Middle East ESIM Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

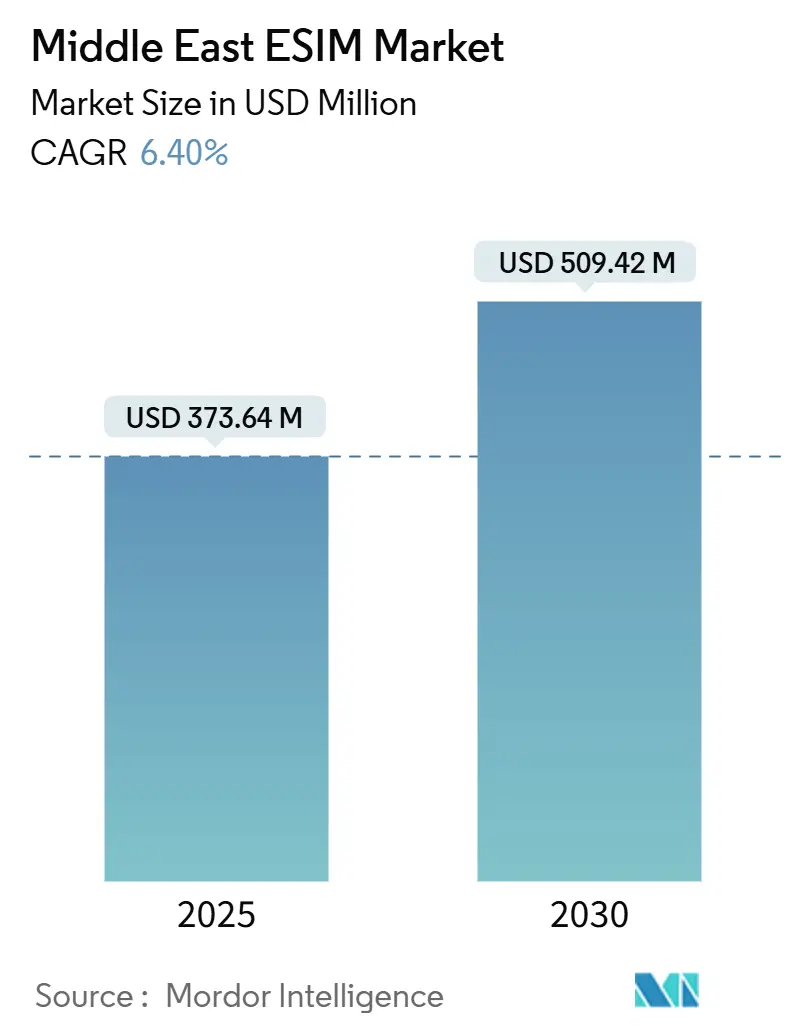

| Market Size (2025) | USD 373.64 Million |

| Market Size (2030) | USD 509.42 Million |

| Growth Rate (2025 - 2030) | 6.40% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East ESIM Market Analysis by Mordor Intelligence

The Middle East ESIM Market size is estimated at USD 373.64 million in 2025, and is expected to reach USD 509.42 million by 2030, at a CAGR of 6.40% during the forecast period (2025-2030).

This healthy growth reflects aggressive 5G rollouts, government digital transformation mandates, and sustained sovereign wealth fund spending on AI and cloud infrastructure. Rapid enterprise IoT adoption in the oil and gas sector, the rise of travel eSIM services for a rebounding tourism industry, and OEM shifts toward native eSIM slots are reinforcing demand for embedded connectivity solutions. Competitive intensity remains moderate; global secure-element vendors partner closely with Gulf telecom operators while regional start-ups attract venture funding for differentiated travel offerings. Near-term headwinds include fragmented carrier support in emerging markets and stringent export-control regimes that complicate semiconductor supply, but a maturing regulatory environment and cross-border roaming agreements continue to unlock new opportunities for the Middle East eSIM market.

Key Report Takeaways

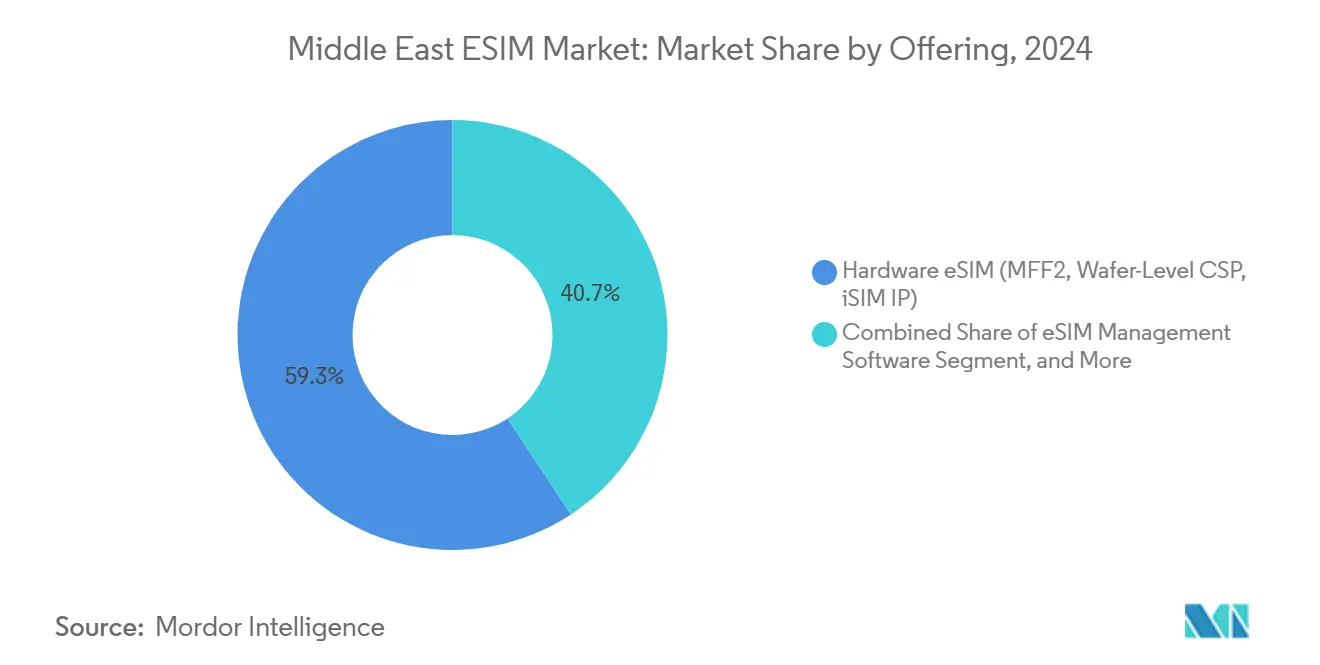

- By offering hardware solutions, it captured 59.29% of the Middle East eSIM market share in 2024; remote SIM-provisioning services are projected to rise at an 11.93% CAGR through 2030.

- By device type, smartphones and feature phones accounted for 69.40% of the Middle East eSIM market size in 2024, while M2M/IoT modules are projected to advance at a 16.62% CAGR through 2030.

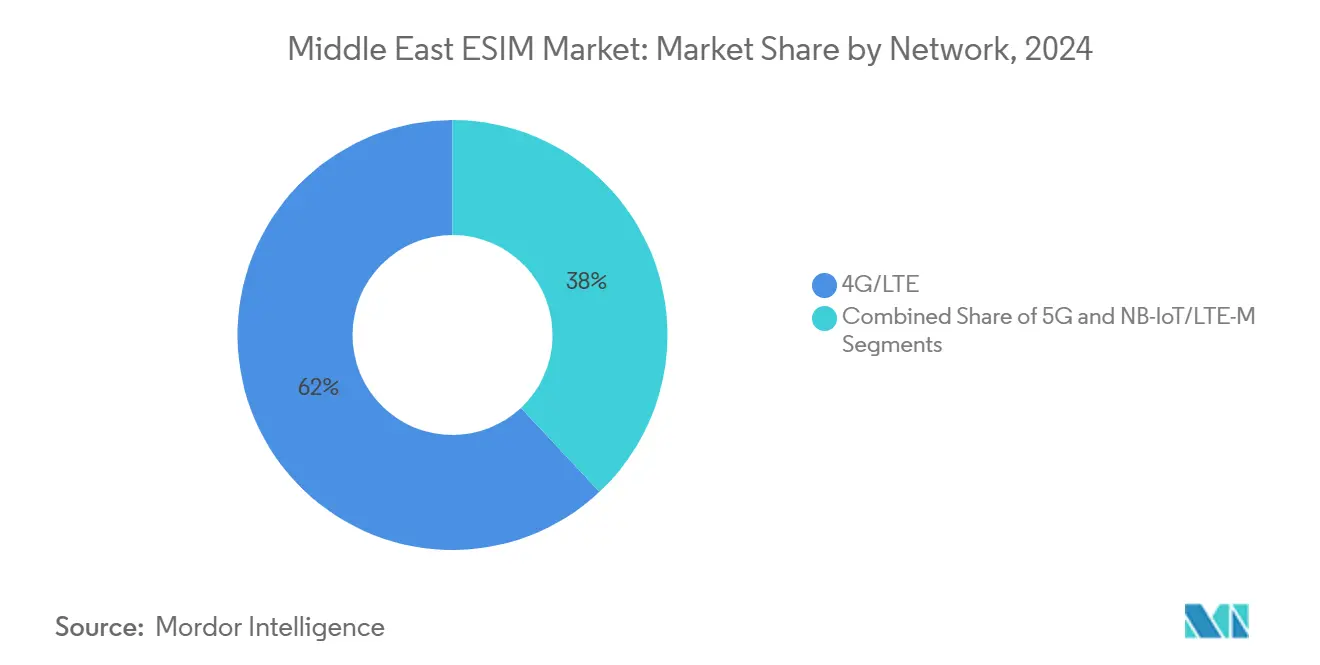

- By network type, 4G/LTE held 61.99% of eSIM connections in 2024; 5G is forecast to expand at a 16.05% CAGR during 2025-2030.

- By end-user industry, consumer electronics led with a 58.78% revenue share in 2024; industrial and manufacturing is expected to post a 22.74% CAGR from 2024 to 2030.

- By country, Saudi Arabia accounted for 28.98% of the Middle East eSIM market share in 2024, whereas Qatar s the fastest projected CAGR at 10.97% through 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Middle East ESIM Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid 5G roll-outs across GCC economies | 1.8% | GCC core markets, spillover to broader Middle East | Medium term (2-4 years) |

| Growing IoT deployments in oil and gas operations | 1.2% | Saudi Arabia, UAE, Qatar, Kuwait | Long term (≥ 4 years) |

| Government digital-transformation mandates (e.g., Vision 2030, UAE Digital Gov.) | 1.5% | Saudi Arabia, UAE, with regional influence | Long term (≥ 4 years) |

| Smartphone OEM shift toward native eSIM slots | 0.9% | Global, with strong adoption in Gulf markets | Short term (≤ 2 years) |

| Mandatory eSIM-only regulations for smart metering (Israel, UAE) | 0.7% | Israel, UAE, expanding to other utilities | Medium term (2-4 years) |

| Tourism-focused short-stay data-plan demand surge | 0.6% | UAE, Saudi Arabia, Qatar, tourism hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerated 5G Infrastructure Investments Drive Enterprise eSIM Adoption

Private and public 5G spending is reshaping industrial connectivity across the Middle East eSIM market. ADNOC’s USD 1.5 billion private 5G network spans 11,000 km² of UAE oil-field operations, enabling remote SIM provisioning for sensors, autonomous vehicles, and inspection drones where physical card swaps are impractical.[1]Mobile Europe Editorial Team, “Industrial 5G drives eSIM demand,” mobileeurope.co.uk Zain Saudi’s USD 340 million 2024 CAPEX lifted 5G population coverage to 66%, underscoring the operator's commitment to eSIM-ready backbone capacity. GSMA-compliant secure-element hardware, paired with cloud-based subscription-management platforms, lets industrial users switch profiles dynamically, minimize site visits, and meet stringent IoT security mandates in environments from offshore rigs to desert pipelines.[2]Source: TelecomLead Bureau, “Zain Saudi invests USD 340 million in 5G,” telecomlead.com

Government Digital-Transformation Mandates Accelerate Public-Sector eSIM Integration

National programs, such as Saudi Arabia’s Vision 2030 and the UAE Digital Government Strategy, oblige agencies to digitize citizen services, triggering the large-scale procurement of eSIM-equipped tablets, handheld devices, and smart meters. UAE Pass now links directly to operator platforms, allowing field inspectors to activate enterprise profiles in seconds, thereby reducing device life-cycle costs and simplifying compliance tracking. Mandatory eSIM smart-metering frameworks in Israel and the UAE lock in long-term demand, while Egypt’s regulator has cleared consumer eSIM launches, signaling broader regional alignment.

Tourism Recovery Fuels Travel eSIM Market Expansion

Gulf tourism rebounded sharply in 2024-2025, and travelers increasingly choose OTA apps such as Airalo to preload multi-country plans. UAE and Saudi subscribers rank among the platform’s top global users, reflecting frequent regional hops between Gulf cities and onward journeys to Europe and Asia. Operators monetize roaming traffic by embedding travel profiles in 5G SIM management hubs, boosting average roaming revenue per user without relying on legacy kiosks.

Smartphone OEM Integration Strategies Reshape Consumer Dynamics

Apple’s eSIM-only iPhone rollout and Samsung’s expanded dual-eSIM support accelerate mainstream adoption in the Middle East eSIM market. Gulf operators partner with OEMs to embed local profiles at the factory, making activation frictionless for premium-segment buyers and introducing digital SIM benefits to lower-tier users. GSMA Intelligence estimates that eSIM-capable devices will account for 68% of regional smartphone connections by 2030, up from 33% in 2025.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Low consumer awareness outside Tier-1 cities | -0.8% | Secondary cities across Middle East | Medium term (2-4 years) |

| Fragmented carrier support in emerging ME markets | -0.6% | Iraq, Syria, Yemen, Jordan | Long term (≥ 4 years) |

| High upfront cost of eSIM orchestration for MVNOs | -0.4% | Regional MVNOs and smaller operators | Medium term (2-4 years) |

| Geopolitical export controls limiting secure-element supply | -0.5% | Region-wide, particularly affecting Chinese suppliers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Consumer Awareness Challenges Limit Adoption Outside Urban Centers

Outside Riyadh, Dubai, and Doha, many subscribers remain unfamiliar with scanning QR codes or downloading operator apps to activate eSIM profiles, hampering uptake in secondary cities. Smaller carriers have fewer resources for consumer education and must still stock physical SIMs to reach cash-paying customers. As eSIM capability becomes standard on mid-range smartphones, operators will need subsidized campaigns and simplified user journeys to bridge the digital divide.

Geopolitical Export Controls Create Secure-Element Vulnerabilities

Expanded U.S. export-control rules now require BIS licenses for advanced chips shipped to or via Bahrain, Egypt, Oman, Qatar, Saudi Arabia, and the UAE, even when Chinese parties are not involved. Secure-element suppliers therefore face longer lead times and higher compliance costs, prompting regional stockpiling strategies and alternative sourcing from foundries outside the U.S. jurisdiction.[3]Clyde & Co Legal Update, “US extends semiconductor export controls to Middle East,” clydeco.comAny disruption could delay device launches and slow the short-term expansion of the Middle East eSIM market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Hardware Dominance Drives Platform Standardization

Hardware secure elements embedded in MFF2 and wafer-level CSP packages held 59.29% of the Middle East eSIM market share in 2024. Remote SIM-provisioning services, however, are projected to grow at a rate of 11.93% as enterprises seek centralized life-cycle management. Regional semiconductor initiatives in the UAE and Saudi Arabia aim to localize chip assembly, reducing supply risk. Over the forecast period, service revenue is expected to outpace one-time hardware sales as operators monetize analytics, subscription management, and compliance reporting.

Hardware adoption surged from 2021 to 2024, as pandemic restrictions highlighted the need for remote device maintenance. From 2025 onward, GSMA SGP.24 v3.2 brings stricter security audits, compelling vendors to bundle certified orchestration software with chips. The resulting ecosystem dynamic positions integrated solution providers—such as Thales, IDEMIA, and G+D—as strategic partners to telecom operators rolling out enterprise IoT programs.

By Device Type: Smartphone Leadership Faces IoT-Module Challenge

Smartphones and feature phones accounted for 69.40% of the Middle East eSIM market in 2024, driven by the launches of Apple’s and Samsung’s flagship models. Yet, M2M/IoT modules are forecast to grow at an annual rate of 16.62%, driven by ADNOC’s sensor deployments and GCC smart-city grids. Tablets and laptops maintain steady corporate demand as governments equip mobile workforces with secure eSIM connectivity aligned to zero-trust security frameworks.

Wearables remain a niche market but are gaining traction among affluent consumers in the UAE and Saudi Arabia, who view independent smartwatch connectivity as a lifestyle upgrade. Over time, industrial IoT volumes are expected to eclipse consumer shipments, further solidifying the Middle East eSIM industry’s shift toward mission-critical applications.

By Network Type: 4G Dominance Transitions to 5G Leadership

4G/LTE accounted for 61.99% of connections in 2024, reflecting the region’s mature LTE footprint. Ongoing 5G investment pushes 5G connections to a 16.05% CAGR, unlocking low-latency use cases from smart grids to autonomous mining trucks. NB-IoT and LTE-M remain strategic niche technologies for low-power sensors operating in harsh desert conditions where battery replacement is difficult.

Enterprise 5G private networks aboard offshore rigs or industrial estates will rely on eSIM for secure profile swaps between private slices and public macro coverage, maintaining service continuity. Network orchestration APIs will let operators upsell SLA-based connectivity bundles to multinational energy companies.

By End-user Industry: Consumer Electronics Lead Industrial Transformation

Consumer electronics captured 58.78% of revenue in 2024. The fastest growth, however, lies in industrial and manufacturing, which is expected to see a 22.74% CAGR as oil-and-gas majors retrofit thousands of assets with eSIM-equipped monitoring devices. Utilities growth accelerates following smart-metering mandates in the UAE and Israel, while automotive gains momentum from connected-car pilots supported by 5G MEC sites in Riyadh and Dubai.

Healthcare adoption starts from a small base but benefits from tele-ICU roll-outs and remote patient monitoring, which require tamper-proof connectivity and end-to-end encryption—capabilities inherent in GSMA-certified eSIM solutions.

Geography Analysis

GCC economies commanded roughly 75% of the total 2024 value, reflecting oil-funded infrastructure budgets and unified regulatory direction. Saudi Arabia’s 28.98% slice came from industrial IoT megaprojects, such as NEOM and the Red Sea developments, which depend on ubiquitous, tamper-resistant connectivity. UAE followed, supported by e& Group’s 5G densification and smart-city projects in Dubai and Abu Dhabi. Qatar’s double-digit growth relies on digital twin initiatives and sustainable city policies that necessitate massive sensor networks.

Outside the Gulf, Israel’s utilities mandate and thriving developer ecosystem make it a test bed for advanced subscription-management platforms serving the wider Middle East eSIM market. Turkey straddles European and Middle-Eastern corridors, positioning its operators to launch cross-border eSIM offers once inflation stabilizes. The remaining Levant and Mesopotamian markets face carrier fragmentation, but as regulatory templates converge, latent demand in segments such as logistics and agriculture will emerge.

Cross-border cooperation—including GCC digital-identity agreements—simplifies roaming profile downloads, a boon for travel eSIM providers whose user bases already rank Dubai, Riyadh, and Doha among their top origin cities. Export-control uncertainties and secure-element lead times remain watchpoints, yet sovereign-wealth-fund capital earmarked for AI fabrics and edge-cloud zones underpins the long-term growth story.

Competitive Landscape

The Middle East eSIM market is moderately concentrated. Hardware titans Thales, IDEMIA, and G+D pair Common-Criteria-certified chips with subscription-management platforms to win multi-year master agreements at STC, e&, and Ooredoo. Semiconductor vendors such as STMicroelectronics and NXP provide secure elements, while Qualcomm and MediaTek embed iSIM capabilities into cellular modems.

Regional carriers differentiate via enterprise suites: e& Group invested AED 1.787 billion in Q2 2024 to densify indoor 5G and broaden API exposure for eSIM provisioning; STC’s DARE strategy pairs edge compute with eSIM to support oil-and-gas telemetry; Ooredoo’s IoT Connect hub integrates profile management and analytics. Venture capital funds inject liquidity into niche markets: Turkey-based Roamless raised USD 5 million from UAE investor Shorooq Partners, exemplifying the appetite for travel-focused propositions.

Barriers to entry increase with GSMA SGP.24 v3.2 compliance, common criteria audits, and sovereign cybersecurity directives. Vendors offering hardware, orchestration software, and managed services in a single stack hold the advantage as operators shift from capex-heavy SIM card logistics to cloud-native digital distribution.

Middle East ESIM Industry Leaders

Thales Group

IDEMIA Group

Samsung Electronics Co., Ltd.

Saudi Telecom Company

Ooredoo Q.P.S.C.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: GSMA issued SGP.24 RSP Compliance Process v3.2, tightening security and functional audit rules for all eSIM elements.

- November 2024: Zain Group disclosed USD 340 million 9M 2024 CAPEX, raising 5G coverage in Saudi Arabia to 66%.

- August 2024: e& Group achieved record 5G speeds and invested AED 1.787 billion in Q2 2024 network modernization.

- August 2024: Egypt’s NTRA confirmed nationwide consumer eSIM launch within one month.

Middle East ESIM Market Report Scope

| Hardware eSIM (MFF2, Wafer-Level CSP, iSIM IP) |

| eSIM Management Software |

| Remote SIM Provisioning Services |

| Smartphones and Feature Phones |

| Tablets and Laptops |

| Wearables |

| M2M/IoT Modules |

| 5G |

| 4G/LTE |

| NB-IoT/LTE-M |

| Consumer Electronics |

| Automotive and Transportation |

| Industrial and Manufacturing |

| Logistics and Asset Tracking |

| Energy and Utilities |

| Healthcare and Wearables |

| Saudi Arabia |

| United Arab Emirates |

| Israel |

| Turkey |

| Qatar |

| Kuwait |

| Oman |

| Bahrain |

| Rest of Middle East (Syria, Yemen, Jordan, Iraq, Iran, others) |

| By Offering | Hardware eSIM (MFF2, Wafer-Level CSP, iSIM IP) |

| eSIM Management Software | |

| Remote SIM Provisioning Services | |

| By Device Type | Smartphones and Feature Phones |

| Tablets and Laptops | |

| Wearables | |

| M2M/IoT Modules | |

| By Network Type | 5G |

| 4G/LTE | |

| NB-IoT/LTE-M | |

| By End-user Industry | Consumer Electronics |

| Automotive and Transportation | |

| Industrial and Manufacturing | |

| Logistics and Asset Tracking | |

| Energy and Utilities | |

| Healthcare and Wearables | |

| By Country | Saudi Arabia |

| United Arab Emirates | |

| Israel | |

| Turkey | |

| Qatar | |

| Kuwait | |

| Oman | |

| Bahrain | |

| Rest of Middle East (Syria, Yemen, Jordan, Iraq, Iran, others) |

Key Questions Answered in the Report

What is the projected value of the Middle East eSIM market by 2030?

The market is expected to reach USD 509.42 million by 2030.

Which country currently holds the largest share of regional eSIM revenue?

Saudi Arabia accounted for 28.98% of 2024 sales, the highest in the region.

Which segment is growing fastest within the Middle East eSIM ecosystem?

M2M/IoT modules show the strongest advance, at a 16.62% CAGR to 2030.

How will 5G affect eSIM adoption in the Gulf?

Extensive 5G roll-outs raise bandwidth and coverage, enabling advanced industrial and travel use cases that rely on remote profile provisioning.

What regulatory development should vendors watch in 2025?

GSMA’s SGP.24 v3.2 raises security-evaluation thresholds, making compliance essential for chip and platform providers.

What supply-chain risk could slow the deployment of eSIM hardware?

Stricter U.S. export controls on secure elements may lengthen lead times and raise costs for regional device manufacturers.

Page last updated on: