Middle East Gum Arabic Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

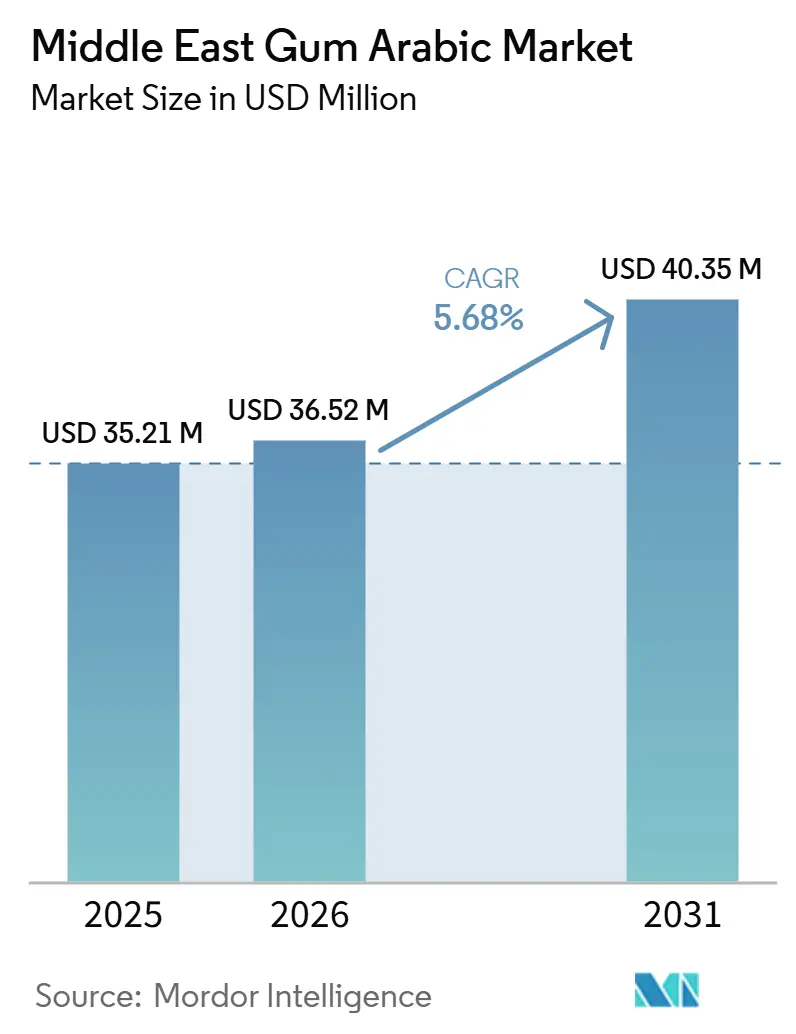

| Base Year Market Size (2025) | USD 35.21 Million |

| Market Size (2026) | USD 36.52 Million |

| Market Size (2031) | USD 40.35 Million |

| Growth Rate (2026 - 2031) | 5.68% CAGR |

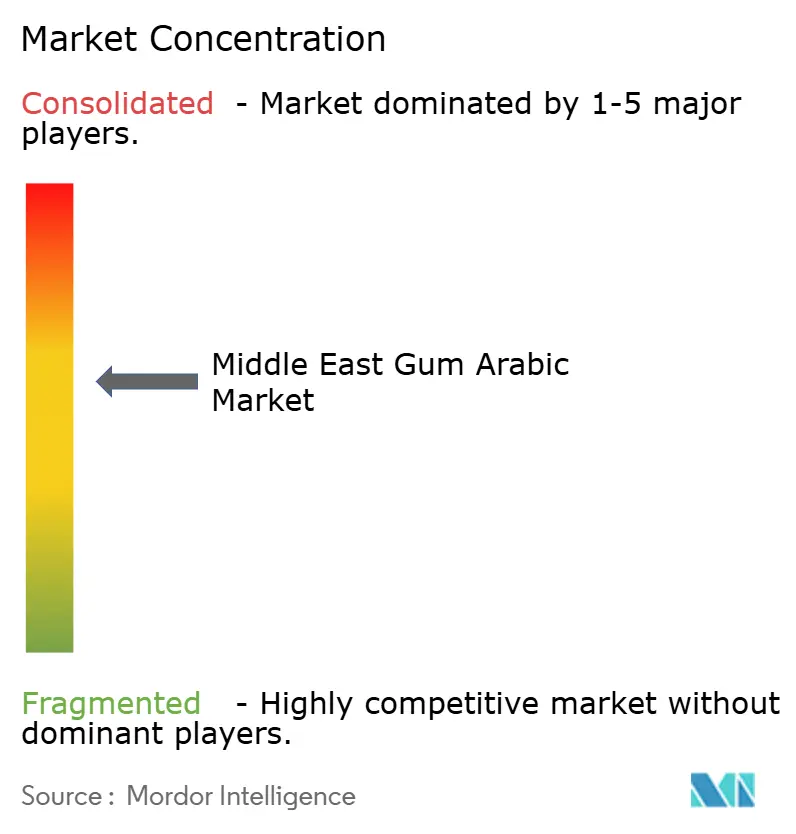

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East Gum Arabic Market Analysis by Mordor Intelligence

The Middle East gum arabic market size is projected to expand from USD 35.21 million in 2025 and USD 36.52 million in 2026 to USD 40.35 million by 2031, registering a CAGR of 5.68% between 2026 and 2031. The Middle East gum arabic market is gaining support from the region’s larger food processing base, where manufacturers are looking for natural stabilizers that fit cleaner ingredient labels and established food additive rules. Gum arabic is also benefiting from broader reformulation work in beverages, confectionery, and bakery products, where processors need stable emulsification, film-forming performance, and labeling comfort that synthetic substitutes do not always provide at the same level of acceptance. Pharmaceutical and nutraceutical demand is adding a higher-value layer to the market because buyers are using gum arabic in delivery systems, encapsulation, and fiber-based formulations that require stronger batch consistency and documentation. The effective supplier field is narrowing because regional buyers increasingly expect Halal, Kosher, food safety, and in some cases pharmaceutical-grade compliance in the same commercial relationship. The Middle East gum arabic market is also being reshaped by supply diversification away from Sudan-only sourcing, which is pushing processors and traders in the GCC toward safety stocks, dual sourcing, and tighter supplier verification practices

Key Report Takeaways

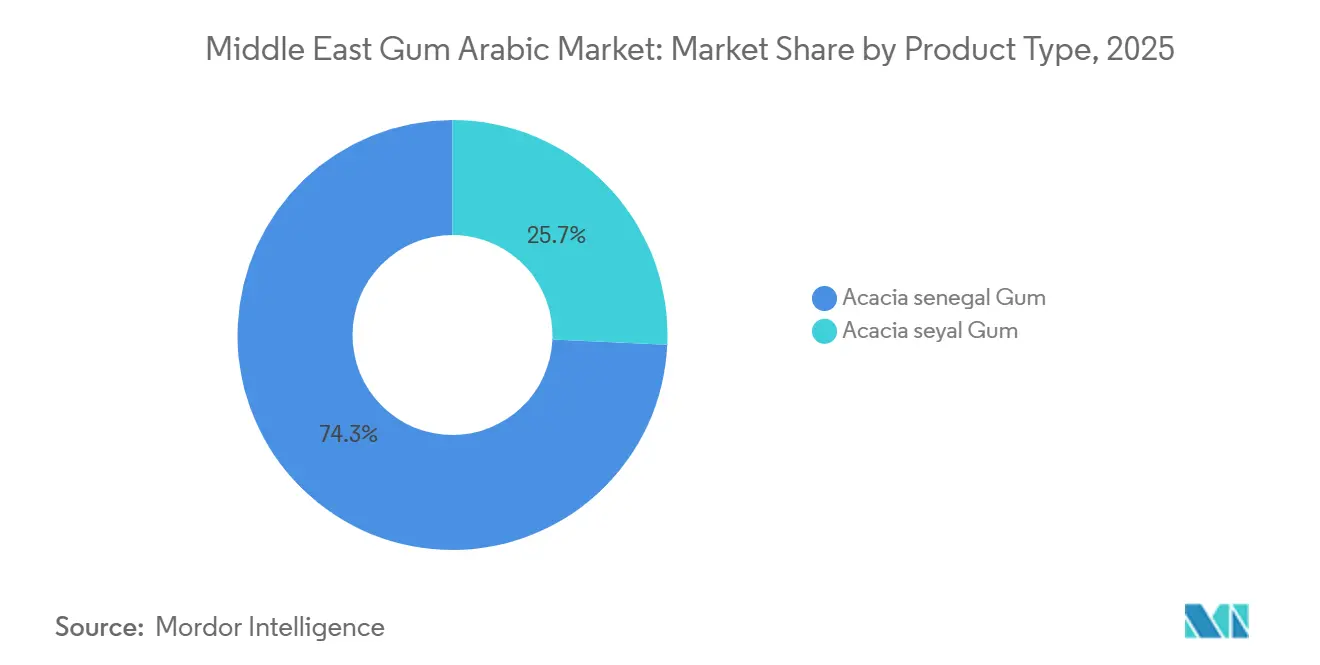

- By product type, Acacia senegal led with 74.27% revenue share in 2025, while Acacia seyal is projected to expand at a 6.78% CAGR through 2031.

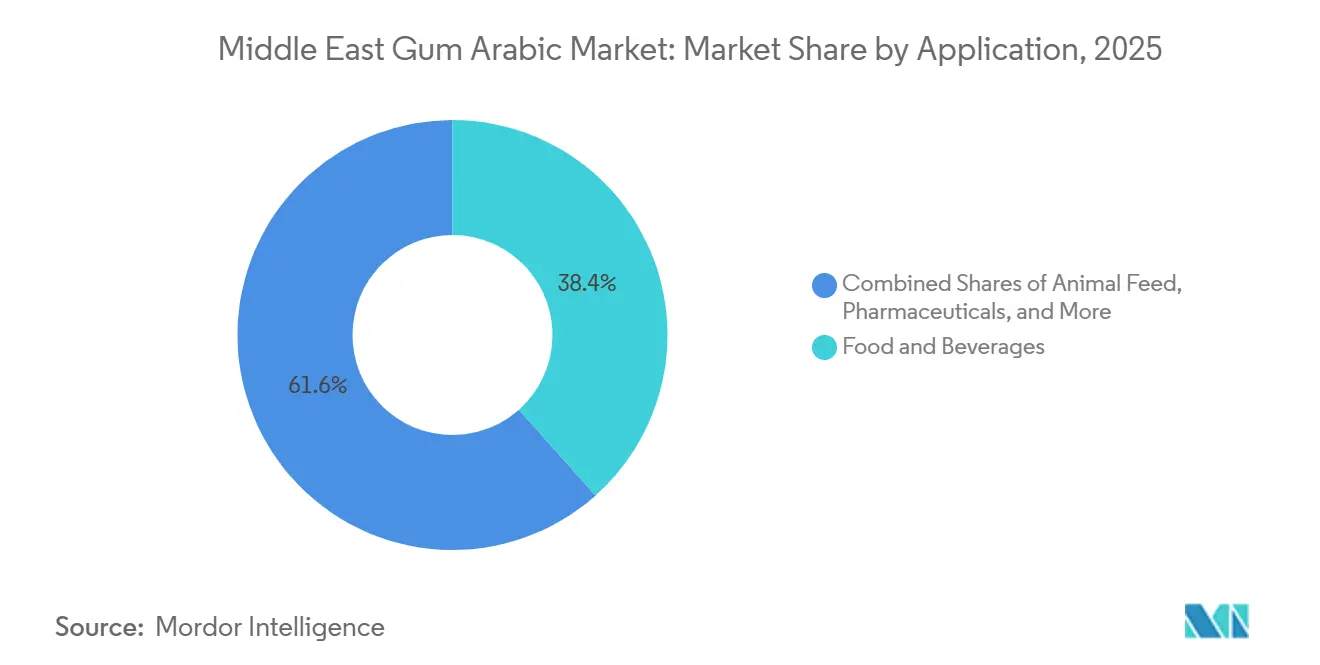

- By application, food and beverages accounted for 38.42% revenue share in 2025, while pharmaceuticals is projected to grow at a 7.02% CAGR through 2031.

- By geography, Saudi Arabia held 32.47% of the Middle East gum arabic market share in 2025, while the United Arab Emirates is projected to expand at a 6.82% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Middle East Gum Arabic Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand For Natural, Clean-Label Stabilizers In Middle Eastern Food Processing. | +1.2% | Saudi Arabia and the United Arab Emirates are primary, Qatar and Iran are secondary | Short term (≤ 2 years) |

| Expansion Of Beverage, Confectionery, And Bakery Reformulation Programs. | +1.0% | Saudi Arabia and the United Arab Emirates are core, with spillover across the GCC | Short term (≤ 2 years) |

| Growth In Halal, Plant-Based, And Free-From Product Claims. | +0.9% | GCC-wide, strongest in Saudi Arabia and the United Arab Emirates | Medium term (2-4 years) |

| Higher Use Of Gum Arabic In Nutraceutical Encapsulation And Fiber Fortification. | +0.8% | United Arab Emirates and Saudi Arabia in re-export and domestic pharmaceutical channels | Medium term (2-4 years) |

| Sudan-Sahel Supply Diversification Into GCC Re-Export And Processing Hubs. | +0.6% | United Arab Emirates is the primary re-export hub and Saudi Arabia is the main domestic processing base | Medium term (2-4 years) |

| Traceability-Led Premiumization For Pharmaceutical And Export-Grade Material. | +0.5% | United Arab Emirates and Saudi Arabia in pharmaceutical and nutraceutical clusters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Natural, Clean-Label Stabilizers in Middle Eastern Food Processing

Food processors in Saudi Arabia and the United Arab Emirates are facing stronger pressure to simplify labels and reduce reliance on additives that appear more artificial to retailers and consumers. Gum arabic fits this requirement because it is recognized under the U.S. food additive framework and Codex standards, which gives manufacturers a clear regulatory reference when they sell into structured retail and export channels[1]Source: Codex Alimentarius Commission, “GSFA Online Food Additive Details for Gum Arabic,” Food and Agriculture Organization of the United Nations, fao.org. The United Arab Emirates food processing sector is projected to generate USD 39.8 billion in 2025, and the country has more than 570 mainly small and mid-sized processors that rely heavily on imported ingredients, which creates a broad and recurring demand base for approved stabilizers. Because Dubai also works as a regional supply and redistribution point, ingredient preferences adopted there can move into neighboring GCC markets through established trade routes and distributor relationships. That pattern supports the Middle East gum arabic market because import demand at the hub level can convert into repeat downstream demand across several countries.

Expansion of Beverage, Confectionery, and Bakery Reformulation Programs

Beverage reformulation remains a core demand channel because gum arabic is widely used in flavor emulsions, spray-dried systems, and beverage bases where stable dispersion is essential. A 2025 peer-reviewed study noted that beverages accounted for 31.5% of global gum arabic usage, which supports the strong relevance of this application in the Middle East gum arabic market as local brands expand reduced-sugar and functional drink portfolios. Dubai International Chamber stated at Gulfood 2026 that retail soft drink sales in the United Arab Emirates are projected to reach USD 4.5 billion by 2030, while ready-to-drink tea is expected to grow at 9%, which points to a rising base for gum arabic use in reformulated drinks Ingredion has also introduced a pre-hydrated gum arabic spray dry powder that cuts mixing time from 4 to 16 hours down to 45 minutes, showing why processors view the ingredient as both a formulation and production tool. Similar logic applies in confectionery and bakery, where glazing, binding, and moisture-barrier roles allow manufacturers to replace some synthetic systems without giving up product handling or halal compatibility.

Growth in Halal, Plant-Based, and Free-From Product Claims

Halal compliance is no longer a niche selling point in the GCC because it functions as a basic commercial requirement for a wide range of food ingredients. Suppliers such as Norevo already present Halal and Kosher certification as standard features in their gum acacia offering, which reflects the level of documentation that many buyers now expect before they approve a product. This matters more in the Middle East gum arabic market because halal requirements are increasingly intersecting with plant-based and free-from positioning, especially in retail categories linked to wellness and premium packaged foods. The 2025 USDA report on the United Arab Emirates also pointed to a food processing base that is expanding its use of imported ingredients, and that environment favors plant-derived inputs that can support cleaner positioning on finished labels[2]Source: U.S. Department of Agriculture Foreign Agricultural Service, “Food Processing Ingredients Annual, United Arab Emirates,” USDA GAIN, apps.fas.usda.gov. As a result, gum arabic benefits not only from being natural in origin, but also from fitting a compliance pattern that retailers, importers, and brand owners can manage more easily than less transparent alternatives.

Higher Use of Gum Arabic in Nutraceutical Encapsulation and Fiber Fortification

Recent scientific work has strengthened the pharmaceutical and nutraceutical case for gum arabic beyond its traditional use as an excipient. A 2025 review in Carbohydrate Polymers described how gum arabic can support hydrogels, nanoparticles, liposomes, and emulsion systems used in cancer therapy, antimicrobial applications, and bioimaging, which broadens its relevance in advanced formulation work. A 2026 study in Carbohydrate Polymer Technologies and Applications also documented gum arabic’s role as an encapsulant for co-delivery of fat-soluble bioactives in W/O/W microcapsule systems with strong gastrointestinal stability. Kerry’s Emulgold Fibre range adds a commercial example because it is positioned around clinically validated prebiotic functionality, which helps explain why supplement and wellness brands are giving more attention to acacia-derived fiber formats. This shift gives the Middle East gum arabic market a stronger premium segment because higher specification demand usually places more weight on documentation, consistency, and traceability than on lowest-price sourcing.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heavy Dependence On Imported Raw Gum And Cross-Border Logistics Risk. | -0.7% | GCC-wide, most acute in Saudi Arabia as the largest importer base | Short term (≤ 2 years) |

| Price Sensitivity Versus Lower-Cost Hydrocolloid Substitutes. | -0.5% | United Arab Emirates and Iran among industrial food processors | Medium term (2-4 years) |

| Batch Variability From Source Fragmentation And Adulteration Risk. | -0.4% | Saudi Arabia and the United Arab Emirates among pharmaceutical and export-grade buyers | Medium term (2-4 years) |

| Conflict, Weather, And Harvest Volatility In The Wider Gum Belt. | -0.6% | GCC-wide exposure through imports from Sudan, Chad, and Nigeria | Short term (≤ 2 years) to Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Heavy Dependence on Imported Raw Gum and Cross-Border Logistics Risk

The region remains dependent on imported raw or semi-processed gum arabic because there is no meaningful domestic acacia cultivation base. Supply risk has risen since the Sudan conflict disrupted flows from the world’s most important producing area, and Reuters reported that uncertified material has moved through neighboring countries into informal channels that complicate origin checks. AIPG stated in March 2025 that Sudan still exported more than 70,000 tonnes in 2024 through Port Sudan, but it also noted that transport from inland producing zones had become more difficult and costly. This creates direct pressure in the Middle East gum arabic market because processors must manage higher freight, longer lead times, and tighter supplier screening before material enters food or pharmaceutical use. The result is a market where security of supply can influence purchasing decisions even when buyers remain resistant to broad price pass-throughs.

Price Sensitivity Versus Lower-Cost Hydrocolloid Substitutes

Price remains a clear barrier in lower-value industrial food uses where manufacturers focus mainly on basic emulsification or texture support. The 2025 peer-reviewed market review noted that pharmaceutical-grade and certified gum arabic can sell at USD 5 to 10 per kilogram, while xanthan gum or guar gum can be available at USD 1 to 3 per kilogram, which creates a wide economic gap in cost-sensitive formulations. That gap matters in Iran and in smaller confectionery or bakery operations across the GCC, where procurement teams may not have the technical support needed to prove gum arabic’s higher functional value in a finished product. In those cases, the Middle East gum arabic market grows faster when suppliers offer application-specific grades and practical formulation support rather than a generic ingredient sale. Without that commercial support, substitute gums remain a credible option for buyers who are managing tight raw material budgets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Acacia Senegal Led While Acacia Seyal Grew Faster

Acacia senegal held 74.27% of the Middle East gum arabic market share in 2025, which kept it as the leading product type by a wide margin. Its position reflects stronger emulsification, film-forming behavior, and broader acceptance in beverage, confectionery, and pharmaceutical uses where performance consistency matters more than the lowest possible cost. The European Union’s 2026 regulation on gum arabic also reinforces the central role of Acacia senegal by setting updated purity and compositional expectations that export-oriented GCC manufacturers will need to follow closely[3]Source: European Commission, “Commission Regulation (EU) 2026/196 of 28 January 2026 Amending Regulation (EC) No 1333/2008 as Regards Gum Arabic (Acacia Gum) (E414),” EUR-Lex, eur-lex.europa.eu. This gives the dominant grade an added regulatory advantage in the Middle East gum arabic market because buyers serving formal retail and pharmaceutical channels tend to prefer the more established specification path. The segment therefore remains the reference grade for quality-sensitive demand across the region.

Acacia seyal is projected to record the fastest growth at a 6.78% CAGR through 2031, and that pace reflects a different value proposition centered on cost accessibility and broader use in beverage stabilization and industrial bakery applications. The Middle East gum arabic market is giving Seyal more room because some processors can accept a lower emulsification intensity when they gain savings and sourcing flexibility in return. Reuters also showed how the disruption around Sudanese Hashab-producing zones has pushed buyers to rethink grade and origin choices, which indirectly helps Seyal when Senegal-heavy sourcing becomes harder to secure on stable terms. Peer-reviewed analysis further noted innovation around blended and lower-carbon acacia formats, which suggests suppliers are trying to position Seyal-based solutions as more practical options rather than simple low-cost substitutes. Within the Middle East gum arabic industry, that gives Seyal a stronger role in value-engineered reformulation programs.

By Application: Food and Beverages Stayed Largest While Pharmaceuticals Expanded Fastest

Food and beverages accounted for a 38.42% share of the Middle East gum arabic market size in 2025, making it the largest application group. This segment covers bakery and confectionery, dairy and dairy products, beverages, and the meat industry, which gives it a wide operational base even when growth rates differ across subcategories. Beverage use remains especially important because gum arabic supports flavor emulsions, spray-dried bases, and cleaner-label product design in ways that align with active reformulation work in the Gulf. Bakery and confectionery remain steady volume users because glazing and binding functions are routine, while dairy applications are gaining more space as manufacturers explore fat replacement and stabilization in modernized product lines. The Middle East gum arabic market therefore still depends heavily on food processing demand, even as higher-value applications gain traction at a faster pace.

The Middle East gum arabic market size for pharmaceuticals is projected to expand at a 7.02% CAGR between 2026 and 2031, which makes it the fastest-growing application. Scientific literature published in 2025 and 2026 supports this shift by documenting gum arabic’s use in colon-targeted systems, vitamin delivery, nanoparticle formulations, and other advanced carrier formats. Cosmetics and personal care are also becoming a premium niche, especially in the United Arab Emirates, where film-forming and natural binder functions fit higher-end formulations that require traceable and certified inputs. Animal feed and pet food remain smaller in value, but EFSA’s safety confirmation supports stable adoption where regional premium feed producers need regulatory comfort. Within the Middle East gum arabic industry, this application mix means growth is no longer driven only by traditional food uses.

Geography Analysis

Saudi Arabia accounted for 32.47% of the Middle East gum arabic market share in 2025, which kept it as the largest country market in the region. Its lead comes from the scale of domestic food manufacturing, the need for halal-compliant ingredient systems, and a procurement environment that is becoming more specification driven. Saudi buyers are also affected more directly by import logistics because the country represents one of the biggest end markets for processed foods in the GCC, so security of supply matters alongside price. Iran contributes a steady base of demand through confectionery and bakery manufacturing, even though import complexity and cost pressure limit how quickly volumes can shift toward premium grades. Qatar adds a smaller but higher-specification channel, where premium food service and selective consumer categories can support demand for certified or pharmaceutical-grade material.

The United Arab Emirates is projected to grow at a 6.82% CAGR through 2031, which makes it the fastest-growing geography in the Middle East gum arabic market. The country combines domestic demand with a re-export role, and that dual function gives suppliers access to both local processors and neighboring GCC destinations from a single commercial base. USDA projected the United Arab Emirates food processing sector at USD 39.8 billion in 2025, supported by a large base of mostly small and mid-sized processors that depend on imported ingredients. The country’s logistics strength and documentation services make it especially important for repackaging, redistribution, and certification-linked trade across the GCC.

The rest of the region adds incremental volume rather than a dominant demand block, but it still matters for regional depth and distribution reach. Smaller GCC economies benefit from the same trade corridors that move ingredients through the United Arab Emirates, which lets suppliers serve multiple markets without building a full direct presence in each one. This pattern supports the Middle East gum arabic market because demand can spread through distributor networks even when country-level consumption remains modest. Over time, the regional balance is likely to keep favoring Saudi Arabia for scale and the United Arab Emirates for growth, while Iran, Qatar, and the wider Middle East provide a steady secondary layer of demand.

Competitive Landscape

The Middle East gum arabic market remains highly fragmented because no single supplier controls the full range of grades, certifications, and end-use relationships across the region. Competition is spread across global ingredient companies, European specialty processors, and origin-linked suppliers that serve the GCC either directly or through traders and re-export channels. Buyers therefore compare vendors not only on price, but also on audit readiness, grade consistency, halal and kosher documentation, and response times during supply disruptions. This keeps the market open to several supplier types at once, but it also raises the minimum operating standard for companies that want durable customer relationships. In practice, the strongest positions are usually held by companies that can combine product performance with traceability and a reliable service model.

Ingredion and Kerry illustrate how larger players are defending their positions through application-driven offerings rather than commodity selling. Ingredion extended its hydrocolloid capabilities with a pre-hydrated gum arabic spray-dried powder that can reduce mixing time to 45 minutes, which directly addresses manufacturing efficiency for beverage processors. Kerry has positioned Emulgold Fibre around clinically validated prebiotic functionality, which gives it a stronger case in nutraceutical and health-focused formulations. These moves matter in the Middle East gum arabic market because customers increasingly want technical support and documented functionality, not only raw supply.

European specialists are also using certification, capacity, and sustainability to strengthen their place in regional supply chains. Alland & Robert published its 2025 CSR report around supply chain ethics and traceability, while DKSH expanded its exclusive distribution agreement with the company across additional markets, showing continued investment in commercial reach and documentation quality. Norevo continues to treat Halal and Kosher certification as standard commercial features, which fits a market where compliance is often part of basic supplier qualification. The Middle East gum arabic market is also leaving room for smaller certified suppliers because conflict-related sourcing shifts have encouraged buyers to widen their approved supplier lists and reduce single-origin exposure

Middle East Gum Arabic Industry Leaders

Kerry Group Plc

Ingredion Incorporated

Agrigum International Limited

Cargill, Inc.

Archer Daniels Midland Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Anadolu Agency reported that Sudan's civil war is actively disrupting global gum arabic supply chains, with Kordofan and Darfur production zones, the heartland of Acacia senegal cultivation, heavily affected by RSF-SAF fighting; the report noted that Sudan supplied 70-80% of pre-war global gum arabic and that illegal logging of acacia trees has compounded the long-term supply risk beyond immediate conflict disruption.

- March 2025: AIPG (Association for International Promotion of Gums) issued an official update confirming that Sudan exported over 70,000 tonnes of acacia gum in 2024, with 50,000 tonnes going to Europe through secure Port Sudan export corridors; the Association affirmed that traceability and legitimacy of certified exports remain intact through AIPG member verification protocols, providing a measure of supply security reassurance for GCC procurement teams.

Middle East Gum Arabic Market Report Scope

| Acacia senegal Gum |

| Acacia seyal Gum |

| Food and Beverages | Bakery and Confectionery |

| Dairy and Dairy Products | |

| Meat Industry | |

| Beverages | |

| Others | |

| Animal Feed and Pet Food | |

| Pharmaceuticals | |

| Cosmetics and Personal Care | |

| Others |

| Saudi Arabia |

| United Arab Emirates |

| Iran |

| Qatar |

| Rest of the Middle East |

| By Product Type | Acacia senegal Gum | |

| Acacia seyal Gum | ||

| By Application | Food and Beverages | Bakery and Confectionery |

| Dairy and Dairy Products | ||

| Meat Industry | ||

| Beverages | ||

| Others | ||

| Animal Feed and Pet Food | ||

| Pharmaceuticals | ||

| Cosmetics and Personal Care | ||

| Others | ||

| By Geography | Saudi Arabia | |

| United Arab Emirates | ||

| Iran | ||

| Qatar | ||

| Rest of the Middle East | ||

Key Questions Answered in the Report

What is the expected value of the Middle East gum arabic market by 2031?

The Middle East gum arabic market is projected to reach USD 40.35 million by 2031 from USD 36.52 million in 2026, with a CAGR of 5.68%.

Which country leads regional demand for gum arabic in the Middle East?

Saudi Arabia led regional demand with a 32.47% revenue share in 2025, supported by its large food manufacturing base and stronger halal-driven ingredient requirements.

Which product type holds the largest share in Middle East gum arabic demand?

Acacia senegal was the leading product type with a 74.27% revenue share in 2025 because it remains the preferred grade for emulsification and compliance-sensitive uses.

Which application is growing the fastest for gum arabic in the region?

Pharmaceuticals is the fastest-growing application, with a projected CAGR of 7.02% through 2031, supported by rising use in encapsulation and advanced delivery systems.

Page last updated on: