Mobile Collaboration Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 67.91 Billion |

| Market Size (2030) | USD 115.92 Billion |

| Growth Rate (2025 - 2030) | 11.29% CAGR |

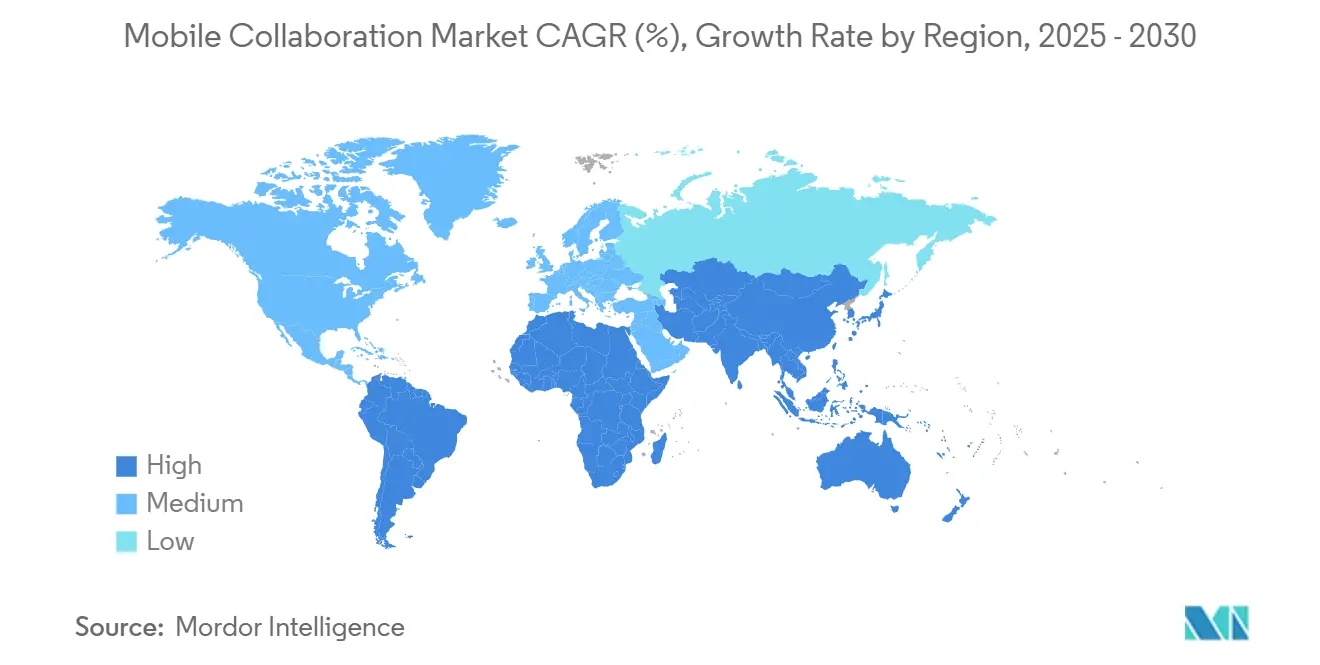

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

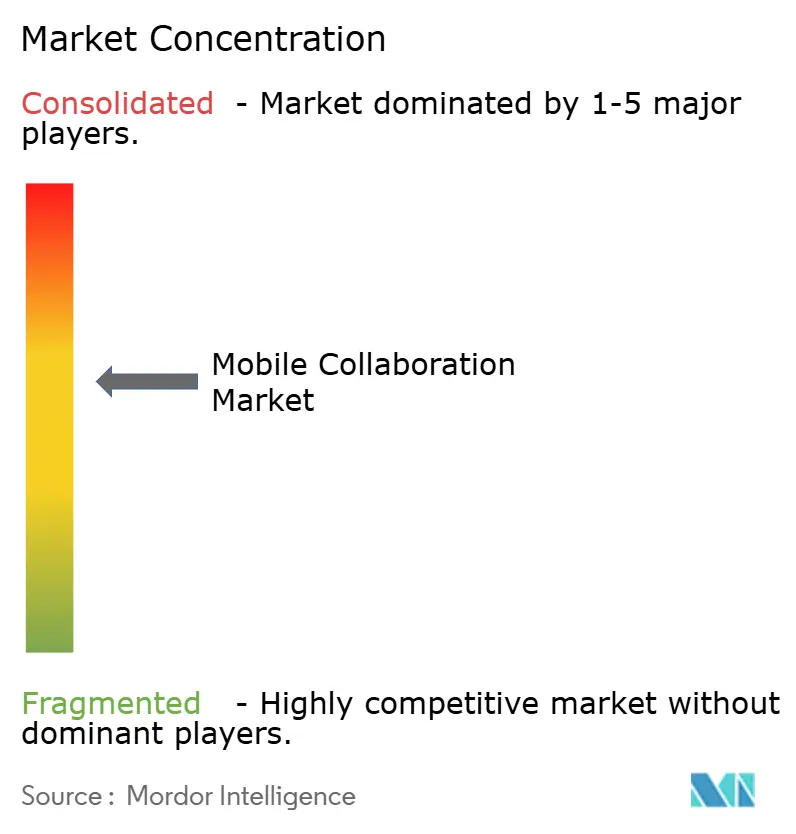

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mobile Collaboration Market Analysis by Mordor Intelligence

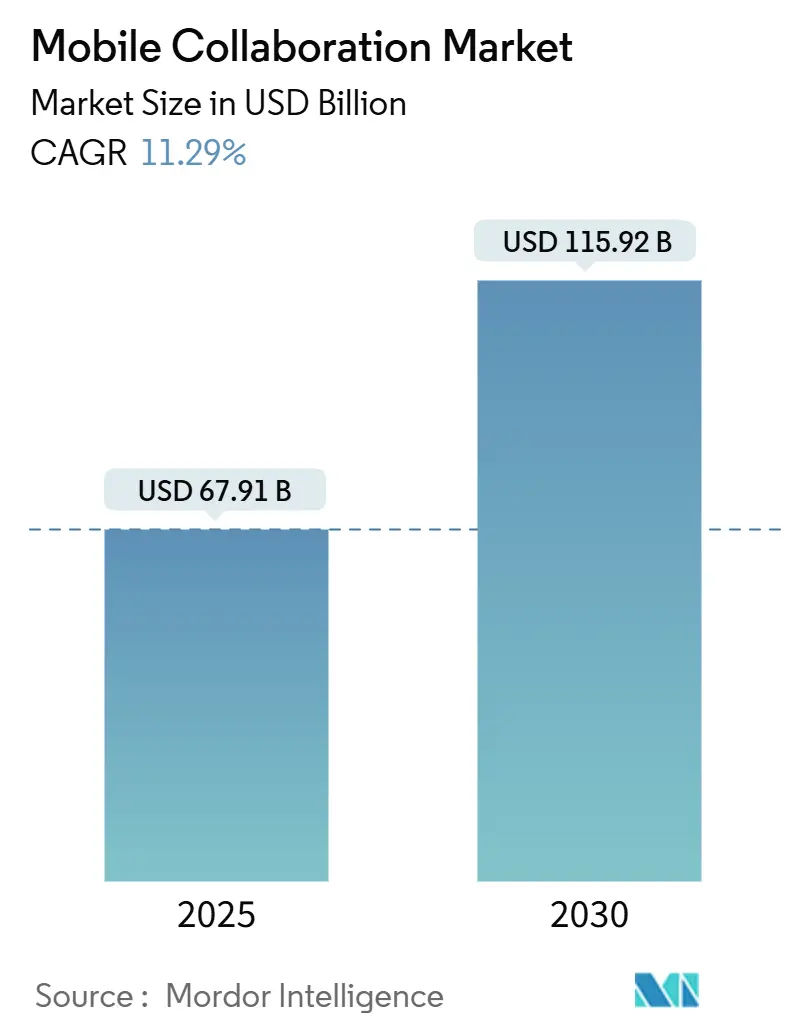

The mobile collaboration market size stands at USD 67.91 billion in 2025 and is projected to reach USD 115.92 billion by 2030, reflecting an 11.29% CAGR during the forecast period. 5G densification, sovereign-AI mandates that keep sensitive data on personal devices, and zero-trust security frameworks are key growth catalysts. Enterprises are replacing desktop-centric workflows with mobile-first architectures, while hyperscalers bundle chat, video, and file sharing directly into workplace suites, squeezing standalone vendors. No-code workflow builders are lowering IT barriers for small and medium enterprises (SMEs), and vertical-specific solutions are expanding addressable demand in regulated fields such as healthcare and financial services. Competitive intensity is rising as vendors embed generative-AI features that automate meeting notes, translations, and task assignments, creating fresh differentiation even in mature solution categories. Fragmented privacy laws, persistent mobile-endpoint threats, and high migration costs remain constraints, but their combined drag is outweighed by greenfield deployments in emerging economies and SME digital transformation programs.

Key Report Takeaways

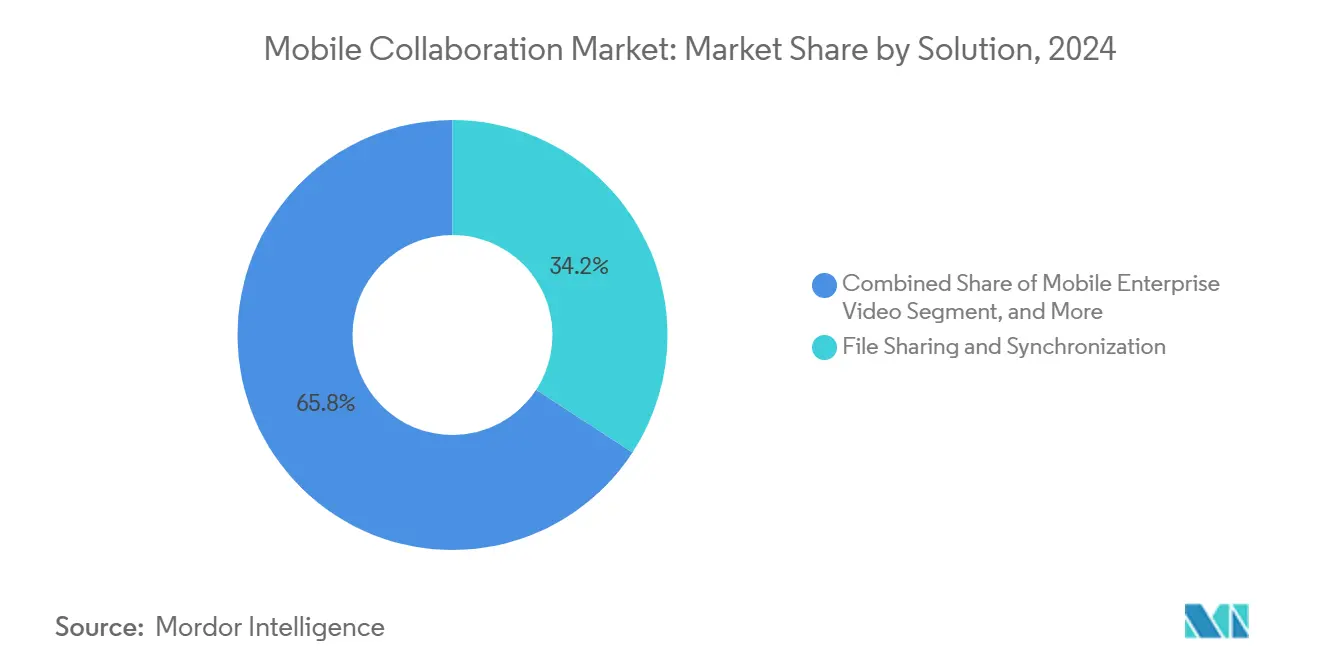

- By solution, File Sharing and Synchronization led with a 34.21% revenue share in 2024; Mobile Enterprise Video is projected to advance at a 11.46% CAGR through 2030.

- By service, Managed Services captured a 46.32% revenue share in 2024, while Training and Support Services showed the fastest forecast CAGR at 12.87% to 2030.

- By deployment mode, Cloud deployment accounted for 73.51% share of the mobile collaboration market size in 2024 and is forecast to grow at a 13.53% CAGR through 2030.

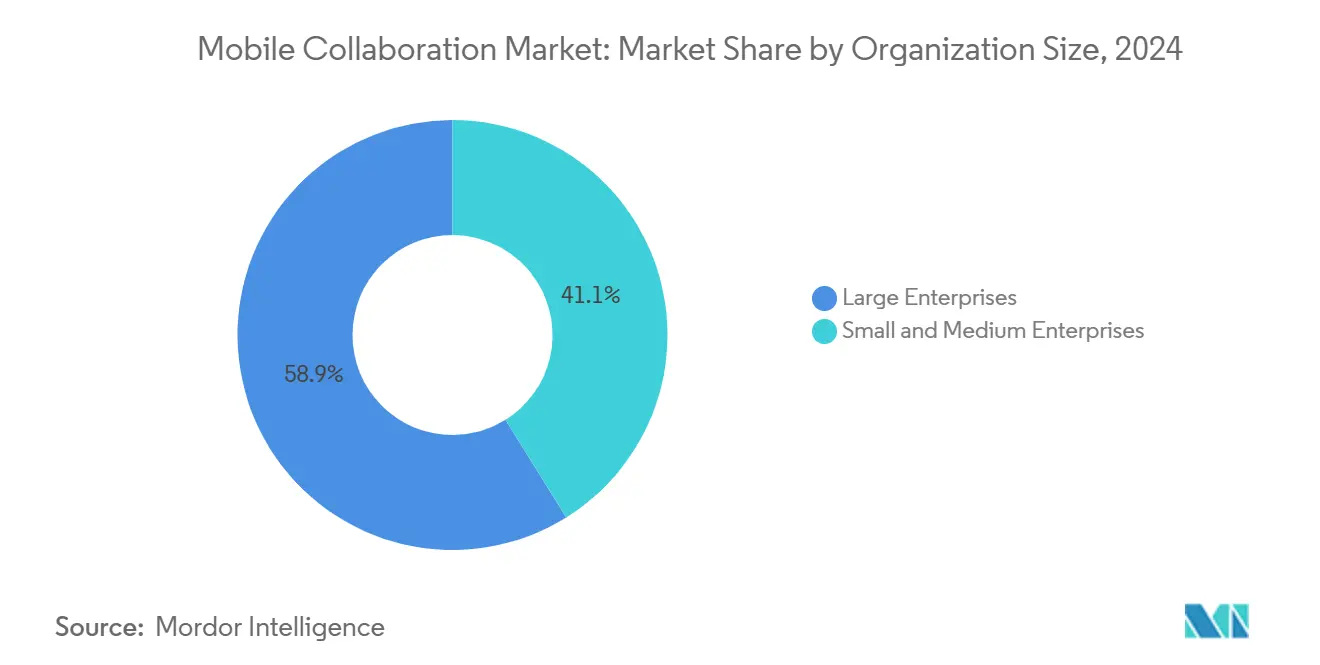

- By organization size, Large Enterprises held 58.87% of 2024 spending, whereas SMEs are expected to expand at a 13.12% CAGR through 2030.

- By end-user industry, Information Technology and Telecom commanded 21.32% of the 2024 revenue, while Healthcare is set to grow at a 12.78% CAGR through 2030.

- By geography, North America captured 38.58% of 2024 revenue; Asia Pacific is the fastest-growing region, advancing at a 12.42% CAGR through 2030.

Global Mobile Collaboration Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of 5G Enabled Mobile Devices | +2.1% | Global, early density in South Korea, China, United States | Medium term (2-4 years) |

| Surge in Remote Working Hybrid Work Policies | +2.4% | North America and Europe core, spillover to Asia Pacific urban centers | Short term (≤ 2 years) |

| Integration of AI Driven Collaboration | +1.9% | Global, led by North America and Western Europe | Medium term (2-4 years) |

| Rising Adoption of Cloud Native Suites | +1.7% | Global, accelerated in Asia Pacific and Latin America SMEs | Long term (≥ 4 years) |

| Need for Real-Time Data Sharing | +1.5% | Global, critical in Healthcare, Manufacturing, Energy, and Utilities | Short term (≤ 2 years) |

| Expansion of Enterprise Mobility Management | +1.3% | North America and Europe, emerging in Middle East and Asia Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proliferation of 5G Enabled Mobile Devices

Global 5G subscriptions reached 1.9 billion in 2024 and may surpass 5.6 billion by 2030, which lowers latency expectations for mobile collaboration. Sub-20 millisecond round-trip times enable real-time co-editing of CAD drawings and simultaneous 4K video streams on handheld devices. South Korea recorded a 140% rise in private enterprise 5G networks during 2024, driven by manufacturers embedding augmented-reality work instructions on assembly lines. Collaboration vendors are refactoring architectures for edge processing that runs on device or at cell towers, cutting backbone bandwidth spending while improving responsiveness. Emerging markets maintain a three-to-four-year adoption gap, creating a two-tier ecosystem in which premium features remain inaccessible to SMEs relying on 4G networks.

Surge in Remote Working Hybrid Work Policies

Hybrid-work policies now dominate operating models, as 58% of surveyed enterprises require two or three in-office days weekly. The arrangement fuels demand for asynchronous tools that support teams across New York, London, and Singapore without overlapping time zones. Channels that combine human users and automated workflow bots deliver 34% more messages than human-only channels, showing AI agents are taking on routine updates and approvals. Legacy video platforms optimized for scheduled meetings are losing favor to spontaneous tap-to-talk sessions, prompting Microsoft to launch Teams Connect, which lets external guests join shared channels without tenant switching. Differing labor rules, such as France’s right-to-disconnect law, require geo-fenced notifications, adding complexity for multinational deployments.

Integration of AI Driven Collaboration Features

Generative-AI has moved from pilot chatbots to indispensable workflow automation. Copilot for Teams earned USD 1.2 billion in annualized revenue nine months after launch. Stanford researchers found that AI-generated summaries compress post-meeting administrative tasks by 40% for 800 knowledge workers. Google’s Duet AI introduced in-meeting translation across 18 languages, aiding multilingual teams across the European Union. Liability concerns persist because AI summaries may misattribute statements, prompting legal teams to demand human validation. Vertical tuning gains traction, as ServiceNow embeds Claude into IT service workflows, showing that domain-specific language models outperform general models in accuracy.

Rising Adoption of Cloud Native Collaboration Suites

Cloud deployments held 73.51% revenue share in 2024 and are forecast to grow at 13.53% CAGR through 2030. On-premise hold-outs in finance and defense are shrinking as vendors add hybrid gateways that keep sensitive records local while routing routine traffic to the cloud. Box Shield accounted for 28% of net-new enterprise deals by automatically flagging anomalous file-sharing patterns, confirming that security drives differentiation within commoditized file sync. Subscription pricing democratizes enterprise-grade capabilities for SMEs, and compliance audits such as SOC 2 Type II have become minimum entry requirements.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent Concerns Around Mobile Data Security | -1.8% | Global, acute in Europe under GDPR and in U.S. under state privacy laws | Short term (≤ 2 years) |

| Limited Network Reliability in Emerging Economies | -1.4% | Africa, South Asia, Latin America rural regions | Long term (≥ 4 years) |

| Fragmented Regulatory Compliance Requirements | -1.1% | Global, most complex between EU, China, and United States | Medium term (2-4 years) |

| High Switching Costs for Legacy System Migration | -0.9% | North America and Europe large enterprises, especially BFSI and Healthcare | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistent Concerns Around Mobile Data Security and Privacy

Mobile devices accounted for 39% of breaches in 2024, up from 31% in 2023. Bring-your-own-device policies expand the attack surface because personal phones seldom run the same endpoint-detection agents as corporate laptops. Zero-trust frameworks enforce continuous authentication, yet only 22% of firms extend device-health checks to contractor phones. GDPR penalties of up to 4% of global revenue pressure vendors to adopt end-to-end encryption and regional data stores. These requirements add complexity and can raise latency when data sharding spans multiple jurisdictions.

Limited Network Reliability in Emerging Economies

Rural areas of Africa, South Asia, and Latin America still face average mobile download speeds below 10 Mbps. The International Telecommunication Union reports that 2.6 billion people remain offline, so real-time collaboration degrades to audio-only calls or asynchronous threads. Offline-first architectures allow local caching, but cause version conflicts when multiple users edit content during outages. The resulting two-tier ecosystem forces global teams to default to the least-connected member, often reverting to email attachments and losing real-time benefits.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution: Visual Communication Outpaces File Sync

Mobile Enterprise Video carries the highest forecast growth at 11.46% CAGR, reflecting rising demand for virtual diagnostics, field-service guidance, and real-time audits. File Sharing and Synchronization led the mobile collaboration market share with 34.21% in 2024, underscoring its maturity within the mobile collaboration market. AI-enabled search that tags files by context increases findability and prolongs relevance for file-centric platforms. Portals and Intranet Platforms act as single entry points for HR, IT, and news, favored by large enterprises operating complex ecosystems. Enterprise Social Networks struggle for adoption beyond niche forums as email and chat remain entrenched. Unified Messaging and Conferencing suites merge chat, video, and telephony to curb tool sprawl, while Project and Task Management solutions integrate tightly with Slack and Teams to capture data at execution moments. Cisco’s Webex Hologram demonstrates how immersive 3D presence can justify premium pricing for design reviews and high-stakes negotiations.

Second-tier segments are splintering along industry lines. Zoom for Healthcare bundles HIPAA-compliant virtual waiting rooms and e-prescription flows, addressing medical-specific regulations. Similar vertical plays emerge in finance and energy, where compliance certifications and workflow connectors out-rank feature parity. The solution mix therefore reflects both horizontal commoditization and vertical specialization, a pattern that accelerates competition but also expands total addressable demand within the mobile collaboration market.

By Services: Training Demand Surges Amid AI Adoption

Managed Services held 46.32% revenue share in 2024, yet Training and Support Services will grow at 12.87% CAGR through 2030 as enterprises seek to harness AI copilots. Continuous feature releases render annual training obsolete, prompting vendors to offer role-based upskilling tied to certification paths. ServiceNow’s partnership with Udemy exemplifies providers monetizing education alongside software. Managed-service partners evolve from ticket resolution to proactive optimization, using telemetry to surface unused features that improve productivity when activated. Professional Services, covering customization and integration, remain pivotal during migrations from on-premise to cloud platforms, especially in regulated sectors where identity management is complex.

Outcome-based contracting is emerging where systems integrators guarantee productivity gains or refund fees, aligning incentives between vendor and client. Enterprises thus view service partners as strategic advisors rather than cost centers, amplifying growth in the mobile collaboration industry. As AI features permeate every module, skill gaps widen, ensuring sustained demand for training over the forecast horizon.

By Deployment Mode: Cloud Dominance Accelerates

Cloud deployments captured 73.51% of mobile collaboration market share in 2024 and will expand at a 13.53% CAGR through 2030, confirming the secular move away from capex-heavy on-premise models. Zero-trust security and compliance certifications such as FedRAMP and C5 neutralize earlier objections about multi-tenant risks. Hybrid-cloud gateways allow sensitive workloads to stay on site while leveraging elastic compute for routine tasks, reducing latency gaps that once favored on-premise. Edge nodes located at base stations blur boundaries by bringing compute closer to users, so latency-sensitive sectors like trading floors can embrace cloud architectures without performance loss. On-premise deployments will persist in defense and select finance niches, yet represent a shrinking share of the mobile collaboration market size through 2030.

Subscription pricing lowers entry barriers for SMEs that lack dedicated IT staff. Vendors frequently bundle analytics, AI add-ons, and security upgrades into subscription tiers, allowing customers to scale features as needs evolve. As a result, lifetime value per user rises even when base-tier pricing remains flat. This monetization model boosts cloud revenue while guarding against churn, reinforcing the cloud segment’s centrality within the mobile collaboration market.

By Organization Size: SMEs Drive Growth as No-Code Tools Democratize Access

Large Enterprises commanded 58.87% spending in 2024, yet SME expenditure will grow at 13.12% CAGR, twice the pace of their larger counterparts. No-code builders and pre-configured templates enable smaller firms to automate approvals and content routing without expensive integrators. Freemium tiers accelerate adoption, and premium conversion typically occurs within 90 days when tangible ROI emerges. Monday.com reported an 18% rise in average revenue per SME user following the rollout of AI-based timeline optimization. Large Enterprises retain higher absolute budgets as they integrate collaboration with ERP and CRM layers, but saturation limits incremental growth. Consolidation is also likely to deepen as global rollouts fold regional pilots into single-vendor agreements.

SMEs favor vendors that offer transparent pricing and rapid onboarding. High churn risk demands ongoing product innovation such as embedded e-signatures and universal search. Conversely, Large Enterprises lock into multi-year licensing that bundles collaboration with productivity suites, insulating incumbents. This dual-speed dynamic drives vendors to segment roadmaps, maintaining consumer-grade usability for SMEs while adding governance controls for large accounts.

By End-User Industry: Healthcare Leads Growth as Telemedicine Embeds Collaboration

Information Technology and Telecom led spending at 21.32% in 2024, reflecting early adoption maturity. Healthcare, however, will post a 12.78% CAGR through 2030 as electronic health-record interoperability mandates embed collaboration tools in clinical workflows. Telemedicine visits rely on real-time video, secure messaging, and integrated diagnostics, driving demand for HIPAA-compliant platforms. Manufacturing deploys augmented-reality overlays that let remote experts annotate live feeds, cutting downtime and travel expenses. Financial services integrate video consults with portfolio dashboards and e-signature flows, bolstering hybrid wealth-advisory models. Retail shifts from walkie-talkies to smartphone-based scheduling and stock checks, while energy utilities coordinate outage response via real-time location sharing.

Public agencies lag due to procurement cycles and stringent certifications, yet pandemic experience broke resistance to remote work, spurring adoption across education, public safety, and social services. Media firms use cloud collaboration to share large video files across distributed editing teams, eliminating shipping delays. The vertical expansion confirms that sector-specific compliance and workflow connectors increasingly dictate platform selection within the mobile collaboration market.

Geography Analysis

North America generated 38.58% of 2024 revenue in the mobile collaboration market, led by the United States, where technology, healthcare, and finance sectors dominate demand. Canada’s bilingual mandates reward vendors that localize interfaces into French, and Mexico’s nearshoring trend ties factories to design hubs through mobile collaboration. Market maturity tempers growth, yet AI upgrades provoke renewal cycles as firms license Copilot and Duet features.

Asia Pacific is the fastest-growing region with a 12.42% CAGR forecast to 2030, propelled by China’s Digital Silk Road, India’s incentive schemes for 5G, and Japan’s work-style reforms. Domestic Chinese platforms such as DingTalk thrive under data-localization laws that limit foreign providers. Indian startups emphasize regional language support and low-bandwidth resilience, while multinationals maintain Teams and Workspace for global integration. Japan’s aging workforce depends on AI-translation and voice-to-text, and South Korea fields cutting-edge 5G and AR pilots, turning it into an innovation testbed.

Europe presents a fragmented landscape shaped by GDPR, which forces in-region data residency. The United Kingdom, Germany, and France account for most spending, driven by financial-sector regulation such as DORA. Southern European SMEs adopt cloud suites through government subsidies. In the Middle East, smart-city programs in Saudi Arabia and the UAE bundle collaboration into digital-service mandates, while Africa remains bandwidth constrained, fostering mobile-first tools optimized for intermittent connectivity. South America’s growth centers on Brazil and Argentina, though currency swings inject volatility into IT budgeting.

Competitive Landscape

Microsoft, Google, and Cisco jointly held roughly 45% of the mobile collaboration market revenue in 2024, supplying bundled suites that commoditize chat and video while monetizing AI add-ons. Atlassian’s USD 975 million purchase of Loom highlights a premium on asynchronous video capability. White-space niches remain in compliance-heavy verticals, where Zoom for Healthcare and Symphony offer specialized workflows. Disruptors such as Monday.com and Smartsheet capture project-centric collaboration by fusing task management with communication.

Patent activity intensifies; Microsoft secured rights for sentiment detection during calls, and Cisco patented 3D spatial audio to replicate in-person acoustics. The EU Digital Markets Act accelerates interoperability, compelling vendors to let Teams message Slack users by 2026. Consolidation continues, but cloud-native startups persistently emerge, maintaining a healthy innovation pipeline within the mobile collaboration market.

Mobile Collaboration Industry Leaders

Cisco Systems Inc.

Microsoft Corporation

Google LLC

Slack Technologies LLC

Zoom Video Communications Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Microsoft released Copilot for Teams with GPT-4, earning USD 1.2 billion in annualized revenue within nine months.

- October 2024: Atlassian closed its USD 975 million Loom acquisition, adding asynchronous video to Jira and Confluence.

- September 2024: Zoom launched HIPAA-compliant Zoom for Healthcare featuring virtual waiting rooms and e-prescription links.

- August 2024: Cisco unveiled Webex Hologram, projecting 3D avatars into physical rooms via AR headsets.

Global Mobile Collaboration Market Report Scope

The Mobile Collaboration Market encompasses a range of solutions and services that facilitate real-time communication, information sharing, and teamwork across mobile devices within enterprise environments. It includes solutions such as portals and intranet platforms, file sharing and synchronization, mobile enterprise video, enterprise social networks, unified messaging and conferencing, and project or task management tools, supported by managed, professional, and training services. The market spans both cloud and on-premise deployment models, serving organizations of all sizes across various industries, including BFSI, public sector, healthcare, energy and utilities, retail, IT and telecom, travel and hospitality, manufacturing, and media and entertainment.

The Mobile Collaboration Market Report is Segmented by Solution (Portals and Intranet Platforms, File Sharing and Synchronization, Mobile Enterprise Video, Enterprise Social Network, Unified Messaging and Conferencing, Project and Task Management Tools), Services (Managed Services, Professional Services, Training and Support Services), Deployment Mode (Cloud, On-Premise), Organization Size (Small and Medium Enterprises, Large Enterprises), End-User Industry (Banking Financial Services and Insurance, Public Sector, Healthcare, Energy and Utilities, Retail, Information Technology and Telecom, Travel and Hospitality, Manufacturing, Media and Entertainment), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Portals and Intranet Platforms |

| File Sharing and Synchronization |

| Mobile Enterprise Video |

| Enterprise Social Network |

| Unified Messaging and Conferencing |

| Project and Task Management Tools |

| Managed Services |

| Professional Services |

| Training and Support Services |

| Cloud |

| On-Premise |

| Small and Medium Enterprises |

| Large Enterprises |

| Banking Financial Services and Insurance |

| Public Sector |

| Healthcare |

| Energy and Utilities |

| Retail |

| Information Technology and Telecom |

| Travel and Hospitality |

| Manufacturing |

| Media and Entertainment |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Kenya | ||

| Rest of Africa | ||

| By Solution | Portals and Intranet Platforms | ||

| File Sharing and Synchronization | |||

| Mobile Enterprise Video | |||

| Enterprise Social Network | |||

| Unified Messaging and Conferencing | |||

| Project and Task Management Tools | |||

| By Services | Managed Services | ||

| Professional Services | |||

| Training and Support Services | |||

| By Deployment Mode | Cloud | ||

| On-Premise | |||

| By Organization Size | Small and Medium Enterprises | ||

| Large Enterprises | |||

| By End-User Industry | Banking Financial Services and Insurance | ||

| Public Sector | |||

| Healthcare | |||

| Energy and Utilities | |||

| Retail | |||

| Information Technology and Telecom | |||

| Travel and Hospitality | |||

| Manufacturing | |||

| Media and Entertainment | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Spain | |||

| Italy | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| India | |||

| Japan | |||

| Australia | |||

| South Korea | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Kenya | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the mobile collaboration market in 2030?

The mobile collaboration market is forecast to reach USD 115.92 billion by 2030, up from USD 67.91 billion in 2025.

Which deployment mode grows fastest through 2030?

Cloud deployment grows at a 13.53% CAGR, driven by zero-trust security and subscription pricing that favor rapid adoption.

Why is healthcare the fastest-growing end-user segment?

Healthcare expands at a 12.78% CAGR because telemedicine and electronic health record mandates embed collaboration into clinical workflows.

How will 5G influence mobile collaboration adoption?

Sub-20 millisecond latency and private 5G networks enable real-time video diagnostics and AR guidance, accelerating enterprise uptake worldwide.

Which region leads revenue and which grows fastest?

North America leads revenue with 38.58% of 2024 spending, while Asia Pacific records the swiftest growth at 12.42% CAGR through 2030.

What is the main security concern restraining adoption?

Mobile endpoints remain breach-prone, with 39% of 2024 incidents traced to compromised devices, prompting costly zero-trust rollouts.

Page last updated on: