Middle East Milk Powder Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

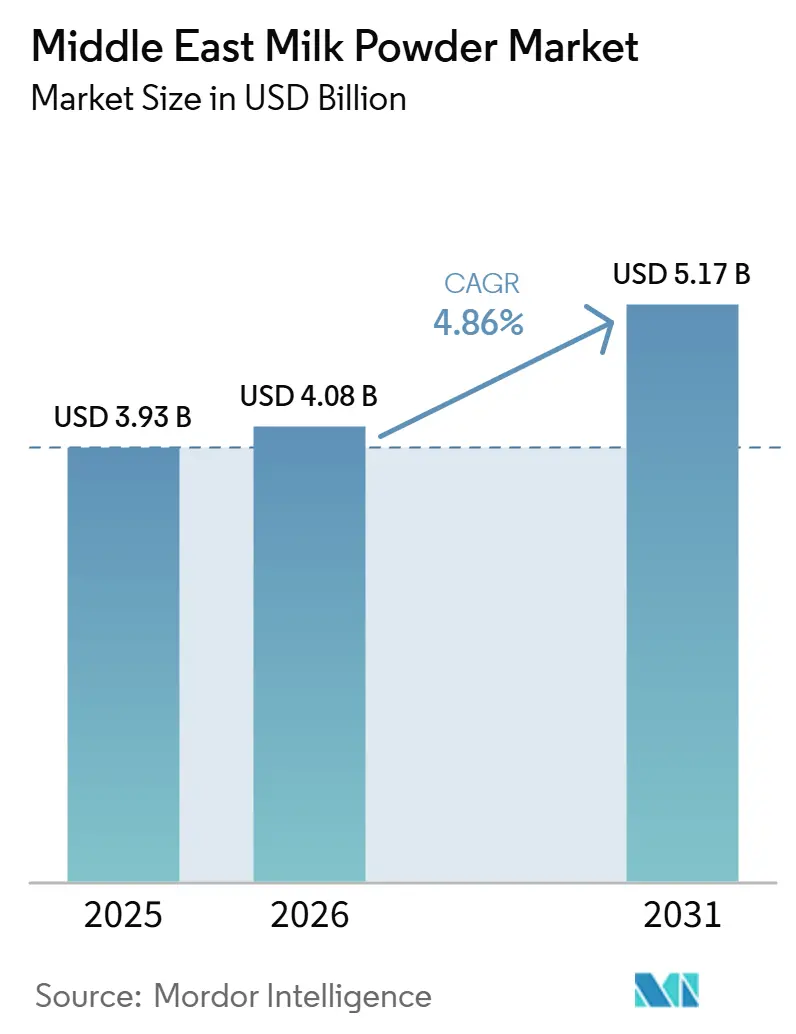

| Base Year Market Size (2025) | USD 3.93 Billion |

| Market Size (2026) | USD 4.08 Billion |

| Market Size (2031) | USD 5.17 Billion |

| Growth Rate (2026 - 2031) | 4.86% CAGR |

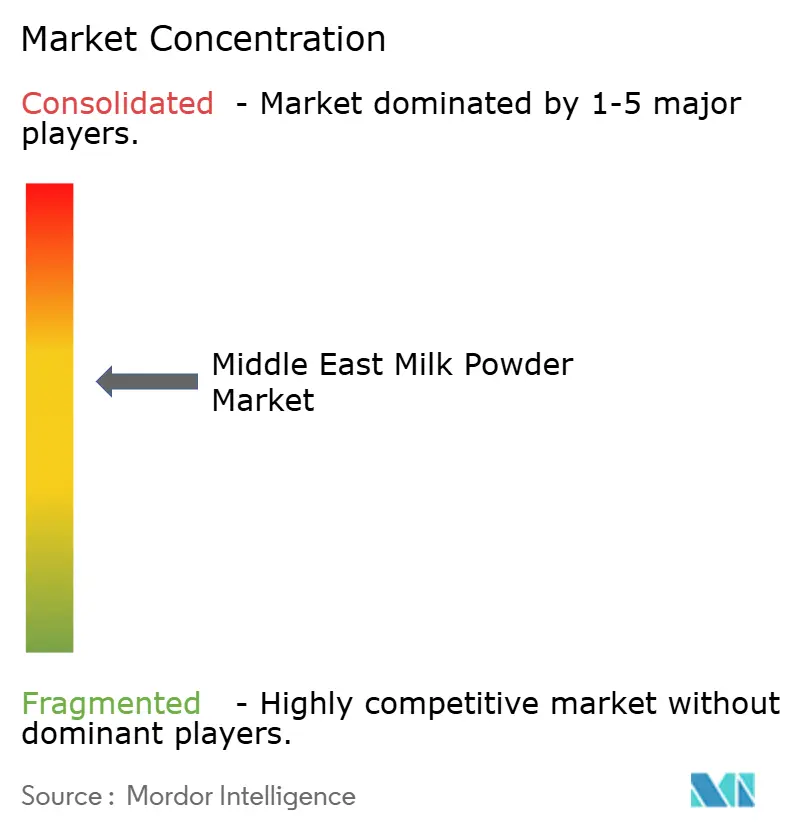

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East Milk Powder Market Analysis by Mordor Intelligence

The Middle East milk powder market size is projected to grow from USD 3.93 billion in 2025 to USD 4.08 billion in 2026 and reach USD 5.17 billion by 2031, registering a CAGR of 4.86% during 2026-2031. Strong demand for shelf-stable dairy products supports the Middle East milk powder market, as water stress and arid farming conditions limit cost-efficient local milk production. Infant nutrition, food processing, and foodservice applications also drive demand, as powdered formats offer storage flexibility and consistent formulation. High lactose intolerance in key markets supports processed dairy applications and expands opportunities for plant-based powder alternatives. Modern grocery channels and digital retail improve access to imported and premium stock-keeping units in major urban centers. Competition remains balanced between global dairy exporters and regional producers with strong distribution reach.

Key Report Takeaways

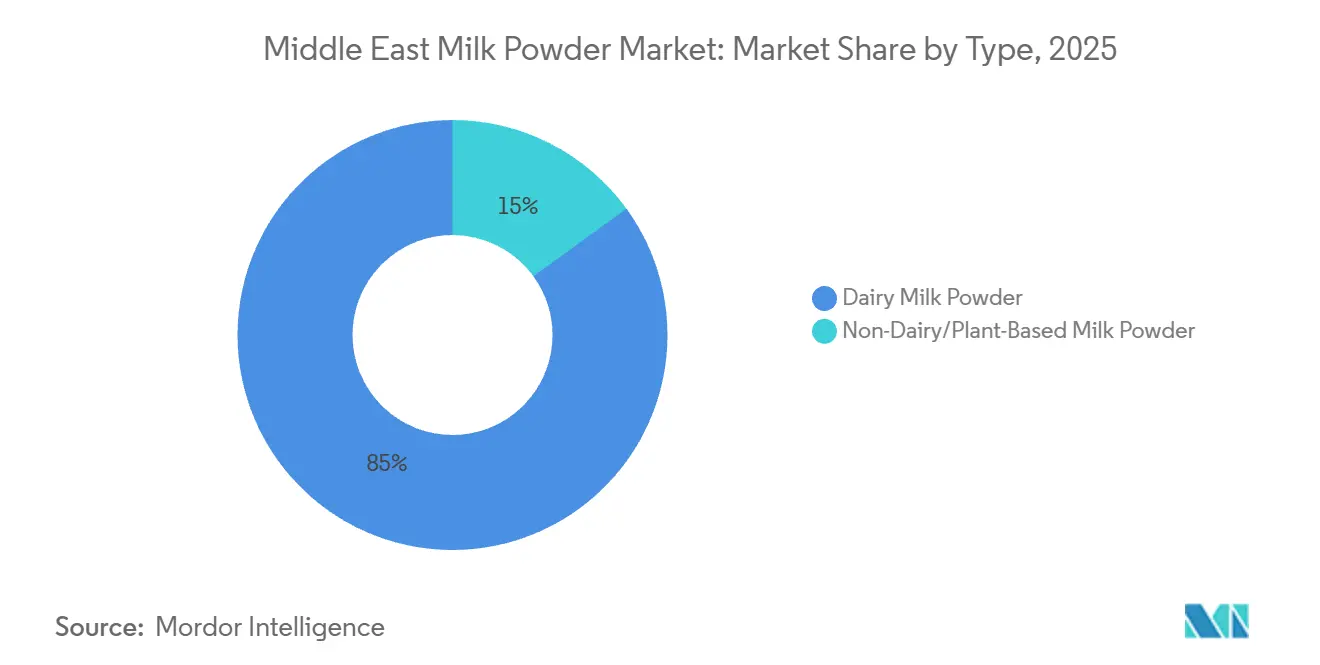

- By type, dairy milk powder held 85% of the Middle East milk powder market share in 2025, while non-dairy and plant-based milk powder is projected to grow at a 5.76% CAGR through 2031.

- By distribution channel, retail accounted for 45.34% share of the Middle East milk powder market size in 2025, while foodservice is forecast to expand at a 6.72% CAGR through 2031.

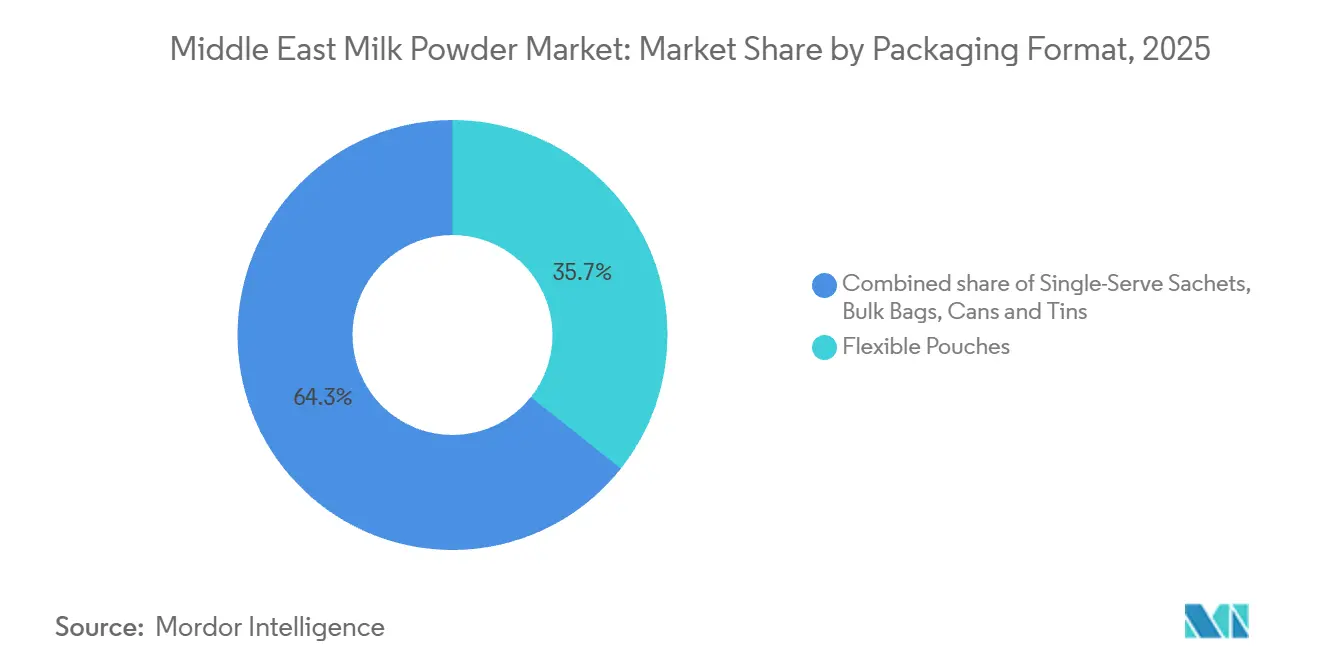

- By packaging format, flexible pouches captured 35.67% share of the Middle East milk powder market size in 2025, while single-serve sachets are expected to advance at a 5.98% CAGR through 2031.

- By geography, Saudi Arabia held 28.45% of the Middle East milk powder market share in 2025, while Bahrain is projected to record the highest CAGR at 6.25% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Middle East Milk Powder Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand From Infant Nutrition | +1.4% | Saudi Arabia, UAE, Qatar | Medium term (2-4 years) |

| Growth In Health-Conscious Consumption | +0.8% | UAE, Saudi Arabia, Kuwait | Long term (≥ 4 years) |

| Expansion Of Convenience Food Usage | +0.7% | GCC core, spill-over to Yemen, Oman | Medium term (2-4 years) |

| Strong Food And Feed Industry Demand | +0.6% | Saudi Arabia, UAE | Medium term (2-4 years) |

| Long Shelf Life Advantage | +0.5% | Global, heightened in GCC and Yemen | Short term (≤ 2 years) |

| Growing E-Commerce And Modern Retail Availability | +0.4% | UAE, Saudi Arabia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Demand From Infant Nutrition

Infant nutrition remains one of the most reliable sources of demand for the Middle East milk powder market. The category benefits from steady household spending in Saudi Arabia, the United Arab Emirates, and Qatar, where consumers are willing to pay more for trusted formulations and certified products. It also favors suppliers that can meet stricter requirements for labeling, composition, and halal compliance. This gives large exporters and established regional distributors an advantage, as they already have the documentation and quality systems required by the trade. Fonterra is expected to strengthen this position in 2026 through a three-year supply agreement with a major Saudi distributor and by doubling its infant formula export volume to the Kingdom. This move shows that infant nutrition not only supports current volumes in the Middle East milk powder market but also influences long-term supplier commitments.

Growth In Health-Conscious Consumption

Health-led consumption is expanding the product mix in the Middle East milk powder market rather than replacing traditional dairy demand. High lactose intolerance in the region is increasing demand for easier-to-digest formulations and plant-based powder alternatives. Conventional milk powder remains important because consumers use it widely in cooked, blended, and processed products, where tolerance can differ from fresh milk. As a result, dairy powder and plant-based powder are growing side by side rather than following a direct substitution trend. Public policy also supports this shift, with the UAE’s food security agenda and Saudi Arabia’s support for local ingredient development giving plant-based formats more institutional visibility. The Middle East milk powder market is therefore expanding across formats, applications, and buyer profiles.

Long Shelf Life Advantage

Shelf stability remains a key factor supporting the strategic importance of the Middle East milk powder market across households, trade channels, and institutional procurement. Extreme temperatures, uneven cold chain coverage, and long inland transport routes make ambient dairy formats easier to store and transport than fresh alternatives. This advantage is most important outside major GCC cities, where refrigeration access is less reliable and inventory losses can rise quickly. Yemen clearly reflects this trend, as powdered milk remains a practical format for meeting a large share of dairy nutrition demand when cold storage is limited. SADAFCO’s management linked the demand for long-life dairy products to ease of use and lower waste, supporting the same operating logic for powdered formats. This storage advantage also helps the Middle East milk powder market fit more effectively into online grocery and cross-border retail fulfillment.

Growing E-Commerce And Modern Retail Availability

The expansion of modern trade and digital grocery is improving access to the Middle East milk powder market for both local and imported brands. Supermarkets, hypermarkets, and online platforms are increasing product visibility and reducing dependence on physical shelf placement. This trend is important for milk powder because the category is well-suited for home delivery and does not require the same cold chain infrastructure as fresh dairy. According to the USDA Foreign Agricultural Service, in the UAE, food e-commerce revenues grew at a positive rate in 2025, indicating strong momentum in digital grocery demand[1]Source: USDA Foreign Agricultural Service, “Retail Foods Annual, UAE”, apps.fas.usda.gov. As more grocery purchases move online, imported milk powder brands can achieve nationwide reach without building the same physical footprint required by earlier entrants. This shift is improving category discoverability and expanding the retail base of the Middle East milk powder market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Climate Constraints On Dairy Farming | -1.0% | Saudi Arabia, UAE, Oman, Kuwait | Long term (≥ 4 years) |

| Quality And Safety Compliance Requirements | -0.6% | GCC, regulatory influence from Saudi SFDA and UAE MOHAP | Medium term (2-4 years) |

| Supply Chain Disruption Risk | -0.5% | Global, concentrated in UAE, KSA, Yemen | Short term (≤ 2 years) |

| Competition From Fresh And Other Dairy Formats | -0.4% | Saudi Arabia, UAE | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Climate Constraints On Dairy Farming

Climate pressure remains the key structural restraint on the Middle East milk powder market, as it limits the expansion of local raw milk production. Water stress is severe across the broader region, and agriculture already uses more than half of total water withdrawals in many MENA countries. This raises dairy farming costs and makes local supply more exposed to water policies, forage constraints, and feed dependence. The issue is long term because it affects the core economics of dairy farming in desert conditions. It also drives companies and governments to seek large-scale production capacity and powder supply outside core GCC markets. As a result, the Middle East milk powder market will continue to depend heavily on imported or externally produced dairy inputs, even as domestic champions expand.

Quality And Safety Compliance Requirements

Compliance standards are increasing operating requirements in the Middle East milk powder market, especially for infant, nutritional, and specialty products. Import screening, labeling rules, shelf-life management, and product testing add cost and time before products reach retail shelves or industrial users. Halal certification also works alongside standard food safety systems, so exporters must maintain process control and product conformity. Larger suppliers can manage these requirements more easily because they already have regulatory teams and multi-market registrations. Smaller distributors and new entrants face a heavier burden, which can slow assortment expansion and product launches. This issue is especially important for new plant-based formulations, where documentation and approval requirements can delay market entry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Dairy Powder Keeps Scale While Plant-Based Powder Adds New Demand

Dairy milk powder is expected to hold an 85% share in 2025, remaining the primary volume driver of the Middle East milk powder market. Its scale reflects the category’s extensive use across bakeries, confectionery, infant formula blending, dairy beverages, and routine household consumption. Whole milk powder remains important in applications where fat content enhances the taste and texture of finished products. Skim milk powder also plays a strong role in blending and industrial applications, where processors require functional dairy solids without added fat. This large installed base keeps dairy powder at the center of the Middle East milk powder industry and limits the pace of rapid substitution.

Non-dairy and plant-based milk powder is the fastest-growing type and is projected to expand at a CAGR of 5.76% through 2031. Growth is driven by lactose intolerance, institutional support for plant-based options, and rising consumer acceptance of soy, almond, and oat formats. However, the segment remains much smaller than dairy powder, so its growth starts from a narrower commercial base. Price remains the key constraint, as plant-based powder often sells at a clear premium to conventional dairy products. Even so, the Middle East milk powder market is gradually expanding its category boundaries as regional buyers adopt plant-based products for wellness, sustainability, and menu diversification.

By Distribution Channel: Retail Holds Scale While Foodservice Expands Faster

Retail is expected to account for a 45.34% share of the Middle East milk powder market size in 2025, remaining the primary purchase channel for consumer packs. Large supermarket and hypermarket networks across the GCC provide milk powder brands with reliable shelf access and support frequent purchase cycles. Retail also enables branded differentiation, as packaging, certifications, and origin labels can influence buyer trust at the point of sale. Online grocery is further strengthening this channel by expanding product availability beyond major physical store networks. This is particularly useful for imported and premium products seeking broad reach without making similar investments in direct physical distribution.

Foodservice is the fastest-growing distribution channel and is expected to register a CAGR of 6.72% through 2031. Hotels, cafés, bakeries, quick-service restaurants, and institutional caterers are using milk powder to improve consistency, reduce spoilage, and manage costs in high-volume operations. Instant and agglomerated formats are gaining traction where beverage performance and quick reconstitution are important. The expansion of ghost kitchens and cloud restaurant models is also supporting smaller-format and digitally sourced procurement. These trends position foodservice as one of the clearest growth drivers for the Middle East milk powder market as hospitality and out-of-home consumption continue to expand across key Gulf cities.

By Packaging Format: Flexible Pouches Lead While Sachets Grow on Convenience

Flexible pouches are expected to account for 35.67% of the Middle East milk powder market size in 2025, maintaining their position as the leading packaging format. Their dominance stems from lower transport weight, strong barrier performance, and broad use in retail and business-to-business shipments. These features are important in a market with long shipping routes, high ambient temperatures, and extensive cross-border movement. Flexible formats also suit automated filling lines and help suppliers manage costs across multiple pack sizes. This combination keeps pouches central to the Middle East milk powder market, even as other packaging types serve niche roles.

Single-serve sachets are projected to register a 5.98% CAGR through 2031, making them the fastest-growing packaging format. Their appeal comes from convenience, portion control, and lower trial risk for new buyers. They also support e-commerce fulfillment because they are easy to ship and fit foodservice beverage preparation needs. For premium or specialized products, sachets let brands test new propositions without requiring consumers to commit to large packs. This trend shows how the Middle East milk powder market is adapting packaging to evolving retail behavior, channel economics, and product positioning.

Geography Analysis

Saudi Arabia is projected to hold a 28.5% share in 2025, maintaining its position as the largest country market within the Middle East milk powder market. This leadership reflects the Kingdom’s scale, large consumer base, and strong domestic dairy infrastructure. Almarai’s revenue is expected to reach USD 1.56 billion in Q2 2026, increasing 11% year-on-year, showing the continued commercial strength of dairy-led food businesses in the country. Saudi Arabia also benefits from well-developed retail and foodservice channels that support both branded milk powder and industrial inputs. However, climate and water constraints keep the country linked to broader regional and international sourcing patterns.

The UAE remains central to the Middle East milk powder market, as it functions as a trade, logistics, and re-export hub for the wider region. Its commercial role extends beyond domestic demand, with UAE-based distribution networks connecting Gulf consumption centers to international suppliers. The expansion of food e-commerce is also positioning the UAE as a launch market for premium, imported, and digitally discoverable milk powder brands. Kuwait and Qatar strengthen the northern Gulf demand cluster, where premiumization and food security concerns continue to support the strategic importance of dairy formats. Qatar’s dairy strategy has also shown that regional producers are willing to invest beyond their home markets when local production constraints limit long-term expansion.

Bahrain is projected to record the fastest growth, registering a 6.3% CAGR through 2031, indicating a smaller but rapidly developing demand base within the Middle East milk powder market. Premium retail expansion, higher foodservice density, and a sizable expatriate consumer base support this growth. Yemen presents a different market dynamic, as powdered milk serves more as a food security staple than as a discretionary packaged dairy product. Across the region, the balance between local production ambitions and imported supply will continue to shape the development of the Middle East milk powder market by country.

Competitive Landscape

The Middle East milk powder market is moderately consolidated, with global exporters and regional dairy leaders operating side by side. Nestlé, Fonterra, FrieslandCampina, Arla Foods, Lactalis, and Danone remain key players due to their scale, formulation capabilities, and broad portfolios. Regional players, such as Almarai, SADAFCO, and Baladna, also hold strong positions through local channel knowledge and access to GCC retail and foodservice networks. This creates a two-layer market, where international companies often lead in supply depth and specialized nutrition, while regional companies compete through distribution reach and domestic brand familiarity. Scale matters, but local execution continues to shape outcomes.

Product differentiation is gaining importance in the Middle East milk powder market as buyers look beyond standard volume supply. Global brands are more active in fortified formulas, staged child nutrition, and performance-led dairy ingredients. Regional producers have typically focused on pack size, availability, and pricing, although this gap is narrowing. SADAFCO signaled a broader innovation push by reporting 32 new stock-keeping unit launches in FY 2025 across its portfolio. Innovation pace will help determine which brands capture premium demand as the Middle East milk powder market becomes more segmented.

Strategic moves expected in 2026 show the direction of competition. Fonterra plans to expand its Saudi infant nutrition presence through a three-year supply agreement with a major local distributor, strengthening its position in a high-value channel. Almarai continues to show the value of vertically integrated scale, with growth supported by its dairy operations and broader category reach. SADAFCO also announced a SAR 100 million investment, equivalent to USD 26.7 million, to increase milk factory capacity by 20% and expand export coverage, highlighting its regional supply ambitions.

Middle East Milk Powder Industry Leaders

Nestlé S.A

Lactalis Group

Fonterra Co-operative Group Limited

FrieslandCampina

Almarai Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Baladna signed a memorandum of understanding with UAE-based Al Dahra Holding for a strategic partnership on global farming collaborations and long-term animal feed supply, directly supporting Baladna’s expanding dairy footprint in Algeria and Syria.

- April 2026: Baladna Algeria signed second-phase agreements worth more than USD 635 million as part of its USD 3.5 billion integrated dairy and milk powder project in Algeria’s Adrar province, including an airlift program for 30,000 high-quality US dairy cows starting in November 2026.

- March 2026: Fonterra Co-operative Group signed a three-year supply agreement with a major Saudi distributor, doubling its infant formula export volume to the Kingdom and reinforcing New Zealand’s position as a premium dairy-origin source for Saudi Arabia.

Middle East Milk Powder Market Report Scope

| Dairy Milk Powder | Whole Milk Powder (WMP) |

| Skim Milk Powder (SMP) | |

| Others | |

| Non-Dairy/Plant-Based Milk Powder | Soy Milk Powder |

| Almond Milk Powder | |

| Coconut Milk Powder | |

| Oat and Other Cereal-Based Powders |

| Retail | Supermarkets/Hypermarkets |

| Convenience and Grocery Stores | |

| Online Retail | |

| Other Distribution Channel | |

| Foodservice | |

| Industrial | Infant and Follow-on Formula |

| Bakery and Confectionery | |

| Dairy-based Beverages and Recombination | |

| Nutritional and Sports Supplements | |

| Others (Ready-Made Meals, cosmetics, etc.) |

| Flexible Pouches |

| Cans and Tins |

| Bulk Bags |

| Single-Serve Sachets |

| Bahrain |

| Kuwait |

| Oman |

| Qatar |

| Saudi Arabia |

| United Arab Emirates |

| Yemen |

| Rest of the Middle East |

| By Type | Dairy Milk Powder | Whole Milk Powder (WMP) |

| Skim Milk Powder (SMP) | ||

| Others | ||

| Non-Dairy/Plant-Based Milk Powder | Soy Milk Powder | |

| Almond Milk Powder | ||

| Coconut Milk Powder | ||

| Oat and Other Cereal-Based Powders | ||

| By Distribution Channel | Retail | Supermarkets/Hypermarkets |

| Convenience and Grocery Stores | ||

| Online Retail | ||

| Other Distribution Channel | ||

| Foodservice | ||

| Industrial | Infant and Follow-on Formula | |

| Bakery and Confectionery | ||

| Dairy-based Beverages and Recombination | ||

| Nutritional and Sports Supplements | ||

| Others (Ready-Made Meals, cosmetics, etc.) | ||

| By Packaging Format | Flexible Pouches | |

| Cans and Tins | ||

| Bulk Bags | ||

| Single-Serve Sachets | ||

| By Geography | Bahrain | |

| Kuwait | ||

| Oman | ||

| Qatar | ||

| Saudi Arabia | ||

| United Arab Emirates | ||

| Yemen | ||

| Rest of the Middle East | ||

Key Questions Answered in the Report

What is the 2031 outlook for Middle East milk powder demand?

The market is expected to reach USD 5.17 billion by 2031 from USD 4.08 billion in 2026, growing at a 4.86% CAGR over 2026 to 2031.

Which product type leads sales in the region?

Dairy milk powder remained the leading type in 2025 with an 85% share, supported by broad use in food processing, household consumption, and institutional channels.

Which channel is expanding the fastest across the region?

Foodservice is the fastest-growing channel and is forecast to grow at a 6.72% CAGR through 2031 as hotels, cafés, bakeries, and caterers increase powder usage.

Why is plant-based powder gaining traction in the Middle East?

High lactose intolerance, institutional support for plant-based options, and wider consumer acceptance are helping non-dairy powder grow at a 5.76% CAGR through 2031.

Page last updated on: