Minoxidil Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.39 Billion |

| Market Size (2031) | USD 2.99 Billion |

| Growth Rate (2026 - 2031) | 4.57% CAGR |

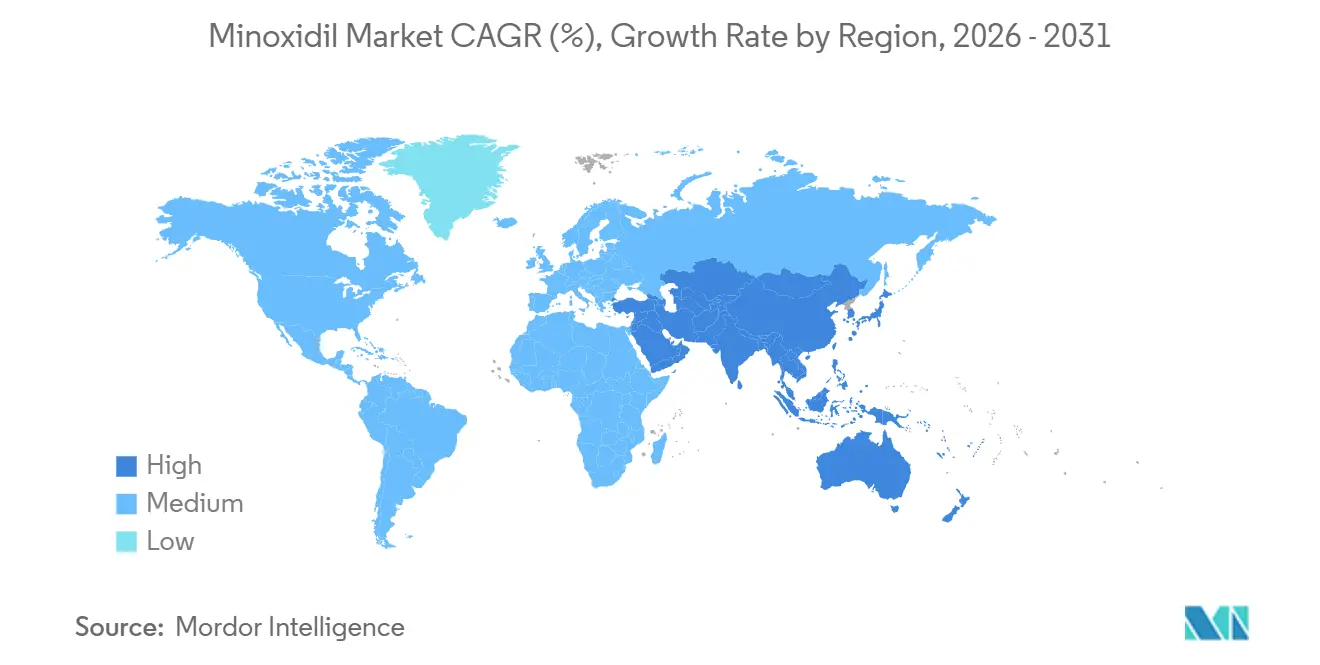

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

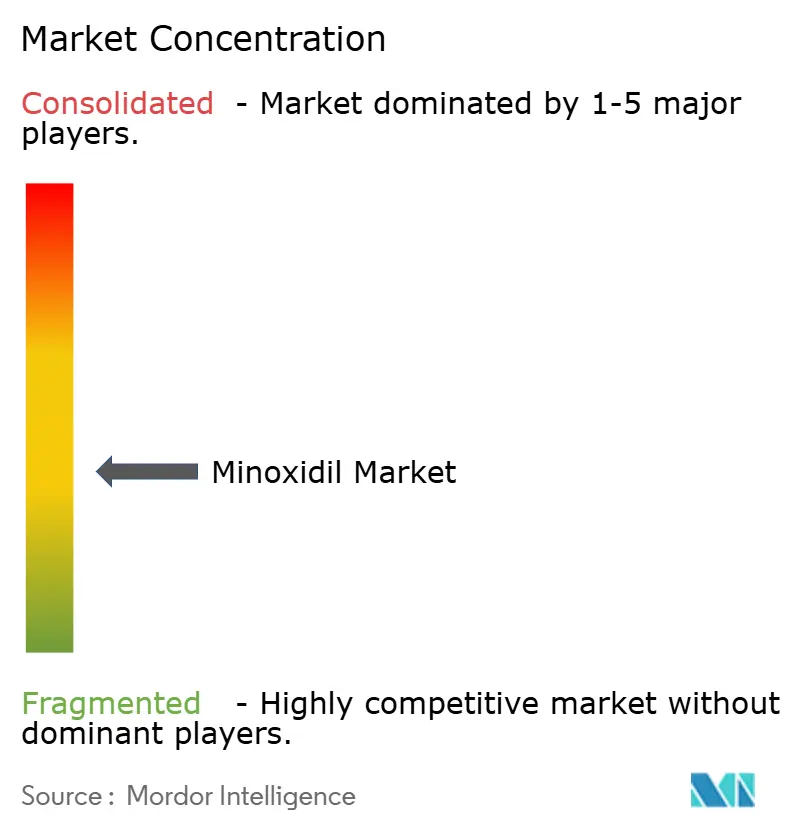

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Minoxidil Market Analysis by Mordor Intelligence

The Minoxidil Market size is expected to increase from USD 2.29 billion in 2025 to USD 2.39 billion in 2026 and reach USD 2.99 billion by 2031, growing at a CAGR of 4.57% over 2026-2031.

Growth is anchored by the dominance of topical formulations and rising acceptance of low-dose oral minoxidil among dermatologists seeking alternatives for patients who do not adhere to twice-daily topical regimens. Direct-to-consumer platforms and e-commerce are expanding access and improving continuity of use through subscription models and integrated telehealth fulfillment. Asia-Pacific is set to grow fastest on the back of large treatment-eligible populations and rising willingness to treat earlier in life. Regulatory oversight of compounded products is shaping product choices toward standardized, pharmacy-grade options in the minoxidil market.

Key Report Takeaways

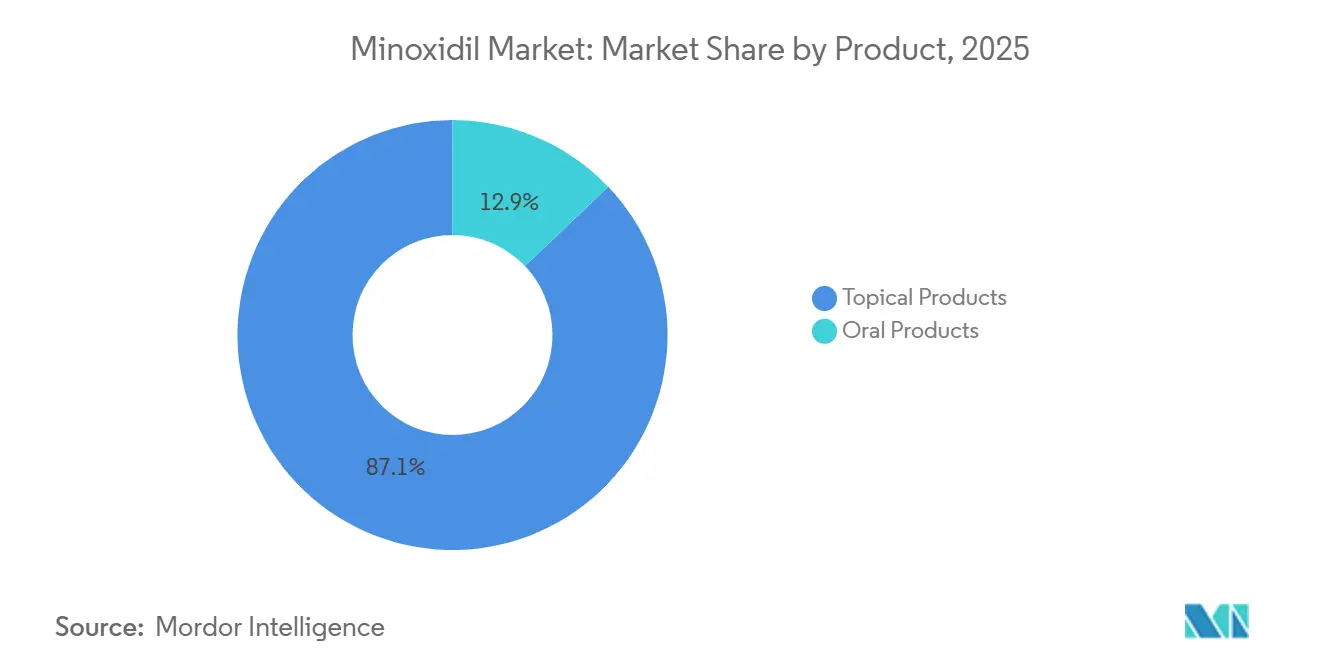

- By product, topical formulations led with 87.10% revenue share in 2025 and are projected to grow at a 4.75% CAGR through 2031.

- By indication, alopecia accounted for 91.20% of 2025 revenue, and the hypertension segment is projected to grow at a 3.16% CAGR to 2031.

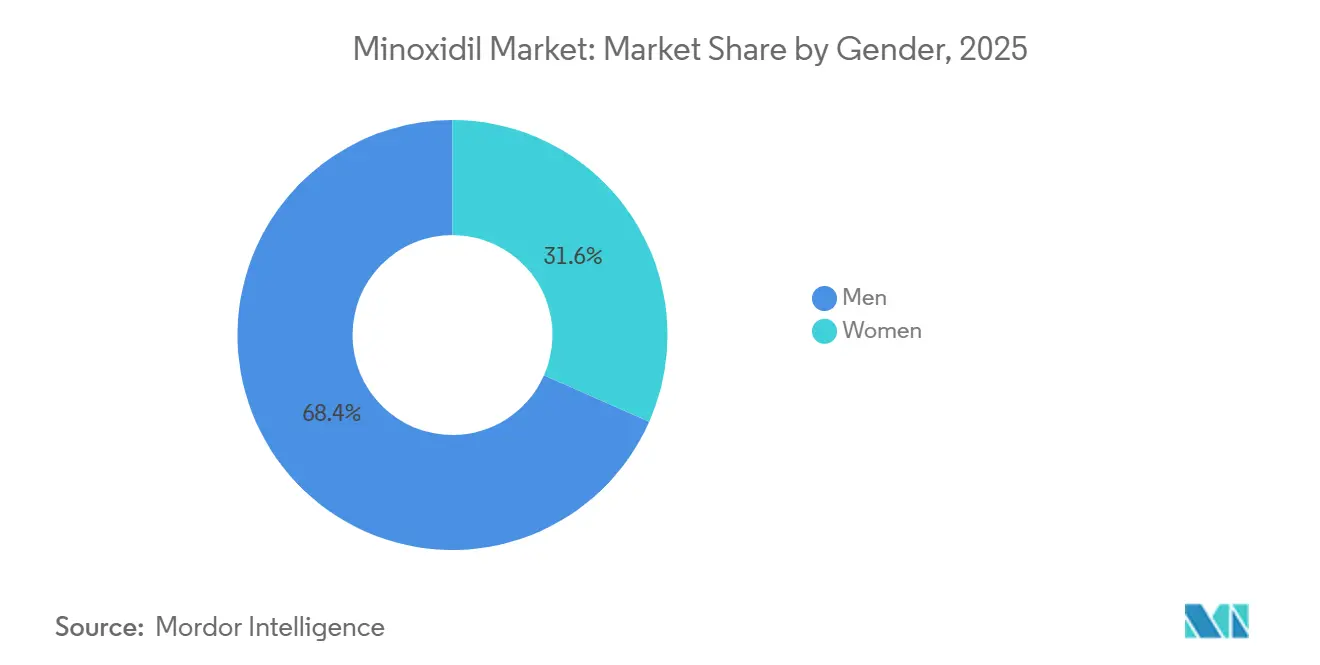

- By gender, men held 68.39% of 2025 revenue, and women are projected to expand at a 4.21% CAGR through 2031.

- By distribution channel, drug store and retail pharmacies captured 52.34% of 2025 revenue, and online providers are expected to grow at a 5.21% CAGR through 2031.

- By geography, North America held 44.56% of 2025 revenue, while Asia-Pacific is projected to be the fastest-growing region with a 5.71% CAGR through 2031 in the minoxidil market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Minoxidil Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| OTC availability of 2% and 5% topical formulations | +1.2% | Global, concentrated in North America, Western Europe, Japan | Medium term (2-4 years) |

| High prevalence of androgenetic alopecia | +1.5% | Global, with APAC core (China, India, Japan, South Korea) showing accelerated growth | Long term (≥ 4 years) |

| Long-term safety familiarity | +0.7% | Global | Long term (≥ 4 years) |

| Expansion of e-commerce and DTC models | +1.1% | North America, APAC urban centers, emerging in Latin America | Short term (≤ 2 years) |

| Rising dermatologist acceptance of LDOM | +0.9% | North America, Europe, Australia, early adoption in India and South Korea | Medium term (2-4 years) |

| Private-label and subscriptions improve affordability | +0.6% | North America, Europe, APAC e-commerce hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

OTC Availability of 2% and 5% Topical Formulations Expands Access in Developed Markets

OTC classification lets consumers purchase minoxidil without a prescription, which sustains the leadership of topical formulations in the minoxidil market. Brand incumbents continue to benefit from broad retail presence, including pharmacy aisles and large-format stores, alongside rising foam and propylene-glycol–reduced presentations designed for better scalp tolerability. In Europe, regulators maintain minoxidil within medicinal frameworks, a posture that keeps products within pharmacy channels and underpins appropriate labeling and risk management. OTC access does not address all adherence barriers, as some users discontinue due to perceived inconvenience or cosmetic concerns. Dose-related hypertrichosis is well documented with oral minoxidil, which shapes physician counseling for patients evaluating non-topical routes of administration. Contact dermatitis linked to propylene glycol in older solutions remains a practical limitation for a subset of users, which has guided interest in foam alternatives in the minoxidil market.

High Prevalence of Androgenetic Alopecia

Androgenetic alopecia is common in adult men and women, and recent regional data highlight a sizable treatment-eligible base in Asia-Pacific. In Japan, a 2024 prevalence survey found that 42.3% of men aged 30–59 experienced AGA, indicating substantial need for pharmacologic treatment and long-term maintenance plans that include minoxidil. The psychosocial burden of hair loss is quantifiable, with meta-analytic evidence from 2025 linking AGA to higher stress, anxiety, and depressive symptoms compared with controls, which supports ongoing engagement with treatment in the minoxidil market. Heightened awareness and earlier intervention in younger cohorts are expanding treatment durations and lifetime exposure to therapies. Interest in new dosage forms and controlled-release options is rising as patients and clinicians seek better adherence and long-term tolerability. A late-stage extended-release oral minoxidil candidate with supportive Phase 2 data has moved toward registrational development, signaling the potential for a standardized oral option to serve patients who do not adhere to topical regimens.

Long-Term Safety Track Record and Decades of Clinical Familiarity

Minoxidil benefits from decades of real-world use, a factor that reassures prescribers and patients and supports sustained utilization in the minoxidil market. Evidence syntheses published in 2025 and 2026 report that low-dose oral regimens produce minimal changes in blood pressure and are generally well tolerated at hair-growth doses, which separates the modern use-case from historical antihypertensive dosing. A prospective 24-week evaluation in male AGA found only small, clinically insignificant reductions in blood pressure at 5 mg daily, which aligns with broader observations from pooled analyses. Safety concerns that have surfaced often trace back to compounding errors or inconsistent quality, rather than to the active ingredient itself at low hair-loss doses.[1]Juan Jimenez-Cauhe et al., “Characterization and Management of Adverse Events of Low-Dose Oral Minoxidil Treatment for Alopecia: A Narrative Review,” Journal of Clinical Medicine, mdpi.com U.S. regulators have reinforced oversight of compounded hair-loss medications, and alerts issued in 2024 and 2025 emphasize the need for compliant manufacturing and proper labeling across telehealth and pharmacy channels. International consensus work in 2025 provided practical guidance on LDOM initiation and monitoring, which has further normalized off-label use in routine dermatology practice.

Rapid Expansion of E-Commerce and Direct-To-Consumer (DTC) Distribution Models

Online channels are capturing a growing share of the minoxidil market through integrated prescribing, fulfillment, and subscription renewals. A leading U.S. DTC platform reported strong growth in 2024 revenue and subscribers, underscoring consumer preference for convenient access, discreet treatment, and bundled regimens that combine minoxidil with complementary agents when clinically appropriate. Teledermatology cohorts have shown high user satisfaction with compounded hair-loss treatments and low rates of self-reported adverse effects, which supports the role of digital platforms in follow-up and long-term adherence. Customized compounded formulations that incorporate minoxidil are associated with improved adherence and clinical outcomes in certain populations compared with standard OTC products, which helps explain the channel’s momentum. Regulatory scrutiny of compounded topical hair-loss medications has increased, and U.S. FDA communications in 2025 may influence which compounded combinations remain available to telehealth platforms or require additional controls. Against this backdrop, standardized pharmacy-grade products and compliant 503B outsourcing can reinforce supply reliability, labeling accuracy, and consistent dosing in the minoxidil market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Dermal irritation, initial shedding, and adherence challenges | -1.3% | Global | Medium term (2-4 years) |

| Alternatives and adjunctive therapies | -0.9% | North America, Europe, APAC urban centers | Long term (≥ 4 years) |

| Regulatory fragmentation across regions and dosage forms | -0.4% | Global with acute impact in Latin America, Middle East/Africa, emerging APAC | Medium term (2-4 years) |

| Heightened regulatory and safety scrutiny | -0.8% | North America, Europe with spill-over to APAC DTC models | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Dermal Irritation, Initial Shedding, and Adherence Challenges

A subset of user's experiences scalp irritation from topical formulations, often linked to excipients such as propylene glycol, which can lead to discontinuation before benefits appear. Patch-test data show positivity to minoxidil and to propylene glycol in some users, and the risk is not evenly distributed across demographic groups, which calls for careful product selection and counseling in the minoxidil market.[2]Alexandra Junge et al., “Contact Dermatitis Caused by Topical Minoxidil: Allergy or Just Irritation,” Acta Dermato-Venereologica, medicaljournalssweden.se Many patients also experience a transient shedding phase early in treatment, which peaks around week 4 in some cohorts and can last longer with specific strengths, yet this shedding correlates with later improvement and should be framed as part of the course rather than a failure of therapy. Adherence can improve when formulations reduce irritation or include adjunctive agents, and compounded topical regimens have been associated with higher continuation and better outcomes than OTC approaches in certain populations. Regulatory alerts in 2025 remind prescribers and patients that some compounded products carry risks when prepared without adequate controls, and that selecting compliant sources is essential. Clear education about the 3–6-month time-to-effect window and expected early shedding helps sustain adherence to baseline therapy in the minoxidil market.

Availability of Alternative and Adjunctive Hair-Loss Therapies

Oral finasteride remains a key option in male pattern hair loss, although European regulators in 2025 strengthened risk communications by confirming suicidal ideation as a safety signal for specific strengths and adding patient card requirements, which influences benefit-risk discussions. Three JAK inhibitors for alopecia areata became available in recent years, and clinical evidence shows meaningful regrowth outcomes at 24 weeks in subsets of patients, which reframes minoxidil as an adjunct in that indication rather than a standalone therapy. Platelet-rich plasma has supportive data for hair density and thickness metrics, and small trials report additive benefits when paired with procedural techniques such as microneedling, which contributes to the popularity of multi-modal plans that incorporate minoxidil. In practice, minoxidil’s vasodilatory mechanism complements androgen blockade and biologic or procedural approaches, making it a platform therapy even when alternatives exist. This adjunctive role preserves long-term relevance for the minoxidil market while also capping monotherapy share in subpopulations that move to higher-cost systemic or procedural routes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Topical Dominance with Oral Formulation Momentum

Topical products commanded 87.10% of 2025 revenue and is expected to grow at a 4.75% CAGR as pharmacy access and brand familiarity continue to support everyday use in the minoxidil market. This persistence reflects OTC availability in mature markets, broad retail distribution, and a steady shift toward foam or propylene-glycol–reduced solutions aimed at users with contact sensitivity. In parallel, customized compounded topicals that pair minoxidil with adjuncts such as retinoids or low-potency corticosteroids have shown stronger adherence and clinical improvement in certain cohorts, which strengthens topical continuity where irritation or plateauing results have been a concern. Regulatory alerts in 2025 have guided prescribers to source compounded products from compliant facilities to balance personalization with quality and labeling assurance. The topical category remains the standard reference point for new users, which sustains visibility and purchasing inertia in pharmacies across the minoxidil market.

Oral products accounted significant share of revenue in 2025, as prescribers weigh convenience benefits against oversight of compounding and dose management. Consensus guidance in 2025 has helped normalize low-dose oral minoxidil initiation and monitoring in clinical practice, which supports steady demand among patients who abandon topical regimens. Safety findings from recent reviews and observational work suggest minimal blood-pressure changes at hair-growth doses, which clarifies the separation between modern hair-loss dosing and the historical antihypertensive context. The path forward for a standardized, extended-release oral option has advanced with a late-stage program enrolling 519 subjects and targeting a potential 505(b)(2) pathway, a development that could reset the oral category’s risk-benefit perception in the minoxidil market. Until then, topical products will continue to define the baseline for access and adoption across regions in the minoxidil industry.

By Indication: Alopecia’s Ascendancy, Hypertension’s Niche

Alopecia accounted for 91.20% of revenue in 2025, underscoring minoxidil’s evolution into a front-line hair-loss therapy in the minoxidil market. Dermatologists favor minoxidil across presentations for pattern hair loss, and real-world adoption continues to broaden as patient education clarifies time-to-effect expectations and the management of initial shedding. Regional epidemiology supports durable demand, with a 2024 Japanese survey reporting a 42.3% prevalence of AGA among men aged 30–59, which adds urgency to early engagement and long-term maintenance in the minoxidil market. In alopecia areata, the role of minoxidil has shifted toward adjunctive use alongside JAK inhibitors where indicated, while data in pattern hair loss continue to support daily topical use or low-dose oral regimens for adherence-sensitive patients. Across these use cases, minoxidil’s tolerability and wide availability remain central to sustained utilization in the minoxidil market.

Hypertension has become a smaller, more specialized use case as first-line antihypertensives meet most needs, and as prescribers confine minoxidil to selected refractory scenarios. The hypertension segment is projected to grow at a 3.16% CAGR to 2031, indicating that this indication will remain a modest contributor relative to alopecia in the minoxidil market size. Recent evidence reviews help clinicians' separate hair-growth dosing from historic cardiovascular dosing, which supports safe use in dermatology while preserving hypertension as a niche setting for the molecule. In both indications, quality assurance in compounding and labeling remains an operational priority where customized products are used.

By Gender: Male Volume Leadership with Growing Female Engagement

Men held 68.39% of revenue in 2025 as the prevalence of androgenetic alopecia and the long track record of topical 5% usage support stable demand in the minoxidil market. Rising use of low-dose oral regimens has created a second-line path for those who do not adhere to topical products, and the 2025 consensus guidance has reinforced practical starting doses and monitoring in routine care. As digital channels scale, once-daily routines, teledermatology follow-up, and refill automation are improving continuity for male patients who prioritize convenience and discretion. Foam formulations that reduce scalp irritation and excipient load are also contributing to steady adherence among men. Together these factors keep men central to near-term revenue in the minoxidil industry.

The women’s segment accounted for significant share, supported by growing clinical comfort with low-dose oral strategies and greater attention to excipient sensitivity, hypertrichosis risk, and dosing flexibility. In clinical practice, adjunctive use with other agents and tailored compounded topicals can improve adherence and outcomes, including among populations where irritation has undermined OTC continuation. Safety reviews highlight that dose selection can manage hypertrichosis risk, which informs shared decision-making in the minoxidil market. The net effect is a patient-centered approach that increases participation by women without compromising tolerability expectations in the minoxidil industry.

By Distribution Channel: Pharmacy Scale Meets Digital Acceleration

Drug store and retail pharmacies captured 52.34% of revenue in 2025, reflecting brand incumbency, OTC access, and established in-aisle placement for topical products in the minoxidil market. Brands with strong consumer recognition and foam-based SKUs benefit from pharmacist counseling and broad shelf coverage, which keeps retail pharmacies vital to acquisition and repeat purchasing. Hospital and clinic pharmacies remain important for prescription-based regimens in systems where dermatology prescribing is concentrated, and for patients who prefer in-person consultation. Regulatory attention to compounding and labeling accuracy is prompting pharmacies and prescribers to rely on compliant outsourcing channels, which supports quality and uniformity. Retail’s large installed base and trusted brands should keep the channel resilient in the minoxidil market.

Online providers are expected to grow at a 5.21% CAGR, the fastest trajectory among channels, driven by telehealth evaluations, convenient fulfillment, and subscription renewals that reduce lapses in therapy. Leading platforms reported strong revenue and subscriber growth in 2024, signaling that integrated care models and personalized regimens are meeting a clear need for convenience and discretion. Digital models can also capture real-world experience at scale, and recent analyses show high reported satisfaction with compounded hair-loss treatments delivered via teledermatology networks. As oversight evolves, platforms are investing in compliant compounding infrastructure and standardized offerings, which can stabilize quality while sustaining differentiation through service and speed in the minoxidil market.

Geography Analysis

North America captured 44.56% of revenue in 2025, reflecting structural maturity, brand familiarity, and early adoption of teledermatology channels in the minoxidil market. Subscription models and click-to-counsel pathways reinforce adherence for consumers who prefer digital care and discreet regimens, as evidenced by expanding revenue and subscriber bases at leading platforms in 2024. Regulatory actions in 2025 underscore U.S. priorities around compounding quality and accurate risk communication for hair-loss products marketed online, which is influencing sourcing and pharmacy partnerships across the region. In this environment, standardized products and pharmacy-grade offerings provide a stable baseline for continuity in the minoxidil market.

Europe is projected to sustain steady growth and operational discipline, with regional dynamics shaped by risk communications for androgen-modulating agents and an emphasis on medicinal classification for minoxidil. Strengthened safety labeling for finasteride in 2025 has sharpened clinician attention to benefit-risk communication, which can redirect some patients toward non-hormonal options or toward adjunctive regimens that include minoxidil. The region’s regulatory stance keeps minoxidil within pharmacy channels and under medicinal oversight, which supports consistent labeling and supervision in the minoxidil market. Country-level differences in retail structure and reimbursement do persist, yet the pharmacy-first framework enables clinicians and pharmacists to guide product selection and proper use across major European markets.

Asia-Pacific is set to be the fastest-growing region with a 5.71% CAGR, supported by large treatment-eligible cohorts, earlier intervention among younger adults, and expanding access points that include retail pharmacies and digital platforms in the minoxidil market. Regional data show substantial prevalence in working-age men in Japan, which supports long-duration therapy decisions and reinforces the need for tolerable, once-daily options to aid adherence.[3]Hamamatsucho First Clinic, “Domestic Survey on AGA (2024: 6,000 Men),” Hamamatsucho First Clinic, hama1-cl.jp Clinical guidance published in recent years has also catalyzed acceptance of low-dose oral approaches in dermatology, which expands the toolkit for patients who do not continue with topical therapies. As channels diversify, quality assurance and consistent dosing remain central to regional growth, especially where compounded products serve niche needs in the minoxidil market.

Competitive Landscape

The global minoxidil market is moderately to highly fragmented, with strong regional brands, large generics suppliers, and digital-first platforms competing on access, formulation, and service. In North America, a long-standing topical brand under a major consumer health company maintains broad shelf presence and continues to represent the reference product for first-time users. Large manufacturers in India and other regions supply topical solutions and foams that extend reach into cost-sensitive markets, while dermatology-focused firms sustain clinician trust in prescription channels. In parallel, digital platforms have emerged as important distribution and care models that bundle prescribing, formulation selection, and delivery under a subscription umbrella, which is reshaping expectations for convenience and continuity in the minoxidil market.

Strategic moves underscore how competition is shifting toward integrated care and product innovation. A leading U.S. platform has invested in compliant compounding capacity and scaled telehealth operations, which enables customizable regimens and rapid fulfillment while maintaining quality controls and audit trails. Consumer health incumbents have emphasized scalp health and preventive care as part of brand strategy, reinforcing education on proper application and regimen continuity for best outcomes in the minoxidil market. On the pipeline front, a late-stage extended-release oral minoxidil program with supportive Phase 2 findings is advancing toward registrational milestones, which could create a premium, standardized oral alternative in coming years.

Regulatory attention to compounding and to accurate risk communication is also a competitive variable, as companies invest in quality systems, validated supply chains, and clear patient information. U.S. FDA alerts in 2024 and 2025 highlight that compounded hair-loss formulations need appropriate controls and labeling, which may favor manufacturers and platforms with compliant infrastructure in the minoxidil market. The net result is a bifurcating competitive field that pairs high-volume OTC topicals with value-added digital services and, potentially, a premium controlled-release oral class if late-stage candidates reach approval.

Minoxidil Industry Leaders

Dr.Reddy’s Laboratories

Kenvue (Kimberly-Clark Corporation)

Laboratoires Bailleul

Perrigo Company plc

Zhejiang Sunshine Mandi Pharmaceutical Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Veradermics, Incorporated, a dermatologist-founded, late-stage biopharmaceutical company, announced the completion of an oversubscribed USD 150 million Series C financing to support registrational development and a planned NDA submission for its lead candidate, VDPHL01. VDPHL01 is a potentially first-in-class extended-release oral minoxidil designed for hair regrowth in women and men. The company also reported preliminary Phase 2 data from the male cohort evaluating VDPHL01 for pattern hair loss.

- June 2025: Hims & Hers Health, Inc. launched the first-ever prescription minoxidil and biotin gummy for hair regrowth in the United States, a chewable once-daily formulation that leverages the company's compounding pharmacy infrastructure (MedisourceRx 503B facility) to deliver a more convenient dosage form than traditional topical or oral presentations.

Global Minoxidil Market Report Scope

Minoxidil is a vasodilator medication originally developed to treat hypertension but now widely used for the treatment of hair loss (androgenetic alopecia). It works by enhancing blood flow to hair follicles and prolonging the anagen (growth) phase of the hair cycle. Topical minoxidil (2% and 5%) is available over-the-counter for male and female pattern hair loss, while oral minoxidil is prescribed primarily for severe hypertension and increasingly used off-label in low doses for hair regrowth. The Minoxidil Market Report is Segmented by Product (Topical Products, and Oral Products), Indication (Alopecia, and Hypertension), Gender (Men, and Women), Distribution Channel (Hospital & Clinic Pharmacies, Drug Store & Retail Pharmacies, and Online Providers), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, and South America). The Market Size and Forecasts are Provided in Terms of Value (USD) for all the above segments.

| Topical Products |

| Oral Products |

| Alopecia |

| Hypertension |

| Men |

| Women |

| Hospital and Clinic Pharmacies |

| Drug Store and Retail Pharmacies |

| Online Providers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Topical Products | |

| Oral Products | ||

| By Indication | Alopecia | |

| Hypertension | ||

| By Gender | Men | |

| Women | ||

| By Distribution Channel | Hospital and Clinic Pharmacies | |

| Drug Store and Retail Pharmacies | ||

| Online Providers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the minoxidil market?

The minoxidil market size was USD 2,389.91 million in 2026 and is forecast to reach USD 2,987.65 million by 2031 at a 4.57% CAGR, driven by topical leadership, rising low-dose oral adoption, and expanding digital channels.

Which product segment leads revenue in the minoxidil market?

Topical formulations led with 87.10% of 2025 revenue and are projected to grow at a 4.75% CAGR, supported by OTC access and broad pharmacy distribution.

Which regions are growing fastest in the minoxidil market?

Asia-Pacific is projected to grow fastest at a 5.71% CAGR through 2031, supported by large treatment-eligible cohorts and earlier intervention trends in working-age adults.

How is e-commerce influencing the minoxidil market?

Online providers are projected to grow at a 5.21% CAGR as telehealth, subscription renewals, and compliant compounding capacity improve convenience and adherence for users.

What safety considerations shape product choices in the minoxidil market?

Reviews in 2025 and 2026 report minimal blood-pressure changes at low-dose oral regimens, while U.S. FDA alerts in 2025 emphasize quality and labeling for compounded topicals, guiding prescribers toward compliant sources.

Which indication holds the largest share in the minoxidil market?

Alopecia accounted for 91.20% of revenue in 2025, reflecting sustained use in pattern hair loss and adjunctive roles in select autoimmune conditions alongside newer systemic therapies.

Page last updated on: