Middle East And Africa Pumps Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2020 - 2023 |

| Market Size (2025) | USD 3.12 Billion |

| Market Size (2030) | USD 3.67 Billion |

| Growth Rate (2025 - 2030) | 3.84% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East And Africa Pumps Market Analysis by Mordor Intelligence

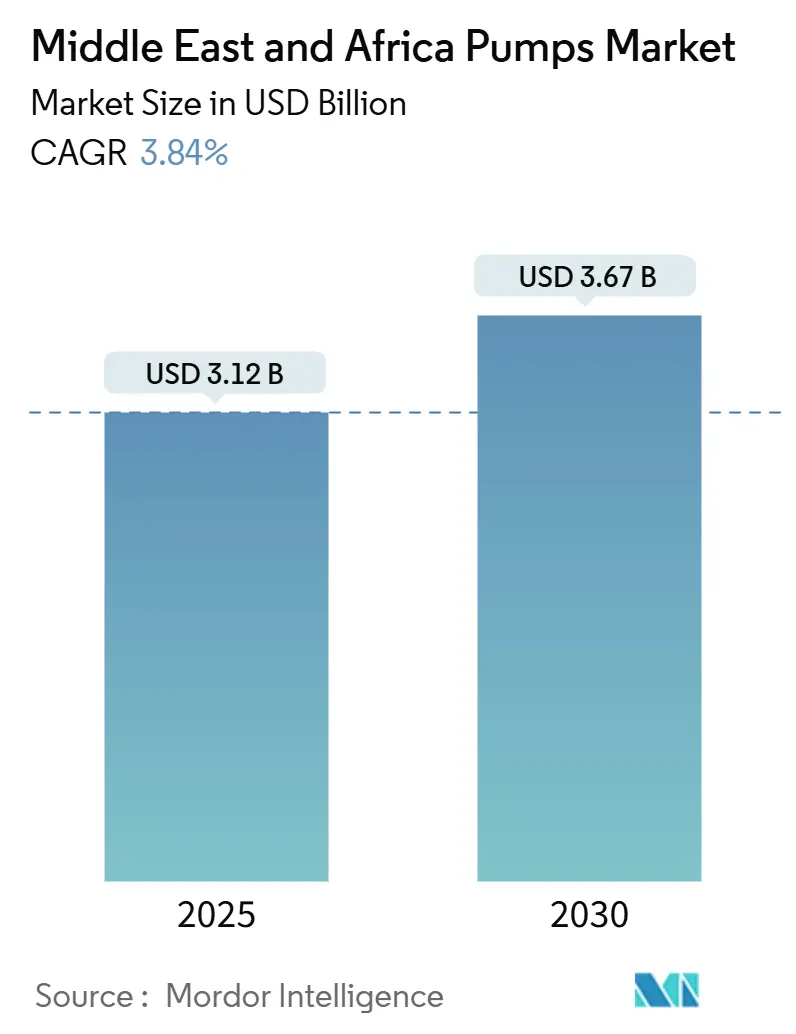

The Middle East And Africa Pumps Market size is estimated at USD 3.12 billion in 2025, and is expected to reach USD 3.67 billion by 2030, at a CAGR of 3.84% during the forecast period (2025-2030).

Sustained investment in desalination, wastewater reuse, and brownfield oil-recovery programs underpins steady equipment demand, while humanitarian agencies accelerate off-grid solar installations across rural sub-Saharan Africa. Centrifugal units dominate high-flow water duties; progressive-cavity and diaphragm designs occupy niche oil-and-gas and chemical-dosing roles. Variable-frequency-drive retrofits, IE3 motor standards, and predictive-maintenance platforms are enlarging aftermarket revenue streams, although copper and steel price swings squeeze supplier margins. Competitive rivalry remains moderate as five multinational incumbents defend territory through localized assembly, long-term service agreements, and product-authentication tools that deter counterfeit imports.

Key Report Takeaways

- By pump type, centrifugal designs held 56.2% of the Middle East and Africa pumps market share in 2024; positive-displacement pumps will record the highest 4.6% CAGR to 2030.

- By drive technology, electric-motor units commanded 63.7% share of the Middle East and Africa pumps market size in 2024, whereas solar- and renewable-powered models are projected to grow at a 10.9% CAGR through 2030.

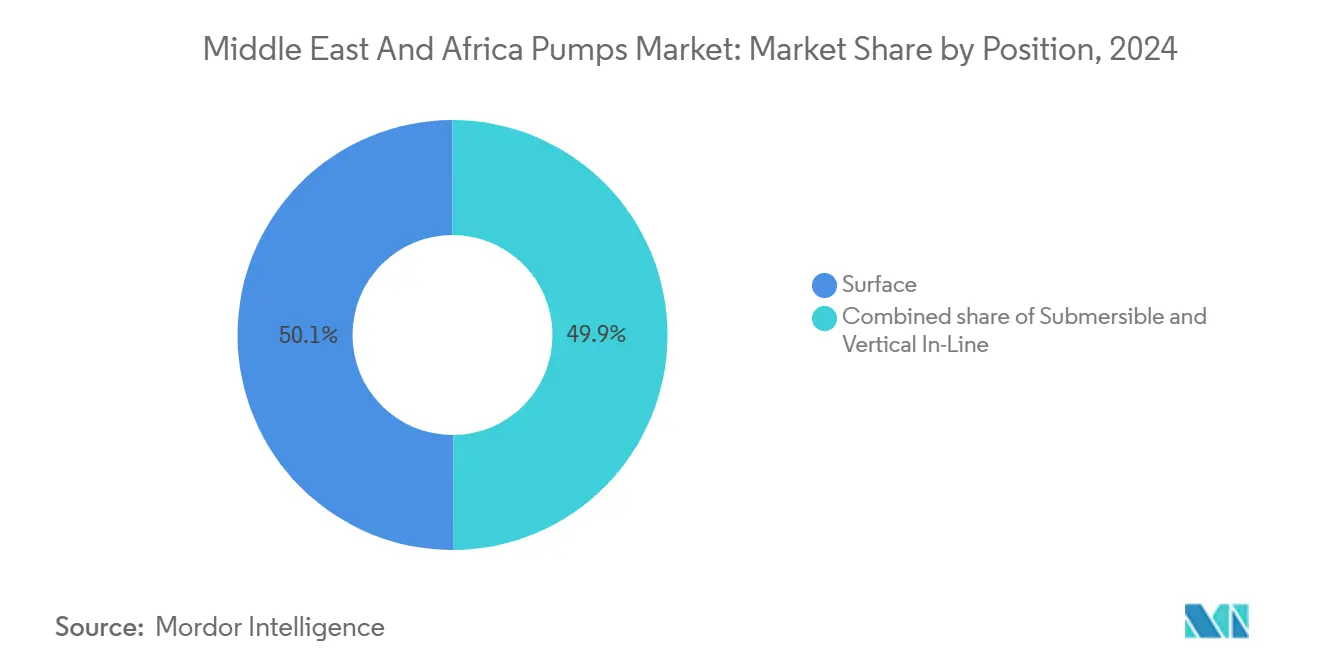

- By position, surface pumps accounted for 50.1% of 2024 revenue; submersible units are set to advance at a 6.5% CAGR between 2025-2030.

- By application, water and wastewater treatment generated 39.3% of the Middle East and Africa pumps market size in 2024 and is forecast to expand at a 4.4% CAGR to 2030.

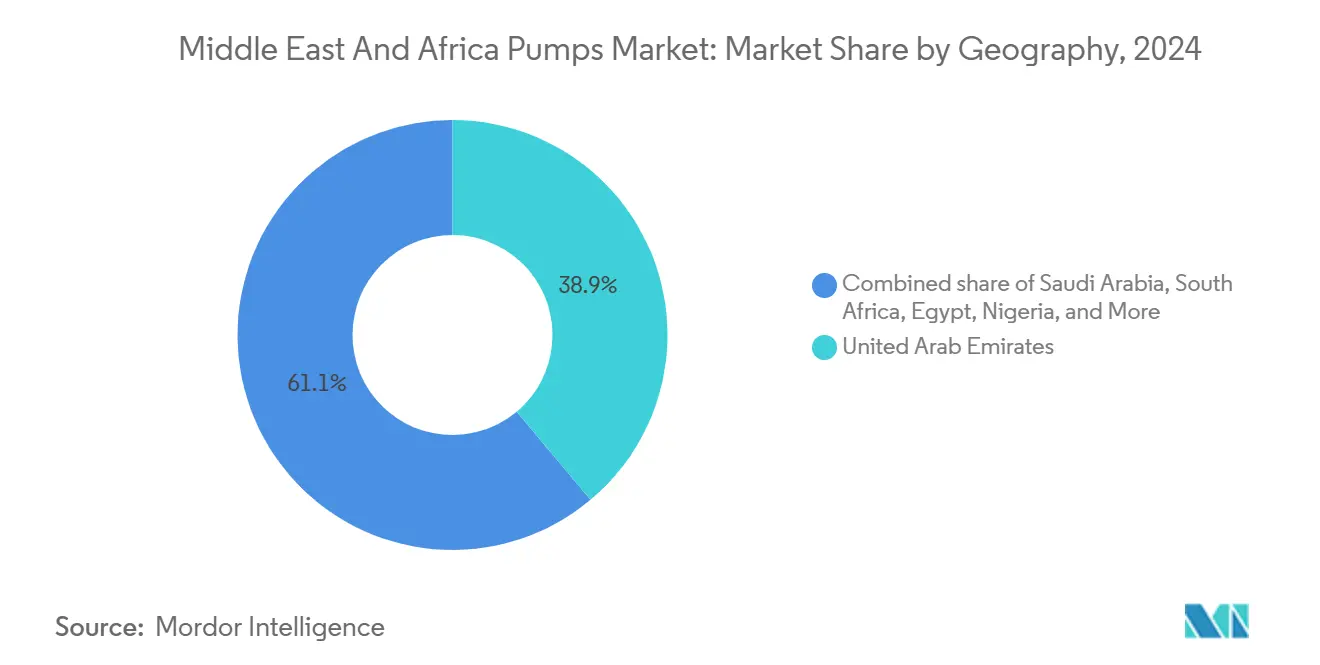

- By geography, the United Arab Emirates led with 38.9% revenue share in 2024 and is expected to post the fastest 4.6% CAGR up to 2030.

Middle East And Africa Pumps Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Large-scale desalination & wastewater CAPEX ramp-up | +1.2% | GCC core (UAE, Saudi Arabia, Qatar), spillover to Oman and Bahrain | Medium term (2-4 years) |

| Energy-efficiency retrofits mandated by GCC utilities | +0.7% | UAE, Saudi Arabia, Qatar | Short term (≤ 2 years) |

| Oil-and-gas brownfield life-extension projects | +0.8% | Saudi Arabia, UAE, Kuwait, Nigeria | Medium term (2-4 years) |

| Mining & battery-metal projects in Southern Africa | +0.6% | South Africa, Namibia | Long term (≥ 4 years) |

| AI-enabled predictive-maintenance adoption | +0.4% | UAE, Saudi Arabia, South Africa | Long term (≥ 4 years) |

| Humanitarian off-grid solar-pump initiatives | +0.3% | Sub-Saharan Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Large-scale Desalination & Wastewater CAPEX Ramp-up

Gulf states continue to double reverse-osmosis capacity to hedge against aquifer depletion and rising water stress. Qatar’s Facility E contract awards of USD 2.8 billion in 2024 specify multistage centrifugal pumps able to withstand brine chloride levels yet maintain energy consumption below 3 kWh per cubic meter. Saudi Arabia’s National Water Company has a USD 27.4 billion pipeline that will add 11 million m³/day of wastewater treatment capacity by 2030, anchoring demand for submersible sewage and vertical turbine pumps. The UAE’s Taweelah B2 project, sanctioned in 2024, will integrate 200 MGD of desalinated output by 2027, relying on corrosion-resistant duplex-steel centrifugal units.[1]Editorial Team, “Taweelah B2 Project Brief,” ewec.ae This spree secures longer-term orders for chemical-dosing diaphragm pumps, high-head intake turbines, and vertical in-line distribution pumps. Regional EPC frameworks increasingly mandate ISO 24516 asset-management compliance, which boosts demand for factory-acceptance testing and performance-validation services.

Energy-efficiency Retrofits Mandated by GCC Utilities

Dubai’s Demand Side Management Strategy aims for a 30% cut in power and water use by 2030, triggering replacement of legacy fixed-speed pumps with variable-frequency-drive models that trim energy draw by 20-35%.[2]Correspondent, “Gulf Utilities Push Efficiency Upgrades,” dsce.gov.ae UAE Cabinet Resolution 23-2023 enforces IE3 motor efficiency from 2025, effectively banning sub-IE2 imports.[3]Press Office, “IE3 Motor Standards Enforced,” moenr.gov.ae Saudi Arabia’s Vision 2030 Energy Efficiency Program has allocated USD 1.8 billion for industrial upgrades, covering pump-system optimization at petrochemical complexes and power plants.[4]Reporter, “Saudi Energy Upgrade Program,” seec.gov.sa Coupled with building-code updates, these mandates favor compact vertical in-line pumps with embedded sensors. The regulations also underpin a secondary consulting market for ISO 50001 audits and life-cycle cost analyses.

Oil- &-Gas Brown-field Life-extension Projects

Saudi Aramco’s 2024-2025 capex prioritizes enhanced recovery across Khurais and Ghawar fields, necessitating high-pressure multistage and progressive-cavity pumps for water and polymer injection. ADNOC’s Bab and Bu Hasa brownfield campaigns, including USD 1.2 billion in wellhead compression contracts, rely on centrifugal and reciprocating units tolerant of high-sand cuts. Nigerian operators retrofit electric submersible pumps to stem output decline but grapple with grid instability and cable theft. Equipment suppliers thus promote armored down-hole motors and low-harmonic VFDs to stabilize performance. Mature field service agreements increasingly bundle cloud-based monitoring to offset technician shortfalls in remote basins.

Mining & Battery-metal Projects in Southern Africa

Lithium and cobalt ventures in South Africa’s Northern Cape and Limpopo provinces attracted USD 800 million of investment during 2024, each requiring dewatering pumps rated for 500 m³/h at heads above 200 m. Namibia’s Uis tin-lithium development secured USD 150 million for a new plant consuming 12 MW of pumping and flotation power. High-chrome horizontal centrifugal pumps with replaceable liners handle slurry solids exceeding 50% by weight. Water scarcity drives adoption of closed-loop tailing systems, pushing up demand for high-head recirculation pumps. Compliance with South Africa’s Mine Health and Safety Act necessitates quarterly vibration audits, cementing aftermarket prospects.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile steel & copper price swings | -0.5% | Global, acute in import-dependent MEA markets | Short term (≤ 2 years) |

| Skilled-technician shortage in remote basins | -0.3% | Nigeria, South Africa, Saudi Arabia Empty Quarter | Medium term (2-4 years) |

| Ramp-up of counterfeit low-spec imports | -0.4% | Nigeria, Egypt, Kenya | Short term (≤ 2 years) |

| Grid-instability curbing smart-pump deployment | -0.3% | Nigeria, Egypt, South Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Steel & Copper Price Swings

Copper windings comprise up to 20% of an electric motor's bill of materials, while stainless-steel casings account for 25-30% of the corrosion-resistant pump cost. London Metal Exchange copper averaged USD 9,200 per t in 2024, 12% above 2023, driven by Chilean supply disruptions and renewables demand. Middle-East hot-rolled coil prices hit USD 620 per t, up 8% year-on-year, lifting casing and impeller costs. Mid-tier suppliers lacking hedging programs must choose between price hikes and margin erosion, risking share loss to Asian vendors. Volatility also complicates five-year service contract pricing, encouraging shorter bidding cycles and index-linked clauses.

Skilled-technician Shortage in Remote Basins

The International Association of Drilling Contractors logged a 22% vacancy rate for mechanical technicians on Middle-East upstream projects in 2024. Security risks in Nigeria’s Niger Delta and South Africa’s deep-shaft mines deter field personnel, prolonging shutdowns. Some operators now stock redundant spare pumps on-site, inflating working capital. AI-driven diagnostics lower the need for frequent visits, yet IoT retrofits cost USD 5,000-15,000 per pump, limiting uptake at small facilities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Pump Type: Centrifugal Units Accelerate on Desalination Scale

Centrifugal pumps generated 56.2% of the Middle East and Africa pumps market revenue in 2024 and will grow at a 4.6% CAGR through 2030. Qatar’s Facility E intake system specifies vertical turbine units rated 50,000 m³/h at 30 m head, a duty point where positive-displacement designs become uneconomic. Saudi wastewater schemes favor end-suction and split-case centrifugal units, flowing 200-2,000 m³/h for collection networks. The Middle East and Africa pumps market size for centrifugal equipment will therefore outstrip overall growth as GCC utilities pivot from energy-intensive multi-stage flash plants to reverse-osmosis configurations that demand 60-80 bar feed pressure.

Positive-displacement alternatives serve viscosity-critical niches. Progressive-cavity pumps keep polymer chains intact in Aramco’s enhanced-oil-recovery lines. Diaphragm metering pumps deliver antiscalants with ±1% accuracy in pretreatment skids, while gear pumps retain roles in fuel transfer. Despite higher acquisition costs and specialized spare-parts inventories, these units retain their foothold where shear-sensitive fluids or self-priming are essential. Suppliers mitigate cost barriers by offering modular cartridge kits that cut overhaul time by 40%.

By Drive Technology: Solar Surge Reshapes Off-Grid Economics

Electric motors accounted for 63.7% of 2024 shipments. IE3 standards and ubiquitous 380-415 V grids in GCC industrial zones cement their dominance. Variable-frequency drives shave 20-35% of energy use in variable-demand loops, aligning with UAE demand-side targets. Yet solar-powered pumps will post the segment’s fastest 10.9% CAGR through 2030. IRENA counted 28% growth in East-African deployments during 2024 as module prices slid below USD 0.20 W.

A typical solar set couples a 4 kW array with a brushless DC submersible delivering 30 m³/day. The Middle East and Africa pumps market embraces these units where grid extension costs exceed USD 15,000 km. Development-finance subsidies, carbon-credit earnings, and falling lithium-iron-phosphate battery prices shorten payback to under four years. Diesel and gas engines linger in remote oil fields but face tightening emissions rules. Magnetically-coupled sealless pumps, though a small fraction, gain share in petrochemicals where zero leakage is mandated, backed by ITT’s 2024 launch rated 250 °C and 40 bar.

By Position: Surface Dominance Meets Submersible Acceleration

Surface configurations captured 50.1% of 2024 revenue, driven by horizontal split-case and end-suction models in power-plant cooling loops and refinery process circuits. Above-ground installation simplifies inspection, and acquisition cost is 20-30% below submersible equivalents. Aramco refineries run split-case units rated 10,000 m³/h nonstop, scheduling quarterly bearing inspections with in-house crews.

Submersible pumps will clock a 6.5% CAGR through 2030, fastest in this category. Saudi collection networks demand solids-handling capacities up to 80 mm and corrosion-proof alloys. South African lithium mines locate submersibles 200 m below grade, relying on high-chrome impellers to withstand 50% solids by weight. Variable-frequency starts minimize water-hammer and extend seal life. Vertical in-line pumps fix directly onto pipework and are gaining share in cramped mechanical rooms, cutting installation footprint by half and trimming steel-baseplate cost.

By Application: Water & Wastewater Leadership Anchored by GCC Megaprojects

Water and wastewater plants generated 39.3% of 2024 revenue and will expand at a 4.4% CAGR to 2030, lifted by more than USD 35 billion of committed GCC capital outlays. Each plant requires thousands of seawater intake, brine-discharge, and recirculation pumps. ISO 24516 asset-management rules enforce rigorous efficiency testing that sustains aftermarket parts demand.

Oil-and-gas facilities form the second pillar, using multistage pumps for water injection and progressive-cavity models for polymer flooding in Saudi and Emirati fields. Mining dispositions in South Africa and Namibia require high-head dewatering and abrasion-resistant slurry transport, while HVAC and building services benefit from GCC energy-efficiency credits that reward VFD retrofits. Food processing, power generation, and pharmaceuticals together make up a smaller but steady slice, guided by hygiene and emission directives.

Geography Analysis

The United Arab Emirates delivered 38.9% of 2024 revenue and is expected to post a 4.6% CAGR through 2030. Dubai Electricity and Water Authority’s roadmap seeks 30% energy and water savings by 2030, catalyzing pump retrofits across commercial towers.[5]Correspondent, “Dubai Demand Side Management Strategy,” dsce.gov.ae Abu Dhabi’s brownfield recovery at mature on-shore wells orders new polymer-injection and water-injection trains. The Taweelah B2 project will commission 200 MGD of desalination by 2027, drawing hundreds of duplex-steel intake pumps.

Saudi Arabia ranks second, its pipeline shaped by Vision 2030 water-security goals and Aramco’s enhanced-oil-recovery spending. The National Water Company’s USD 27.4 billion program adds 11 million m³/day of wastewater treatment and thousands of submersible units. The Khurais expansion targets 300 k bbl/d incremental crude by 2027 using progressive-cavity polymer pumps.

South Africa offers a distinct growth vector led by battery-metal mining in the Northern Cape and Limpopo. Atlantic Lithium’s Ewoyaa project needs dewatering flows of 500 m³/h. Rolling load-shedding drives hybrid solar-diesel pump trials in off-grid shafts. Egypt’s industrial corridor and Nile mitigation efforts spur intake and booster orders, yet grid instability delays smart-pump uptake. Nigeria’s brownfield on-shore producers retrofit diesel and solar drives as cable theft undermines electric options. Smaller markets, including Oman, Bahrain, Kenya, and Namibia, add incremental volume through municipal boreholes, mining, and humanitarian irrigation projects, collectively expanding the addressable Middle East and Africa pumps market.

Competitive Landscape

The top five suppliers, Flowserve, Sulzer, Grundfos, KSB, and Xylem, account for roughly 45-50% of regional shipments, giving the Middle East and Africa pumps market a moderate concentration score. Each maintains localized assembly: Flowserve in Dammam, Grundfos in Dubai, Sulzer in Abu Dhabi, KSB in Johannesburg, and Xylem in Jebel Ali. Grundfos embedded QR-code authentication in 2024, letting users verify origin by smartphone and countering counterfeit pumps in Nigeria and Egypt. Flowserve’s USD 25 million Dammam remanufacturing JV trims overhaul lead times from 12 weeks to 4 weeks and lowers carbon output from new builds.

Technology differentiation pivots on predictive-maintenance ecosystems. Xylem’s Flygt Concertor line uses edge analytics to forecast bearing failure up to two months in advance, cutting unscheduled wastewater downtime by 40% in pilot UAE sites. Sulzer fitted 350 ADNOC pumps with vibration sensors during 2024 retrofits, targeting similar uptime gains. Regional challengers such as Kirloskar Brothers and Ruhrpumpen win slots by offering modular quick-repair cartridges that slash field time by 60%. Copper and steel surcharges forced multinationals to add price-index clauses to 2024 contracts, while Gulf Standardization Organization efficiency labels disadvantage offshore entrants without in-region test rigs.

Middle East And Africa Pumps Industry Leaders

Flowserve

Sulzer

Grundfos

KSB

Xylem

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Wilo SE completed the doubling of its Dubai manufacturing facility capacity, positioning the company to serve growing regional demand while establishing an export hub for Middle East and Africa markets.

- December 2024: ACWA Power secured a USD 693 million contract for the Hamriyah Independent Water Project in Sharjah, featuring 410,000 m³ per day desalination capacity that will require hundreds of specialized pumps.

- September 2024: Alkhorayef Water and Power Technologies won a USD 59 million contract for Dammam sewage treatment plant expansion, raising capacity to 125,000 m³ per day and necessitating comprehensive pump system upgrades.

- September 2024: Taqa Water Solutions allocated USD 2.7 billion for 80 water infrastructure projects across Abu Dhabi, driving future pump demand.

Middle East And Africa Pumps Market Report Scope

Pumps, mechanical devices, convert energy to elevate, transport, or compress fluids, be it liquids or gases. By transforming mechanical energy into hydraulic or pneumatic energy, pumps generate a pressure difference, propelling fluids from lower to higher pressure zones.

The Middle East and Africa pumps market is segmented by pump type, drive technology, position, application, and geography. By pump type, the market is segmented into centrifugal and positive-displacement. By drive technology, the market is segmented into electric motor, diesel/gas engine, solar/renewable, and magnetically-driven/sealless. By position, the market is segmented into surface, submersible, and vertical in-line. By application, the market is segmented into water and wastewater, chemical and petrochemical, HVAC and building services, oil and gas, food and beverage, mining and metals, power generation, pharmaceuticals and biotech, and others. The report also covers the market sizes and forecasts for the Middle East and Africa pumps market across major countries. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Centrifugal |

| Positive-Displacement |

| Electric Motor |

| Diesel/Gas Engine |

| Solar/Renewable |

| Magnetically-Driven/Sealless |

| Surface |

| Submersible |

| Vertical In-Line |

| Water and Wastewater |

| Chemical and Petrochemical |

| HVAC and Building Services |

| Oil and Gas (Upstream, Midstream, Downstream) |

| Food and Beverage |

| Mining and Metals |

| Power Generation (Thermal, Nuclear, Renewables) |

| Pharmaceuticals and Biotech |

| Others |

| Saudi Arabia |

| United Arab Emirates |

| South Africa |

| Egypt |

| Nigeria |

| Qatar |

| Rest of Middle East and Africa |

| By Pump Type | Centrifugal |

| Positive-Displacement | |

| By Drive Technology | Electric Motor |

| Diesel/Gas Engine | |

| Solar/Renewable | |

| Magnetically-Driven/Sealless | |

| By Position | Surface |

| Submersible | |

| Vertical In-Line | |

| By Application | Water and Wastewater |

| Chemical and Petrochemical | |

| HVAC and Building Services | |

| Oil and Gas (Upstream, Midstream, Downstream) | |

| Food and Beverage | |

| Mining and Metals | |

| Power Generation (Thermal, Nuclear, Renewables) | |

| Pharmaceuticals and Biotech | |

| Others | |

| By Geography | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Nigeria | |

| Qatar | |

| Rest of Middle East and Africa |

Key Questions Answered in the Report

How large is the Middle East and Africa pumps space today and what is its growth outlook?

Revenue reached USD 3.04 billion in 2024 and is projected to grow to USD 3.67 billion by 2030 at a 3.84% CAGR.

Which pump category contributes the most sales across the region?

Centrifugal equipment leads with 56.2% of 2024 revenue because it dominates desalination, municipal water and cooling services.

What is driving rapid adoption of solar-powered pumping systems?

Module prices below USD 0.20 W and off-grid water needs make photovoltaic pump sets more economical than diesel options, underpinning a 10.9% CAGR.

Why are energy-efficiency mandates important for replacement demand?

IE3 motor rules and demand-side programs in the UAE and Saudi Arabia push building owners to retrofit variable-frequency-drive pumps that cut energy use by up to 35%.

How do copper and steel price swings influence supplier profitability?

Copper at USD 9,200 t and higher coil steel costs raise winding and casing expenses, forcing OEMs to decide between passing surcharges on or accepting margin compression.

Which firms hold the strongest regional position?

Flowserve, Sulzer, Grundfos, KSB and Xylem maintain roughly half of shipments by combining local assembly with long-term service agreements.

Page last updated on: