Middle East Fixed Broadband Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

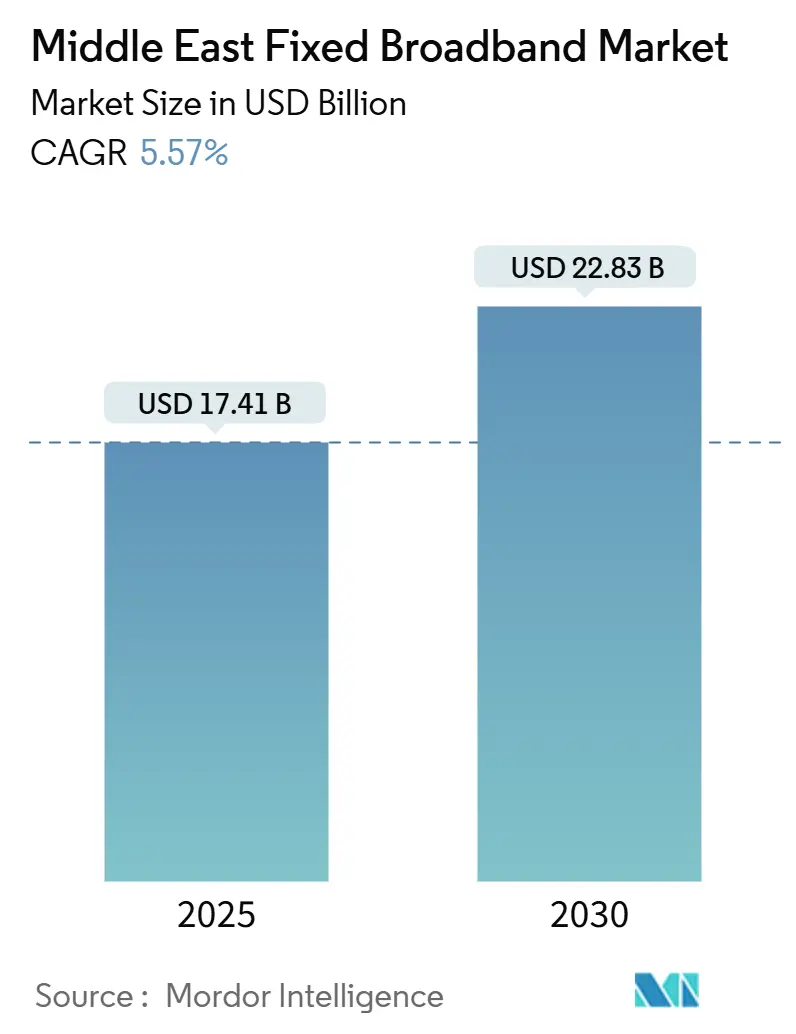

| Market Size (2025) | USD 17.41 Billion |

| Market Size (2030) | USD 22.83 Billion |

| Growth Rate (2025 - 2030) | 5.57% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East Fixed Broadband Market Analysis by Mordor Intelligence

The Middle East Fixed Broadband Market size is estimated at USD 17.41 billion in 2025, and is expected to reach USD 22.83 billion by 2030, at a CAGR of 5.57% during the forecast period (2025-2030).

Robust government-backed gigabit agendas, operator fiber-first strategies, hyperscale data-center build-outs, and rapidly rising cloud and gaming traffic underpin this dependable growth path. Accelerated Fiber-to-the-Home/Premises (FTTH/B) roll-outs, 5G Fixed Wireless Access (FWA) for suburban fill-in, and megaproject smart-city requirements form a virtuous investment cycle that keeps capital flowing into last-mile and backhaul infrastructure. Competitive dynamics are widening as open-access regulations invite over-builders and as LEO-satellite concessions become commercially viable for desert and offshore links. Incumbent telcos guard their base through XGS-PON, 25G PON, and Wi-Fi 7 upgrades, while disruptive Fixed Wireless ISPs ride 5G-Advanced spectrum assets to win cost-sensitive households. Macroeconomic resilience, coupled with young, digitally savvy demographics, keeps household broadband penetration expanding despite sporadic price competition and political headwinds.

Key Report Takeaways

- By technology, FTTH/B captured 46.66% revenue share of the Middle East fixed broadband market in 2024, while the same platform is on track for an 11.28% CAGR through 2030.

- By speed tier, the 100 Mbps–1 Gbps band led with 64.43% share in 2024, whereas services above 1 Gbps are forecast to expand at a 20.60% CAGR to 2030.

- By end user, residential connections held 86.98% share in 2024, while commercial subscriptions are projected to grow at a 9.18% CAGR over the forecast period.

- By application, video streaming and entertainment accounted for 35.82% share in 2024, whereas smart home and IoT connectivity is expected to register a 13.62% CAGR to 2030.

- By deployment environment, urban areas dominated with 70.98% share in 2024, while rural roll-outs are advancing at an 8.00% CAGR through 2030.

- By ownership, incumbent telcos commanded 38.96% share in 2024, whereas fixed wireless ISPs are expanding at a 10.54% CAGR over the same period.

- By geography, Saudi Arabia led with 40.66% revenue share in 2024, and Oman is poised to grow at an 8.59% CAGR through 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Worldwide, activity is shaped by contributions from multiple regions, with Middle east representing one of the more structurally developed among them. The global report on fixed broadband market by Mordor Intelligence reflects how these regional layers combine into a single system.

Middle East Fixed Broadband Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| FTTH acceleration under national gigabit agendas | 1.1% | Saudi Arabia, UAE, Qatar, Kuwait | Medium term (2-4 years) |

| 5G-based Fixed Wireless Access filling suburban coverage gaps | 1.2% | GCC region, Turkey, Israel | Short term (≤ 2 years) |

| Large-scale hyperscale and edge-data-centre build-outs needing terabit backhaul | 0.8% | UAE, Saudi Arabia, Qatar | Long term (≥ 4 years) |

| Megaproject smart-city roll-outs demanding multi-gig residential links | 0.6% | Saudi Arabia (NEOM), Qatar (Lusail) | Long term (≥ 4 years) |

| Open-access fibre regulations incentivising competitive over-builders | 0.4% | Saudi Arabia, UAE | Medium term (2-4 years) |

| Licensed LEO satellite constellations bringing broadband to oilfields and deserts | 0.3% | Saudi Arabia, Oman, UAE remote areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

FTTH Acceleration Under National Gigabit Agendas

Gulf governments place fiber connectivity at the core of digital strategies, evidenced by Saudi Arabia’s 10 Gbps Society program and the UAE’s world-leading 99.3% FTTH reach. [1]SAMENA Telecommunications Council, “FTTH/B Uptake in the GCC,” samena.org Unified right-of-way, bulk-procurement, and wholesale mandates lower deployment costs and shorten build cycles. Regulators such as Saudi Arabia’s CITC require infrastructure sharing, allowing alternative players to lease dark fiber and extend coverage. [2]Communications and Information Technology Commission, “Wholesale Fiber Access Regulations,” citc.gov.saQatar and Kuwait mirror these policies through multi-year public tenders that bundle urban and rural clusters, generating scale efficiencies for vendors. As a result, operators upgrade passive networks to XGS-PON and initiate 25G PON trials, ensuring that new capacity headroom aligns with cloud gaming and 8K streaming trajectories.

5G-based Fixed Wireless Access Filling Suburban Coverage Gaps

Operators leverage mid-band and mmWave licenses to deliver broadband without trenching, a tactic that cuts lead times from months to days. In the UAE, du surpassed 600 000 FWA lines while maintaining premium ARPU compared with entry-tier fiber packages. Zain’s USD 427 million program targets 122 Saudi cities, bundling outdoor CPE with unlimited plans that siphon traffic from legacy DSL loops. Rapid plug-and-play characteristics make FWA the default fix for exurban neighborhoods and new villa compounds pending fiber civils. Network slicing and carrier aggregation baked into 5G-Advanced roadmaps promise multi-gigabit throughput, narrowing experiential gaps between wireless and wireline.

Large-Scale Hyperscale and Edge-Data-Center Buildouts Needing Terabit Backhaul

Cloud majors, global CDNs, and regional telcos funnel capital into campus-style facilities that anchor wholesale fiber demand. stc realized a 1 Tbps single-wavelength record on its data-center ring using Nokia PSE-6s optics, pre-empting escalating east-west traffic. [3]Nokia, “stc Achieves 1 Tb/s Data Center Connection,” nokia.com AWS’s Bahrain availability zones, coupled with fresh builds in Riyadh and Dubai, concentrate workloads that stress inter-metro trunks. Edge nodes serving gaming and XR offload propagate dense metro rings, while submarine extensions such as the 45 000 km Africa 2 Pearls cable expand international reach. The virtuous circle between data-center gravity and backhaul upgrades reinforces the long-term bandwidth slope.

Megaproject Smart-City Rollouts Demanding Multi-Gig Residential Links

Flagship developments like NEOM and Lusail weave fiber deep into every premises, dictating symmetrical 10 Gbps baselines for homes, offices, and public venues. NEOM’s blueprint prescribes fiber-to-the-room for immersive XR, autonomous transport telemetry, and AI-driven utilities. These requirements spill over into adjacent municipalities as operators harmonize speed tiers across footprints to avoid brand dilution. Suppliers benefit from volume orders of 10G ONTs and coherent pluggables, while integrators capture design-and-build contracts for in-building cabling and neutral-host Wi-Fi 7 meshes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High last-mile capex across sparsely populated terrain | -0.7% | Oman, Saudi Arabia rural areas, UAE remote regions | Long term (≥ 4 years) |

| Ongoing geopolitical conflicts delaying network roll-outs in Levant and Yemen | -0.5% | Syria, Yemen, Lebanon, affected regional routes | Medium term (2-4 years) |

| Legacy copper/DSL lock-in inflating opex for incumbents | -0.4% | Turkey, Israel, parts of Saudi Arabia | Medium term (2-4 years) |

| Ultra-cheap mobile data plans cannibalising fixed subscriptions | -0.3% | Regional, particularly price-sensitive segments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Last-Mile Capex Across Sparsely Populated Terrain

Desert expanses and rugged mountains challenge trenching economics, with per-home-passed costs tripling when density dips below 50 dwellings per square kilometer. Operators mitigate through hybrid blueprints that blend 5G FWA, microwave backhaul, and, increasingly, LEO satellite overlays. Starlink and OneWeb secure landing rights to serve oil rigs and border posts, although terminal subsidies remain a hurdle for consumer pricing. Government funds under Saudi Vision 2030 offset part of the bill, yet unit economics still trail urban fiber yields, restraining aggregate take-up curves.

Ongoing Geopolitical Conflicts Delaying Network Rollouts in Levant and Yemen

Physical damage exceeding USD 2.2 billion in Syria’s telecom grid and chronic currency shortages in Lebanon stall rehabilitation timetables. Submarine cable reroutes circumvent disputed waters, adding latency and incremental capex to redundancy paths. Vendor risk committees apply higher hurdle rates to projects in conflict zones, meaning finance closes slower and equipment ships later. While eventual reconstruction could unlock step-change demand, forecasting visibility remains clouded, shaving points off the near-term growth outlook.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Fiber Dominance Drives Market Evolution

FTTH/B holds the largest 46.66% share of the Middle East fixed broadband market in 2024, and its 11.28% CAGR through 2030 underscores a decisive pivot away from copper. The Middle East fixed broadband market size for FTTH/B is forecast to widen by USD 2.9 billion between 2025 and 2030 as operators transition to 10G PON overlays. Cable DOCSIS networks sustain relevance in Israel and urban Turkey, but upgrade roadmaps to DOCSIS 4.0 merely hedge against fiber over-builders. DSL shrinkage accelerates following Telecom Egypt’s 96% copper-to-fiber migration milestone.

Fixed Wireless Access scales in lockstep with 5G coverage, delivering interim broadband while fiber permits are secured. Satellite options now ride LEO constellations that cut round-trip delay to 30–40 ms, making OTT video watchable and VoIP reliable. Vendor ecosystems mature: Nokia tallied 166 commercial F5.5G sites worldwide, and Huawei surpassed 300 million global gigabit subs, translating into predictable supply-chain availability for regional roll-outs. The technology mix therefore solidifies around a fiber core complemented by wireless edge extensions.

By Speed Tier: Multi-Gigabit Services Reshape Expectations

Connections above 1 Gbps recorded a blistering 20.60% CAGR to 2030, yet the 100 Mbps–1 Gbps band still owns 64.43% of the Middle East fixed broadband market in 2024. Cloud gaming, 8K streaming, and AI-enabled smart homes normalise multi-gig aspirations, prompting operators to bundle 2 Gbps and 10 Gbps options alongside gaming routers. The Middle East fixed broadband market size for ≥ 1 Gbps tiers is projected to triple by 2030 as edge caching and Wi-Fi 7 adoption lower in-home bottlenecks.

Below-25 Mbps plans decline as incumbents retire ADSL ports and force-migrate legacy users. Bezeq’s Wi-Fi 7 launch couples XGS-PON backhaul with 10 Gbps LAN, turning the living room into a low-latency e-sports arena. This cascading uplift in advertised speeds cements user perception that anything under 100 Mbps is obsolete, driving self-selection into higher ARPU brackets.

By End User: Commercial Segment Accelerates Digital Transformation

Residential demand remains the backbone, but commercial circuits grow fastest at 9.18% CAGR as enterprises pursue SD-WAN overlays and cloud-first productivity. The Middle East fixed broadband market share for commercial accounts is expected to reach 18% by 2030, fueled by data-center interconnects and SaaS adoption. Hybrid work persistence forces SMEs to upgrade from best-effort ADSL to SLA-backed fiber, pushing operators to segment product portfolios.

Meanwhile, retail subscribers benefit from telco-OTT bundles that package streaming, gaming passes, and smart-home sensors into multi-play contracts. This cross-sell environment raises churn barriers and monetizes bandwidth increments. Commercial clients demand symmetric throughput and burstable options that dovetail with multi-cloud traffic, generating margin-accretive upsell opportunities.

By Application: Smart Home and IoT Connectivity Drives Innovation

Video streaming and entertainment capture 35.82% revenue share, but smart-home and IoT workloads top the growth leaderboard at 13.62% CAGR. Saudi Arabia’s 50% gamer penetration and UAE’s 77% gamer rate inject low-latency volatility into evening peaks, convincing ISPs to prioritize packet acceleration and network-based QoS. The Middle East fixed broadband market continues to pivot toward use-cases that demand symmetrical bandwidth, such as telehealth diagnostics and VR schooling.

Industrial IoT inside oil fields and logistics corridors gains traction via private fiber loops and satellite uplinks, underwriting partnerships between telcos and vertical-specific integrators. Application diversity thus underlines the strategic need for programmable networks capable of slicing throughput for deterministic latency.

By Deployment Environment: Urban Concentration with Rural Upside

Urban areas own 70.98% of active lines, reflecting population clustering and megacity investments. Still, rural environments display an 8.00% CAGR thanks to subsidy schemes and FWA plug-ins that skirt trenching hurdles. The Middle East fixed broadband market size attributable to rural roll-outs will almost double by 2030 once LEO satellites commoditize backhaul for desert hamlets.

Suburban belts around Riyadh, Jeddah, and Muscat serve as battlegrounds where incumbents drop aerial fiber while challengers seed 5G CPE promos. Remote oil installations pivot to satellite backhaul augmented by fiber-spurs where feasible, illustrating a mosaic deployment pattern anchored in cost-per-bit calculus.

By Ownership: Fixed Wireless ISPs Challenge Incumbent Dominance

Incumbent telcos still command 38.96% of subscribers, yet Fixed Wireless ISPs clip double-digit growth as spectrum-light entrants harness 5G FWA to cherry-pick underserved clusters. Open-access edicts permit over-builders to lease fiber, spawning multi-tenant networks that diversify service propositions. The Middle East fixed broadband industry witnesses tower-co spinoffs, typified by the PIF-STC entity that now controls 30 000 masts, slashing passive opex and freeing capital for core upgrades.

Cable MSOs retain beachheads in Israeli metros through DOCSIS 3.1 expansions, while satellite network operators court maritime and remote enterprise clientele. Ownership heterogeneity fuels price competition, catalyzing faster adoption curves in consumer segments and bespoke SLA tiers for corporates.

Geography Analysis

Saudi Arabia cements its pre-eminence with 40.66% of 2024 revenue, propelled by Vision 2030 digital imperatives that prioritize FTTH to 3.5 million new dwellings and nationwide 5G coverage. Zain’s USD 427 million injection and stc’s terabit backhaul trials illustrate continuous capex intensity, while CITC’s open-access orders spark smaller fiber players to over-build dense districts. Megaprojects like NEOM enforce 10 Gbps benchmarks, effectively dragging nationwide service menus upward.

The United Arab Emirates showcases 99.3% FTTH penetration, the highest globally, exemplifying how cohesive policy and proactive regulation fast-track universal broadband. du’s 5G-Advanced pilots yield headline residential rates above 2 Gbps, complemented by UAE-IX’s 400G peering fabric that lowers content round-trip latency for streaming platforms. Data-center investments topping USD 1.5 billion through 2027 escalate enterprise connectivity orders in Dubai and Abu Dhabi, reinforcing the Middle East fixed broadband market as a backbone for cloud economics.

Oman leads growth charts at an 8.59% CAGR on the back of early 5G FWA roll-outs and a wholesale fiber network that opened last-mile access to newcomers. Qatar, Kuwait, and Bahrain sustain mid-single-digit expansion, riding smart-city investments and favorable spectrum policies. The Levant struggles under geopolitical strain, but stabilizing pockets in Jordan and Iraq hint at deferred demand ready to convert once governance and capital return. Remote regions across the Arabian Peninsula witness the first commercial LEO satellite packages, promising to close the digital divide once terminal prices slide under USD 200.

Mordor Intelligence provides coverage of the fixed broadband market across other key regional markets, including South America, Africa, and North America, each with their regulatory frameworks and demand patterns.

Competitive Landscape

Competition remains moderately concentrated, yet structural reforms push the Middle East fixed broadband market toward greater plurality. Incumbents anchor multi-play bundles and exploit scale to roll out parallel 5G and fiber networks, but must now contend with Fixed Wireless ISPs using agile go-to-market models and lower unit-cost CPE. Open-access regimes in Saudi Arabia and the UAE dismantle historical bottlenecks, empowering smaller over-builders to target high-ARPU neighborhoods with promotional gigabit tiers.

Technology races orbit around 10G PON and 25G PON trials, Wi-Fi 7 gateways, and network slicing for low-latency gaming. Tower-co monetization, typified by the USD 1.3 billion PIF-STC merge, releases balance-sheet headroom for fiber densification while ensuring shared passive infrastructure lowers rural build costs. Suppliers such as Nokia and Huawei provide converged fiber-plus-wireless toolkits that let telcos deliver deterministic SLAs, real-time telemetry, and AI-driven self-optimizing networks.

White-space opportunities cluster in enterprise cloud connect, managed SD-WAN for SMEs, and rural satellite wholesaling. LEO constellations catalyze new service categories for offshore rigs and desert camps, further fragmenting the addressable base. Against this backdrop, the Middle East fixed broadband industry evolves from a vertically integrated telco model into an ecosystem of wholesale-retail specialists, infra-cos, and application-centric over-the-top partners.

Middle East Fixed Broadband Industry Leaders

Saudi Telecom Company

Emirates Telecommunications Group Company PJSC

Turkcell Superonline

Bahrain Telecommunications Company B.S.C.

Emirates Integrated Telecommunications Company PJSC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: PIF and STC completed tower merger creating the Middle East’s largest towerco with approximately 30 000 towers and USD 1.3 billion annual revenue.

- December 2024: Ooredoo Group and TASC Towers finalized consolidation valued at USD 2.2 billion covering nearly 30 000 towers across six MENA markets.

- November 2024: STC Group launched “Africa 2 Pearls” submarine cable project spanning 45 000 km with USD 300 million investment.

- October 2024: Nokia and ACES-NH announced Saudi Arabia’s first 25G PON-based neutral-host network deployment.

Middle East Fixed Broadband Market Report Scope

| Fiber to the Home / Premises (FTTH/B) |

| Cable (DOCSIS) |

| Digital Subscriber Line (DSL) and Copper |

| Fixed Wireless Access (5G/LTE) |

| Satellite Broadband |

| Up to 25 Mbps |

| 100 Mbps - 1 Gbps |

| Above 1 Gbps (Multi-Gig) |

| Residential |

| Commercial |

| Video Streaming and Entertainment |

| Online Gaming and Immersive Media |

| Remote Work and Cloud Collaboration |

| Smart Home and IoT Connectivity |

| Telehealth and Distance Learning |

| Industrial and Enterprise Automation |

| Urban |

| Suburban |

| Rural |

| Remote and Hard-to-Reach |

| Incumbent Telcos |

| Competitive Fibre Over-builders |

| Cable Multiple System Operators (MSOs) |

| Fixed Wireless ISPs |

| Satellite Network Operators |

| Saudi Arabia |

| United Arab Emirates |

| Israel |

| Turkey |

| Qatar |

| Kuwait |

| Oman |

| Bahrain |

| Rest of Middle East (Syria, Yemen, Jordan, Iraq, Iran and others) |

| By Technology | Fiber to the Home / Premises (FTTH/B) |

| Cable (DOCSIS) | |

| Digital Subscriber Line (DSL) and Copper | |

| Fixed Wireless Access (5G/LTE) | |

| Satellite Broadband | |

| By Speed Tier | Up to 25 Mbps |

| 100 Mbps - 1 Gbps | |

| Above 1 Gbps (Multi-Gig) | |

| By End User | Residential |

| Commercial | |

| By Application | Video Streaming and Entertainment |

| Online Gaming and Immersive Media | |

| Remote Work and Cloud Collaboration | |

| Smart Home and IoT Connectivity | |

| Telehealth and Distance Learning | |

| Industrial and Enterprise Automation | |

| By Deployment Environment | Urban |

| Suburban | |

| Rural | |

| Remote and Hard-to-Reach | |

| By Ownership | Incumbent Telcos |

| Competitive Fibre Over-builders | |

| Cable Multiple System Operators (MSOs) | |

| Fixed Wireless ISPs | |

| Satellite Network Operators | |

| By Country | Saudi Arabia |

| United Arab Emirates | |

| Israel | |

| Turkey | |

| Qatar | |

| Kuwait | |

| Oman | |

| Bahrain | |

| Rest of Middle East (Syria, Yemen, Jordan, Iraq, Iran and others) |

Key Questions Answered in the Report

What is the current value of the Middle East fixed broadband market?

The market is valued at USD 17.41 billion in 2025 and is forecast to climb to USD 22.83 billion by 2030.

How fast is FTTH/B growing across the region?

FTTH/B connections are expanding at 11.28% CAGR, the fastest among all fixed-line technologies.

Which country leads regional broadband revenues?

Saudi Arabia contributes 40.66% of total revenue, supported by Vision 2030 digital priorities.

Why are 5G FWA services important for suburban areas?

5G FWA lets operators bypass costly trenching, offering plug-and-play gigabit service that widens coverage in low-density districts.

What applications are driving multi-gigabit uptake?

Cloud gaming, 8K streaming, and smart-home IoT demand symmetrical multi-gigabit speeds with low latency.

How does tower-co consolidation affect broadband roll-outs?

Asset-light tower-cos cut passive opex for operators, freeing capital to accelerate fiber and 5G deployments.

Page last updated on: