Middle East And Africa Ice Cream Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2020 - 2023 |

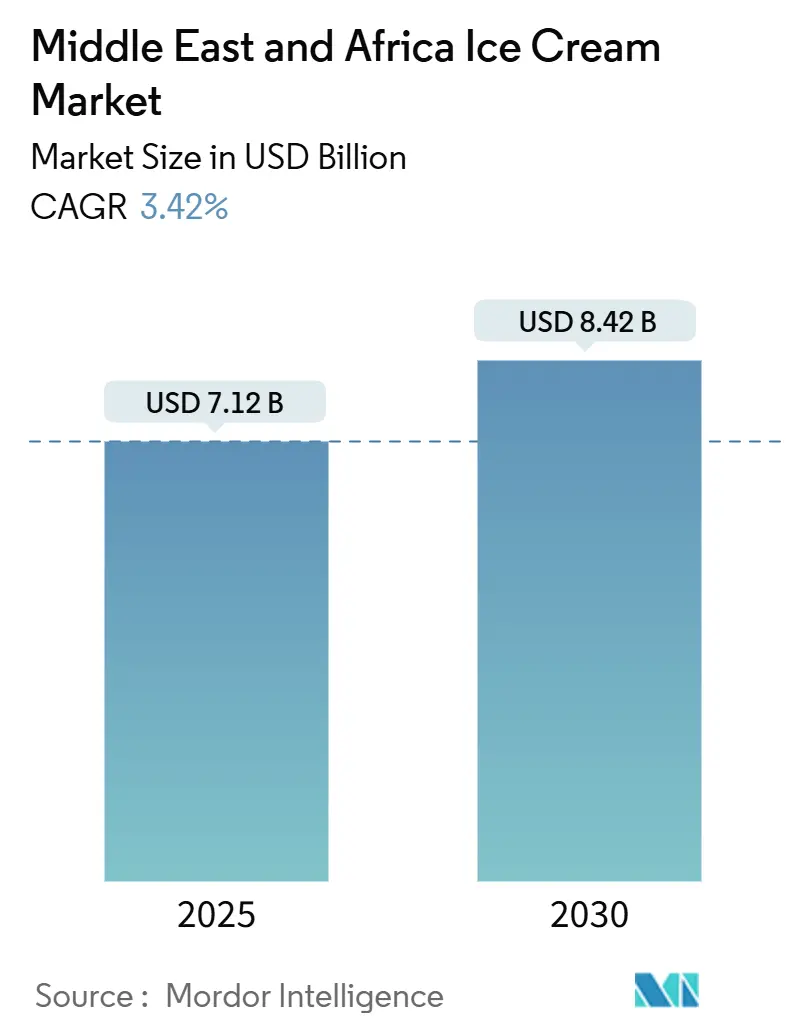

| Market Size (2025) | USD 7.12 Billion |

| Market Size (2030) | USD 8.42 Billion |

| Growth Rate (2025 - 2030) | 3.42% CAGR |

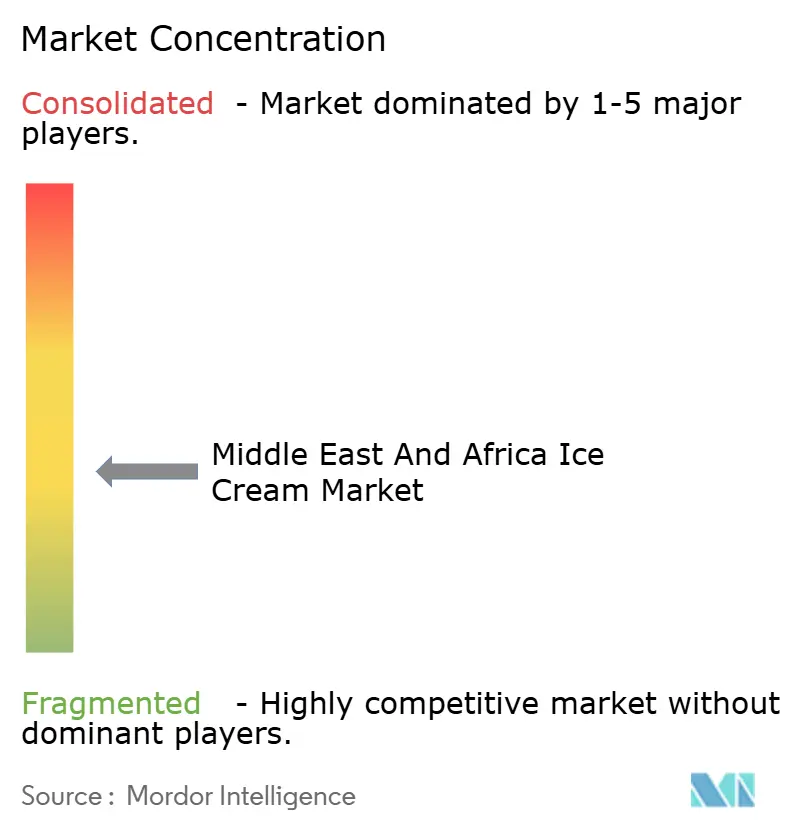

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Middle East And Africa Ice Cream Market Analysis by Mordor Intelligence

The Middle East and Africa ice-cream market size reached USD 7.12 billion in 2025 and is projected to climb to USD 8.42 billion by 2030, reflecting a 3.42% CAGR. This growth is driven by the expansion of cold-chain infrastructure, a shift towards premiumization, and rising urban disposable incomes. However, the market faces challenges from fluctuating energy prices and regulatory complexities across multiple countries. Increasing lactose intolerance and the adoption of vegan lifestyles have boosted demand for plant-based and dairy-free ice cream options. Additionally, the launch of low-fat, keto-friendly, and sugar-free variants has attracted health-conscious consumers. The use of local ingredients, such as coconut, date-palm, and hibiscus, along with the development of unique blended flavors, has expanded the market's appeal and spurred new product launches. Moreover, the growing tourism and hospitality industries in cities like Dubai and Riyadh have driven ice cream consumption in restaurants, hotels, and leisure venues. Saudi Arabia continues to be the primary revenue contributor, while Nigeria is experiencing significant growth momentum. Premium craft formats are also transforming consumer expectations. While large retailers maintain their dominance in terms of volume, the rapid growth of online channels is reshaping last-mile delivery economics. Furthermore, strategic initiatives by global and regional players, combined with halal standardization and blockchain traceability, are expected to intensify competition.

Key Report Takeaways

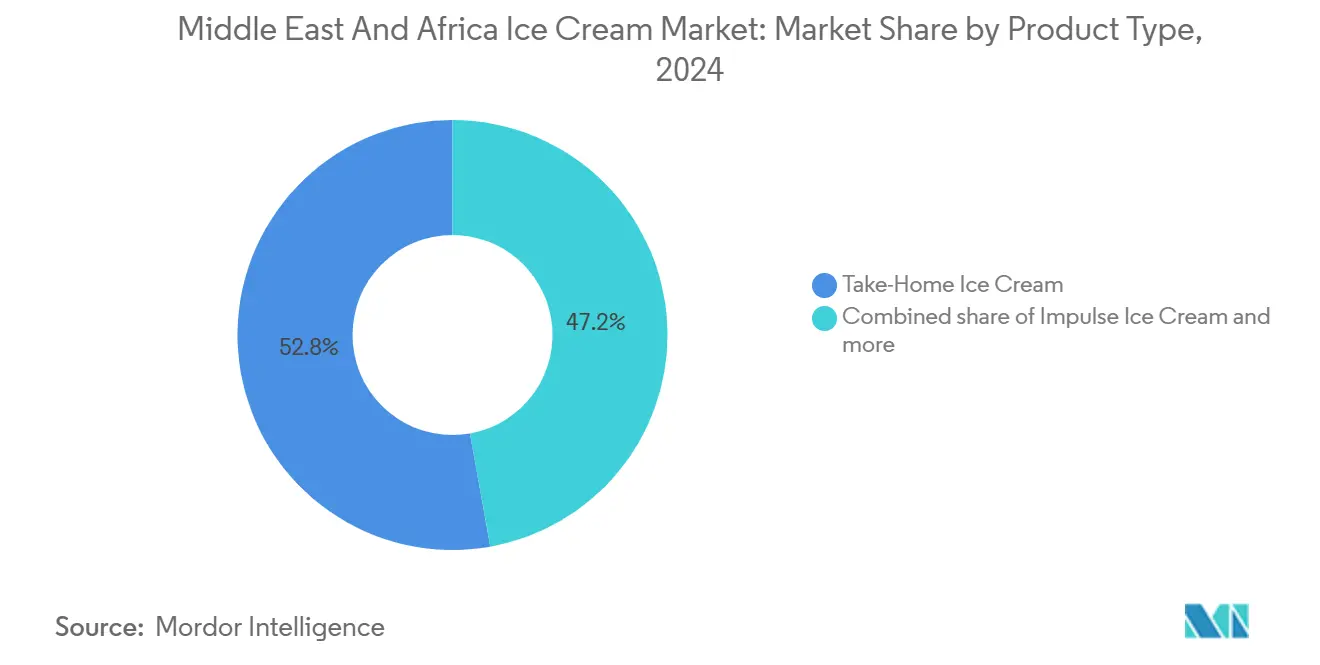

- By product type, take-home ice cream led with 52.84% revenue share in 2024; artisanal is forecast to expand at a 6.36% CAGR through 2030.

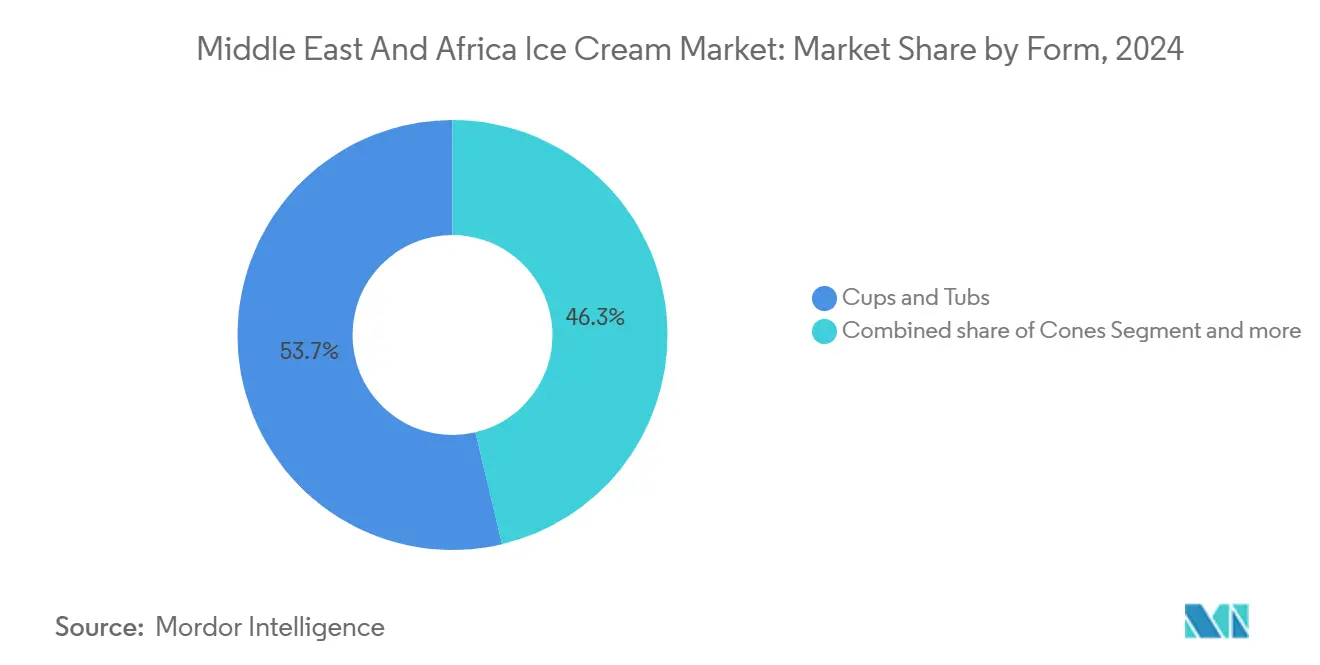

- By form, cups and tubs held 46.28% share of the Middle East and Africa ice-cream market size in 2024; bars and sticks record the highest projected CAGR at 6.23% through 2030.

- By flavor, chocolate commanded 35.57% of the Middle East and Africa ice-cream market share in 2024, yet fruit flavors are set to rise at a 5.83% CAGR between 2025-2030.

- By distribution channel, supermarkets and hypermarkets captured 55.21% of the Middle East and Africa ice-cream market size in 2024, whereas online retail is registering the fastest growth at a 7.04% CAGR.

- By geography, Saudi Arabia accounted for 20.64% of the Middle East and Africa ice-cream market share in 2024, while Nigeria is advancing at a 5.88% CAGR to 2030.

Middle East And Africa Ice Cream Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact On CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Technological advancements in cold-chain logistics | +0.8% | United Arab Emirates, Saudi Arabia, Egypt | Medium term (2-4 years) |

| Growing emphasis on sustainability and ethical sourcing | +0.5% | GCC and North Africa | Long term (≥4 years) |

| Premiumization and artisanal growth | +0.7% | Urban Saudi Arabia, United Arab Emirates, Egypt, South Africa | Short term (≤2 years) |

| Flavor innovation and localization | +0.4% | Saudi Arabia, United Arab Emirates | Medium term (2-4 years) |

| Marketing and influencer engagement | +0.3% | GCC, urban Egypt, Nigeria | Short term (≤2 years) |

| Blockchain-based cold-chain transparency | +0.2% | United Arab Emirates, Saudi Arabia | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Technological advancements in cold-chain logistics

Technological advancements in cold-chain logistics are a key driver of growth in the Middle East and Africa ice cream sector. These innovations expand market reach, minimize spoilage, enhance product variety, and strengthen customer confidence in product quality. RSA Cold Chain's Advanced Regional Distribution Centre in Dubai's Jebel Ali Free Zone serves as a notable example. With temperature control capabilities as low as -25°C, this facility is transforming ice cream distribution economics across the region. Its partnership with Americold incorporates global best practices, addressing the critical issue of insufficient cold storage, which often results in food waste and limits frozen dessert availability. Additionally, companies like Koolboks are leading the way with solar-powered refrigeration solutions. These advancements are making cold storage affordable for small retailers who previously could not invest in conventional systems. Consequently, ice cream brands are now able to access rural markets that were previously unreachable, while also reducing operational costs through the integration of renewable energy.

Premiumization and artisanal growth

The artisanal ice cream segment is expected to grow at a 6.36% CAGR through 2030, reflecting urban consumers' willingness to pay for premium craft experiences. This trend is driven by higher disposable incomes that support experimental flavors and premium offerings. Research on incorporating Adansonia digitata pulp flour into ice cream showcases regional advancements in functional ingredients. Institutions in Saudi Arabia and Egypt are developing antioxidant-rich formulations that successfully command premium pricing. Kuwait Danish Dairy Company has introduced a no-added-sugar ice cream, clinically proven to improve post-meal glucose responses in type 2 diabetes patients. In 2024, the International Diabetes Federation reported a 17.6% diabetes prevalence in the Middle East and North Africa[1]International Diabetes Federation, "IDF Diabetes Atlas - Eleventh Edition (2025)", idf.org. This highlights how health-focused premiumization aligns consumer wellness with business profitability. The artisanal trend also emphasizes traditional production methods. For example, tiger nut milk ice cream provides a cost-effective alternative to conventional dairy bases, offering superior nutritional profiles and signaling premiumization opportunities in the plant-based segment.

Flavor innovation and localization

Flavor innovation and localization are key drivers of the Middle East and Africa ice cream market, addressing changing consumer preferences and regional tastes while enhancing product differentiation. Thurath Al-Madina's introduction of Milaf Cola, the world's first soft drink made entirely from dates, highlights broader localization trends that ice cream manufacturers can utilize for regional flavor differentiation. For instance, in March 2023, Simply Ice Cream launched seven new flavors specifically designed for the Middle Eastern market. These flavors include Date with Caramelised Walnut, Cinnamon, Honey and Figs, Mango and Cardamon, Pistachio, Turkish Delight and Rose, and Pomegranate and Mint Sorbet. This innovation supports Saudi Arabia's Vision 2030 economic diversification goals and reflects consumer interest in incorporating indigenous ingredients into frozen desserts. Positioned as a healthier alternative to sugary beverages, the product contains no added sugar and is rich in natural nutrients, offering a model for ice cream flavor development that addresses health concerns while celebrating regional culinary traditions. Additionally, Halal certification requirements across GCC markets add complexity to flavor innovation, as ingredients must adhere to Islamic dietary laws while satisfying diverse cultural taste preferences.

Marketing and influencer engagement

In the Arab Gulf, female social media influencers are reshaping the engagement strategies of ice cream brands targeting Generation Z. By weaving together emotional narratives with tangible product features, these influencers are fostering trust and influencing purchasing choices. Central to this marketing evolution are the principles of authenticity and interactivity. Influencers are tapping into their personal stories, striking a chord with audiences from diverse cultural backgrounds. This method proves especially potent in regions where conventional advertising struggles to gain traction or trust. Major ice cream brands are now collaborating with these influencers, not just to unveil limited-edition flavors but also to spearhead digital campaigns and boost brand presence during pivotal moments like Ramadan and Eid. In Africa, the surging internet usage is bolstering the role of social media influencers, propelling not just the ice cream sector but a myriad of consumer markets. As of 2024, 38% of individuals were using the internet in Africa, according to the International Telecommunication Union[2]International Telecommunication Union, "Facts and Figures 2024", itu.int. The fusion of social media marketing with e-commerce is allowing brands to seamlessly transition from engagement to sales. This is particularly significant given that online retail is the industry's fastest-growing distribution channel, boasting a 7.04% CAGR.

Restraints Impact Analysis*

| Restraint | (~) % Impact On CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sugar-tax expansion across GCC | −0.6% | Saudi Arabia, United Arab Emirates, Bahrain, Oman, Kuwait, Qatar | Medium term (2-4 years) |

| Seasonality and climate variability | −0.4% | North Africa, Gulf, Sub-Saharan Africa | Short term (≤2 years) |

| Health concerns on sugar and additives | −0.3% | Urban GCC, Egypt, South Africa | Medium term (2-4 years) |

| Volatile power supply raising refrigeration OPEX | −0.5% | Nigeria, Egypt, rural Sub-Saharan Africa | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Sugar-tax expansion across GCC

To combat rising obesity rates and the growing prevalence of noncommunicable diseases, GCC governments have implemented expanded taxation on sugar-sweetened beverages (SSBs) as part of their broader public health strategies. According to the General Authority for Statistics (Saudi Arabia), the share of Saudi Arabian obese men and women was 22.8% and 23.5% respectively, in 2024[3]General Authority for Statistics (Saudi Arabia), "Health Determinants Statistics", stats.gov.sa. The taxation has resulted in significant declines in SSB sales, with Saudi Arabia reporting a drop from 5.4% to 1.3% and the UAE seeing a reduction from 7.4% to 5.9%. Although these measures primarily target beverages, their effects have also influenced the frozen dessert market. Manufacturers have responded by reformulating products and launching no-added-sugar ice cream variants to meet shifting consumer preferences and regulatory demands. Compliance factors, such as ingredient transparency and front-of-pack labeling, now play a critical role in product innovation cycles. However, concerns remain that further tax expansions could negatively impact volume growth, especially in price-sensitive market segments. To address this challenge, brands must actively diversify their product portfolios by introducing low-sugar and functional offerings, ensuring they adapt to changing consumer needs while maintaining market competitiveness.

Seasonality and climate variability

The Arab world experiences extreme heat and water scarcity at nearly double the global average, intensifying the seasonality of ice cream demand and complicating cold chain logistics. This volatility disproportionately affects low-income consumers and small retailers, who often lack the resources to invest in adaptive technologies. Brands operating in these markets must implement localized inventory and distribution strategies. By utilizing predictive analytics, they can align production with seasonal demand spikes and minimize waste during off-peak periods. Manufacturers face challenges in optimizing inventory: overproduction leads to waste during the low season, while underproduction results in missed sales during peak demand. Storage and distribution logistics must adapt to these seasonal fluctuations, increasing operational costs and complexities. Demand variations also create inefficiencies in cold chain logistics and supplier coordination, further complicating cost management.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Take-Home Continues to Anchor, Artisanal Accelerates

In 2024, take-home formats captured a significant 52.84% share of the ice-cream market in the Middle East and Africa. This segment's success was primarily driven by the value offered through multipacks, its suitability for family-oriented occasions, and its broad shelf availability, which ensures accessibility to a wide range of consumers. Retailers prefer take-home formats due to their extended shelf life, which helps minimize product shrinkage and reduces inventory losses. On the other hand, artisanal operators experienced a robust 6.36% CAGR, expanding their presence through innovative strategies such as pop-up counters and cloud kitchens. These approaches allow them to cater to premium urban consumers who prioritize quality and exclusivity. Consumers increasingly associate small-batch production and the use of local ingredients with health benefits and authenticity, which has led to a greater willingness to pay for artisanal offerings. While impulse formats remain a staple at transit hubs due to their convenience, their growth rate continues to trail behind the rapidly expanding gourmet segment.

Further analysis reveals that halal and clean-label regulations are driving reformulation efforts across both mass-market and artisanal segments. Artisanal brands are differentiating themselves by incorporating unique elements such as local fruits, date molasses, and additive-free bases, which not only appeal to health-conscious consumers but also help secure premium shelf space at gourmet grocery stores. In contrast, mass-market brands are focusing on strategies like optimizing bundle pricing and forming partnerships with quick-commerce platforms to strengthen their foothold in the Middle East and Africa's ice-cream market. These efforts enable mass brands to remain competitive while addressing evolving consumer preferences and market dynamics.

By Flavor: Chocolate Dominates but Fruit Flavors Gain Momentum

In 2024, chocolate flavors accounted for a significant 35.57% market share, primarily driven by their widespread global appeal and the extensive scale of suppliers. This dominance reflects the universal familiarity and preference for chocolate among consumers worldwide. The taste profile of chocolate aligns well with regional desserts and sweet indulgences, making it a natural favored choice among consumers. On the other hand, fruit flavors are experiencing notable growth, with a compound annual growth rate (CAGR) of 5.83%. Brands are increasingly incorporating regional ingredients such as baobab, citrus, and date puree into their products, catering to evolving consumer preferences. Health-conscious shoppers are particularly attracted to fruit-based flavors due to their perceived natural qualities and inherent antioxidant properties, which align with the growing demand for healthier options. Vanilla and nut-based profiles continue to hold their ground, thanks to their adaptability across various applications, while experimental blends featuring local spices are gaining traction among Gen Z consumers who seek unique and adventurous flavor experiences.

Localization efforts are playing a crucial role in ensuring compliance with halal standards and avoiding the use of controversial additives, which is particularly important in certain regions. Companies that launch limited-time seasonal fruit flavor campaigns are leveraging the power of social media to amplify their reach. This increased online engagement is directly translating into higher e-commerce sales, emphasizing the strong connection between innovative flavor offerings and the rapid growth of digital sales channels. This trend is especially evident in the ice cream markets of the Middle East and Africa, where flavor innovation and digital platforms are driving significant market expansion.

By Form: Cups and Tubs Lead; Bars and Sticks Rising Fast

In 2024, cups and tubs emerged as the leading segment in the Middle East and Africa's ice-cream market, capturing a significant 46.28% share. Their versatility in portion sizes makes them suitable for both take-home consumption and on-the-go snacking, appealing to a wide range of consumer preferences. Additionally, their strong presence in supermarkets has been instrumental in maintaining consistent volume sales. On the other hand, bars and sticks are projected to achieve a robust 6.23% CAGR during the forecast period. This growth is attributed to their convenience, the hygiene benefits of single-serve formats, and their compatibility with quick-commerce delivery models, which are gaining traction in the region. Cones, while occupying a niche position as a premium treat in foodservice settings, continue to contribute significantly to brand differentiation by offering a unique and indulgent experience.

Sustainability is increasingly influencing packaging decisions across all product formats. To comply with single-use plastic bans, companies are actively testing biodegradable cups and cellulose-based wraps as eco-friendly alternatives. This shift toward sustainable packaging aligns with the preferences of environmentally conscious consumers, who are also driving the premiumization trend within the Middle East and Africa's ice-cream market. By addressing these evolving consumer demands, companies are positioning themselves to remain competitive in a market that values both quality and environmental responsibility.

By Distribution Channel: Supermarkets Dominate; Online Retail Takes Off

In 2024, supermarkets and hypermarkets held a dominant 55.21% market share, driven by their ability to foster strong shopper trust and maintain efficient cold-chain systems. These large-scale retailers also offer private-label product lines, which have intensified price competition within the market. On the other hand, online retail is experiencing significant growth, with a compound annual growth rate (CAGR) of 7.04% (2025-2030). This growth is fueled by the increasing penetration of smartphones, the widespread adoption of digital payment systems, and the popularity of instant delivery models. Specialist stores focus on offering curated premium product lines, encouraging consumers to make impulse upgrades to higher-value items. Meanwhile, convenience stores continue to attract transit shoppers by catering to their immediate needs.

Regulatory mandates for digital traceability, which are set to take effect in 2025, will require all retail channels to implement batch-level monitoring systems. This development is expected to standardize compliance costs across the board. Early adopters in the e-commerce segment have already begun advertising real-time temperature tracking capabilities, a feature that is gaining significant traction among urban millennials in the Middle East and Africa's ice-cream market. This innovation is likely to influence consumer preferences and drive further growth in the sector.

Geography Analysis

Saudi Arabia held 20.64% of regional revenue in 2024, sustained by Vision 2030 investments. These initiatives focus on expanding cold storage infrastructure, encouraging domestic dairy production, and implementing phased bans on single-use plastics to promote sustainability. The Saudi Food and Drug Authority has played a pivotal role by enforcing strict labeling regulations, compelling brands to adopt recyclable packaging and provide clear allergen disclosures. Premium product lines have experienced significant growth in Riyadh and Jeddah, where per-capita spending on ice cream exceeds the regional average, reflecting the rising demand for high-quality offerings in these cities.

Nigeria, experiencing rapid urbanization and leveraging solar-powered refrigeration technology, has achieved the region's fastest compound annual growth rate (CAGR) of 5.88%. This technological advancement has made ice cream accessible even in remote, off-grid towns. In January 2024, the Value4Dairy Consortium, led by FrieslandCampina, secured a USD 5 million grant from the Bill and Melinda Gates Foundation to support the development of Nigeria's dairy sector. This project aims to enhance dairy productivity, improve sustainability, and stabilize the supply of key ingredients. The strongest growth is observed in urban centers such as Lagos, Kano, and Port Harcourt, where quick-commerce delivery services cater to peak afternoon demand by providing timely access to impulse ice cream bars.

The UAE has positioned itself as a hub for innovation in the ice cream market. Federal regulations prioritize product traceability and uphold halal integrity, while the adoption of digitalized certification processes has significantly reduced export lead times. The country's high tourist influx and diverse, cosmopolitan consumer base have created an ideal environment for testing craft and plant-based ice cream formats. Meanwhile, Egypt capitalizes on its irrigated agricultural resources to produce fruits used in localized flavors, although currency volatility poses challenges to the import of dairy inputs. South Africa's well-established retail network supports intense competition among private-label brands, while Morocco and Turkey play a critical role in supplying citrus and nut ingredients that drive intra-regional trade. Collectively, these factors highlight how governance quality, energy stability, and robust infrastructure are key determinants of a country's ability to capture value in the Middle East and Africa ice cream market.

Competitive Landscape

The ice-cream market in the Middle East and Africa exhibits moderate fragmentation. Global leaders such as Unilever PLC, Nestlé SA, and Mars Inc. maintain a strong presence across multiple countries, while regional players like Almarai, IFFCO Group, and Saudia Dairy and Foodstuff Co. capitalize on their ability to source locally and leverage halal branding to secure their market positions. Unilever's recent decision to separate its global ice-cream division into an independent company, valued at USD 8 billion, introduces a layer of strategic uncertainty. This move could potentially lead to portfolio restructuring and the establishment of licensing agreements, reshaping the competitive dynamics within the market.

The market continues to witness significant interest in mergers and acquisitions. Investor groups are actively exploring opportunities in mixed-format joint ventures, reflecting their confidence in the ongoing shift toward premium products. Local companies are attracting substantial capital by emphasizing innovative offerings such as plant-based product lines and blockchain-verified supply chains, which enhance transparency and traceability. Emerging startup brands that excel in influencer-driven marketing are rapidly scaling their operations, effectively targeting niche consumer segments before larger multinational competitors can replicate their unique flavors. The key players are primarily focused on introducing new products to meet evolving consumer preferences. They are prioritizing product development and innovation to deliver diverse flavors and maintain high product quality, aligning with the trend of premiumization. Additionally, mergers and acquisitions remain a core strategy for these companies to strengthen their market positions and expand their portfolios.

Technological advancements are emerging as a critical differentiator in the market. Blockchain technology is being piloted to enhance product recall capabilities and streamline customs clearance processes for export markets, thereby improving operational efficiency. Artificial intelligence (AI)-driven demand forecasting is helping companies minimize waste and optimize production schedules, ensuring better resource utilization. Furthermore, sustainability commitments are increasingly influencing retailer shelf space allocation, creating pressure on companies that fail to meet these expectations. Collectively, these technological and sustainability-driven forces are shaping a highly competitive environment. Success in the Middle East and Africa ice-cream market will depend on a company's ability to remain agile in areas such as product formulation, regulatory compliance, and distribution strategies.

Middle East And Africa Ice Cream Industry Leaders

-

General Mills, Inc.

-

IFFCO Group

-

Nestlé S.A.

-

Unilever PLC

-

Saudia Dairy and Foodstuff Co.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Saudia Dairy and Foodstuff Company (SADAFCO) opened its Saudia Ice Cream Factory at Kidzania, situated in Jeddah's Arab Mall, Saudi Arabia, as part of its efforts to expand its regional presence.

- February 2025: Dairyland, a prominent Kenyan dairy and chocolate brand, has launched a revamped design for its ice cream tubs, combining innovation with style.

- January 2025: Unilever introduced a wide range of innovative ice cream products, highlighting its focus on meeting evolving consumer preferences. Talenti's signature transparent packaging showcases the premium, multi-layered ingredients in each new offering.

- January 2025: Dairy Queen has announced a strategic expansion plan focusing on the UAE and Saudi Arabia to leverage the increasing demand for premium ice cream experiences in the Gulf.

Middle East And Africa Ice Cream Market Report Scope

| Impulse Ice Cream |

| Take-Home Ice Cream |

| Artisanal Ice Cream |

| Chocolate |

| Fruit |

| Cups and Tubs |

| Bars and Sticks |

| Cones |

| On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Specialist Stores | |

| Online Retail Stores | |

| Other Distribution Channels |

| United Arab Emirates |

| South Africa |

| Saudi Arabia |

| Nigeria |

| Egypt |

| Morocco |

| Turkey |

| Rest of Middle East and Africa |

| By Product Type | Impulse Ice Cream | |

| Take-Home Ice Cream | ||

| Artisanal Ice Cream | ||

| By Flavor | Chocolate | |

| Fruit | ||

| By Form | Cups and Tubs | |

| Bars and Sticks | ||

| Cones | ||

| By Distribution Channels | On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Specialist Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geograohy | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the Middle East and Africa ice-cream market?

It was valued at USD 7.12 billion in 2025 and is expected to reach USD 8.42 billion by 2030.

Which country contributes the most revenue to regional ice-cream sales?

Saudi Arabia leads with 20.64% share of regional revenue in 2024.

Which product type is growing fastest?

Artisanal ice cream is expanding at a 6.36% CAGR through 2030.

How fast is online retail expanding in regional ice-cream distribution?

Online channels are registering a 7.04% CAGR, outpacing all other distribution formats.

Page last updated on: