Middle East Mobile Broadband Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

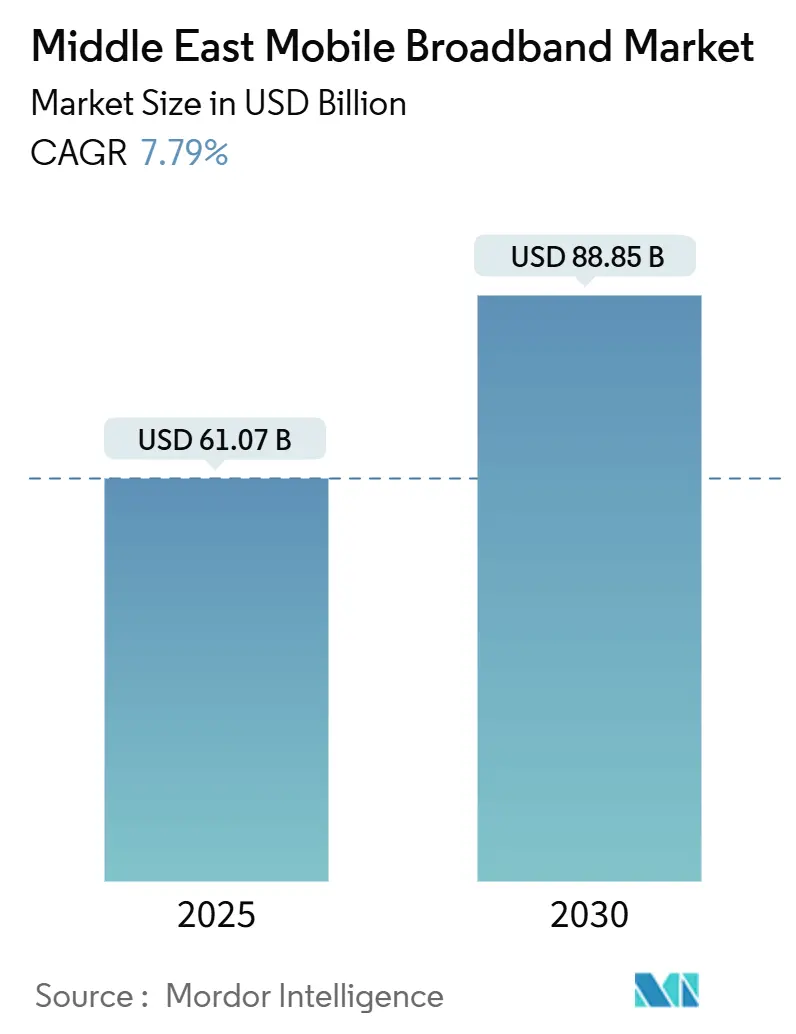

| Market Size (2025) | USD 61.07 Billion |

| Market Size (2030) | USD 88.85 Billion |

| Growth Rate (2025 - 2030) | 7.79% CAGR |

| Fastest Growing Market | Middle East |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East Mobile Broadband Market Analysis by Mordor Intelligence

The Middle East Mobile Broadband Market size is estimated at USD 61.07 billion in 2025, and is expected to reach USD 88.85 billion by 2030, at a CAGR of 7.79% during the forecast period (2025-2030).

Intensifying 5G deployments, mid-band spectrum awards, and sovereign AI initiatives are lifting data-traffic demand and spurring fresh infrastructure investment. GCC operators already cover more than 70% of their populations with 5G, while enterprise pilots in oil and gas, logistics, and smart-city services highlight rising low-latency requirements. Infrastructure-sharing deals, tower carve-outs, and spectrum harmonization lower capital intensity, helping operators redirect cash toward edge computing and artificial-intelligence platforms. Yet usage gaps above 45% in non-GCC markets, together with escalating spectrum prices, weigh on operator margins and threaten equitable connectivity.

Key Report Takeaways

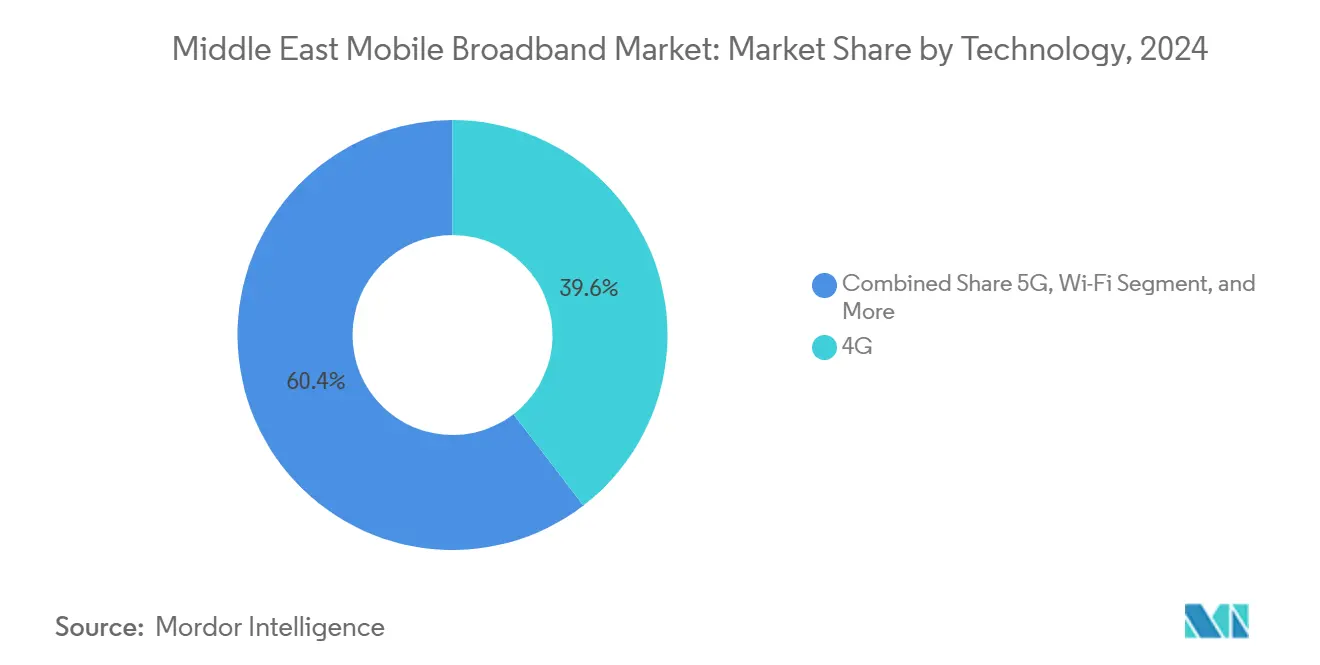

- By technology, 4G held 39.57% of the Middle East mobile broadband market share in 2024, while 5G is advancing at an 11.48% CAGR through 2030.

- By service, mobile data plans commanded 76.24% of revenue in 2024; Voice-over-LTE is forecast to expand at a 15.60% CAGR to 2030.

- By end-user, consumer connections represented 72.43% of 2024 revenue, whereas enterprise subscriptions are accelerating at a 15.14% CAGR.

- By application, entertainment and media captured 36.30% share in 2024; healthcare and education apps are scaling at a 16.27% CAGR to 2030.

- By spectrum band, mid-band (1-6 GHz) accounted for 48.10% of 2024 traffic and is growing at a 12.73% CAGR.

- By geography, Saudi Arabia led with 26.94% of 2024 revenue; Bahrain is poised for an 11.73% CAGR through 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Middle east contributes to a system defined not by any single geography but by the interaction of many. The global mobile broadband market data by Mordor Intelligence represents that combined structure.

Middle East Mobile Broadband Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 5G roll-outs with >70% population coverage | +2.1% | GCC expanding to non-GCC | Medium term (2–4 years) |

| Affordable 3.3-3.8 GHz awards | +1.8% | Saudi Arabia, UAE, Qatar, Kuwait, Bahrain | Short term (≤ 2 years) |

| Mobile data per-user >20% CAGR | +1.5% | Highest in GCC and Turkey | Long term (≥ 4 years) |

| 5G FWA closing fixed gaps | +1.2% | Iraq, Jordan, Syria, Yemen | Medium term (2–4 years) |

| Import bans on 2G/3G-only devices | +0.9% | Qatar, UAE, region-wide rollout | Short term (≤ 2 years) |

| Private 5G + edge pilots | +0.8% | Saudi Arabia, UAE, Kuwait, Oman | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerated 5G roll-outs drive infrastructure modernization

GCC operators extended 5G coverage from roughly 30 to 60 governorates in Saudi Arabia and to 90% of residents in the UAE by 2024. These deployments enable migration from non-stand-alone to stand-alone cores, unlocking network slicing for enterprise services. stc Group secured 140 MHz across multiple bands and committed USD 1.6 billion to build more than 7,000 5G sites, while Zain KSA earmarked USD 427 million for 66% population coverage upgrades. [1]Zain KSA Investor Relations, “2024 Annual Report,” zain.com Eight Middle Eastern countries now operate live 5G networks, and upcoming launches in Libya, Tunisia, and Turkey will further widen the regional footprint. Operators pair massive-MIMO antennas with carrier aggregation to deliver gigabit-class speeds that rival fiber, especially in suburban zones where laying fiber remains cost-prohibitive.

Mid-band spectrum optimization enhances capacity

Saudi Arabia’s 2024 auction of 3.5 GHz blocks is projected to contribute SAR 25 billion in GDP gains by 2030. Mid-band strikes a balance between reach and throughput, supporting the 430% increase in data consumption forecast between 2021 and 2027. The UAE’s regulator (TDRA) proposes opening 6 GHz for license-exempt use, enabling Wi-Fi 6E offload that relieves cellular congestion. [2]TDRA, “UAE Spectrum Outlook 2026-2031,” tdra.gov.aeCarrier aggregation, which stitches together low-, mid-, and high-band frequencies, allows operators to sustain 1 Gbps service in dense downtown corridors without sacrificing rural coverage. ITU-aligned policies, such as Saudi Arabia’s G5 framework, ensure that spectrum is priced to accelerate investment, rather than deter it.

Mobile data-consumption surge transforms revenue models

Average Middle Eastern users consumed 25 GB per month in 2024 and are tracking above a 20% CAGR, fueled by mobile video and social media that account for 36.3% of traffic. Zain Group’s data revenue climbed to USD 2.44 billion, 38% of group turnover, underscoring the pivot from voice to data. Unlimited plans are now table stakes in GCC markets, prompting operators to invest in edge-caching partnerships with AWS and other hyperscalers. These caches lower back-haul costs and trim latency for emerging applications such as cloud gaming. With traffic elasticity rising, operators bundle content, cybersecurity, and managed cloud to guard margins as raw data prices soften.

Fixed Wireless Access bridges connectivity gaps

Zain added 1.1 million 5G FWA customers in non-GCC zones, competing directly with fiber incumbents by leveraging existing towers. Oman counted 75,000 5G FWA lines in 2024, equal to 15% of fixed broadband subscriptions. FWA’s success rests on quick rollouts and lower per-home costs, particularly in rural valleys and coastal areas where trenching fiber is uneconomic. Capacity modeling, however, is critical: high-density FWA can throttle spectrum for mobile users unless operators deploy additional mid-band or millimeter-wave resources. Governments view FWA as a strategic lever to hit digital-inclusion targets ahead of the UN’s Connect 2030 deadline.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Usage gap >45% tied to affordability & skills | -1.4% | Rural & non-GCC | Long term (≥ 4 years) |

| Political instability curbs investment | -0.8% | Iraq, Syria, Yemen | Medium term (2-4 years) |

| Rising spectrum cost-to-revenue ratios | -0.6% | Saudi Arabia, UAE, Qatar | Short term (≤ 2 years) |

| Rural back-haul fiber scarcity | -0.5% | Region-wide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Affordability barriers constrain penetration

Handset prices equal 12-19% of monthly income for many MENA households, far above the 2% affordability benchmark set by international agencies. Smartphone ownership among women in lower-middle-income countries trails men by 18%, and digital-skills deficits further depress demand. Financing programs, device subsidies, and school-based digital-literacy schemes are gaining traction, yet funding remains piecemeal. Without a concerted push, the Middle East risks a dual-tier broadband landscape where rural and low-income populations remain offline despite network availability. [3]ITU, “G5 Benchmark for Evidence-Based Spectrum Policy,” itu.int

Political instability disrupts network investment

Conflict in Iraq, Syria, and Yemen deters foreign capital and jeopardizes existing sites, leading operators to prioritize maintenance over expansion. Currency volatility and sanctions inflate equipment costs, while cybersecurity risks rise amid ungoverned spectrum use. Although these three markets host more than 80 million people, their combined share of regional capex is minimal. Stabilization and transparent licensing regimes are prerequisites to unlock pent-up demand for reliable mobile broadband.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: 5G scales while 4G remains the base

4G generated 39.57% of the Middle East mobile broadband market size in 2024, underpinned by nationwide LTE-Advanced coverage in Saudi Arabia, the UAE, and Qatar. Operators continue upgrading 4G with 256-QAM and massive-MIMO to squeeze spectral efficiency and serve cost-sensitive segments. Meanwhile, 5G subscriptions are growing at an 11.48% CAGR, driven by device subsidies, enterprise pilots, and network-slicing trials. The coexistence of both layers lets carriers assign latency-sensitive apps to 5G while off-loading best-effort traffic onto 4G. Over the forecast horizon, standalone 5G cores should overtake non-stand-alone implementations, enabling fully cloud-native service delivery and ultra-reliable low-latency communication.

The Middle East mobile broadband market continues to blend Wi-Fi 6E, satellite backhaul, and emerging Wi-Fi 7 into a heterogeneous network fabric. Oman Airports’ 2024 Wi-Fi 7 deployment illustrates how non-cellular technologies off-load dense indoor venues while preserving licensed spectrum for macro coverage. Satellite Low Earth Orbit constellations provide redundancy for offshore rigs and desert pipelines, complementing terrestrial 5G. Regulators pressing for 2G/3G sunsets by 2025 accelerate device replacement cycles, further shifting traffic onto 4G and 5G layers.

By Service Type: Data plans dominate, VoLTE re-invents voice

Mobile-data plans delivered 76.24% of 2024 service revenue, reflecting the consumer pivot toward video streaming, mobile gaming, and social media. Operators compete on generous data caps, bundled content, and zero-rating offers, with unlimited tiers now common in GCC bundles. At the same time, Voice-over-LTE subscriptions are growing at a 15.60% CAGR as carriers retire legacy circuit-switched networks. VoLTE improves spectrum utilization by as much as 40%, freeing 900 MHz bands for NB-IoT and LTE-M services. 5G New Calling trials across Kuwait and Bahrain take voice a step further with high-fidelity codecs and real-time translation add-ons.

Specialized fixed-wireless data plans linked to RedCap chipsets herald a new class of mid-speed, low-cost IoT FWA tariffs. stc Kuwait’s early 2024 launch targets industrial clients that require deterministic performance but not the full bandwidth of enhanced mobile broadband. Cloud-managed SIMs, eSIM onboarding, and private APN packages expand the service mix, creating fresh upsell paths for operators eager to diversify beyond consumer data.

By End-User: Consumers lead, enterprises accelerate

Consumers accounted for 72.43% of the Middle East mobile broadband market size in 2024, fueled by entertainment, social networking, and remote work. Yet enterprise connections are rising at a brisk 15.14% CAGR as factories, refineries, and logistics hubs integrate private 5G and edge platforms. National oil companies in Saudi Arabia and the UAE pilot network slices that guarantee 1 ms latency for autonomous drilling and predictive maintenance.

Managed-service revenue is outpacing pure connectivity as operators bundle cybersecurity, cloud storage, and analytics. e& booked USD 720 million in enterprise sales during 2024, up 32% year-on-year, while Mobily posted USD 963.1 million, up 21%. Government agencies leveraging 5G for smart-city surveillance, intelligent transportation, and digital-identity programs amplify enterprise demand, cementing B2B as the next growth engine.

By Application: Media still on top, healthcare and education surge

Entertainment and media captured 36.30% of 2024 traffic, driven by 4K streaming, real-time esports, and influencer-driven short-video formats. Average session times lengthened by 17% as unlimited plans removed usage anxiety. Meanwhile, healthcare and education applications are growing at a 16.27% CAGR, underpinned by telehealth mandates, electronic health-record integrations, and virtual classrooms.

Connected ambulances in Abu Dhabi stream ultrasound scans to hospital specialists over 5G uplinks, cutting diagnostics time by 28%. Education ministries distribute cloud-native learning content over carrier networks to rural schools, using FWA where fiber remains scarce. E-commerce, fintech, and social-commerce apps round out the application mix, keeping uplink traffic growth closely aligned with downstream video surge.

By Spectrum Band: Mid-band is the workhorse

Mid-band (1-6 GHz) contributed 48.10% of 2024 traffic and is projected to climb at a 12.73% CAGR, cementing its role as the capacity layer for urban and suburban 5G. Saudi Arabia’s 600 MHz deployment provides a coverage layer that slashes site count in rural areas by 30% and lifts average cell-edge throughput. At the other extreme, operators test mmWave for stadiums and high-density downtown nodes, clocking 8 Gbps peak throughput in prototype trials.

Dynamic spectrum-sharing technologies let carriers overlay 4G and 5G on the same blocks, accelerating 5G adoption without accelerating spectrum spend. Regulators that align auction calendars across GCC states lower cross-border interference and unlock economies of scale in radio hardware.

Geography Analysis

Saudi Arabia captured 26.94% revenue in 2024, anchored by USD 1.6 billion in 5G capex and nationwide Vision 2030 digital-economy targets. stc, Zain, and Mobily lease or own the region’s densest mid-band footprint, enabling multi-gigabit speeds in 122 cities. The UAE remains an innovation bellwether with 90% 5G population coverage, low-band 700 MHz for desert reach, and joint ventures with AWS and Microsoft to host sovereign clouds. Qatar’s regulator ordered a 3G shutdown for December 2025, nudging subscribers to 4G and 5G and accelerating handset refresh cycles.

Bahrain’s nationwide 5G blanket and agile licensing pushed the kingdom to an 11.73% CAGR trajectory, positioning it as the fastest-growing Middle East mobile broadband market. Kuwait and Oman sustain moderate expansion; both prioritize spectrum refarming and solar-powered sites to meet carbon-neutral pledges. Israel blends open-RAN pilots with dynamic-spectrum-sharing to accommodate a crowded vendor ecosystem, whereas Turkey depends on domestic production policies to spur supply-chain localization.

Iraq, Syria, and Yemen remain constrained by security risks, yet Iraq’s tax-removal policy spurred double-digit revenue growth for surviving operators. Jordan maintains stable, if subdued, momentum thanks to prudent spectrum pricing and regional fiber links to Europe. Iran’s operators, hampered by sanctions, focus on incremental 4G densification while eyeing future 5G once equipment channels normalize.

The mobile broadband market is analyzed by Mordor Intelligence across multiple other geographies, with in-depth regional assessments available for South America, Africa, and Europe.

Competitive Landscape

Four operator groups—stc, e&, Zain, and Ooredoo—control most regional revenue, but infrastructure monetization is lowering barriers for MVNOs and hyperscale newcomers. PIF and stc merged TAWAL and LATIS into a 30,000-tower giant that will book SAR 4.8 billion in annual sales, releasing capital for edge nodes and AI-driven automation. e& pursued a carve-out of its regional data-center assets into a neutral-host model, courting cloud providers that crave low-latency colocation.

Competition pivots away from basic connectivity toward “Beyond Connectivity” portfolios: stc Advanced Solutions, Mobily Business Cloud, and Ooredoo’s cybersecurity arm each chase double-digit B2B growth. Operators leverage public-cloud partnerships to shorten service-launch cycles, offering network APIs for quality-on-demand slices that embed directly into enterprise apps.

Private-network opportunity remains fertile; ports in Jeddah, industrial estates in Abu Dhabi, and smart logistics corridors in Kuwait pilot dedicated 5G with deterministic latency. Supplier diversity is widening, with open-RAN hardware trials in Dubai Metro and Turkey’s Turkcell forging R&D partnerships with local tech firms. Energy efficiency is a differentiator; solar-powered base stations and AI-adaptive cooling trim opex by up to 40% in peak summer months.

Middle East Mobile Broadband Industry Leaders

STC Group

Zain Group

Ooredoo

Turkcell

Omantel

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: SAMENA Council spotlighted 5G FWA in South Asia–Middle East–North Africa at its annual forum.

- October 2024: STC Group and Ooredoo signed an MoU to co-develop regional digital-service platforms.

- June 2024: du UAE partnered with Huawei on 5G-Advanced and FWA/FTTH convergence strategies.

- May 2024: Zain KSA announced a USD 427 million 5G expansion to cover 122 cities and holy sites.

Middle East Mobile Broadband Market Report Scope

| 4G |

| 5G |

| LTE |

| Wi-Fi |

| Other Technology |

| Mobile Data |

| Voice over LTE (VoLTE) |

| Mobile Hotspot |

| Consumers |

| Businesses/Enterprises |

| Entertainment and Media (Streaming, Gaming) |

| E-commerce and Retail |

| Social Media and Communication |

| Healthcare and Education |

| Other Applications |

| Sub-1 GHz (Coverage bands) |

| 1 - 6 GHz (Mid-band) |

| >6 GHz mmWave and Terahertz |

| Saudi Arabia |

| United Arab Emirates |

| Israel |

| Turkey |

| Qatar |

| Kuwait |

| Oman |

| Bahrain |

| Rest of Middle East (Syria, Yemen, Jordan, Iraq, Iran, and others) |

| By Technology | 4G |

| 5G | |

| LTE | |

| Wi-Fi | |

| Other Technology | |

| By Service Type | Mobile Data |

| Voice over LTE (VoLTE) | |

| Mobile Hotspot | |

| By End-User | Consumers |

| Businesses/Enterprises | |

| By Application | Entertainment and Media (Streaming, Gaming) |

| E-commerce and Retail | |

| Social Media and Communication | |

| Healthcare and Education | |

| Other Applications | |

| By Spectrum Band | Sub-1 GHz (Coverage bands) |

| 1 - 6 GHz (Mid-band) | |

| >6 GHz mmWave and Terahertz | |

| By Country | Saudi Arabia |

| United Arab Emirates | |

| Israel | |

| Turkey | |

| Qatar | |

| Kuwait | |

| Oman | |

| Bahrain | |

| Rest of Middle East (Syria, Yemen, Jordan, Iraq, Iran, and others) |

Key Questions Answered in the Report

How fast is 5G adoption progressing in the Gulf states?

Subscriptions are expanding at an 11.48% CAGR as Saudi Arabia, the UAE, and Bahrain already cover at least 70% of their populations with 5G service.

What share of revenue comes from mobile data plans?

Mobile data plans generated 76.24% of sector revenue in 2024, underscoring the pivot from voice to data services.

Which country shows the strongest growth outlook through 2030?

Bahrain leads with an expected 11.73% CAGR, driven by nationwide 5G coverage and supportive regulation.

Why are mid-band frequencies essential for network performance?

The 1-6 GHz layer balances reach and capacity, delivering 48.10% of 2024 traffic while supporting carrier-aggregation speeds above 1 Gbps.

What challenges keep usage rates low outside the Gulf?

Handset affordability and digital-skills gaps leave a 45% usage gap in many non-GCC areas despite network availability.

How are operators improving returns on their tower assets?

Infrastructure-sharing deals such as stc’s tower merger create a 30,000-site neutral host that frees cash for 5G and edge-cloud upgrades.

Page last updated on: