Mounjaro Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 29.69 Billion |

| Market Size (2031) | USD 118.79 Billion |

| Growth Rate (2026 - 2031) | 31.95% CAGR |

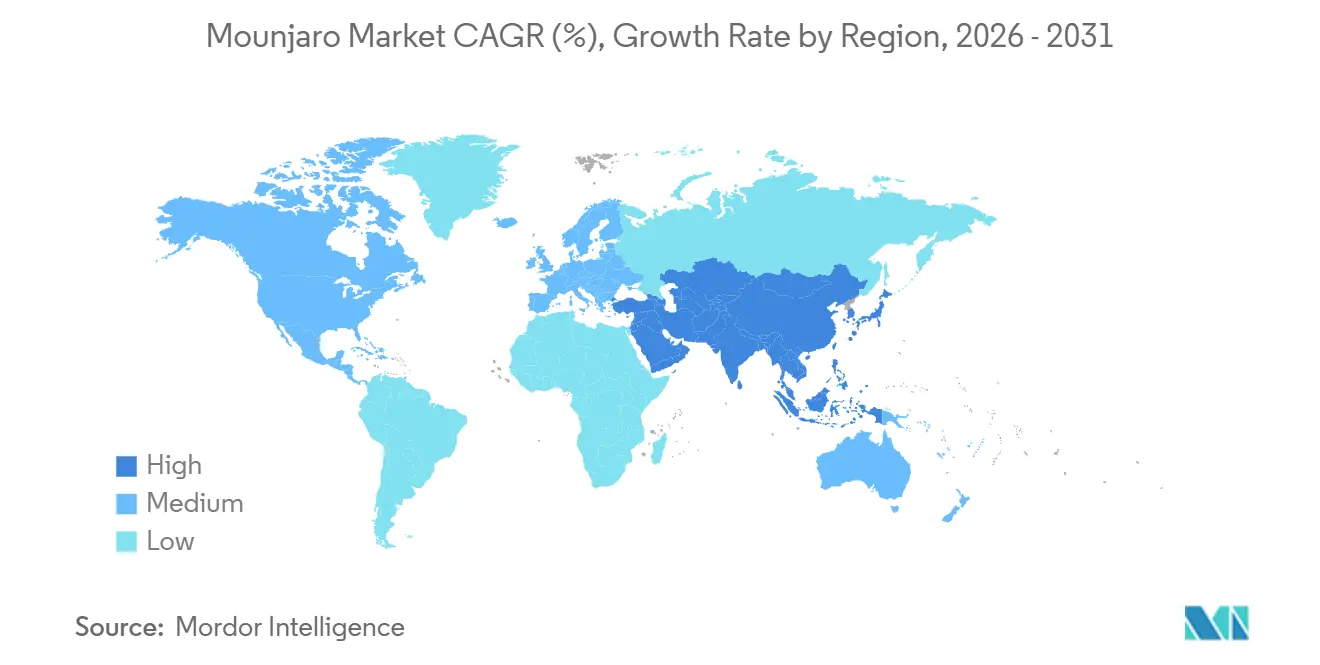

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

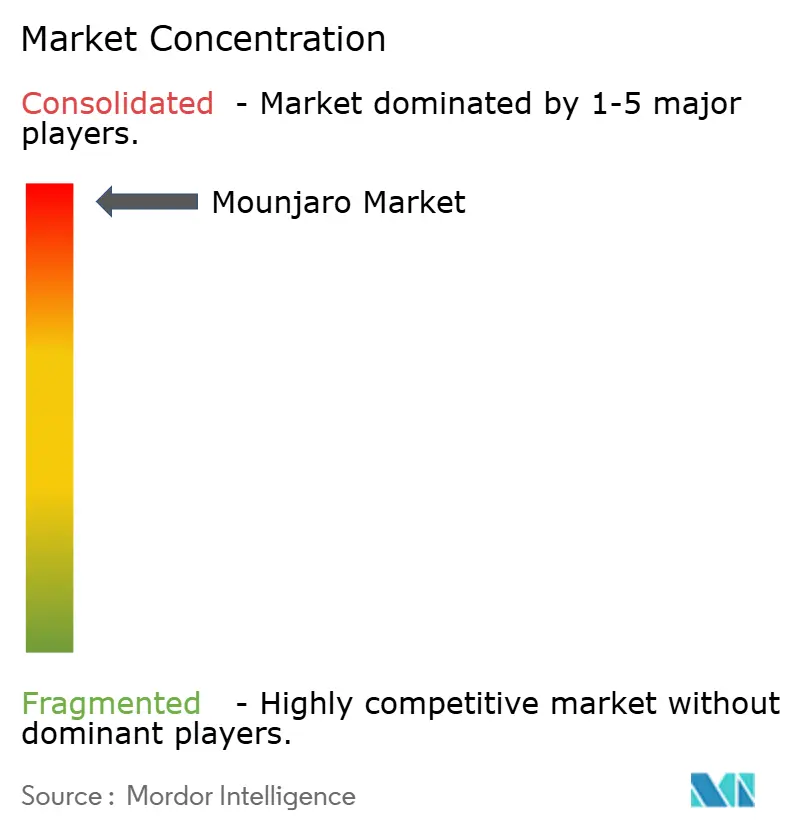

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mounjaro Market Analysis by Mordor Intelligence

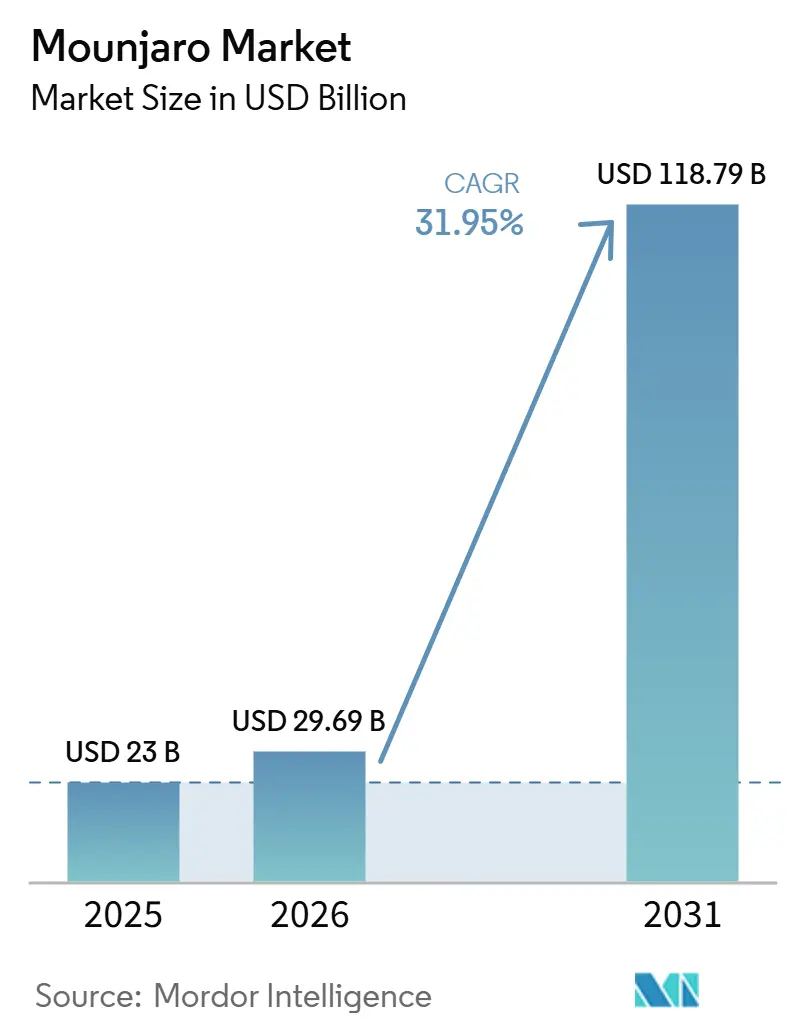

The Mounjaro Market size was valued at USD 23 billion in 2025 and is estimated to grow from USD 29.69 billion in 2026 to reach USD 118.79 billion by 2031, at a CAGR of 31.95% during the forecast period (2026-2031).

The mounjaro market is scaling on the back of an unusually strong commercial ramp for tirzepatide, with combined Mounjaro and Zepbound revenue reaching USD 36.5 billion in FY2025 and accounting for 56% of Eli Lilly’s total revenue, which shows how central this franchise has become to Lilly’s growth profile. The Mounjaro market is also benefiting from concurrent demand across diabetes care, chronic weight management, and sleep-related obesity treatment, which broadens the prescriber base and reduces the risk of a single-use growth ceiling after the initial launch phase. The mounjaro market has gained additional reach through LillyDirect and retail pick-up expansion, which improved access for self-pay patients and supported channel growth outside the conventional reimbursement path. The Mounjaro market is likely to keep expanding as Lilly adds manufacturing capacity, although payer restrictions for obesity treatment and tighter pricing outside the United States will continue to influence how much of the clinical demand converts into realized revenue.

Key Report Takeaways

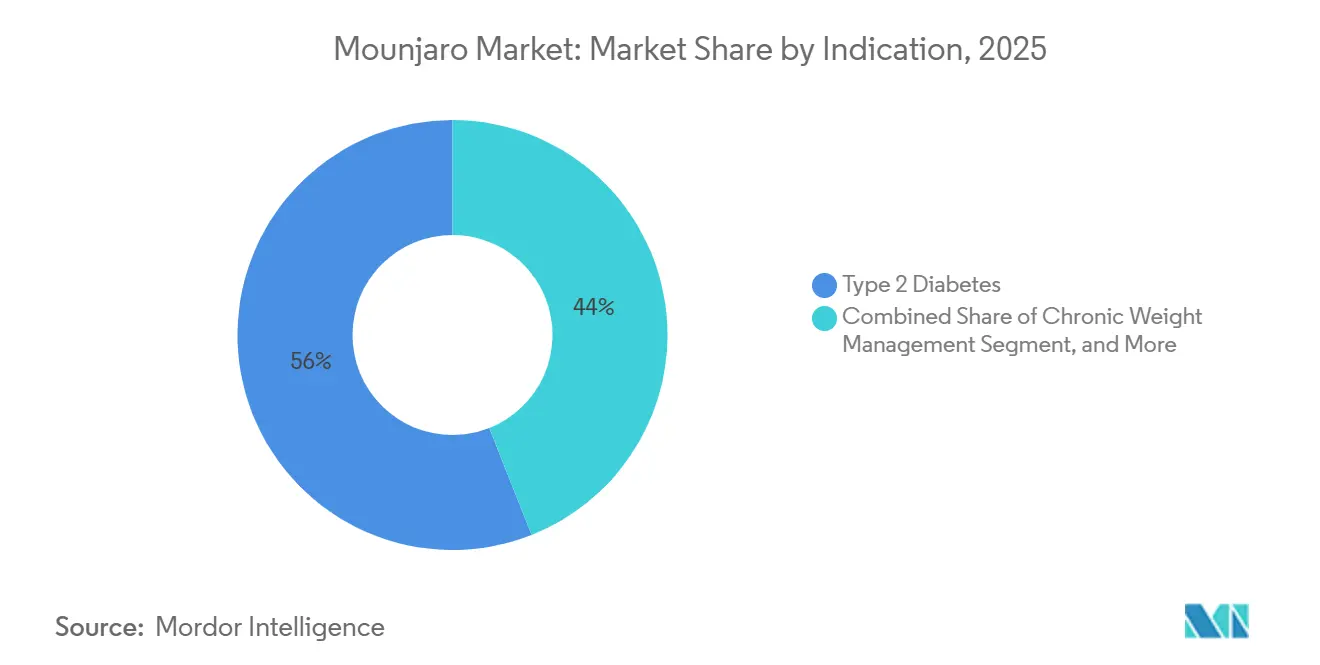

- By indication, type 2 diabetes held 56.03% of revenue in 2025, while chronic weight management is forecast to grow at 35.84% CAGR through 2031.

- By dosage form, single-dose pen held 60.18% of revenue in 2025, while single-dose vial is projected to advance at 36.76% CAGR through 2031.

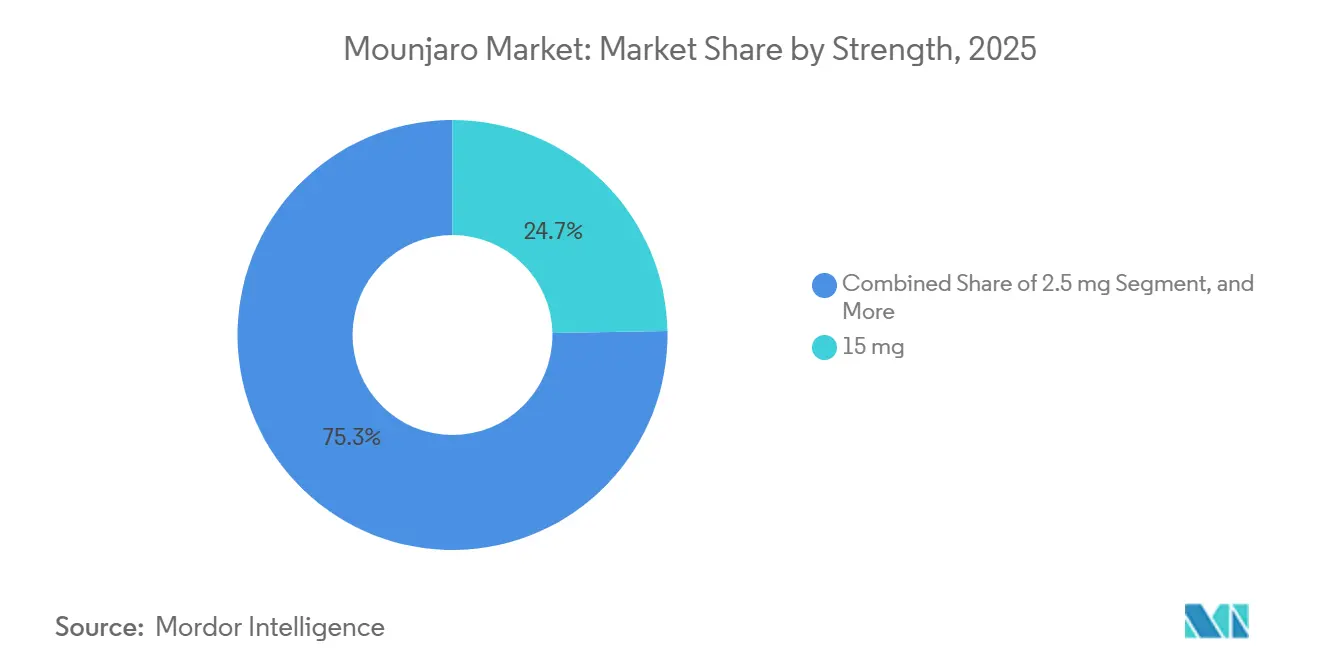

- By strength, the 15 mg strength accounted for 24.67% of revenue in 2025, while the fastest-growing strength is projected to advance at 32.57% CAGR through 2031.

- By distribution channel, retail pharmacies represented 34.03% of revenue in 2025, while online pharmacies are forecast to grow at 33.94% CAGR through 2031.

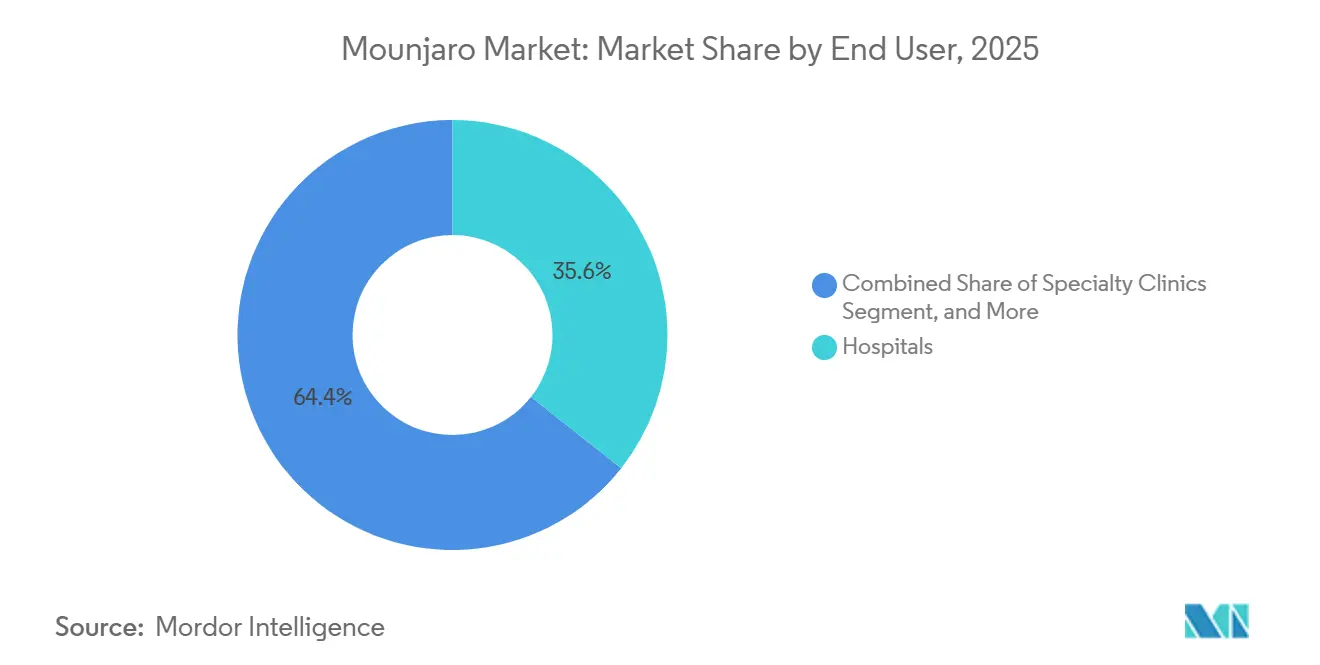

- By end user, hospitals captured 35.63% of revenue in 2025, while outpatient and primary care centers are projected to expand at 34.74% CAGR through 2031.

- By geography, North America accounted for 39.28% of revenue in 2025, while Asia-Pacific is forecast to grow at 36.04% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Mounjaro Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Type 2 Diabetes Burden and Earlier Treatment Initiation | +8.2% | Global | Long term (≥ 4 years) |

| Superior Dual GIP and GLP-1 Efficacy Versus Single-Pathway Therapies | +6.5% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| Label Expansion Into Obesity and Obstructive Sleep Apnea | +4.8% | North America and Europe, spill-over to APAC | Medium term (2-4 years) |

| Employer and Self-Pay Demand for High-Efficacy Anti-Obesity Treatment | +2.9% | North America | Short term (≤ 2 years) |

| Cross-Condition Use Potential in Cardiometabolic Care Pathways | +2.1% | Global, highest in Europe and North America | Long term (≥ 4 years) |

| Persistently Low Real-World Treatment Persistence Creates Repeat Prescribing Value | +1.8% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Type 2 Diabetes Burden and Earlier Treatment Initiation

The mounjaro market continues to draw strength from the expanding global diabetes population, but the larger commercial shift comes from earlier use of high-efficacy agents in the treatment pathway rather than from prevalence alone. The IDF Diabetes Atlas reported 589 million adults living with diabetes in 2025, with 42.8% of cases still undiagnosed, which leaves a large untreated pool that can move into drug therapy as screening improves.[1]International Diabetes Federation, “IDF Diabetes Atlas 11th Edition 2025, Global Diabetes Data and Insights,” IDF Diabetes Atlas, diabetesatlas.org The Mounjaro market is benefiting because treatment practice is moving away from delayed escalation, and dual GIP and GLP-1 therapy is being considered earlier for patients who need glycemic control with parallel weight benefit. SURPASS-PEDS added another layer to this shift by showing efficacy and safety in children and adolescents with Type 2 Diabetes, which opens a new prescribing group that had limited high-efficacy options before 2025. This means the mounjaro market can grow faster than the underlying diagnosed population because more eligible patients are reaching tirzepatide earlier in the care sequence.

Superior Dual GIP and GLP-1 Efficacy Versus Single-Pathway Therapies

The mounjaro market is also being supported by head-to-head clinical evidence that strengthens tirzepatide’s position against competing incretin therapies. SURMOUNT-5 showed that tirzepatide was superior to semaglutide in reducing body weight and waist circumference over 72 weeks, which gave prescribers and payers comparative data that had been missing in this class.[2]Ania M. Jastreboff et al., “Tirzepatide as Compared with Semaglutide for the Treatment of Obesity,” New England Journal of Medicine, nejm.org The mechanistic case is reinforced by published clinical reviews showing that tirzepatide’s dual receptor activity creates a broader metabolic effect than a single-pathway GLP-1 therapy. A 2025 meta-analysis further supported better weight loss and glycemic outcomes for tirzepatide versus several comparators, which makes formulary preference decisions more defensible for payers. The mounjaro market, therefore, gains not only from patient demand but also from stronger evidence that can shift institutional prescribing patterns in a more durable way.

Label Expansion Into Obesity and Obstructive Sleep Apnea

The mounjaro market has moved beyond a single-disease profile because tirzepatide now addresses obesity-related conditions that bring in new specialist channels. The FDA approved tirzepatide as the first prescription medicine for moderate to severe obstructive sleep apnea in adults with obesity in December 2024, which created a treatment route that did not previously exist in this setting.[3]U.S. Food and Drug Administration, “FDA Approves First Medication for Obstructive Sleep Apnea,” FDA Press Announcements, fda.gov That decision matters because obesity, sleep apnea, and Type 2 Diabetes often overlap in the same patient, so a single prescription can now sit across more than one clinically recognized need. SURMOUNT-OSA also showed improvements beyond airway events, including systolic blood pressure and patient-reported outcomes, which supports broader clinical acceptance in this pathway. The Mounjaro market is therefore expanding through a wider referral network that now includes sleep medicine and pulmonary specialists in addition to endocrinology and primary care.

Cross-Condition Use Potential in Cardiometabolic Care Pathways

The mounjaro market is increasingly shaped by evidence that tirzepatide fits into broader cardiometabolic management rather than standing as a diabetes-only or obesity-only therapy. SURPASS-CVOT confirmed noninferior cardiovascular protection versus dulaglutide and also showed a statistically significant 16% reduction in all-cause mortality, which gives the drug relevance in treatment discussions beyond glycemic control alone. The SUMMIT trial added to that position by showing reduced risk of cardiovascular death or worsening heart failure events in patients with heart failure with preserved ejection fraction and obesity. A 2025 review in Therapeutic Advances in Cardiovascular Disease described tirzepatide as a therapy emerging across metabolic, cardiorenal, and heart failure settings, which supports a multi-specialty prescribing future. As a result, the Mounjaro market is moving into care pathways where cardiologists and heart failure specialists can influence uptake alongside traditional metabolic prescribers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium Monthly Cost and Coverage Restrictions | -3.8% | Global, most acute in North America and Europe | Short term (≤ 2 years) |

| Ongoing Supply Constraints and Dose Availability Friction | -2.4% | Global | Short term (≤ 2 years) |

| Injectable Administration and Titration Friction | -1.6% | Global, highest in APAC and MEA | Medium term (2-4 years) |

| Compounded or Off-Label Substitution Pressure in Shortage Cycles | -1.2% | North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Premium Monthly Cost and Coverage Restrictions

The mounjaro market still faces a large conversion gap between clinical eligibility and commercial access, especially where obesity treatment is not broadly reimbursed. Lilly’s own self-pay channel is evidence of that gap because the company priced single-dose vials at USD 349 to USD 499 per month to reach patients outside standard coverage pathways. This structure helps the Mounjaro market reach motivated cash-pay patients, but it also shows that mainstream payer support is not yet wide enough to absorb demand at scale through ordinary pharmacy benefit routes. Access conditions are also uneven across indications, because diabetes treatment generally faces a stronger reimbursement base than obesity treatment, which limits how quickly obesity demand can be monetized in community care settings. The mounjaro market can therefore maintain strong patient interest while still losing part of its reachable volume when monthly cost remains the main barrier.

Compounded or Off-Label Substitution Pressure in Shortage Cycles

The mounjaro market also carries residual friction from the period when supply shortages pushed some patients toward compounded alternatives. The FDA stated in December 2024 that the tirzepatide shortage had been resolved and set end dates for routine compounding tied to shortage conditions, which was an important step toward re-centering branded supply. Even with that change, the mounjaro market still has to win back patients who were introduced to lower-cost substitute channels during the shortage window and may not immediately return to the brand. Lilly’s expanded vial offering through LillyDirect is a direct response because it gives self-pay patients a legal brand option across all approved doses and reduces the price gap versus compounded products. This means substitution pressure is lower than it was during supply disruption, but the Mounjaro market still needs sustained brand access and dose availability to fully neutralize that behavior.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Indication: Weight Management Accelerates While T2D Anchors the Base

Type 2 diabetes held 56.03% of the mounjaro market size in 2025, which kept it as the main revenue base even as newer use cases expanded more quickly. Chronic weight management is projected to grow at 35.84% CAGR through 2031, making it the fastest-moving indication in the mounjaro market as obesity prescribing spreads into broader outpatient settings. The mounjaro market still depends on the diabetes indication for commercial stability because hospital formularies, specialist protocols, and existing treatment pathways were built around glycemic management first. That base gives Lilly a dependable core while newer obesity-linked channels add incremental volume on top of established use.

The second growth layer comes from label broadening and referral diversification. FDA approval for obstructive sleep apnea in adults with obesity created a new channel where pulmonologists and sleep specialists can refer or prescribe tirzepatide, which expands the Mounjaro market beyond the traditional diabetes and obesity clinic base. Pediatric evidence from SURPASS-PEDS also matters because it opens an early-stage opportunity in youth-onset Type 2 Diabetes, where treatment needs are rising and effective options are limited. The American Academy of Sleep Medicine has highlighted that tirzepatide became the first FDA-approved medication for sleep apnea, which reinforces how distinct this pathway is from historical device-led care. Taken together, these developments mean the Mounjaro market is growing through both a well-established base indication and newer referral sources that can keep patient inflow strong over the forecast period.

By Dosage Form: Vial Channel Disrupts the Prefilled-Pen Status Quo

Single-dose pen accounted for 60.18% of the Mounjaro market size in 2025, reflecting its established fit with hospital, specialty-clinic, and nurse-led injection workflows. That leadership position is tied to provider familiarity and the convenience of a prefilled device in routine diabetes care. The Mounjaro market still leans on the pen format because it supports mainstream prescribing patterns and fits existing administration habits. At the same time, the single-dose vial is forecast to rise at 36.76% CAGR through 2031, which makes it the more disruptive format from a commercial standpoint.

The reason for that disruption is not the container alone, but the access model it enables. Lilly offered approved Zepbound single-dose vials through LillyDirect Self Pay Pharmacy Solutions at USD 349 to USD 499 per month, which created a lower-priced branded route for cash-pay patients and widened access beyond traditional insured dispensing. Lilly then extended that model through Walmart Pharmacy retail pick-up in October 2025, which reduced delivery friction while keeping the direct channel intact. This shift matters because the Mounjaro market can now capture patients who were priced out of conventional branded incretin access but are still willing to self-pay for therapy. The result is that format mix is becoming a commercial strategy issue, not just a device preference issue, within the mounjaro industry.

By Strength: High-Dose Dominance Reflects Clinical Titration Endpoints

The 15 mg strength represented 24.67% of segment revenue in 2025 and is forecast to rise at 32.57% CAGR through 2031, which made it the largest single dose within the six-step titration ladder. This pattern shows that the mounjaro market derives its strongest value from maintenance doses rather than from early initiation doses that patients pass through for a shorter period. Lower strengths remain essential because the treatment protocol requires stepwise titration, but they function more as pathway points than as the main long-duration revenue anchors. In practical terms, this keeps all strengths relevant while concentrating the highest commercial value toward the upper end of the ladder.

Strength mix also depends on how well patients stay on therapy long enough to reach and maintain higher doses. Lilly’s decision to make all 6 approved Zepbound vial doses available through LillyDirect reduced dose-access gaps and gave self-pay patients a more complete branded pathway from titration to maintenance. Real-world research published in 2026 showed that 1-year persistence among GLP-1 receptor agonist initiators improved sharply through the first half of 2024, which suggests that better availability and smoother access can materially improve continuity. As persistence improves, the Mounjaro market is likely to see a greater share of prescriptions settling into high-value maintenance strengths. That creates a reinforcing effect where better supply and access support higher realized value per treated patient over time.

By Distribution Channel: Online Channels Rewrite Pharmacy Economics

Retail pharmacies held 39.03% of revenue in 2025, which kept them as the largest dispensing route in the mounjaro market because insured diabetes patients were already tied to standard pharmacy benefit flows. Hospital Pharmacies remained important for inpatient initiation and specialist-managed care, where titration could be monitored in structured settings. The Mounjaro market also continued to depend on physical dispensing infrastructure because cold-chain handling and counseling are still central to injectable therapy use. Online pharmacies, however, are projected to grow at 33.94% CAGR through 2031 and are reshaping how self-pay access is organized.

That change is being driven by brand-controlled direct distribution rather than by generic e-commerce expansion alone. LillyDirect became a major entry point for self-pay Zepbound access, and Lilly stated that the platform accounted for a large share of new prescriptions before the Walmart pick-up extension broadened convenience further. The online route matters because the Mounjaro market can connect prescription generation, fulfillment, and patient follow-up more directly than in the legacy wholesale model. It also compresses the boundary between online and offline dispensing, since patients can begin through a digital path and still collect treatment through physical retail. This hybrid structure should allow the Mounjaro market to keep shifting toward higher online participation while preserving trust and access for patients who prefer store-based pickup.

By End User: Primary Care Migration Unlocks Population-Scale Prescribing

Hospitals accounted for 35.63% of revenue in 2025, which reflected their role as the most established setting for early formulary adoption, complex titration, and specialist oversight. Specialty clinics remained a second concentration point because endocrinology and metabolic centers were early users of tirzepatide in both diabetes and obesity care. The mounjaro market also includes long-term care facilities and research institutions, but those settings contribute smaller volumes and tend to carry more targeted clinical use. This leaves hospitals as the current anchor, while the broader volume opportunity sits elsewhere.

Outpatient and primary care centers are forecast to grow at 34.74% CAGR through 2031, showing that the mounjaro market is migrating from specialist-led adoption into wider community prescribing. Real-world evidence published in Diabetes, Obesity and Metabolism showed rising tirzepatide initiation outside specialist settings, with primary care emerging as the fastest-growing prescriber category for weight-management use. This shift is commercially important because population-scale expansion depends on generalist adoption rather than on limited specialist capacity. It also introduces a management challenge because primary care physicians often need more support with titration and gastrointestinal side-effect monitoring than specialty centers do. Even so, the Mounjaro market stands to benefit materially as routine outpatient care becomes a larger gateway for both initiation and longer-term follow-up in the mounjaro industry.

Geography Analysis

North America accounted for 39.28% of the mounjaro market share in 2025, which kept it as the largest regional contributor. The United States remained the regional core because it had the broadest commercial infrastructure for tirzepatide, the deepest branded obesity demand, and the most advanced direct-to-consumer channel development. Lilly reported USD 22.965 billion in U.S. Mounjaro revenue in FY2025, which showed how much of the global franchise was still concentrated in the domestic base. The region also benefited from the addition of the sleep apnea indication and from stronger availability after earlier supply constraints began to ease.

Asia-Pacific is forecast to grow at 36.04% CAGR through 2031, making it the fastest-expanding regional block in the Mounjaro market. The main reason is scale, because large diabetes populations and broad obesity need to create a much wider long-term treatment pool than most other regions can match. Lilly’s first-quarter 2026 results showed ex-U.S. Mounjaro revenue of USD 4.4 billion, up from USD 1.2 billion in the comparable period of 2025, which signals that international markets are now contributing at a much faster pace. The Mounjaro market in Asia-Pacific also benefits from a mix of mature and emerging demand centers, with established uptake in developed healthcare systems and growing launch momentum in large-volume countries. This makes Asia-Pacific the region where volume expansion is likely to outpace revenue realization most clearly as access broadens and pricing conditions become more varied.

Europe held a meaningful position in the 2025 mounjaro market, supported by established diabetes reimbursement and a large treated population across major Western markets. Growth is steadier in Europe because reimbursement review is generally more measured, especially for obesity use, even when clinical interest is strong. Lilly’s November 2025 decision to build a USD 3 billion oral medicine manufacturing facility in the Netherlands showed that the company views Europe as strategically important both for supply and for future platform expansion. Middle East and Africa, and South America remain earlier-stage opportunities in the Mounjaro market, with adoption still building from a smaller base. Their role in the forecast period is less about immediate share leadership and more about adding new pockets of demand as regulatory access and commercial infrastructure continue to improve.

Competitive Landscape

The mounjaro market remains structurally unusual because Eli Lilly controls 100% of tirzepatide supply across approved indications and geographies. This gives the company full control over manufacturing, channel design, pricing architecture, and label expansion, which is rarely seen at this revenue scale in large pharmaceuticals. The mounjaro market therefore, has very high concentration today, even though competitive pressure still exists through substitute therapies such as semaglutide and through Lilly’s own next-generation pipeline. Clinical data from SURMOUNT-5 and cardiovascular evidence across SURPASS-CVOT and SUMMIT have strengthened Lilly’s current defense by making tirzepatide harder to displace on efficacy and broader cardiometabolic relevance.

Manufacturing scale is the company’s most important strategic moat in the current Mounjaro market. Lilly’s disclosed U.S. investment program included a USD 27 billion manufacturing expansion announced in February 2025, a USD 6.5 billion active pharmaceutical ingredient facility in Texas announced in September 2025, and a USD 3.5 billion injectable medicine and device facility in Pennsylvania announced in January 2026. Those moves do more than add capacity because they also reduce the risk of shortage-linked disruption that previously opened room for compounded alternatives. The Mounjaro market is likely to stay favorable to Lilly while this scale advantage holds, since a rival cannot quickly replicate both volume and reliability in the same period. Lilly’s additional USD 4.5 billion commitment across Indiana manufacturing sites in January 2026 further shows that supply readiness is being treated as a commercial strategy, not only as an operations requirement.

Channel control is the third major layer of competitive positioning in the Mounjaro market. LillyDirect and the Walmart Pharmacy pick-up partnership gave Lilly a branded self-pay route that reduced reliance on conventional payer-mediated dispensing and created a closer link with patients who were otherwise harder to reach. The company is also preparing for the next phase of competition by building oral medicine manufacturing capacity in Europe, which points to the importance of future non-injectable metabolic products within the same broad franchise logic. Even with this advantage, the Mounjaro market will not remain insulated forever because next-generation multiagonists and alternative GLP-1 formats can narrow differentiation over time. For now, Lilly’s combination of evidence depth, supply expansion, and direct channel innovation keeps the Mounjaro market firmly in its control.

Mounjaro Industry Leaders

Eli Lilly and Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Eli Lilly reported Q1 2026 worldwide Mounjaro revenue of USD 8.7 billion, up 125% year-on-year; the company raised full-year 2026 revenue guidance to USD 82-85 billion. Ex-US Mounjaro revenue reached USD 4.4 billion in a single quarter, reflecting rapid volume growth in NRDL-listed markets, including China.

- February 2026: Eli Lilly reported FY2025 annual results with total revenues of USD 65.179 billion (44.7% YoY increase), becoming the world's top-earning pharmaceutical company by revenue ahead of Merck & Co., driven primarily by tirzepatide franchise growth.

- January 2026: Eli Lilly announced plans to invest more than USD 3.5 billion in a new injectable medicine and device manufacturing facility in Lehigh Valley, Pennsylvania—the company's 10th US manufacturing site since 2020—to produce next-generation weight-loss therapies, including retatrutide.

- January 2026: Eli Lilly committed an additional USD 4.5 billion across its Lebanon, Indiana manufacturing sites, expanding planned tirzepatide API production capacity and adding facilities for genetic medicine and next-generation pipeline compounds including orforglipron and retatrutide.

Global Mounjaro Market Report Scope

The Mounjaro market refers to the global commercial market for Mounjaro (tirzepatide), a prescription injectable medication developed by Eli Lilly and Company for the treatment of type 2 diabetes mellitus and, in many countries, chronic weight management under approved indications. The market encompasses the development, manufacturing, distribution, marketing, and sale of Mounjaro through hospitals, specialty clinics, retail pharmacies, and online pharmacies.

The Mounjaro market is segmented by indication, dosage form, strength, distribution channel, and end user. Based on indication, the market is categorized into Type 2 Diabetes, Chronic Weight Management, and Obstructive Sleep Apnea. By dosage form, the market is divided into Single-Dose Pen and Single-Dose Vial. Based on strength, the market includes 2.5 mg, 5 mg, 7.5 mg, 10 mg, 12.5 mg, and 15 mg formulations. By distribution channel, the market is segmented into Hospital Pharmacies, Retail Pharmacies, and Online Pharmacies. Based on end user, the market comprises Hospitals, Specialty Clinics, Outpatient and Primary Care Centers, Long-Term Care Facilities, and Research and Academic Institutions.

| Diagnosis Method | Chest X-Ray |

| CT Scan | |

| Sputum Culture | |

| Blood Tests | |

| Pulse Oximetry | |

| Treatment Type | Antibiotics |

| Oxygen Therapy | |

| Hospitalization | |

| Supportive Care |

| Bacterial Pneumonia |

| Viral Pneumonia |

| Fungal Pneumonia |

| Atypical Pneumonia |

| Infants |

| Children |

| Adults |

| Geriatric Population |

| Chronic Diseases |

| Smoking |

| Alcoholism |

| Weakened Immune System |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Diagnosis & Treatment | Diagnosis Method | Chest X-Ray |

| CT Scan | ||

| Sputum Culture | ||

| Blood Tests | ||

| Pulse Oximetry | ||

| Treatment Type | Antibiotics | |

| Oxygen Therapy | ||

| Hospitalization | ||

| Supportive Care | ||

| By Pathogen Type | Bacterial Pneumonia | |

| Viral Pneumonia | ||

| Fungal Pneumonia | ||

| Atypical Pneumonia | ||

| By Age Group | Infants | |

| Children | ||

| Adults | ||

| Geriatric Population | ||

| By Risk Factors | Chronic Diseases | |

| Smoking | ||

| Alcoholism | ||

| Weakened Immune System | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is driving mounjaro's revenue growth through 2031?

Growth is being supported by expansion across diabetes, chronic weight management, and obstructive sleep apnea, along with wider access through LillyDirect and major manufacturing investments.

How large is mounjaro expected to become by 2031?

The mounjaro market is forecast to reach USD 118.79 billion by 2031, rising from USD 29.69 billion in 2026 at a 31.95% CAGR.

Which indication contributes the most revenue for tirzepatide today?

Type 2 diabetes remained the largest indication in 2025 with 56.03% of revenue, which kept it as the commercial anchor even as obesity-related use expanded faster.

Which region is growing fastest for Mounjaro sales?

Asia-Pacific is projected to post the fastest growth through 2031 with a 36.04% CAGR, supported by large patient pools and rising international uptake.

Why are online pharmacies gaining importance for tirzepatide access?

Online channels are growing quickly because LillyDirect connects self-pay prescribing, fulfillment, and follow-up more directly, and the Walmart pick-up option added retail convenience.

Page last updated on: