.9% | North America, Europe production hubs | Medium term (2-4 years) |

| Long Diagnostic Delays in Emerging Regions | -0.8% | Latin America, MEA, South Asia | Long term (≥ 4 years) |

| Vector-Induced Dorsal-Root-Ganglia Toxicity | -0.6% | Global trials | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Reimbursement Caps for Ultra-High-Cost Orphan Biologics

England’s cost watchdog declined ERT funding with ICERs above GBP 1 million per QALY, and Germany cut galsulfase prices 22% after downgrading its benefit rating.[3]Institute for Quality and Efficiency in Health Care, “Galsulfase Benefit Assessment,” iqwig.de Gene-therapy list prices of USD 2.5-4 million are triggering five-year outcome-based contracts, extending market-access timelines by up to 18 months.

Manufacturing Yield Bottlenecks for High-Dose AAV Vectors

Only four global CDMOs can routinely manufacture AAV9 batches above 1 × 10¹⁵ genomes, doubling lead times to 26 months and pushing RGX-121’s BLA from late 2024 into H2 2025. Vector production is climbing to 48% of list price, eroding commercial margins.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Treatment Modality: Gene Therapy Gains Despite ERT Dominance

Enzyme replacement therapy held 73.81% of the mucopolysaccharidosis treatment market share in 2025, anchored by decades of longitudinal safety data and established reimbursement pathways. Gene therapy, however, is forecast to surge at a 9.26% CAGR through 2031, signaling a pivot toward one-time curative vectors that circumvent lifelong infusions. REGENXBIO’s RGX-121 achieved its primary endpoint in 19 of 21 evaluable patients, making a late-2026 FDA filing plausible. Stem-cell transplants remain a niche, with roughly 80 procedures annually worldwide, although Sangamo’s autologous zinc-finger approach could triple the addressable cohort.

The mucopolysaccharidosis gene therapy market is projected to accelerate once manufacturing constraints ease, yet payers are scrutinizing the post-treatment monitoring, which adds USD 80,000-120,000 per patient over 15 years. ERT incumbents face mounting price pressure; BioMarin’s laronidase revenue slipped 6% in 2024 despite moderate patient growth. Orchard’s OTL-203 produced 88% event-free survival at three-year follow-up, securing EMA PRIME status in January 2025.

By MPS Type: Sanfilippo Subtypes Drive Growth

MPS IV accounted for 33.17% of 2025 revenue, reflecting Vimizim’s prevalence of 1 in 200,000 births. The mucopolysaccharidosis treatment market, driven by MPS III, is growing fastest, thanks to intrathecal gene therapies that stabilize neurodegeneration. Lysogene’s AAV-SGSH delivered sustained enzyme activity with early cognitive stabilization in 14 of 17 patients. Abeona’s ABO-102 produced similar biochemical durability, though transient dorsal-root-ganglia MRI changes highlight safety vigilance.

MPS I and MPS II still account for 38% of consolidated revenue, but growth is tapering as biosimilar entrants near patent cliffs. Galsulfase generated USD 143 million in 2024, but ultra-rare conditions such as MPS VII remain sub-USD 30 million programs due to a prevalence of fewer than 1 in 1,000,000. Gene-therapy developers are increasingly targeting neuronopathic subtypes with dire natural histories, a strategy that both commands premium pricing and accelerates regulatory timelines.

By End User: Home Infusion Reshapes Delivery

Hospitals retained 45.72% of 2025 volume, driven by initiation doses and complex comorbidity management. Home infusion, nevertheless, is expanding at 11.66% yearly as insurers embrace bundled payments that lock in 12% ERT discounts in exchange for at-home administration mandates. Mucopolysaccharidosis treatment market share in home settings is set to rise steadily as more payers adopt Anthem’s model and EMA guidance standardizes caregiver training.

A 2024 claims analysis found that patients receiving ERT at home averaged 2.1 yearly hospitalizations, compared with 3.8 for peers receiving hospital-infused ERT, largely because remote monitoring detected reactions earlier. Specialty clinics serve 28% of demand and remain pivotal for physiotherapy and orthopedic coordination, whereas research centers account for 12% aligned with gene-therapy trials.

Geography Analysis

North America delivered 41.43% of 2025 revenue, underpinned by widespread newborn screening, high diagnosis rates, and favorable reimbursement. Europe followed at 32%, aided by national rare-disease plans that centralize procurement and negotiate volume rebates. The mucopolysaccharidosis treatment market in Asia-Pacific is forecast to grow the fastest, at a 13.42% CAGR through 2031, as Japan, China, and South Korea expand coverage.

Japan’s approval of pabinafusp alfa drove first-year sales of JPY 4.2 billion (USD 28 million). China’s CANbridge filed MPS I and II therapies in late 2024, targeting an estimated 1,200 diagnosed patients. South Korea reimbursed elosulfase alfa in January 2025, reflecting growing political will to fund ultra-rare therapies. Latin America and MEA combined represented 11% of 2025 revenue, constrained by diagnostic delays and fragmented payer systems; however, Brazil’s inclusion of laronidase and idursulfase into its high-cost drug program in April 2024 expanded access to roughly 340 patients.

Competitive Landscape

The mucopolysaccharidosis treatment market is moderately consolidated. BioMarin’s four-therapy franchise posted USD 1.02 billion in 2024 sales yet guided to a 3-5% annual decline through 2028 due to looming biosimilars in Europe. Takeda’s global commercial footprint underpins idursulfase stability but also provides a launchpad for brain-penetrant enzymes co-developed with Denali.

Gene-therapy entrants are fragmenting the field by carving out niches for neuronopathic therapies. REGENXBIO’s NAV capsid platform is licensed to eight developers, creating a royalty stream that mitigates single-asset risk. Denali’s transferrin-receptor transport vehicle achieved 40-fold higher brain enzyme exposure in preclinical models and earned a USD 200 million upfront from Takeda in March 2025. Immusoft’s engineered B-cell therapy secured Rare Pediatric Disease designation for ISP-002 in January 2026, reflecting regulatory appetite for innovative modalities.

White-space opportunities persist in MPS VII and MPS IX, as well as in substrate-reduction adjuncts that may complement ERT. GC Pharma’s December 2024 laronidase biosimilar filing signals intensifying price competition in mainstream subtypes. Manufacturing yield limitations remain the biggest moat against small biotech entrants, yet advances in suspension cultures and scalable plasmid-free systems could erode incumbents’ cost advantages over the forecast period.

Mucopolysaccharidosis Treatment Industry Leaders

Takeda Pharmaceutical

Sanofi SA

Allievex Corporation

REGENXBIO

Paradigm Biopharmaceuticals

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Immusoft received U.S. FDA Rare Pediatric Disease designation for ISP-002, an engineered-B-cell therapy for MPS II.

- January 2026: FDA placed clinical holds on REGENXBIO’s RGX-111 and RGX-121 after a neoplasm signal in one trial participant.

- September 2025: JCR Pharmaceuticals presented five-year data showing sustained neurocognitive benefit with pabinafusp alfa at ICIEM 2025 in Kyoto.

- August 2025: FDA extended the RGX-121 PDUFA date to February 2026, adding manufacturing review time.

Global Mucopolysaccharidosis Treatment Market Report Scope

The Mucopolysaccharidosis (MPS) Treatment Market refers to the global biopharmaceutical industry focused on the research, development, manufacturing, and commercialization of therapies specifically designed to treat mucopolysaccharidoses, a group of rare, inherited lysosomal storage disorders caused by deficiencies in enzymes that break down glycosaminoglycans (GAGs), leading to progressive accumulation of these substances in tissues and organs.

The Mucopolysaccharidosis Treatment Market Report is segmented by treatment modality into enzyme replacement therapy, stem-cell therapy/HSCT, gene therapy, and other treatment modalities; by MPS type into MPS I, MPS II, MPS III, MPS IV, MPS VI, MPS VII, and ultrarare types; by end user into hospitals, specialty clinics, home-infusion settings, and research & academic centers; and by geography into North America, Europe, Asia-Pacific, Middle East & Africa, and South America. Market forecasts are provided in terms of value (USD).

| Enzyme Replacement Therapy (ERT) |

| Stem-Cell Therapy / HSCT |

| Gene Therapy |

| Other Treatment Modality (Small-Molecule Modulators, Supportive & Adjunctive Therapies, etc.) |

| MPS I (Hurler – Scheie) |

| MPS II (Hunter) |

| MPS III (Sanfilippo A–D) |

| MPS IV (Morquio A/B) |

| MPS VI (Maroteaux-Lamy) |

| MPS VII (Sly) |

| Ultrarare Types (e.g., MPS IX) |

| Hospitals |

| Specialty Clinics |

| Home-Infusion Settings |

| Research & Academic Centers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Treatment Modality | Enzyme Replacement Therapy (ERT) | |

| Stem-Cell Therapy / HSCT | ||

| Gene Therapy | ||

| Other Treatment Modality (Small-Molecule Modulators, Supportive & Adjunctive Therapies, etc.) | ||

| By MPS Type | MPS I (Hurler – Scheie) | |

| MPS II (Hunter) | ||

| MPS III (Sanfilippo A–D) | ||

| MPS IV (Morquio A/B) | ||

| MPS VI (Maroteaux-Lamy) | ||

| MPS VII (Sly) | ||

| Ultrarare Types (e.g., MPS IX) | ||

| By End User | Hospitals | |

| Specialty Clinics | ||

| Home-Infusion Settings | ||

| Research & Academic Centers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the mucopolysaccharidosis treatment market in 2031?

The market is forecast to reach USD 4.98 billion by 2031, driven by an 8.72% CAGR.

Which therapy class is expected to grow fastest over the forecast period?

Gene therapy is projected to post the fastest 9.26% CAGR through 2031 as one-time CNS-targeted vectors progress toward approval.

Why is Asia-Pacific the quickest-growing region?

Recent approvals of brain-penetrant enzymes in Japan and expanding rare-disease reimbursement in China and South Korea support a 13.42% CAGR for the region.

How are home-infusion models changing treatment economics?

Home infusion cuts per-infusion costs by almost 40% and improves adherence, prompting payers to negotiate bundled discounts tied to in-home delivery.

What are the main regulatory hurdles facing gene therapies?

FDA guidance now requires extended monitoring of the dorsal root ganglia and 15-year post-therapy follow-up, lengthening trial timelines and increasing lifecycle costs.

Page last updated on: