Motion Positioning Stages Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

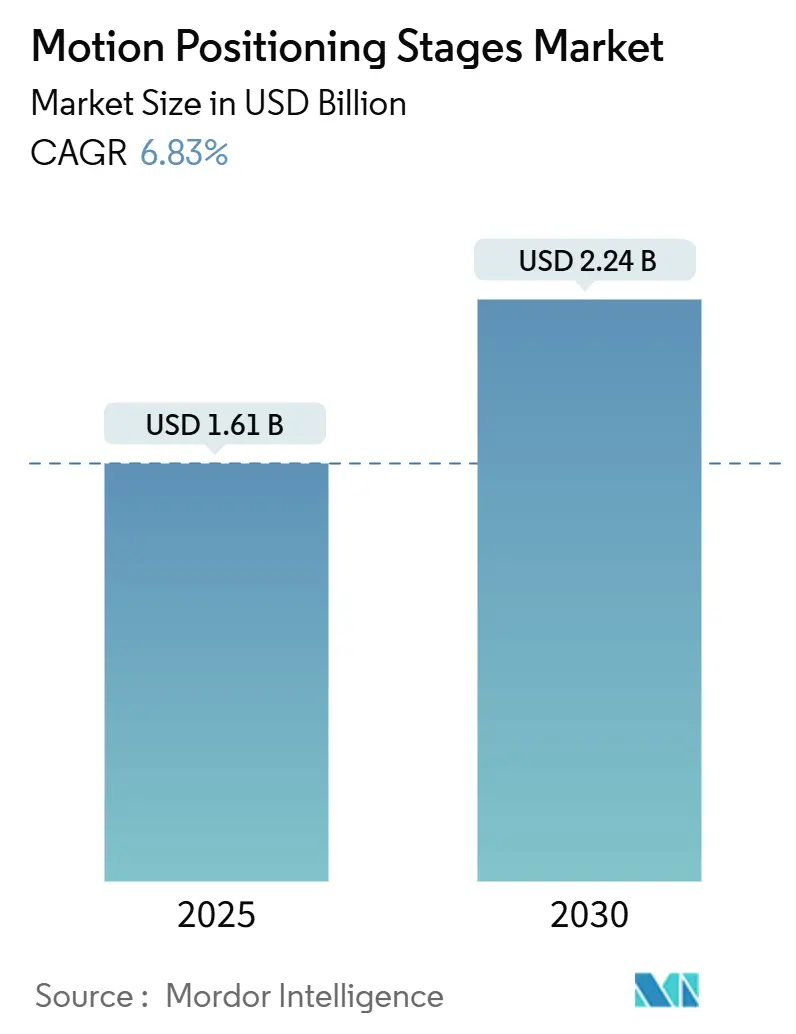

| Market Size (2025) | USD 1.61 Billion |

| Market Size (2030) | USD 2.24 Billion |

| Growth Rate (2025 - 2030) | 6.83% CAGR |

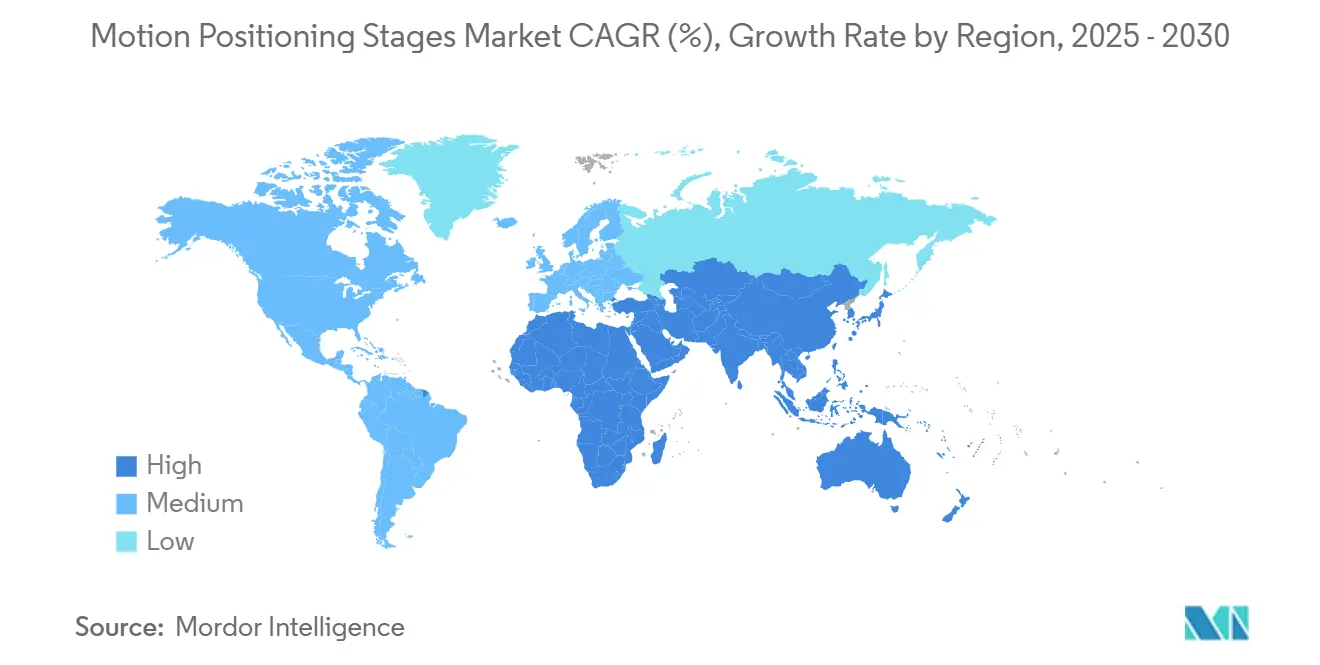

| Fastest Growing Market | Africa |

| Largest Market | Asia Pacific |

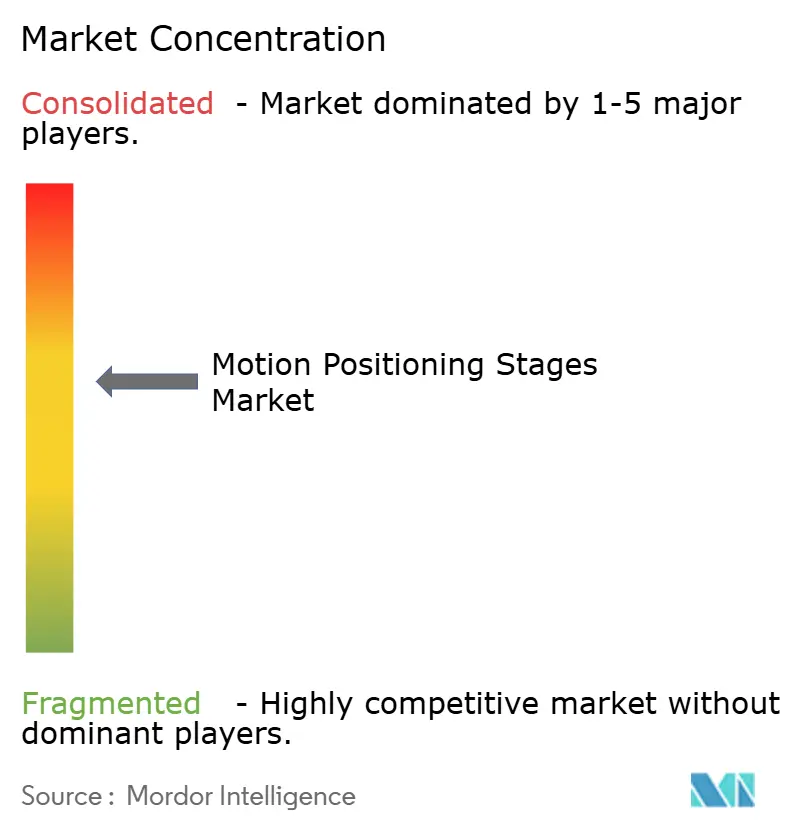

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Motion Positioning Stages Market Analysis by Mordor Intelligence

The motion positioning stages market size is estimated at USD 1.61 billion in 2025 and is projected to reach USD 2.24 billion by 2030, growing at a 6.83% CAGR. Robust semiconductor capital expenditure, surging demand for automated microscopy, and precision requirements in aerospace optical payloads are steering revenue expansion. Linear stages continue to anchor wafer transport lines, while XYZ platforms gain momentum as heterogeneous integration moves mainstream. Motorized mechanisms remain the leading drive class, though piezoelectric actuators are scaling quickly as quantum laboratories and atomic-scale metrology specify electromagnetic-silent motion. Semiconductor manufacturing still delivers the largest shipment volumes; however, life sciences workflows are the fastest-growing opportunity, as drug discovery automates imaging and liquid handling tasks. Regionally, the Asia-Pacific dominates shipments, driven by multi-billion-dollar fab projects in China and South Korea. In contrast, Africa posts the highest growth rate, largely due to automotive localization and electronics assembly projects.

Key Report Takeaways

- By stage type, linear stages commanded a 41.22% market share of the motion positioning stages market in 2024, while XYZ positioning stages are expected to expand at a 7.91% CAGR through 2030.

- By drive mechanism, motorized platforms held 58.76% of the motion positioning stages market size in 2024, and piezoelectric units are forecast to grow at 7.48% through 2030.

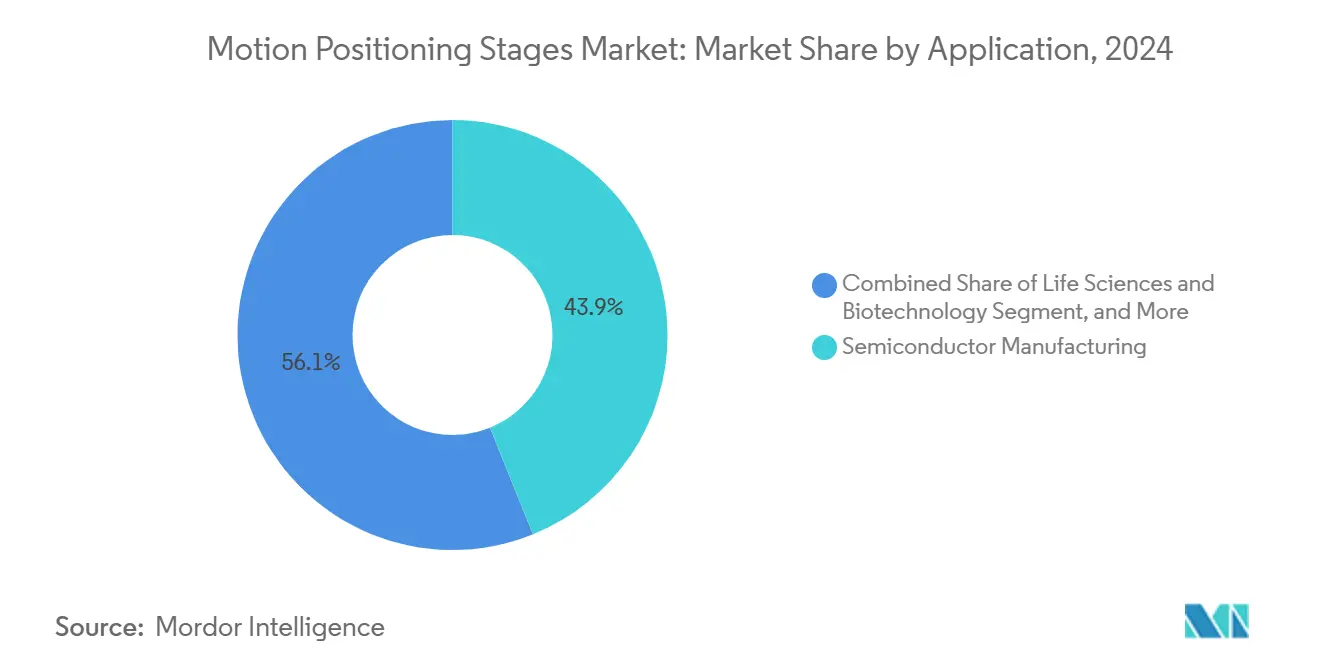

- By application, semiconductor manufacturing is projected to deliver 43.89% of the revenue in 2024, whereas life sciences and biotechnology are projected to register an 8.13% CAGR through 2030.

- By end-user industry, electronics accounted for 39.17% of the 2024 demand, and healthcare is poised to grow at a 7.83% CAGR through 2030.

- By geography, the Asia-Pacific region captured 45.32% of the revenue in 2024, while Africa is projected to grow at a rate of 7.89% through 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Motion Positioning Stages Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating Demand for Sub-Micron Semiconductor Lithography | +1.8% | Asia-Pacific core, spill-over to North America and Europe | Medium term (2-4 years) |

| Proliferation of High-Throughput Automated Microscopy Platforms | +1.3% | Global, with concentration in North America and Europe | Short term (≤ 2 years) |

| Rapid Adoption of Laser-Based Additive Manufacturing Lines | +1.1% | North America and Europe, emerging in Asia-Pacific | Medium term (2-4 years) |

| Integration of Smart Encoders for Predictive Maintenance | +0.9% | Global, led by North America and Germany | Long term (≥ 4 years) |

| Miniaturization Trend in Quantum Research Instrumentation | +0.7% | North America and Europe, nascent in China | Long term (≥ 4 years) |

| Growing Capital Investments in Advanced Packaging Facilities | +1.5% | Asia-Pacific dominant, secondary in North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerating Demand for Sub-Micron Semiconductor Lithography

Gate-all-around transistor roadmaps and backside power delivery are driving lithography toolmakers to specify reticle and wafer stages with repeatability of less than 5 nm. ASML’s extreme-ultraviolet scanners, which generated EUR 7.9 billion (USD 8.6 billion) in revenue in 2024, rely on magnetically levitated stages that achieve 2 nm accuracy across 150 mm travel ranges.[1]ASML Holding, “Annual Report 2024,” ASML.com Taiwan Semiconductor Manufacturing Company’s 2 nm node, entering volume production in 2025, requires 1.5 nm overlay precision, prompting the adoption of interferometric feedback with picometer resolution. Intel’s USD 20 billion Arizona fabs feature 18 next-generation lithography systems, each embedding up to eight high-precision stages. High-numerical-aperture scanners expected in 2027 will push thermal-stability specs even lower, keeping demand elevated well into the forecast window.

Proliferation of High-Throughput Automated Microscopy Platforms

Drug discovery is shifting from manual slide review to robotic imaging that screens 384-well plates within minutes. Thermo Fisher Scientific’s CX7 platform positions samples with 0.5 µm repeatability at 50 mm s-1, enabling phenotypic assays across 10,000 fields of view per plate.[2]Thermo Fisher Scientific, “CX7 High-Content Screening Platform Product Launch,” ThermoFisher.com The National Institutes of Health allocated USD 1.2 billion to shared instrumentation in 2024, with roughly one-third of the funds designated for automated imaging systems. Spatial transcriptomics workflows now require closed-loop Z-stages that maintain a 1 µm focus across large tissue sections. Combined, these factors reduce lead-optimization timelines by 40%, spurring laboratories to invest in higher-throughput motion platforms.

Rapid Adoption of Laser-Based Additive Manufacturing Lines

Metal additive manufacturing has moved from prototypes to serial production. General Electric’s Auburn plant produces 40,000 fuel nozzles annually using stages that maintain 20 µm accuracy across 400 mm build areas. The Federal Aviation Administration certified its first additively manufactured turbine blade in 2024, cementing traceability requirements that hinge on precise motion logs. Boeing’s USD 50 million additive facility adopted hybrid machines with rotary and linear stages to replicate complex blade profiles during repair cycles. These milestones validate high-precision motion as a production necessity rather than a research luxury.

Integration of Smart Encoders for Predictive Maintenance

Embedding temperature and vibration sensors inside linear encoders is lowering unplanned downtime. Siemens’ Sinumerik One platform ingests encoder telemetry and flags bearing degradation weeks in advance, allowing fabs to coordinate repairs during scheduled stops.[3]Siemens, “Sinumerik One CNC Platform Release,” Siemens.com International Society of Automation studies show condition-based strategies trim downtime by up to 35%. As stages migrate into safety-critical proton-therapy gantries, smart encoders are becoming a de facto standard to satisfy functional-safety requirements.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Initial Capital Outlay for Nanopositioning Systems | -1.2% | Global, acute in emerging markets | Short term (≤ 2 years) |

| Thermal Drift Challenges in Ultra-Precision Environments | -0.8% | Global, concentrated in semiconductor and optics sectors | Medium term (2-4 years) |

| Supply Chain Volatility of Precision Linear Guides | -0.9% | Global, most severe in North America and Europe | Short term (≤ 2 years) |

| Shortage of Skilled Mechatronics Engineers | -0.7% | North America and Europe, emerging in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Initial Capital Outlay for Nanopositioning Systems

A closed-loop piezo stage with 100 µm travel typically costs USD 40,000-60,000, versus USD 8,000-12,000 for an open-loop motorized equivalent, a five-fold premium that strains university and start-up budgets. Import duties in emerging economies add another 15-25%, and ancillary infrastructure, such as vibration isolation, can tack on USD 10,000-20,000. Lease programs cut upfront spending by as much as 70%, but remain scarce outside North America and Western Europe.

Thermal Drift Challenges in Ultra-Precision Environments

Aluminum stages expand 23 µm m-1 °C-1, generating positional errors that exceed tolerances in sub-100 nm applications. Semiconductor metrology tools must be recalibrated every 30 minutes, which can trim throughput by up to 15%. Granite frames cut expansion fivefold but triple the mass, hampering dynamic performance. Active cooling adds cost and introduces new failure modes, while the absence of harmonized ISO test protocols forces buyers to conduct in-house validation that prolongs procurement cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Stage Type: Linear Stages Anchor Wafer Handling

Linear stages secured a 41.22% motion positioning stages market share in 2024, reflecting their embedded role in wafer transfer and inspection cells. Installed bases exceed 50,000 tool sets worldwide, each containing multiple axes. XYZ platforms are forecast to grow 7.91% as chiplet assembly mandates synchronous control across three translational axes. Rotary units remain vital for angular indexing in laser machining, albeit at lower growth rates. Gantry systems, meanwhile, are scaling in flat-panel display lines and large-format additive printing that require meter-scale work envelopes. Vendors now merge coarse linear travel with piezo tip-tilt inserts, simplifying the bill of materials and reducing system cost.

The migration from ball-screw to linear-motor drives triples acceleration and reduces maintenance needs. HIWIN reported 35% year-over-year growth in linear-motor shipments in 2024, as Chinese display makers retooled for 10.5-generation glass. Direct-drive rotary tables reduce backlash to under 1 arcsecond, meeting the specifications for fiber-optic connector alignment. Carbon-fiber gantry beams lower moving mass 40%, enabling faster traverse without compromising stiffness. Miniaturized XY stages with 50 mm footprints and 5 µm repeatability unlock handheld diagnostic devices, expanding addressable use cases.

By Drive Mechanism: Piezoelectric Gains on Motorized Incumbents

Motorized mechanisms accounted for 58.76% of 2024 revenue, primarily due to their long travel ranges and off-the-shelf controller compatibility. Piezoelectric platforms, however, are projected to grow at a 7.48% CAGR, buoyed by quantum computing labs that demand sub-nanometer resolution with minimal electromagnetic noise. Stroke limitations under 200 µm necessitate hybrid coarse-fine assemblies, which add mechanical complexity yet deliver unbeatable repeatability. Manual stages decline gradually but retain relevance in cost-constrained prototyping. Voice-coil and ultrasonic motors occupy niche roles, although Parker Hannifin’s hybrid coarse-linear plus piezo-fine stage, launched in 2024, signals the emergence of multi-mechanism architectures.

Multilayer actuator advances boosted piezo force output by 50% between 2020 and 2024, while reducing hysteresis to 5%. Absolute encoders now equip many motorized axes, eliminating the need for lengthy homing routines. Manual units gain digital readouts, blurring category lines and extending service life in semi-automated labs.

By Application: Life Sciences Outpaces Semiconductor Growth

Semiconductor tools accounted for 43.89% of application revenue in 2024, driven by the pervasive need for motion across lithography, etch, clean, and metrology. The life sciences and biotechnology sector is projected to grow at an 8.13% CAGR to 2030, driven by the need for spatial biology workflows that require micron-level registration over extended time-lapse imaging. Optics and photonics benefit from data-center upgrades that require precise fiber alignment, while industrial automation offers steady retrofit demand in electronics assembly and battery manufacturing. Aerospace and defense, though lower in volume, commands premium pricing owing to MIL-STD qualification hurdles.

Spatial biology now involves imaging the same tissue section 20-40 times with different stains, requiring 1 µm registration over 12-hour scans. Illumina’s NovaSeq X leverages linear stages, achieving 0.3 µm repeatability to maintain 90% base-calling accuracy. Fast-steering mirrors on piezo tip-tilt platforms correct atmospheric turbulence in free-space optics. Collaborative robots integrate compliant stages that absorb positioning errors, broadening penetration in general manufacturing.

By End-User Industry: Healthcare Ascends Amid Robotics Surge

Electronics retained a 39.17% share in 2024 due to the high stage count inside semiconductor and display fabs. Healthcare, however, is expected to post a 7.83% CAGR as surgical robotics, digital pathology, and proton therapy embed high-accuracy motion. Automotive battery-cell lines require 0.5 mm placement accuracy during welding, fueling demand for rigid, high-payload stages. Aerospace and defense rely on radiation-hardened motion for orbital instruments. Research institutes, under budget constraints, consolidate purchasing into versatile motorized cores rather than niche piezo platforms.

Intuitive Surgical’s da Vinci robot uses six stages per arm to achieve 1-2 mm instrument placement. The U.S. Food and Drug Administration cleared the first fully digital pathology workflow in 2024, spurring hospitals to replace manual microscopes with automated scanners. Electronics plants deploy stages with integrated vision that cut surface-mount defect rates up to 30%.

Geography Analysis

Asia-Pacific commanded 45.32% revenue in 2024, underpinned by China’s USD 143 billion semiconductor-fab pipeline and South Korea’s USD 44 billion memory expansions. Dense electronics clusters in the Pearl and Yangtze River Deltas source dozens of stages per factory line, reinforcing regional dominance. Japan sustains ultra-high-precision demand through Nikon and Canon tool sets, albeit with muted growth. India’s USD 2.3 billion incentive scheme is driving greenfield smartphone assembly, targeting mid-tier XY stages. Australia adopts automated mineral-analysis rigs employing linear motion under harsh mine-site conditions.

North America accounted for 28% of the revenue, driven by USD 52 billion in CHIPS Act subsidies that fund new fabs in Arizona, Ohio, and New York. Boston and San Francisco life-science clusters account for more than 300 automated microscopes shipped in 2024. Canada’s aerospace sector specifies 10-µm accuracy for turbine-blade repair rigs, while Mexico’s television factories are migrating to fully automated optical inspection, adding thousands of stage units annually.

Europe captured 22% of the revenue, with Germany’s machine-tool builders embedding stages in laser cutters and CNC centers, and the United Kingdom’s photonics firms ordering fiber-alignment platforms. The European Chips Act, budgeted at EUR 43 billion (USD 47 billion), is set to catalyze stage demand once fabs in Germany, France, and Italy break ground.

Africa is forecast to grow at a rate of 7.89% through 2030. South Africa’s automotive hubs localize sensor and ECU assembly, requiring precision pick-and-place stages. Egypt’s USD 1.8 billion electronics plan introduces motorized inspection stages into nascent lines. Middle Eastern diversification sees the United Arab Emirates’ aerospace composite shops adopting 5-axis motion for trimming carbon parts. South America accounts for 4.8% of the revenue; Brazil’s Embraer utilizes 50 µm-accuracy inspection stages, while Argentina’s lithium producers automate sample preparation under high tariff burdens.

Competitive Landscape

The motion positioning stages market is moderately fragmented. The top five suppliers, PI Physik Instrumente, Aerotech, Thorlabs, Newport, and Parker Hannifin, collectively command roughly 35-40% revenue, while numerous regional specialists occupy the remaining share. Nanopositioning below 10 nm remains largely a PI-Aerotech duopoly protected by capacitive-sensor and piezo-control patents. Motorized mid-tier stages face intense price pressure from Chinese vendors, such as HIWIN, whose linear-motor units can be 25-30% cheaper than those of their Western peers.

Competitive leverage is shifting to software ecosystems. Vendors now bundle motion libraries compatible with LabVIEW, Python, and MATLAB, reducing integration friction for OEM engineers. White-space opportunity lies in hybrid coarse-fine assemblies, such as Dover Motion’s patent for a linear plus voice-coil stack. Servitization emerges as Zaber Technologies rolls out cloud-connected stages that log performance data for remote diagnostics. Vertical integration accelerates; Thorlabs’ 2024 acquisition of a bearing-grinding facility secures supply and lifts margins. ISO 230-2 compliance has become a quasi-entry barrier, favoring incumbents with accredited calibration labs. Patent filings in 2024 showed 60% emphasis on trajectory optimization, vibration damping, and thermal compensation, underscoring software as the next battleground.

Motion Positioning Stages Industry Leaders

PI Physik Instrumente GmbH and Co. KG

Aerotech Inc.

Thorlabs Inc.

Newport Corporation

Parker Hannifin Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: PI Physik Instrumente announced a EUR 25 million (USD 27 million) expansion of its Karlsruhe piezo-actuator plant, boosting capacity 40% for quantum computing and semiconductor customers.

- September 2025: Aerotech partnered with TSMC on wafer stages targeting 1 nm overlay for high-NA EUV tools in a USD 15 million joint program.

- July 2025: Thorlabs acquired Steinmeyer Mechatronik, adding air-bearing stages up to 1 000 mm travel to its catalog.

- May 2025: Parker Hannifin introduced Trilogy 500 linear-motor stages with integrated absolute encoders and 1 µm repeatability.

Global Motion Positioning Stages Market Report Scope

The Motion Positioning Stages Market Report is Segmented by Stage Type (Linear Stages, Rotary Stages, Gantry Stages, XY Positioning Stages, XYZ Positioning Stages), Drive Mechanism (Motorized, Piezoelectric, Manual), Application (Semiconductor Manufacturing, Life Sciences and Biotechnology, Optics and Photonics, Industrial Automation, Aerospace and Defense, Research and Academia), End-User Industry (Electronics, Healthcare, Automotive, Aerospace and Defense, Research Institutes), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

| Linear Stages |

| Rotary Stages |

| Gantry Stages |

| XY Positioning Stages |

| XYZ Positioning Stages |

| Motorized |

| Piezoelectric |

| Manual |

| Semiconductor Manufacturing |

| Life Sciences and Biotechnology |

| Optics and Photonics |

| Industrial Automation |

| Aerospace and Defense |

| Research and Academia |

| Electronics |

| Healthcare |

| Automotive |

| Aerospace and Defense |

| Research Institutes |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Stage Type | Linear Stages | ||

| Rotary Stages | |||

| Gantry Stages | |||

| XY Positioning Stages | |||

| XYZ Positioning Stages | |||

| By Drive Mechanism | Motorized | ||

| Piezoelectric | |||

| Manual | |||

| By Application | Semiconductor Manufacturing | ||

| Life Sciences and Biotechnology | |||

| Optics and Photonics | |||

| Industrial Automation | |||

| Aerospace and Defense | |||

| Research and Academia | |||

| By End-User Industry | Electronics | ||

| Healthcare | |||

| Automotive | |||

| Aerospace and Defense | |||

| Research Institutes | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the projected value of the motion positioning stages market by 2030?

The market is forecast to reach USD 2.24 billion by 2030.

Which application area is expected to grow fastest through 2030?

Life sciences and biotechnology is projected to expand at an 8.13% CAGR on rising adoption of automated imaging and screening platforms.

Why are piezoelectric stages gaining traction despite higher cost?

Piezoelectric actuators deliver sub-nanometer repeatability without electromagnetic interference, a specification essential for quantum computing and atomic-scale metrology.

Which region currently leads global demand for motion positioning stages?

Asia-Pacific accounted for 45.32% of 2024 revenue, driven by heavy semiconductor and electronics investments.

How does predictive maintenance influence stage procurement decisions?

Encoders with embedded sensors enable condition-based maintenance, trimming unplanned downtime up to 35% and lowering total cost of ownership for high-volume manufacturers.

What level of accuracy do next-generation semiconductor lithography stages require?

Upcoming high-numerical-aperture extreme ultraviolet tools demand reticle and wafer stages capable of 1-2 nm overlay precision.

Page last updated on: